Hypodermic Needles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

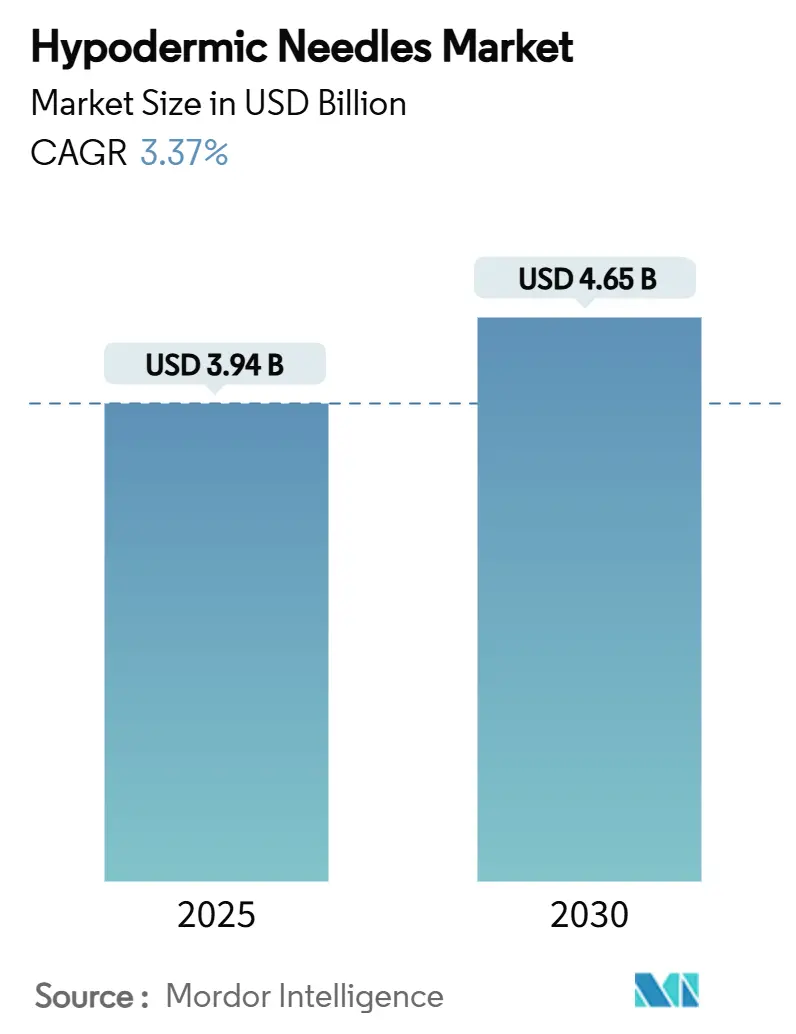

| Market Size (2025) | USD 3.94 Billion |

| Market Size (2030) | USD 4.65 Billion |

| Growth Rate (2025 - 2030) | 3.37% CAGR |

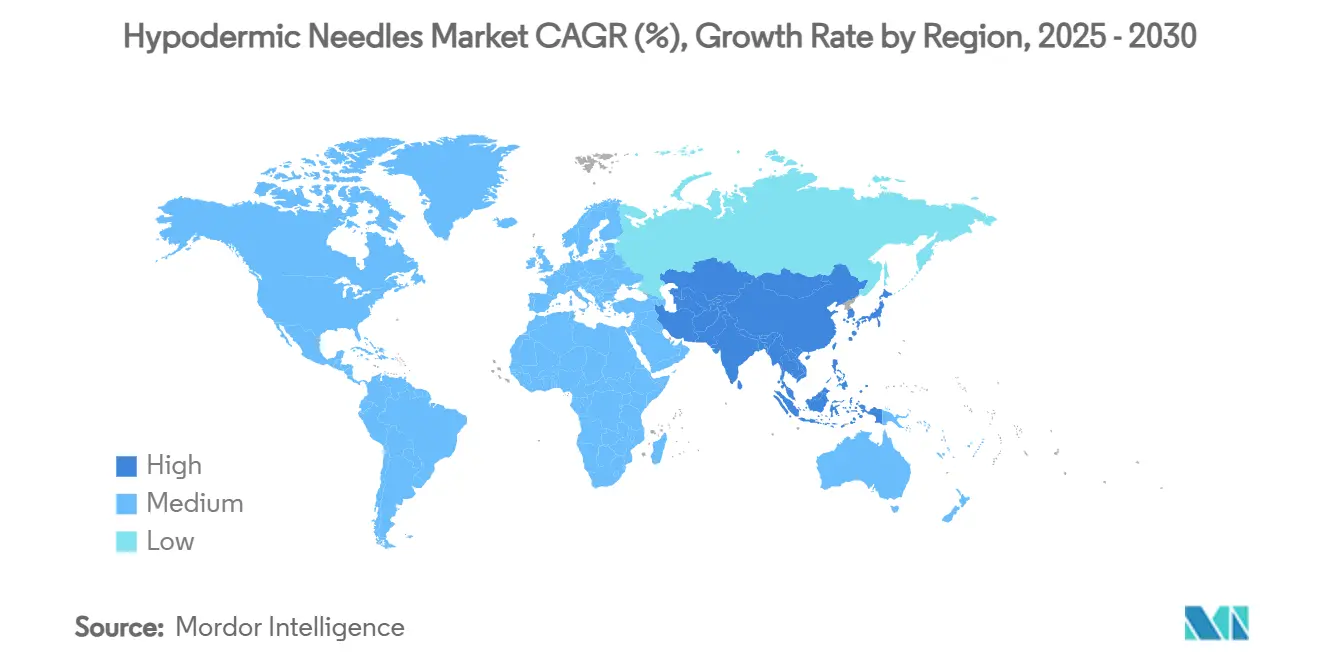

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hypodermic Needles Market Analysis by Mordor Intelligence

The global hypodermic needles market size stood at USD 3.94 billion in 2025 and is projected to reach USD 4.65 billion by 2030, reflecting a 3.37% CAGR over the forecast period. Robust demand for safety-engineered devices, expanding chronic-disease therapy volumes, and sustained immunization spending collectively buttress this measured expansion. Safety hypodermic needles dominate procurement decisions as hospital groups, payors, and regulators align around needlestick-injury prevention. Growth is further reinforced by the widening prevalence of diabetes, obesity, and autoimmune disorders that depend on injectable therapies, while new once-weekly formulations sustain per-patient needle value despite lower frequency. Meanwhile, the vaccination infrastructure built during the COVID-19 era continues to propel volume, especially across Asia-Pacific, South Asia, and parts of Africa. Competitive intensity has begun tilting toward manufacturers able to certify devices to multiple safety standards, driving incremental consolidation within the hypodermic needles market.

Key Report Takeaways

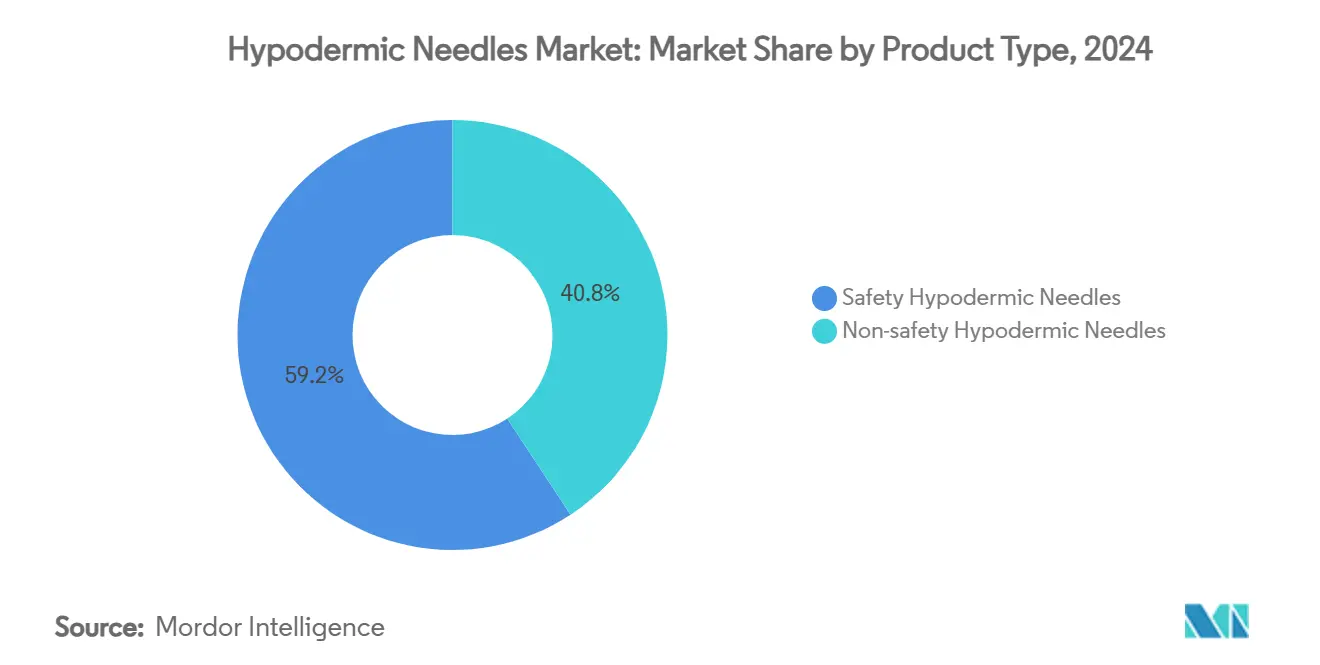

- By product type, safety hypodermic needles led with 59.24% revenue share in 2024; the same segment is forecast to expand at a 6.66% CAGR to 2030.

- By gauge size, 18G-22G needles held 53.23% of the hypodermic needles market share in 2024, while <18G variants record the highest projected CAGR at 5.24% through 2030.

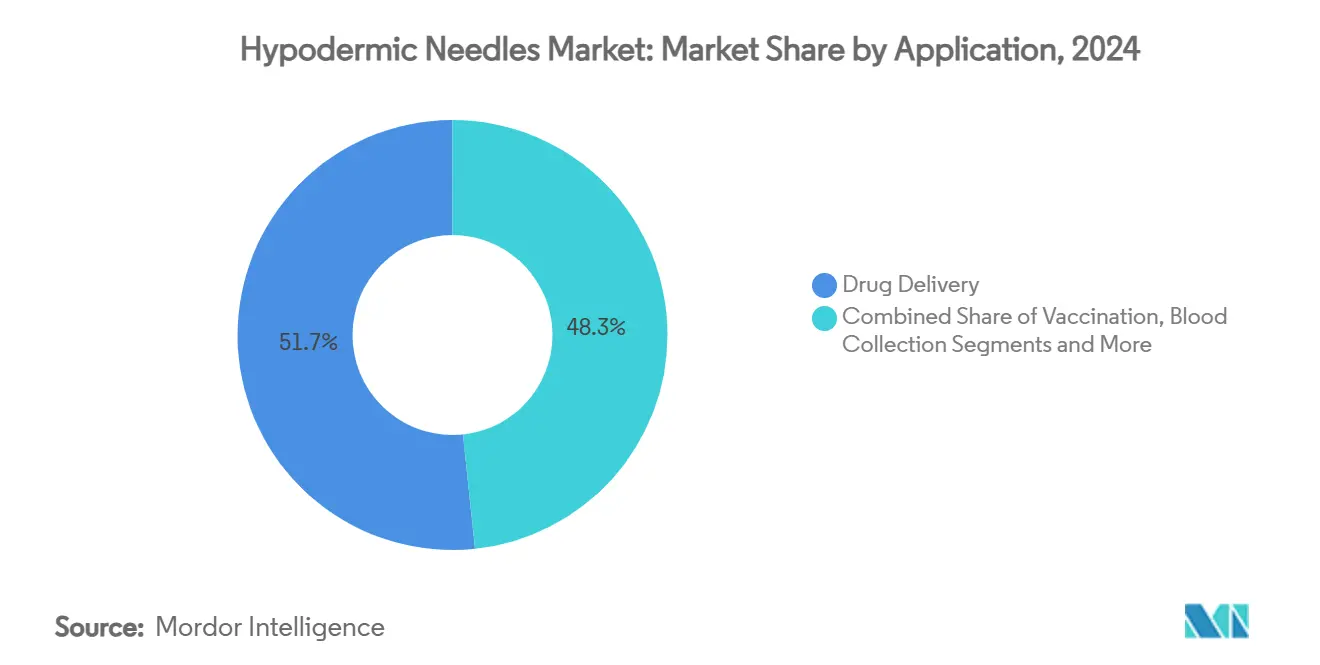

- By application, drug-delivery accounted for 51.66% share of the hypodermic needles market size in 2024; vaccination is advancing at a 7.36% CAGR through 2030.

- By end user, hospitals and ambulatory surgery centers captured 45.24% demand in 2024; home healthcare and self-injection channels are growing at 6.79% CAGR to 2030.

- By geography, North America retained 31.67% share in 2024, whereas Asia-Pacific is poised for a 5.47% CAGR through 2030.

Global Hypodermic Needles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Chronic Diseases Requiring Injectable Therapies | +0.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Global Safety-Engineered Needle Mandates | +0.7% | Global, led by North America & EU regulatory frameworks | Medium term (2-4 years) |

| Mass Immunization & Booster Programs | +0.5% | Global, with emphasis on developing regions | Short term (≤ 2 years) |

| Integrated Auto-Disable Needle-Syringe Innovations | +0.4% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Sustainability Push For Thin-Wall, Low-Waste Designs | +0.3% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Community Harm-Reduction Initiatives Supplying Safe-Injection Kits | +0.2% | North America & Europe, select urban centers globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Requiring Injectable Therapies

Diabetes, obesity, and autoimmune conditions are converging to create a larger pool of patients who need long-term injectable regimens. Novo Nordisk recorded 24% sales growth in its GLP-1 portfolio during 2024, signalling the scale at which weekly injectable obesity drugs are penetrating. The diabesity cohort now exceeds 500 million patients, and forecasts indicate GLP-1 users will quadruple to more than 60 million in the next decade. Although once-weekly insulin icodec may reduce injection frequency, its viscous profile calls for specialized needles that command premium pricing.[1]Roberto Trevisan, “Once-Weekly Insulins: A Promising Approach to Reduce the Treatment Burden in People With Diabetes,” Diabetologia, springer.comConsequently, volume growth moderates while value per unit rises, sustaining the hypodermic needles market even as alternative drug-delivery options mature.

Global Safety-Engineered Needle Mandates

Regulators across the United States, Canada, the European Union, and large emerging economies are aligning around universal adoption of safety needles to cut sharps injuries. WHO’s 2015 “smart syringe” policy remains a powerful procurement lever, and the EU Medical Device Regulation (MDR) demands expanded clinical evidence and post-market surveillance for needle systems.[2]WHO News Desk, “WHO Calls for Worldwide Use of ‘Smart’ Syringes,” World Health Organization, who.int In 2024 the FDA harmonized Quality System requirements with ISO13485, a step that favors established manufacturers already compliant with global standards.[3]Mary Harris, “Medical Devices; Quality System Regulation Amendments,” Federal Register, federalregister.gov Together these frameworks push safety needles from premium line item to baseline specification, accelerating replacement cycles and lifting the overall hypodermic needles market.

Mass Immunization & Booster Programs

COVID-19 infrastructure, annual influenza drives, HPV catch-up campaigns, and new malaria vaccines collectively elevate vaccination volumes. WHO’s Immunization Agenda 2030 aims to avert 4.6 million deaths annually; 2023 efforts prevented 4.2 million, leaving headroom for incremental syringes and needles. Expanded programs often stipulate precise gauge and length combinations, prompting product differentiation within the hypodermic needles market. Moreover, donor-funded initiatives in Gavi countries guarantee multi-year purchasing, cushioning cyclicality. Needle-free jet injectors are making inroads, yet limits on dose accuracy for viscous biologics and higher unit costs restrict widespread substitution for now.

Integrated Auto-Disable Needle-Syringe Innovations

Auto-disable (AD) technology prevents reuse, sharply lowering cross-infection risk in low-resource settings. WHO documented Madagascar’s success with AD syringes, citing >90% health-worker acceptance when paired with adequate training. Production scale is compressing the cost gap between conventional and AD variants, bringing them within tender thresholds for emerging-market ministries of health. New concepts such as KAIST’s temperature-responsive P-CARE needle, which softens irreversibly after one use, exemplify the innovation pipeline. As global funding pivots toward safety and waste reduction, AD devices are poised to widen their share of the hypodermic needles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of Needle-Free Delivery Platforms | -0.6% | North America & Europe, expanding to developed APAC | Medium term (2-4 years) |

| Shift Toward Pen Injectors & Wearable Pumps | -0.4% | Global, led by diabetes care segments | Long term (≥ 4 years) |

| High Unit Cost Of Safety Needles | -0.3% | Developing regions, price-sensitive segments | Short term (≤ 2 years) |

| ESG-Driven Material-Sourcing Restrictions | -0.2% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Needle-Free Delivery Platforms

Needle-free jet injectors have secured Class II status with the FDA, enabling streamlined 510(k) clearances for high-volume immunization drives. Pediatric and geriatric populations value these devices for painless administration and the absence of sharps disposal, prompting hospital pilots across the United States and Europe. Pharmaceutical alliances now target subcutaneous biologics, with several phase-III trials scheduled to report efficacy data by 2027, potentially broadening the addressable market. However, dose-volume limits and reduced accuracy for viscous formulations keep adoption largely confined to vaccines and low-viscosity drugs. Unit economics also remain challenging: most jet systems cost 5-10 times more per use than conventional needles, restricting uptake in cost-sensitive public-health tenders. The net effect trims the overall hypodermic needles market CAGR by 0.6% but does not yet displace core volumes.

Shift Toward Pen Injectors & Wearable Pumps

Prefilled pens and patch pumps integrate the needle into a single disposable device, markedly reducing the need for standalone cannulas. Ypsomed shipped 1.7 billion pens in 2024, confirming scale and consumer preference for concealed-needle formats. BD’s collaboration with Ypsomed on the XtraFlow autoinjector highlights how drug-device co-development concentrates value within proprietary ecosystems. Wearable insulin pumps convert multiple daily injections into one cannula insertion every three days, depressing annual needle counts for diabetes management. Nevertheless, each pen or pump still relies on specialty needles embedded within the device, keeping the upstream demand for precision cannulas intact. Overall, the migration toward integrated delivery trims 0.4 percentage points off forecast CAGR but does not negate growth driven by new biologic launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Safety Features Anchor Market Expansion

Safety needles captured 59.24% revenue in 2024, supported by OSHA, EU MDR, and WHO guidelines that embed injury-prevention criteria in hospital tenders. Built-in shields, passive retraction, and auto-disable mechanisms accommodate both clinical workflows and community programs, broadening customer bases. Cost gaps versus non-safety alternatives narrow as production scales, easing adoption in middle-income markets. Non-safety needles endure in procedural niches where bulky shields obstruct clinician visibility, yet their share erodes steadily.

B. Braun’s NRFit rollout demonstrates how proprietary connectors elevate switching costs while aligning with ISO 80369 standards, thereby solidifying customer loyalty. Concurrently, the FDA’s warning letters to unauthorized Chinese syringes heighten buyer caution and reinforce demand for certified safety brands. As a result, the hypodermic needles market increasingly values total compliance packages—device certification, traceability, and post-market surveillance—over lowest unit price.

By Gauge Size: 18G-22G Dominates, Fine-Wall Variants Gain Speed

The 18G-22G band accounted for 53.23% revenue in 2024, balancing flow rate with patient comfort. For high-viscosity biologics, manufacturers deploy thinner-wall cannulas that preserve lumen volume while reducing outer diameter. This engineering advance improves tolerability without compromising delivery, reinforcing the segment’s dominance. Fine-wall <18G needles are advancing at 5.24% CAGR, propelled by GLP-1 agonists and monoclonal antibodies that demand wider bore sizes to limit injection force.

22G needles remain indispensable for pediatrics, intradermal testing, and aesthetic procedures requiring minimal tissue disruption. Precision machining, electropolishing, and siliconization norms create high entry barriers at these diameters, enabling incumbents to sustain premium margins. Consequently, gauge diversification bolsters the overall hypodermic needles market by matching device attributes to evolving pharmacological profiles.

By Application: Vaccination Growth Surpasses Drug-Delivery Base

Drug-delivery held 51.66% of 2024 revenue, anchored by insulin, heparin, and biologics that necessitate regular injections. The hypodermic needles market size for vaccination, however, is projected to outpace other sectors with a 7.36% CAGR through 2030, underpinned by expanded childhood schedules, adult boosters, and emerging malaria and RSV vaccines. Donor-funded campaigns often mandate auto-disable formats, channeling incremental value into safety-segment revenue. Blood-collection applications contribute steady demand, with oncology and therapeutic apheresis driving specialized high-flow cannulas.

Anesthesia, dermatology, and intravitreal therapies populate the “Other” category, where custom needle attributes justify higher selling prices. Each subsegment demands specific gauge-length pairs, sustaining SKU complexity across the hypodermic needles market. Although oral and transdermal formulations nibble at injection volumes, biologic expansion outweighs substitution pressures.

By End User: Home Healthcare Surges Amid Decentralized Care

Hospitals and ambulatory surgery centers generated 45.24% of 2024 demand, yet growth momentum has shifted toward home-healthcare channels, expanding at 6.79% CAGR. Payers encourage self-administration to curb inpatient costs, driving adoption of prefilled syringes with passive safety features. The hypodermic needles market size attached to retail prescription fills is expected to climb as GLP-1 and autoimmune biologics proliferate. Diagnostic and pathology centers sustain regular venipuncture purchases, insulated from substitution risks by laboratory throughput requirements.

Structured diabetic-patient programs round out demand by bundling needles with education and monitoring services, improving adherence. Regulators are issuing guidance for device “human-factors” validation in non-clinical settings, compelling manufacturers to simplify labeling and packaging. This patient-centric design ethos further widens the user base for the hypodermic needles market.

Geography Analysis

North America retained 31.67% revenue share in 2024, upheld by OSHA regulations, high insurance penetration, and rapid integration of safety innovations. Market participants expanded local manufacturing footprints—BD has committed USD 2.5 billion to U.S. capacity over five years—to mitigate supply-chain risk and satisfy “Made in USA” procurement clauses. Europe follows closely, buoyed by the MDR’s emphasis on clinical evidence and sustainability. Circular-economy directives encourage thin-wall, low-waste designs, nudging purchasing committees toward premium SKUs; the region’s procurement thus tilts toward value-added models.

Asia-Pacific exhibits the fastest 5.47% CAGR through 2030 on the back of community-health infrastructure expansion, growing middle-class populations, and surging incidences of diabetes and cardiovascular disease. China’s recent clampdown on substandard syringe imports, coupled with WHO guideline adoption, accelerates premiumization trends. India and Indonesia capitalize on Gavi and UNICEF funding to roll out auto-disable devices, broadening the hypodermic needles market footprint.

The Middle East and Africa show varied growth trajectories; Gulf Cooperation Council states import safety needles to meet JCI accreditation requirements, whereas sub-Saharan nations rely on donor-funded immunization drives, anchoring demand predictability. Latin America progresses steadily despite currency volatility; Brazil’s private hospitals and Terumo’s Puerto Rico plant strengthen regional supply security. Collectively, geographical patterns highlight a dual-track hypodermic needles market: mature regions prioritizing safety and ESG attributes, and developing markets scaling baseline access.

Competitive Landscape

The hypodermic needles market is moderately concentrated. BD, Terumo, and B. Braun leverage broad portfolios, global regulatory dossiers, and multi-site manufacturing to secure preferred-supplier status in hospital tenders. BD’s planned separation of its Biosciences and Diagnostic Solutions units signals sharper focus on core medical-technology segments, including advanced needle systems. Terumo posted 12.4% revenue growth in fiscal 2024, underpinned by strong Asia-Pacific orders and global demand for infusion therapy solutions.

Retractable Technologies specializes in auto-retractable designs, addressing North American group-purchasing requirements. Nipro operates six manufacturing plants, supporting competitive pricing for conventional needles while incrementally adding safety variants. Strategic alliances—such as BD’s partnership with Ypsomed—underscore convergence between drug formulation complexity and device engineering. Heightened FDA enforcement against unauthorized imports tilts U.S. purchasing toward established, fully audited suppliers, squeezing smaller entrants. M&A activity is expected to intensify as mid-tier players seek scale to manage ESG and MDR compliance loads, further concentrating the hypodermic needles market.

Hypodermic Needles Industry Leaders

-

Becton, Dickinson and Company

-

B. Braun Melsungen AG

-

Terumo Corporation

-

Nipro Corporation

-

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Terumo launched the Injection Filter Needle, featuring an integrated 5-micron filter to prevent particulate transfer in hypodermic and intravitreal injections.

- February 2024: Terumo Medical Corporation broke ground on a 64,000-ft² facility in Caguas, Puerto Rico, a USD 30 million investment to expand global device supply by mid-2025.

Global Hypodermic Needles Market Report Scope

| Safety Hypodermic Needles |

| Non-safety Hypodermic Needles |

| <18G |

| 18G–22G |

| >22G |

| Drug Delivery |

| Vaccination |

| Blood Collection |

| Others |

| Hospitals & Ambulatory Surgery Centers |

| Diagnostic & Pathology Centers |

| Home Healthcare & Self-Injection |

| Diabetic Patient Group Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Safety Hypodermic Needles | |

| Non-safety Hypodermic Needles | ||

| By Gauge Size | <18G | |

| 18G–22G | ||

| >22G | ||

| By Application | Drug Delivery | |

| Vaccination | ||

| Blood Collection | ||

| Others | ||

| By End User | Hospitals & Ambulatory Surgery Centers | |

| Diagnostic & Pathology Centers | ||

| Home Healthcare & Self-Injection | ||

| Diabetic Patient Group Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global hypodermic needles market in 2025?

It stood at USD 3.94 billion in 2025 and is on track to reach USD 4.65 billion by 2030.

Which product category is expanding most rapidly through 2030?

Safety hypodermic needles exhibit the fastest 6.66% CAGR thanks to regulatory mandates and hospital injury-prevention protocols.

Why do clinicians favor 18G-22G gauges for most injections?

These gauges balance flow rate and patient comfort, giving them a 53.23% revenue share in 2024.

How much growth is expected from Asia-Pacific sales?

Asia-Pacific is forecast to register a 5.47% CAGR to 2030 as healthcare spending and immunization drives accelerate.

In what ways do safety regulations affect needle demand?

OSHA, EU MDR, and WHO “smart syringe” policies convert safety features from premium to baseline specifications, lifting replacement cycles.

Are needle-free devices eroding traditional needle volumes?

Jet injectors and similar systems reduce growth by 0.6% on the projected CAGR, signaling incremental—not disruptive—impact for now.

Page last updated on: