Excavator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

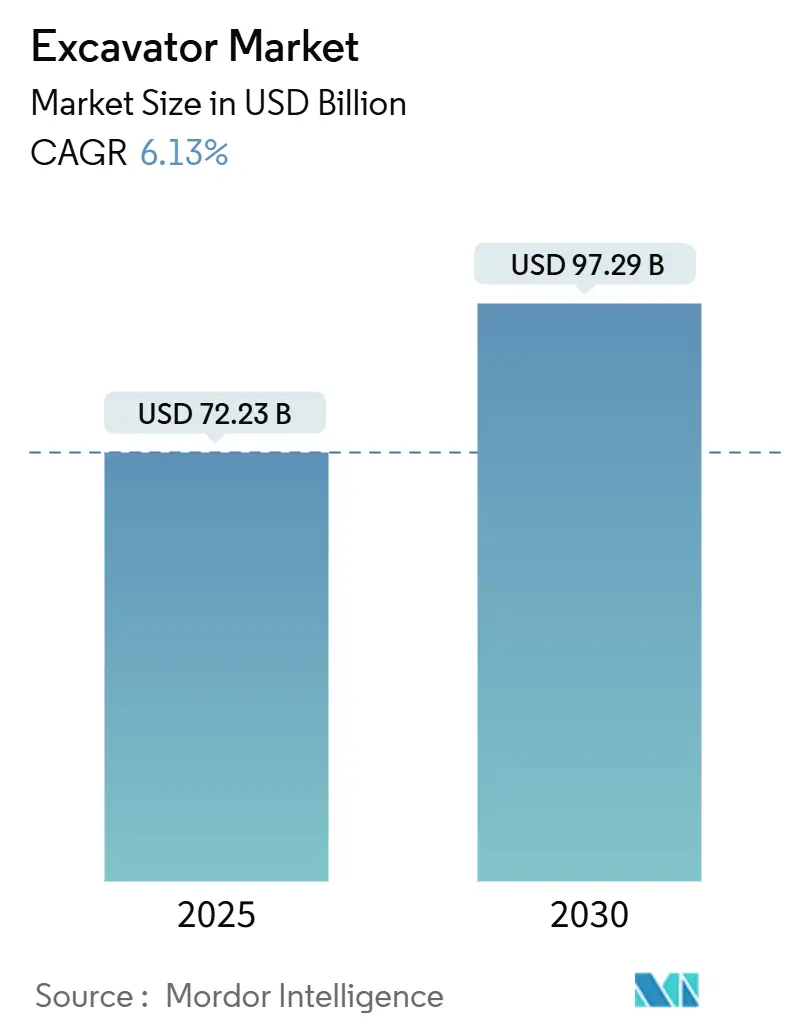

| Market Size (2025) | USD 72.23 Billion |

| Market Size (2030) | USD 97.29 Billion |

| Growth Rate (2025 - 2030) | 6.13% CAGR |

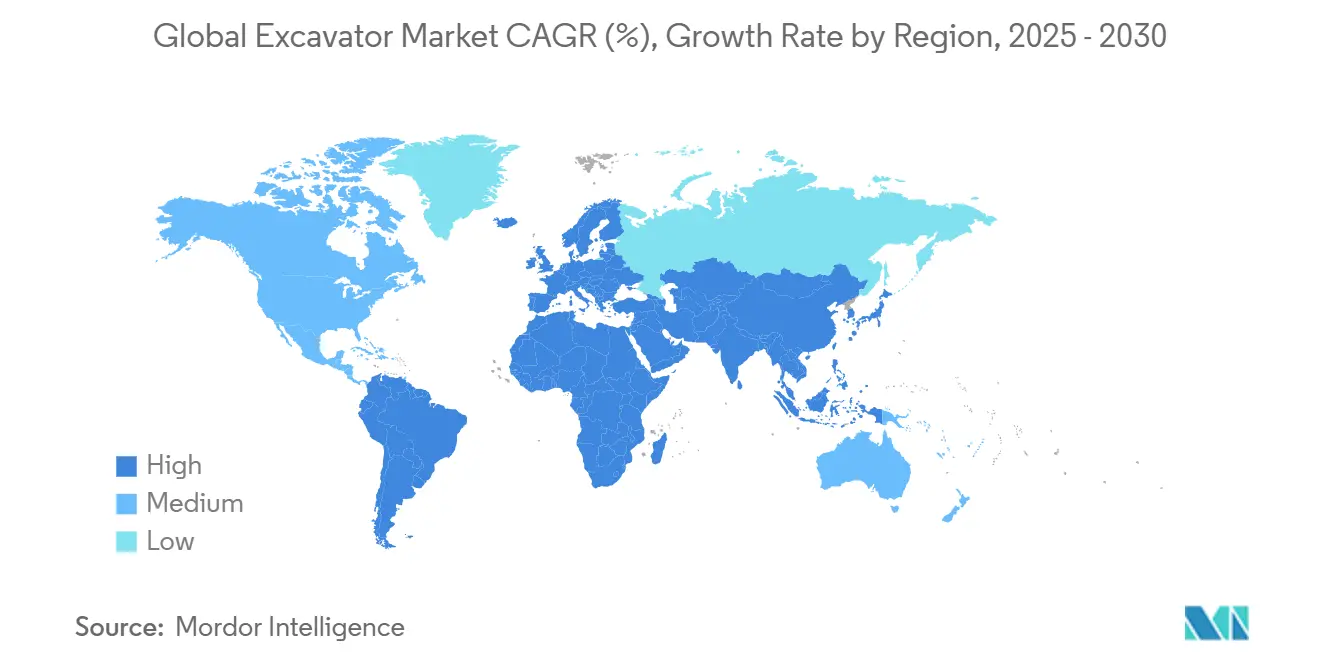

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Excavator Market Analysis by Mordor Intelligence

The excavator market size was USD 72.23 billion in 2025 and is projected to reach USD 97.29 billion by 2030, registering a 6.13% CAGR. Sustained public-works funding in the United States and Germany, rapid urban infrastructure renewal across the European Union, and ongoing electrification initiatives in China are reshaping capital-equipment demand patterns within the excavator market. OEMs prioritize mid-size crawlers and compact machines that satisfy space-constrained job-site requirements while integrating battery-electric and hybrid powertrains to satisfy Stage V and China IV emission norms.

Key Report Takeaways

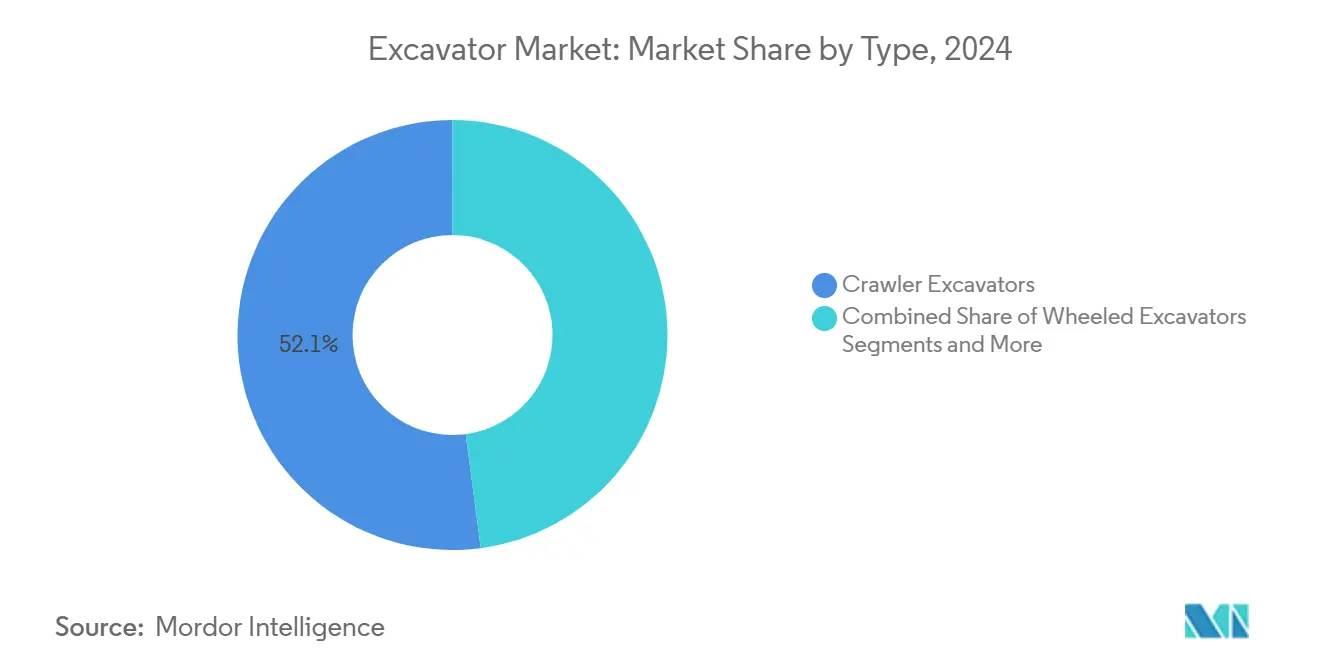

- By type, crawler excavators held 52.13% of the excavator market share in 2024, while short-swing-radius models are advancing at a 9.84% CAGR through 2030.

- By propulsion, diesel/ICE units represented 78.06% of the excavator market size in 2024; battery-electric variants lead growth at 13.72% CAGR through 2030.

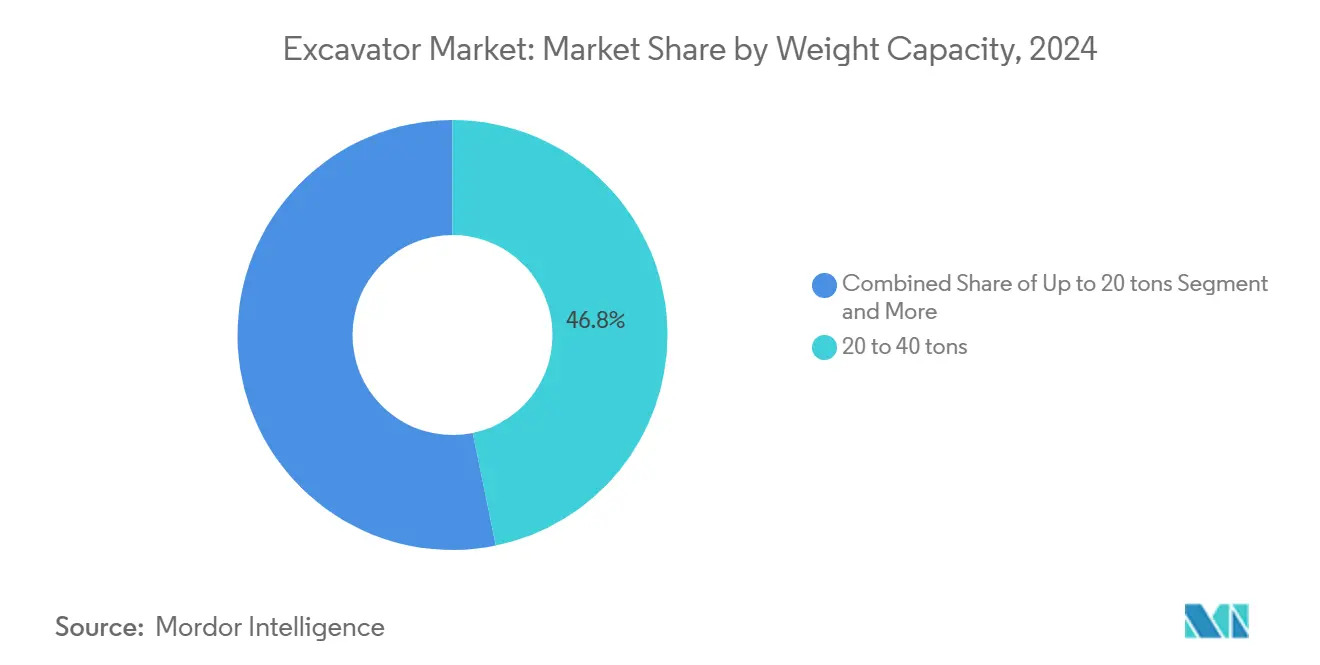

- By weight capacity, the 20 to 40 ton segment accounted for 46.27% of the excavator market size in 2024, whereas sub-20 ton units are forecast to post an 8.41% CAGR to 2030.

- By size classification, medium excavators accounted for 49.12% of the global excavator market in 2024, while mini excavators are projected to grow at a 10.18% CAGR through 2030.

- By geography, Asia-Pacific commanded 48.33% of the excavator market share in 2024; Europe is projected to expand fastest at an 8.63% CAGR through 2030.

Global Excavator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-Led Public Spending Surge | +1.8% | North America, Europe, India | Medium Term (2–4 Years) |

| Shift Toward Rental and Leasing Models | +1.2% | North America, Europe | Short Term (≤ 2 Years) |

| Electrification and Hybrid Launches | +0.9% | Europe, North America, Spill-Over to Asia-Pacific | Long Term (≥ 4 Years) |

| Automated Digging Systems in Mid-Tier SKUs | +0.7% | North America, Europe, Expanding to Asia-Pacific | Medium Term (2–4 Years) |

| Hydrogen ICE Prototypes for ≥40-Ton Crawlers | +0.4% | Europe, North America | Long Term (≥ 4 Years) |

| OEM Localization in South America & Africa | +0.3% | South America, Africa | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Infrastructure-led Public Spending Surge (2025-2030)

Government infrastructure commitments create sustained excavator demand through megaproject pipelines extending beyond traditional construction cycles. The US Infrastructure Investment and Jobs Act allocates USD 550 billion in new spending over 8 years, with transportation infrastructure receiving USD 284 billion and utilities USD 266 billion, directly translating to earthmoving equipment requirements[1]Daniel Fidanque, "February Update: 2025 Construction Outlook & Trends," Machinery Partner, machinerypartner.com. . Germany's infrastructure modernization program targets USD 1.1 trillion investment through 2030, emphasizing transportation networks and energy grid upgrades that necessitate heavy excavation work. This spending surge differs from cyclical construction booms by focusing on long-term asset replacement rather than capacity expansion, creating predictable demand patterns that enable OEMs to optimize production planning and dealer inventory management. The infrastructure emphasis on utility upgrades and transportation modernization particularly benefits compact and mid-size excavator segments, as these projects require precision digging in confined spaces rather than bulk earthmoving. State-level implementation of federal programs generates additional demand multipliers, with individual states launching complementary infrastructure initiatives that extend project timelines and equipment utilization rates.

Accelerating Shift Toward Rental and Leasing Business Models

Rental penetration approaching 56% for construction equipment fundamentally alters excavator ownership economics and fleet composition strategies. United Rentals' acquisition of H&E Equipment Services for USD 2.3 billion in 2024 demonstrates consolidation dynamics that concentrate rental fleet purchasing power and influence OEM pricing strategies[2]"Yellow Table: 10 Largest Construction Equipment Manufacturers of 2024," equipmentworld.com.. Rental companies increasingly demand higher-specification machines with telematics integration and predictive maintenance capabilities, driving technology adoption across mid-tier product lines previously limited to basic functionality. This shift creates revenue stability for OEMs through fleet replacement cycles and aftermarket services, while reducing cyclical exposure to individual contractor purchasing decisions. The rental model particularly benefits electric excavator adoption by eliminating upfront cost barriers and providing fleet-level charging infrastructure that individual contractors cannot justify. Rental companies' focus on total cost of ownership rather than acquisition price incentivizes OEMs to develop more durable, efficient machines with lower operating costs, accelerating technological advancement across the industry.

Electrification and Hybrid-Powertrain Launches Across All Tonnage Classes

Electric excavator market expansion reaches USD 70.96 billion in 2025, with China accounting for 80% of global electric construction equipment sales, demonstrating rapid technology maturation and cost competitiveness. Volvo's EC230 Electric excavator achieves performance parity with diesel equivalents while reducing operating costs by 30-40% in urban applications where noise restrictions and emission zones limit conventional equipment access. Battery technology advances enable 8-hour operation cycles with 30-minute fast charging, addressing the primary adoption barrier of downtime during recharging periods. The electrification trend extends beyond environmental compliance to operational advantages, including instant torque delivery for improved digging performance and reduced maintenance requirements due to fewer moving parts. OEMs leverage electric platforms to introduce advanced automation features that require precise power control, creating competitive differentiation through integrated technology packages rather than standalone electrification.

Automated/Machine-Control Digging Systems Moving from Premium to Mid-Tier SKUs

Grade control and machine guidance systems previously exclusive to premium excavator models now appear in mid-tier offerings as component costs decline and competitive pressures intensify. Technology democratization enables contractors with smaller fleets to access productivity enhancements that previously required capital investments exceeding USD 500,000 per machine. Automated digging systems reduce operator skill requirements while improving precision and fuel efficiency, addressing labor shortages that constrain construction activity across developed markets. The integration of machine control with telematics platforms creates data-driven fleet management capabilities that optimize equipment utilization and maintenance scheduling. This technological shift particularly benefits rental companies by reducing operator training requirements and minimizing equipment damage from inexperienced users, accelerating adoption rates across the rental fleet segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel and Battery Raw-Material Prices | -1.1% | Global, High Exposure in Asia-Pacific Plants | Short Term (≤ 2 Years) |

| Cyclical Construction Demand and Interest-Rates | -0.8% | North America, Europe, Global Spill-Over | Medium Term (2–4 Years) |

| Tightening EU Stage V / China IV Emission Rules Raising Compliance Costs | -0.6% | Europe, China, Expanding to Emerging Asian Markets | Medium Term (2–4 Years) |

| Semiconductor and Hydraulic-Valve Shortages Delaying Deliveries (Under-Reported) | -0.5% | Global, Concentrated in North America and Asia-Pacific Supply Chains | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Volatile Steel and Battery Raw-Material Prices Compressing OEM Margins

Raw material cost volatility creates unprecedented margin pressure as steel prices fluctuate between USD 600-900 per ton while lithium carbonate costs range from USD 15,000-45,000 per ton, directly impacting excavator production economics. Komatsu's forecast of 27.3% operating profit decline for fiscal 2026 reflects industry-wide challenges in managing input cost inflation while maintaining competitive pricing. Battery material shortages particularly affect electric excavator production, with nickel and cobalt supply constraints limiting production scalability despite growing demand. OEMs implement hedging strategies and long-term supplier contracts to mitigate volatility, but these measures reduce flexibility and increase working capital requirements. The material cost pressure forces consolidation among smaller OEMs unable to achieve procurement scale economies, while larger manufacturers gain competitive advantages through vertical integration and supply chain control.

Cyclical Construction Demand and Interest-Rate Sensitivity

Construction equipment demand remains highly sensitive to interest rate cycles, with financing costs directly affecting contractor equipment acquisition decisions and project viability. Rising interest rates increase the total cost of ownership for financed excavator purchases, driving contractors toward rental options and delaying fleet replacement cycles. Cat Financial's 9% growth in retail new business volume demonstrates strong demand for financing solutions, but higher financing rates compress profit margins and limit accessibility for smaller contractors. Economic uncertainty creates project delays and cancellations that reduce equipment utilization rates, particularly affecting larger excavator segments used in major construction projects. The cyclical nature of construction demand creates inventory management challenges for OEMs and dealers, requiring sophisticated demand forecasting and production planning to avoid overproduction during downturns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Crawler Dominance Meets Urban Specialization

Short-swing-radius excavators achieve 9.84% CAGR through 2030 despite crawler excavators maintaining 52.13% market share in 2024, reflecting urbanization pressures that prioritize maneuverability over raw power. Urban construction projects increasingly require excavators capable of operating in confined spaces with minimal tail swing, driving demand for specialized variants that sacrifice some digging force for enhanced mobility. Crawler excavators retain dominance in infrastructure and mining applications where stability and digging power outweigh mobility constraints, but face pressure from wheeled variants in road construction and utility work where rapid repositioning reduces project timelines.

Long-reach excavators serve niche applications in dredging and demolition, while the "Others" category encompasses specialized variants for forestry and material handling that represent emerging market opportunities. The segmentation shift reflects broader construction industry evolution toward specialized equipment optimized for specific applications rather than general-purpose machines. This trend benefits OEMs with diverse product portfolios while challenging manufacturers focused on traditional crawler designs to expand their offerings or risk market share erosion.

By Propulsion Type: Electric Transition Accelerates Despite ICE Dominance

Battery electric excavators surge at 13.72% CAGR while internal combustion engines maintain 78.06% market share in 2024, creating a bifurcated market where adoption patterns vary dramatically by application and geography. Electric variants achieve cost competitiveness in urban applications where noise restrictions, emission zones, and fuel cost savings justify higher acquisition prices. Hydraulic and electric hybrid systems bridge the performance gap by providing electric operation for precision work while maintaining diesel power for heavy digging, appealing to contractors requiring operational flexibility.

The propulsion transition accelerates in Europe due to stringent emission regulations and urban access restrictions that limit diesel equipment operation. China's dominance in electric construction equipment manufacturing, representing 80% of global production, creates cost advantages that enable rapid market penetration in price-sensitive segments. ICE technology continues advancing through efficiency improvements and alternative fuel integration, with hydrogen combustion engines receiving regulatory approval for European markets, extending the viability of internal combustion platforms beyond traditional diesel applications.

By Weight Capacity: Mid-Range Leadership Faces Compact Challenge

Excavators in the 20 to 40 ton range command 46.27% market share in 2024, reflecting their versatility across construction, mining, and infrastructure applications, while compact units under 20 tons achieve 8.41% growth driven by urban construction and rental market preferences. The weight distribution reflects construction industry requirements for machines capable of handling diverse tasks without requiring specialized transport or site preparation. Kubota's 40% production capacity expansion in Germany specifically targets mini-excavator production, indicating OEM confidence in compact segment growth potential.

Above-40-ton excavators serve specialized mining and major infrastructure projects where productivity advantages justify higher operating costs and transport complexity. The weight segmentation increasingly correlates with technology adoption patterns, as compact excavators lead electric powertrain integration due to favorable power-to-weight ratios, while larger machines pioneer automation and remote operation capabilities. This technological divergence creates distinct market dynamics within weight categories, with compact segments competing on efficiency and mid-range machines emphasizing versatility.

By Size Classification: Medium Segment Stability Versus Mini Innovation

Medium excavators maintain 49.12% market share in 2024 through their optimal balance of capability and operational flexibility, while mini excavators accelerate at 10.18% CAGR driven by technological innovation and expanding application scope. The size classification reflects operational requirements more than weight specifications, with medium machines serving as industry workhorses for general construction and infrastructure projects. Mini excavator growth stems from urban construction density, landscape development, and utility work that requires precise operation in confined spaces.

Large excavators face cyclical demand patterns tied to major construction and mining projects, creating volatility that contrasts with steady medium segment performance. The classification system increasingly incorporates technology features alongside size specifications, as mini excavators integrate advanced hydraulics and automation features previously exclusive to larger machines. This technological convergence enables smaller excavators to compete for applications traditionally requiring larger equipment, expanding their addressable market and driving sustained growth rates above industry averages.

Geography Analysis

Asia-Pacific commands 48.33% market share in 2024 despite facing construction equipment market contraction, with China's excavator sales above 10 tons remaining at relatively low levels following consecutive years of declining demand. The region's market leadership stems from manufacturing concentration and domestic demand from infrastructure development, though growth patterns vary significantly between countries. India implements CEV-V emission norms effective January 2025, creating replacement demand for older equipment while driving technology upgrades across the fleet. Japan's market maturity and focus on precision construction applications support premium excavator segments, while Southeast Asian markets benefit from infrastructure investment and urbanization trends. The region's dominance in electric construction equipment manufacturing, representing 80% of global production, positions Asia-Pacific as the technology leader despite current demand challenges.

Europe emerges as the fastest-growing region with 8.63% CAGR through 2030, driven by infrastructure modernization, urban housing construction, and stringent emission regulations that accelerate equipment replacement cycles. Germany's USD 1.1 trillion infrastructure spending bill and broader European Union infrastructure initiatives create sustained demand for earthmoving equipment across multiple project categories. EU Stage V emission standards impose compliance costs exceeding USD 15,000 per machine but drive technology advancement and fleet renewal that benefits OEMs with advanced product portfolios. The region's focus on urban construction and space-constrained projects particularly benefits compact and short-swing-radius excavator segments, while renewable energy infrastructure development creates new application areas for specialized equipment.

North America maintains steady demand supported by the Infrastructure Investment and Jobs Act's USD 550 billion in new spending, though rental market dynamics alter traditional ownership patterns and equipment specification requirements. The region's construction equipment rental penetration approaching 56% creates concentrated purchasing power among major rental companies, influencing OEM product development and pricing strategies. South America and Middle East & Africa represent emerging opportunities as OEMs establish local manufacturing to avoid tariff escalations and serve growing infrastructure demands, with Brazil and South Africa leading regional development initiatives that require substantial earthmoving equipment deployment.

Competitive Landscape

The excavator market exhibits moderate consolidation with established OEMs maintaining dominant positions through technological differentiation and global distribution networks, while emerging competition intensifies from Chinese manufacturers and electric vehicle specialists entering construction equipment segments. Strategic patterns emphasize technology integration, with OEMs investing heavily in electrification, automation, and connectivity features to differentiate products and capture aftermarket revenue streams through data-driven services.

White-space opportunities emerge in hydrogen-powered heavy excavators and autonomous operation systems, where regulatory approval and technology maturation create first-mover advantages for innovative manufacturers. JCB's hydrogen combustion engine approval for European markets represents breakthrough technology that could reshape propulsion competition, while Liebherr's USD 2.8 billion partnership with Fortescue demonstrates large-scale deployment of electric and autonomous excavators in mining applications.

Technology adoption patterns favor OEMs with strong R&D capabilities and manufacturing scale, as the integration of advanced features requires substantial investment in product development and production tooling that smaller competitors cannot easily replicate.

Excavator Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Hitachi Construction Machinery Co., Ltd.

-

Volvo Construction Equipment AB

-

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fortescue Metals Group and Liebherr announced a USD 2.8 billion partnership to deploy 475 zero-emission machines, including 55 electric R 9400 E excavators, creating one of the world's largest zero-emission mining fleets with autonomous haulage systems and fast-charging infrastructure.

- September 2024: Fortescue Metals Group and Liebherr announced a USD 2.8 billion partnership to deploy 475 zero-emission machines, including 55 electric R 9400 E excavators, creating one of the world's largest zero-emission mining fleets with autonomous haulage systems and fast-charging infrastructure.

Global Excavator Market Report Scope

| Crawler Excavators |

| Wheeled Excavators |

| Short-Swing-Radius Excavators |

| Long-Reach Excavators |

| Others |

| Internal Combustion Engine |

| Hydraulic and Electric |

| Up to 20 tons |

| 20 to 40 tons |

| Above 40 tons |

| Mini/Midi |

| Medium |

| Large |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Crawler Excavators | |

| Wheeled Excavators | ||

| Short-Swing-Radius Excavators | ||

| Long-Reach Excavators | ||

| Others | ||

| By Propulsion Type | Internal Combustion Engine | |

| Hydraulic and Electric | ||

| By Weight Capacity | Up to 20 tons | |

| 20 to 40 tons | ||

| Above 40 tons | ||

| By Size Classification | Mini/Midi | |

| Medium | ||

| Large | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which excavator segment is growing the fastest?

Short-swing-radius excavators are expanding at a 9.84% CAGR, reflecting demand for maneuverable machines in dense urban projects.

What proportion of excavators use diesel engines today?

Diesel and other ICE models still account for 78.06% of global shipments, although electric variants are gaining share quickly.

Why are rental companies important to future demand?

Rental firms now control 56% of North American equipment fleets, concentrating purchasing decisions and pushing OEMs toward telematics-ready, low-emission machines.

Which region is expected to post the highest growth through 2030?

Europe leads with an 8.63% CAGR thanks to USD 1.1 trillion in infrastructure commitments and stringent Stage V emission standards.

What is the main raw-material risk to OEM profitability?

Volatile steel and battery-material prices can swing OEM margins by more than 100 basis points, prompting hedging and long-term supply contracts.

Page last updated on: