Peripheral Artery Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

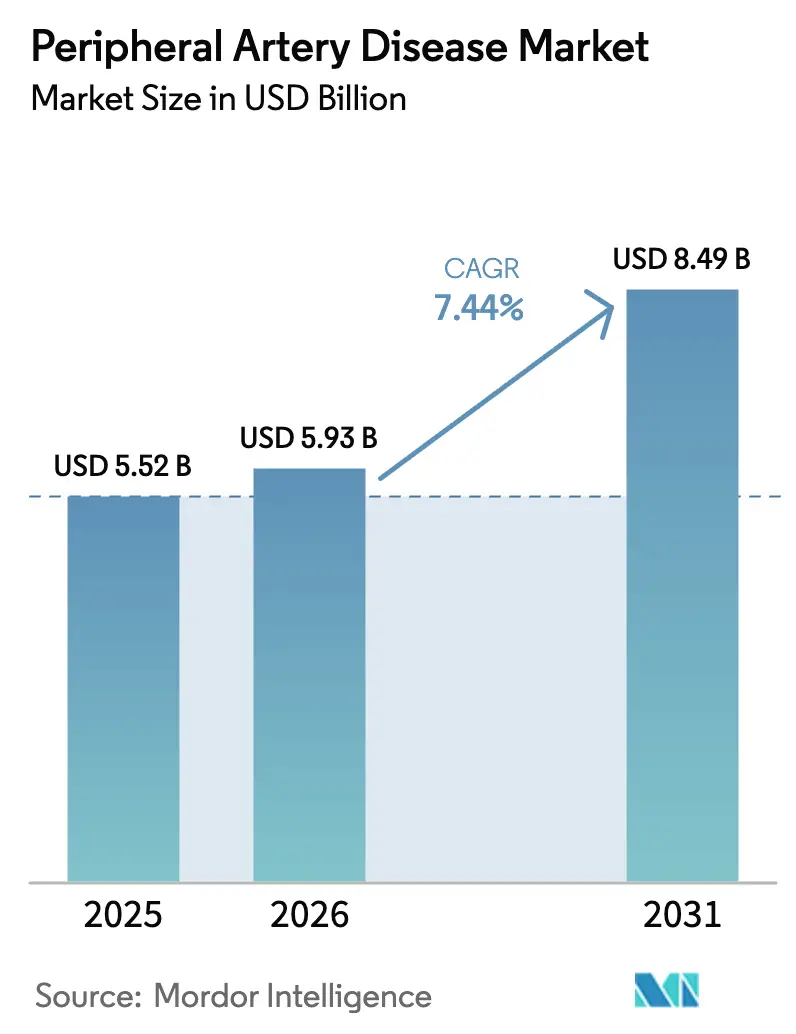

| Market Size (2026) | USD 5.93 Billion |

| Market Size (2031) | USD 8.49 Billion |

| Growth Rate (2026 - 2031) | 7.44% CAGR |

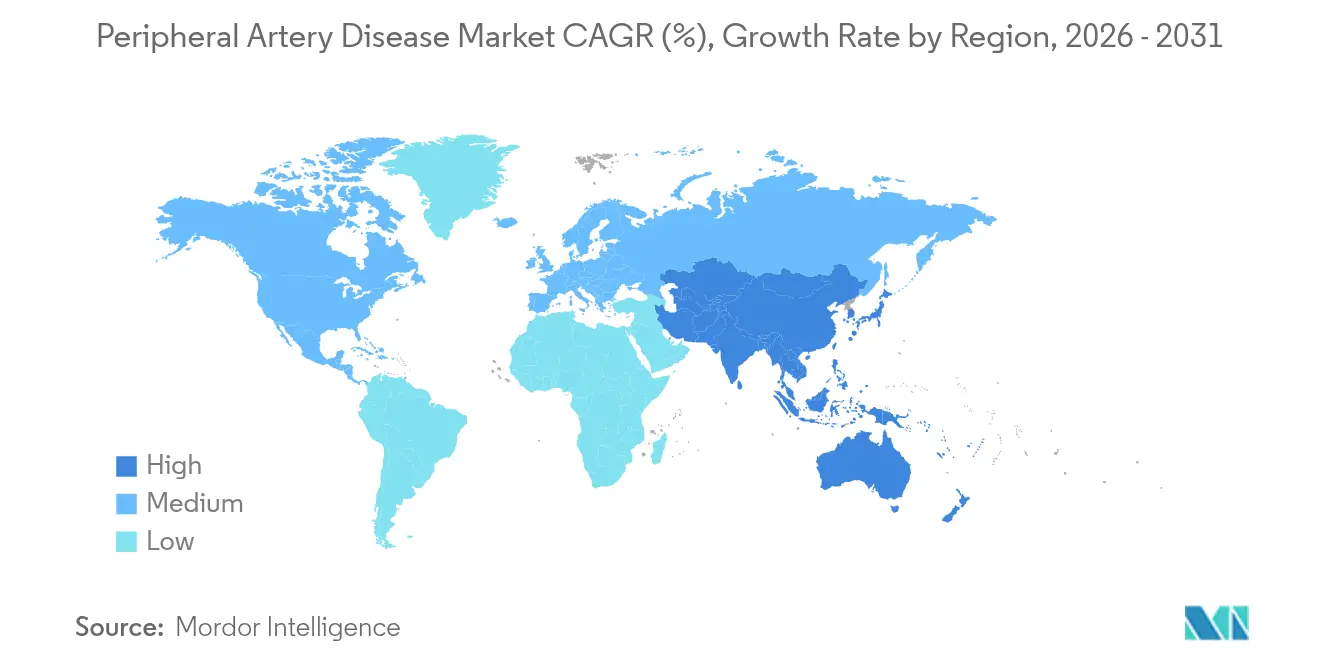

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Peripheral Artery Disease Market Analysis by Mordor Intelligence

The peripheral artery disease market size is expected to grow from USD 5.52 billion in 2025 to USD 5.93 billion in 2026 and is forecast to reach USD 8.49 billion by 2031 at 7.44% CAGR over 2026-2031. Rising diabetes prevalence, rapid uptake of minimally invasive endovascular devices, and wider adoption of value-based reimbursement programs are aligning to accelerate procedure volumes. Device-centric therapies keep expanding as hospitals modernize catheter laboratories and outpatient centers pursue same-day discharge models. Regulatory support remains visible, with the FDA green-lighting 15 new peripheral vascular devices in 2024. At the same time, supply constraints for medical-grade nitinol and renewed scrutiny of paclitaxel-coated technologies temper near-term growth in cost-sensitive regions. Strategic acquisitions, highlighted by Stryker’s USD 4.9 billion purchase of Inari Medical, hint at deeper consolidation aimed at next-generation solutions.

Key Report Takeaways

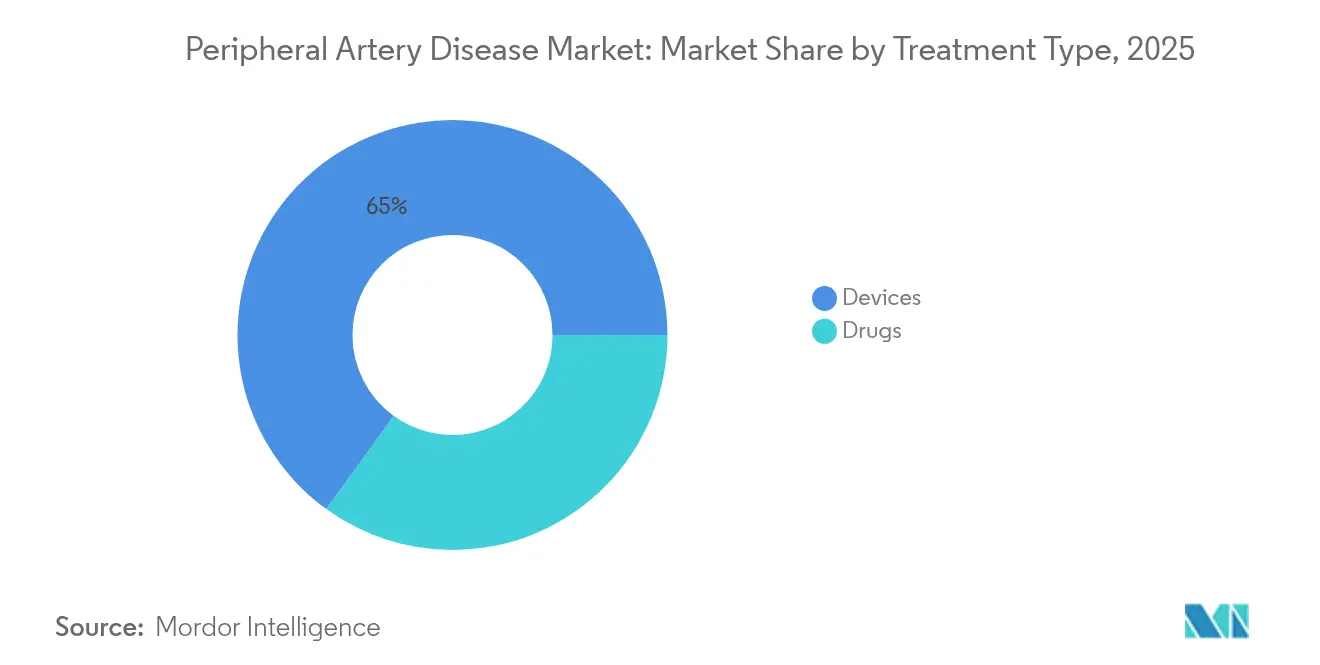

- By treatment type, devices led with 65.02% of peripheral artery disease market share in 2025, while pharmaceuticals are expanding at a 9.88% CAGR to 2031.

- By end user, hospitals controlled 65.85% of the peripheral artery disease market size in 2025; ambulatory surgical centers (ASCs) post the fastest 9.47% CAGR through 2031.

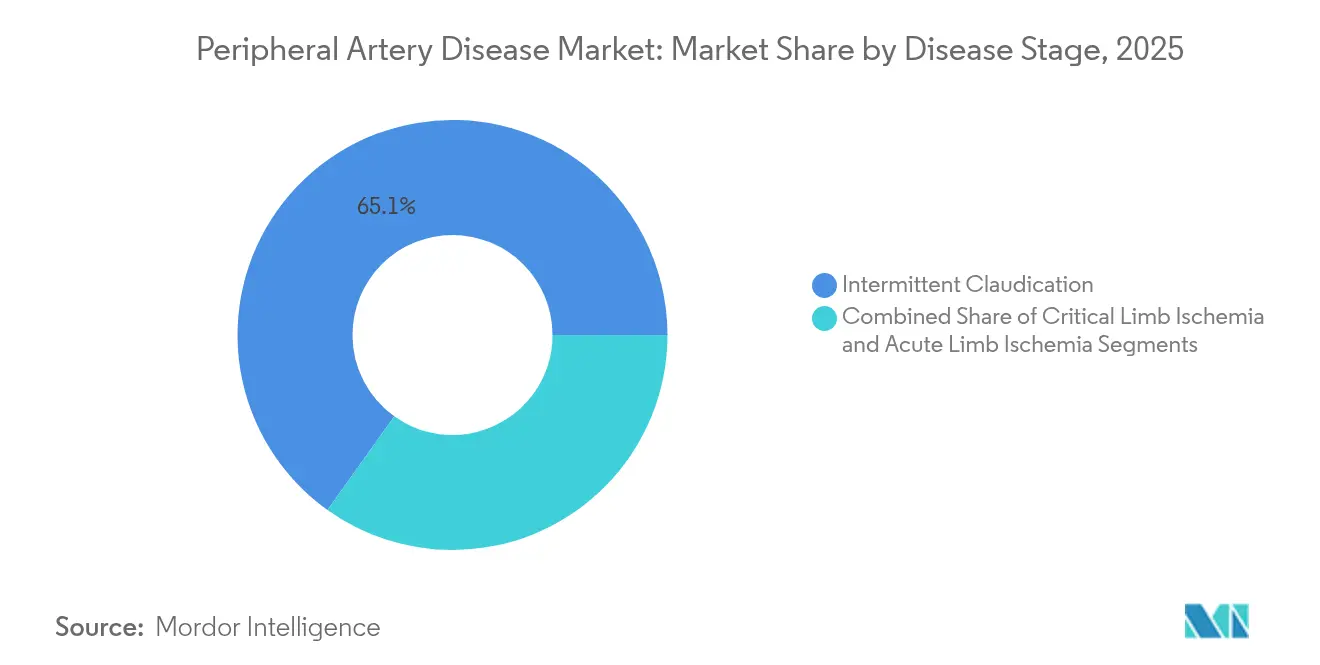

- By disease stage, intermittent claudication held 65.12% share of the peripheral artery disease market in 2025, whereas critical limb ischemia (CLI) advances at an 8.55% CAGR.

- By anatomy treated, lower-extremity procedures captured 78.05% of peripheral artery disease market share in 2025 and renal-visceral interventions are projected to grow at a 9.31% CAGR.

- By geography, North America accounted for 40.88% of 2025 revenue; Asia-Pacific shows the fastest 8.43% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Peripheral Artery Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of peripheral artery disease | +1.8% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Increasing prevalence of diabetes & hypertension | +1.5% | Global, faster in Asia-Pacific | Medium term (2-4 years) |

| Technological advances in endovascular devices | +1.2% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| Shift toward minimally invasive, outpatient PAD interventions | +1.0% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| AI-enabled vascular imaging for earlier PAD diagnosis | +0.8% | North America & EU, selective APAC | Medium term (2-4 years) |

| Value-based reimbursement models drive limb-salvage outcomes | +0.6% | North America core, expanding to EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden Of Peripheral Artery Disease

Roughly 12 million Americans live with PAD, and prevalence among those older than 70 years approaches 20%[1]Centers for Disease Control and Prevention, “About Peripheral Arterial Disease (PAD),” cdc.gov. Demographic ageing boosts procedure demand as larger cohorts enter peak incidence age brackets. Disease progression from asymptomatic plaque to CLI creates a cascade of diagnostic imaging, drug therapy, and endovascular intervention that lifts device utilization. Outcomes are time-sensitive; each 10-day delay from diagnosis to revascularization raises amputation risk by 2.5%. Hospitals therefore prioritize rapid referral pathways, reinforcing investment in on-site imaging and hybrid operating theaters. The resulting uptick in elective revascularizations underpins steady revenue visibility for suppliers.

Increasing Prevalence Of Diabetes & Hypertension

Diabetic patients older than 50 exhibit markedly higher PAD rates than age-matched non-diabetics. Asia-Pacific bears the brunt as urban lifestyles accelerate early-onset metabolic syndrome. Complicated below-the-knee lesions are common in this group, pushing demand for smaller drug-coated balloons, atherectomy platforms, and advanced imaging. Providers respond with integrated vascular-endocrine clinics capable of aggressive risk-factor control and early intervention. Post-COVID analyses show 49% mortality among PAD amputees versus 39% in the pre-pandemic era, underscoring the importance of timely therapy.

Technological Advances In Endovascular Devices

Intravascular lithotripsy has achieved 100% lesion-crossing success in early studies, signaling a leap forward for heavily calcified occlusions. FDA clearance of Abbott’s Esprit BTK drug-coated balloon adds an option for CLI patients requiring below-the-knee therapy. Robotic systems advance too; Microbot Medical filed a 510(k) submission for its LIBERTY platform designed to cut radiation exposure for physicians[2]Microbot Medical, “FDA Submission for LIBERTY Endovascular Robotic System,” ir.microbotmedical.com. Such innovations prompt hospitals and ASCs to refresh capital equipment, sustaining device order pipelines.

Shift Toward Minimally-Invasive, Outpatient PAD Interventions

CMS payment rules introduced in 2024 improved reimbursement for outpatient endovascular procedures, accelerating migration from inpatient suites to ASCs[3]U.S. Department of Health & Human Services, “CY 2025 Physician Fee Schedule,” federalregister.gov. ASCs emphasize same-day discharge, shorter recovery, and lower infection risk, aligning with patient preferences. Device makers optimize product designs for quick deployment and minimal complications, including rapid arterial closure systems such as Vasorum’s Celt ACD Plus. Payers benefit from cost efficiency, further fortifying outpatient adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device cost & complex reimbursement pathways | -1.2% | Global, highest in emerging markets | Medium term (2-4 years) |

| Stringent regulatory approvals and product recalls | -0.9% | Global, regulatory variations by region | Short term (≤ 2 years) |

| Safety debate over paclitaxel-coated balloons & stents | -0.7% | North America & EU | Medium term (2-4 years) |

| Supply-chain shortages of medical-grade nitinol | -0.5% | Global manufacturing and supply networks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Cost & Complex Reimbursement Pathways

Value-based purchasing requires documented cost-effectiveness before payers authorize premium devices. The retirement of certain Local Coverage Determinations for pneumatic compression treatments illustrates shifting reimbursement sands. Emerging markets feel the pinch most, often defaulting to older-generation stents to preserve limited budgets. Innovators that lack dedicated billing codes must finance real-world evidence programs to support payer negotiations, stretching commercialization timelines.

Stringent Regulatory Approvals And Product Recalls

Post-market surveillance tightened after several high-profile recalls of peripheral devices in 2024, lengthening approval cycles and elevating compliance costs. Smaller firms face resource strain navigating parallel pathways across the FDA, EMA, and varying national agencies. The result is delayed market entry, constricted competition, and heightened acquisition interest from larger players equipped with robust regulatory teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Devices Drive Innovation Leadership

Devices held 65.02% of peripheral artery disease market share in 2025 as hospitals prioritized definitive revascularization over medical management. Drug-coated balloons, self-expanding nitinol stents, and plaque modification systems dominate the revenue mix. Intravascular lithotripsy and atherectomy are the fastest-growing device niches, offering solutions for calcified lesions that historically required open surgery. Bioresorbable scaffolds gather momentum in complex femoropopliteal disease, while guidewires, sheaths, and adjunctive closure tools log steady replacement demand. Pharmaceutical therapy grows at a 9.88% CAGR as broader indications for antiplatelet agents and PCSK9 inhibitors spur uptake. Combination protocols—drug-eluting devices paired with dual antiplatelet therapy—illustrate convergence of device and drug strategies. Adjunctive agents such as cilostazol remain vital for symptom relief in claudication cohorts, ensuring pharmacies benefit alongside device suppliers.

By End User: Hospital Dominance Faces ASC Challenge

Hospitals controlled 65.85% of peripheral artery disease market size in 2025, capitalizing on infrastructure suited for complex, comorbidity-laden patients. Tertiary centers manage emergency bypass, dialysis access rescue, and multilevel occlusions needing hybrid approaches. ASCs are the fastest-growing venue at 9.47% CAGR as reimbursement parity improves and patients favor low-acuity settings. These centers specialize in straightforward femoral or tibial interventions with same-day discharge, easing inpatient bed pressure. Specialty vascular clinics fit between the two, delivering targeted expertise with imaging and wound-care integration. Tele-health and remote monitoring extend post-procedure oversight into homes, creating opportunity for connected wearables and AI-guided wound photography. A hub-and-spoke ecosystem thus emerges, balancing high-acuity cases in hospitals against volume procedures in outpatient nodes.

By Disease Stage: Claudication Volume Meets CLI Urgency

Intermittent claudication accounted for 65.12% of peripheral artery disease market share in 2025 as guideline revisions encouraged early endovascular therapy to improve walking distance and life quality. Routine office-based duplex screening now feeds more patients into intervention pipelines before limbs face imminent risk. Critical limb ischemia generates an 8.55% CAGR thanks to better imaging, increased diabetic foot surveillance, and aggressive limb-salvage mandates. CLI cases command higher revenue per patient due to multilevel treatment and adjunctive wound products. Acute limb ischemia remains numerically smaller yet attracts premium pricing for on-call thrombectomy kits and intensive care capacity. Risk-stratified care pathways aim to intercept high-risk claudicants before progression, aligning with value-based contracts that penalize major amputations.

By Anatomy Treated: Lower-Extremity Focus Expands Upward

Lower-extremity arteries delivered 78.05% of peripheral artery disease market share in 2025, reflecting entrenched procedure algorithms for femoral, popliteal, and tibial disease. Below-the-knee work is particularly buoyant in diabetic populations, encouraging launch of smaller balloons, thin-strut stents, and dedicated crossing catheters. Renal and visceral territories post the strongest 9.31% CAGR as next-generation steerable sheaths and advanced imaging open complex abdominal branches to endovascular therapy. Upper-extremity interventions retain steady volume through dialysis access maintenance and occasional subclavian stenosis cases. The anatomical broadening underlines the maturation of peripheral skills among interventional cardiologists, radiologists, and vascular surgeons, enlarging addressable opportunity for niche device suppliers.

Geography Analysis

North America retained 40.88% of global revenue in 2025, supported by insurance coverage, expansive catheter lab infrastructure, and uniform clinical guidelines that favor early intervention. Medicare bundled payments encourage limb-salvage outcomes, pushing hospitals to invest in advanced imaging and hybrid theaters. Canada offers universal coverage, while Mexico’s private sector and rising medical tourism diversify regional demand.

Asia-Pacific exhibits an 8.43% CAGR to 2031, the fastest worldwide. China scales tertiary cardiovascular centers under public insurance reform, and Japan’s ageing demographics sustain steady procedural volumes allied to high technology adoption. India, though cost-sensitive, represents a large untreated population; tier-one cities now host dedicated vascular institutes, catalyzing uptake of value-engineered devices. Australia and South Korea act as regional reference markets where novel technologies first secure reimbursement.

Europe maintains modest expansion underpinned by universal health coverage and clinical excellence across Germany, France, Italy, Spain, and the United Kingdom. Germany leads procedural counts through dense hospital networks, while the UK navigates budget constraints yet preserves guideline-based access. Eastern European countries modernize angiography suites, broadening market potential. Regulatory harmonization continues under the EU Medical Device Regulation, yet post-Brexit pathways introduce distinct UK approvals, requiring dual submissions for continent-wide access.

Competitive Landscape

Competition is moderate as diversified multinationals duel with agile innovators. Medtronic, Boston Scientific, and Abbott leverage global sales footprints, broad product catalogs, and sizeable R&D budgets to defend share. Stryker moved decisively into the space with its USD 4.9 billion acquisition of Inari Medical, targeting thrombectomy and venous disease adjacencies. Teleflex likewise expanded by purchasing BIOTRONIK’s vascular portfolio, signalling appetite for one-stop platforms.

Emerging disruptors exploit white space in robotic navigation, AI-guided imaging, and bioresorbable scaffolds. Microbot Medical seeks to commercialize the LIBERTY robotic system once FDA clearance finalizes. Boston Scientific broadened its laser toolkit via the Bolt Medical acquisition and continues to publish supportive trial data, reinforcing clinician confidence. Patent filings covering aspiration catheter tips, drug-elution chemistries, and steerable micro-catheters highlight an innovation pipeline that remains active despite mounting capital intensity.

Value-based care shifts competition toward demonstrable outcome superiority and total cost-of-care savings. Vendors that combine real-world evidence, device-drug synergies, and digital follow-up platforms position themselves to capture formulary preference as hospitals rationalize vendor panels. Strategic alliances with AI imaging specialists and wound-care companies illustrate the drive toward ecosystem offerings rather than single-device sales.

Peripheral Artery Disease Industry Leaders

Boston Scientific Corporation

Becton, Dickinson and Company,

Medtronic plc

Abbott Laboratories

Edwards Lifesciences Corporation.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Boston Scientific completed the acquisition of Bolt Medical, adding advanced laser platforms for coronary and peripheral artery disease pending FDA commercialization.

- November 2024: Philips initiated a clinical trial of a new PAD treatment device with the first successful patient procedure.

Global Peripheral Artery Disease Market Report Scope

As per the scope of the report, peripheral artery disease (PAD) narrows arteries in the legs or arms, diminishing blood flow to these limbs. Often stemming from atherosclerosis, PAD involves the accumulation of fatty deposits in the arteries. Symptoms range from leg pain or cramping during activity to numbness; in severe instances, ulcers or non-healing wounds may occur. PAD is closely associated with other cardiovascular diseases and risk factors, including diabetes, high blood pressure, high cholesterol, and smoking.

The peripheral artery disease market is segmented by treatment type, end user, and geography. By treatment type, the market is divided into devices and drugs. By devices, the market is segmented into balloon catheters, plaque modification devices, stents, atherectomy devices, guidewires and sheaths, and other devices. The other devices segment includes bypass graft devices and hemodynamic flow alteration devices. By drugs, the market is segmented into lipid-lowering drugs, antiplatelet drugs, thrombolytic agents, triple-H therapy, and other drugs. The other drugs segment includes glucose-regulating drugs, inotropes, and anti-inflammatory agents. By end user, the market is segmented into hospitals, specialty clinics, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done based on value (in USD).

| Devices | Balloon Catheters | Drug-Coated Balloons |

| Plain Old Balloons | ||

| Plaque Modification Devices | ||

| Stents | Drug-Eluting Stents | |

| Bare-Metal Stents | ||

| Bioresorbable Scaffolds | ||

| Atherectomy Devices | ||

| Guidewires & Sheaths | ||

| Bypass Grafts & Hemodynamic Flow-Alteration | ||

| Drugs | Lipid-Lowering Agents | |

| Antiplatelet Agents | ||

| Anticoagulants & Thrombolytics | ||

| Vasodilators | ||

| Other Adjunctive Drugs | ||

| Hospitals |

| Specialty Vascular Clinics |

| Ambulatory Surgical Centers |

| Home-Care & Tele-health Settings |

| Intermittent Claudication |

| Critical Limb Ischemia |

| Acute Limb Ischemia |

| Lower-Extremity Arteries |

| Upper-Extremity Arteries |

| Renal & Visceral Arteries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Devices | Balloon Catheters | Drug-Coated Balloons |

| Plain Old Balloons | |||

| Plaque Modification Devices | |||

| Stents | Drug-Eluting Stents | ||

| Bare-Metal Stents | |||

| Bioresorbable Scaffolds | |||

| Atherectomy Devices | |||

| Guidewires & Sheaths | |||

| Bypass Grafts & Hemodynamic Flow-Alteration | |||

| Drugs | Lipid-Lowering Agents | ||

| Antiplatelet Agents | |||

| Anticoagulants & Thrombolytics | |||

| Vasodilators | |||

| Other Adjunctive Drugs | |||

| By End User | Hospitals | ||

| Specialty Vascular Clinics | |||

| Ambulatory Surgical Centers | |||

| Home-Care & Tele-health Settings | |||

| By Disease Stage | Intermittent Claudication | ||

| Critical Limb Ischemia | |||

| Acute Limb Ischemia | |||

| By Anatomy Treated | Lower-Extremity Arteries | ||

| Upper-Extremity Arteries | |||

| Renal & Visceral Arteries | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the peripheral artery disease market?

The peripheral artery disease market size reached USD 5.93 billion in 2026 and is forecast to hit USD 8.49 billion by 2031.

Which segment holds the largest share of the peripheral artery disease market?

Devices dominate with 65.02% of 2025 revenue, reflecting widespread preference for minimally invasive revascularization.

Which end-user setting is growing fastest for PAD procedures?

Ambulatory surgical centers are expanding at a 9.47% CAGR as favorable reimbursement and same-day discharge encourage outpatient treatment.

What region shows the highest growth rate in the peripheral artery disease market?

Asia-Pacific posts the fastest regional CAGR at 8.43% through 2031 due to rising diabetes prevalence and expanding healthcare access.

How are technological advances shaping the peripheral artery disease industry?

Breakthroughs such as intravascular lithotripsy, drug-coated balloons for below-the-knee disease, and robotic navigation systems are improving procedural success and widening treatable patient pools.

Page last updated on: