Peripheral Vascular Devices And Accessories Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

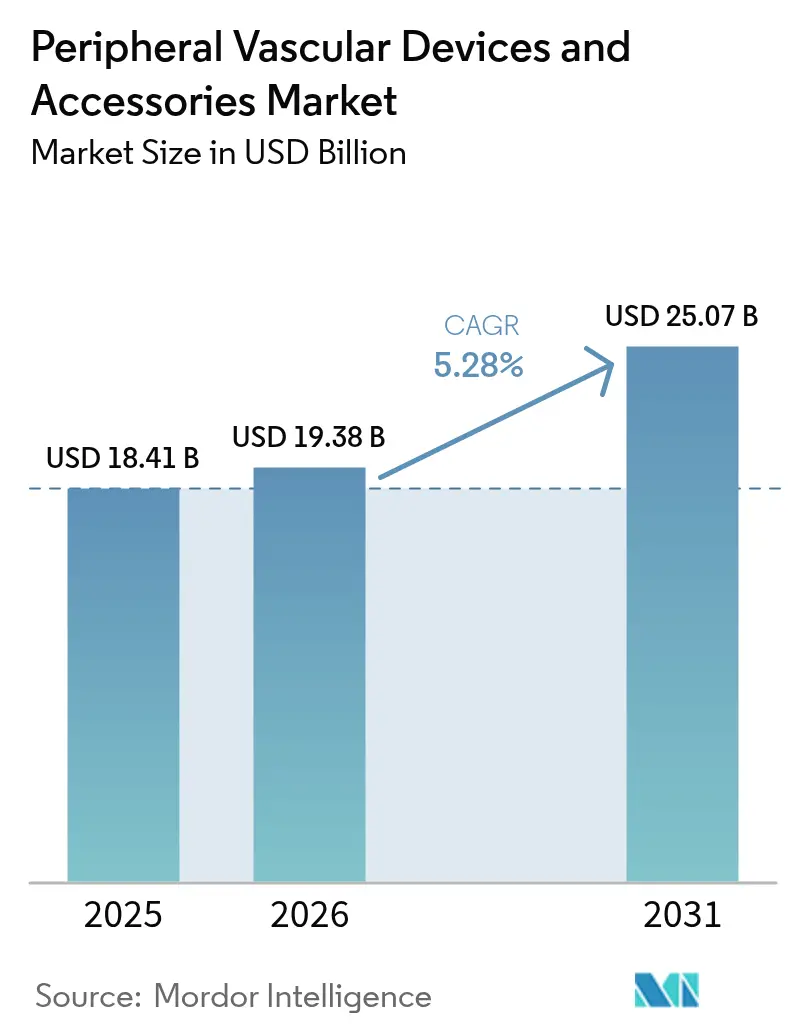

| Market Size (2026) | USD 19.38 Billion |

| Market Size (2031) | USD 25.07 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

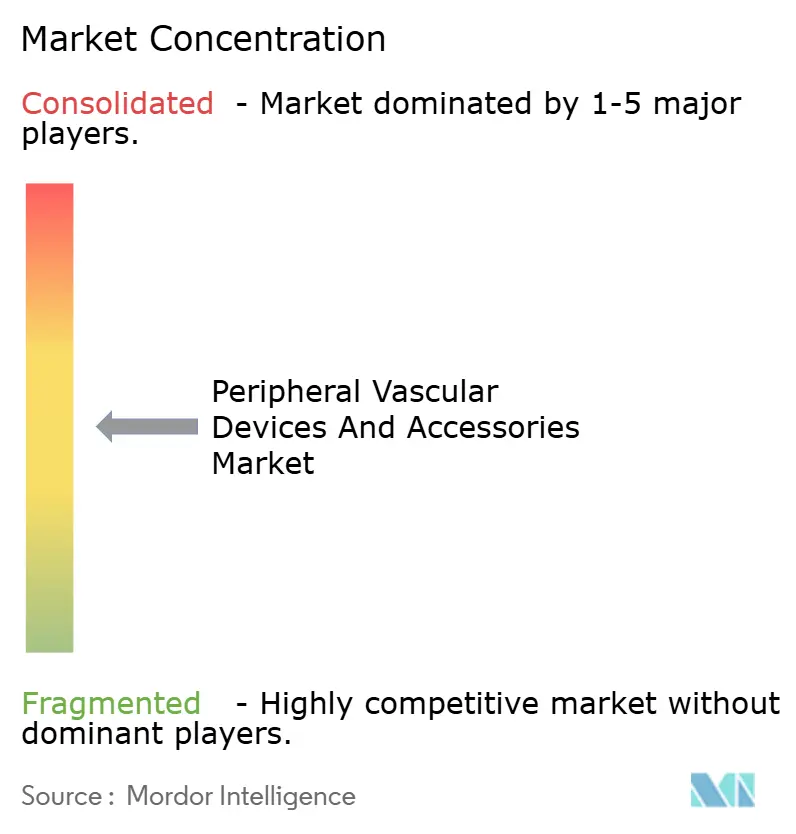

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peripheral Vascular Devices And Accessories Market Analysis by Mordor Intelligence

The peripheral vascular devices and accessories market size is expected to grow from USD 18.41 billion in 2025 to USD 19.38 billion in 2026 and is forecast to reach USD 25.07 billion by 2031 at 5.28% CAGR over 2026-2031. The growth path is shifting from pure procedure volume to value-based innovation, with AI-guided imaging, drug-eluting balloons and bio-absorbable scaffolds winning premium reimbursement. Demand escalates as ageing populations swell the pool of peripheral artery disease (PAD) patients who favor minimally invasive endovascular solutions that shorten hospital stays. At the same time, hospital groups and ambulatory surgical centers (ASCs) accelerate the migration of complex vascular procedures to outpatient settings to curb costs and improve patient convenience. Heightened regulatory scrutiny slows small innovators yet advantages scale players that can fund robust evidence generation and navigate the U.S.-FDA and EU-MDR regimes. Intensifying M&A—more than USD 12 billion in disclosed deals during 2024-2025—signals a pivot toward end-to-end product portfolios spanning devices, accessories and connected digital workflows.

Key Report Takeaways

- By product type, devices led with 73.85% of peripheral vascular devices and accessories market share in 2025, while accessories are projected to expand at a 5.94% CAGR through 2031.

- By application, PAD accounted for 44.72% share of the peripheral vascular devices and accessories market size in 2025; varicose-vein treatment is advancing at a 6.55% CAGR to 2031.

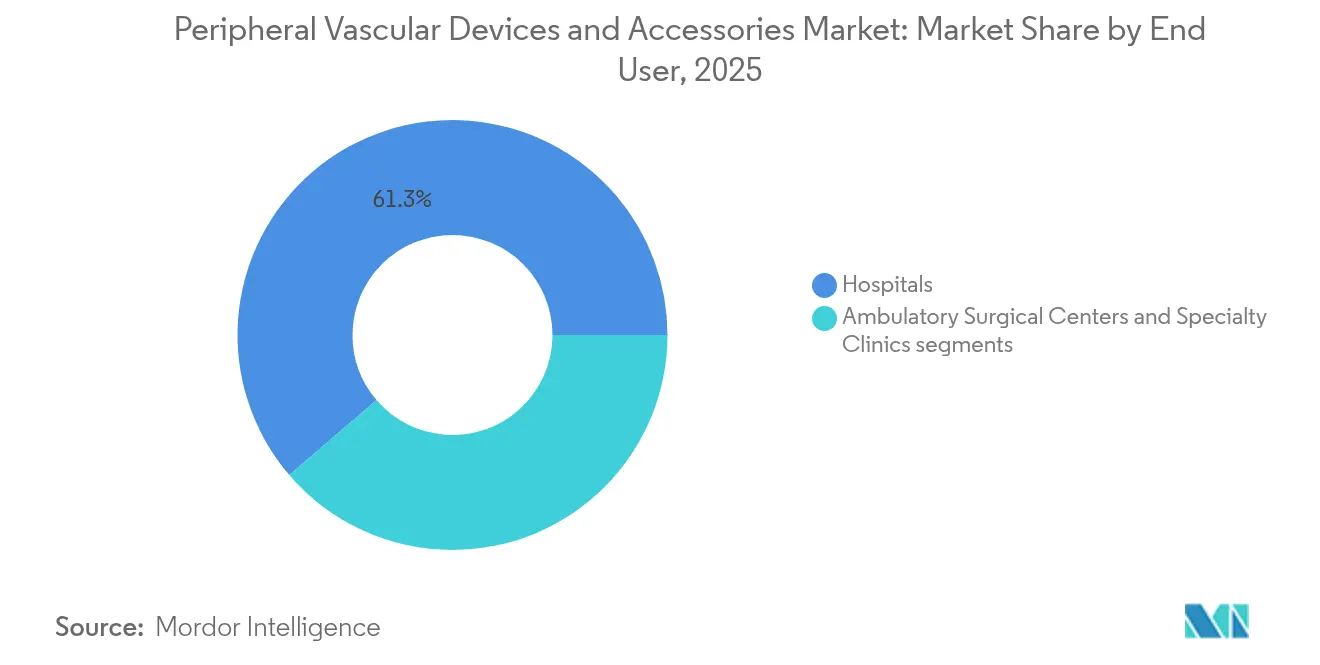

- By end user, hospitals held 61.28% revenue share in 2025, whereas ASCs record the fastest growth at 6.73% CAGR during 2026-2031.

- By geography, North America captured 39.92% share of the peripheral vascular devices and accessories market size in 2025; Asia-Pacific is expanding at a 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peripheral Vascular Devices And Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising PAD prevalence in ageing population | +1.20% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Preference for minimally-invasive endovascular therapy | +1.00% | Global, led by North America & APAC adoption | Medium term (2-4 years) |

| Favourable reimbursement for drug-eluting stents & balloons | +0.80% | North America & EU core markets | Short term (≤ 2 years) |

| AI-guided intravascular imaging catheters boost procedural success | +0.60% | North America & APAC early adopters | Medium term (2-4 years) |

| 3-D printed, patient-specific vascular grafts enter pilot use | +0.40% | North America & EU research centers | Long term (≥ 4 years) |

| Government cath-lab build-outs in tier-2 Chinese cities from 2025 | +0.30% | APAC, specifically China tier-2 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising PAD Prevalence in Ageing Population

More than 20 million U.S. adults live with PAD, and growth in the 65-plus population is increasing procedure volumes. Elderly patients frequently present multivessel, calcified lesions that require premium drug-coated balloons, bio-absorbable scaffolds and advanced atherectomy tools. Medicare reimbursement for outpatient vascular interventions broadens access, and hospital networks lean on same-day discharge pathways to manage capacity. Demand for patient-specific grafts is rising because anatomical variability increases with age, supporting early adoption of 3-D-printed or tissue-engineered options. Collectively, the demographic wave sustains double-digit growth in the high-value device sub-segments of the peripheral vascular devices and accessories market.

Preference for Minimally Invasive Endovascular Therapy

Clinical evidence indicates that endovascular approaches reduce complications and speed recovery compared with open surgery, with ASCs emerging as the fastest-growing site of service and spurring compact, integrated device designs, while drug-coated balloons and intravascular lithotripsy catheters deliver hospital-level outcomes without major capital outlays, and CMS now provides distinct outpatient reimbursement codes for these technologies. As payers lean on bundled payments, suppliers that bundle devices, navigation software and post-procedure monitoring apps gain negotiating leverage.

Favourable Reimbursement for Drug-Eluting Stents & Balloons

In July 2024 CMS created new device pass-through categories that top up payments when facilities use innovative peripheral devices, giving early-mover manufacturers clear economic headroom [1]Source: Centers for Medicare & Medicaid Services, “July 2024 Hospital Outpatient Prospective Payment System Update,” cms.gov . U.S. policy aligns with the EU’s hospital funding models that reward lower re-intervention rates, boosting uptake of long-acting drug-eluting stents (DES) and balloons (DEB). Established vendors that published five-year patency data lock in coding advantages, while late entrants face steeper data demands under EU-MDR. Reimbursement certainty also underpins premium pricing, enabling firms to channel margin into next-generation polymer coatings and sustained-release drug platforms for the peripheral vascular devices and accessories market.

AI-Guided Intravascular Imaging Catheters Boost Procedural Success

AI-enabled systems automatically extract vessel diameter, plaque composition and flow reserve data in real time, allowing operators to optimize balloon sizing and stent placement. FDA-cleared platforms such as AVVIGO demonstrated a 26% drop in target-vessel failure when imaging guidance informed therapy choices. The technology simultaneously reduces fluoroscopy time and contrast load, attractive benefits for frail renal patients. AI workflow analytics feed into remote mentoring dashboards, opening skill-transfer pathways in underserved regions. Vendors able to fuse imaging, AI and therapeutic delivery on a single console position themselves as system partners rather than product suppliers in the peripheral vascular devices and accessories market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent US-FDA & EU MDR evidence requirements | -0.70% | North America & EU regulatory markets | Medium term (2-4 years) |

| High device recall incidence hurting clinician confidence | -0.50% | Global, concentrated in established markets | Short term (≤ 2 years) |

| Shortage of trained interventional radiologists in ASEAN & LATAM | -0.40% | ASEAN & LATAM emerging markets | Long term (≥ 4 years) |

| Hospital CAPEX freezes amid value-based procurement in Europe | -0.30% | Europe, with spillover to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent US-FDA & EU-MDR Evidence Requirements

Since September 2024 European regulators demand deeper clinical datasets and ongoing post-market surveillance before renewing licenses, lengthening development timelines and raising compliance costs . The U.S. Quality System Regulation rewrite, effective February 2026, mirrors ISO 13485 and obliges manufacturers to document risk-management loops from design through end of life. Mid-size firms struggle to bankroll new randomized trials, which accelerates consolidation as they seek the shelter of multinationals’ regulatory infrastructures. While the bar deters fast followers, first movers with mature quality systems turn the compliance burden into a durable moat within the peripheral vascular devices and accessories market.

High Device Recall Incidence Hurting Clinician Confidence

Recent Class I recalls, such as the 7,820-unit pullback of the Pipeline Vantage Embolization Device, underscore safety concerns in complex delivery systems. Each public alert triggers extra training requirements, slows adoption curves and raises malpractice insurance costs for physicians. Hospitals respond with stricter value-analysis committee reviews, stretching sales cycles. Conversely, suppliers that can show single-digit complaint rates and real-time field-service dashboards win clinician loyalty. The recall climate also fuels demand for AI-driven procedural safeguards that flag atypical pressure gradients or embolic risk during use, supporting premium accessory sales in the peripheral vascular devices and accessories market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Device Dominance Faces Accessory Innovation

The device category accounted for 73.85% of peripheral vascular devices and accessories market share in 2025, anchored by percutaneous transluminal angioplasty (PTA) balloons and self-expanding stents with proven long-term patency. Drug-eluting formulations and next-generation nitinol architectures allow these workhorse products to defend unit prices even as hospitals push bulk-buy contracts. Atherectomy and thrombectomy systems deepen margins by addressing calcific, chronic total occlusion and venous thromboembolism cases that demand specialized toolkits. IVC filters and embolic-protection lines remain smaller niches, yet their critical safety roles secure formulary access.

Accessories, although accounting for only 26.15% of 2025 revenue, are projected to outpace the parent class at a 5.94% CAGR through 2031, thereby lifting the overall peripheral vascular devices and accessories market size trajectory. Hydrophilic-coated guidewires, torque-responsive catheters and steerable sheaths shorten procedure times in tortuous anatomy, directly translating into ASC throughput gains. Vascular closure devices such as MYNX CONTROL cut time-to-ambulation by more than 50%, aligning with value-based metrics. Compression systems and pressure-monitoring kits unlock post-discharge revenue streams and embed vendors deeper into episode-of-care economics.

By Application: PAD Leadership Challenged by Varicose-Vein Innovation

PAD commanded 44.72% of 2025 revenue after decades of clinical guideline support and payer familiarity. Five-year data from the IN.PACT Global study showed 69.4% freedom from target-lesion revascularization, supporting drug-coated balloon use in femoropopliteal disease. Hospitals continue to invest in IVL consoles that safely fracture calcium and expand lumen area without overheating or distal embolization.

Varicose-vein treatment is growing fastest at 6.55% CAGR to 2031, buoyed by office-based radiofrequency and endovenous laser ablation that require minimal capital outlay. Medicare utilization climbed from 0.3 to 2.6 procedures per 1,000 beneficiaries between 2017 and 2024, highlighting a robust shift toward cosmetic–functional hybrid care. Deep-vein thrombosis interventions also gain momentum as mechanical thrombectomy devices such as FlowTriever remove large clot burdens without thrombolytics. Hemodialysis-access maintenance remains a specialized segment; Wrapsody endoprosthesis showed 89.8% six-month primary patency, easing reintervention burdens for vascular surgeons.

By End User: Hospital Dominance Erodes to ASC Efficiency

Hospitals retained 61.28% revenue share in 2025 thanks to imaging suites, hybrid ORs and intensive-care backup needed for multilevel disease. However, fixed-cost pressure and value-based purchasing curb the pace of premium-device adoption. Instead, administrators negotiate multi-year, volume-based agreements that squeeze list prices across the peripheral vascular devices and accessories market.

ASCs capture the highest growth at 6.73% CAGR, catalyzed by physician ownership models and transparent bundled pricing that appeals to commercial insurers. Procedure migration spans from simple superficial venous work to complex iliac angioplasty as low-profile devices and imaging carts mature. Specialty vascular clinics add a third care tier, blending outpatient efficiency with focused expertise. Device makers that package balloons, closure systems and cloud-based reporting tools in single-invoice kits resonate strongly with ASC buyers.

Geography Analysis

North America delivered 39.92% of global revenue in 2025, powered by early reimbursement for breakthrough devices such as Abbott’s Esprit BTK dissolving scaffold and Humacyte’s SYMVESS tissue-engineered vessel . The region’s hospitals adopt predictive analytics to flag restenosis risk, and payers expand peripheral bundles that reward durable patency. M&A activity—Stryker’s USD 4.9 billion Inari purchase and Boston Scientific’s serial bolt-ons—reflect scale plays to defend share amid price compression. Canada and Mexico trail U.S. adoption curves by two to three years but accelerate catheter-lab capacity expansion under public-private partnership models.

Europe balances innovation leadership against intensified regulation. Full EU-MDR enforcement forces companies to run longer pivotal trials, stretching average approval timelines past 24 months. National health systems pivot to value-based procurement, pushing suppliers to package devices with training, registries and remote monitoring. Germany and the United Kingdom remain the top adopters of AI-guided imaging, while France channels stimulus funds into outpatient facility upgrades. Southern European nations emphasize cost-effective DES and guidewire kits to manage rising PAD burden without inflating hospital budgets.

Asia-Pacific is the fastest-growing theatre, set to grow at 7.05% CAGR through 2031. China’s central government is underwriting cath-lab rollouts in more than 120 tier-2 cities, directly fueling bulk tenders for balloons, stents and IVL consoles. Local manufacturing incentives reduce tariff barriers and encourage Western OEMs to form joint ventures for value-engineering. Japan’s super-aged society drives demand for low-contrast, low-radiation tools, and insurers reimburse IVL at hospital-outpatient parity to cut length of stay. India expands private cardiac-care chains, seeking mid-price devices that balance cost and durability, while Australia and South Korea prioritize AI-enabled guidance to offset interventional radiologist shortages. Collectively, the region reshapes competitive dynamics by favoring companies that tailor portfolios to diverse price points within the peripheral vascular devices and accessories market.

Competitive Landscape

Consolidation intensified during 2024-2025, with disclosed deals surpassing USD 12 billion as strategics raced to assemble full-continuum portfolios. Stryker vaulted into venous thrombectomy by buying Inari Medical, capturing high-margin FlowTriever and ClotTriever systems that address pulmonary embolism and DVT. Boston Scientific pursued a platform strategy, adding Silk Road Medical’s TCAR stroke-prevention system and Bolt Medical’s IVL catheter to complement its leading DEB and DES lines. Teleflex broadened reach by purchasing BIOTRONIK’s peripheral portfolio, then announced a corporate split to sharpen focus on vascular access.

Large players leverage supply-chain resilience, omnichannel sales and regulatory scale to defend pricing. They also integrate digital command centers—combining imaging, AI analytics and remote mentoring—to entrench themselves as solution partners. Meanwhile, disruptive entrants target white spaces: Humacyte secured the first FDA clearance for an acellular tissue-engineered vessel that could redefine trauma reconstruction, and several start-ups deploy 3-D-printed grafts tuned to patient anatomy.

Competitive emphasis is shifting toward software-driven ecosystems. AI algorithms that auto-segment vessel morphology, alert to pressure anomalies and suggest balloon sizing may soon become gating features for tenders. Vendors capable of bundling hardware, disposables, analytics and cloud-based case registries can differentiate beyond per-unit discounts. As hospital groups adopt centralized value-analysis committees, suppliers with demonstrable outcome data and low recall incidence win preferred-vendor status across the peripheral vascular devices and accessories market.

Peripheral Vascular Devices And Accessories Industry Leaders

Boston Scientific Corporation

Abbott

Becton, Dickinson and Company

Medtronic plc

Cook Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Boston Scientific completed the acquisition of Bolt Medical for up to USD 664 million, adding acoustic-wave IVL technology.

- March 2025: Shockwave Medical launched the Javelin peripheral IVL catheter in the United States.

- February 2025: Teleflex acquired BIOTRONIK’s vascular-intervention business for EUR 760 million (USD 791 million).

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the peripheral vascular devices and accessories market as all new, commercially available devices, including stents, drug-coated balloons, atherectomy and thrombectomy systems, IVC filters, guidewires, introducer sheaths, and vascular closure and compression aids, used to diagnose or treat blood-vessel disorders outside the heart and brain. According to Mordor Intelligence, accessories are included whenever they form an essential part of the procedural kit, and revenues are reported at manufacturer selling price.

Scope exclusion: We purposely leave out implantable cardiac and neuro-interventional products, as well as any refurbished equipment.

Segmentation Overview

- By Product Type

- Device (Value)

- Percutaneous Transluminal Angioplasty (PTA) Balloons

- Peripheral Stents (Bare-metal, Drug-eluting, Covered)

- Atherectomy Devices

- Thrombectomy Devices

- Inferior Vena Cava (IVC) Filters

- Embolic Protection Devices

- Accessories (Value)

- Guidewires

- Introducer Sheaths

- Vascular Closure Devices

- Compression Devices

- Device (Value)

- By Application (Value)

- Peripheral Artery Disease

- Deep Vein Thrombosis

- Varicose Veins

- Hemodialysis Access

- By End User (Value)

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We then interview interventional radiologists, vascular surgeons, cath-lab managers, and procurement officers across North America, Europe, Asia-Pacific, and selected emerging hubs. These conversations let us validate utilization rates, average selling prices, and adoption curves that were unclear in secondary material, and they inform the final assumption set before modeling.

Desk Research

We start by combing open data sets from bodies such as the American Heart Association, World Bank, OECD health statistics, and Eurostat; these give us prevalence, procedure, and spend trends that anchor incidence and treatment volumes. Trade registers, US FDA 510(k) filings, and patent databases like Questel help us track product launches and competitive intensity. Company 10-Ks, investor decks, tender notices from Tenders Info, and news feeds aggregated through Dow Jones Factiva round out pricing and capacity signals.

The desk sources named are illustrative only; our analysts consulted many additional publicly available and subscription references during dataset build and verification.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient model builds global demand pools, which are then reconciled with sampled bottom-up supplier revenue checks to adjust outliers. Key variables we track include the diagnosed Peripheral Artery Disease population, procedure mix shift toward minimally invasive care, average stent and balloon ASP progression, hospital bed expansion, and reimbursement updates. Multivariate regression links those drivers to annual market value, while scenario analysis stress-tests currency and pricing swings. Any missing unit data are imputed through region-level trade statistics and benchmarked against peer interviews before finalization.

Data Validation & Update Cycle

Triangulation, anomaly flags, and multi-step peer review precede sign-off. Our models refresh every twelve months, and we issue interim tweaks when recalls, major approvals, or macro shocks materially alter device demand. A fresh analyst pass is always completed just before a report is released to clients.

Why Our Peripheral Vascular Devices and Accessories Baseline Inspires Confidence

Published estimates often diverge because firms pick different device baskets, price points, and update rhythms. We anchor our baseline on a clearly stated scope, live ASP tracking, and annual prevalence audits, making it easier for decision makers to trace every input.

Key gap drivers arise when others omit accessory revenue, rely on static exchange rates, or apply aggressive discount curves not verified with providers, which pulls their totals materially lower than ours.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 18.41 Bn (2025) | Mordor Intelligence | |

| USD 11.14 Bn (2025) | Global Consultancy A | Narrow device basket and limited country coverage |

| USD 11.43 Bn (2024) | Global Consultancy B | Hospital survey only, fixed exchange rates |

| USD 13.51 Bn (2025) | Industry Journal C | Conservative ASP trend, omits closure devices |

The comparison shows that, by selecting the full accessory line, validating prices through field checks, and updating every year, Mordor Intelligence delivers a balanced, transparent baseline that users can reproduce and trust for planning.

Key Questions Answered in the Report

What is the current size of the peripheral vascular devices and accessories market?

The market is valued at USD 19.38 billion in 2026 and is projected to reach USD 25.07 billion by 2031.

Which product segment is growing fastest?

Accessories—such as guidewires, sheaths and closure devices—are forecast to expand at a 5.94% CAGR to 2031, outpacing core devices.

Why are ambulatory surgical centers important for future growth?

ASCs enable complex vascular procedures in lower-cost, outpatient settings, and their share is rising at 6.73% CAGR over 2026-2031 as payers reward same-day discharge pathways.

Which region offers the highest growth opportunity?

Asia-Pacific leads with a 7.05% CAGR through 2031, driven by large patient pools and expanding cath-lab infrastructure in China, India and Southeast Asia.

How are AI technologies influencing the market?

AI-guided imaging platforms reduce procedure time, cut radiation exposure and lower target-vessel failure rates, allowing vendors to command premium prices.

Page last updated on: