Human Reproductive Technologies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 33.46 Billion |

| Market Size (2031) | USD 37.87 Billion |

| Growth Rate (2026 - 2031) | 2.51% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

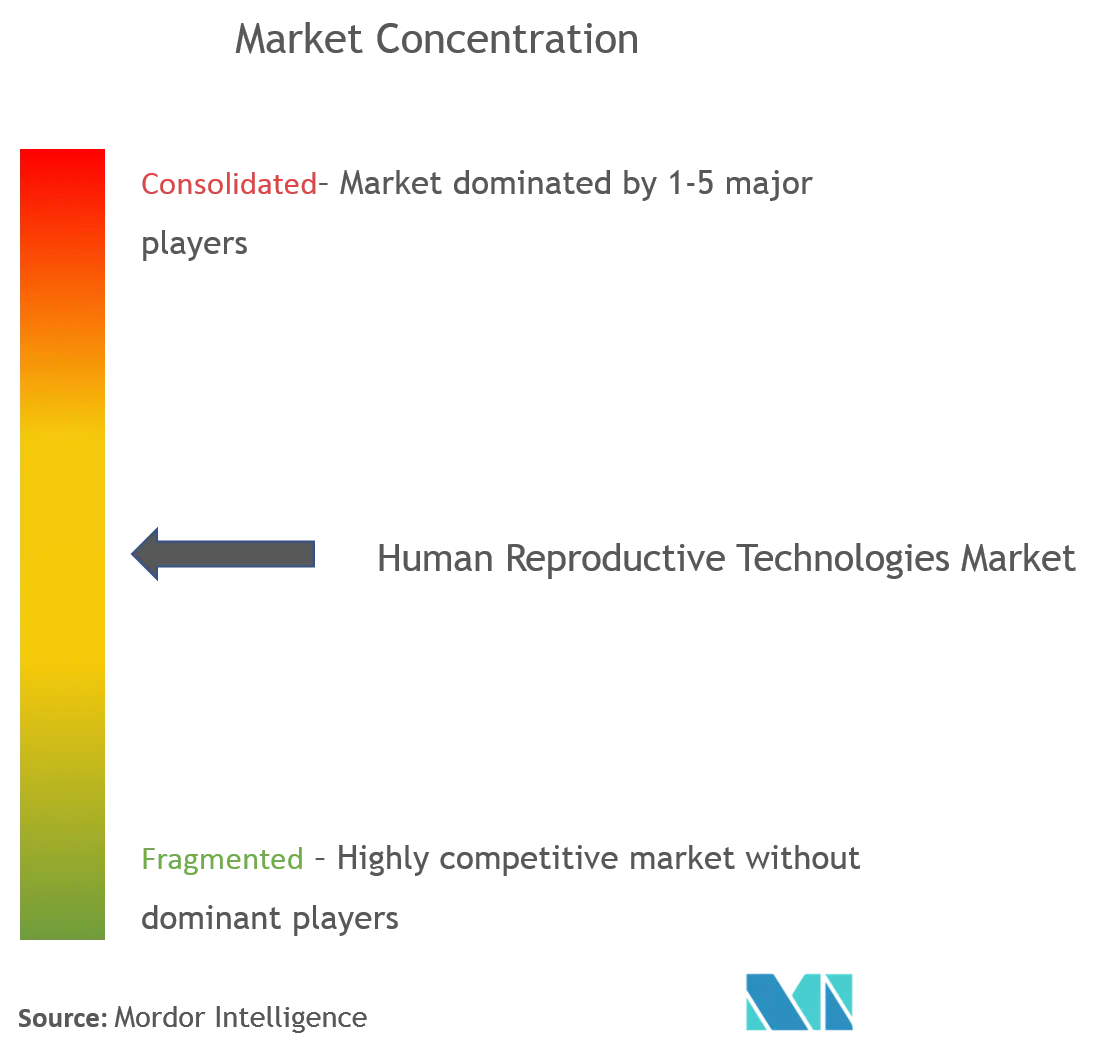

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Reproductive Technologies Market Analysis by Mordor Intelligence

Human reproductive technologies market size in 2026 is estimated at USD 33.46 billion, growing from 2025 value of USD 32.64 billion with 2031 projections showing USD 37.87 billion, growing at 2.51% CAGR over 2026-2031. Demand is lifted by rising global infertility prevalence, later-in-life parenthood, and constant product innovation that now blends artificial intelligence, robotics, and genetic testing. Corporate fertility-benefit programs and expanding public reimbursement schemes further widen patient access, while private-equity consolidation accelerates clinical scale and standardization. At the same time, ethical debates, workforce shortages, and uneven insurance coverage temper expansion, creating a balanced yet durable growth profile for the human reproductive technologies market. Competitive advantage increasingly hinges on technology adoption, data-driven care models, and the ability to serve both contraceptive and infertility segments under diversified service offerings.

Key Report Takeaways

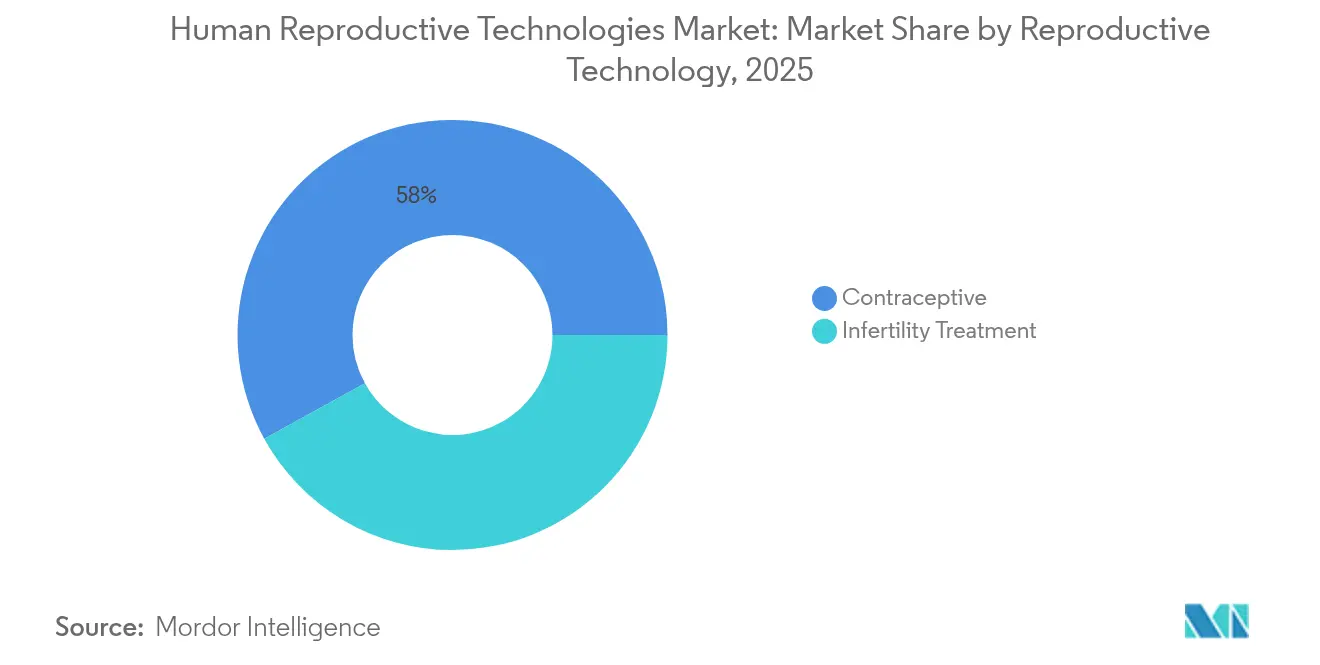

- By reproductive technology, contraceptives led with a 58.02% revenue share in 2025, while infertility treatments are projected to grow at a 3.02% CAGR to 2031.

- By gender, the female segment held 85.05% of human reproductive technologies market share in 2025; male-focused solutions are forecast to expand at a 3.28% CAGR through 2031.

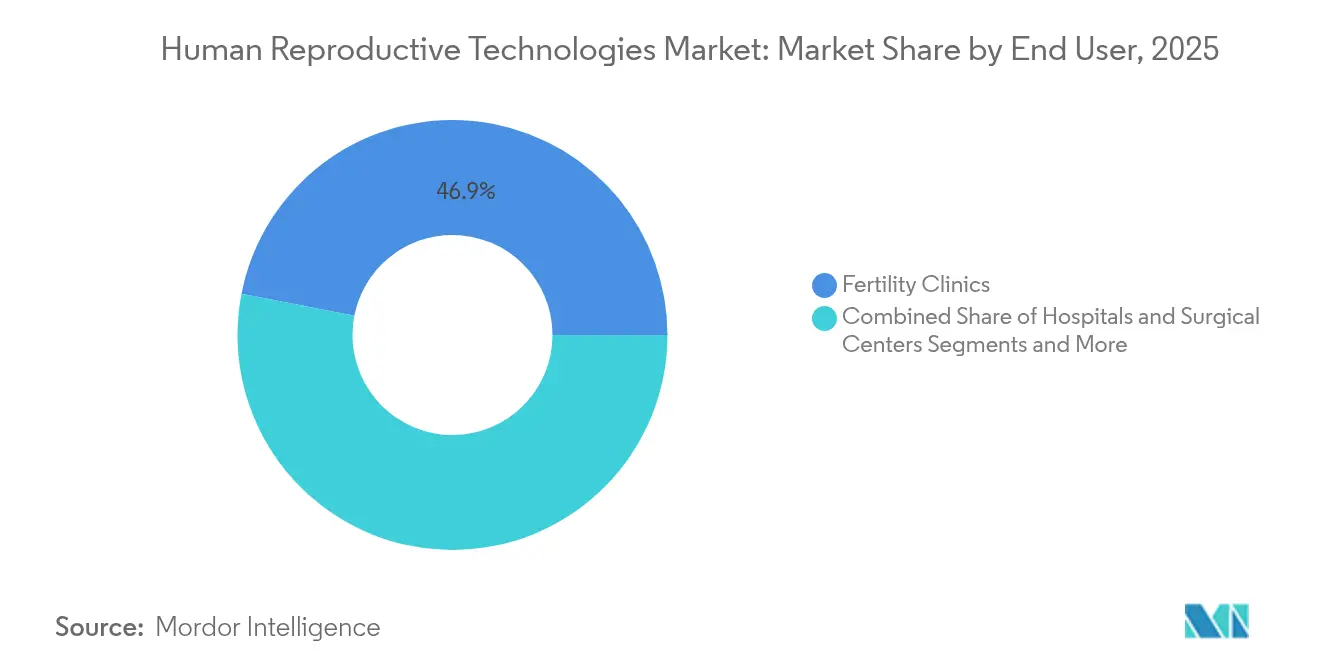

- By end user, fertility clinics accounted for 46.92% of human reproductive technologies market size in 2025, whereas homecare and over-the-counter solutions will advance at a 3.67% CAGR to 2031.

- By product mode, drugs dominated with a 61.74% share of human reproductive technologies market size in 2025; devices and equipment are set to grow at a 3.27% CAGR between 2026 and 2031.

- By geography, North America held 44.78% of human reproductive technologies market share in 2025, with Asia-Pacific positioned for the fastest expansion at a 3.92% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Human Reproductive Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Infertility | +0.8% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Continuous Technological Progress—ICSI, Pre-Implantation Genetic Testing | +0.6% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Delayed Family Planning & Higher Maternal Age | +0.5% | Global, particularly urban centers | Long term (≥ 4 years) |

| Growing Government Support & Reimbursement | +0.4% | APAC core, spill-over to emerging markets | Medium term (2-4 years) |

| Employer-Funded Fertility-Benefit Programs | +0.3% | North America & EU | Short term (≤ 2 years) |

| AI-Powered Embryo & Gamete Analytics | +0.2% | Global, led by technology hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Infertility

One in six adults now experiences infertility at some stage, underscoring a public-health challenge that drives sustained demand for advanced reproductive care. In the United States, the share of married women under 50 who reported infertility rose to 8.7% in 2019, up from 6.7% in the earlier half of the decade [1]U.S. Centers for Disease Control and Prevention, “Infertility statistics 2024,” cdc.gov. Several Asia-Pacific economies face even sharper pressures, with South Korea’s total fertility rate plummeting to 0.8, the lowest worldwide. Environmental exposure, lifestyle changes, and postponement of childbearing compound biologic risk, pushing more couples toward assisted reproductive technology (ART). These factors collectively sustain the mid-single-digit growth segments within the broader human reproductive technologies market.

Continuous Technological Progress—ICSI & Pre-implantation Genetic Testing

AI-enhanced embryo selection now achieves up to 75% clinical pregnancy-prediction accuracy, improving over traditional morphology-only assessment [2]Frontiers in AI Editorial Team, “Deep-learning embryo selection improves IVF outcomes,” frontiersin.org. Robot-controlled intracytoplasmic sperm injection (ICSI) has demonstrated higher fertilization rates while allowing remote operation over distances exceeding 2,300 miles. Non-invasive pre-implantation genetic testing that analyzes cell-free DNA in spent culture media matches the concordance of biopsy-based methods, reducing embryo manipulation risk. Time-lapse imaging systems combined with deep learning allow continuous embryo monitoring without exposure changes, optimizing selection protocols. Such advances cut cycle numbers, raise success rates, and compress patient costs, reinforcing adoption across the human reproductive technologies market.

Delayed Family Planning & Higher Maternal Age

Birth rates for women aged 30 and older continue to rise, and demand for fertility services has followed suit as clinical tools extend the biologic window for conception. New research initiatives into ovarian longevity, alongside employer funding for egg-freezing benefits, help women postpone childbirth without surrendering reproductive options. Early-stage in-vitro gametogenesis (IVG) research hints at future avenues for age-Independent gamete creation, while uptake of company-sponsored fertility coverage jumped to 42% of U.S. employers in 2024. The trend enlarges the market’s addressable base and steers investment toward preservation, testing, and advanced ART protocols.

Growing Government Support & Reimbursement

China’s feasibility study on including ART in public medical insurance suggested an additional 3.3–9.6 million live births could be achieved per year if coverage is widened. Japan adopted new surgical fee codes for IVF and ICSI in 2024, strengthening insurance backing for infertility care. In February 2025, a U.S. executive order mandated expanded IVF access for military families and federal employees, emphasizing affordability and equitable coverage. Singapore, Malaysia, and other Asia-Pacific nations continue to co-fund ART cycles, illustrating how proactive policy can shape the human reproductive technologies market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Insurance Coverage for ART | -0.4% | Global, particularly developing markets | Short term (≤ 2 years) |

| Ethical & Religious Opposition | -0.3% | Regional variations, concentrated in conservative markets | Long term (≥ 4 years) |

| Stringent Regulatory Pathways and Lengthy Approval Timelines | -0.5% | Global, with higher impact in developed markets | Medium term (2-4 years) |

| Shortage of Reproductive Endocrinologists | -0.6% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Insurance Coverage for ART

Even as employer benefits expand, many patients still face out-of-pocket costs of USD 12,000–25,000 per IVF cycle in the United States, limiting uptake among middle-income households. In numerous low- and middle-income countries, ART fees can exceed 200% of GDP per capita, rendering services inaccessible for the vast majority[3]Reproductive Health Journal, “Affordability barriers in low-income settings,” reproductive-health-journal.biomedcentral.com. Insurance policies often cover diagnostics while excluding treatment, creating fragmented pathways that suppress the potential of the human reproductive technologies market. These reimbursement gaps slow volume growth, especially in price-sensitive emerging markets.

Ethical & Religious Opposition

Religious doctrine shapes ART acceptance: Roman Catholic teaching rejects most assisted reproductive procedures, while many Islamic scholars limit third-party gamete involvement. Such positions influence policymaking and cultural attitudes in Latin America, parts of Europe, and sections of the Middle East. Debate intensifies as emerging tools such as gene editing and IVG raise concerns over embryo status and “designer baby” scenarios, potentially lengthening regulatory timelines. Resistance can delay clinic openings, constrain technology scope, and curb demand in conservative markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Reproductive Technology: Contraceptive Pre-eminence Meets ART Momentum

Contraceptive solutions dominated revenue with a 58.02% stake in 2025, testifying to long-established demand across demographics. Oral pills remain the mainstay, yet long-acting reversible contraception gains share as next-generation intra-uterine systems introduce sustained-release mechanisms. In parallel, infertility treatments outpace overall human reproductive technologies market growth, registering a 3.02% CAGR projected through 2031. Broadening public funding, AI-guided embryo analytics, and reduced procedural complexity propel treatment cycles higher, especially in Asia-Pacific clinics. Combination drug-and-device protocols lower stimulation doses and shorten cycle lengths, broadening patient appeal.

R&D investment targets gamete quality enhancement, non-invasive genetic testing, and robotic micromanipulation—areas anticipated to lift success-rate benchmarks beyond today’s 42% live-birth per cycle ceiling. As a result, integrated providers that offer both preventive and therapeutic services position themselves to capture rising cross-segment demand within the human reproductive technologies market.

By Gender: Female Dominance Faces Rising Male Focus

The female segment commanded 85.05% of revenue in 2025, anchored by contraceptive prevalence and well-established fertility treatments. However, breakthrough male contraceptive pipelines promise to reshape share dynamics. A topical hormonal gel now in Phase III delivers 86% sperm suppression within 15 weeks, faster than historic injectables. Non-hormonal options such as selective retinoic acid receptor antagonists and hydrogel-based vas-occlusive implants advance through early trials, appealing to men seeking reversible methods without hormonal side effects.

Male infertility diagnostics also benefit from AI-assisted sperm-quality prediction, reducing laboratory workload while increasing predictive accuracy. These innovations explain the segment’s forecast-leading 3.28% CAGR, illustrating how the human reproductive technology industry is broadening gender-inclusive care portfolios.

By End User: Clinic Networks Strengthen as Homecare Scales

Fertility clinics retained 46.92% of 2025 revenue, underpinned by a wave of private-equity-backed roll-ups that streamline protocols and deepen technology investments. A 2024 peer-reviewed study found that newly consolidated chains improved live-birth rates by 13.6% and expanded cycle volume by 27% within two years. Homecare and OTC solutions, covering ovulation tests, at-home semen analysis, and self-injectable contraception, are set to climb at a 3.67% CAGR as consumers prioritize convenience and confidentiality.

Digital health platforms now integrate tele-consults, medication adherence tracking, and outcome analytics, linking clinics, pharmacies, and diagnostic labs into a cohesive patient journey. Hospitals and research institutes remain vital for complex interventions and technology validation, but the fastest-growing revenues increasingly flow from hybrid care pathways that bridge facility-based and home-based services within the human reproductive technologies market.

By Product Mode: Drug Supremacy Meets Accelerating Device Adoption

Drugs held 61.74% of human reproductive technologies market size in 2025, covering ovarian stimulants, hormonal contraceptives, and adjunct therapies. Meanwhile, device revenue will rise at a 3.27% CAGR as AI-enabled imaging, robotic micromanipulators, and advanced culture systems gain traction. The U.S. FDA’s 2024 guidance for intravaginal culture devices set clear biocompatibility and performance standards, accelerating market entry for innovative systems.

Start-ups such as Gameto advance iPSC-derived ovarian support cells that mature oocytes outside the body, demonstrating how convergence of cell therapy and medical hardware can slash hormonal drug usage by 80%. Long-acting contraceptive implants incorporating nanotech carriers offer multi-year efficacy with minimal systemic exposure, highlighting how materials science upgrades will steadily narrow the gap between device and drug segments.

Geography Analysis

North America generated 44.78% of 2025 revenue, benefiting from mature healthcare financing, broad employer fertility benefits, and early adoption of AI-driven clinical protocols. The region also enacts supportive federal policy, exemplified by the 2025 executive order extending IVF benefits to military and civil-service families. Yet growth is partially constrained by a projected shortfall of 5,170 reproductive endocrinologists by 2030, which intensifies competition for clinical talent and incentivizes tele-medicine and robotic solutions to balance supply gaps.

Asia-Pacific represents the fastest-growing geography with a 3.92% CAGR expected through 2031. Policy levers play a central role: China’s exploration of national ART reimbursement could unlock millions of incremental treatment cycles per year. Japan’s updated surgical codes for IVF and ICSI similarly expand coverage, while Singapore and Malaysia subsidize up to 75% of treatment costs to combat declining birth rates. Fertility tourism into regional hubs further boosts procedure volumes and encourages high-tech clinic build-outs.

Europe maintains steady, mid-single-digit growth as universal health systems shield patients from high out-of-pocket spend. The region also hosts leading research networks such as ESHRE, which disseminate best-practice standards adopted worldwide. Regulatory debate over embryo-testing ethics and cross-border surrogacy can lengthen approval timelines, yet clinical sophistication and high disposable income sustain procedure uptake.

Emerging economies in the Middle East, Africa, and South America still account for a modest slice of human reproductive technologies market size, but investment in private clinics and technology transfer partnerships is catalyzing double-digit local growth rates from a low base.

Regulatory Landscape

Regulation spans medical devices, IVD/genetic testing, medicines, and the handling of substances of human origin used in ART. In the European Union, Regulation (EU) 2024/1938 introduced a unified quality and safety framework for substances of human origin (SoHO), which affects procurement, traceability, and quality systems for reproductive cells, tissues, and embryos across member states and cross-border care pathways.

In the United States, federal actions in February 2025 (Executive Order 14216) elevated IVF access as a policy priority, followed by May 2026 Federal Register updates on “Excepted Fertility Benefits” that shape how fertility benefits are structured and administered. India tightened oversight in April 2026 when CDSCO directed strict regulation of IVF and ART medical devices under the Drugs and Cosmetics Act, 1940 and the Medical Devices Rules, 2017, raising compliance requirements for importers, manufacturers, and distributors. Across major markets, AI-based embryo assessment and other software tools increasingly fall under Software as a Medical Device pathways, which increases the emphasis on clinical evaluation and post-market controls rather than treating these solutions as unregulated software.

Value Chain Analysis

The value chain starts with upstream inputs and manufacturing of fertility drugs (gonadotropins, progesterone support, hormonal contraceptives) and specialized devices and consumables used in embryology labs (incubators, imaging systems, micromanipulators, catheters, culture media, cryostorage hardware, and lab consumables). Established device manufacturers such as CooperSurgical, Vitrolife, and Esco Medical supply equipment and workflow solutions to fertility clinics and hospitals through direct sales and distributor networks, while service providers and integrators support installation, validation, maintenance, and user training.

In the midstream, laboratories and tissue banks operate under stringent quality and regulatory requirements, with standardized assays such as the Mouse Embryo Assay (MEA) used as a quality control anchor for products that contact gametes or embryos. Turnkey IVF lab providers (for example, Shivani Scientific) bundle lab design, equipment installation, and technician training to reduce fragmentation and accelerate new clinic ramp-up. Downstream, care delivery occurs mainly through fertility clinic networks and hospital-based ART units, where payer and employer-benefit administrators influence patient access and channel mix. Digital platforms also expand scheduling, counseling, and adherence support, linking clinics, pharmacies, and diagnostics into a more integrated care pathway.

Competitive Landscape

Competition is moderate and trending toward concentration as private-equity funds roll up independent clinics to build national and regional networks. From 2017 to 2024, investors committed more than USD 625 million across 30-plus fertility platform deals, seeking scale advantages in marketing, lab automation, and payer contracting. Data from a 2024 Management Science study show that network clinics deliver 13.6% better live-birth outcomes post-integration, underscoring technical synergies.

Technology differentiation is equally decisive. AI-guided embryo-scoring software achieves 75–86% predictive accuracy, outperforming manual morphology and offering clinics a tangible success-rate edge. Robotic micromanipulation platforms reduce technician variability and enable remote operation, opening new tele-lab business models. Innovators such as Gameto, NEXT Life Sciences, and TMRW Life Sciences position themselves as ecosystem enablers through cell therapy, male contraception, and automated cryostorage, respectively.

Drug manufacturers remain essential partners, providing recombinant gonadotropins, progesterone support, and novel contraceptive formulations. Device specialists such as CooperSurgical and Hamilton Thorne supply consumables, imaging systems, and laser equipment that integrate with laboratory information software. Insurers and digital-health platforms like Progyny and Maven Clinic create a third axis of competition, using data analytics and bundled coverage to steer patients toward preferred provider networks, thereby influencing volume allocation within the human reproductive technologies market.

Human Reproductive Technologies Industry Leaders

CooperSurgical

Teva Pharmaceutical Industries

AbbVie Inc.

Ferring B.V

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory formalization is creating whitespace for compliant device and consumable suppliers in markets where enforcement has been uneven. India’s 2026 classification and enforcement actions around IVF/ART devices (including commonly used items such as IUI kits and sperm-wash centrifuges) increase the value of registered portfolios, strengthen local distribution discipline, and elevate documentation-ready quality systems for suppliers serving fast-growing clinic footprints in Asia-Pacific.

Automation and validated decision-support tools are also becoming clearer purchase criteria for clinics that face staffing constraints and need to standardize outcomes across multi-site networks. Capital formation around automated IVF laboratories provides a market proof point, including Conceivable’s USD 50 million Series A in September 2025 to develop and commercialize an AI-powered automated IVF lab concept. In parallel, public and professional bodies are actively shaping the development pathway for novel ART, with the UK outlining a technology-neutral approach for emerging modalities such as in vitro gametogenesis under Human Fertilisation and Embryology Authority oversight, and ASRM issuing an April 2026 ethics opinion that channels IVG research through institutional review board supervision. Together, these signals support opportunities for manufacturers and clinic networks that can generate prospective clinical evidence, build traceable lab workflows, and align product roadmaps with evolving oversight for genetic testing and next-generation ART.

Recent Industry Developments

- July 2026: CooperSurgical announced support for the Saving Mothers initiative to advance global womens health and fertility education. While not a product launch, the program strengthens patient and provider engagement in maternal and reproductive health channels that influence demand for contraception and fertility services. The initiative reinforces brand positioning with clinic stakeholders and health systems amid widening public attention to fertility access.

- October 2025: EMD Serono (Merck KGaA) entered a public-private agreement with the U.S. government to expand access to IVF therapies through the TrumpRX.gov platform, offering an 84% discount on a portfolio that includes Gonal-f, Ovidrel, and Cetrotide. The initiative operationalizes a direct access and affordability mechanism for high-cost fertility drugs and can redirect patient volume toward participating therapies. In the same announcement, the company also committed to file Pergoveris under the FDA Commissioners National Priority Voucher program to pursue an accelerated review pathway.

- November 2024: SpOvum launched SpOvum ARTGPT, an AI-enabled platform aimed at streamlining patient interaction and decision support in fertility clinics. The release highlights the shift toward software-led workflow optimization alongside traditional lab devices and drugs. It also reflects growing competitive emphasis on digital tools that help clinics manage counseling load, standardize communication, and improve patient journey efficiency.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues linked to human reproductive technologies used to prevent pregnancy or support conception, across commonly used drugs, devices, and procedure-enabling tools sold through clinical and healthcare channels.

Scope exclusions: We exclude broader women's health products that are not directly tied to contraception or infertility care, and we also exclude non-medical wellness offerings.

Segmentation Overview

- By Reproductive Technology

- Infertility Treatment

- Drugs

- Follitropin Alfa

- Follitropin Beta

- Menotropins

- Others

- Devices

- Sperm Separation Devices

- Sperm Analyzer Systems

- Ovum Aspiration Pumps

- Micromanipulator Systems

- Others

- Drugs

- Contraceptive

- Drugs

- Oral Contraceptives

- Topical Contraceptives

- Contraceptive Injectables

- Devices

- Condoms

- IUD

- Cervical Caps

- Diaphragms

- Drugs

- Infertility Treatment

- By Gender

- Male

- Female

- By End User

- Fertility Clinics

- Hospitals & Surgical Centers

- Homecare & OTC

- Research Institutes

- By Product Mode

- Drugs

- Devices & Equipment

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public data that helps map the demand pool and the flow of reproductive health products. Sources such as the World Health Organization, the World Bank, the United Nations Population Division, and OECD health statistics were used to ground country-level context on fertility, demographics, and healthcare access. We also reviewed publications from public health agencies, such as the CDC, to understand procedure prevalence and how care pathways differ.

On the supply and regulatory side, we checked filings and safety updates from agencies such as the US FDA and the European Medicines Agency to track product availability and major label changes. We then added company annual reports, investor presentations, reputable press coverage, and scientific literature (for example, peer-reviewed journals covering IVF lab practices and contraception effectiveness) to refine assumptions such as adoption speed and pricing direction. Patent database subscriptions were used selectively to spot where innovation activity could change product mixes over time. These sources are illustrative and not exhaustive, and we relied on additional public references for cross-checking, validation, and clarification.

Primary Interviews and Surveys

Primary interviews focused on validating what is counted as market revenue and how quickly product mixes are changing in clinics and hospitals. We spoke with a mix of manufacturers, distributors, fertility clinic administrators, clinicians, and lab specialists across APAC, EMEA, and the Americas, so the model could be checked against on-the-ground pricing, protocol usage, and reimbursement realities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 30% | EMEA: 36% |

| Smaller Players: 17% | Managers: 57% | Americas: 20% |

Market-Sizing & Forecasting

The core sizing uses a top-down approach where population and healthcare indicators are translated into a treated-demand pool, then converted into market value using typical therapy and procedure baskets. In practice, country estimates are built from indicators such as infertility prevalence, contraceptive prevalence, ART cycle volumes, average embryos transferred or frozen per cycle, and the share of cycles using add-on lab testing. Pricing inputs reflect reference price points for key drug classes, typical device and consumable bundles used per cycle, and local reimbursement or out-of-pocket patterns that shape the real paid price.

To keep totals realistic, we corroborated results with selective bottom-up approximations such as sampled average selling price multiplied by estimated volumes for key consumables, plus channel checks on clinic purchasing behavior. Where bottom-up detail is incomplete, gaps are handled using proxy utilization rates from similar markets, and we then adjust them based on interview feedback before final totals are set.

For forecasting, scenario analysis is used, guided by expert views on how cycle volumes, delayed parenthood, insurance coverage expansion, and clinic capacity constraints may shift in each region. The final outlook stays aligned with visible demand signals, and one-off shocks are separated from steady adoption trends.

Data Validation & Update Cycle

Outputs are checked through multiple layers so obvious mismatches are caught early and investigated with clear explanations. We compare country totals against independent signals such as procedure counts, demographic trends, and healthcare spending patterns, and large variances are traced back to a limited set of assumptions including volumes, pricing, or mix. If a value appears out of line, analysts re-check the underlying input series, and when needed, re-contact interviewees to confirm whether a local change has occurred.

Before sign-off, a second analyst reviews the model to confirm that formulas, currency conversion timing, and growth logic are applied consistently across regions. Reports refresh on an annual cycle, with interim updates triggered by material events such as reimbursement changes, major regulatory actions, or sudden shifts in clinic activity. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Human Reproductive Technologies Market Size Compared Against Other Published Estimates

Published market sizes for human reproductive technologies can differ, even when the topic name looks the same. Variations typically come from what is counted as revenue, which years are used as anchors, and how procedure-linked consumables and services are treated across countries.

Some published figures fold in broader fertility service revenues and adjacent women's health spending that sits outside product-linked reproductive technology. In Mordor Intelligence's sizing, the value is limited to contraception and infertility treatment revenues tied to drugs, devices, and procedure-enabling tools, and then it is checked against cycle volumes and pricing patterns before forecasting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 33.46 B (2026) | |

| Global Consultancy A | USD 36.41 B (2025) | Uses an earlier base year and appears to include a wider set of fertility services and related offerings, which can lift totals beyond product and procedure-tool revenues. Faster growth assumptions may also reflect more aggressive uptake of add-on services across regions. |

| Industry Publisher B | USD 27.60 B (2025) | Lower sizing is consistent with a narrower revenue capture, where parts of devices, clinic-linked consumables, or newer lab technologies may be under-counted or treated as optional add-ons. Differences can also come from currency timing and slower assumed price progression. |

The table shows that most of the spread can be explained by scope choices and how procedure-linked revenue is translated into value across countries. By tying estimates to clear demand indicators such as contraception usage and ART cycles, and by keeping pricing logic transparent, the final number remains repeatable and easier to reconcile with real-world signals over time.

Key Questions Answered in the Report

What is the current Human Reproductive Technologies Market size?

The human reproductive technologies market is valued at USD 33.46 billion in 2026.

Who are the key players in Human Reproductive Technologies Market?

CooperSurgical, Teva Pharmaceutical Industries, AbbVie Inc., Ferring B.V and Merck KGaA are the major companies operating in the Human Reproductive Technologies Market.

Which is the fastest growing region in Human Reproductive Technologies Market?

Asia-Pacific is forecast to post the quickest growth, at a 3.92% CAGR between 2026 and 2031.

Why are employer fertility-benefit programs important?

Corporate plans now cover 42% of U.S. employers, reducing out-of-pocket costs and expanding access to advanced fertility care.

Page last updated on: