Vascular Patches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

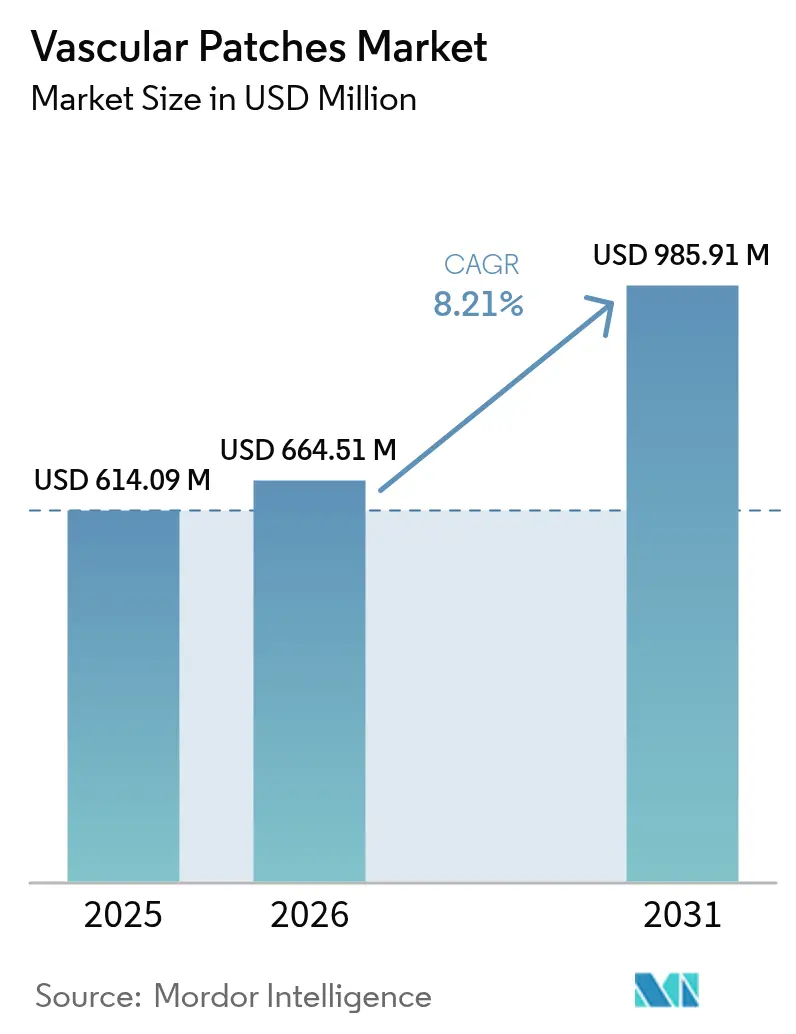

| Market Size (2026) | USD 664.51 Million |

| Market Size (2031) | USD 985.91 Million |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

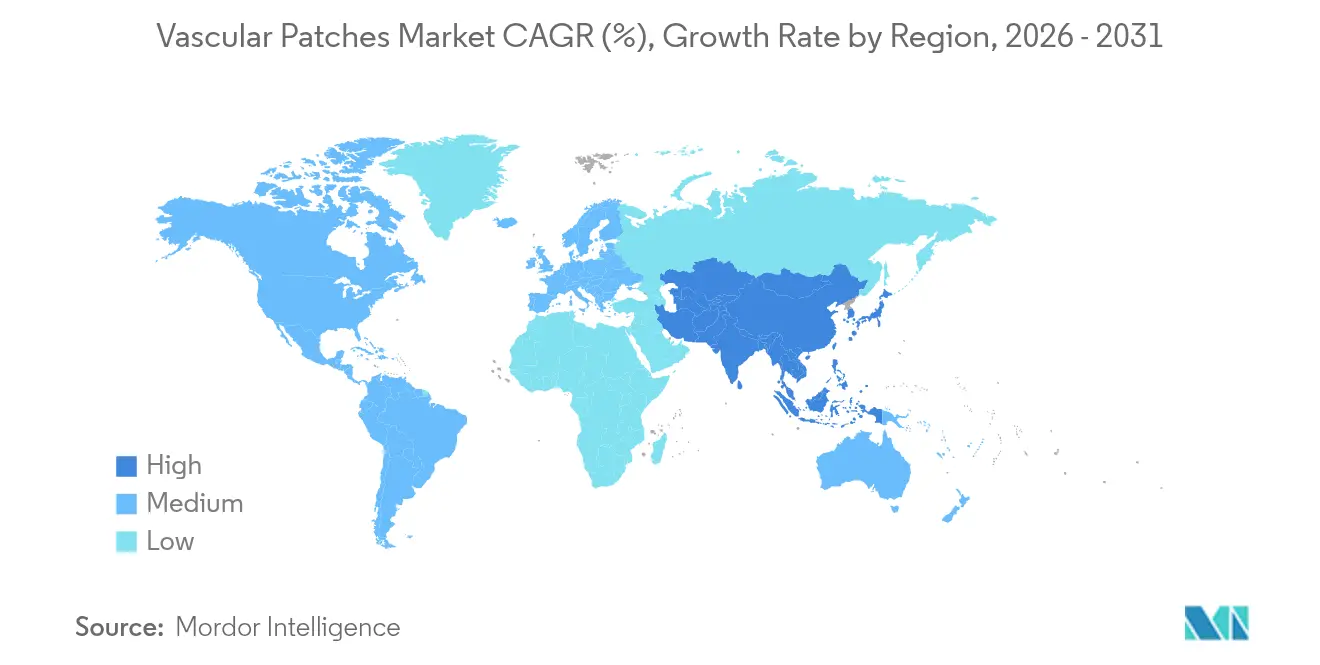

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vascular Patches Market Analysis by Mordor Intelligence

The Vascular Patches Market size in 2026 is estimated at USD 664.51 million, growing from 2025 value of USD 614.09 million with 2031 projections showing USD 985.91 million, growing at 8.21% CAGR over 2026-2031. Expansion reflects an aging population that demands more complex vascular repair, regulatory fast-tracking of resorbable and tissue-engineered patches, and wider acceptance of outpatient vascular surgery. Growth is reinforced by hospitals upgrading toward value-based care models that reward clinical outcomes, while surgeons increasingly rely on patch angioplasty to improve long-term patency. Synthetic materials gain ground thanks to scalable manufacturing and lower unit costs, yet biologic products continue to dominate high-risk and contaminated procedures. Regionally, North America leads on revenue, but Asia-Pacific provides the steepest growth curve as cardiovascular disease prevalence rises and surgical capacity expands.

Key Report Takeaways

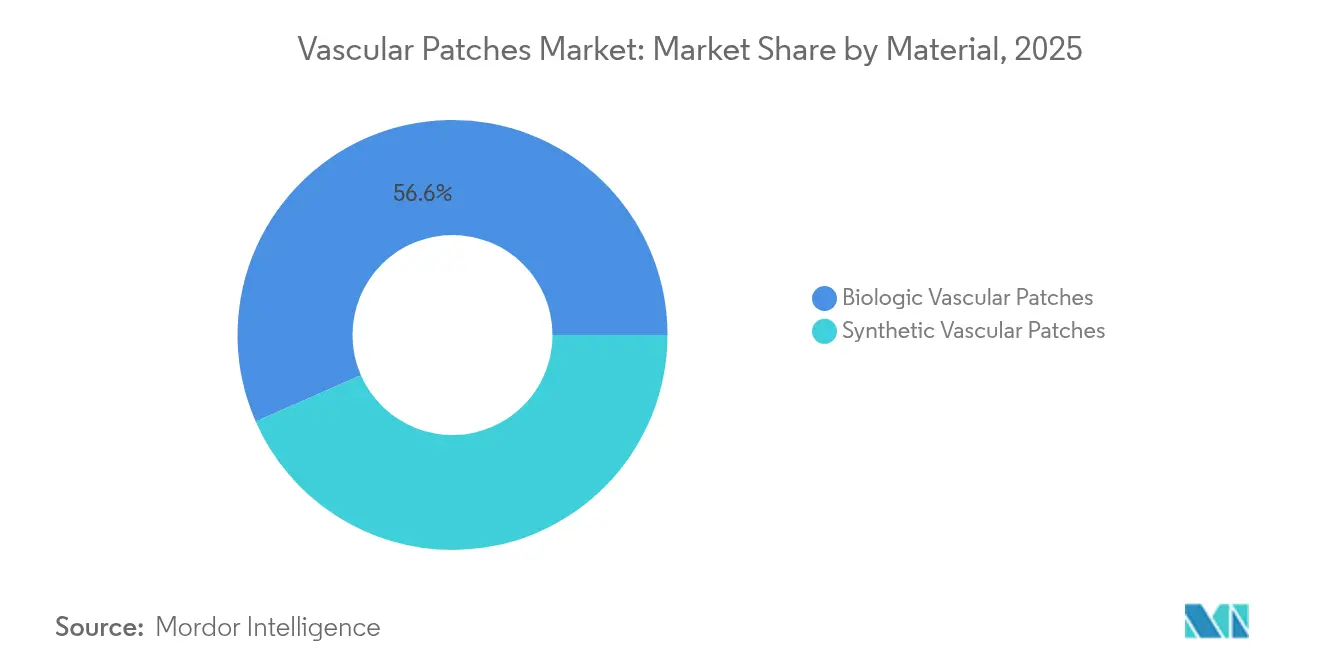

- By material, biologic products led with a 56.58% revenue share in 2025, whereas synthetic patches are set to expand at a 8.88% CAGR through 2031.

- By application, carotid endarterectomy held 54.63% of the vascular patches market share in 2025, while aortic aneurysm repair is projected to grow at 9.24% CAGR to 2031.

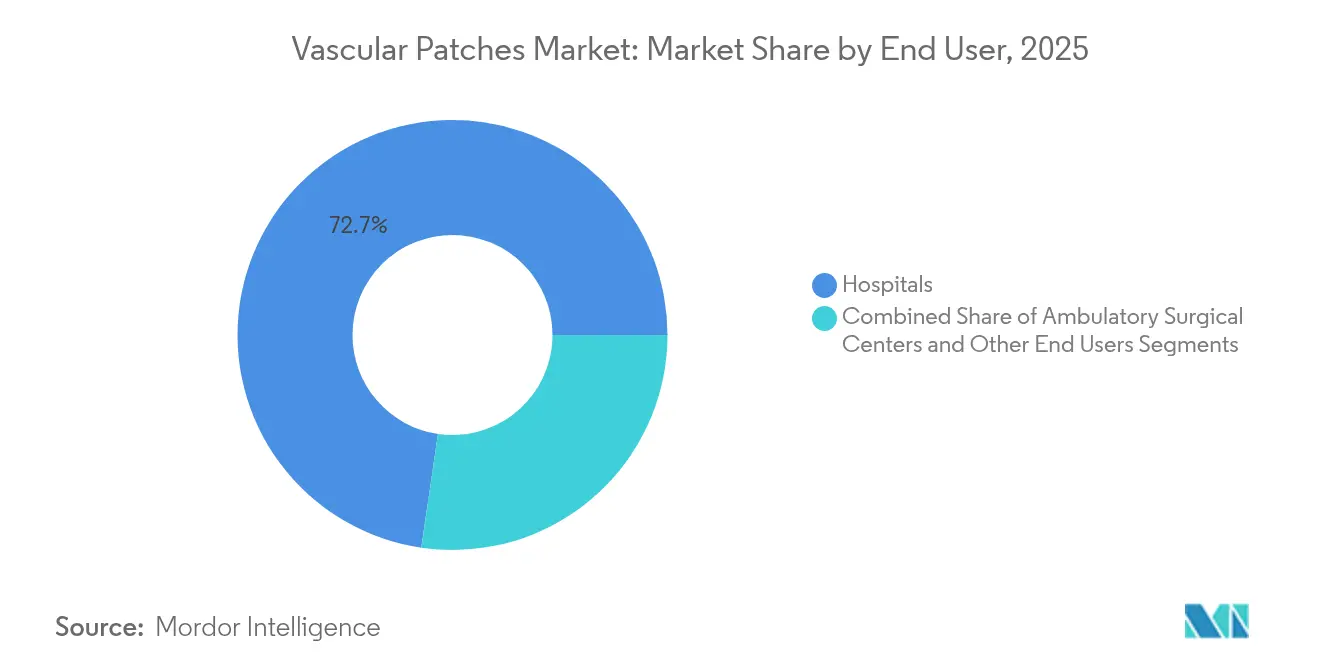

- By end user, hospitals accounted for 72.68% of the vascular patches market size in 2025, yet ambulatory surgical centers will rise at 8.61% CAGR through 2031.

- By geography, North America commanded 35.96% of the vascular patches market in 2025; Asia-Pacific shows the fastest CAGR of 9.62% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vascular Patches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Growing Geriatric Population and Prevalence of Vascular Diseases | +1.8% | Global, with highest concentration in North America and Europe | Long term (≥ 4 years) |

| Surge in Carotid Endarterectomy and Other Vascular Procedures | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Increased Adoption of Biologic Patches | +0.9% | Global, led by developed markets | Medium term (2-4 years) |

| Adoption of 3-D Printed Patient-Specific Vascular Patches | +0.7% | North America & EU core, early adoption in APAC | Long term (≥ 4 years) |

| Regulatory Fast-Tracking of Resorbable ECM Patches for Pediatric Use | +0.6% | Global, with FDA and EMA leading | Short term (≤ 2 years) |

| Outpatient-Based Reimbursement Models for Peripheral Vascular Repair | +0.4% | North America primarily, expanding to EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapidly Growing Geriatric Population and Prevalence of Vascular Diseases

Older adults now represent the single largest cohort undergoing vascular repair, and their numbers continue to climb. Age-related atherosclerosis, carotid stenosis, and peripheral artery disease often require patch angioplasty because primary closure poses higher restenosis risk. Multimorbidity typical in seniors drives surgeons toward materials that integrate smoothly and lower infection odds, a gap biologic patches fill well. Clinical evidence suggests that biologic patches demonstrate superior performance in elderly patients due to reduced inflammatory responses and better integration with aging vascular tissue.

Surge in Carotid Endarterectomy and Other Vascular Procedures

Carotid endarterectomy procedures are experiencing renewed growth as stroke prevention strategies evolve and diagnostic capabilities improve, with patch closure becoming the preferred technique over primary closure due to superior long-term patency rates. Meta-analysis shows patch angioplasty lowers restenosis by 30% versus primary closure, cementing the patch as standard of care regardless of material. Multi-center studies confirm that different patch materials—bovine pericardial, polyester, and venous—yield comparable long-term results, suggesting that procedural technique rather than material choice drives clinical success.[1]Source: David J. Liesker, “Similar Long-Term Outcomes for Venous, Bovine Pericardial, and Polyester Patches for Primary Carotid Endarterectomy,” World Journal of Surgery, wileyonlinelibrary.com

Increased Adoption of Biologic Patches

Clinical trials reveal that biologic patches boast a 91.5% patency rate, outpacing the 78.9% rate of their synthetic counterparts. Furthermore, biologics exhibit a notably lower infection rate of 0.9%, in stark contrast to the 8.4% rate seen with synthetics. The FDA's December 2024 nod to Humacyte's acellular tissue-engineered vessel underscores the viability of large-scale manufacturing for biologic grafts. This endorsement has spurred quicker adoption in hospitals, even in light of the grafts' steeper list prices. These clinical findings not only highlight the superior performance of biologic patches but also suggest significant long-term cost savings for patients.

Adoption of 3-D Printed Patient-Specific Vascular Patches

Three-dimensional printing technology is revolutionizing vascular patch manufacturing by enabling patient-specific geometries that optimize hemodynamic flow patterns and reduce turbulence-related complications. Bioprinting now produces patches that match vessel geometry, smoothing blood flow and shortening healing time. Harvard-led studies highlight embedded micro-vascular networks that promote integration, and automated printing cuts per-unit costs, making patient-specific solutions feasible beyond complex reconstructions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Immune Response and Infection Risk with Xenogeneic Material | -1.1% | Global, particularly in emerging markets with limited post-operative care | Medium term (2-4 years) |

| Product Failures and High-Profile Recalls | -0.8% | Global, with regulatory scrutiny highest in North America and EU | Short term (≤ 2 years) |

| High Device Cost Vs. Limited Reimbursement in Emerging Markets | -0.6% | APAC, MEA, and Latin America primarily | Long term (≥ 4 years) |

| Disruptions in the Bovine-Pericardium Supply Chain (Zoonotic Outbreaks) | -0.4% | Global supply chain, with manufacturing concentrated in specific regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Immune Response and Infection Risk with Xenogeneic Material

Bovine pericardium remains the mainstay of biologic patches yet can trigger alpha-gal reactions in roughly 3% of patients, compelling surgeons to stock alternative materials. Although anti-calcification processing mitigates immune events, infection risk still outpaces autologous options, especially when postoperative care resources are scarce. Clinical studies indicate that bovine pericardial patches demonstrate excellent biocompatibility in most patients, but the subset experiencing adverse reactions requires alternative treatment approaches that complicate surgical planning and inventory management.[2]Source: Ben R. Saleem, “Patch Angioplasty During Carotid Endarterectomy Using Different Materials Has Similar Clinical Outcomes,” Journal of Vascular Surgery, jvascsurg.org

Product Failures and High-Profile Recalls

FDA recalls in 2024 spanning multiple vascular devices shook confidence and forced hospitals to heighten vendor screening. Smaller innovators now face heavier compliance costs that can delay market entry and slow the vascular patches market trajectory. Regulatory agencies are implementing more stringent post-market surveillance requirements that increase compliance costs and extend product development timelines, particularly affecting smaller manufacturers with limited regulatory resources. The recall environment creates competitive advantages for established players with robust quality systems while potentially stifling innovation from emerging companies that lack extensive regulatory track records.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Biologic Dominance Faces Synthetic Innovation

Biologic patches retained 56.58% of 2025 revenue, underscoring surgeon confidence in their superior tissue integration. That segment anchors the vascular patches market because elderly and high-risk patients often present contaminated fields where reduced infection matters most. The synthetic category, however, is advancing at 8.88% CAGR, outpacing the overall vascular patches market as heparin-bonded ePTFE and new copolymers close the biocompatibility gap. Hospitals under fiscal pressure see synthetics as a cost-effective standard for routine arteriotomy closure, especially in outpatient settings.

Competitive focus has therefore shifted from blanket material replacement to application-specific choice: biologic patches dominate complex reconstructions, whereas synthetics expand in predictable, lower-risk repairs. The vascular patches market size for synthetic materials is projected to climb steadily alongside ASC procedure growth, while the biologic share remains durable in value-based care.

By Application: Carotid Procedures Lead, Aortic Repair Accelerates

Carotid endarterectomy generated 54.63% of the vascular patches market in 2025, powered by clinical guidelines that favor patch closure over primary suture for stroke prevention. Strong evidence showing lower restenosis rates sustains high utilization even as stenting alternatives mature. Aortic aneurysm repair is the fastest-growing niche, with 9.24% CAGR, driven by expanding screening programs and technological advances in minimally invasive surgery.

The vascular patches market size for aortic applications is moving upward as endovascular devices increasingly incorporate patch components for seal reinforcement. Pediatric and trauma patches remain smaller segments but promise upside as tissue-engineered and resorbable solutions clear regulatory hurdles.

By End User: ASC Growth Challenges Hospital Dominance

Hospitals retained 72.68% of the vascular patches market size in 2025, yet ambulatory surgical centers are gaining momentum at 8.61% CAGR through 2031. Payment reforms reward lower-cost sites, and surgeons comfortable with patch techniques are migrating routine cases. For ASCs, predictable hemostasis and low infection rates are essential; as a result, high-performance synthetics with anti-thrombogenic coatings see robust uptake.

The vascular patches market share held by hospitals may contract modestly, yet complex open repairs will still anchor inpatient demand. Specialty vascular centers and military facilities form niche demand pockets that prioritize field-ready inventory and rapid application.

Geography Analysis

North America holds the largest regional share at 35.96%, driven by high procedure volume and early adoption of breakthrough devices. Medicare’s reimbursement structure, which increasingly favors ambulatory procedures, drives diffusion of patches that balance cost efficiencies with superior outcomes. FDA fast-track designations, such as the December 2024 approval of Humacyte’s ATEV, keep the region at the forefront of biologic innovation.

Asia-Pacific is the vascular patches market’s fastest-growing geography, expanding at a 9.62% CAGR. Aging populations and westernized lifestyles raise cardiovascular disease incidence, while government-led infrastructure development improves surgical capacity. Local price sensitivity favors high-volume synthetic products, yet widening middle-class insurance coverage unlocks demand for premium biologics in major urban centers. Regulatory harmonization through initiatives such as ASEAN Medical Device Directive is shortening product approval times, offering manufacturers a clearer path to market leadership.

Europe, Middle East & Africa, and South America together contribute material revenue though with varied growth trajectories. EU MDR increases compliance costs and could slow the introduction of novel patches, but mature surgical expertise supports stable demand. South America’s growth hinges on economic stability and public-private partnerships that expand access to vascular surgery. In MEA, limited reimbursement and supply-chain hurdles curb adoption; nonetheless, select Gulf states invest heavily in tertiary cardiovascular centers, creating pockets of high-end demand. Across these regions, supply-chain resilience and cost-effective synthetic innovations determine competitive edge.

Regulatory Landscape

Regulation for vascular patches is tied to implantable cardiovascular prosthesis requirements and related performance expectations. In the United States, vascular grafts and patches are typically classified as Class II devices under 21 CFR 870.3450, with many products moving through 510(k) pathways aligned to FDA special controls, including the FDA guidance on Vascular Prostheses 510(k) Submissions. Manufacturers also follow FDA medical device reporting (MDR) expectations for post-market vigilance, which has increased attention to quality and complaint handling in the context of the broader 2024 recall sensitivity noted in the market materials.

Across regions, conformity to international standards remains a key market-access lever. ISO 7198:2016 sets requirements for vascular prostheses (including vascular patches), while ISO 10993-1 frames biological evaluation for implantable materials, shaping test plans for both synthetic and biologic constructs. Material safety expectations have also tightened, including the FDA's updated PFAS-related guidance released in August 2025, which affects material selection, supplier qualification, and documentation for polymer-based or coated patch platforms sold globally.

Value Chain Analysis

The vascular patch value chain begins with specialized inputs, notably bovine pericardium and other collagen-rich tissues for biologic patches, and ePTFE, polyester, and other biocompatible polymers for synthetic products. Tissue sourcing and traceability are critical for biologics, with bovine tissue sourcing from Australia cited for certain commercial patches, and the chain remains exposed to single-source risk and veterinary or zoonotic disruptions noted in the report context. Component and process inputs extend to fixation and coating chemistries (for example, collagen or gelatin impregnation) and validated sterilization (such as ethylene oxide), which shape shelf life, handling requirements, and clinical adoption in hospitals and ambulatory settings.

Manufacturing and commercialization are driven by established device companies and regional specialists, with quality systems aligned to FDA QSR (21 CFR Part 820) and ISO 13485, alongside vascular prosthesis guidance expectations. Distribution is concentrated around hospital procurement and group purchasing dynamics, while ambulatory surgical centers increasingly influence product selection through standardization needs and predictable workflow. Clinical evidence generation and regulatory filing are built into the chain for newer platforms; for example, Vivasure advanced its PerQseal program through a U.S. IDE pivotal study readout shared in October 2024, and Teijin moved SYNFOLIUM into commercial distribution in Japan in June 2024, showing how trial milestones and country-specific launches affect supply planning and channel expansion.

Competitive Landscape

The vascular patches market is moderately fragmented. LeMaitre Vascular, Baxter International, and W.L. Gore & Associates rely on legacy brands and vast sales networks, collectively anchoring procurement contracts with teaching hospitals. Boston Scientific’s USD 1.16 billion purchase of Silk Road Medical in 2024 signaled a push toward platform solutions spanning carotid intervention and patch closure, while Stryker’s acquisition of Inari Medical expanded its peripheral vascular footprint. These deals highlight the value of scale and multi-product portfolios in a procurement environment increasingly influenced by bundled payments.

Emerging tissue-engineering specialists like Humacyte challenge incumbents with fully biologic, off-the-shelf vessels that demonstrate high patency in trauma and dialysis access trials. Early adopters cite superior infection resistance and a smoother learning curve compared with autologous graft harvesting. Meanwhile, 3-D printing startups partner with academic centers to prototype patient-specific patches, shortening design-to-implant timelines and reinforcing the shift toward personalized surgery.

Competitive strategy is shifting from standalone product launches to evidence-based outcome packages. Leaders now fund real-world data registries, ensuring that cost-utility analyses favor their devices under value-based purchasing. Companies able to document reduced reoperation, lower infection, and faster discharge times will hold a pricing premium even in cost-pressured environments.

Vascular Patches Industry Leaders

Baxter International Inc

Terumo Corporation

Getinge AB

LeMaitre Vascular

W. L. Gore & Associates

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate where clinical workflows and evidence requirements are pushing differentiated patch performance beyond conventional materials. Tissue-engineered and ECM-based constructs can benefit from clearer regulatory pathways and adoption signals in developed markets, supported by the FDA's December 2024 approval of Humacyte's acellular tissue-engineered vessel as an example of scalable biologic manufacturing. The report's focus on outpatient-based reimbursement models also points to whitespace for patches and adjunct closure solutions that reduce operative time, simplify storage and handling, and support minimally invasive and hybrid procedures.

Large-bore access and complex aortic and structural-heart procedures create adjacent demand for patch-enabled repair and closure solutions. Haemonetics received FDA approval in March 2026 to expand labeling for its VASCADE MVP XL venous vascular closure system to accommodate larger sheath sizes, reflecting the procedural shift toward larger-bore venous access in electrophysiology and structural interventions and supporting procurement at sites that are standardizing peri-access tools. Pipeline activity further supports specialization: Vivasure submitted a PMA to the FDA in June 2025 for PerQseal Elite (arterial) and obtained expanded CE-marked venous indications in Europe, while clinical-trial activity in China for LeMaitre's XenoSure biological patch, with primary completion in November 2025, highlights an access pathway for premium biologic patches in price-sensitive markets where local evidence and approvals are established.

Recent Industry Developments

- April 2026: Getinge reported that its Intergard Synergy antimicrobial vascular graft achieved EU MDR approval. The milestone strengthens portfolio continuity in Europe under tighter MDR requirements and supports hospital purchasing that prioritizes antimicrobial performance and compliant labeling for implantable vascular products.

- May 2025: Terumo announced commercial availability of the ROADSAVER Carotid Stent System in the United States. Broader carotid intervention adoption supports procedure ecosystem growth around carotid endarterectomy and carotid repair pathways where patch use remains standard in many surgical protocols.

- December 2024: Terumo Interventional Systems launched the 200 cm R2P NaviCross peripheral support catheter in the United States. Longer-length peripheral access tools expand the addressable set of complex peripheral cases and reinforce demand for complementary vascular repair consumables used in open and hybrid workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of vascular patches used in open and hybrid vascular surgeries to repair, reinforce, or widen a blood vessel, typically during procedures like endarterectomy and patch angioplasty. The sizing includes biologic and synthetic patch materials sold for vascular use across major geographies.

Scope exclusions: We exclude vascular grafts, stent grafts, sutures, and non-vascular soft tissue patches that are not indicated for blood vessel repair.

Segmentation Overview

- By Material

- Biologic Vascular Patches

- Synthetic Vascular Patches

- By Application

- Carotid Endarterectomy

- Aortic Aneurysm Repair

- Profundaplasty and Femoral Patch Angioplasty

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a simple fact base on procedure volumes, care settings, and pricing direction, then mapping which patch materials are commonly used by indication. Public and official sources, such as the US FDA device databases, the US Centers for Medicare and Medicaid Services (procedure and reimbursement references), the CDC for cardiovascular burden context, and OECD health statistics, help us anchor demand signals to actual healthcare activity.

We also review peer reviewed clinical journals for patch utilization patterns in carotid endarterectomy and femoral patch angioplasty, and then cross-check mix shifts across biologic and synthetic patches using trade association publications and hospital procurement notes. Company filings, investor presentations, and reputable press releases are used to confirm product availability, regional exposure, and broad revenue direction. Select paid databases are used for company financials and intelligence plus patent tracking to confirm product pipelines and material trends. The sources listed here are illustrative and not exhaustive, since we reviewed many other references to clarify inputs and validate outputs.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that are hard to see in public data, like average patches used per procedure, typical ASP ranges by material, and how outpatient migration changes product mix. We interview and survey a blend of clinicians, hospital procurement contacts, distributors, and manufacturing-side experts across APAC, EMEA, and the Americas, then reconcile their inputs against the desk model until the drivers align.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 43% |

| Mid tier: 54% | Functional/Unit leaders: 39% | EMEA: 30% |

| Smaller Players: 18% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

The core sizing uses a top-down approach where procedure and treated-patient signals are reconstructed into an addressable demand pool for vascular patch use, then converted into value using typical patches-per-case and pricing ranges by material type. To keep the totals realistic, we corroborate the outputs with selective bottom-up checks like sampled supplier roll-ups, channel feedback on volume direction, and a quick ASP times volume approximation for high-usage procedures.

Key inputs in this market include carotid endarterectomy volumes, femoral and profunda patch angioplasty activity, the share of cases using patch closure versus primary closure, biologic versus synthetic material mix, and ASP progression by hospital versus ambulatory settings. Where country-level procedure reporting is incomplete, gaps are handled using proxy indicators such as vascular surgery capacity, population age bands, and published disease prevalence, and then validating the implied utilization with expert feedback.

For forecasting, we use scenario analysis supported by a light multivariate regression on procedure growth and care setting mix, followed by analyst adjustments that reflect material innovation and adoption pacing. After the main drivers are agreed during calls, the final forecast path is checked for smooth year-to-year movement so unusual jumps are flagged and reworked.

Data Validation & Update Cycle

Before sign-off, our estimates are triangulated across three layers, the procedure-led demand build, pricing logic, and independent checks such as reported product revenue direction and clinical utilization signals. Outliers are reviewed stepwise, first at the country level and then at the regional roll-up level. If a variance cannot be explained clearly, we re-contact interviewees to confirm whether it reflects a true market change or a modeling artifact.

Each report is refreshed annually, and interim updates are done when material events occur, such as major regulatory changes, a sharp change in procedure volumes, or a significant pricing shift. Before delivery, an analyst performs a fresh pass on key inputs and the latest public updates so clients receive a current view rather than an older snapshot.

Mordor Intelligence's Vascular Patch Market Size Versus Other Published Estimates

Published market values for vascular patches can look far apart because sources do not always count the same products, they may anchor the model to different procedure pools, and they refresh pricing and mix assumptions at different times. Differences also show up when one estimate leans more on historical revenues and another leans more on expected adoption of newer materials.

Soft tissue repair patches that are not used for blood vessel repair sit outside Mordor Intelligence's scope, which is one practical reason our market value will not line up with broader patch categories that some publishers blend into a single number. Other gaps typically come from whether outpatient migration is modeled as a mix shift with different ASPs, whether composite patches are grouped with biologic or synthetic, and whether currency conversion is done using an average year rate or a point-in-time rate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 664.51 M (2026) | |

| Regional Consultancy A | USD 452.90 M (2024) | Uses an earlier base year and a narrower current-year definition that can understate value when later-year procedure volumes and ASP updates are not carried through, and the scope language is less clear on adjacent patch categories. |

| Global Consultancy B | USD 624.14 M (2023) | Anchors the series on a prior-year starting value and a shorter horizon, which can shift totals when outpatient mix, material mix, and inflation-linked ASP progression are not updated consistently across regions. |

In simple terms, the spread mainly reflects different year anchors and what each publisher counts as a vascular patch versus a broader patch family. When the scope stays tight to vascular repair procedures and the model ties back to procedure activity plus realistic pricing bands, the final market number is easier to follow and repeat.

Key Questions Answered in the Report

What is the current size of the vascular patches market?

The vascular patches market is valued at USD 664.51 million in 2026 and is projected to reach USD 985.91 million by 2031.

Which material category leads the vascular patches market?

Biologic patches hold the lead with 56.58% market share in 2025, favored for superior integration and lower infection risk.

Which application segment is expanding fastest?

Aortic aneurysm repair is the fastest-growing application, advancing at a 9.24% CAGR between 2026 and 2031.

Why are ambulatory surgical centers important for future growth?

ASC volumes are growing at 8.61% CAGR because outpatient settings lower costs and align with value-based reimbursement models.

Which region offers the highest growth potential?

Asia-Pacific delivers the steepest growth curve at 9.62% CAGR thanks to rising cardiovascular disease incidence and expanding surgical capacity.

How are manufacturers differentiating in a competitive market?

Companies increasingly invest in clinical evidence and technology platforms such as tissue-engineered or 3-D printed patches that improve outcomes and justify premium pricing.

Page last updated on: