Vaginal Rejuvenation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

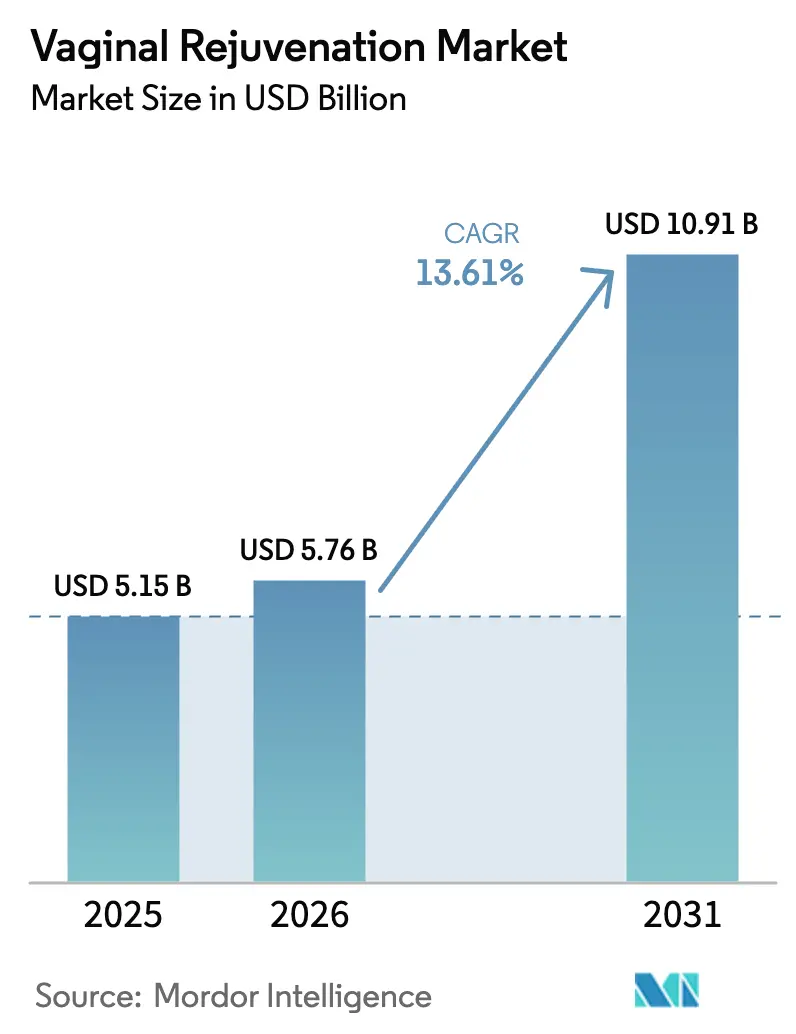

| Market Size (2026) | USD 5.76 Billion |

| Market Size (2031) | USD 10.91 Billion |

| Growth Rate (2026 - 2031) | 13.61% CAGR |

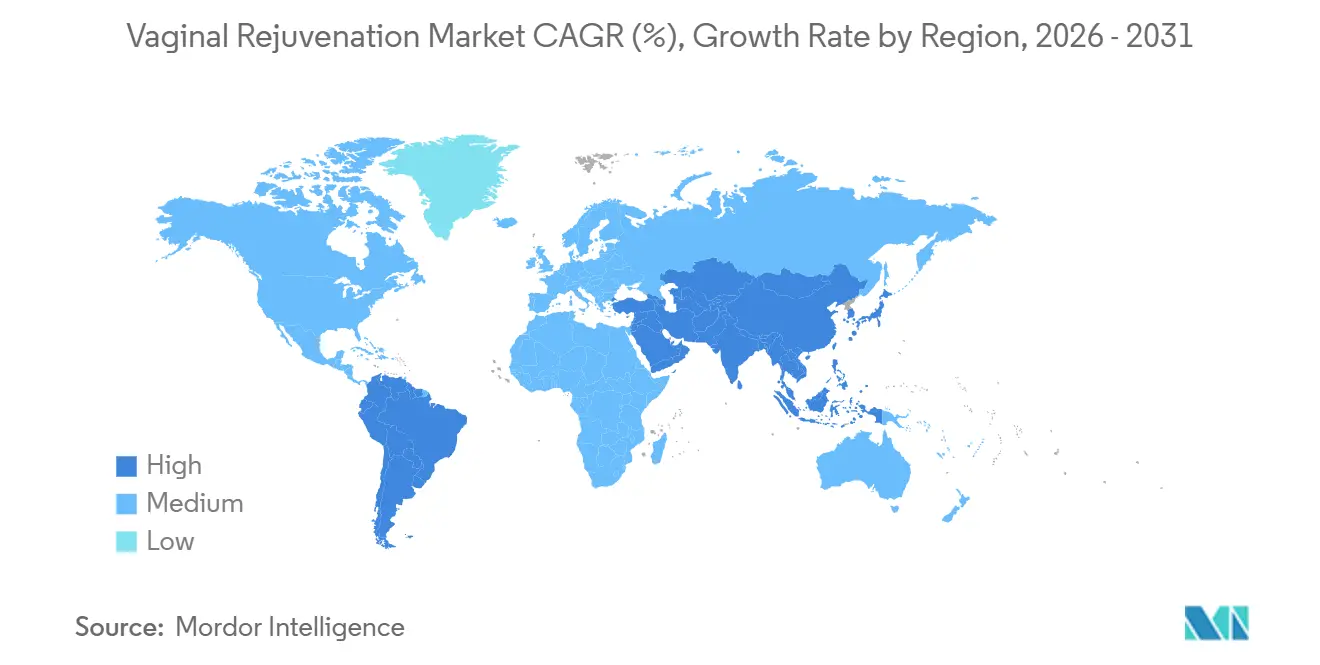

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

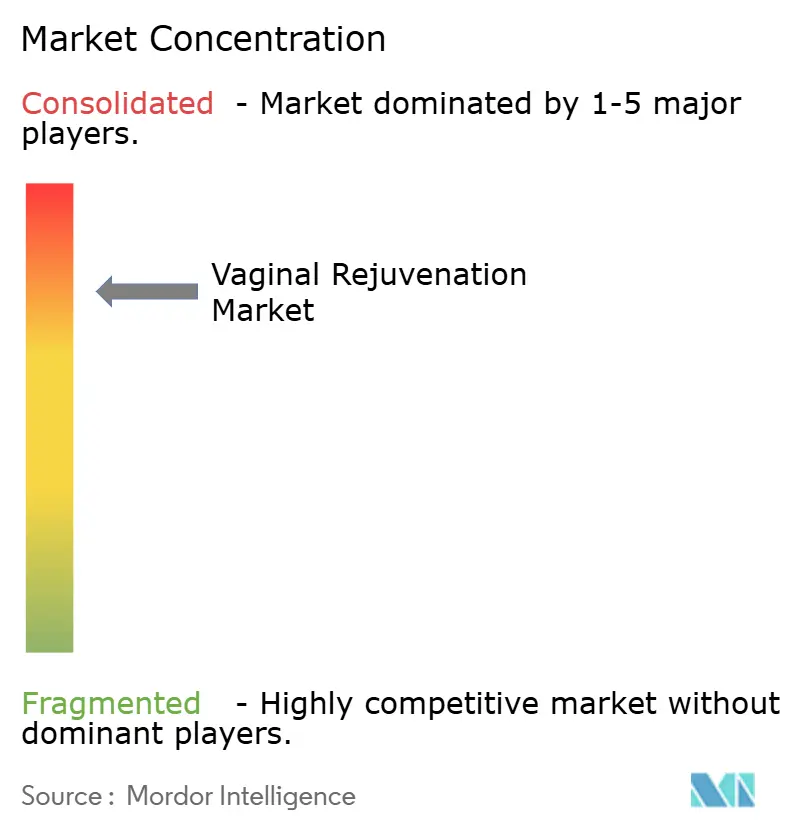

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vaginal Rejuvenation Market Analysis by Mordor Intelligence

The Vaginal Rejuvenation Market size is expected to increase from USD 5.15 billion in 2025 to USD 5.76 billion in 2026 and reach USD 10.91 billion by 2031, growing at a CAGR of 13.61% over 2026-2031.

Device innovation, a growing population of women over 50, and wider clinical acceptance of energy-based modalities are accelerating adoption despite fragmented regulation. Cosmetic procedures remain the prime revenue engine as wellness spending rises, while reconstructive indications create a hedge against regulatory pushback. Hospitals dominate revenue today because reimbursement pathways for functional repair favor inpatient settings, yet ambulatory surgical centers (ASCs) are quickly scaling as they unbundle cosmetic sessions from hospital overhead. Competitive intensity stays high, with firms differentiating on radiofrequency versus CO₂ laser platforms and on hybrid treatment bundles that combine pelvic-floor electromagnetic stimulation with laser consoles.

Key Report Takeaways

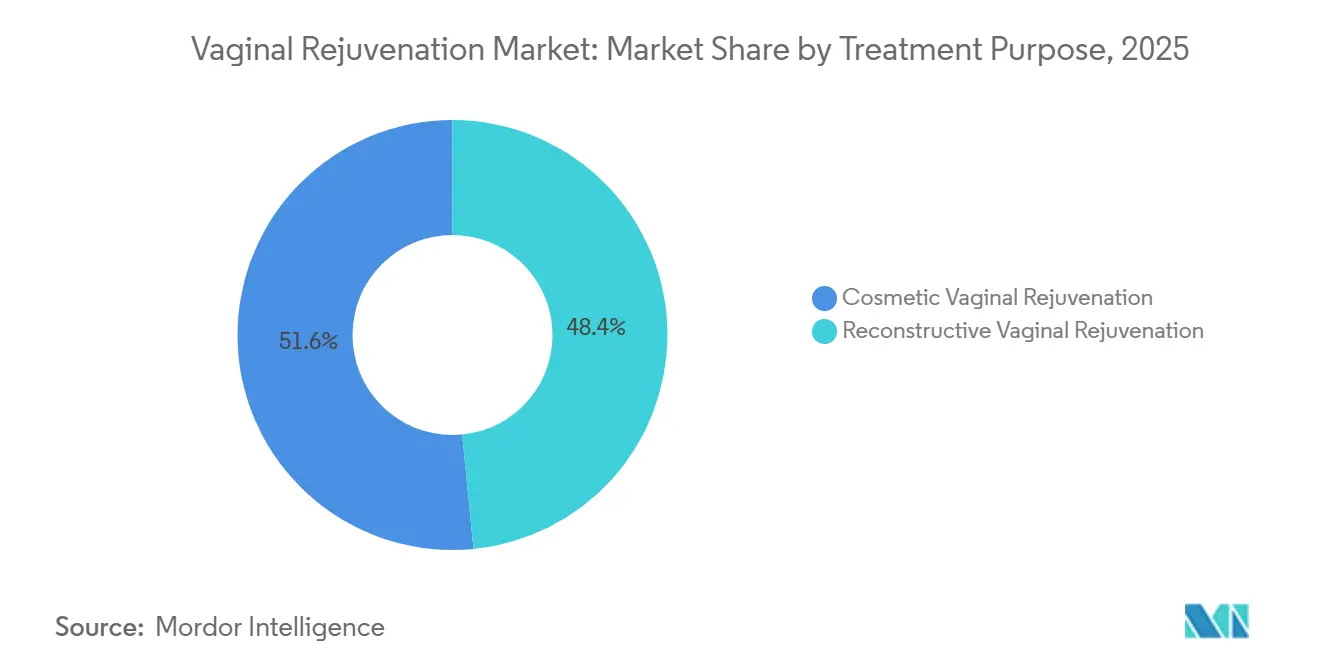

- By treatment purpose, cosmetic procedures held 51.56% of vaginal rejuvenation market share in 2025 and are expanding at a 16.02% CAGR through 2031.

- By modality, energy-based devices accounted for 44.74% of revenue in 2025 and are growing at a 17.25% CAGR to 2031.

- By end user, hospitals controlled 61.23% of revenue in 2025, while ASCs post the fastest growth at 15.33% through 2031.

- By geography, North America delivered 41.11% of global revenue in 2025, whereas Asia-Pacific registers the highest regional CAGR at 15.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vaginal Rejuvenation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for energy-based treatments | 2.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Increasing adoption of non-invasive gynecological procedures | 2.5% | Global, particularly APAC and Middle East emerging markets | Long term (≥ 4 years) |

| Rising disposable incomes & aesthetic awareness | 2.1% | APAC core (China, India, South Korea), spill-over to Middle East | Long term (≥ 4 years) |

| Integration of pelvic-floor digital therapeutics & EMS chair devices | 1.9% | North America and Europe, early APAC adopters | Medium term (2-4 years) |

| Uro-gynecologic crossover (stress-urinary-incontinence synergy) | 1.7% | Global, with reimbursement pathways in North America and Europe | Short term (≤ 2 years) |

| Menopause-tech platforms bundling laser sessions | 1.4% | North America, Western Europe, urban APAC hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Energy-Based Treatments

Energy-based platforms such as CO₂ lasers, erbium:YAG systems, radiofrequency devices, and high-intensity focused ultrasound are displacing surgical vaginoplasty because they offer shorter recovery, minimal scarring, and same-day discharge. A 2025 study showed platelet-rich plasma with hyaluronic acid outperformed topical estrogen for vulvovaginal atrophy, highlighting the value of adjunct biologics.[1]Ufuk Atlihan, “Comparison of Topical Estrogen and Platelet-Rich Plasma Injections in the Treatment of Postmenopausal Vaginal Atrophy,” Frontiers in Medicine, frontiersin.org InMode’s women’s health portfolio grew 19% year over year in Q3 2024, validating commercial demand despite regulatory caution. Yet no energy-based device carries explicit FDA clearance for cosmetic vaginal indications, and an International Menopause Society white paper reported randomized trials that failed to prove laser superiority over sham, a gap that limits reimbursement.[2]Ann-Sophie Page, “Laser Versus Sham for Genitourinary Syndrome of Menopause: A Randomised Controlled Trial,” BJOG, pubmed.ncbi.nlm.nih.gov

Increasing Adoption of Non-Invasive Gynecological Procedures

Office-based treatments reshape patient expectations and clinic economics. The American Society of Plastic Surgeons logged 10,827 labiaplasties in 2024, a 2% rise from the prior year. Radiofrequency systems such as Hologic’s TempSure Vitalia deliver controlled thermal energy without incisions, allowing quick turnaround sessions. A 2024 meta-analysis ranked high-intensity focused electromagnetic therapy among the top interventions for stress urinary incontinence, aligning muscle-stimulation chairs with vaginal rejuvenation packages.[3]Chiara Leonardo, “High-Intensity Focused Electromagnetic Technology for Urinary Incontinence: A Systematic Review,” Frontiers in Medicine, frontiersin.orgHowever, NICE guidance still favors vaginal estrogen and recommends lasers only in research protocols, so payer coverage remains limited.

Rising Disposable Incomes and Aesthetic Awareness

Wealth creation in China, India, and South Korea fuels demand for procedures once confined to Western clinics. China reclassified radiofrequency devices to Class III in 2024, delaying market entry until firms secure new clinical approvals. Japanese device maker Ya-Man saw China sales fall 37% after the rule shift, showing revenue sensitivity to policy swings. Meanwhile, a Beijing-made Nd:YAG laser won U.S. FDA 510(k) clearance in March 2025, signaling that Chinese manufacturers will pursue higher-margin export market. Social stigma still limits uptake in conservative areas, so vendors invest in culturally attuned marketing and training.

Integration of Pelvic-Floor Digital Therapeutics and EMS Chair Devices

High-intensity focused electromagnetic chairs such as BTL Emsella strengthen pelvic muscles without patients needing to undress, bridging physiotherapy and aesthetics. A 2025 systematic review recorded significant reductions in urinary-incontinence episodes after HIFEM sessions. Clinics bundle chair programs with radiofrequency or laser treatments, enlarging per-patient revenue streams. Digital therapeutics add remote coaching and subscription billing, yet reimbursement covers only medically coded stress-incontinence use, so cosmetic indications remain self-pay.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory scrutiny & uncertain approvals | -2.3% | Global, with North America, Europe, and Australia most affected | Short term (≤ 2 years) |

| Social stigma & ethical debate | -1.6% | Middle East, parts of APAC, and conservative regions in North America | Long term (≥ 4 years) |

| Escalating litigation & liability-insurance premiums | -1.2% | North America and Europe, with spillover to other developed markets | Medium term (2-4 years) |

| Digital-advertising restrictions on "vaginal-rejuvenation" claims | -0.9% | Global, particularly platforms operating in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Scrutiny and Uncertain Approvals

The FDA issued 2018 warning letters to seven manufacturers and has not cleared any laser or radiofrequency system specifically for cosmetic vaginal use. Australia canceled all devices from its register in November 2024, citing safety concerns. China elevated radiofrequency beauty devices to Class III in 2024, creating a compliance bottleneck until April 2026. The European Union’s Medical Device Regulation heightens post-market surveillance demands, raising cost and delaying launches.

Social Stigma and Ethical Debate

The American College of Obstetricians and Gynecologists warns that vaginal rejuvenation may medicalize normal anatomy. In conservative regions, patients often seek functional diagnoses to avoid social judgment, complicating consent. A British Medical Journal article detailed HIV transmission from unlicensed platelet-rich plasma injections, underscoring reputational risk. Manufacturers counter by sponsoring patient-education campaigns and collaborating with professional societies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Purpose: Cosmetic Demand Leads, Reconstructive Builds Resilience

Cosmetic procedures captured 51.56% of revenue in 2025, reflecting strong interest in aesthetic genital care. That slice of vaginal rejuvenation market share expands as social acceptance widens and ASCs lower entry costs. Cosmetic sessions often utilize energy-based devices that shorten recovery, allowing clinics to schedule higher daily volumes. Reconstructive indications, including pelvic-organ prolapse repair and stress-urinary-incontinence management, draw reimbursement but grow slower because payers mandate stricter evidence. Breast-cancer survivors and post-menopausal patients drive reconstructive demand, creating overlap across care pathways. Manufacturers now design single consoles usable in both cohorts, protecting revenue against shifts in payer policy. Despite the momentum, NICE still advises estrogen first for urogenital atrophy, constraining reconstructive growth in the United Kingdom. Continued multicenter trials are required to unlock wider coverage and accelerate adoption.

The cosmetic segment continues to command premium pricing, enabling higher margins even when procedure volumes fluctuate. Word-of-mouth and influencer endorsements play a disproportionate role in patient acquisition, and clinics differentiate through bundled offerings that include topical products and at-home pelvic-floor devices. On the reconstructive side, surgeons emphasize durability and functional outcomes, favoring modalities with published long-term data. As evidence matures, especially around combined radiofrequency and platelet-rich plasma protocols, the reconstructive share of the vaginal rejuvenation market could rise, but near-term growth remains anchored in cosmetics.

By Modality: Energy-Based Devices Dominate Growth Trajectory

Energy-based platforms generated 44.74% of 2025 revenue and post the fastest 17.25% CAGR, underscoring their central role in the vaginal rejuvenation market. CO₂ lasers hold the largest installed base thanks to early movers such as Lumenis and Cynosure, yet radiofrequency devices gain momentum because they heat tissue without ablation, lowering complication risk. Er:YAG systems offer precise thermal profiles with less collateral damage, appealing to risk-averse practitioners. High-intensity focused ultrasound remains niche, but ongoing thermal-science studies may broaden its clinical rationale. Surgical vaginoplasty remains the standard for severe laxity, though demand is limited by higher costs and downtime. Injectable biologics like platelet-rich plasma and crosslinked hyaluronic acid deliver complementary benefits, with a 2025 trial showing superior outcomes to topical estrogen. Still, inconsistent regulation and variable technique limit widespread adoption. Over-the-counter pelvic-floor trainers and HIFEM chairs occupy the self-care corner of the vaginal rejuvenation market, offering non-invasive alternatives that broaden the funnel for in-clinic services.

Capital expenditure dynamics influence modality mix: lasers and radiofrequency consoles carry higher upfront costs but allow billing across multiple indications, improving return on investment. Vendors bundle software upgrades and consumable tips under subscription models, smoothing clinic cash flows. Competition pushes rapid feature releases, including real-time thermal feedback and AI-assisted treatment planning. These improvements build practitioner confidence and reinforce the transition from surgical to energy-based care.

By End User: Hospitals Maintain Control, ASCs Accelerate Expansion

Hospitals accounted for 61.23% of revenue in 2025, as reconstructive procedures such as pelvic-organ prolapse repair require full operating-room resources. Complex cases receive insurance coverage when coded as functional repair, reinforcing hospital dominance. Nonetheless, ASCs post a 15.33% CAGR to 2031 because they cater to self-pay cosmetic patients seeking discreet, efficient experiences. ASCs invest in multifunction energy-based consoles and HIFEM chairs, enabling high patient throughput and packaged pricing. Specialty uro-gynecology and aesthetic clinics occupy a middle ground, combining reconstructive capability with spa-like amenities, and they leverage social-media branding to attract niche demographics.

Direct-to-consumer e-commerce remains minor, limited to pelvic-floor trainers, topical moisturizers, and subscription telehealth services. Yet digital menopause platforms may redirect patient flow toward partner clinics that offer bundled laser sessions, expanding the referral ecosystem. Reimbursement diversity across end-user settings shapes pricing power: hospitals rely on insurance codes, whereas ASCs and clinics depend on transparent self-pay fees. This divergence influences technology procurement, with hospital committees emphasizing clinical evidence and ASCs prioritizing patient experience.

Geography Analysis

North America contributed 41.11% of 2025 revenue thanks to high disposable incomes, widespread aesthetic-clinic infrastructure, and relatively permissive regulation that stops short of outright bans. Median menopause age is 52, and surgical menopause adds to the candidate pool, sustaining demand for both cosmetic and functional care. InMode’s women’s health division booked USD 73.5 million in Q3 2024, signaling robust device utilization across U.S. and Canadian centers. FDA warning letters dampen marketing claims but have not halted procedure volume. Mexico benefits from cross-border medical tourism, offering cost-effective cosmetic packages to U.S. residents.

Asia-Pacific records the fastest regional CAGR at 15.21%, driven by rising incomes and urbanization. China’s Class III reclassification delays new radiofrequency launches, giving early-certified firms an advantage. Indian metros and South Korean specialty clinics showcase rapid adoption, while Australia’s November 2024 device cancellation shifts demand to neighboring countries with lighter oversight. Local distributors tailor marketing to cultural sensitivities, an essential strategy because stigma still suppresses uptake outside major cities.

Europe holds a mid-tier share, with Germany, the United Kingdom, France, Italy, and Spain as lead markets. The EU Medical Device Regulation tightens evidence and post-market surveillance, delaying some device renewals. The United Kingdom’s NICE guidance recommends lasers only inside research protocols, tempering growth in reconstructive indications. Vendors seek CE certification for combination radiofrequency and electromagnetic field systems, such as Venus Fiore, to diversify revenue streams across European and Latin American markets. Middle East and Africa plus South America represent emerging markets where medical tourism and affluent local populations drive niche demand. Nevertheless, social conservatism and limited reimbursement slow broad expansion.

Competitive Landscape

The vaginal rejuvenation market remains fragmented. InMode, Hologic (Cynosure), BTL Industries, Alma Lasers, and Fotona compete on core technology and on bundled treatment ecosystems. InMode’s EmpowerRF console integrates internal and external radiofrequency applicators with electromagnetic pelvic-floor stimulation, helping clinics cross-sell multiple procedures per patient. Hologic leverages TempSure Vitalia inside broader OB/GYN relationships, while BTL bundles Emsella chairs with Exilis facial-body contouring systems to maximize capital-equipment ROI. Fotona positions Er:YAG platforms for precise tissue interaction, capturing surgeons wary of thermal injury risk.

Clinical evidence and regulatory compliance emerge as decisive differentiators. Larger companies finance multicenter trials, real-world data registries, and post-market safety surveillance, activities that smaller rivals struggle to match. Viveve Medical’s failure to meet trial endpoints illustrates the high bar for demonstrating durable outcomes and the financial vulnerability of under-capitalized entrants. Chinese manufacturers such as Beijing Nubway pursue FDA clearance to gain credibility and enter premium export markets, intensifying price competition. Strategic partnerships with digital therapeutic platforms and menopause-focused telehealth companies further redefine the competitive field, creating vertically integrated care pathways that generate recurring revenue beyond the initial console sale.

Vaginal Rejuvenation Industry Leaders

Alma Lasers

ThermiGen LLC

Venus Concept

Lutronic

Viveve

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Genitique Clinic introduced Thailand’s first Ladylift fibre laser, offering non-surgical intimate rejuvenation.

- September 2025: Australia’s Therapeutic Goods Administration canceled all vaginal rejuvenation devices from the national register, citing safety concerns.

- June 2025: FIGO’s ethics committee published a statement in the International Journal of Gynecology & Obstetrics urging caution around cosmetic genital procedures.

Global Vaginal Rejuvenation Market Report Scope

As per the scope, vaginal rejuvenation deals with vaginal corrective treatments such as vaginal tightness and urinary incontinence. Vaginal rejuvenation is generally performed to address or treat various vaginal problems that occur after a child's birth or due to the aging process and include conditions such as laxity of the vagina, stress urinary incontinence, and lack of lubrication.

The Vaginal Rejuvenation Market is Segmented by Treatment purpose, modality, end user and geography. By Treatment Purpose, market is segmented into Cosmetic, Reconstructive. By Modality, market is segmented into Surgical, Energy-Based Devices, Injectable/Biologic Therapies, OTC & Pelvic-Floor Devices. By End User, market is segmented into Hospitals, ASCs, Specialty Clinics, DTC/E-commerce. By Geography, market is segmented into North America, Europe, APAC, MEA, South America. The Market report also covers the estimated market sizes and trends of 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Cosmetic Vaginal Rejuvenation |

| Reconstructive Vaginal Rejuvenation |

| Surgical Procedures | |

| Energy-Based Devices | CO₂ Laser Systems |

| Er:YAG Laser Systems | |

| Radio-frequency Devices | |

| High-Intensity Focused Ultrasound (HIFU) | |

| Injectable / Biologic Therapies (PRP, Stem-cell, Fillers) | |

| OTC & Pelvic-Floor Devices |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Aesthetic & Uro-gynecology Clinics |

| Direct-to-Consumer / E-commerce |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Purpose | Cosmetic Vaginal Rejuvenation | |

| Reconstructive Vaginal Rejuvenation | ||

| By Modality | Surgical Procedures | |

| Energy-Based Devices | CO₂ Laser Systems | |

| Er:YAG Laser Systems | ||

| Radio-frequency Devices | ||

| High-Intensity Focused Ultrasound (HIFU) | ||

| Injectable / Biologic Therapies (PRP, Stem-cell, Fillers) | ||

| OTC & Pelvic-Floor Devices | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Aesthetic & Uro-gynecology Clinics | ||

| Direct-to-Consumer / E-commerce | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the vaginal rejuvenation market in 2026?

The vaginal rejuvenation market size is USD 5.76 billion in 2026 and is forecast to reach USD 10.91 billion by 2031.

Which segment grows fastest within the market?

Energy-based devices post the quickest growth at a 17.25% CAGR through 2031.

Which region records the highest CAGR?

Asia-Pacific expands at a 15.21% CAGR, the fastest regional rate over the forecast period.

What share do cosmetic procedures hold?

Cosmetic treatments account for 51.56% of 2025 revenue and continue to lead growth.

What is the main regulatory challenge?

The main regulatory challenge is the lack of specific FDA approval for cosmetic vaginal indications and the 2018 warning letters that limit marketing claims.

Page last updated on: