Vaginal Slings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

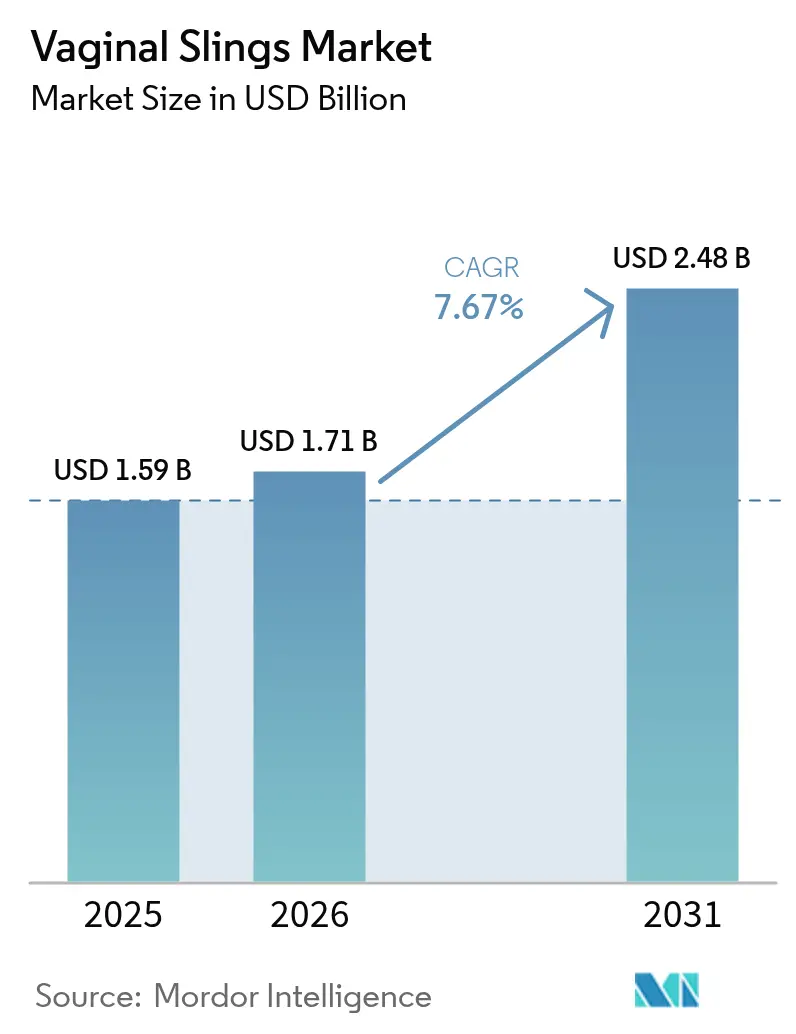

| Market Size (2026) | USD 1.71 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 7.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

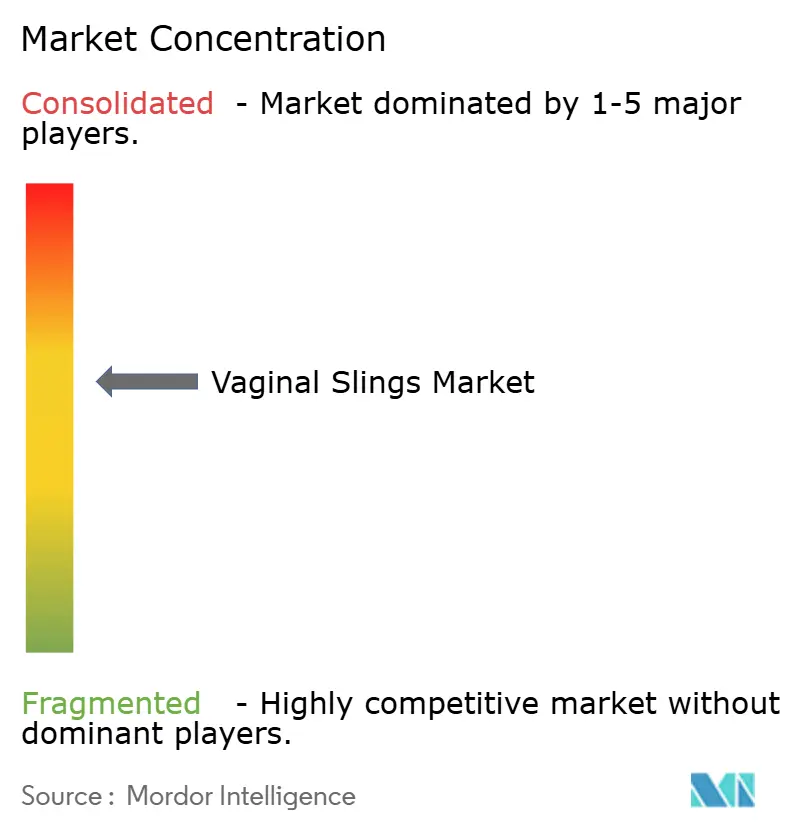

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vaginal Slings Market Analysis by Mordor Intelligence

The Vaginal Slings Market size was valued at USD 1.59 billion in 2025 and estimated to grow from USD 1.71 billion in 2026 to reach USD 2.48 billion by 2031, at a CAGR of 7.67% during the forecast period (2026-2031).

The upward trajectory reflects high acceptance of minimally-invasive mid-urethral sling techniques, strong clinical evidence of long-term efficacy and reduced complication rates, and steady growth in the addressable patient pool as global populations age. Product design improvements especially lighter meshes made of polyvinylidene fluoride (PVDF) further strengthen surgeon confidence by lowering erosion and pain risks relative to older polypropylene implants. Demand is boosted by favorable reimbursement in North America and the European Union; new Medicare procedure codes and clearer device labeling guidelines speed provider adoption while protecting patients. Asia-Pacific registers the fastest procedural growth because of expanding ambulatory surgery centers (ASCs), growth in medical tourism, and public health campaigns that heighten awareness of pelvic floor disorders. Competitive intensity remains moderate as leading suppliers consolidate adjacent technologies exemplified by Boston Scientific’s USD 3.7 billion purchase of Axonics in 2024 to capture a broader urology franchise bostonscientific.com.

Key Report Takeaways

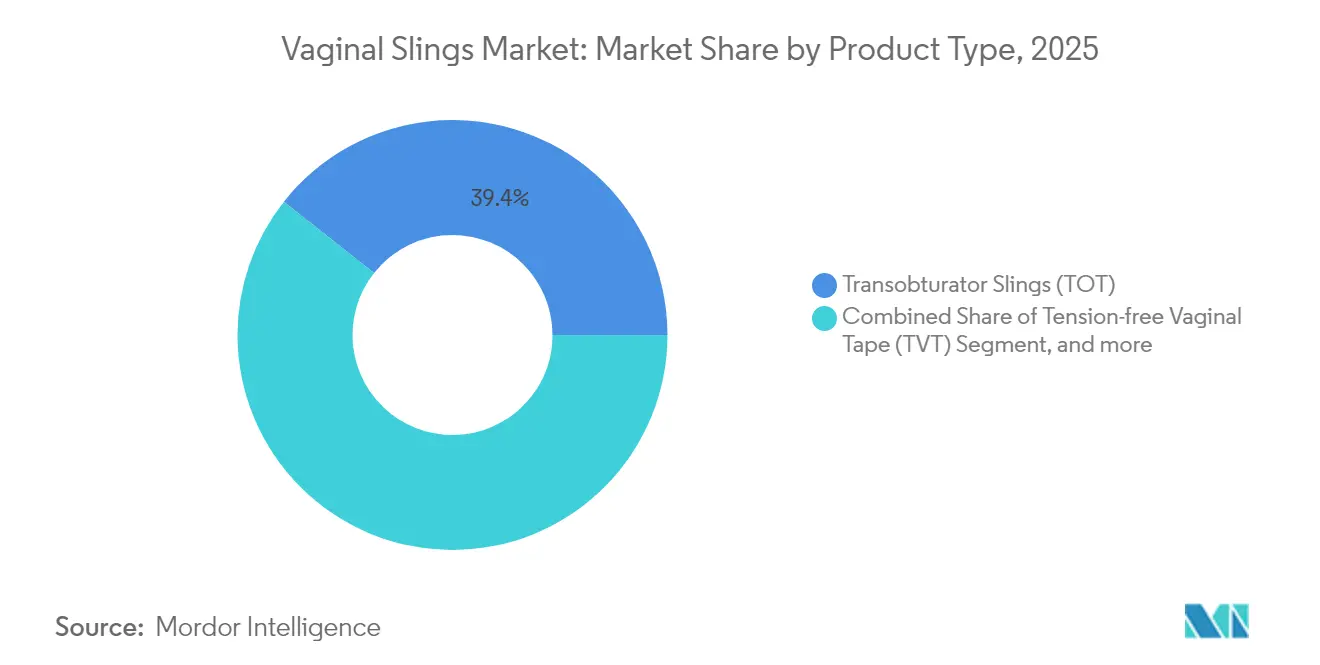

- By product type, transobturator slings led with 39.35% of the vaginal slings market share in 2025; mini / single-incision systems post the fastest 11.59% CAGR to 2031.

- By material, polypropylene maintained 51.78% share of the vaginal slings market size in 2025, while PVDF meshes are set to grow at a 12.67% CAGR through 2031.

- By incontinence type, stress urinary incontinence accounted for 72.10% share of the vaginal slings market size in 2025 and is expanding at an 8.39% CAGR.

- By end user, hospitals commanded 57.20% of revenue in 2025; specialty clinics register the quickest 9.61% CAGR to 2031.

- By geography, North America captured 37.65% revenue in 2025, whereas Asia-Pacific is projected to climb at an 10.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vaginal Slings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Stress Urinary Incontinence | +2.1% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Increasing Adoption of Minimally Invasive Mid-Urethral Sling Procedures | +1.8% | Global, led by developed markets | Medium term (2-4 years) |

| Supportive Reimbursement Frameworks in Key Healthcare Markets | +1.4% | North America & EU primarily | Short term (≤ 2 years) |

| Ongoing Innovations in Lightweight Meshes and PVDF Materials | +1.2% | Global, with early adoption in North America | Medium term (2-4 years) |

| Integration of AI Tools for Optimized Patient Selection | +0.8% | North America & EU initially | Long term (≥ 4 years) |

| Rising Medical Tourism in Developing Countries | +0.5% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Stress Urinary Incontinence

Stress urinary incontinence incidence is rising in lockstep with population aging and higher metabolic disease prevalence. Projections indicate that US women with pelvic floor disorders will grow from 28.1 million in 2010 to 43.8 million by 2050, enlarging the core patient pool. Cardiometabolic comorbidities such as type 2 diabetes and high cholesterol heighten symptom severity, encouraging earlier clinical referrals. The RISE FOR HEALTH study reports that 79% of US women experience at least one lower urinary tract symptom, yet only 7.1% receive care, underscoring vast unmet need.[1]Journal of Urology Editorial Board, “RISE FOR HEALTH Study on Lower Urinary Tract Symptoms,” auajournals.org Menopause compounds risk, meaning baby-boomer cohorts will keep the vaginal slings market on a long-run expansion path. Health-system screening initiatives are expected to surface a larger share of untreated cases.

Increasing Adoption of Minimally Invasive Mid-Urethral Sling Procedures

Mid-urethral slings deliver 80-90% long-term success with lower morbidity than open surgery, making them the gold standard treatment. FDA literature reviews confirm that mini-slings maintain equivalent effectiveness and safety to traditional approaches over 36 months, validating surgeon confidence.[2]U.S. Food and Drug Administration, “Mini-Slings for Stress Urinary Incontinence: Systematic Literature Review 2013-2023,” fda.govMore than 60% of urology procedures now take place in outpatient facilities, where shorter stays and local anesthesia reduce costs for payers and patients. Boston Scientific’s blue-tinted mesh improves intra-operative visualization, trimming operating time, and sharpening placement accuracy. Single-incision devices achieve 88% patient satisfaction and 81% subjective continence on follow-up, accelerating share gains within the vaginal slings market.

Supportive Reimbursement Frameworks in Key Healthcare Markets

In October 2024, the US Centers for Medicare & Medicaid Services introduced new HCPCS codes for pelvic floor devices, signaling a willingness to cover broader pelvic health solutions.[3]CGS Administrators, “2024 HCPCS Code Updates for Pelvic Floor Devices,” cgsmedicare.com Medicare already reimburses sling placement under CPT 57288, supporting steady procedural volumes in hospital and ASC settings. Health-economic modeling in Colombia showed mid-urethral tapes cost USD 2,417 per additional improved case versus open fascia slings, reinforcing payer value arguments. Private insurers now cover digital therapeutic systems such as Leva, saving USD 820 per patient across 24 months relative to current standard care. European funding bodies likewise recognize that early surgical correction curbs downstream spend on pads, infections, and productivity losses.

Ongoing Innovations in Lightweight Meshes and PVDF Materials

PVDF meshes deliver 60% higher ultimate tensile strength and 35% better pull-out force than polypropylene while exhibiting negligible degradation across 24 months in vivo. Lower bending stiffness and reduced inflammatory response translate into fewer erosions and pain complaints, lessening litigation exposure. Comparative sacrocolpopexy trials in Europe register lower erosion and dyspareunia rates for PVDF implants, prompting surgeons to shift preference toward bioneutral materials. Researchers are fabricating 3D non-woven PVDF scaffolds that support stromal-cell growth, opening future regenerative pathways. Together these advances expand surgeon choice and spur premium-priced product tiers within the vaginal slings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ongoing Legal Scrutiny Over Mesh Implants | -1.6% | Global, most severe in North America & EU | Short term (≤ 2 years) |

| Cultural and Social Barriers Contributing to Delayed Diagnosis | -1.2% | APAC core, spill-over to MEA & Latin America | Long term (≥ 4 years) |

| Growing Preference for Non-Surgical Options Such as Bulking Agents and Energy-Based Therapies | -0.9% | Global, led by developed markets | Medium term (2-4 years) |

| Environmental and Supply Chain Constraints Impacting Availability of Polypropylene Materials | -0.7% | Global, with highest impact in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ongoing Legal Scrutiny Over Mesh Implants

Courts continue to levy sizable penalties against manufacturers for past marketing practices. Johnson & Johnson’s Ethicon unit was fined USD 302 million in 2024, reinforcing patient concerns about mesh safety and slowing procedure growth in litigious regions. England’s first group settlement, covering 140 women set a precedent that may increase liability across Europe. The FDA reclassified transvaginal mesh for prolapse repair as Class III, demanding stringent pre-market approvals and expensive post-market surveillance. About 5-10% of recipients may need revision surgery for mesh-related complications, adding weight to negative publicity. These dynamics dampen near-term uptake and push companies to accelerate next-generation materials.

Growing Preference for Non-Surgical Options Such as Bulking Agents and Energy-Based Therapies

Patients wary of permanent implants increasingly opt for conservative treatments that promise symptom relief without foreign bodies. High-intensity focused electromagnetic (HIFEM) therapy cuts pad test volumes from 4.2 g to 0.6 g after six sessions, delivering measurable quality-of-life gains. Polyacrylamide hydrogel injections show one-year continence rates comparable to surgery yet can be performed in an office visit, appealing to frail or surgery-averse individuals. Emerging laser modalities stimulate collagen remodeling with minimal downtime, broadening the therapeutic toolbox. AI-guided pelvic floor training helps tailor home-based regimens that may delay or negate surgical need, eroding a slice of the vaginal slings market. While late-term granuloma risk exists, the immediate safety perception keeps momentum behind non-invasive care.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-Incision Innovation Drives Growth

Transobturator systems delivered 39.35% revenue in 2025, cementing their role as the most implanted solution within the vaginal slings market. Clinical familiarity, low bladder perforation rates, and robust long-term data ensure steady procedural volumes in both hospital and ASC settings. Surgeons favor these devices for reproducible outcomes across varied anatomies, sustaining their hold on the vaginal slings market. Mini / single-incision slings, although newer, expand at an 11.59% CAGR as users gravitate toward faster placement and reduced dissection planes. Studies show Solyx achieving 100% objective cure at 3 months versus 91.1% for MiniArc, yet both platforms offer high subjective satisfaction. As ergonomic delivery tools emerge, single-incision systems gain broader acceptance in low-resource settings that value minimal OR time.

Objective performance also elevates tension-free vaginal tape methods, whose 71-97% 10-year subjective cure rates maintain surgeon loyalty. Meanwhile, adjustable autologous slings appeal to patients avoiding synthetics; modified laparoscopic sacral colpopexy with polyester sutures offers mesh-free durability at lower material cost. Personalized continence therapy trials underscore clinical appetite for patient-specific adjustability, suggesting gradual diversification of the product mix.

By Material Type: PVDF Emergence Reshapes Preferences

Polypropylene held 51.78% share of the vaginal slings market size in 2025 due to decades of surgeon experience and lower unit price. However, PVDF meshes lead growth with a 12.67% CAGR as superior biocompatibility and stability win clinical endorsements. Bench testing confirms larger elastic recovery and lower creep deformation than polypropylene, translating to lower erosion in vivo. Six-country registry data show fewer chronic pain complaints in PVDF recipients, accelerating conversion in Europe and North America. Absorbable and bioresorbable scaffolds carve a niche where permanent implants are culturally sensitive; poly-4-hydroxybutyrate constructs gradually resorb after 18 months while sustaining pelvic floor support, although high production costs limit immediate scale.

Material innovation attracts venture funding for 3D-printed lattice meshes tailored to individual anatomy, hinting at mass customization over the forecast horizon. As litigation risk remains tied to polymer degradation, suppliers that transition portfolios toward PVDF and bioresorbable will capture premium segments of the vaginal slings market.

By Incontinence Type: Stress Dominance with Mixed Growth

Stress urinary incontinence generated 72.10% of 2025 revenues and continues to post the fastest 8.39% CAGR. The rise in metabolic syndrome fuels incidence: lipid accumulation elevates stress incontinence odds by 63% in post-menopausal women. Early screening of cardiometabolic indices thus enlarges candidacy for surgical repair. Environmental exposure to cadmium, lead, and mercury further correlates with symptom onset, especially in younger cohorts, adding urgency to address risk factors. Clinical trials comparing mid-urethral slings with onabotulinumtoxinA injections in mixed incontinence aim to define sequencing that balances urgency and stress components. Biomarker work such as red-blood-cell-distribution-width-to-albumin ratio supports refined subtype diagnosis to guide sling selection. Dietary research indicates processed foods exacerbate leakage, while fruit-rich diets appear protective, suggesting lifestyle management alongside surgery.

Mixed and urge incontinence segments grow steadily through guideline updates that integrate combination therapies, yet stress remains the bellwether category keeping the vaginal slings market on a solid expansion path.

By End User: Specialty Clinics Lead Growth

Hospitals accounted for 57.20% revenue in 2025, leveraging 24 / 7 imaging, anesthesiology, and critical-care capacity for complex cases. Their multidisciplinary teams manage comorbid elderly patients, anchoring volume leadership inside the vaginal slings market. Yet specialty clinics post a 9.61% CAGR as focused expertise, shorter wait times, and bundled care models resonate with payers and patients.

The ambulatory surgery network processed 3.4 million Medicare beneficiaries through 6,308 ASCs in 2023, driving USD 6.8 billion in spend and proving their economic significance. Urology-centered ASCs now host more than 60% of procedures once restricted to inpatient wards, while office-based sling placement under local anesthesia emerges for select low-BMI candidates with low operative risk. Accreditation drives protocol standardization and outcome tracking, enhancing patient confidence in these settings. As reimbursement increasingly rewards site-of-service savings, specialty clinics will intensify competition for hospital volume.

Geography Analysis

North America retained 37.65% revenue leadership in 2025, propelled by stable Medicare coverage, procedural familiarity, and a mature ASC infrastructure. The announcement of new pelvic-floor HCPCS codes in 2024 will extend reimbursement to adjunct devices, incentivizing broader care pathways. The vaginal slings market also benefits from FDA guidance that clarifies mesh labeling and affirms mini-sling safety, enabling providers to reassure patients despite legal headwinds. Nonetheless, multi-state litigation and the USD 302 million Ethicon penalty continue to temper growth in certain jurisdictions.

Asia-Pacific is the fastest-growing region with an 10.97% CAGR through 2031. Governments expand insurance coverage while private providers develop pelvic health centers that attract inbound medical tourism. Chinese studies reveal sizeable underdiagnosis across provinces, catalyzing public campaigns and specialist training. Japan and Australia adopt PVDF and single-incision technologies early, whereas India’s burgeoning middle class fuels volume growth in polypropylene solutions owing to cost sensitivity. Diverse regulatory landscapes require localized clinical evidence, but rising surgical capacity and ASC adoption uplift the regional vaginal slings market. Europe maintains steady growth under the 2017/745 Medical Device Regulation that mandates rigorous clinical evaluation and post-market scrutiny, enhancing trust and driving gradual product upgrades. German clinicians, having navigated evolving mesh rules, share practice patterns that reduce complications and litigation risk. The United Kingdom’s group settlement reinforces calls for safer materials yet may encourage payers to fund premium PVDF devices to mitigate future claims. Markets in the Middle East & Africa and South America progress from a small base, aided by lower-cost laparoscopic options, local-anesthesia protocols, and growing medical tourism corridors that funnel cross-border demand.

Value Chain Analysis

The vaginal slings value chain begins with polymer and biologic inputs, then moves through precision converting and sterile kit assembly before reaching hospitals, ambulatory surgery centers (ASCs), and specialty clinics. Key inputs include specialized monofilament polypropylene resin (often linked to large petrochemical supply hubs), emerging PVDF mesh materials, and, for absorbable or biologic offerings, pharmaceutical-grade collagen and graft materials from accredited tissue-bank networks. Manufacturing typically involves laser cutting, folding, and polymer joining (for example, ultrasonic or RF welding for subassemblies), followed by validated sterilization (often ethylene oxide) and packaging with traceable lot controls.

Commercialization runs via direct sales into urogynecology and urology accounts, as well as through tenders or group purchasing organizations that bundle device pricing with site-of-service economics, particularly in ASCs. Compliance and documentation requirements affect throughput, including labeling and registration or listing obligations in the United States, plus post-market clinical follow-up expectations under the EU MDR; capacity constraints at notified bodies can also extend recertification timelines. Operational risk centers on single-source or regionally concentrated resin supply, sterilization capacity and validation, and the specialist surgeon training pipeline that influences how quickly procedure volumes scale across care settings.

Competitive Landscape

The vaginal slings market displays moderate concentration. Boston Scientific, Coloplast, and Johnson & Johnson control the largest installed bases through comprehensive sling families, surgical delivery tools, and professional education programs. Boston Scientific’s 2024 Axonics acquisition adds sacral neuromodulation, creating a full-continuum incontinence portfolio and signaling broader convergence across urology devices. Coloplast advances fixation-system ergonomics, recently securing FDA clearance for its Saffron device that simplifies suture anchoring. Ethicon reinforces physician outreach after litigation setbacks, investing in PVDF research to restore brand equity.

Material innovation is the primary differentiation vector. Companies that commercialize PVDF and bioresorbable meshes gain premium pricing and regulatory goodwill, while laggards risk share erosion as surgeons migrate away from polypropylene. Artificial-intelligence platforms for patient selection, outcome prediction, and surgical planning emerge as new battlegrounds; start-ups position algorithmic decision support to established OEMs seeking competitive edge.

Strategic acquisitions continue as firms seek broader therapy ecosystems. Beyond Axonics, med-tech players explore partnerships with digital pelvic-floor-training vendors to offer hybrid conservative-surgical packages. Geographic expansion also shapes rivalry: tier-one suppliers deepen localization in China and India through CME programs and domestic manufacturing, whereas niche innovators license IP to regional distributors rather than build global salesforces. Collectively these strategies maintain a balanced yet dynamic competitive environment for the vaginal slings market.

Vaginal Slings Industry Leaders

Boston Scientific Corporation

Coloplast Corp

Promedon Group

A.M.I. GmbH

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clearer, multi-year regulatory and payer signals create whitespace for differentiated sling platforms that reduce complication concerns while maintaining familiar surgical workflows. In June 2026, Health Canada finalized an assessment of the long-term (five or more years) safety and effectiveness of standard synthetic mid-urethral slings for stress urinary incontinence, concluding clinical effectiveness equivalent to surgical alternatives without vaginal surgical mesh. In January 2026, Australias Medical Devices and Human Tissue Advisory Committee completed a post-listing review of mid-urethral slings on the Prescribed List, with no change to listing status or benefit amounts, supporting continued access pathways in a major developed market.

Innovation opportunities are focused on materials and evidence generation rather than reopening higher-risk indications. The US FDA continues to distinguish stress urinary incontinence slings, including mini-slings supported by post-market surveillance evidence, from transvaginal pelvic organ prolapse mesh, which remains under Class III PMA requirements. Suppliers that shift portfolios toward lightweight meshes and PVDF-based options, invest in post-market registries, and incorporate patient selection tools into clinician training programs have room to compete on safety confidence and total episode efficiency across hospitals and ASCs. At the same time, the competitive set faces pressure to substantiate long-term outcomes to defend procedure volumes against non-surgical alternatives such as bulking agents and energy-based therapies.

Recent Industry Developments

- June 2026: Boston Scientific-related claimant notices advanced in Australias mesh settlement process, with final individual notices of assessment being distributed to claimants tied to the previously announced AUD 105 million settlement. The ongoing handling of legacy mesh liabilities keeps attention on long-term safety evidence and risk management across pelvic health device portfolios.

- January 2026: Coloplast reported termination of an observational post-market clinical study involving Transabdominal Restorelle meshes, reflecting heightened scrutiny around mesh follow-up commitments. Changes in study status can affect how manufacturers prioritize post-market evidence plans and portfolio focus in urogynecology.

- October 2024: Coloplast obtained US FDA 510(k) clearance (K242473) covering multiple sling systems, including Altis Single Incision, Aris Transobturator, and Supris Retropubic. The clearances reinforce the importance of maintaining compliant product lines across key sling modalities while supporting continuity of supply to hospital and outpatient channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the sales value of vaginal sling systems used in surgical management of female stress or mixed urinary incontinence, as supplied as sterile, factory-built kits for use in hospitals, ambulatory surgery centers, and specialty clinics.

Scope exclusions: Male incontinence-only products, injectable bulking agents, and pelvic organ prolapse mesh kits are not counted in this market.

Segmentation Overview

- By Product Type

- Transobturator Slings (TOT)

- Tension-free Vaginal Tape (TVT)

- Mini / Single-Incision Slings

- Adjustable Autologous / Biological Slings

- By Material Type

- Polypropylene Mesh

- PVDF Mesh

- Absorbable / Biological Mesh

- By Incontinence Type

- Stress Urinary Incontinence

- Mixed Urinary Incontinence

- By End User

- Hospitals

- Ambulatory Surgery Centres

- Speciality Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with public, traceable datasets that help anchor procedure demand and clinical adoption. Sources reviewed include items such as CDC and National Center for Health Statistics releases, CMS utilization and payment files, FDA device safety communications and approvals, and selected peer-reviewed clinical journals on mid-urethral sling outcomes and safety.

To keep the model practical, we also use supporting secondary material such as company annual reports, investor presentations, and medical association webpages that describe treatment pathways and guideline shifts. Where needed, we use paid subscription materials for company financials and news to cross-check revenue direction and major portfolio changes, and we use a paid patent database to sense innovation timing around sling designs and materials. These are illustrative examples only, and we also relied on many other public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test desk assumptions, especially around the split of sling types, typical selling price movement, and the share of cases shifting to outpatient settings. We speak with clinicians, procurement stakeholders, and manufacturer-side functions across APAC, EMEA, and the Americas, then align the inputs to one consistent market definition before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 13% | APAC: 42% |

| Mid tier: 48% | Functional/Unit leaders: 37% | EMEA: 34% |

| Smaller Players: 17% | Managers: 50% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool where procedure volumes for female urinary incontinence are reconstructed, then filtered to sling-eligible cases and typical sling usage per procedure. The resulting volume is valued using a blended price that reflects the in-market mix of retropubic, transobturator, single-incision, and adjustable systems. To keep totals realistic, we corroborate with selective bottom-up approximations like sampled price checks by care setting and limited supplier roll-ups in larger countries, then adjust where public procedure reporting is thin.

Several inputs drive most of the estimate in this market, so we track them closely and update them with interview feedback. Key examples include surgical treatment rates for stress urinary incontinence, the outpatient shift between hospitals and ambulatory surgery centers, mesh-related litigation and guideline signals that can change adoption, the product mix across sling designs, and currency timing for cross-country conversions. For forecasting, we run scenario analysis around policy and safety-event sensitivity, then apply regression-style linking of procedure growth to aging female population trends and care-setting shifts. Assumptions are reviewed with experts so the forward path stays plausible.

Data Validation & Update Cycle

Outputs are checked against independent signals such as procedure trend direction, import and shipment patterns where visible, and reported category revenue movement in public filings. If something looks off, we rework the assumptions and send follow-up questions back into primary channels so the variance is explained before sign-off.

Before publication, the model goes through multi-step analyst review where definitions, math, and year-over-year movements are rechecked, and outliers are documented. The report is refreshed annually, and interim updates are made when material events occur, for example major safety communications or reimbursement shifts. Right before delivery, we do a final pass to confirm the latest data points are reflected.

Mordor Intelligence's Vaginal Slings Market Estimate Compared With Other Published Estimates

Published numbers for vaginal slings do not always line up because the market can be defined narrowly as sterile sling kits for female stress or mixed urinary incontinence, or more broadly by folding in adjacent urogynecology devices and related procedures. Differences also come from the base year chosen, how procedure volumes are inferred, and whether pricing is held flat or allowed to move with product mix changes.

The main gap comes from scope overlap with prolapse mesh kits and non-sling incontinence options. Mordor Intelligence counts only factory-built vaginal sling systems used for female stress or mixed urinary incontinence, and leaves out injectable bulking agents and male-only products. Another driver is the demand signal used, since some estimates lean heavily on historical revenue anchors, while our approach ties value back to procedure-linked volumes and a blended price by sling type, and then converts currencies using consistent timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.59 B (2025) | |

| Global Consultancy A | USD 1.90 B (2023) | Uses an earlier base year and may lean on reported category revenues with broader product adjacency, which can overcount when related urogynecology devices are bundled with slings. |

| Industry Publisher B | USD 1.70 B (2025) | Likely applies a wider product taxonomy and a different sling mix and ASP progression, which can shift totals even when the headline year matches. |

The spread in the table is mostly explained by what gets counted and how demand is translated into dollars. When procedure-linked volume, sling-type mix, and pricing logic are kept explicit, the market total becomes easier to trace, repeat, and update as clinical practice and safety signals evolve.

Key Questions Answered in the Report

What is the current size of the vaginal slings market?

The vaginal slings market was valued at USD 1.71 billion in 2026 and is projected to reach USD 2.48 billion by 2031 at a 7.67% CAGR.

Which product type holds the largest share in the vaginal slings market?

Transobturator slings led with 39.35% revenue in 2025, benefitting from long-standing clinical familiarity and favorable safety data.

Why are PVDF meshes gaining popularity over polypropylene?

PVDF offers higher tensile strength, lower bending stiffness, and superior in-vivo stability, which together reduce erosion and pain complications that have affected polypropylene implants.

Which region will grow the fastest through 2031?

Asia-Pacific is forecast to expand at an 10.97% CAGR, driven by rising procedure volumes in China, India, Japan, and Australia alongside robust medical tourism.

How are legal actions influencing market growth?

Large settlements and stricter regulatory classifications slow near-term adoption in North America and Europe, prompting manufacturers to develop safer materials and more rigorous clinical evidence.

What role do ambulatory surgery centers play in market expansion?

ASCs handle more than 60% of urology procedures in the United States, offering cost advantages and patient convenience that support wider access to sling surgeries.

Page last updated on: