Vacuum Truck Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.17 Billion |

| Market Size (2030) | USD 3.01 Billion |

| Growth Rate (2025 - 2030) | 6.74% CAGR |

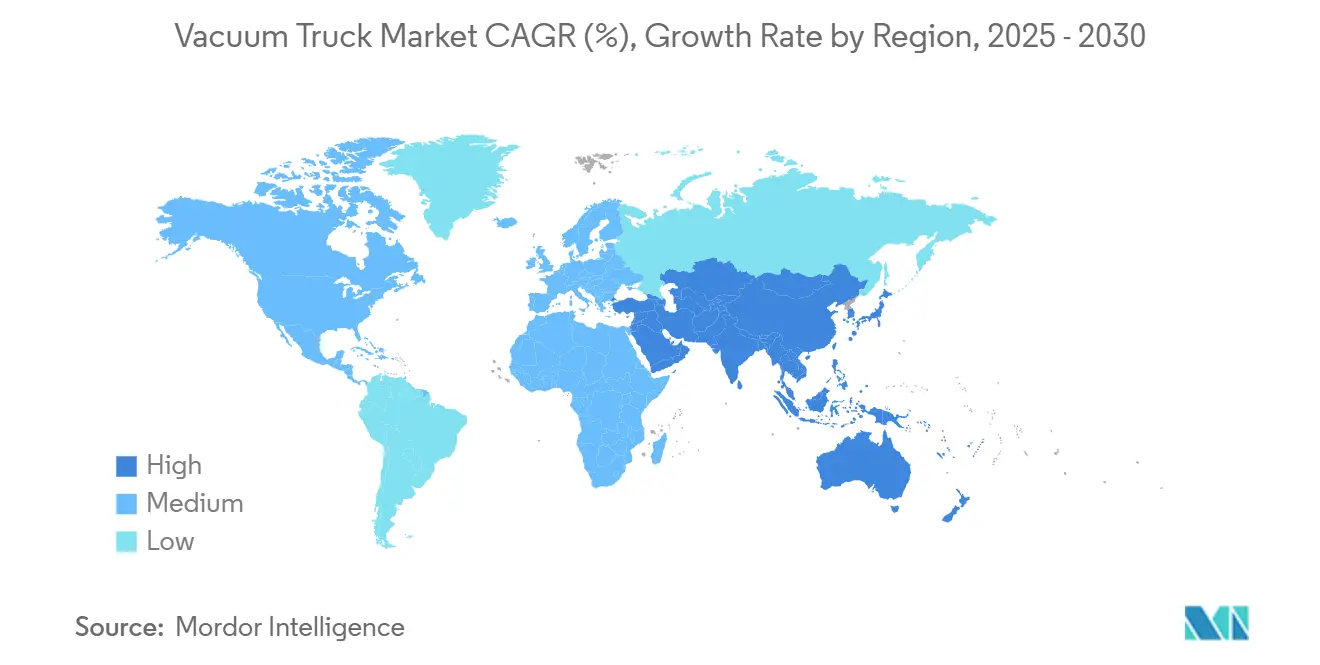

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vacuum Truck Market Analysis by Mordor Intelligence

The Vacuum Truck Market size is estimated at USD 2.17 billion in 2025 and is expected to reach USD 3.01 billion by 2030, at a CAGR of 6.74% during the forecast period (2025-2030). Robust regulatory enforcement on hazardous-waste handling, rapid urban infrastructure upgrades, and mounting demand for non-destructive excavation underpin this growth trajectory. Combination units that handle wet and dry materials dominate new purchases, while dry-only variants see heightened interest from battery-recycling facilities and precision industrial cleaning. Parallel advances in AI-enabled telematics deliver measurable gains in asset utilization, fuel economy, and compliance monitoring, prompting fleet owners to accelerate digital retrofits. Electric propulsion remains a niche but strategically important pathway as European low-emission zones tighten, although payload penalties still temper broad adoption outside municipal duty cycles. The vacuum truck market attracts strategic acquisitions and private-equity investments that consolidate regional fleets, expand product portfolios, and embed data-driven service models.

Key Report Takeaways

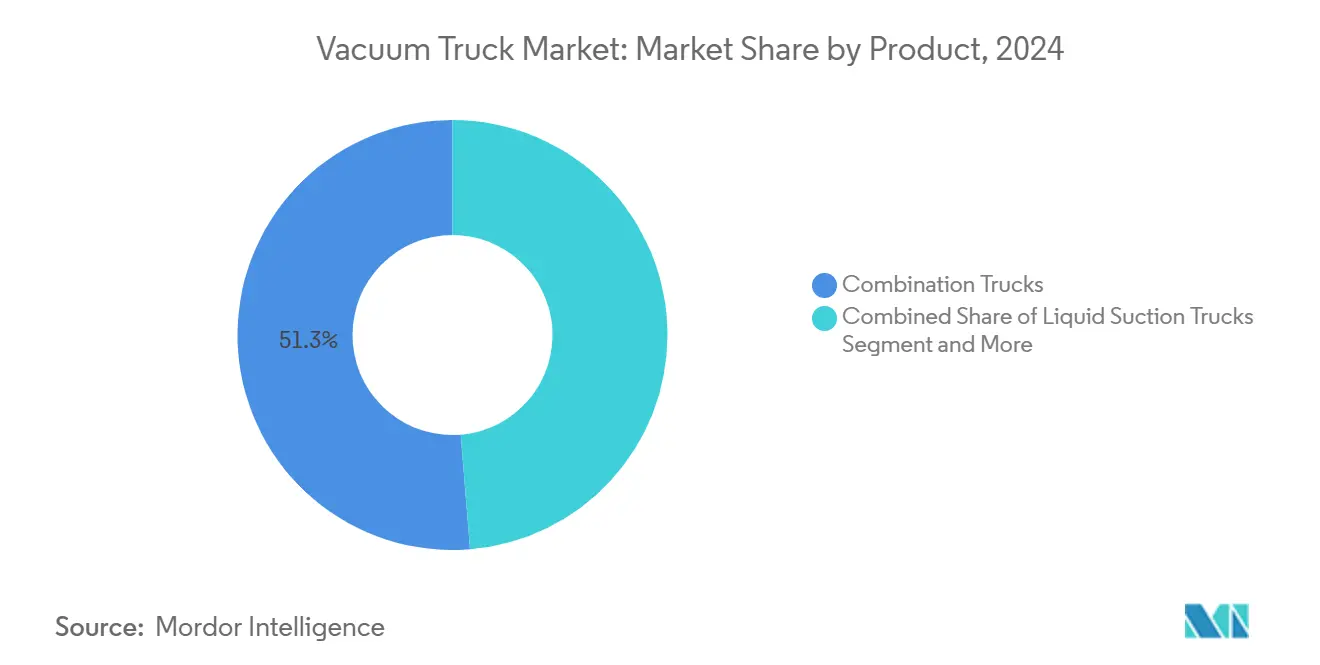

- By product category, combination trucks captured 51.27% of the vacuum truck market share in 2024; dry suction units are forecast to advance at a 6.77% CAGR during the forecast period (2025-2030).

- By fuel type, internal combustion engines held 83.46% share of the vacuum truck market in 2024, while electric variants are projected to scale at a 6.75% CAGR during the forecast period (2025-2030).

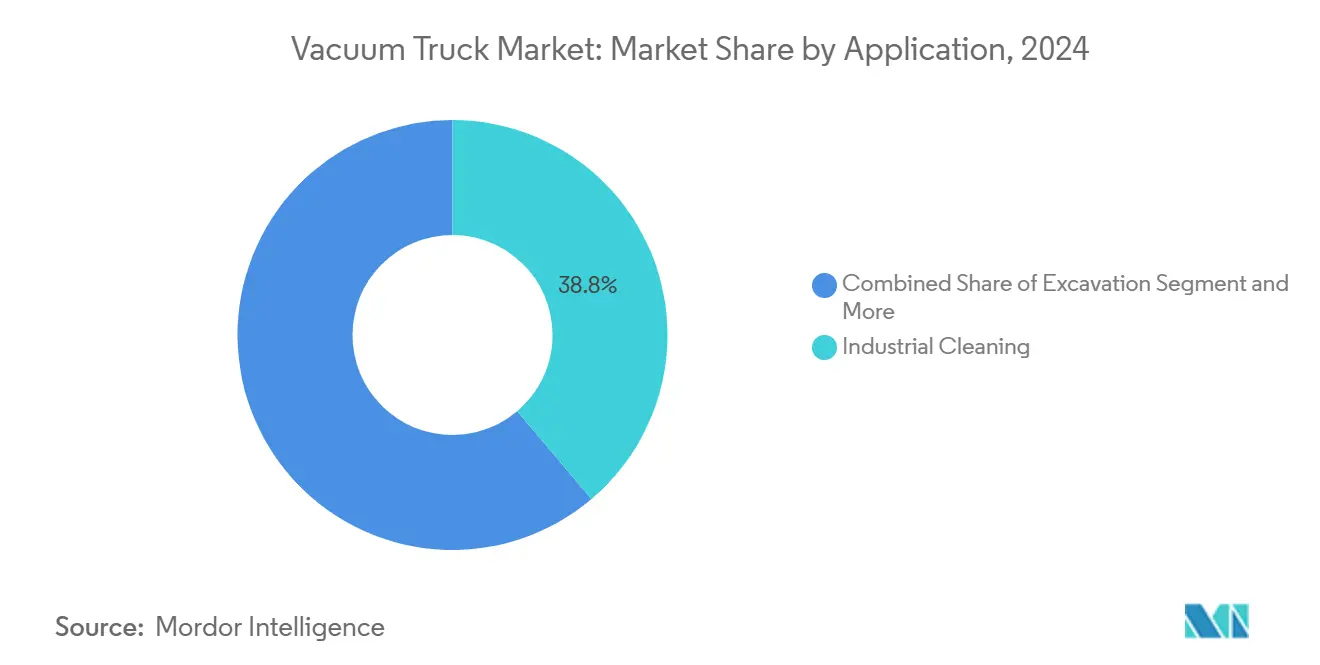

- By application, industrial cleaning accounted for a 38.83% share of the vacuum truck market in 2024, and excavation activities are expected to expand at a 6.78% CAGR during the forecast period (2025-2030).

- By capacity, medium-class trucks led the vacuum truck market with a 46.35% share in 2024; small units are expected to log the highest 6.79% CAGR during the forecast period (2025-2030).

- By region, Europe commanded 36.71% share of the vacuum truck market in 2024, whereas Asia-Pacific is expected to grow at a 6.81% CAGR during the forecast period (2025-2030).

Global Vacuum Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental Regulations | +1.8% | Global, with emphasis on North America and EU | Medium term (2-4 years) |

| Urban Infrastructure Expansion | +1.5% | Asia Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| Industrial Cleaning Outsourcing | +1.2% | Global, concentrated in industrial hubs | Short term (≤ 2 years) |

| AI-Enabled Telematics | +0.9% | North America and EU early adoption | Medium term (2-4 years) |

| 5G Utility-Mapping Mandates | +0.7% | Global, led by developed markets | Medium term (2-4 years) |

| Battery-Recycling Facilities | +0.5% | Global, concentrated in EV manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations on Sludge & Hazardous-Waste Handling

Environmental compliance standards continue to intensify, obliging municipalities and industrial operators to deploy vacuum trucks capable of safely transferring corrosive slurries, PFAS-laden residuals, and lithium-ion black mass. The U.S. Environmental Protection Agency’s updated Coal Combustion Residuals rule and fresh PFAS remediation mandates have already spurred procurement of advanced containment systems that raise unit costs by one-fifth yet remain non-discretionary for permit holders[1]“Hazardous and Solid Waste Management System; Disposal of Coal Combustion Residuals,” Environmental Protection Agency, epa.gov . Tennessee’s wastewater rehabilitation program illustrates how local authorities now embed vacuum extraction capacity into capital plans[2]“State Wastewater Treatment Facility Enforcement Actions,” Tennessee Department of Environment & Conservation, tn.gov . Similar enforcement waves are rolling through the EU’s Urban Waste-Water Treatment Directive revisions, solidifying premium pricing for compliant equipment. Industrial clients increasingly outsource these tasks to avoid liability, expanding the vacuum truck market as service providers scale up fleets and certification programs.

Urban Infrastructure Expansion Boosting Non-Destructive Excavation Demand

Rapid urbanization across Asia-Pacific pushes underground utility corridors to critical density, making hydro-excavation the default method for installing fiber optics, 5G towers, and smart-grid conduits without disrupting service lines. City-center contractors report nighttime vacuum excavation requests rising quarterly as municipal authorities restrict daytime lane closures. Provinces in eastern China and metropolitan regions in India earmark multi-year budgets for water-pipe rehabilitation and storm-drain replacement, both of which require precision potholing. Medium-capacity vacuum trucks serve as multipurpose assets that remove spoil while exposing fragile buried assets, thereby minimizing repair costs and safety incidents. The convergence of permit stipulations, real-time utility mapping, and zero-dig mandates continues to enlarge the addressable vacuum truck market, particularly for operators offering micro-excavation as a managed service.

Industrial Cleaning Outsourcing in Process Industries

Process-intensive sectors—chemicals, refining, pulp, and food—accelerate outsourcing of high-risk cleaning operations to slash capital budgets and satisfy audit requirements. Environmental service companies now embed vacuum trucks equipped with HEPA filtration, spark-resistant blowers, and confined-space monitoring sensors into turnkey contracts that guarantee uptime for plant owners. Jobs involving industrial vacuums command premium rates. This is attributed to the specialized handling protocols for hazardous materials and the advanced high-vacuum pump technology integrated into each chassis. Major waste-management firms note double-digit expansion of recurring contracts as manufacturers redesign vendor lists around environmental, social, and governance metrics. Predictable multi-year volumes reinforce investment cases for fleet upgrades, increasing the vacuum truck market’s installed base.

AI-Enabled Telematics Improving Fleet Utilization & TCO

Edge-connected sensors stream pump performance, filter pressure, and payload weight, enabling predictive maintenance that reduces unscheduled downtime by up to two-fifths. Penske’s machine-learning platform records one-tenth of fuel savings across mixed vocational fleets by dynamically routing units to minimize deadhead miles. Operators can sidestep expensive overweight penalties by integrating onboard scales with telematics systems, safeguarding their slim profit margins. Manufacturers such as GapVax embed operator-guidance displays that flag optimal engine RPM, cutting unnecessary idling and slashing soot accumulation. Such digitally enabled value propositions sustain equipment differentiation and elevate resale values, encouraging customers to favor premium, data-ready models despite higher sticker prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Maintenance Complexity | -1.1% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Shortage Of Certified Hydro-Excavation Operators | -0.8% | North America and EU primarily | Medium term (2-4 years) |

| Range & Payload Penalties | -0.6% | Global, acute in early EV adoption markets | Short term (≤ 2 years) |

| PFAS-Filtration Compliance Driving Up Unit Costs | -0.4% | North America and EU regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex & Maintenance Complexity of High-Capacity Pumps

By integrating onboard scales with telematics systems, operators can sidestep expensive overweight penalties and enhance operational efficiency and compliance. This integration helps safeguard their slim profit margins while ensuring smoother fleet management. Smaller contractors in Latin America and Southeast Asia often struggle to secure financing for such assets, delaying fleet expansion just as infrastructure projects ramp up. Service life-cycle models show maintenance costs consuming nearly one-third of annual operating expenditure during the first five years, especially where certified technicians are scarce. Downtime risk, therefore, nudges risk-averse buyers toward rentals or used units, dampening near-term unit sales and trimming the vacuum truck market’s potential CAGR by an estimated rate.

Shortage of Certified Hydro-Excavation Operators

Hydro-excavation crews must master confined-space entry, high-pressure water jet handling, and Class-B commercial driving, skills that collectively take six to twelve months to certify. North American training centers report one-fifth applicant dropout, and annual turnover exceeds double in specific geographies, creating bidding wars for experienced supervisors. European utilities, meanwhile, cite workforce aging as a principal risk to meeting dig-free mandates by 2027. Insufficient labor forces companies to underutilize existing trucks, depressing revenue per asset and constraining the vacuum truck market’s expansion runway despite robust end-market demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Combination Trucks Address Diverse Customer Needs

Combination models retained 51.27% of the vacuum truck market share in 2024 as multipurpose fleets prioritized chassis that could switch from liquid waste retrieval in the morning to dry debris collection in the afternoon. These units streamline scheduling and reduce yard footprint, boosting return on capital—an increasingly critical metric for public environmental service firms. Federal Signal’s acquisition strategy underscores the premium on product breadth; by adding Hog Technologies’ street-sweeper know-how and Standard Equipment’s industrial vac capabilities, the conglomerate now fields a catalogue spanning municipal sewer cleaning to refinery turnarounds. In parallel, the vacuum truck market size for dry-only systems is set to grow fastest at a 6.77% CAGR during the forecast period (2025-2030), as battery-recycling lines and cement kilns mandate dust-controlled intake ports for combustible powders.

In practical terms, contractors often dispatch a two-truck convoy—a combination unit for bulk slurry removal followed by a dry extractor for residual fines—when clearing fouled grit chambers or mine tailings ponds. Such paired workflows elevate per-job revenue and justify premium rental rates in the vacuum truck market. Technological advances, such as GapVax’s dual-reel jetter design, enhance utilization by enabling simultaneous jetting and vacuuming, cutting person-hours by up to one-fourth on sewer-line cleans. Continuous innovation around ergonomics, noise reduction, and filter-media life positions combination platforms to protect their leadership regardless of incoming niche challengers.

By Fuel: ICE Dominance Gradually Yields to Electric Niche

Internal combustion powertrains accounted for an 83.46% share of the vacuum truck market in 2024, anchored by mature diesel infrastructure and unmatched torque curves necessary for high-vacuum operation. Fleet managers appreciate the straightforward refueling logistics and predictable depreciation curves, mainly when operating in remote oil fields or mining sites. Yet the vacuum truck market registers a palpable pivot toward battery-electric prototypes as urban clean-air zones widen. Dutch municipalities, for example, subsidize electric hydro-vac units for downtown sewer-jetting rounds that rarely exceed 100 km per shift. Although battery packs trim payload by one-fourth, design optimizations—such as composite debris tanks and regenerative braking for boom hydraulics—help narrow the gap. Total cost of ownership analyses suggest parity by the late decade for stop-and-go municipal cycles where idling emissions are heavily penalized.

Range anxiety and public charging scarcity continue to restrict electric adoption in North America, but pilot projects with depot-based overnight charging show promise. Europe’s forthcoming Euro VII standards could elevate diesel after-treatment costs to a level that pushes medium-sized contractors toward electrified alternatives sooner than expected. Hybrid auxiliary drives also emerge, allowing diesel propulsion on highways and electric pump operation on site, thus curbing noise and fumes during early-morning utilities work. Consequently, electric variants are forecast to post a 6.75% CAGR during the forecast period (2025-2030), outpacing overall vacuum truck market growth yet remaining a minority share until energy-density breakthroughs arrive.

By Application: Industrial Cleaning Leads as Excavation Accelerates

Industrial cleaning generated a 38.83% share of the vacuum truck market in 2024, propelled by stringent process-plant audits and the rise of outcome-based service contracts that bundle workforce, equipment, and waste disposal. Large refineries renew three-year master service agreements that guarantee 24-hour sludge removal capability during planned shutdowns, effectively locking in fleet utilization for service providers. Disaster-response sub-segments—covering hurricanes, floods, and chemical spills—grow even faster, rewarding fleets with high CFM blowers and multi-stage filtration that can tackle heterogeneous debris. Conversely, non-destructive excavation is the vacuum truck market’s fastest-growing application at a 6.78% CAGR during the forecast period (2025-2030), as telecommunications carriers deploy dense fiber networks and utilities replace legacy gas mains beneath congested streets.

Municipal maintenance, encompassing catch-basin cleanouts and sewer-line jetting, remains a reliable but slower-growing pillar. Competitive bids often weigh lifecycle cost analyses that favor mid-capacity chassis offering the best payload-to-GVWR ratio. General commercial cleaning—parking garages, mall grease traps, stadium spill response—rounds out the application mix but commands lower daily rates. Operators diversify across segments, sending the same unit from an overnight excavation pothole job to a daytime mill-cleaning contract, optimizing billable hours and maximizing their position in the vacuum truck market.

By Capacity: Medium Units Balance Payload and Maneuverability

Medium‐capacity models captured 46.35% share of the vacuum truck market in 2024 because they straddle highway weight restrictions while carrying enough volume to minimize dump cycles. Operators appreciate chassis that fall below the standard 32-ton gross limits, avoiding special route permits in urban cores. Telemetry data indicates these rigs deliver the lowest cost per ton of material removed across mixed service portfolios. Small units under 5 yd³ now chart the steepest growth trajectory at a 6.79% CAGR during the forecast period (2025-2030), mirroring the rise in micro-trenching for 5G antenna linkups and curbside utility repairs. Contractors leverage the smaller turning radius and reduced axle loads to work inside tight alleys and pedestrianized zones where larger trucks cannot legally enter.

Conversely, large units above 12 yd³ remain essential for mine-site cleanup and major industrial outages but face greater scrutiny under bridge-loading statutes and emissions caps. Manufacturers mitigate the burden through onboard weighing linked to telematics, alerting drivers before overfills lead to fines. Innovations in lightweight aluminum tanks and high-strength steels offer incremental capacity without breaching axle ratings, yet price premiums slow widespread adoption. As regulatory bodies tighten enforcement, the vacuum truck market increasingly emphasizes right-sizing, fueling demand for advanced fleet-planning software that aligns capacity with job-site constraints.

Geography Analysis

Europe retained a 36.71% share of the vacuum truck market in 2024, underpinned by mature sewer networks, PFAS removal mandates, and aggressive emissions legislation that collectively intensify equipment specifications. German wastewater utilities, for instance, now require onboard particulate filters as part of tender criteria, nudging vendors toward sophisticated after-treatment packages. Nordic countries offer attractive subsidies for electric chassis, fostering localized clusters of zero-emission vacuum trucks that navigate pedestrian cores without violating noise ordinances. Simultaneously, tightened landfill regulations boost back-hauls of dewatered sludge to bioenergy plants, enhancing round-trip economics for high-vacuum rigs.

Asia-Pacific is the fastest-growing territory, posting a 6.81% CAGR during the forecast period (2025-2030). China’s 14th Five-Year Plan earmarks trillions of yuan for water-pipeline leak detection and soil-remediation work, which rely heavily on non-destructive excavation technologies. India’s urban smart-city initiatives likewise bundle trenchless pipe replacement with fiber-optic rollout, demanding compact hydro-excavators suitable for narrow streets. Price sensitivity remains acute, steering public tenders toward mid-tier domestic brands; however, safety specifications tighten annually, gradually steering demand toward imported premium configurations. Japan and South Korea sustain specialist niches in semiconductor fab cleaning, requiring ultrapure vacuum trucks outfitted with stainless-steel tanks and chemical-resistant seals.

North America combines entrenched regulation with high outsourcing penetration, enabling service providers to uphold premium day rates. U.S. industrial hubs along the Gulf Coast rely on vacuum trucks for refinery turnarounds, while Canadian provinces expand hydrovac mandates to protect underground telecommunication lines. Latin America, the Middle East, and Africa represent an emerging one-fifth slice of the vacuum truck market, characterized by fragmented ownership and sporadic public-sector procurement. The rollout of mega-projects—such as Saudi Arabia’s NEOM city and Brazil’s sanitation PPPs—signals pockets of high-value demand once financing and training hurdles are cleared.

Competitive Landscape

Global suppliers and regional specialists collectively fuel a moderately fragmented competitive field. Federal Signal's 2024 purchase of street-cleaning innovator Hog Technologies added curb-and-gutter expertise to its Vactor vacuum line, strengthening cross-selling among municipal buyers. The firm acquired Standard Equipment earlier that year, adding industrial vacuum integration capabilities and expanding aftermarket parts distribution.

Capital deployment from institutional investors intensifies. Goldman Sachs Alternatives acquired Liquid Environmental Solutions in July 2025, inheriting 64 service depots and 26 treatment plants across North America[3]"Goldman Sachs Alternatives to Acquire Liquid Environmental Solutions," Goldman Sachs Group Inc., goldmansachs.com . Infusing private-equity capital accelerates fleet electrification trials and data analytics platforms that feed real-time compliance dashboards to industrial clients. Niche manufacturers filling white-space roles—such as dry-only loaders for battery-recycling plants—win orders by pairing application-specific hardware with operator-training modules, thus offsetting the incumbent scale advantage.

Technology differentiation widens the moat depth. GapVax integrates lidar-based boom collision avoidance and voice-assisted operator prompts, trimming accident claims and enhancing brand loyalty. Rival municipal-focused builders emphasize modular debris tanks that detach for quick decontamination between PFAS and biosolids jobs. Across all tiers, telematics partnerships with cloud providers anchor service-based revenue models, transforming what was once a capital-equipment sale into an ongoing data subscription and predictive-maintenance contract. These dynamics collectively strengthen margins yet raise competency thresholds, subtly nudging the vacuum truck market toward a more consolidated future even as regional newcomers still find space in localized niches.

Vacuum Truck Industry Leaders

-

Federal Signal Corporation (Vactor)

-

CAPPELLOTTO S.p.A.

-

Vac-Con Inc.

-

FULONGMA GROUP Co., Ltd.

-

KOKS Group BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Goldman Sachs Alternatives acquired Liquid Environmental Solutions from Audax Private Equity, adding 64 service locations and 26 treatment facilities to expand its non-hazardous liquid-waste footprint.

- February 2025: Vortex Companies launched a Water Division focused on infrastructure rehabilitation, bundling design, construction, and maintenance services for municipal and industrial water systems.

Global Vacuum Truck Market Report Scope

| Combination Trucks |

| Liquid Suction Trucks |

| Dry Suction Trucks |

| Internal Combustion Engine (ICE) |

| Electric |

| Industrial Cleaning |

| Excavation |

| Municipal |

| General Cleaning |

| Others |

| Small |

| Medium |

| Large |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | Combination Trucks | |

| Liquid Suction Trucks | ||

| Dry Suction Trucks | ||

| By Fuel | Internal Combustion Engine (ICE) | |

| Electric | ||

| By Application | Industrial Cleaning | |

| Excavation | ||

| Municipal | ||

| General Cleaning | ||

| Others | ||

| By Capacity | Small | |

| Medium | ||

| Large | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the vacuum truck market be by 2030?

The vacuum truck market is projected to reach USD 3.01 billion by 2030, reflecting a 6.74% CAGR from 2025.

Which product type generates the most revenue?

Combination trucks lead with 51.27% revenue share because they can handle liquid and dry materials in a single shift.

What is the key growth driver in Asia-Pacific?

Accelerating urban infrastructure projects and tight utility corridors are fuelling the adoption of non-destructive excavation services.

Why are dry vacuum trucks gaining popularity?

Dry suction units suit battery-recycling and dust-sensitive industrial sites, driving their 6.77% CAGR over the forecast horizon.

Are electric vacuum trucks commercially viable today?

Electric models remain niche due to payload limits, yet municipal low-emission zones in Europe are spurring pilot fleets and gradual scale-up.

How are operators cutting the total cost of ownership?

AI-enabled telematics deliver fuel savings and predictive maintenance, boosting asset utilization and reducing downtime.

Page last updated on: