Cervical Dysplasia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

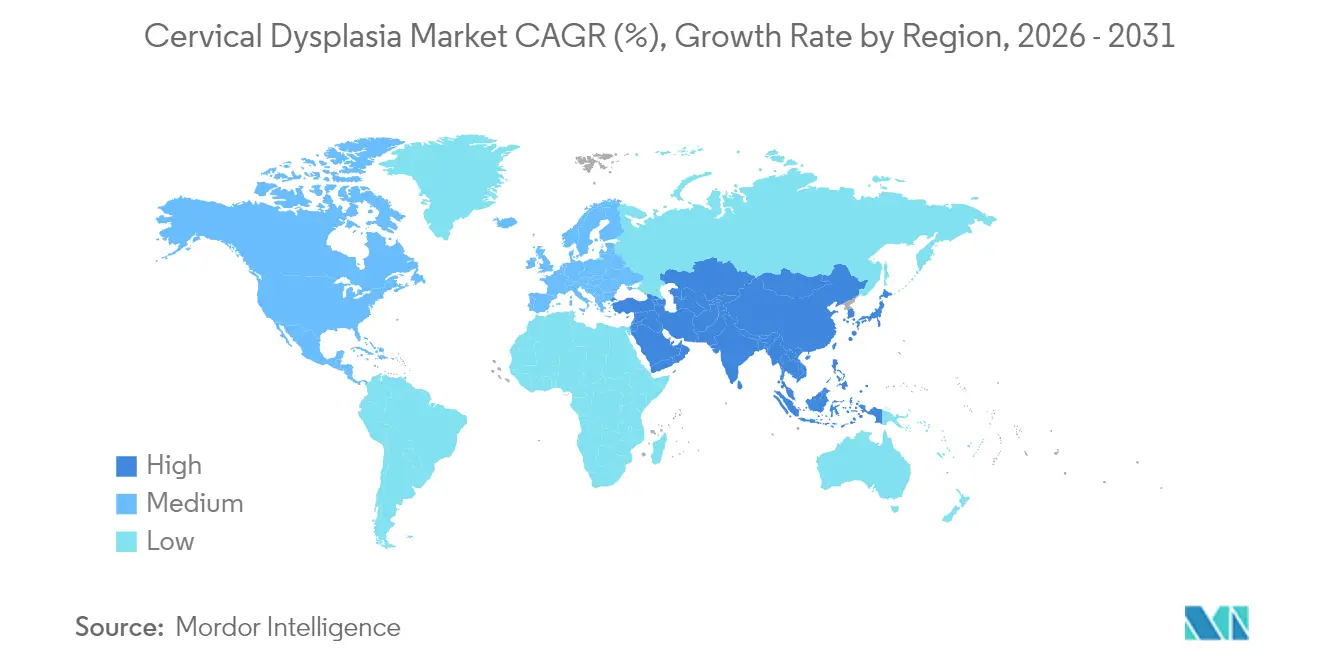

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cervical Dysplasia Market Analysis by Mordor Intelligence

cervical dysplasia market size in 2026 is estimated at USD 0.82 billion, growing from 2025 value of USD 0.77 billion with 2031 projections showing USD 1.14 billion, growing at 6.78% CAGR over 2026-2031. Growth is underpinned by rising human papillomavirus (HPV) prevalence, rapid uptake of molecular diagnostics, and the scaling of government-funded screening programs aligned with the World Health Organization’s 90-70-90 elimination targets[1]Source: Pan American Health Organization, "HPV Testing and Single-Dose Vaccine Key to Tackle Cervical Cancer in the Americas, PAHO Report Says," Pan American Health Organization, paho.org . North America maintained the largest regional position in 2024, reflecting early technology adoption and favorable reimbursement structures, while Asia-Pacific emerged as the fastest-growing arena owing to expanding healthcare access and employer-sponsored screening initiatives. Diagnostics continued to dominate overall revenue, supported by FDA approvals for self-collection HPV tests and AI-enabled digital cytology that shorten interpretation time and improve accuracy. Meanwhile, portable single-visit thermal ablation devices and low-cost point-of-care DNA assays are opening fresh opportunities in low- and middle-income countries where facility readiness remains a critical gap..

Key Report Takeaways

- By product type, diagnostics led with 66.65% of cervical dysplasia market share in 2025, while therapeutics is projected to rise at a 7.62% CAGR through 2031.

- By end user, hospitals and clinics held 46.05% revenue share in 2025; specialty gynecology centers record the highest expected CAGR at 8.02% to 2031.

- By geography, North America commanded 34.25% of the global cervical dysplasia market in 2025, whereas Asia-Pacific is set to advance at a 8.74% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cervical Dysplasia Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HPV prevalence & sub-optimal vaccination coverage | +2.1% | Global, with highest impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Expansion of government-funded screening guidelines | +1.8% | North America, Europe, with spillover to emerging markets | Long term (≥ 4 years) |

| Rapid adoption of molecular diagnostics (HPV DNA, LBC) | +1.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Portable single-visit "screen-and-treat" thermal ablation programs | +0.9% | LMIC regions, sub-Saharan Africa, rural Asia | Medium term (2-4 years) |

| AI-enabled cervical imaging triage platforms | +0.6% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Employer-sponsored women's health screening packages in Asia-Pacific | +0.3% | Asia-Pacific core, Japan, Singapore, Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising HPV Prevalence & Sub-optimal Vaccination Coverage

Recent epidemiological meta-analyses covering 2.7 million women in China reported 17.70% HPV infection, while Slovakia documented 21.59% prevalence within its national program[2]Source: Mingxia Li et al., “Prevalence of HPV Infection in Chinese Women,” BMC Medicine, bmcmed.biomedcentral.com . Despite robust vaccine efficacy, only 48% of eligible countries have rolled out HPV immunization. Canada’s decision to switch to a single-dose schedule aims to accelerate uptake against a 75% lifetime infection risk among unvaccinated populations canada.ca. Persistent transmission in women <21 and >61 years sustains lesion incidence and fuels cervical dysplasia market growth.

Expansion of Government-Funded Screening Guidelines

The UK National Health Service completed rollout of primary HPV screening in 2019 and continues to record improved detection at earlier stages. A recent PAHO partnership with Spanish agencies seeks to accelerate elimination efforts across Latin America, where more than 78,000 cases still arise each year. Bangladesh’s adoption of the DHIS2 tracker has already registered over 4.6 million women, illustrating the role of digital platforms in scaling coverage.

Rapid Adoption of Molecular Diagnostics

FDA clearance of self-collection HPV testing for Roche cobas and BD Onclarity assays allows patients to provide vaginal samples in healthcare settings without clinician sampling, broadening reach while preserving accuracy. DiaCarta’s QuantiVirus E6/E7 mRNA test augments specificity by identifying active oncogene expression, thereby reducing unnecessary colposcopies. BD’s alliance with Techcyte integrates AI algorithms with whole-slide imaging, enabling pathologists to triage high-risk cases more efficiently and mitigating staffing shortages.

Portable Single-Visit “Screen-and-Treat” Thermal Ablation Programs

A randomized trial of 3,124 women in Zambia found portable thermal ablation non-inferior to both cryotherapy and loop electrosurgical excision, delivering 74.0% cure rates while bypassing CO₂ refrigeration needs. The US National Cancer Institute now supports development of battery-powered devices priced for LMIC deployment, aiming to curtail loss to follow-up that often exceeds 30% when treatment requires multiple visits

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Insufficient healthcare infrastructure in LMICs | -1.4% | Sub-Saharan Africa, rural Asia, Latin America | Long term (≥ 4 years) |

| High capital cost of next-gen diagnostic platforms | -0.8% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| CO₂ refrigerant supply volatility limiting cryotherapy adoption | -0.5% | LMIC regions, remote areas with supply chain constraints | Medium term (2-4 years) |

| Litigation risk of over-treatment driving conservative guidelines | -0.3% | North America, Europe, developed markets with legal frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Insufficient Healthcare Infrastructure in LMICs

A national facility assessment in Nepal showed cervical screening readiness at 59.1%, with rural clinics trailing significantly. In the Philippines, visual inspection with acetic acid failed to detect 28 HPV-positive women in a community audit, underscoring diagnostic gaps joghr.org. Systematic reviews reveal that women with disabilities are 35% less likely to be screened, compounding inequity. These hurdles limit uptake of both diagnostics and therapeutics, tempering cervical dysplasia market momentum in high-burden regions.

High Capital Cost of Next-Gen Diagnostic Platforms

AI-driven digital cytology demands investments in slide scanners, servers, and workforce training. Smaller laboratories hesitate when device costs can exceed USD 200,000, delaying adoption outside tier-one centers. Rice University’s low-cost HPV DNA prototype, targeting USD 500 hardware and sub-USD 5 cartridges, demonstrates a viable route to affordability and could ease this capital bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diagnostics Anchor Market Leadership

Diagnostics accounted for 66.65% of cervical dysplasia market share in 2025, reflecting the clinical pivot toward high-sensitivity HPV DNA assays and image-enhanced colposcopy. The segment is forecast to expand steadily on the back of AI-enabled workflows that halve slide review time and reduce false negatives.

Therapeutics, although smaller today, is the fastest climber with a 7.62% CAGR predicted through 2031. Portable thermal ablation tools and next-generation photodynamic therapy agents are set to reshape outpatient treatment, lowering reliance on operating theatres and anesthesia. Continued evidence of non-inferiority to traditional LEEP has encouraged Ministries of Health in Kenya and Zambia to purchase more than 1,500 handheld devices in 2024. As these programs mature, the therapeutics slice of the cervical dysplasia market is expected to widen, although reimbursement discussions remain crucial for sustained penetration.

By End User: Specialty Centers Capture Growth Momentum

Hospitals and clinics retained 46.05% share of the cervical dysplasia market in 2025, buttressed by integrated infrastructure for screening, diagnosis, and outpatient excision. These facilities typically hold advanced colposcopy suites and have direct reimbursement pathways for HPV genotyping. However, specialty gynecology centers are projected to log an 8.02% CAGR, the highest among end-user categories, driven by patient preference for focused care and shorter wait times.

The cervical dysplasia market size captured by specialty centers is expected to rise in tandem with employer-sponsored packages in Japan, Singapore, and Malaysia that channel women toward centers of excellence. Self-collection pilot programs bundling HPV tests with telemedicine consultations have also taken root in Australia, reinforcing a consumer-centric approach. As these models proliferate, diagnostic laboratories may form strategic alliances with specialty clinics to secure stable specimen volumes and support scalable AI cloud deployments.

Geography Analysis

North America commanded 34.25% of global cervical dysplasia market share in 2025, supported by Medicare coverage for Pap testing every 24 months and HPV cotesting every five years in eligible women. Multiple FDA clearances for self-collection sampling and AI-enabled cytology further solidify the region’s leadership. Robust specialist density permits same-day colposcopy in many urban centers, which translates into higher treatment completion rates and underpins market resilience.

Asia-Pacific is the fastest-growing territory, forecast to record a 8.74% CAGR to 2031 on the back of large susceptible populations and expanding public health funding. China’s 17.70% HPV prevalence highlights unmet need and fuels rapid uptake of molecular tests, especially in provincial screening caravans that visit rural counties on a monthly schedule. In India, fewer than 22% of eligible women have ever been screened, prompting adoption of mobile VIA units coupled with instantaneous thermal ablation to close follow-up gaps.

Europe presents steady, policy-driven expansion. The United Kingdom completed nationwide primary HPV screening transition, while Germany reimburses dual-stain p16/Ki-67 testing for ambiguous cytology. Many European Union members are evaluating self-sampling within organized programs after pilot studies in Sweden documented 10-percentage-point coverage gains in women overdue for screening. Spain’s move to invite vaccination of boys is expected to damp long-term HPV circulation and thus moderates future disease burden. Nevertheless, Eastern European countries still show lower uptake, leaving room for technology adoption that can address workforce shortfalls through AI and telecolposcopy.

Competitive Landscape

Competition remains moderate, with several multinational device manufacturers and a cadre of emerging diagnostics start-ups. Hologic, BD, and Roche are the key players, each leveraging diversified women’s health portfolios and deep regulatory experience. Strategic moves have accelerated: Hologic acquired Gynesonics for USD 350 million in October 2024, adding the Sonata System for fibroid treatment and signalling intent to expand beyond screening. Roche and BD secured the first FDA nods for self-collected HPV specimens, tapping an under-served user base that previously avoided clinic exams.

Disruptive entrants also influence rivalry. Teal Health raised USD 23 million and obtained National Cancer Institute backing to commercialize the Teal Wand, an at-home self-collection device now under FDA review. DiaCarta touts mRNA-based HPV oncogene detection aimed at minimizing false positives that drive unnecessary colposcopy diacarta.com. Several regional players in India and Brazil produce affordable colposcopes and thermal ablation units, applying value engineering to penetrate price-sensitive segments.

Pricing competition is limited by stringent regulatory requirements, yet service innovation is heightening differentiation. Many players now bundle cloud-based AI analytics with per-test pricing, which shifts capital cost away from end users. Partnerships with telehealth platforms allow same-day electronic follow-up, boosting adherence and elevating brand stickiness. Over the forecast horizon, cumulative evidence of superior clinical and economic outcomes is expected to drive hospital procurement policies toward integrated solutions, reinforcing the importance of R&D pipelines grounded in real-world performance data.

Cervical Dysplasia Industry Leaders

-

Qiagen

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd.

-

Becton, Dickinson and Company

-

Hologic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Teal Health completed a USD 10 million seed round to advance FDA review of the Teal Wand self-collection device and secured a USD 1.68 million National Cancer Institute grant for clinical validation

- January 2025: Hologic finalized the acquisition of Gynesonics for roughly USD 350 million, adding minimally invasive fibroid therapy to its women’s health platform.

- May 2024: Roche received FDA clearance for self-collected vaginal specimens processed with the cobas HPV test, expanding US screening options

Global Cervical Dysplasia Market Report Scope

As per the scope of the report, cervical dysplasia refers to abnormal cell changes on the cervix, which can be precursors to cervical cancer if not monitored or treated. The cervical dysplasia market is segmented by diagnosis type, end-user, and geography. By diagnosis type, the market is segmented into diagnostic tests and diagnostic devices. The diagnostic tests segment is further classified into HPV test, Pap smear test, and biopsy test. By end-user, the market is segmented into hospitals, specialty clinics, cancer and radiation therapy centers, and diagnostic centers. The report also covers the market size and forecasts for the cervical dysplasia market in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Diagnostics | Pap Smear Tests |

| HPV DNA Tests | |

| Liquid-Based Cytology | |

| Colposcopes | |

| Biopsy Devices | |

| Therapeutics | Cryotherapy Devices |

| Loop Electrosurgical Excision Procedure (LEEP) Systems | |

| Thermal Ablation Devices | |

| Topical & Systemic Pharmacologics |

| Hospitals & Clinics |

| Diagnostic Centers |

| Specialty Gynecology Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Diagnostics | Pap Smear Tests |

| HPV DNA Tests | ||

| Liquid-Based Cytology | ||

| Colposcopes | ||

| Biopsy Devices | ||

| Therapeutics | Cryotherapy Devices | |

| Loop Electrosurgical Excision Procedure (LEEP) Systems | ||

| Thermal Ablation Devices | ||

| Topical & Systemic Pharmacologics | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Centers | ||

| Specialty Gynecology Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the cervical dysplasia market?

• The cervical dysplasia market reached USD 0.82 billion in 2026 and is projected to climb to USD 1.14 billion by 2031.

Which region leads global revenue?

• North America held 34.25% of global cervical dysplasia market share in 2025, supported by mature screening infrastructure and favorable reimbursement.

Which segment is expanding the fastest?

• Therapeutics is the fastest-growing product segment, with a 7.62% CAGR driven by portable thermal ablation and novel photodynamic therapy devices.

How will self-collection HPV testing influence growth?

• FDA approval for self-collected samples is expected to widen access, reduce barriers, and contribute a positive 1.5% impact on forecast CAGR.

Page last updated on: