Artificial Blood Vessels Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.45 Billion |

| Market Size (2031) | USD 4.68 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Blood Vessels Market Analysis by Mordor Intelligence

The Artificial Blood Vessels Market size was valued at USD 3.25 billion in 2025 and is estimated to grow from USD 3.45 billion in 2026 to reach USD 4.68 billion by 2031, at a CAGR of 6.25% during the forecast period (2026-2031).

This mid-single-digit trajectory is shaped by three structural forces: rising global cardiovascular and peripheral artery disease incidence, regulatory validation of bioengineered conduits that challenge long-standing polyethylene terephthalate and expanded polytetrafluoroethylene grafts, and defense-funded innovation that is seeding shelf-stable trauma devices for civilian use. Humacyte’s December 2024 FDA clearance of SYMVESS, the first acellular tissue-engineered vessel for extremity trauma, signaled a regulatory inflection point that is accelerating investment in bacterial nanocellulose scaffolds, smart-sensor hybrids, and 3-D-printed patient-specific geometries. Concurrently, the 2024 ACC/AHA peripheral artery disease guideline reaffirmed surgical autogenous vein as the preferred infra-inguinal bypass option, a stance that tempers synthetic graft uptake even as thoracic endovascular aortic repair fuels demand for large-diameter stent-graft systems[1]American College of Cardiology, “2024 Peripheral Artery Disease Guideline,” acc.org.

Key Report Takeaways

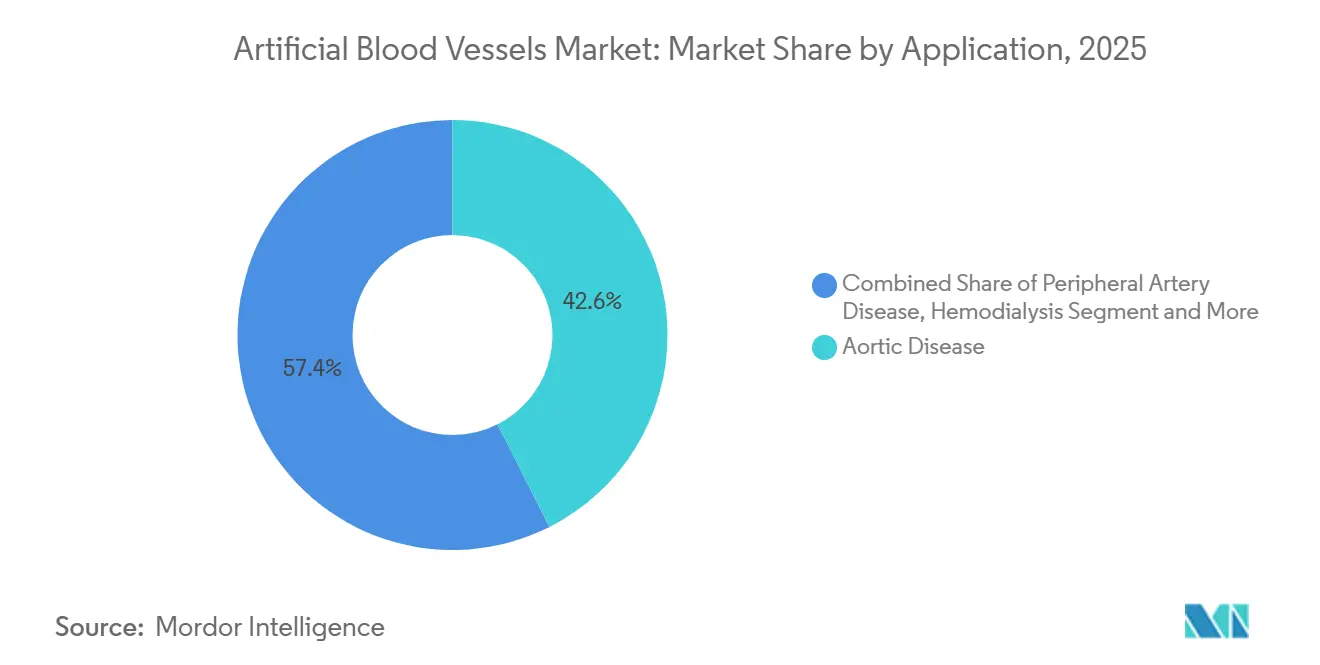

- By application, aortic disease led with 42.56% revenue share in 2025. Traumatic vascular injury is forecast to expand at an 11.25% CAGR to 2031, the fastest among all indications.

- By Polymer Type, Polyethylene terephthalate retained 36.53% of the Artificial Blood Vessels market share in 2025, while bacterial nanocellulose is advancing at a 12.85% CAGR through 2031.

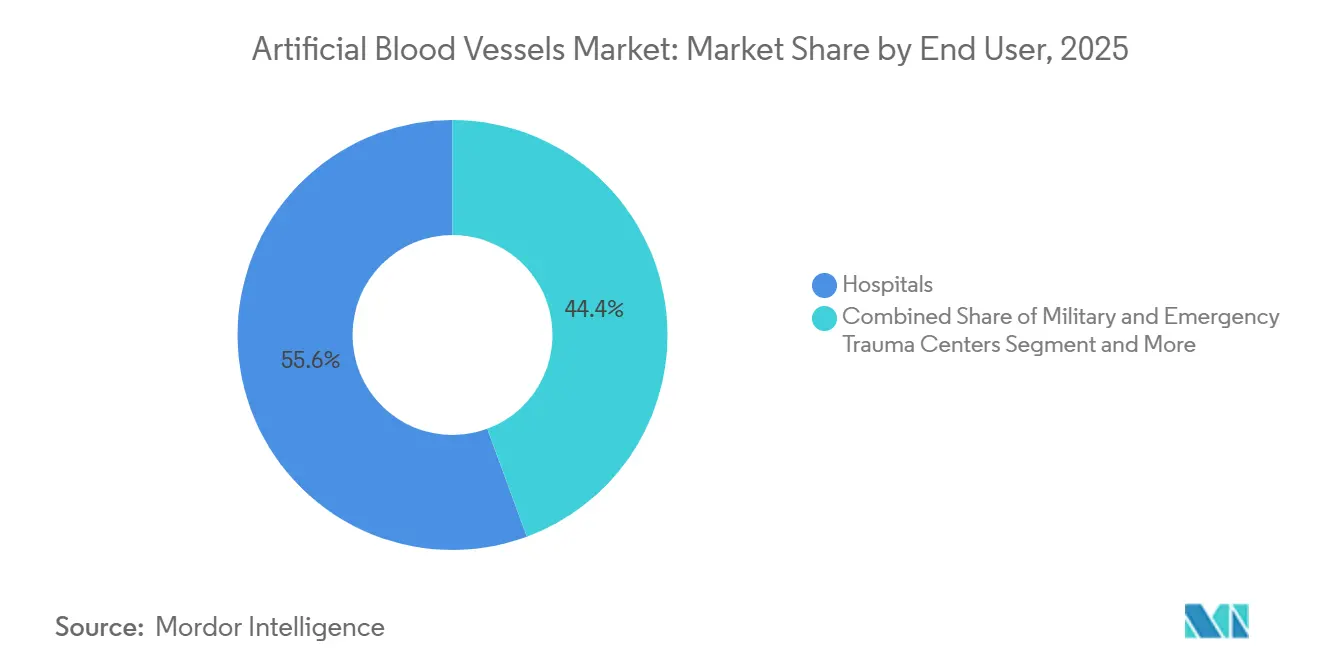

- By End User, Hospitals accounted for a 55.63% slice of the Artificial Blood Vessels market size in 2025; military and emergency trauma centers are growing at a 10.87% CAGR.

- By Device Type, Smart sensor-enabled grafts posted the fastest device-level growth at 13.7% CAGR between 2026 and 2031.

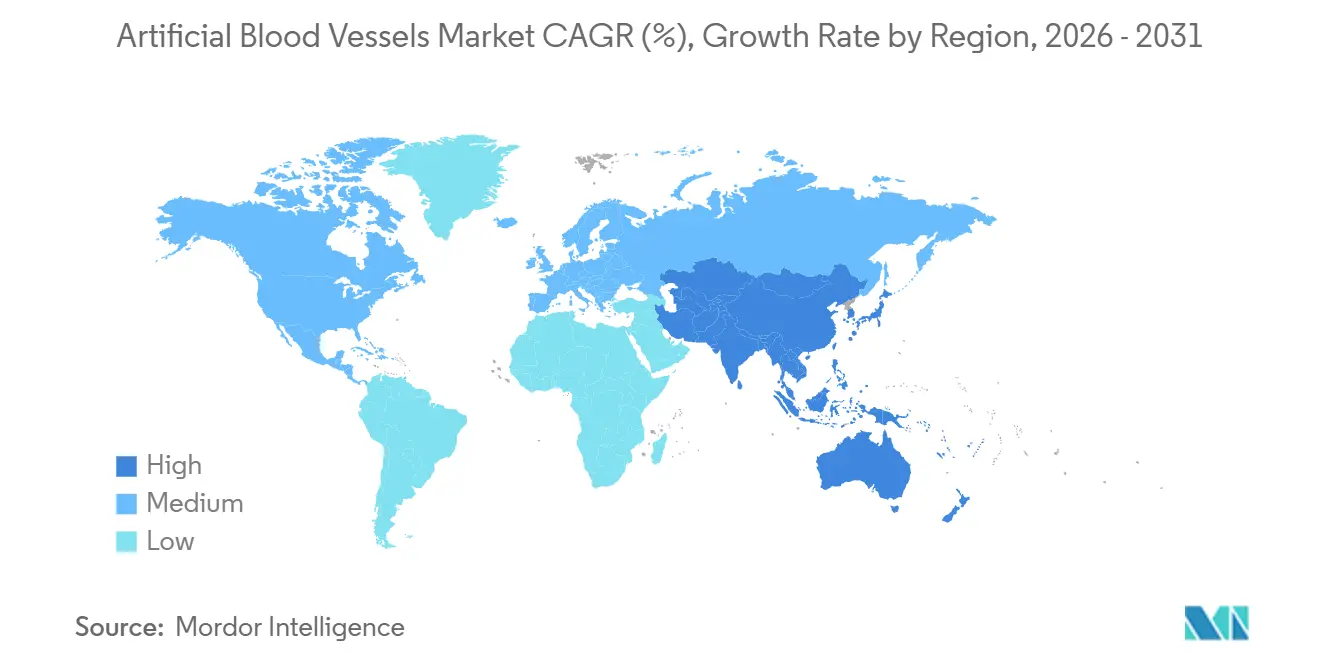

- By geography, North America commanded 42.13% sales in 2025, while Asia-Pacific is projected to deliver a 10.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Artificial Blood Vessels Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular & peripheral artery diseases | +1.8% | Global; acute in Asia-Pacific and aging North America & Europe | Long term (≥ 4 years) |

| Growing adoption of minimally-invasive endovascular procedures | +1.3% | North America & Europe lead; Asia-Pacific accelerating | Medium term (2-4 years) |

| Advances in biomaterials & tissue-engineered graft platforms | +1.5% | North America & EU for approvals; China for scale-up | Medium term (2-4 years) |

| Expansion of the global hemodialysis population | +1.2% | North America, Europe, Japan; emerging China & India | Long term (≥ 4 years) |

| 3-D printing and digital-twin personalization | +0.9% | North America & EU early adoption; Asia-Pacific manufacturing | Medium term (2-4 years) |

| Defense-funded trauma programs | +0.6% | U.S. DoD, NATO partners, Asia-Pacific militaries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular & Peripheral Artery Disease

Peripheral artery disease affected 113 million people worldwide in 2025, including 6.5 million U.S. patients, and prevalence doubles with each decade of life after age 50. The aging demographic profiles of Japan, Germany, and South Korea therefore anchor long-term demand for durable vascular conduits. While supervised exercise therapy now precedes many interventions per the 2024 guideline, patients who progress to revascularization often present with advanced disease that mandates a reliable graft when autogenous vein is unavailable. Consequently, the Artificial Blood Vessels market benefits from a smaller yet higher-acuity treatment pool.

Advances in Biomaterials & Tissue-Engineered Graft Platforms

SYMVESS achieved 67% primary patency at 30 days and became the first tissue-engineered graft cleared in the United States in December 2024. The milestone validated two decades of extracellular-matrix research and is compressing review cycles for follow-on platforms. Bacterial nanocellulose synthesized by Komagataeibacter xylinus replicates collagen’s nanofibrillar structure, surpasses 200 MPa tensile strength, and promotes endothelial adhesion, positioning it as the fastest-growing polymer in the Artificial Blood Vessels market. China’s TEDA Bioprinting recorded 95% cell viability in 10 cm patient-specific grafts in 2024 and begins clinical trials in 2025.

Expansion of the Global Hemodialysis Population

USRDS noted that 80% of U.S. dialysis patients initiate treatment with a catheter, and 38.9% of fistulas fail to mature, sustaining demand for prosthetic arteriovenous grafts. Although KDOQI favors fistula-first strategies, elderly cohorts with calcified vessels rely on predictable polytetrafluoroethylene conduits that mature in 2–4 weeks. Japan’s ≥ 65 population share of 28% amplifies this need, and antimicrobial-coated bioengineered grafts are gaining traction in infection-prone dialysis settings.

3-D Printing & Digital-Twin Personalization of Patient-Specific Grafts

TEDA’s 2024 bioprinting breakthrough allows conduits to match the diameter, curvature, and branch geometry captured on CT angiography, mitigating compliance mismatch and turbulence that accelerate failure in conventional off-the-shelf grafts. DARPA is exploring similar technology for battlefield trauma, reinforcing the near-term defense influence on the Artificial Blood Vessels market. Before wider adoption, multicenter randomized trials must validate computational fluid-dynamic simulations and shelf-life claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure and device costs | -1.1% | Global; acute in India, Indonesia, MENA, South America | Short term (≤ 2 years) |

| Stringent multi-jurisdictional regulatory pathways | -0.8% | FDA, MDR, PMDA, NMPA oversight | Medium term (2-4 years) |

| Drug-eluting stent alternatives | -0.7% | North America & Europe; emerging Asia-Pacific metros | Medium term (2-4 years) |

| PTFE & PET supply-chain disruptions | -0.4% | North America & Europe production hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure and Device Costs

Medicare’s 2025 ambulatory payment range of USD 5,702–17,957 per vascular code does not fully offset total episode-of-care costs, which include premium graft pricing, radiology, anesthesia, and surveillance[2]Centers for Medicare & Medicaid Services, “2025 APC Payments,” cms.gov. BEST-CLI showed 32% fewer major limb events with autogenous vein, reinforcing payer skepticism toward synthetic grafts in infra-inguinal disease. Outside high-income markets, out-of-pocket expenditure above 40% in India and Indonesia narrows the addressable base for bioengineered products.

Stringent Multi-Jurisdictional Regulatory Pathways

Class III vascular devices face 3–5-year FDA premarket reviews, detailed quality-system audits, and manufacturing inspections. Europe’s Medical Device Regulation heightens clinical-evidence requirements, and Japan’s PMDA imposes bridging studies that delay Asia-Pacific launches. These hurdles raise capital needs for emerging players and favor incumbents with legacy dossiers, stretching time to revenue for tissue-engineered platforms in the Artificial Blood Vessels market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Trauma Outpaces Chronic Indications

Traumatic vascular injury drove an 11.25% CAGR outlook from 2026 to 2031, fueled by military procurement and level-1 trauma centers prioritizing shelf-stable grafts that bypass vein harvesting delays. SYMVESS’s 67% primary patency and 9% amputation rate in extremity trauma demonstrate outcome parity with legacy synthetics while cutting operative time. Aortic disease, by contrast, retained 42.56% of the Artificial Blood Vessels market share in 2025 behind the ascendancy of thoracic endovascular repair, which now handles 81% of abdominal aneurysm cases in the United States. Open surgical volumes are falling, yet each hybrid stent-graft incorporates polyethylene terephthalate or polytetrafluoroethylene fabric, sustaining material demand. Peripheral artery disease applications encounter guideline-driven headwinds favoring autogenous vein, whereas dialysis vascular access remains resilient due to fistula maturation failure rates that exceed 38%[3]United States Renal Data System, “2024 Annual Data Report,” usrds.org.

By Polymer Type: Nanocellulose Rises, PET Defends Share

Bacterial nanocellulose is on track for a 12.85% CAGR through 2031, propelled by mechanical compliance mirroring collagen and superior cell adhesion that reduces intimal hyperplasia risk. Polyethylene terephthalate kept a 36.53% foothold in 2025 as woven and knitted PET grafts remain the standard for large-diameter aortic repairs, especially in Europe where surgeons value burst strength and kink resistance. Expanded polytetrafluoroethylene continues to dominate small- and medium-diameter bypasses, augmented by heparin-bonded surfaces like PROPATEN that lengthen patency. Hybrid composite polymers are emerging in complex arch repairs, combining polytetrafluoroethylene luminal surfaces with PET structural meshes to balance compliance and radial strength.

By End User: Defense Medicine as Growth Engine

Military and emergency trauma centers will grow at a 10.87% CAGR as the U.S. DoD, NATO allies, and selected Asia-Pacific militaries adopt acellular grafts for forward surgery and damage-control scenarios. Hospitals still preserved 55.63% of the Artificial Blood Vessels market size in 2025, underwritten by Medicare reimbursement and their central role in aneurysm repair, dialysis access, and complex limb salvage. Ambulatory surgical centers are drawing less complex peripheral bypasses, and cardiac catheterization labs are broadening endovascular services, but trauma and aortic surgery keep the inpatient channel dominant.

By Device Type: Sensors Enable Predictive Monitoring

Smart sensor-enabled grafts will advance at 13.7% CAGR to 2031, integrating microelectromechanical systems that transmit real-time pressure and flow data to clinicians’ dashboards, facilitating pre-symptomatic thrombosis interventions. Synthetic vascular grafts still commanded 46.53% market share in 2025 due to entrenched clinical familiarity. Bioengineered acellular vessels now have an FDA-validated pathway, while drug-eluting grafts with paclitaxel or sirolimus coatings are entering peripheral segments where patency deficits persist.

Geography Analysis

North America retained 42.13% of global revenues in 2025 amid substantial Medicare reimbursement, yet vein-first clinical guidance and the competitively successful BEST-CLI study curb infra-inguinal prosthetic usage. Still, 6.5 million U.S. peripheral artery disease patients and a surge in thoracic endovascular repairs sustain baseline demand. Canadian and Mexican uptake trails, but Humacyte’s SYMVESS approval sets a precedent that is catalyzing U.S. investigational device submissions for follow-on tissue-engineered grafts.

Asia-Pacific is projected to post the fastest 10.51% CAGR, leveraging high cardiovascular disease prevalence in China and India. However, healthcare spending patterns marked by > 40% out-of-pocket outlays in several markets dampen uptake of premium bioengineered products. China’s TEDA Bioprinting is positioning to export patient-specific conduits, while Japan and South Korea apply fast-track approvals for locally manufactured grafts to meet dialysis and peripheral artery disease demand. Australia’s universal insurance and South Korea’s single-payer system support rapid adoption of endovascular techniques and associated grafts.

Europe’s growth lags North America and Asia-Pacific but benefits from a mature vascular surgery infrastructure. The 2025 European Society of Vascular Surgery consensus reported 7.3% in-hospital mortality and 5.0% stroke during arch TEVAR, prompting iterative design upgrades in stent-graft geometry and delivery systems. Germany, France, and the United Kingdom remain volume anchors; Spain and Italy contribute smaller but steady demand. MDR compliance presents cost and time-to-market challenges that favor incumbents, yet CE-first strategies, as executed by PECA Labs with its growth-accommodating exGraft, remain attractive for U.S. start-ups. Latin America and the Middle East & Africa are nascent, with Dubai and Riyadh tertiary centers importing high-end grafts, while Brazil favors cost-effective synthetics in its public system.

Competitive Landscape

The Artificial Blood Vessels market is moderately fragmented: Medtronic, Terumo and others guard polytetrafluoroethylene and polyethylene terephthalate positions through incremental surface and drug-delivery upgrades, while bioengineered entrants Humacyte and Xeltis pursue acellular and resorbable strategies that promise superior compliance and long-term remodeling. Gore’s PROPATEN heparin-bonded graft and VIABAHN stent-graft capitalize on antithrombotic technology to differentiate in peripheral bypass and iliac repair niches. Terumo’s USD 30 million Puerto Rico expansion announced in February 2024 underscores its commitment to vascular access ancillaries that complement graft portfolios. Humacyte’s SYMVESS established a regulatory template that accelerates acellular vessel adoption and pressures incumbents to license or build in-house tissue-engineering capacity.

White-space innovation focuses on smart sensor-enabled grafts that detect early hemodynamic anomalies, with prototypes embedding telemetry chips within graft walls that interface with cloud dashboards. PECA Labs’ exGraft secured CE Mark in March 2024 for pediatric use, addressing the unmet need of growth-accommodating conduits that obviate serial reoperations. Start-ups such as InnAVasc Medical and Vascudyne are targeting dialysis access with antimicrobial coatings and extracellular-matrix scaffolds, respectively. Regulatory hurdles remain high, but the SYMVESS precedent lowers perceived risk for investors and shortens expected approval timelines. Incumbents’ scale, distribution, and surveillance datasets provide competitive ballast, yet a moderate consolidation wave is likely as digital health and biomaterial capabilities converge.

Artificial Blood Vessels Industry Leaders

B. Braun Melsungen

Terumo Medical Corporation

Medtronic

Cook Medical Incorporated

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: University of Sydney researchers 3-D printed glass-based blood vessels that replicate native fluid dynamics, enabling new stroke pathway insights.

- December 2024: FDA approved SYMVESS, the first acellular tissue-engineered vessel for urgent extremity arterial repair when vein graft is infeasible.

Global Artificial Blood Vessels Market Report Scope

As per the scope of the report, artificial blood vessels are tubes made from synthetic (chemically produced) materials to restore blood circulation. These synthetic blood vessels are manufactured by using biosynthetic materials such as polyethylene terephthalate and Polydioxanone owing to high water and chemical resistance, high conductivity and high permeability to oxygen.

The segmentation of the artificial blood vessels market is categorized by application, polymer type, end user, device type, and geography. By application, it includes aortic disease, peripheral artery disease, hemodialysis, coronary artery bypass grafting, traumatic vascular injury, and pediatric congenital vessel repair. By polymer type, it comprises polydioxanone, polyurethane, polyethylene terephthalate, expanded PTFE, biosynthetic/tissue-engineered, bacterial nanocellulose, and hybrid composite polymers. By end user, it is segmented into hospitals, ambulatory surgical centers, cardiac catheterization laboratories, specialty vascular clinics, and military & emergency trauma centers. By device type, it includes synthetic vascular grafts, bioengineered acellular vessels, drug-eluting vascular grafts, and smart sensor-enabled grafts. By geography, the market is segmented into North America, Europe, Asia-Paicific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Aortic Disease |

| Peripheral Artery Disease |

| Hemodialysis |

| Coronary Artery Bypass Grafting |

| Traumatic Vascular Injury |

| Pediatric Congenital Vessel Repair |

| Polydioxanone |

| Polyurethane |

| Polyethylene Terephthalate |

| Expanded PTFE |

| Biosynthetic / Tissue-Engineered |

| Bacterial Nanocellulose |

| Hybrid Composite Polymers |

| Hospitals |

| Ambulatory Surgical Centers |

| Cardiac Catheterization Laboratories |

| Specialty Vascular Clinics |

| Military & Emergency Trauma Centers |

| Synthetic Vascular Grafts |

| Bioengineered Acellular Vessels |

| Drug-Eluting Vascular Grafts |

| Smart Sensor-Enabled Grafts |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Aortic Disease | |

| Peripheral Artery Disease | ||

| Hemodialysis | ||

| Coronary Artery Bypass Grafting | ||

| Traumatic Vascular Injury | ||

| Pediatric Congenital Vessel Repair | ||

| By Polymer Type | Polydioxanone | |

| Polyurethane | ||

| Polyethylene Terephthalate | ||

| Expanded PTFE | ||

| Biosynthetic / Tissue-Engineered | ||

| Bacterial Nanocellulose | ||

| Hybrid Composite Polymers | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Cardiac Catheterization Laboratories | ||

| Specialty Vascular Clinics | ||

| Military & Emergency Trauma Centers | ||

| By Device Type | Synthetic Vascular Grafts | |

| Bioengineered Acellular Vessels | ||

| Drug-Eluting Vascular Grafts | ||

| Smart Sensor-Enabled Grafts | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Artificial Blood Vessels market in 2026?

The market stands at USD 3.45 billion, expanding toward USD 4.68 billion by 2031 at a 6.25% CAGR.

Which application contributes the most revenue?

Aortic disease accounts for 42.55% of global sales in 2025, supported by the dominance of endovascular aortic repair.

What is the fastest-growing application area?

Traumatic vascular injury shows an 11.25% CAGR outlook through 2031, driven by military and civilian trauma adoption.

Which polymer segment is gaining the quickest traction?

Bacterial nanocellulose leads with a projected 12.85% CAGR through 2031 due to superior biocompatibility and compliance.

Why is Asia-Pacific growing faster than other regions?

High cardiovascular disease prevalence, rising procedure volumes in China and India, and emerging local manufacturing propel a 10.51% CAGR despite spending constraints.

How are smart sensor-enabled grafts changing post-operative care?

Embedded microelectromechanical sensors provide real-time flow and pressure data, enabling early thrombosis detection and preventive intervention.

Page last updated on: