Market Overview

| Study Period | 2020 - 2031 |

|---|---|

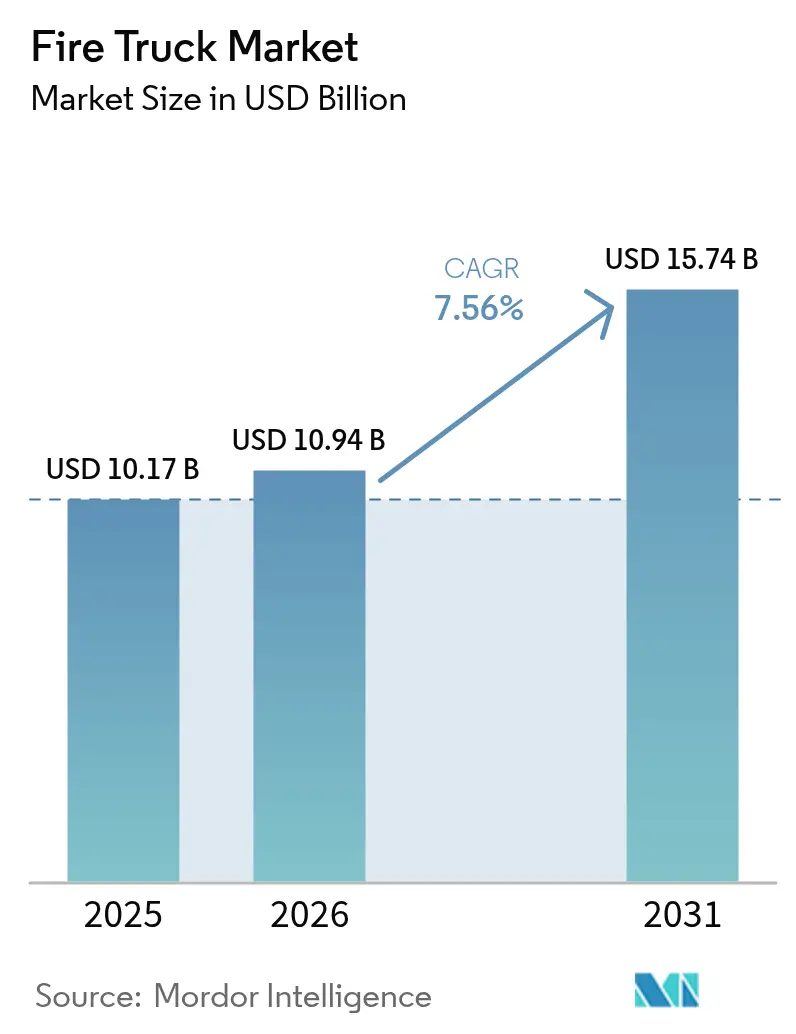

| Market Size (2026) | USD 10.94 Billion |

| Market Size (2031) | USD 15.74 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

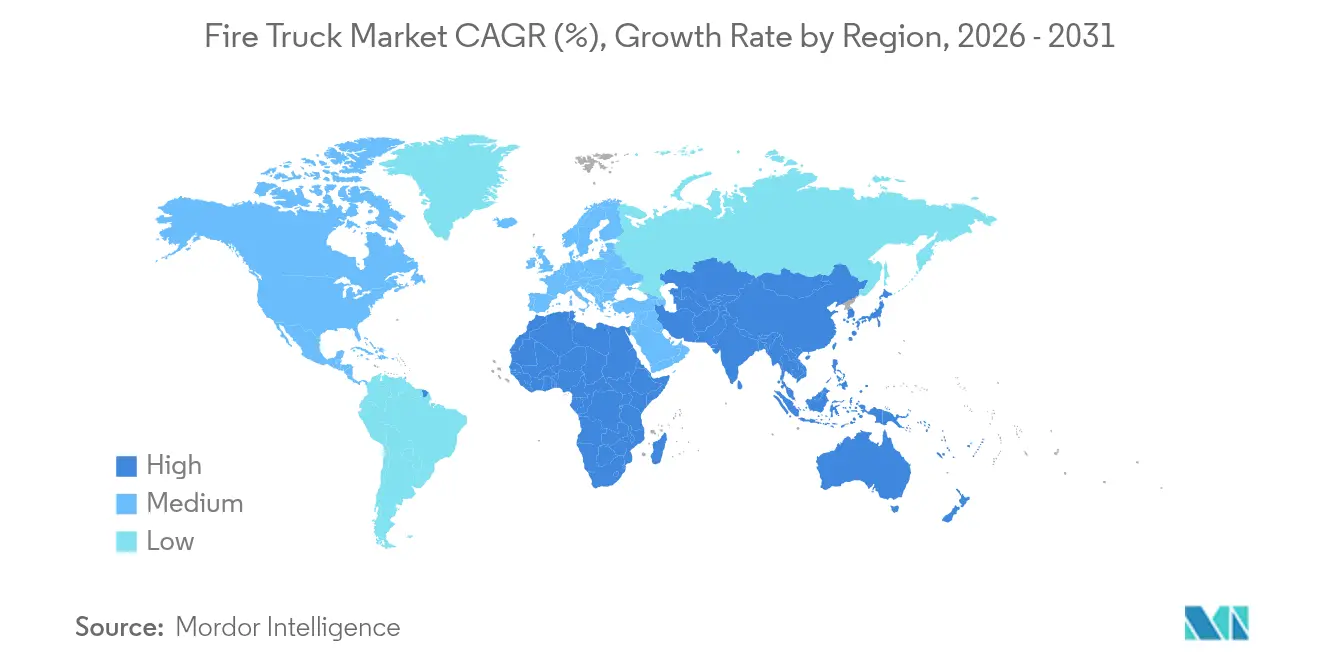

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fire Truck Market Analysis by Mordor Intelligence

The Fire Truck Market size is expected to grow from USD 10.17 billion in 2025 to USD 10.94 billion in 2026 and is forecast to reach USD 15.74 billion by 2031 at 7.56% CAGR over 2026-2031. Fleet replacement cycles, electrification momentum, and climate-driven wildfire risk are combining to lift procurement budgets despite lingering supply-chain bottlenecks. Extended order lead times of 18-33 months are prompting departments to modernize maintenance programs while they wait for new deliveries. Yet, the fire truck market continues to absorb higher unit prices as safety and performance features become non-negotiable. Battery-electric models are moving from pilot to production status in North America and Europe, supported by clean-fleet mandates and measurable savings in fuel and maintenance outlays. Meanwhile, an increase in large-scale wildfire incidents stimulates demand for specialized wildland configurations, and consolidated OEM power is drawing heightened regulatory scrutiny in the United States.

Key Report Takeaways

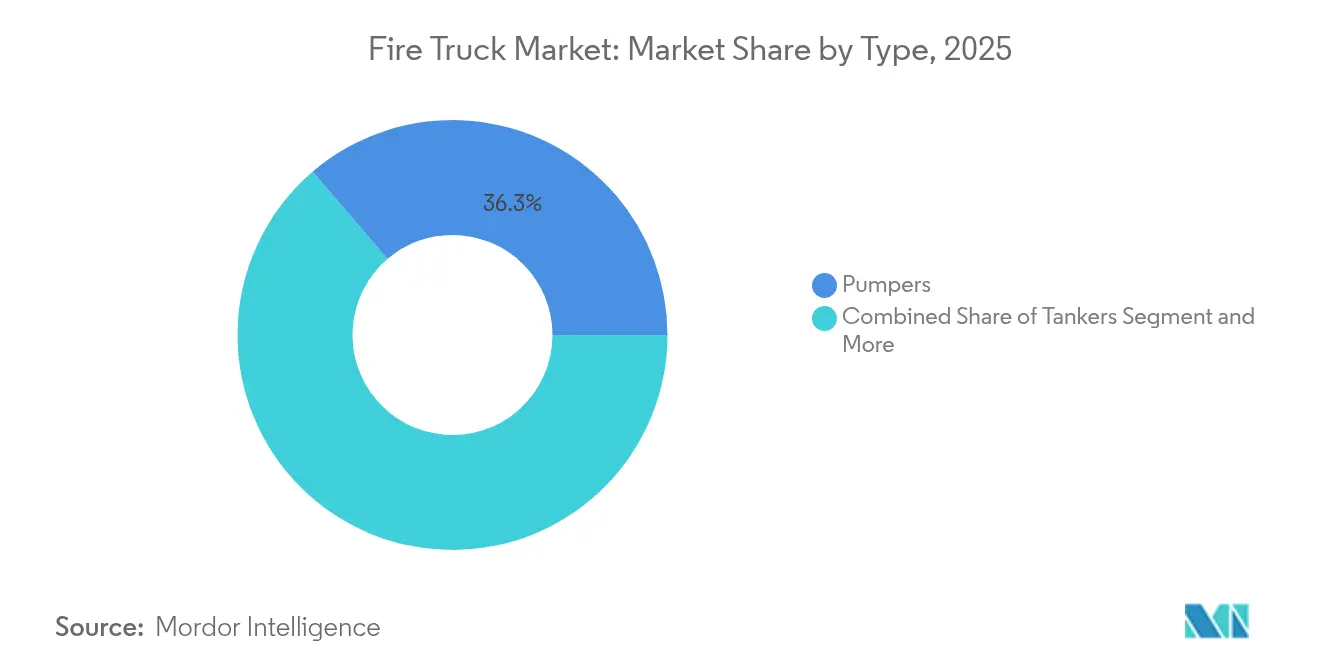

- By type, pumpers led with 36.28% revenue share in 2025, and the segment is projected to expand at a 7.62% CAGR through 2031.

- By application, residential & commercial operations accounted for 56.90% of the fire truck market share in 2025, while wildland & forestry applications are on track for an 7.86% CAGR to 2031.

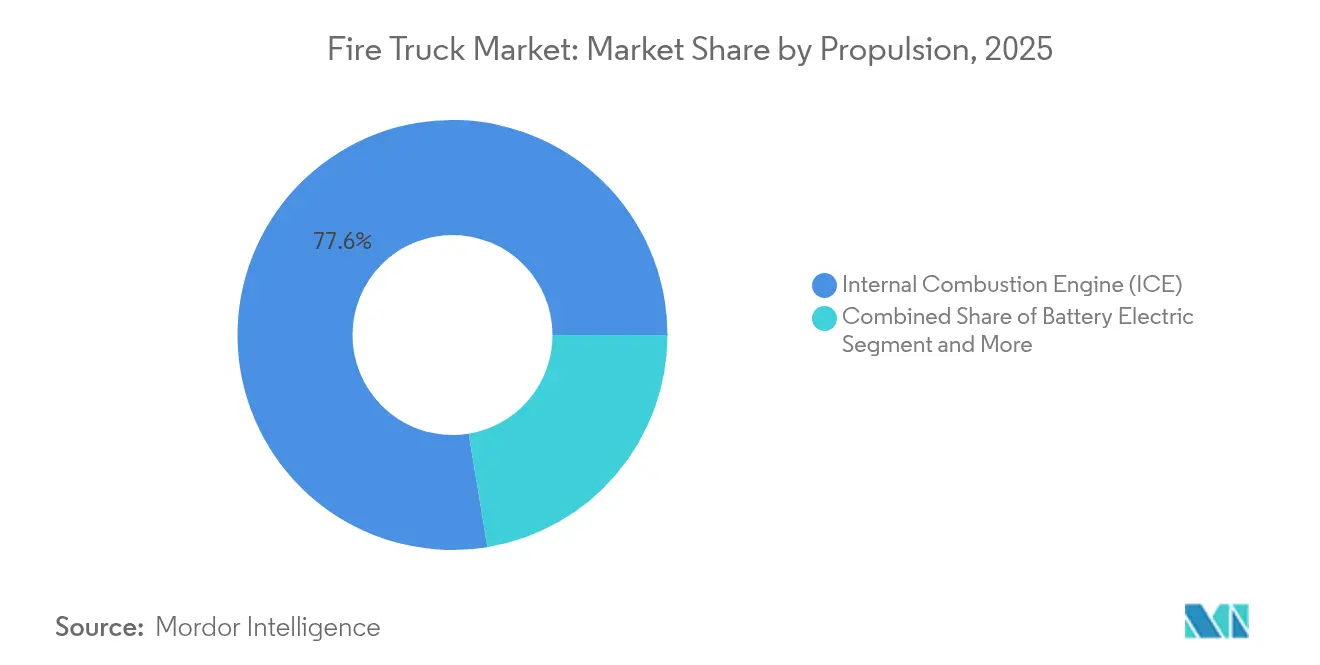

- By propulsion, internal-combustion platforms retained 77.60% share in 2025, yet battery-electric units post the highest growth at 7.71% CAGR through 2031.

- By end-user, municipal departments captured 60.55% of demand in 2025, whereas airport authorities record the strongest 7.58% CAGR outlook to 2031.

- By geography, North America held 33.95% of 2025 revenues, while Asia-Pacific is poised for a 7.72% CAGR on the back of rapid urbanization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fire Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global & regional fire-safety regulations | +1.8% | Global, with early gains in North America, EU, Australia | Long term (≥ 4 years) |

| Rising frequency & severity of wildfires | +1.5% | North America, Australia, Mediterranean Europe | Short term (≤ 2 years) |

| Growing adoption of electric fire trucks | +1.2% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Rapid replacement of ageing municipal fleets | +1.1% | Europe core, spill-over to North America | Medium term (2-4 years) |

| Urban high-rise construction | +0.9% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Integration of IoT-telematics | +0.8% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent global & regional fire-safety regulations

The new NFPA 1900 standard unifies previous apparatus rules and introduces mandatory rear-view cameras, LED lighting and electric-vehicle guidance.[1]Larry Anderson, “New NFPA 1900 Standard Guides Manufacture of Fire Apparatus,” thebigredguide.com By shifting from prescriptive checklists toward performance-based criteria, regulators give OEMs room to innovate while still elevating baseline safety. Harmonized requirements also support cross-border apparatus deployment, a benefit for manufacturers with global logistics footprints. Compliance costs, however, are accelerating consolidation among smaller builders, reinforcing the high-concentration profile of the fire truck market.

Rising frequency & severity of wildfires

U.S. wildfire acreage hit 7.7 million acres in 2024, outpacing the 10-year average despite fewer total incidents.[2]Katie Hoover and Laura Hanson, “Wildfire Statistics,” fas.org Larger, more intense events drive orders for Type 1 Wildland-Urban Interface engines with auxiliary pumps that operate while the vehicle is moving. Federal and state grants aimed at wildfire readiness funnel capital into specialized equipment, keeping demand insulated from municipal budget cycles. The extended season now covers nearly the full calendar year, requiring departments to maintain year-round readiness and boosting the baseline for apparatus utilization.

Growing adoption of electric fire trucks

Deployments now extend beyond pilots, with Boulder Fire-Rescue operating two Rosenbauer RTX pumpers, a first for any U.S. department. The St. Paul Fire Department purchased a USD 1.8 million RTX that is projected to cut USD 25,000 in annual operating costs. Electric drivetrains lower noise and diesel-fume exposure, improving crew health and communication. Cold-weather testing shows battery thermal systems maintaining performance in sub-zero conditions. With NFPA 1900 integrating propulsion-specific requirements, compliance hurdles for electric units have eased. These factors, together with municipal carbon-neutral targets, underpin a steady rise in electric orders across the fire truck market.

Rapid replacement of ageing municipal fleets in Europe

Roughly more than two fifth of European fire stations were built before 1985, and many trucks exceed their nominal 20-year life. Stricter emissions rules, effective in 2027, are further shortening replacement intervals. Municipalities leverage cooperative purchasing to secure volume discounts and navigate wait-times exceeding two years. This dynamic steers demand toward modular designs that integrate telematics and low-emission drivetrains, positioning pumpers and aerials at the forefront of European fleet upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of next-gen platforms | -1.4% | Global, with acute impact in developing economies | Short term (≤ 2 years) |

| Semiconductor & chassis supply-chain | -1.1% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Shortage of skilled emergency-vehicle operators | -0.6% | Global, with acute impact in North America and EU | Long term (≥ 4 years) |

| Tight municipal budgets | -0.5% | APAC, South America, MEA core markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High upfront cost of next-gen platforms

An electric pumper such as the RTX lists close to a million dollar, roughly double a comparable diesel engine. While operational savings improve total cost of ownership, the initial capital hurdle delays adoption for volunteer and rural departments. Grant programs partially offset costs—Boulder secured a decent amount in external funding for its second electric unit—but financing gaps persist outside well-funded metros. Battery costs are falling yet are unlikely to reach parity with diesel until production runs scale meaningfully after 2027. This two-tier dynamic slows the transition in developing regions, restraining global fire truck market growth in the near term.

Semiconductor & chassis supply-chain disruptions

Chip shortages have stretched apparatus lead times to 18-33 months, forcing departments like Grand Chute, WI, to keep aged ladder trucks in service far longer than planned. Senators Hawley and Kim have opened inquiries into the pricing power of the consolidated OEM cohort and the impact of delayed deliveries on public safety. Chassis bottlenecks intensify the squeeze as fire truck builders vie with commercial-truck makers for base frames. Builders with vertically integrated supply chains can buffer shocks, but smaller players face schedule slippages that challenge market credibility. Recovery to normal delivery windows is unlikely before 2026, injecting downside risk into near-term fire truck market forecasts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pumpers sustain leadership while nurturing innovation

The pumper segment held 36.28% of the fire truck market in 2025 and is set to advance at a 7.62% CAGR to 2031. Pumper evolution adds compressed-air foam systems and modular bodywork, giving departments multi-purpose capability. Segment revenue also benefits from early electrification, with Rosenbauer’s RTX platform offering identical pump-rating performance to diesel models. Tankers remain indispensable where hydrant networks are sparse, and ladder platforms satisfy growing urban skylines, including Bronto Skylift’s 230-foot reach that covers 20-story buildings.

Modern rescue units embed hydraulic extrication tools and battery-powered cutting devices, reducing scene set-up time. Demand is also rising for combination apparatus that blend pumper, tanker and rescue functions to save procurement budgets and station footprints. Wildland trucks add auxiliary pumps that deliver water while the vehicle is moving, a feature vital during fast-moving fires. ARFF vehicles command premium pricing due to FAA Part 139 standards that mandate stringent acceleration and foam-delivery benchmarks. With incremental innovation, the pumper’s share of the fire truck market is likely to remain above one-third through the forecast horizon.

By Application: Wildland growth narrows the gap with structural demand

Residential & commercial protection accounted for 56.90% of 2025 revenues, making it the largest single application inside the fire truck market. Fire service mandates for dense urban cores keep order flow steady, and new building codes continue to shift equipment needs toward higher pump capacity and integrated decontamination systems.

Wildland & forestry, however, is expanding at 7.86% CAGR as climate patterns intensify severity and length of fire seasons. Vehicle designs incorporate greater ground clearance, reinforced underbodies and pump-and-roll capacity so crews can attack advancing flames without stopping. Federal grants tied to wildfire mitigation programs sustain procurement budgets even during municipal revenue downturns. Industrial applications demand chemical-proof seals and fire suppression agents compatible with class B hazards, while airports continue ordering ARFF units compliant with fluorine-free foam requirements set by the FAA’s ongoing F3 transition initiative. Taken together, these shifts demonstrate how diverse risk profiles shape the evolving fire truck market.

By Propulsion: Electric acceleration challenges diesel dominance

Internal-combustion engines still controlled 77.60% of deliveries in 2025, sustaining the traditional backbone of the fire truck market. Yet battery-electric units are climbing at 7.71% CAGR, aided by municipal climate objectives and evidence of operational savings. Early adopters such as the City of Boulder report meaningful reductions in diesel-particulate exposure for crews, bolstering the case for wider rollout.

Hybrid configurations present an interim solution, allowing electric pump operation at scene and diesel power for long-range travel. Fuel-cell concepts remain nascent but could solve range and recharge downtime for rural agencies once hydrogen infrastructure expands. NFPA 1900’s propulsion-agnostic architecture brings electric safety features under the same umbrella as diesel, reducing compliance uncertainty. With these enablers, the electric share of the fire truck market could reach one fifth of the total by the end of the decade, particularly in urban jurisdictions that backfill diesel fleets with zero-emission replacements.

By End-User: Airport authorities outpace municipal purchasers

Municipal departments delivered 60.55% of demand in 2025, reflecting their core role in community protection. Nonetheless, airport authorities exhibit the fastest 7.58% CAGR, propelled by terminal expansions and stricter ARFF vehicle criteria. Foam system transitions away from PFAS chemicals add urgency to refresh older fleets, while modern aircraft sizes demand higher agent-flow rates for incident response.

Industrial brigades continue to specify purpose-built units for petrochemical and manufacturing sites, integrating gas-detection telemetry with vehicle control systems. Defense agencies maintain specialized fleets that can deploy abroad or on-base, often procuring through multi-year contracts that stabilize builder production lines. Private-contract services are also gaining traction, particularly in campus-style industrial parks where dedicated fire protection yields insurance advantages. This expanding buyer mix broadens the addressable fire truck market beyond its municipal nucleus.

Geography Analysis

North America commanded 33.95% of 2025 revenue, benefiting from mature emergency-services funding and advanced technology trials. The region hosts the bulk of early electric deployments, reinforcing its role as a bellwether for future global adoption patterns. Ongoing federal infrastructure programs provide supplemental funding to replace apparatus older than 20 years, keeping the order pipeline resilient.

Asia-Pacific, recording a 7.72% CAGR, is rapidly scaling municipal fire services to match urbanization in China, India and Southeast Asia. China’s tier-2 and tier-3 cities allocate capital to expand station networks and invest in pumpers and aerials designed for dense, high-rise districts. India issues regular tenders that prioritize local assembly, encouraging joint ventures between global OEMs and domestic chassis suppliers. Emerging interest in battery-electric commercial vehicles at a robust CAGR hints at a budding market for zero-emission apparatus once charging infrastructure matures.

Europe remains a large yet slower-growing arena focused on green compliance and replacement rather than fleet expansion. Tightening emissions rules and NFPA-aligned standards influence procurement criteria, stimulating uptake of Euro-VI engines and hybrid drives. The Middle East & Africa register steady orders linked to expanding urban footprints and industrial megaprojects, while South America’s demand is tempered by macroeconomic volatility. Collectively, these regional trajectories underscore the geographic diversity underpinning the fire truck market.

Regulatory Landscape

Fire truck design and procurement are anchored to safety and performance standards that increasingly harmonize requirements across apparatus types and propulsion. NFPA 1900 consolidated multiple prior NFPA apparatus standards into one framework effective January 1, 2024, while NFPA 1910 consolidated inspection, maintenance, and testing requirements, which shifts manufacturers and departments toward clearer, unified compliance checklists that also incorporate guidance for electric-vehicle integration.

In Europe, EN 1846-2 (issued in 2024 and updated into 2025 national adoptions such as SS-EN 1846-2 and NEN-EN 1846-2) sets common safety and performance requirements for firefighting and rescue service vehicles, supporting cross-border tender comparability. In the United States, operational and vehicle-level rules also shape apparatus configurations and use, including FMCSA provisions (49 CFR 390.3T(f)(5)) that address emergency-operation exemptions, and NHTSA updates in June 2026 that amended portions of FMVSS references relevant to modern vehicle systems. Electric powertrain integrity requirements under FMVSS 305a include a mandatory compliance date beginning September 1, 2027 (with certain extensions for specific manufacturer categories), which creates a defined validation timeline for electric and hybrid fire apparatus.

Value Chain Analysis

The fire truck value chain starts with chassis and powertrain supply (commercial truck OEMs and specialty platforms), then moves to body and module fabrication, pump and foam-system integration, electrical and lighting packages, and the final assembly and certification workflows for municipal, industrial, and ARFF applications. A multi-tier supplier ecosystem provides pumps, valves, tanks, hose reels, agent systems, lighting, and control electronics, while final-stage builders handle integration, water-flow testing, road testing, and configuration-to-spec documentation aligned with standards such as NFPA 1900 and EN 1846-2.

Lead-time management and chassis availability remain central to how value is captured and risk is managed across the chain. OEMs have leaned into modular production to decouple body manufacturing from chassis delivery, illustrated by Rosenbauer marking the delivery of its 100th tanker fire truck using the modular MT body design in April 2026, with modules manufactured in-house ahead of chassis arrival to shorten the critical path. Upstream partnerships also help secure base platforms and service coverage, such as Zoomlion signing a global strategic cooperation agreement with Mercedes-Benz Trucks in April 2025 focused on specialized fire truck chassis and overall vehicle solutions, aligning chassis supply, integration engineering, and aftersales support across regions.

Competitive Landscape

The fire truck market is highly concentrated; three global manufacturers account for roughly around four fifth of deliveries, giving them scale advantages in R&D and supply-chain bargaining. This dominance has drawn bipartisan Senate attention over pricing power and delivery delays, with legislators probing whether consolidation undermines preparedness.[3]Elizabeth Warren, “Bipartisan Investigation Into Harms of Private Equity,” warren.senate.gov OEMs respond by expanding domestic capacity; Pierce Manufacturing, for instance, added production shifts and facility square footage to trim backlogs.

Electrification has become the primary competitive arena. Oshkosh exhibited its AI-enabled Collision Avoidance Mitigation System at CES 2025, positioning software-driven safety as a differentiator. Rosenbauer’s continued rollout of the RTX series in North America and Europe signals confidence in scaling electric production. REV Group leverages its mixed-fleet portfolio to offer hybrid ladder trucks aimed at cities with sparse charging infrastructure.

New entrants target niche opportunities like IoT-based fleet-management platforms that integrate predictive maintenance and driver-behavior analytics. Smaller chassis integrators also find openings in custom wildland configurations, where agility and specialized protection features outweigh scale. With buyer priorities shifting toward life-cycle value over upfront cost alone, integrated service contracts that bundle training, parts and telematics stand to reshape the revenue mix for participants in the fire truck industry.

Fire Truck Industry Leaders

Oshkosh Corporation

Rosenbauer International AG

Magirus GmbH.

REV Group

Morita Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Electrification has moved into higher-complexity apparatus categories, creating whitespace for suppliers that can deliver certified performance, thermal management, and duty-cycle reliability in heavy, safety-critical missions. In June 2026, Rosenbauer unveiled the L32A-XS electric aerial ladder on a MAN eTGM chassis at INTERSCHUTZ 2026, positioned as the first all-electric aerial ladder under 16 tonnes. This expands the addressable zero-emission portfolio beyond pumpers into aerial segments where payload, stability, and power-demand requirements are more demanding. ARFF electrification is also showing up in in-service trials, with Rosenbauer delivering an all-electric PANTHER 6x6 to Dallas Fire-Rescue at Love Field for a six-month trial, and OEM roadmaps highlighting electric ARFF platforms such as Rosenbauer PANTHER electric and Oshkosh Airport Products Striker Volterra.

Extended delivery windows and visible pricing pressure support modular architectures, lifecycle service contracts, and digital fleet tools that reduce downtime while departments wait for new apparatus. With reported order lead times stretching into multi-year cycles in parts of the market, demand is shifting toward solutions that improve availability, including modular builds that reduce rework, predictive maintenance offerings, and standardized option packages that simplify procurement. Updated compliance frameworks (NFPA 1900 and EN 1846-2:2024/2025) also reinforce a clearer pathway for manufacturers to commercialize electric and hybrid variants at scale, while raising the bar on documentation, testing, and safety features that can differentiate suppliers able to industrialize these platforms across municipal, airport, and industrial end users.

Recent Industry Developments

- June 2026: Rosenbauer unveiled the L32A-XS electric aerial ladder built on a MAN eTGM chassis at INTERSCHUTZ 2026, positioned as the first all-electric aerial ladder under 16 tonnes. The launch extends electrification beyond pumpers into aerial apparatus where payload, stability, and power demands are higher. It also broadens competitive differentiation around battery management, integration engineering, and compliance readiness for zero-emission configurations.

- March 2026: Oshkosh Airport Products announced that Groupe ADP ordered a fourth Striker Volterra 6x6 electric ARFF vehicle for Paris-Le Bourget Airport. Repeat orders from a major airport operator signal operational confidence and support broader adoption of electric ARFF platforms in airport fleet renewal cycles. The deal strengthens Oshkosh positioning in premium ARFF segments where specifications and total lifecycle support heavily influence procurement.

- December 2024: Rosenbauer America partnered with Dallas Fire Rescue to deploy a PANTHER 6x6 electric fire truck at Dallas Love Field Airport in 2025. The collaboration placed electrified ARFF technology into an operational airport environment, supporting validation of performance, charging workflows, and maintenance needs. It also helped normalize electric specifications in airport tenders as foam systems, safety requirements, and emissions goals converge.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues earned from new fire trucks that are purpose-built for firefighting and rescue response, including specialized units used by municipal services, airports, industrial facilities, and defense users. Values are tracked at the point of vehicle sale, in nominal USD.

Scope exclusions: Used vehicle resale, routine maintenance services, financing, and stand-alone spare parts are not counted unless they are bundled into a new vehicle contract value.

Segmentation Overview

- By Type

- Pumpers

- Tankers

- Rescue Trucks

- Aerial / Platform Trucks

- Multi-tasking Modular Trucks

- Wildland Fire Trucks

- Airport Crash Tender (ARFF)

- By Application

- Residential & Commercial

- Industrial & Manufacturing

- Airports

- Military

- Wildland & Forestry

- By Propulsion

- Internal Combustion Engine (ICE)

- Hybrid

- Battery Electric

- Fuel-Cell Electric

- By End-User

- Municipal Fire Departments

- Industrial Facility Brigades

- Airport Authorities

- Defense & Military

- Contract & Private Fire Services

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research begins by building the fire-services demand and procurement context, because purchase cycles and public budgets are direct drivers in this market. We reviewed public sources such as national fire incident reporting statistics, government procurement portals, and transport or vehicle registration releases where available, and then cross-checked complete-vehicle coverage using customs trade data.

To keep assumptions grounded, we also used municipal and airport authority budget documents, standards and guidance references published by fire protection bodies, and peer-reviewed or engineering journals that address vehicle safety, pump performance, and equipment requirements. Company annual reports, investor decks, and trusted press were reviewed to understand order backlogs and delivery lead times. Where specific company financial splits were not public, paid subscriptions for company financials and news intelligence, plus patent databases and shipment-level import and export data, were used to fill gaps. This list is not exhaustive, and many other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with vehicle OEM staff, component suppliers, dealers and integrators, and end users involved in procurement and fleet planning. Respondent input was used to confirm regional replacement timing, the cadence of new-vehicle orders, and how alternative propulsion options are being considered, then these checks were applied to fine-tune the model across the Americas, EMEA, and APAC.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 43% |

| Mid tier: 49% | Functional/Unit leaders: 33% | EMEA: 32% |

| Smaller Players: 22% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down method where public procurement spend patterns, fleet replacement cycles, and vehicle delivery pipelines are reconstructed by region, then allocated into fire truck types and end-user pools. The totals were checked with selective bottom-up approximations, mainly by sampling typical unit pricing by truck class and multiplying by estimated annual deliveries, and then adjusting where channel checks showed consistent gaps.

A few inputs carried the most weight: annual municipal and airport capital budget trends, incident and wildfire activity signals that affect fleet urgency, average replacement age and out-of-service rates, order backlog and lead-time ranges, and price movement driven by chassis, pumps, and onboard safety equipment. Where unit volumes were not directly observable, gaps were handled using import and export flows for complete vehicles, alongside expert-led ranges for local assembly versus imported share.

Forecasts were produced using scenario analysis supported by regression checks on budget growth, replacement timing, and delivery capacity constraints, because these variables explain year-to-year movement more reliably than a straight-line trend. Assumptions were finalized after discussions on what changes first in a tightening cycle, which is typically order intake and delivery timing rather than immediate cancellations.

Data Validation & Update Cycle

Model outputs are cross-checked against independent signals such as public tender activity, disclosed backlog commentary, and visible trade flows, and then variances are reviewed before sign-off. If a region shows an unusual swing, we re-check currency timing, large one-off procurement programs, and whether delivery delays shifted revenue across years.

The work goes through multi-step analyst review so assumptions, calculations, and definitions stay consistent across segments and regions. Reports are refreshed annually, and interim updates are triggered when material events occur, such as large regulatory changes, major fleet recapitalization announcements, or sustained price shifts. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Fire Truck Market Size Compared With Other Published Estimates

Published market sizes for fire trucks often differ even when the topic label appears the same, because the included vehicle classes and the revenue point in the value chain can change across studies. Differences also come from the starting year, how multi-year delivery backlogs are recognized, and whether pricing is treated as stable or adjusted over time.

In fire trucks specifically, the gap usually comes from whether airport rescue and specialized rescue units are fully included, whether refurbishment and service contracts are added to new-vehicle revenue, and whether the model is anchored to procurement and delivery timing instead of relying only on long-run vehicle parc assumptions. Currency conversion timing and the use of aggressive versus conservative replacement-cycle assumptions also shift results, particularly when lead times extend and deliveries move across calendar years.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.94 B (2026) | |

| Global Consultancy A | USD 8.37 B (2025) | Uses an earlier base year and a slower growth view, and it can understate value when long delivery lead times shift revenue recognition away from procurement intent. |

| Trade Journal B | USD 12.35 B (2026) | Tends to group adjacent emergency-response apparatus and related contract values into the total, which can lift the figure versus a new-vehicle-only view. |

The table shows that scope choices and timing assumptions are the main reasons for different values, not a simple math error. When specialized units are separated from adjacent apparatus, and revenues are aligned to delivery-linked vehicle sales rather than broader emergency spending, the estimate stays easier to replicate and explain, which is the approach applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current value of the fire truck market?

The fire truck market size is valued at USD 10.94 billion in 2026, with projections pointing to USD 15.74 billion by 2031.

Which fire truck type generates the most revenue?

Pumpers hold the lead, securing 36.28% of 2025 global revenue and maintaining the fastest 7.62% CAGR outlook to 2031.

How quickly are electric fire trucks being adopted?

Battery-electric models are expanding at 7.71% CAGR, and early adopter departments report annual savings of about USD 25,000 per unit.

Why are airport authorities a key growth segment?

Airport fire services must meet strict ARFF standards and are modernizing fleets amid terminal expansions, driving 7.58% CAGR growth through 2031.

What factors constrain near-term supply?

Semiconductor shortages and chassis bottlenecks have stretched delivery windows to as long as 33 months, delaying fleet replacements.

How concentrated is the competitive landscape?

Three global manufacturers control roughly around four fifth of output, leading to a market concentration score of 8.

Page last updated on: