Medical Lifting Slings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

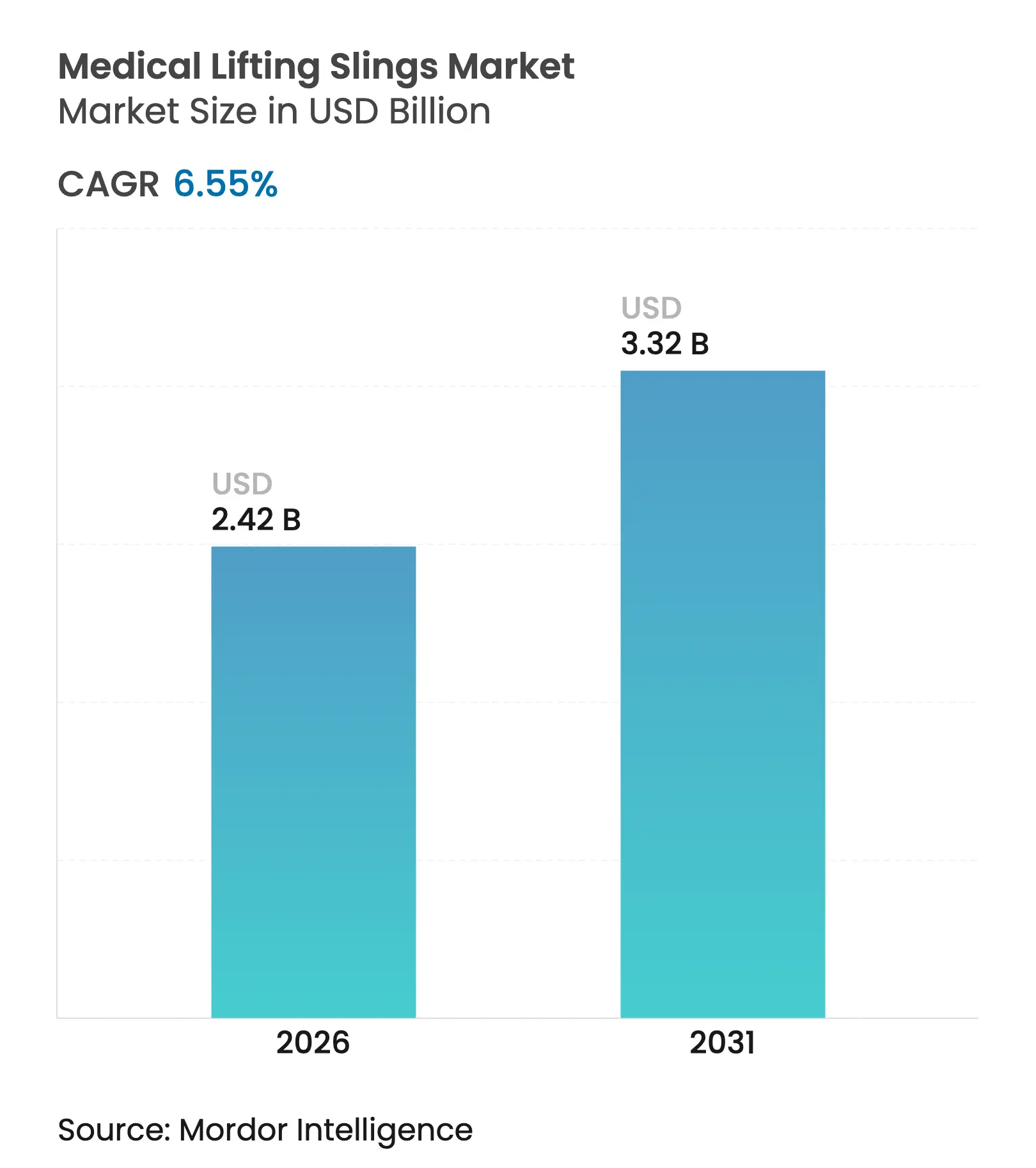

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 3.32 Billion |

| Growth Rate (2026 - 2031) | 6.55 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Medical Lifting Slings Market Analysis by Mordor Intelligence

Medical lifting sling market size in 2026 is estimated at USD 2.42 billion, growing from 2025 value of USD 2.27 billion with 2031 projections showing USD 3.32 billion, growing at 6.55% CAGR over 2026-2031. Demand stems from aging demographics, rising chronic disease incidence, and workplace safety mandates that push healthcare providers toward mechanized patient-handling solutions. Hospitals continue replacing manual transfers to limit musculoskeletal injuries and meet OSHA and FDA standards, while smart sling innovations and antimicrobial fabrics widen functional appeal. Heightened labor shortages also accelerate technology adoption, with the United States alone set to add 2.1 million healthcare jobs by 2032. Finally, reimbursement improvements for durable medical equipment (DME) boost patient access, especially in home and long-term care settings.

Key Report Takeaways

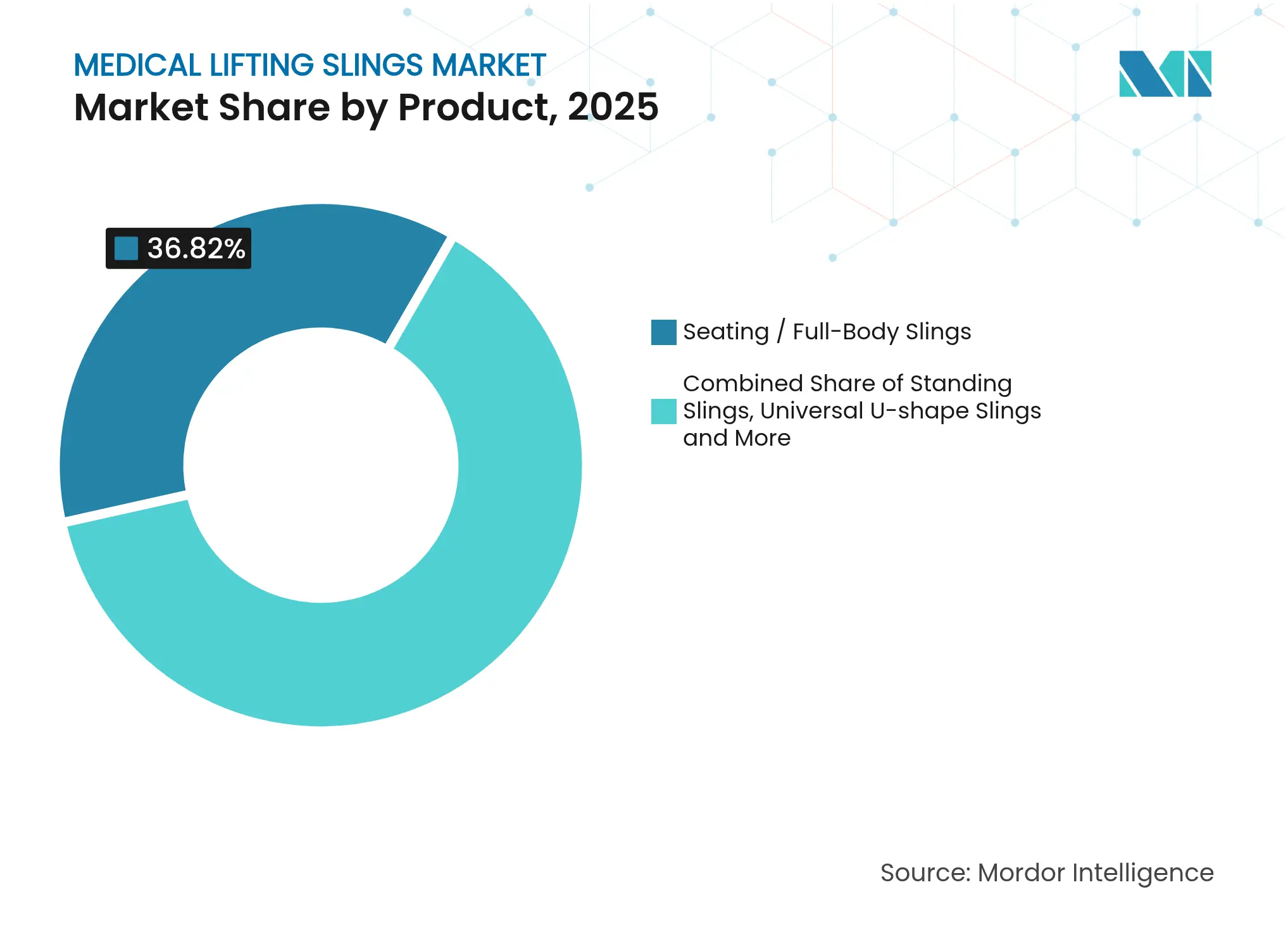

- By product type, seating and full-body slings led with 36.82% revenue share in 2025; bariatric and bari-plus models are forecast to expand at an 10.79% CAGR to 2031.

- By material, polyester accounted for 68.11% of the medical lifting sling market share in 2025, while technical textiles incorporating antimicrobials are advancing at a 10.42% CAGR through 2031.

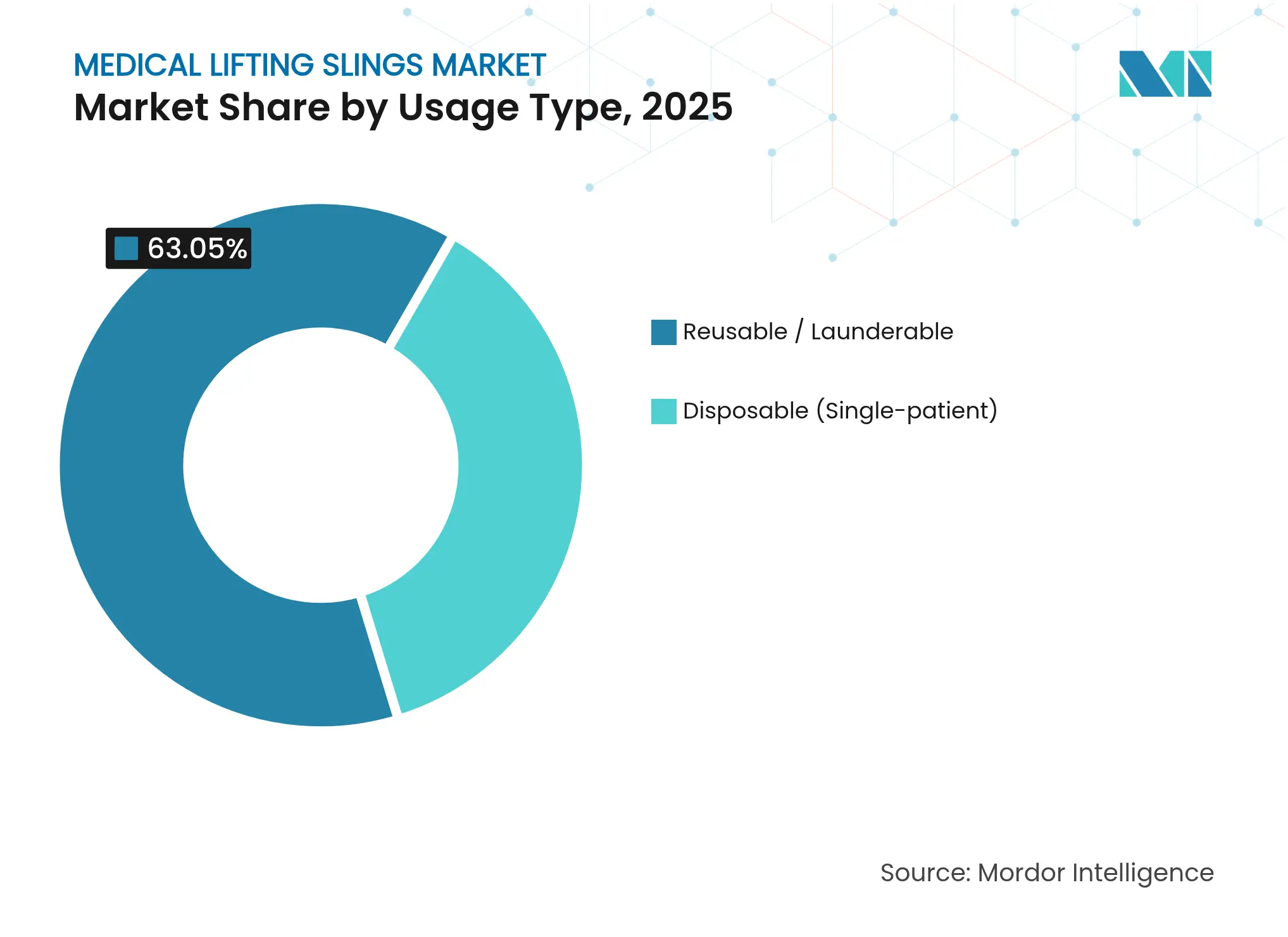

- By usage type, reusable formats commanded 63.05% of the medical lifting sling market size in 2025; disposable variants are growing at a 9.11% CAGR to 2031.

- By end user, hospitals and surgical centers held 56.14% share of the medical lifting sling market in 2025, whereas home-care and long-term care settings record an 11.02% CAGR through 2031.

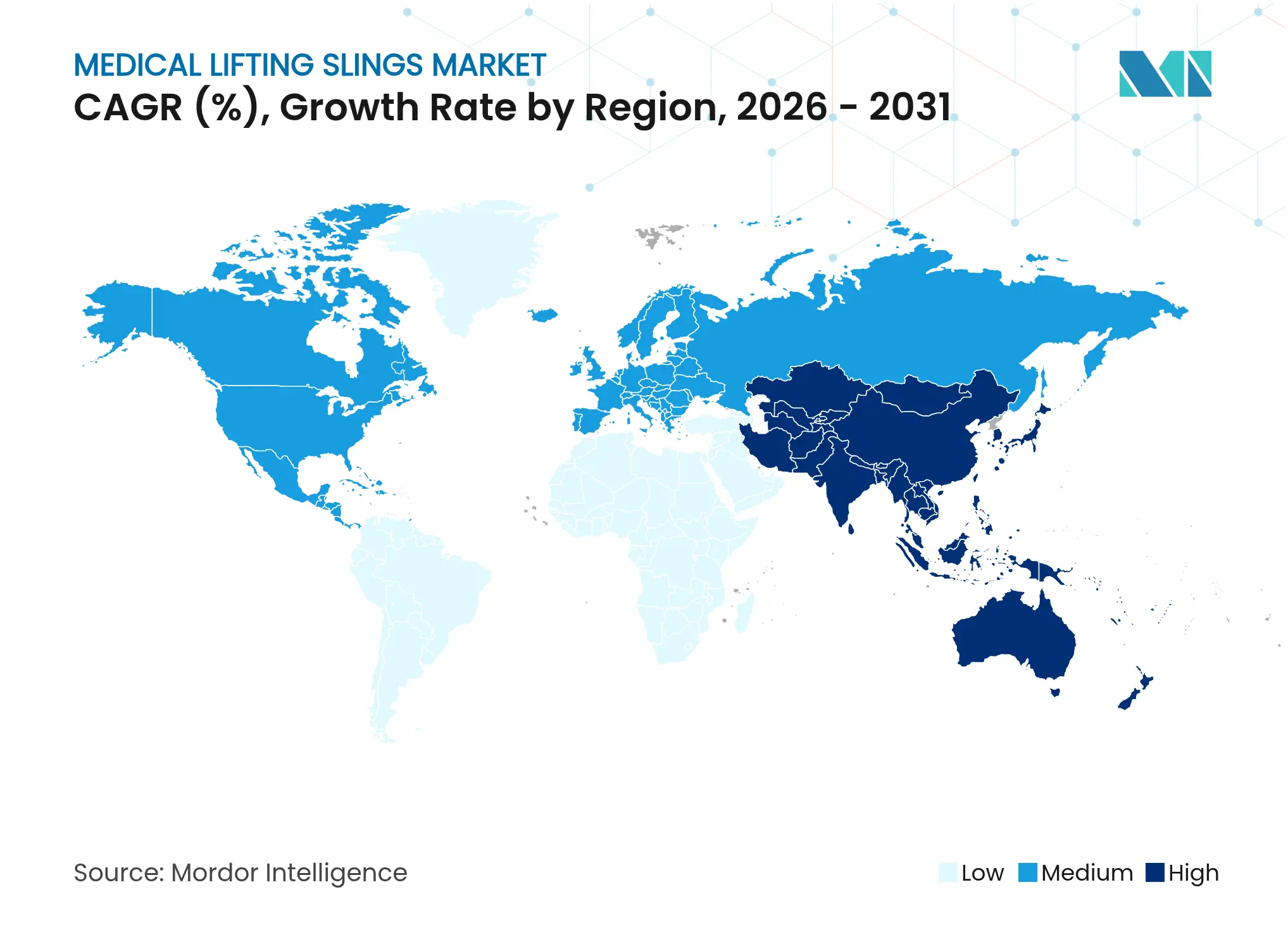

- By geography, North America captured 34.37% of the medical lifting sling market size in 2025; Asia-Pacific registers the fastest 11.21% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Lifting Slings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapidly Ageing Population & Chronic Lifestyle Diseases

Rapidly Ageing Population & Chronic Lifestyle Diseases

| +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:+1.2% | Geographic Relevance:

Global, with concentration in North America & Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Shift To Home-Healthcare & Long-Term Care Settings

Shift To Home-Healthcare & Long-Term Care Settings

| +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Stricter Safe-Patient-Handling Regulations In Hospitals

Stricter Safe-Patient-Handling Regulations In Hospitals

| +0.9% | Global, led by developed markets | Short term (≤ 2 years) | |||

Reimbursement Expansion For Durable Medical Equipment

Reimbursement Expansion For Durable Medical Equipment

| +1.1% | North America, selective EU markets | Medium term (2-4 years) | |||

Rental / Subscription Models Unlocking SMB Adoption

Rental / Subscription Models Unlocking SMB Adoption

| +0.7% | Global, with early adoption in North America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapidly Ageing Population & Chronic Lifestyle Diseases

Across developed economies, older adults and patients with diabetes or cardiovascular disease require frequent assisted transfers, driving sustained demand for the medical lifting sling market. Mechanical slings reduce caregiver injuries and elevate patient safety, particularly in long-term care environments where bariatric and complex positioning needs are common.

Shift to Home-Healthcare & Long-Term Care Settings

Medicare’s 2025 home health payment update raises reimbursements 2.7% and obliges agencies to assess mobility-care capacity before accepting referrals, stimulating purchases of compact, caregiver-friendly devices[1]Centers for Medicare & Medicaid Services, “CY 2025 Home Health Prospective Payment System Rate Update,” federalregister.gov. The medical lifting sling market responds with portable frames and intuitive sling designs suited for non-professional users.

Stricter Safe-Patient-Handling Regulations in Hospitals

NIOSH and OSHA guidelines have evolved into enforceable requirements, compelling facilities to install certified lifting systems for transfers above set weight thresholds[2]Centers for Disease Control and Prevention, “About Safe Patient Handling and Mobility,” cdc.gov. Compliance fuels equipment replacement cycles and spurs demand for slings meeting FDA low-transfer-height standards.

Reimbursement Expansion for Durable Medical Equipment

New HCPCS codes for powered patient-handling aids classify many sling systems as medically necessary, widening insurance coverage and supporting steady growth in the medical lifting sling market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High Upfront Cost & Limited Staff Training

High Upfront Cost & Limited Staff Training

| -0.6% | Global, more pronounced in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-0.6%

| Geographic Relevance:

Global, more pronounced in emerging markets

| Impact Timeline:

Short term (≤ 2 years)

|

Patient Discomfort & Cultural Reluctance

Patient Discomfort & Cultural Reluctance

| -0.4% | Global, varying by cultural context | Long term (≥ 4 years) | |||

Infection-Control Mandates Favouring Single-Use Slings

Infection-Control Mandates Favouring Single-Use Slings

| -0.3% | Global, led by developed healthcare systems | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

High Upfront Cost & Limited Staff Training

Sling systems demand capital expenditure and ongoing education; under-trained staff often underuse installed devices, limiting near-term uptake despite long-run safety payoffs.

Patient Discomfort & Cultural Reluctance

Perceptions of dignity and independence influence acceptance, especially in home settings where familial preferences steer equipment choice, tempering broader adoption of the medical lifting sling market in certain regions.

Segment Analysis

By Product: Bariatric Solutions Drive Specialized Growth

Seating and full-body products held 36.82% of 2025 revenue due to versatility across departments, yet bariatric and bari-plus models are climbing at an 10.79% CAGR as obesity prevalence rises. The medical lifting sling market size for bariatric solutions is forecast to expand swiftly because patients exceeding 180 kg require reinforced fabrics and wider geometry. Standing and universal U-shape variants satisfy rehabilitation centers, whereas transfer sheets enhance lateral moves in ICUs. Pediatric and specialty slings occupy niche volume but enjoy stable demand from children’s hospitals.

The product mix exemplifies tailored care: facilities match sling characteristics to body habitus, medical condition, and transfer scenario. Suppliers differentiate through ergonomic padding, pressure-distribution fabrics, and modular loop-strap systems. Smart sensors integrated into certain bariatric devices capture usage metrics, easing audits for safe-patient-handling compliance and deepening data-driven purchasing within the medical lifting sling market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Technical Textiles Gain Antimicrobial Edge

Polyester contributes 68.11% share because of durability and wash-fastness, anchoring cost-efficient fleet management in large hospitals. Antimicrobial technical fabrics register a 10.42% CAGR as silver-ion or copper-fiber treatments deliver ≥99% bacterial log-kill without compromising breathability. Mesh and spacer fabrics improve airflow to protect fragile skin, while nylon reinforces bariatric weight loads. Quilted blends provide comfort during extended immobilization. Environmental targets push suppliers to develop recyclable composites, although price premiums restrain near-term conversion outside high-infection-risk units.

Technical advances support infection-control savings: fewer laundering cycles and shorter turnaround times translate to operational efficiencies, strengthening hospital value propositions within the broader medical lifting sling market.

By Usage Type: Disposable Adoption Accelerates

Reusable slings continue to account for 63.05% of units in 2025, favored by high-throughput hospitals with on-site laundries. Still, infection-prevention strategies raise disposable uptake at a 9.11% CAGR, especially in oncology, transplant, and isolation wards. Guidance on reprocessed single-use devices complicates reuse, nudging administrators toward single-patient options. Consequently, procurement teams increasingly weigh contamination risk, laundering cost, and sustainability targets when determining sling mix, fostering segmentation sophistication inside the medical lifting sling market.

Note: Segment shares of all individual segments available upon report purchase

By End User: Home Care Expansion Reshapes Demand

Hospitals and surgical centers presently hold 56.14% revenue share yet face flat population growth. Conversely, home-health and long-term care facilities grow 11.02% annually, boosted by Medicare policy shifts, aging-in-place preferences, and workforce shortages in institutional care. Manufacturers respond with space-saving mobile lifts and intuitive slings operable by family caregivers, widening the addressable medical lifting sling market.

Geography Analysis

North America generates 34.37% of global revenue. Mature reimbursement, strict OSHA enforcement, and a growing senior population sustain equipment renewal cycles. Canada’s public health insurers fund ceiling lifts in long-term care, while Mexico accelerates DME procurement under universal coverage initiatives. Regulatory updates mandating 17-inch low transfer heights spur design upgrades, bolstering the region’s contribution to the medical lifting sling market.

Asia-Pacific achieves the fastest 11.21% CAGR as China, Japan, and India upscale hospital infrastructure and adopt Western safe-handling standards. Demographic aging collides with smaller family units, increasing institutional-care reliance and fueling purchases of modern lifting slings. Local producers emphasize cost-effective polyester and nylon blends, yet premium imported antimicrobial fabrics are winning share in top-tier urban hospitals, enlarging the medical lifting sling market footprint.

Europe maintains moderate growth. Universal healthcare and EU worker-safety directives keep baseline demand stable, while Eastern European modernization adds incremental volume. Brexit prompts U.K. providers to re-validate CE-marked devices, creating short-term uncertainty yet medium-term opportunities for agile suppliers. Population aging and rising bariatric admissions underpin steady needs across the medical lifting sling market.

Competitive Landscape

Market Concentration

The sector remains moderately fragmented. Global leaders ARJO, Hillrom Services (Baxter), and Invacare leverage integrated platforms, training programs, and service contracts to protect share. Niche innovators such as Silvalea (acquired by Savaria) specialize in custom slings spanning 800 designs, reinforcing customer lock-in for complex cases. Product roadmaps emphasize smart textiles with RFID tracking, antimicrobial coatings, and sensor-enabled load monitoring that streamline audits.

Strategic activity intensifies. StarFish Medical’s 2024 acquisition of Omnica adds design resources for single-use and surgical slings, while RoundTable’s 2025 investment in EHOB broadens pressure-injury prevention portfolios. Suppliers also pilot subscription and equity-rental schemes targeting mid-sized facilities reluctant to commit capital upfront, expanding reach across the medical lifting sling market.

Medical Lifting Slings Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: StarFish Medical acquired California-based Omnica Corporation, adding disposable-device engineering capabilities.

- November 2024: CMS finalized the 2025 Home Health Prospective Payment System, raising rates 2.7% and adding capacity-assessment rules.

Table of Contents for Medical Lifting Slings Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rapidly Ageing Population & Chronic Lifestyle Diseases

- 4.2.2Shift To Home-Healthcare & Long-Term Care Settings

- 4.2.3Stricter Safe-Patient-Handling Regulations In Hospitals

- 4.2.4Reimbursement Expansion For Durable Medical Equipment

- 4.2.5Rental / Subscription Models Unlocking SMB Adoption

- 4.3Market Restraints

- 4.3.1High Upfront Cost & Limited Staff Training

- 4.3.2Patient Discomfort & Cultural Reluctance

- 4.3.3Infection-Control Mandates Favouring Single-Use Slings

- 4.4Porter's Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Standing Slings

- 5.1.2Seating / Full-Body Slings

- 5.1.3Universal U-shape Slings

- 5.1.4Bariatric & Bari-plus Slings

- 5.1.5Transfer Sheets & Slide Slings

- 5.1.6Specialty & Paediatric Slings

- 5.2By Material

- 5.2.1Polyester

- 5.2.2Padded / Quilted

- 5.2.3Mesh / Spacer-fabric

- 5.2.4Nylon

- 5.2.5Technical Textiles

- 5.3By Usage Type

- 5.3.1Disposable (Single-patient)

- 5.3.2Reusable / Launderable

- 5.4By End User

- 5.4.1Hospitals & Surgical Centres

- 5.4.2Home-Care & Long-Term-Care Facilities

- 5.4.3Rehabilitation Centres

- 5.4.4Emergency Medical Services / Ambulance

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1ARJO

- 6.3.2Baxter International (Hillrom Services Inc.)

- 6.3.3Invacare Corporation

- 6.3.4Drive DeVilbiss Healthcare

- 6.3.5Etac AB (Molift)

- 6.3.6Joerns Healthcare LLC

- 6.3.7Guldmann Inc.

- 6.3.8Bestcare LLC

- 6.3.9Medline Industries LP

- 6.3.10GF Health Products Inc.

- 6.3.11Prism Medical Ltd.

- 6.3.12Sunrise Medical LLC

- 6.3.13Vancare Inc.

- 6.3.14Handicare Group AB

- 6.3.15NAUSICAA Medical

- 6.3.16Winncare Group

- 6.3.17HoverTech International

- 6.3.18SPH Medical

- 6.3.19Med-Mizer Inc.

- 6.3.20UpLyft Inc.

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product

- Standing Slings

- Seating / Full-Body Slings

- Universal U-shape Slings

- Bariatric & Bari-plus Slings

- Transfer Sheets & Slide Slings

- Specialty & Paediatric Slings

- Standing Slings

- By Material

- Polyester

- Padded / Quilted

- Mesh / Spacer-fabric

- Nylon

- Technical Textiles

- Polyester

- By Usage Type

- Disposable (Single-patient)

- Reusable / Launderable

- Disposable (Single-patient)

- By End User

- Hospitals & Surgical Centres

- Home-Care & Long-Term-Care Facilities

- Rehabilitation Centres

- Emergency Medical Services / Ambulance

- Hospitals & Surgical Centres

- Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- China

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Our Medical Lifting Slings Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.27 B (2025) | Mordor Intelligence | Anonymized source:Mordor Intelligence | Primary gap driver: | |

USD 1.01 B (2023) | Global Consultancy A | Omits disposable slings and home-care demand; relies on 2023 hospital procurement snapshot | ||

USD 0.56 B (2025) | Trade Journal B | Counts only single-use units and excludes Asia-Pacific; unit-shipment × ASP approach lacks revenue reconciliation |