Vascular Snare Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

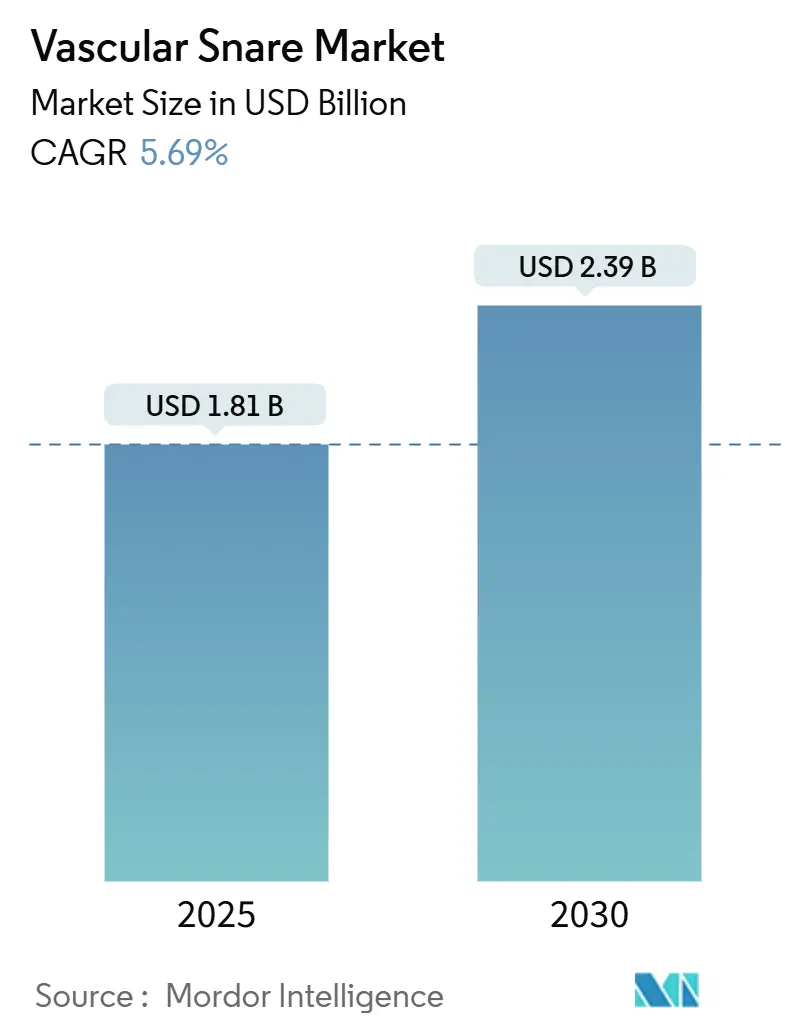

| Market Size (2025) | USD 1.81 Billion |

| Market Size (2030) | USD 2.39 Billion |

| Growth Rate (2025 - 2030) | 5.69% CAGR |

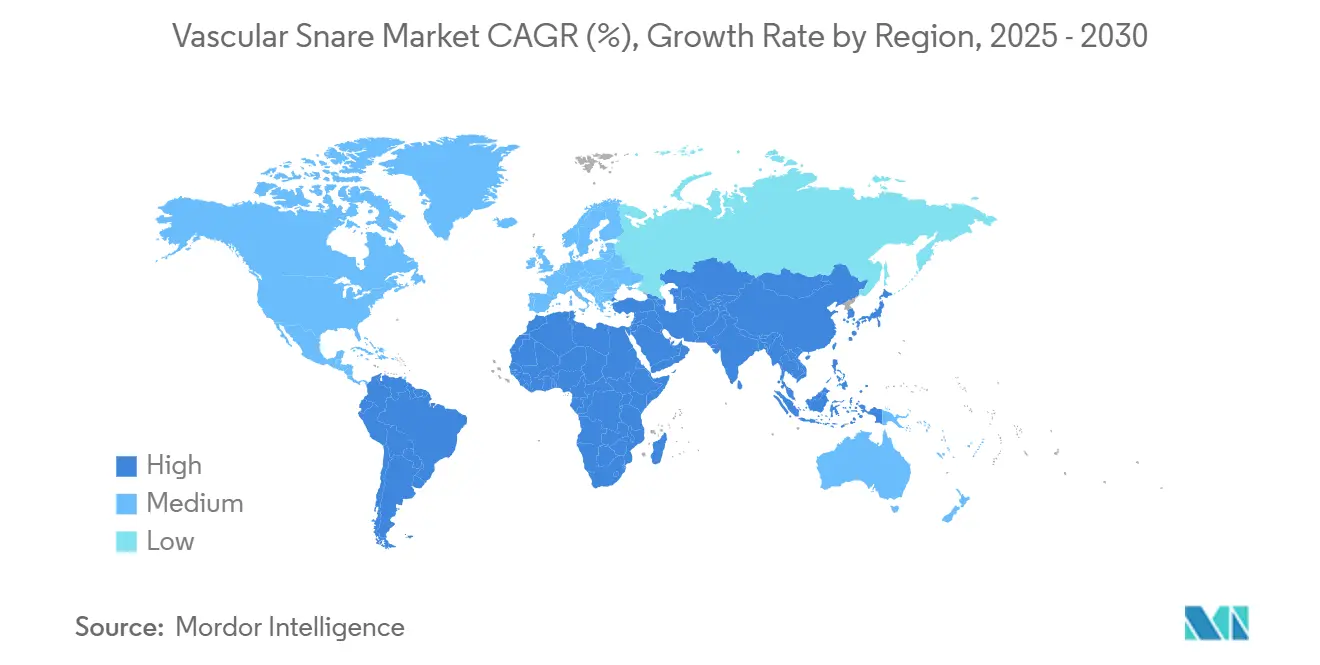

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vascular Snare Market Analysis by Mordor Intelligence

The vascular snare market size stood at USD 1.81 billion in 2025 and is forecast to reach USD 2.39 billion in 2030, advancing at a 5.69% CAGR over the period. Demand rises in tandem with the post-pandemic spike in cardiovascular disease, the growing complexity of endovascular procedures, and the rapid shift toward minimally invasive care models. Hospitals and ambulatory surgery centers now manage heavier case loads as deferred diagnoses surface, pushing retrieval volumes higher in both emergency and elective settings. Single-loop devices keep procedural workflows simple, yet multi-loop innovations win share in anatomically challenging cases. Meanwhile, nitinol’s shape-memory advantages and expanding robotic applications sustain premium pricing despite raw-material volatility. Market leaders differentiate through steerability, radiopacity, and platform compatibility, while smaller firms target niche uses in structural heart and robotic-assisted interventions.

Key Report Takeaways

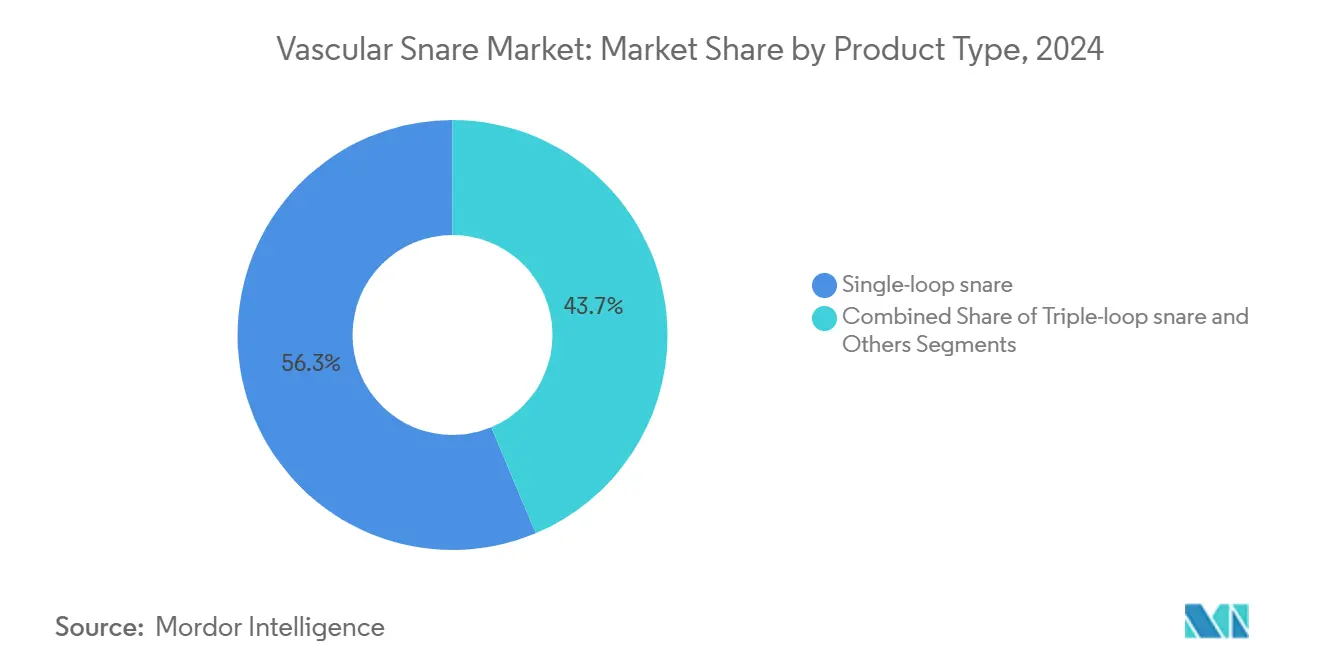

- By product type, single-loop devices held 56.32% of the vascular snare market share in 2024; triple-loop configurations are projected to expand at a 9.37% CAGR to 2030.

- By diameter, the 7–15 mm category accounted for 44.62% of the vascular snare market size in 2024 and will grow steadily, while >30 mm snares post the fastest 7.68% CAGR through 2030.

- By application, device retrieval commanded 51.47% of the vascular snare market size in 2024; EVAR and TAVR assistance is advancing at a 9.67% CAGR to 2030.

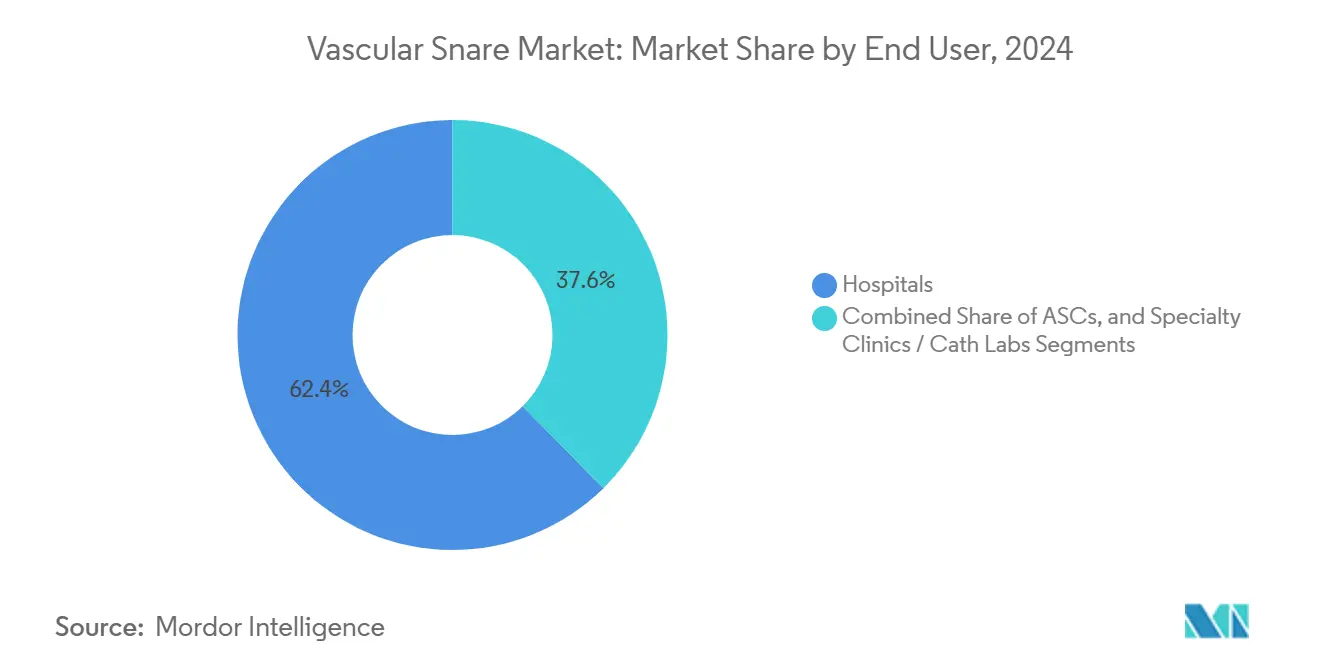

- By end user, hospitals controlled 62.38% of the vascular snare market size in 2024, while ambulatory surgery centers record the highest 8.33% CAGR through 2030.

- By material, nitinol captured 68.43% of the vascular snare market size in 2024 and is expected to surge at an 8.94% CAGR to 2030.

- North America led with 36.73% vascular snare market share in 2024; Asia-Pacific is poised to accelerate at a 7.56% CAGR during 2025–2030.

Global Vascular Snare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic surge in cardiovascular and peripheral vascular disease | +0.9% | Global; highest in North America and Europe | Medium term (2–4 years) |

| Shift toward minimally invasive endovascular interventions | +0.7% | Global; led by developed markets | Long term (≥ 4 years) |

| Advances in steerability and radiopacity of snare loops | +0.5% | North America and Europe | Medium term (2–4 years) |

| Integration with robotic-assisted catheter systems | +0.3% | North America; extending to Asia-Pacific | Long term (≥ 4 years) |

| Growing use in complex structural heart procedures | +0.6% | Global; concentrated in developed markets | Medium term (2–4 years) |

| Expansion of ambulatory surgery centers in emerging economies | +0.5% | Asia-Pacific, Latin America, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Cardiovascular & Peripheral Vascular Diseases Surge Post-Pandemic

The American Heart Association logged a 4.1% rise in cardiovascular deaths in 2024 over pre-pandemic baselines, while peripheral artery disease prevalence climbed 12% among adults over 65.[1]American Heart Association, “2024 Heart Disease and Stroke Statistics Update,” Circulation, ahajournals.orgThese statistics lift baseline demand for snares as backlogged patients present with more advanced disease, driving retrieval volumes for both emergency and elective procedures. Balloon angioplasty alone proves insufficient in many delayed cases, necessitating snare-assisted techniques to resolve complications. Older, multi-morbid patients further magnify needs because they experience a higher incidence of device migrations. Health-system planners expect the elevated demand plateau to extend through 2027 as deferred care is steadily addressed.

Shift Toward Minimally Invasive Endovascular Interventions

Transcatheter procedures represented 78% of all aortic valve replacements in 2024, up from 65% a year earlier. Device complexity has climbed in parallel, and rare embolizations—about 0.3% of cases—require immediate snare retrieval to avert catastrophic outcomes.[2]María-Cruz Ferrer-Gracia, María Eugenia Guillén Subirán, and José Antonio Diarte de Miguel, “Severe Aortic Stenosis Treated With Three Self-Expandable Valves: Embolization of the First Two and Successful Implantation of a Larger One,” Complications, mdpi.comAmbulatory surgery centers now handle an increasing share of complex procedures once confined to hospitals, widening the installed base for portable, intuitive snares. Economic benefits such as shorter stays and quicker recoveries sustain the procedural shift despite higher device costs, embedding retrieval tools as routine inventory.

Technological Improvements in Steerability & Radiopacity of Snare Loops

Next-generation nitinol alloys deliver 40% better shape memory than earlier formulations, easing navigation in tortuous anatomy.[3]Alleima Medical Materials Group, “Nitinol Innovation in Medical Devices,” alleima.comFull-circumference radiopaque markers enhance visualization, trimming procedure time by 15–20% in clinical studies. Hybrid devices combining multiple loop configurations inside one shaft allow operators to adapt swiftly without gear exchanges, and improved wire-drawing processes have lowered snare fracture rates once seen in 2–3% of demanding retrievals. These innovations resonate strongly in robotic suites where tactile feedback is limited, making visual guidance paramount.

Integration of Vascular Snares in Robotic-Assisted Catheter Systems

Early adopters of endovascular robotics report 25% higher procedural success in complex cases. Robotic workflows require snares with advanced steerability and force-feedback translation, prompting manufacturers to design platform-specific models that command premium pricing. Next-generation systems are expected to offer semi-automated capture protocols, reducing operator burden and standardizing outcomes. Although centers need 50–75 cases to master robotic methods, evidence shows retrieval tasks benefit substantially from enhanced control and visualization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition cost and budget constraints in small hospitals | −0.5% | Global; strongest in emerging markets | Short term (≤ 2 years) |

| Stringent regulatory and clinical evidence requirements | −0.3% | North America and Europe | Medium term (2–4 years) |

| Risk of vessel injury and embolization in challenging anatomies | −0.3% | Global; higher in complex cases | Medium term (2–4 years) |

| Price volatility and supply-chain risk of nitinol and cobalt-chromium alloys | −0.2% | Manufacturing hubs worldwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost & Budget Constraints in Small Hospitals

Specialized snares sell for USD 800–1,500 per unit, straining budgets at facilities performing fewer than 50 endovascular procedures each month. Rural providers often lack volume-based contracts and must transfer complicated retrieval cases to larger centers, prolonging treatment and increasing costs. Refurbishment and leasing offer partial relief, but regulatory limits on reprocessed single-use items restrict widespread adoption.

Stringent Regulatory & Clinical Evidence Requirements Delaying Product Launches

The 2024 FDA Quality System Regulation amendments added three to four months to average review times. Authorities now request head-to-head trials showing comparative effectiveness, pushing smaller innovators to the sidelines. Europe’s MDR regime imposes similar hurdles, encouraging firms to stagger launches until clearer precedents form, especially for devices with novel radiopaque markers or hybrid loop configurations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-Loop Dominates Despite Triple-Loop Innovation

Single-loop devices controlled 56.32% of the vascular snare market in 2024, benefiting from operator familiarity and effectiveness in routine retrievals. Triple-loop models, though smaller in volume, post a 9.37% CAGR as operators confront complex anatomies where multi-loop capture reaches 92% success when single-loop attempts fail. Hybrid snares that combine both formats on one shaft blur traditional category lines, enabling operators to adapt mid-procedure without exchanging equipment.

The rising share of triple-loop snares mirrors the structural-heart boom, especially valve-in-valve TAVR and cerebral protection cases that demand high capture reliability. Premium pricing is justified by reduced procedure time and lower complication rates. As robotic workflows scale, manufacturers integrate interface modules allowing seamless switching between single- and triple-loop modes, preserving the vascular snare market’s established procedural routines while elevating capability.

By Diameter/Loop Size: Mid-Range Dominance With Large-Bore Growth

Mid-range 7–15 mm snares formed 44.62% of the vascular snare market size in 2024, covering most coronary and peripheral retrievals. Large-bore devices >30 mm grow fastest at 7.68% CAGR as EVAR and TAVR case volumes expand. Pediatric and coronary specialists still rely on 2–6 mm snares for small-diameter vessels, while 16–30 mm fills an intermediate niche.

Oversized snares excel in aortic-root and valve-embolization retrievals where constrained maneuvering space demands both reach and radial strength. Manufacturers now leverage high-strength nitinol to maintain flexibility while increasing loop diameter, an improvement that keeps profile low for introducer compatibility. Clinical data show oversized snares decrease fluoroscopy time by 18% compared with makeshift multi-snare strategies, reinforcing their value proposition.

By Application: Device Retrieval Leads While TAVR Assistance Accelerates

Routine device retrieval claimed 51.47% vascular snare market share in 2024. EVAR and TAVR assistance is the fastest-moving sub-segment, posting 9.67% CAGR, as structural-heart programs extend to lower-risk cohorts. Foreign body extraction keeps steady demand, while IVC filter retrieval remains technically challenging yet clinically necessary.

Cerebral protection systems used alongside TAVR require retrieval in 5% of deployments. Advanced snare-forceps combinations now reach 96% success for embedded IVC filters. These data underscore the need for versatile retrieval arsenals capable of addressing a spectrum of clinical scenarios, ensuring the vascular snare market remains integral across procedural types.

By End User: Hospital Dominance Challenged by ASC Growth

Hospitals represented 62.38% of the vascular snare market size in 2024, supported by bulk purchasing and the breadth of retrieval scenarios encountered. Ambulatory surgery centers expand at 8.33% CAGR, propelled by payer incentives and patient preference for outpatient care. Specialty clinics hold a stable middle ground, serving high-volume focused procedures and maintaining tailored snare inventories.

ASC managers embrace standardized snare kits that address common retrieval needs while minimizing shelf stock. Partnerships with hospitals for complex backup ensure continuity of care but underline inventory limitations. Manufacturers developing cost-efficient, multi-purpose kits position themselves to capture emerging ASC demand without cannibalizing hospital relationships, protecting overall vascular snare market growth.

By Material: Nitinol Supremacy Despite Supply Challenges

Nitinol captured 68.43% of the vascular snare market size in 2024 and is projected to log an 8.94% CAGR. Shape-memory and fatigue resistance allow precise loop deployment with minimal vessel trauma. Stainless-steel alternatives cover cost-sensitive use cases, while cobalt-chromium and other alloys serve niche requirements such as heightened radiopacity.

Supply-chain constraints continue to pose risk, motivating dual-source procurement and investment in alternative alloys or hybrid materials embedding radiopaque markers directly into nitinol. Processing advancements such as vacuum heat treatments mitigate nickel-related biocompatibility concerns, reinforcing nitinol’s standing as the premium option in the vascular snare market.

Geography Analysis

North America retained 36.73% market share in 2024, buoyed by high procedural volumes, favorable reimbursement, and clinician familiarity with advanced retrieval tools. Integrated hospital networks streamline inventory management, allowing rapid adoption of newly cleared devices. Regulatory certainty, despite lengthier reviews, still provides a transparent path that encourages innovation, keeping leading OEMs anchored in the region.

Europe holds steady, aided by harmonized MDR regulations that gradually stabilize market entry processes. Budgetary pressures spur hospitals to evaluate cost-effectiveness, favoring snares that cut fluoroscopy time and reduce complication rates. Regional centers of excellence for structural-heart interventions accelerate demand for large-bore and multi-loop configurations, maintaining momentum for the vascular snare market.

Asia-Pacific posts the highest 7.56% CAGR as governments invest heavily in cath-lab infrastructure and minimally invasive programs. China’s cardiovascular initiative funds provincial hospital upgrades, expanding retrieval volumes in both coronary and peripheral segments. Ambulatory growth in India and Southeast Asia widens the addressable base, especially for mid-range snares and standardized kits. Manufacturers that localize regulatory filings and build distributor partnerships are best placed to capture the region’s outsized growth.

Competitive Landscape

Sector concentration remains moderate. Top companies leverage differentiated steerability and radiopacity to secure contracts with high-volume centers. Teleflex’s 2025 acquisition of BIOTRONIK’s vascular unit for EUR 760 million strengthens its European footprint and broadens its snare portfolio. Abbott maintains leadership in structural-heart aligned retrieval solutions, while Cook Medical advances robotic-compatible models.

Strategic focus shifts toward platform integration as robotic catheter systems gain credence. OEMs co-develop interface standards so that snares plug seamlessly into robotic consoles, creating high switching costs. Start-ups pursue niche angles such as pediatric applications, force-feedback handles, or AI-guided capture algorithms that signal new competitive dynamics.

Innovation pipelines emphasize hybrid loop designs, automated deployment, and materials science breakthroughs. Recent patent trends reveal automated tension-controlled loops that self-center around dislodged objects, promising to shorten procedure time and standardize outcomes. As vendors compete on capability more than price, clinicians gravitate toward devices with proven success in complex anatomies, reinforcing the vascular snare market’s value-driven orientation.

Vascular Snare Industry Leaders

Medtronic plc

Cook Medical

Merit Medical Systems

Teleflex Incorporated

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed acquisition of BIOTRONIK’s Vascular Intervention business for EUR 760 million (USD 825 million), expanding its European presence.

- December 2024: Jingtu Medical Instrument, a Mednovo Group subsidiary, obtained NMPA Class III approval for its SnareMan Intravascular kit.

Global Vascular Snare Market Report Scope

| Single-loop snare |

| Triple-loop snare |

| Others (multi-loop, specialty-configured) |

| 2–6 mm |

| 7–15 mm |

| 16–30 mm |

| >30 mm |

| Device retrieval (catheters, stents, guidewires) |

| Foreign body removal |

| IVC filter retrieval |

| EVAR & TAVR assistance |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics / Cath Labs |

| Nitinol |

| Stainless Steel |

| Other Alloys |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single-loop snare | |

| Triple-loop snare | ||

| Others (multi-loop, specialty-configured) | ||

| By Diameter/Loop Size | 2–6 mm | |

| 7–15 mm | ||

| 16–30 mm | ||

| >30 mm | ||

| By Application | Device retrieval (catheters, stents, guidewires) | |

| Foreign body removal | ||

| IVC filter retrieval | ||

| EVAR & TAVR assistance | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics / Cath Labs | ||

| By Material | Nitinol | |

| Stainless Steel | ||

| Other Alloys | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the vascular snare market today?

The vascular snare market size reached USD 1.81 billion in 2025 and is projected to climb to USD 2.39 billion by 2030.

Which snare configuration sells the most?

Single-loop models lead with 56.32% share, favored for everyday device retrieval in routine endovascular procedures.

What material dominates snare manufacturing?

Nitinol captures 68.43% share because its shape-memory and fatigue resistance enhance maneuverability and safety.

Why are ambulatory surgery centers important for future growth?

ASCs are expanding case volumes by 15–20% each year in emerging regions, driving strong incremental demand for standardized snare kits.

Which region will grow fastest through 2030?

Asia-Pacific is forecast to advance at a 7.56% CAGR, underpinned by cath-lab expansion and rising adoption of minimally invasive techniques.

Page last updated on: