Vitrectomy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

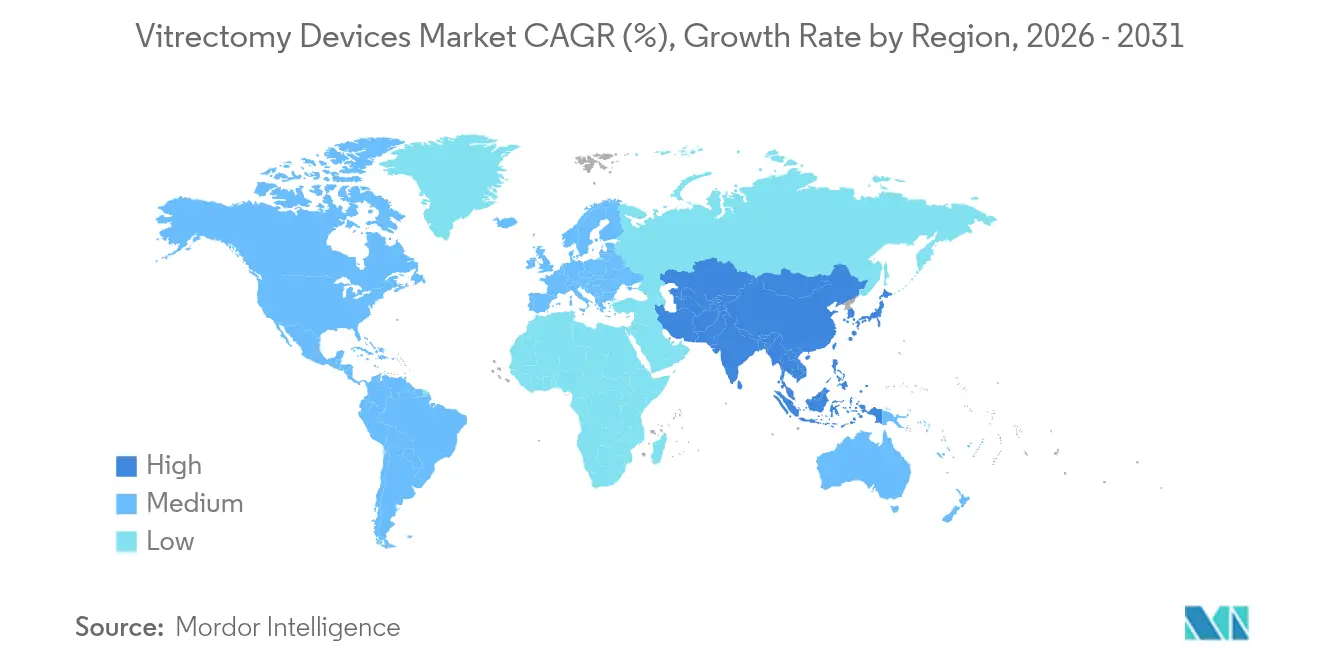

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

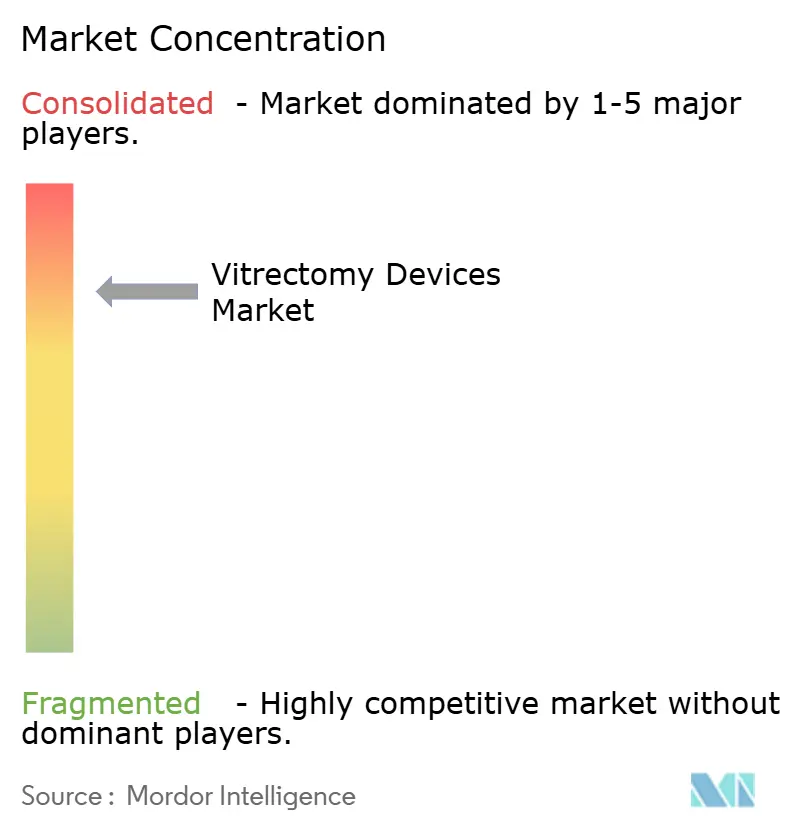

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vitrectomy Devices Market Analysis by Mordor Intelligence

The Vitrectomy Devices Market size in 2026 is estimated at USD 1.9 billion, growing from 2025 value of USD 1.8 billion with 2031 projections showing USD 2.51 billion, growing at 5.72% CAGR over 2026-2031. Growth flows from demographic ageing, rising diabetes prevalence, and rapid advances in minimally invasive surgery platforms. Hospitals and clinics see stable reimbursement for complex retina work, helping suppliers maintain high equipment utilisation. Technology-led differentiation around small-gauge instrumentation and hypersonic cutters is widening the performance gap between legacy consoles and next-generation systems. Consolidation among leading manufacturers and retina service groups is tightening purchase-decision dynamics, while the shift of routine cases to ambulatory settings enlarges the installed base of portable platforms. Regulators in the United States and Europe are easing market entry for specific ophthalmic categories, shortening time-to-market for innovative offerings and supporting steady procedural growth.

Key Report Takeaways

- By product type, vitrectomy packs led with 30.85% of vitrectomy devices market share in 2025, while vitrectomy systems are projected to expand at a 6.95% CAGR through 2031.

- By application, diabetic retinopathy captured 39.88% revenue share of the vitrectomy devices market size in 2025; macular hole treatments are advancing at a 7.45% CAGR to 2031.

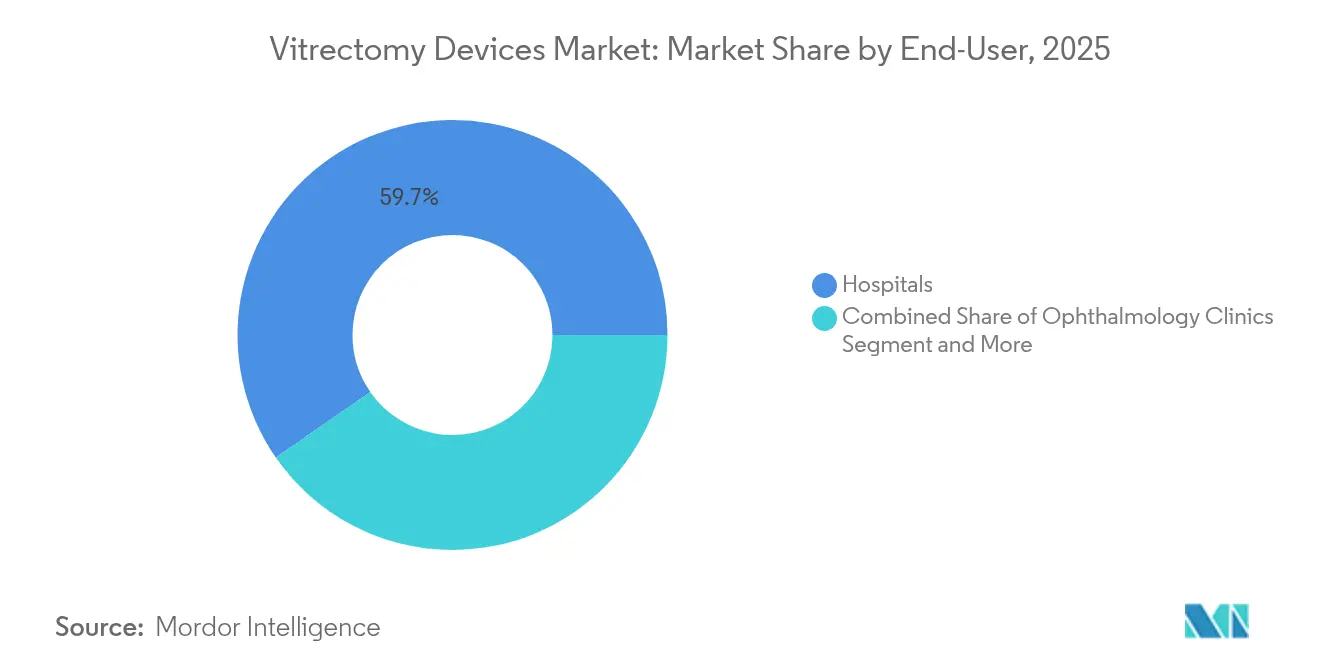

- By end-user, hospitals accounted for 59.65% of the vitrectomy devices market size in 2025, whereas ophthalmology clinics are growing fastest at a 6.58% CAGR through 2031.

- By geography, North America commanded 37.75% of the vitrectomy devices market share in 2025, while Asia-Pacific is the fastest-growing region at an 7.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vitrectomy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Burden of Vitreoretinal Disorders (DR, RRD, AMD) | +1.8% | Global, with highest impact in North America & Asia-Pacific | Long term (≥ 4 years) |

| Aging Population Boosting Surgical Volume Across Developed and Emerging Regions | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Advances in Minimally-invasive Vitrectomy Technologies | +1.2% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Increased Awareness and Early Diagnosis | +0.8% | Global, with early gains in urban centers | Medium term (2-4 years) |

| Expansion of Ambulatory Surgical Centers & Favorable Outpatient Reimbursement for Retina | +0.9% | North America & EU primarily | Short term (≤ 2 years) |

| Shift Toward Single-use Ophthalmic Instruments Driven by Strict Infection-control Mandates | +0.6% | Global, with fastest adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Burden of Vitreoretinal Disorders Drives Surgical Demand

Diabetic retinopathy affects nearly 10 million Americans and more than 100 million people worldwide, pushing continuous demand for surgical intervention. Proliferative disease often requires pars plana vitrectomy, as confirmed by a 10-year Indian cohort study highlighting the procedure’s role in vision preservation. Age-related macular degeneration cases could reach 67 million in the European Union and 26 million in China, adding further load on surgical capacity. Cataract complications also create downstream vitrectomy need, maintaining baseline procedure volume.

Aging Population Demographics Reshape Surgical Volume Patterns

By 2025, adults aged 65 and older outnumber youth in the WHO European Region, underlining the demographic pivot toward older cohorts. The United Nations projects that one in six people globally will be over 60 by 2030, with 80% living in low and middle-income countries by 2050. This demographic reality compels healthcare systems to invest in vitreoretinal surgical capacity and advanced device technologies to serve an increasingly elderly patient population requiring complex interventions.

Advances in Minimally-invasive Vitrectomy Technologies

Small-gauge instrumentation reduces surgical trauma and speeds recovery. A prospective study showed 25-gauge beveled-tip systems achieving procedural objectives in all cases with controlled operative times. Hypersonic platforms running at 31 kHz generate millions of cuts each minute, lowering vitreous traction and improving fluidics.[1]Source: Editors, “Hypersonic Vitrectomy: A Different Perspective,” Retina Today, retinatoday.com These benefits have fuelled office-based vitrectomy, which delivered a 97.3% single-surgery success rate for retinal detachment in Japan. These technological advances enable surgeons to perform complex procedures in outpatient settings, reducing healthcare costs while improving patient convenience and outcomes.

Ambulatory Surgical Centres Expand Market Access

Medicare incentives and lower facility costs stimulate a steady shift from hospital theatres to ambulatory sites. United States build-out costs for two-room ophthalmic centres range from USD 750,000 to USD 1 million, making ownership attractive for high-volume groups. Sixty-six percent of retina surgeons intend to adopt office-based surgery within five years, supported by over 60,000 procedures already documented in the iRWD registry. This shift toward ambulatory care models creates demand for portable, efficient vitrectomy systems optimized for outpatient environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Maintenance Cost of Systems | -1.1% | Global, with highest impact in emerging markets | Long term (≥ 4 years) |

| Post-operative Complications & Patient Anxiety | -0.7% | Global, with regional variation in patient education | Medium term (2-4 years) |

| Limited Availability of Skilled Vitreoretinal Surgeons in Developing Countries and Supply-chain Vulnerability for Precision Components | -0.9% | Developing countries & rural areas globally | Long term (≥ 4 years) |

| Lengthy and Stringent Regulatory Approval Cycles | -0.5% | Global, with variation by regulatory jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements Limit Market Penetration

Comprehensive equipment packages for two operating rooms can cost up to USD 1 million, an outlay that strains hospital budgets in emerging economies.[2]Source: M Boston, “Building and Owning an Ambulatory Surgery Center,” CRSToday, crstoday.com The cost-effectiveness analysis of vitrectomy procedures shows favorable outcomes, with pars plana vitrectomy costing EUR 1,468.26 while delivering 6.84 lifetime quality-adjusted life years.[3]Source: R Blomquist, “Cost Analysis of Scleral Buckle and Pars Plana Vitrectomy for Retinal Detachment,” Dove Press, dovepress.com Although lifetime cost-effectiveness analyses favour vitrectomy in terms of quality-adjusted life years, the initial capital barrier remains significant for many healthcare facilities, particularly those serving underserved populations where vitreoretinal expertise is most needed.

Skilled Surgeon Shortage Constrains Market Growth

The United States expects a 30% shortfall of ophthalmologists by 2035, with rural availability dropping to 29% of required staffing levels. Asia-Pacific shows pronounced disparities, from 114 ophthalmologists per million residents in Japan to negligible coverage in some areas. Limited fellowship slots and complex learning curves for cutting-edge consoles act as a brake on utilisation of installed systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Systems Drive Innovation While Packs Retain Volume Leadership

Vitrectomy packs delivered 30.85% of the vitrectomy devices market share in 2025, reflecting their role as consumables for every case. Vitrectomy systems are projected to grow at a 6.95% CAGR, lifting their slice of the vitrectomy devices market size through 2031 as hospitals replace ageing consoles with integrated imaging and hypersonic technologies. Packs benefit from stable procedure counts and preference for manufacturer-matched consumables, giving suppliers predictable recurring revenue.

Instruments and photocoagulation lasers post mid-single digit gains, supported by stricter infection-control rules that favour single-use tools. FDA clearance of integrated platforms such as Alcon’s Unity VCS underscores the shift toward multifunctional consoles that combine cutting, illumination, and laser features within one footprint.

By Application: Diabetic Complications Lead While Precision Interventions Accelerate

Diabetic retinopathy accounted for 39.88% of the vitrectomy devices market size in 2025, mirroring the worldwide diabetes burden and high conversion of proliferative cases to surgery. Macular hole procedures are increasing at a 7.45% CAGR, supported by success rates exceeding 90% when modern imaging guides peeling and tamponade selection.

Retinal detachment volumes hold steady thanks to emergency referrals, while vitreous haemorrhage cases decline modestly as pharmacotherapy reduces intraocular bleeding risk. Precision instruments tailored to epiretinal membrane removal and proliferative vitreoretinopathy expand the addressable pool of complex pathologies and deepen the market penetration of advanced platforms.

By End-User: Hospitals Dominate Yet Clinics Gain Ground

Hospitals held 59.65% of the vitrectomy devices market size in 2025, supported by emergency coverage and co-management of multi-morbid patients. Outpatient migration drives a 6.58% CAGR for ophthalmology clinics, which bundle vitrectomy, cataract, and glaucoma procedures within streamlined care pathways. Ambulatory surgical centres capture the highest procedural growth as Medicare and private payers continue to favour lower-cost settings, sustaining equipment orders for compact systems that fit into two-room clinics.

The shift toward outpatient care models reflects technological advances that enable complex procedures in non-hospital settings, improved patient convenience, and healthcare cost containment pressures. This trend accelerates as minimally invasive techniques reduce procedure complexity and recovery time, making clinic-based vitrectomy increasingly viable for routine cases.

Geography Analysis

North America anchors 37.75% of the vitrectomy devices market in 2025, driven by 2.2 million annual procedures, strong reimbursement, and early adoption of hypersonic cutters. Workforce shortages loom, yet policy adjustments that widen scope of practice for optometrists and allied personnel may protect throughput. The FDA’s decision to reclassify selected ultrasound devices from Class III to Class II has lowered market entry hurdles for component innovations. Canada pursues similar risk-based pathways, sustaining device inflows, while Mexico’s Seguro Popular reforms are widening access to public ophthalmic care.

Asia-Pacific is forecast to post an 7.62% CAGR through 2031, buoyed by rapid demographic ageing and expanding middle-class insurance cover. Japan exemplifies clinical sophistication, operating with more than 114 ophthalmologists per million residents, whereas Indonesia and parts of South Asia still grapple with shortages. China’s central procurement policies are pressuring average selling prices, yet procedure growth is offsetting margin compression for global suppliers. India’s tier-2 cities welcome freestanding retina centres that adopt affordable 25-gauge consoles sourced under concessional import schemes.

Europe records steady mid-single digit growth thanks to universal health coverage and ageing demographics. Harmonised Medical Device Regulation simplifies simultaneous multi-country approvals, though post-market surveillance duties raise compliance costs that smaller entrants may struggle to meet. Germany and France lead regional demand, while the United Kingdom carves a separate approval route via the UKCA mark, extending timelines for dual submissions. Environmental mandates are encouraging adoption of reusable handpieces and regulated reprocessing to lower surgical waste, influencing future product design choices.

Competitive Landscape

Leading suppliers combine broad procedural portfolios, global service footprints, and active acquisition pipelines to preserve competitive moats. Alcon reinforced its laser portfolio by acquiring LENSAR for USD 356 million, a move that strengthens its integrated cataract-retina offering. Bausch + Lomb differentiates through hypersonic vitrectomy that delivers 31 kHz cutting frequencies, and its recent Elios glaucoma device acquisition widens cross-selling potential. The competitive intensity reflects the market's technical complexity and high barriers to entry, requiring substantial R&D investment, regulatory expertise, and clinical validation to achieve market success.

New entrants focus on cost-efficient disposables and portable consoles for office-based sites. The FDA's 510(k) clearance process creates opportunities for innovative companies to challenge established players, as demonstrated by breakthrough device designations for novel technologies like LumiThera's Valeda system for dry AMD treatment.

White-space opportunities exist in emerging markets, office-based surgery solutions, and AI-enhanced surgical guidance systems, while the shift toward single-use instruments creates new revenue streams and competitive dynamics. Emerging disruptors focus on cost-effective solutions for developing markets, portable surgical systems, and specialized applications that address unmet clinical needs in vitreoretinal surgery.

Vitrectomy Devices Industry Leaders

Alcon

BVI

Bausch + Lomb (Bausch Health)

Carl Zeiss Meditec AG (DORC)

Geuder AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BVI Medical completed a USD 1 billion capital raise to accelerate global expansion.

- September 2024: Microsurgical Technology and Vista Ophthalmics unveiled the Vista 1-Step 27-gauge dual-blade vitrector.

- April 2024: Carl Zeiss Meditec finalised the acquisition of Dutch Ophthalmic Research Center, integrating the EVA NEXUS platform.

- February 2023: Mani, Inc. launched Mani Micro Forceps for vitreoretinal surgery in Japan.

Global Vitrectomy Devices Market Report Scope

Vitrectomy is an eye surgery used to remove some or all of the vitreous humor from the eye. It involves making a small cut (incision) or using special blades to insert the instruments into the sclera of the eyes.

The Vitrectomy Devices Market is Segmented by Product Type (Vitrectomy System, Illumination Devices, Infusion Devices, Instruments, and Other Product Types), Application (Diabetic Retinopathy, Retinal Detachment, Macular Hole, Vitreous Hemorrhage, and Other Applications), End-User (Hospitals, Ophthalmology Clinics, and Ambulatory Surgical Centers), and Geography (North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific), Middle East and Africa GCC, South Africa, and Rest of the Middle East and Africa), and South America (Brazil, Argentina, Rest of South America)). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Vitrectomy Systems |

| Vitrectomy Packs |

| Photocoagulation Lasers |

| Instruments |

| Other Product Types |

| Diabetic Retinopathy |

| Retinal Detachment |

| Macular Hole |

| Vitreous Hemorrhage |

| Other Applications |

| Hospitals |

| Ophthalmology Clinics |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Vitrectomy Systems | |

| Vitrectomy Packs | ||

| Photocoagulation Lasers | ||

| Instruments | ||

| Other Product Types | ||

| By Application | Diabetic Retinopathy | |

| Retinal Detachment | ||

| Macular Hole | ||

| Vitreous Hemorrhage | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Ophthalmology Clinics | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the vitrectomy devices market?

The vitrectomy devices market stands at USD 1.9 billion in 2026 and is projected to reach USD 2.51 billion by 2031.

Which product category holds the largest share?

Vitrectomy packs lead with 30.85% of vitrectomy devices market share, reflecting their recurring use in every procedure.

Which application area is growing fastest?

Macular hole interventions are forecast to expand at a 7.45% CAGR through 2031 due to improved imaging and surgical techniques.

Which region shows the highest growth potential?

Asia-Pacific is projected to grow at an 7.62% CAGR as ageing populations and expanding insurance cover boost procedure volumes.

What technology trend is reshaping equipment purchasing?

Hypersonic small-gauge vitrectomy systems that cut at 31 kHz are gaining traction by lowering traction forces and enabling office-based surgery.

Page last updated on: