Vascular Guidewires Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

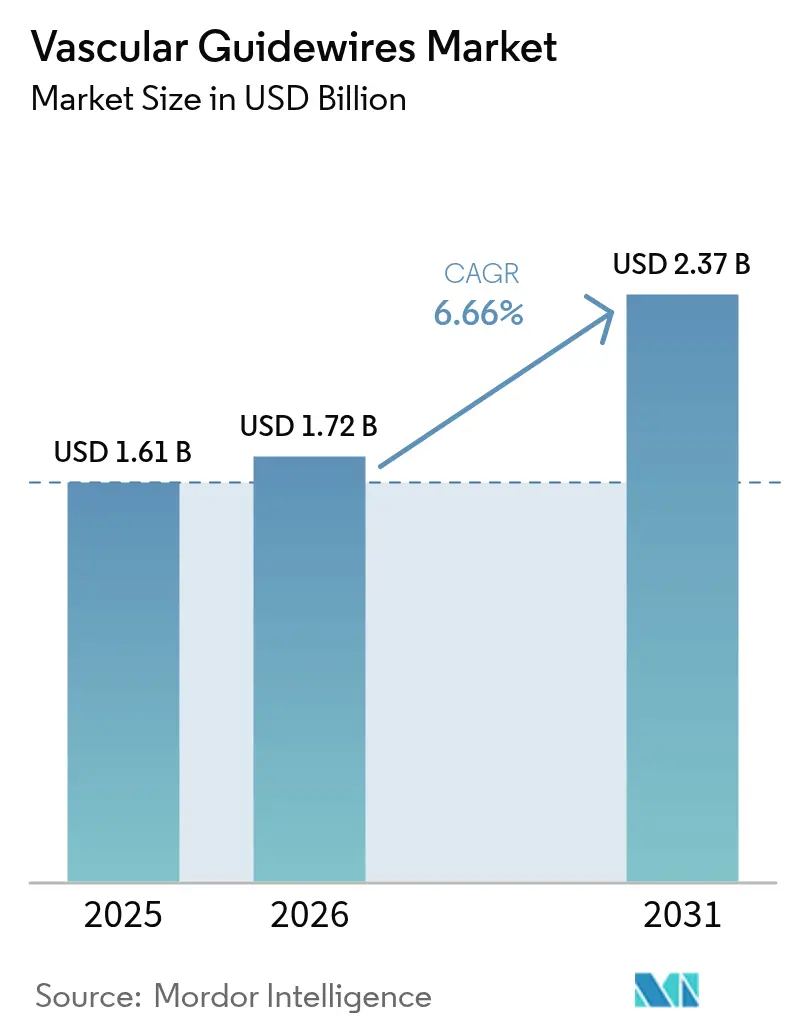

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 2.37 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

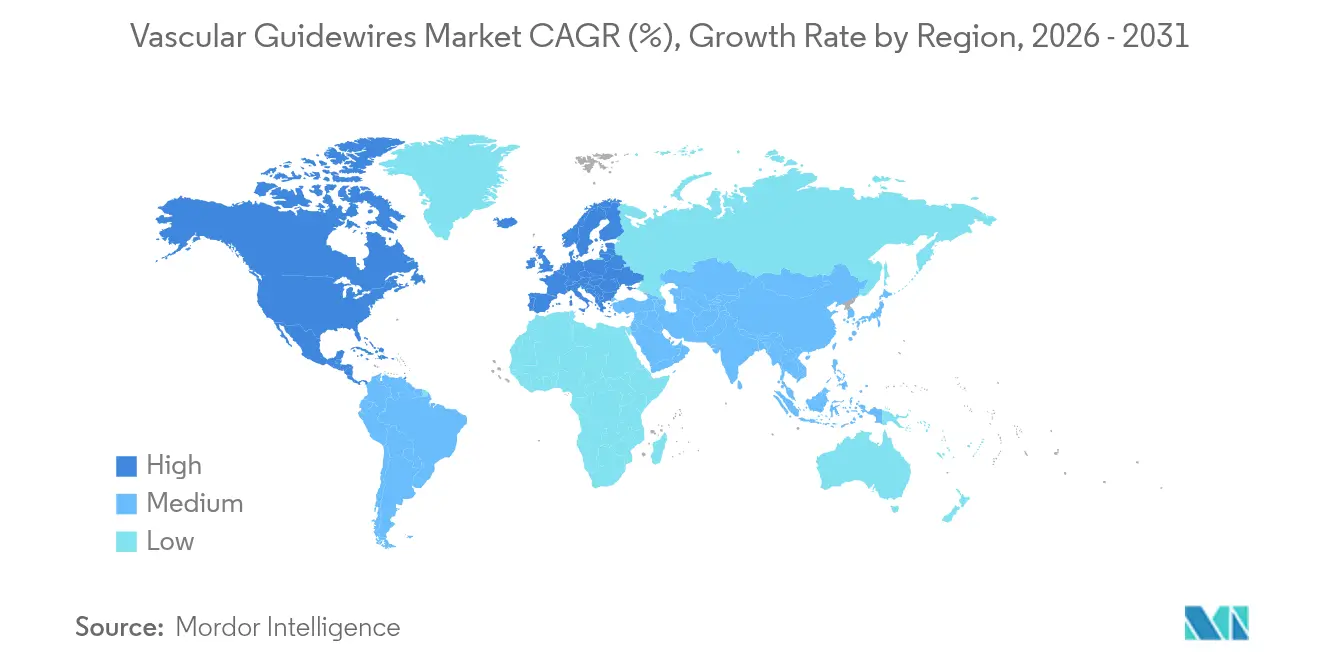

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vascular Guidewires Market Analysis by Mordor Intelligence

The vascular guidewires market size is expected to grow from USD 1.61 billion in 2025 to USD 1.72 billion in 2026 and is forecast to reach USD 2.37 billion by 2031 at 6.66% CAGR over 2026-2031. Rising cardiovascular disease prevalence, the global pivot toward minimally invasive interventions, and continuous improvements in steerability and torque response are sustaining demand. Device makers are also benefiting from expanding catheterization lab capacity, broader reimbursement for outpatient vascular procedures, and the commercialization of robotic-assisted endovascular suites. Supply-chain localization of medical-grade nitinol and investments in PFAS-free coatings illustrate how manufacturers are de-risking production while aiming for long-term sustainability. Regionally, North America remains the leading revenue contributor, whereas Asia-Pacific shows the most rapid growth owing to healthcare infrastructure development and higher procedure volumes.

Key Report Takeaways

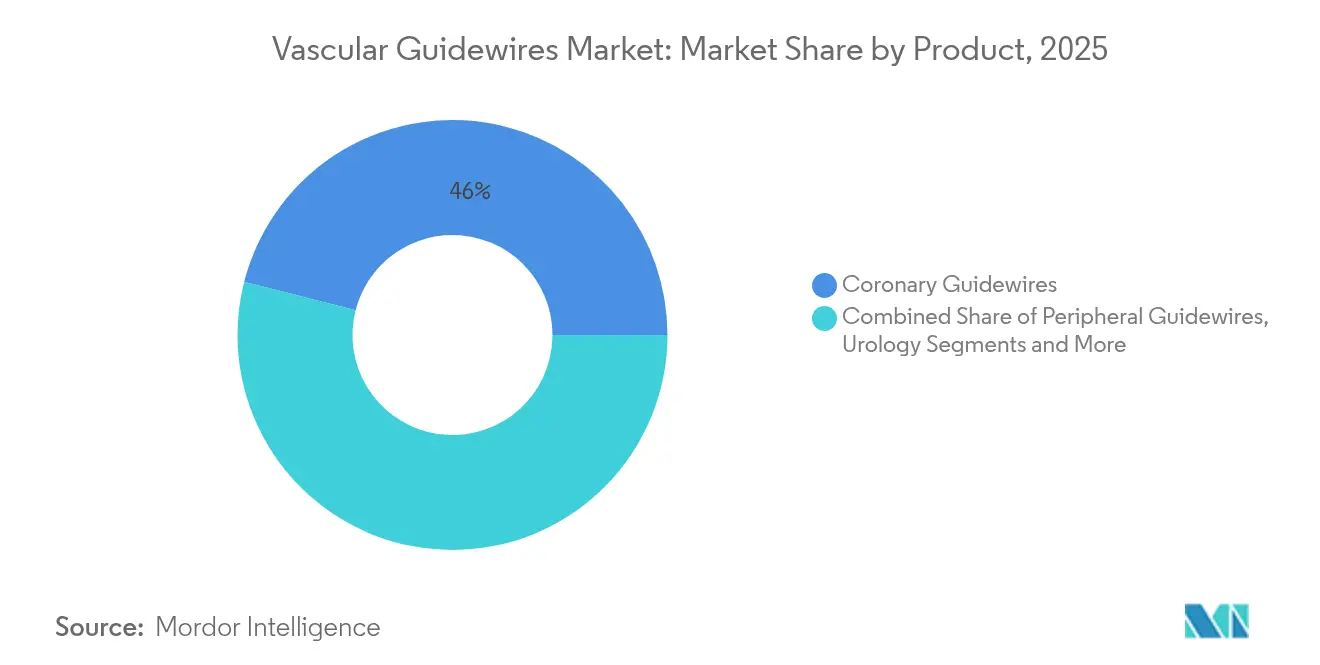

- By product category, coronary guidewires held 46.02% vascular guidewires market share in 2025, while neurovascular guidewires are forecast to expand at an 8.14% CAGR through 2031.

- By coating, coated guidewires accounted for 62.48% of the vascular guidewires market size in 2025; non-coated guidewires are advancing at a 7.69% CAGR to 2031.

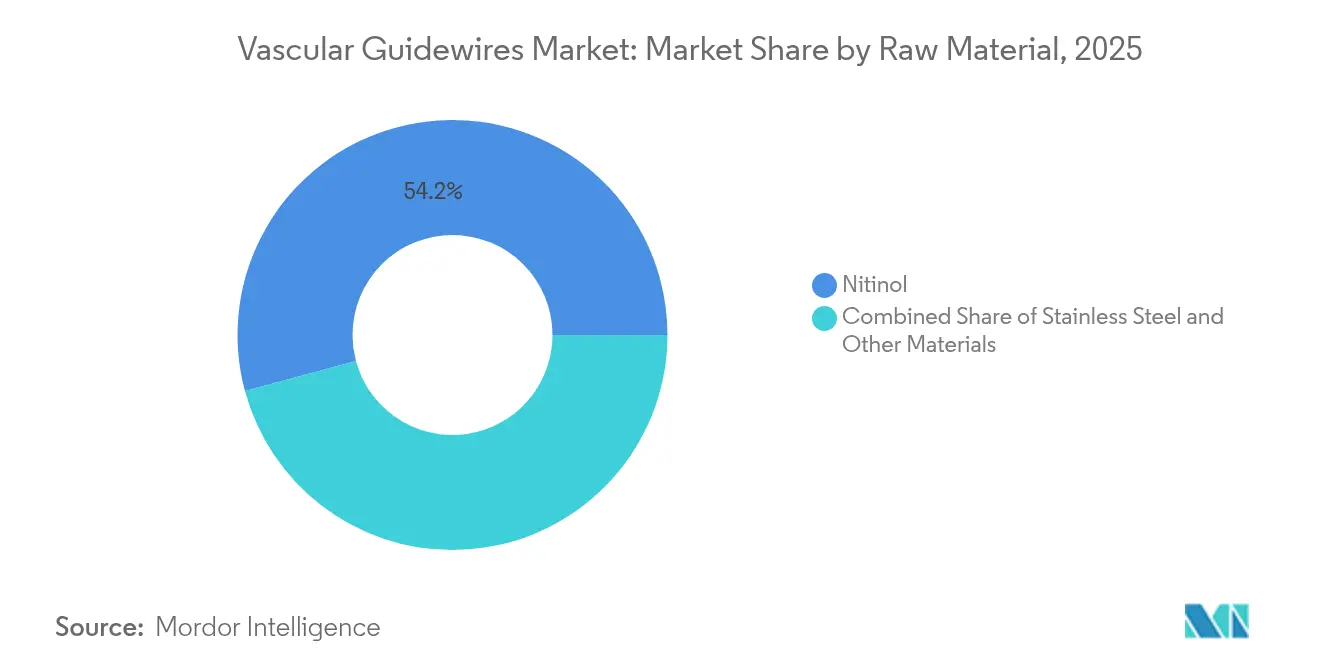

- By raw material, nitinol led with 54.20% share of the vascular guidewires market size in 2025, whereas stainless steel is projected to grow at a 7.46% CAGR during 2026-2031.

- By end user, hospitals commanded 69.52% of vascular guidewires market share in 2025, yet ambulatory surgical centers are set to record the highest CAGR of 8.17% up to 2031.

- By geography, North America contributed 44.88% revenue in 2025, while Asia-Pacific is set to expand at an 8.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vascular Guidewires Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cardiovascular disease burden | +1.8% | Global, notably North America & Europe | Long term (≥ 4 years) |

| Growing preference for minimally invasive surgeries | +1.5% | Global, led by North America & Asia-Pacific | Medium term (2-4 years) |

| Technological breakthroughs in steerable & torque-enhanced wires | +1.2% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Ageing population expanding interventional case-load | +1.0% | Global, strongest in developed markets | Long term (≥ 4 years) |

| Hospital adoption of robotic-assisted endovascular suites | +0.8% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Supply-chain localisation of medical-grade nitinol | +0.5% | North America & Europe with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Cardiovascular Disease Burden

Global hypertension prevalence is forecast to climb from 51.2% in 2020 to 61.0% by 2050, while diabetes rises from 16.3% to 26.8%. These epidemiological shifts elevate procedure volumes for coronary, peripheral, and neurovascular interventions, positioning guidewires as essential access tools. Stroke-related costs alone are anticipated to increase 535% to USD 423 billion by 2050, underscoring long-term demand for neurovascular devices. Hospital systems are expanding cath-lab capacity and procuring torque-responsive wires that address complex anatomy in older patients. Preventive interventions are also gaining traction, enlarging the overall addressable vascular guidewires market [1]American Heart Association, “Cardiovascular Health & Disease Statistics—2025 Update,” heart.org.

Growing Preference for Minimally Invasive Surgeries

Ambulatory surgical centers (ASCs) are expected to handle more than half of US outpatient surgeries by 2028, representing a USD 33 billion opportunity at a 6.9% CAGR. Only 1.8% of percutaneous coronary interventions currently occur in ASCs, leaving headroom for growth[2]Society for Cardiovascular Angiography and Interventions, “Percutaneous Coronary Intervention in the Outpatient Setting,” scai.org. Cost savings, faster recovery, and comparable safety records are compelling payers and providers to favor outpatient endovascular care, thereby increasing demand for versatile guidewires that perform reliably across procedural settings.

Technological Breakthroughs in Steerable & Torque-Enhanced Wires

Steerable devices such as the SideEye catheter have reduced target vessel cannulation time to 199 seconds versus 703 seconds for conventional options. Innovations combining nitinol cores with variable cross-section shafts deliver high torque without sacrificing flexibility. Hybrid designs, exemplified by Terumo’s Runthrough wire, are challenging incumbents by lowering the need for buddy wires in complex lesions.

Ageing Population Expanding Interventional Case-Load

Patients aged 80 years and above register the highest rehospitalization rates for heart failure within 36 months of coronary angiography. Frailty-informed procedural planning is shifting device selection toward wires offering sensitive tactile feedback and improved pushability. Specialty training programs and guidewire refinements aim to mitigate the anatomical challenges posed by calcified and tortuous vessels prevalent in elderly cohorts.

Hospital Adoption of Robotic-Assisted Endovascular Suites

The CorPath GRX system achieved 94% completion without unplanned manual conversion during cerebral aneurysm embolizations, highlighting the precision advantages of robotic navigation. Hospitals adopting robotics seek lower radiation exposure and enhanced workflow efficiency, creating demand for guidewires optimized for robotic interfaces.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of product recalls & FDA warning letters | -1.2% | Global, most severe in North America | Short term (≤ 2 years) |

| Price erosion amid commoditization in mature markets | -0.8% | North America & Europe | Medium term (2-4 years) |

| Global nitinol feedstock shortages | -0.6% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| PFAS-linked regulation of hydrophilic coatings | -0.4% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Product Recalls & FDA Warning Letters

Class I recalls in 2024-2025, including coating separation events, have affected leading manufacturers and hundreds of thousands of devices. The heightened regulatory environment is prompting providers to diversify suppliers, while manufacturers strengthen quality controls to preserve market confidence.

Price Erosion Amid Commoditization in Mature Markets

Group purchasing organizations use consolidated buying power to negotiate lower prices, pressuring margins in standard guidewire categories. New entrants from Asia-Pacific offer cost-competitive substitutes, amplifying price competition in North America and Europe.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Expanding Clinical Breadth Drives Differentiation

Coronary guidewires held a 46.02% share of the vascular guidewires market in 2025 owing to high global PCI volumes. Neurovascular guidewires, though smaller in revenue, are forecast for an 8.14% CAGR, reflecting rising stroke awareness and improvements in distal access devices. Advanced hybrid wires are influencing clinician preferences by combining soft tips with proximal stiffness, reducing reliance on multiple wire exchanges. Artificial intelligence integration is under exploration, pointing to future smart guidewires capable of real-time vessel mapping.

The peripheral segment continues stable growth fuelled by increasing peripheral artery disease incidence. Urology guidewires benefit from the broader shift toward minimally invasive stone management, although they remain niche compared with cardiovascular applications.

By Coating: Hydrophilic Performance Meets Regulatory Headwinds

Coated guidewires represented 62.48% of vascular guidewires market size in 2025 as hydrophilic layers improve lubricity in tortuous anatomy. PFAS-related regulatory scrutiny is accelerating R&D into alternative chemistries, prompting manufacturers to file new patents for fluorine-free or biodegradable coatings. Non-coated guidewires are expanding at a 7.69% CAGR as operators value direct tactile feedback in certain coronary and peripheral cases, and as price-sensitive markets re-evaluate premium coating benefits.

By Raw Material: Nitinol Superelasticity Under Supply Constraints

Nitinol accounted for 54.20% share because its shape memory characteristics support complex vessel navigation. Recent feedstock shortages and price increases are influencing sourcing strategies, including localized melt facilities near major device hubs. Stainless steel remains appealing for its cost profile and reliable torque, posting a 7.46% CAGR. Polymer-metal hybrids and PEEK cores are gaining attention for pediatric and neurovascular specialties where ultra-low profiles are critical.

By End User: Outpatient Shift Reshapes Procurement

Hospitals absorbed 69.52% of 2025 demand due to their ability to manage complex emergencies. Yet the vascular guidewires market is witnessing rapid ASC expansion at 8.17% CAGR, driven by favorable reimbursement and demonstrated safety equivalence in PCIs. Specialty clinics and dedicated cath labs fill a growing niche for high-volume routine interventions, emphasizing standardization and cost control.

Geography Analysis

North America retained a 44.88% revenue share in 2025. Robust reimbursement, early adoption of robotic platforms, and broad clinical training networks sustain demand. However, stricter FDA post-market surveillance is lengthening approval cycles and raising compliance costs. Value-based care contracts increasingly require outcome evidence, pressuring suppliers to link device performance with total cost of care.

Asia-Pacific is projected for an 8.47% CAGR through 2031. China’s device market, targeted to reach USD 55.67 billion by 2029, benefits from policies such as Made in China 2025 that foster domestic production. Indonesia reached USD 2.3 billion in 2024 and continues to leverage TKDN rules that mandate local content. India’s new marketing conduct codes are improving transparency, though they require short-term adjustments for multinational suppliers. Rising procedure volumes, expanding insurance coverage, and government investments in cardiovascular care position the region as the key driver for incremental vascular guidewires market revenue.

Europe exhibits steady demand amid rigorous regulatory frameworks. Harmonized standards updated in 2024 introduce clearer pathways for CE marking, albeit with higher documentation requirements . The continent’s aging demographic keeps procedure numbers high, while cost-effectiveness evaluations encourage adoption of guidewires that balance performance with economic value. Brexit-induced divergence still complicates UK-EU supply logistics but is gradually being mitigated through mutual recognition agreements.

Middle East & Africa and South America show emerging potential. Gulf Cooperation Council countries invest in cardiovascular centers of excellence, whereas Brazil and Argentina expand cath-lab networks despite reimbursement hurdles. Market access relies heavily on distributor partnerships and compliance with evolving local regulations.

Competitive Landscape

The vascular guidewires market displays moderate consolidation. Boston Scientific’s USD 1.26 billion takeover of Silk Road Medical in 2024 strengthened its carotid portfolio. Teleflex bolstered its presence by acquiring BIOTRONIK’s vascular intervention unit for EUR 760 million, gaining entry to a USD 10 billion addressable space.

Alongside acquisitions, leading firms intensify R&D on steerable and robotic-compatible wires. Patent filings highlight variable cross-section shafts and switchable stiffness zones enabling single-wire procedures across lesion morphologies.

Emerging disruptors exploit additive manufacturing to tailor microstructure geometry for improved torque response. Start-ups specializing in pediatric and neurovascular niches secure FDA clearances, as seen with the Minima Stent System designed for neonates weighing at least 1.5 kg. Established brands defend share by scaling integrated solutions—bundling guidewires, catheters, and robotic platforms to offer end-to-end procedural ecosystems. Quality track records and supply resilience are increasingly decisive as providers scrutinize vendors following recent recalls.

Vascular Guidewires Industry Leaders

Boston Scientific Corporation

Stryker Corporation

Terumo Medical Corporation

Abbott Laboratories

B. Braun Melsungen AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Philips obtained FDA clearance for the enhanced LumiGuide guidewire and treated its 1000th patient using 3D device guidance technology.

- March 2024: Baylis Medical Technologies secured 510(k) clearance and launched the PowerWire Pro RF Guidewire in the United States.

- April 2023: Guangdong Hicicare Science and Zylox-Tonbridge Medical Technology formed a strategic partnership to co-brand vascular guidewire products in China.

Global Vascular Guidewires Market Report Scope

As per the scope of the report, vascular guidewires are found to be thin tubes made of medical grade, which are inserted in the body, especially in the veins, to perform surgeries or treat chronic diseases. Basically, these tubes or medical devices allow the administration of gases, access to surgical instruments, and drainage, along with performing various tasks depending on the patient's condition. The Vascular Guidewires Market is Segmented by Product (Peripheral Guidewires, Coronary Guidewires, Urology Guidewires and Neurovascular Guidewires), Coating (Coated and Non-coated), Raw Material (Nitinol, Stainless Steel and Other Raw Materials), End User (Hospitals, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Peripheral Guidewires |

| Coronary Guidewires |

| Urology Guidewires |

| Neurovascular Guidewires |

| Coated |

| Non-Coated |

| Nitinol |

| Stainless Steel |

| Other Materials (PEEK, Polymer Hybrids) |

| Hospitals |

| Ambulatory Surgical Centres |

| Specialty Clinics & Cath Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Peripheral Guidewires | |

| Coronary Guidewires | ||

| Urology Guidewires | ||

| Neurovascular Guidewires | ||

| By Coating | Coated | |

| Non-Coated | ||

| By Raw Material | Nitinol | |

| Stainless Steel | ||

| Other Materials (PEEK, Polymer Hybrids) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres | ||

| Specialty Clinics & Cath Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Vascular Guidewires Market size?

The vascular guidewires market size stands at USD 1.72 billion in 2026 and is forecast to reach USD 2.37 billion by 2031 with a 6.66% CAGR.

Who are the key players in Vascular Guidewires Market?

Boston Scientific Corporation, Stryker Corporation, Terumo Medical Corporation, Abbott Laboratories and B. Braun Melsungen AG are the major companies operating in the Vascular Guidewires Market.

Which segment is growing fastest within the vascular guidewires market?

Neurovascular guidewires post the highest growth, expanding at an 8.14% CAGR through 2031 due to rising stroke interventions and technology advances.

Which region has the biggest share in Vascular Guidewires Market?

North America holds the largest regional share at 44.88% thanks to advanced infrastructure and broad reimbursement for vascular interventions.

Page last updated on: