Market Overview

| Study Period | 2019 - 2031 |

|---|---|

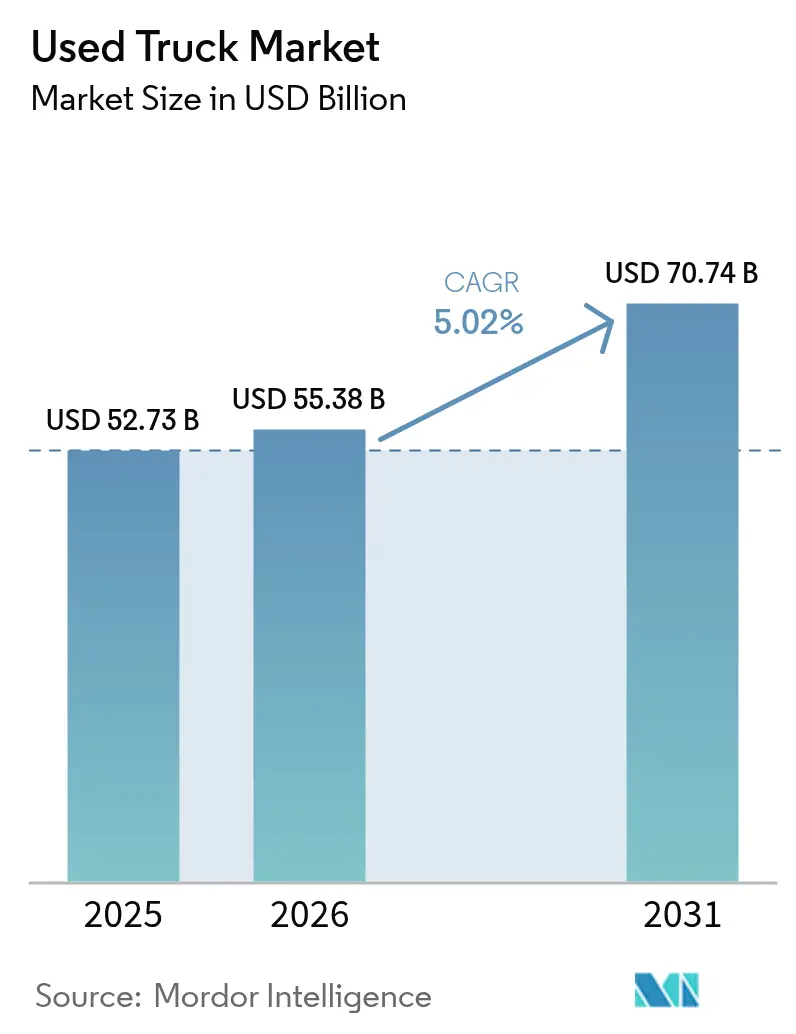

| Market Size (2026) | USD 55.38 Billion |

| Market Size (2031) | USD 70.74 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Used Truck Market Analysis by Mordor Intelligence

The used truck market size is expected to increase from USD 52.73 billion in 2025 to USD 55.38 billion in 2026 and reach USD 70.74 billion by 2031, growing at a CAGR of 5.02% over 2026-2031. This expansion reflects a structural shift in fleet-ownership economics as carriers weigh up-front capital constraints against tightening emission rules and rising digital-auction penetration. Heavy-duty models still anchor residual values, but last-mile demand is tilting growth toward lighter classes. Digital marketplaces are compressing information gaps, while certified pre-owned programs from leading truck makers are raising trust in the secondary channel. Supply patterns also hinge on regulatory divergence, with European NOx limits discouraging older imports even as scrappage incentives in India remove aged inventory and lift prices for mid-life assets.

Key Report Takeaways

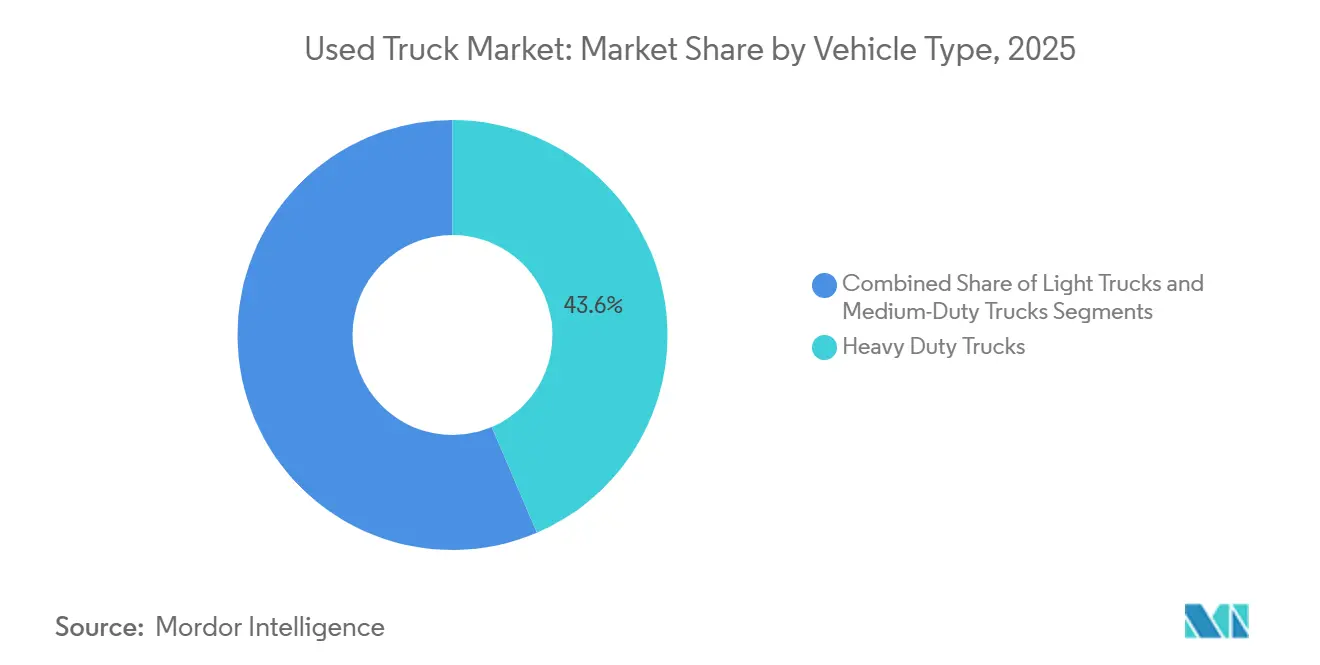

- By vehicle type, heavy-duty trucks led the used truck market with a 43.57% share in 2025, while light trucks are projected to expand at a 7.69% CAGR to 2031.

- By fuel type, diesel held a commanding 93.36% used truck market share in 2025, while the hybrid and battery-electric segment is expected to post a 22.55% CAGR through 2031.

- By age bracket, 4-7-year-old vehicles accounted for 38.39% of the used-trucks market in 2025, whereas trucks up to 3 years old are set to post a 9.23% CAGR through 2031.

- By vehicle class, Class 8 maintained 39.42% of the used truck market share in 2025, whereas Class 4 is set to grow at a 7.18% CAGR between 2026 and 2031.

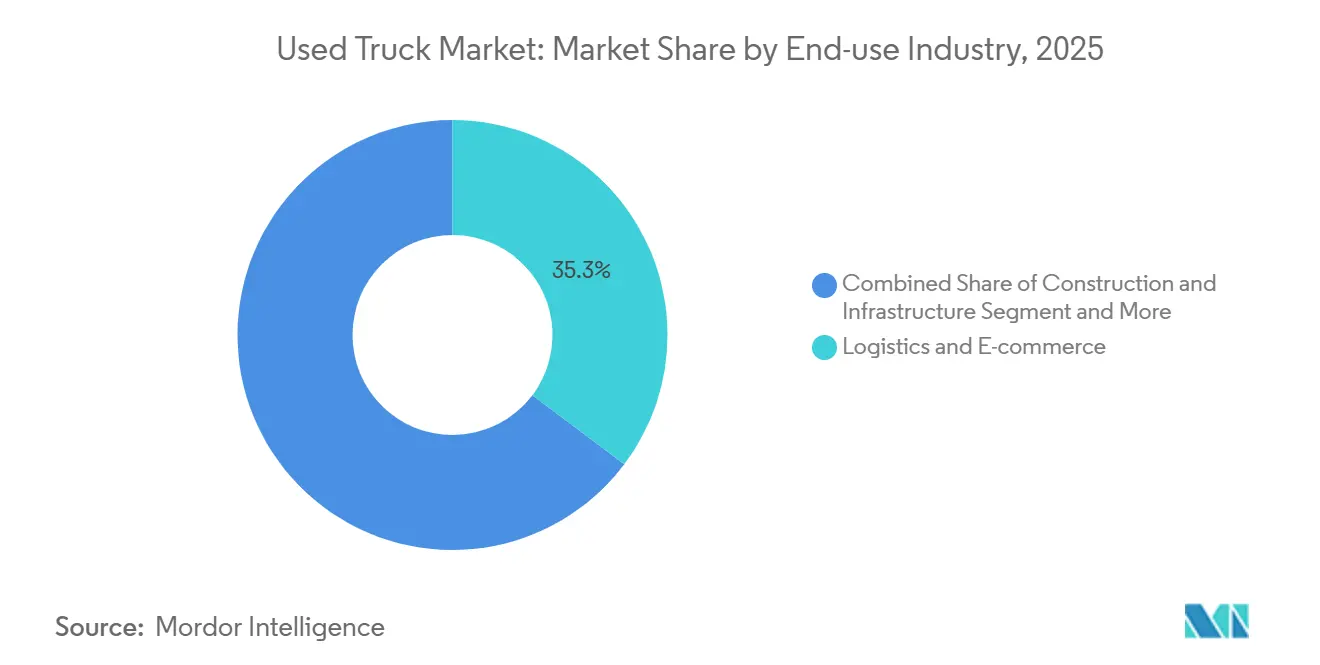

- By end-use industry, logistics and e-commerce led the used truck market with a 35.27% share in 2025, while construction and infrastructure are projected to register a CAGR of 9.02% through 2031.

- By sales channel, independent dealers captured 53.94% of 2025 revenues, while online peer-to-peer and auction platforms are advancing at a 12.31% CAGR to 2031.

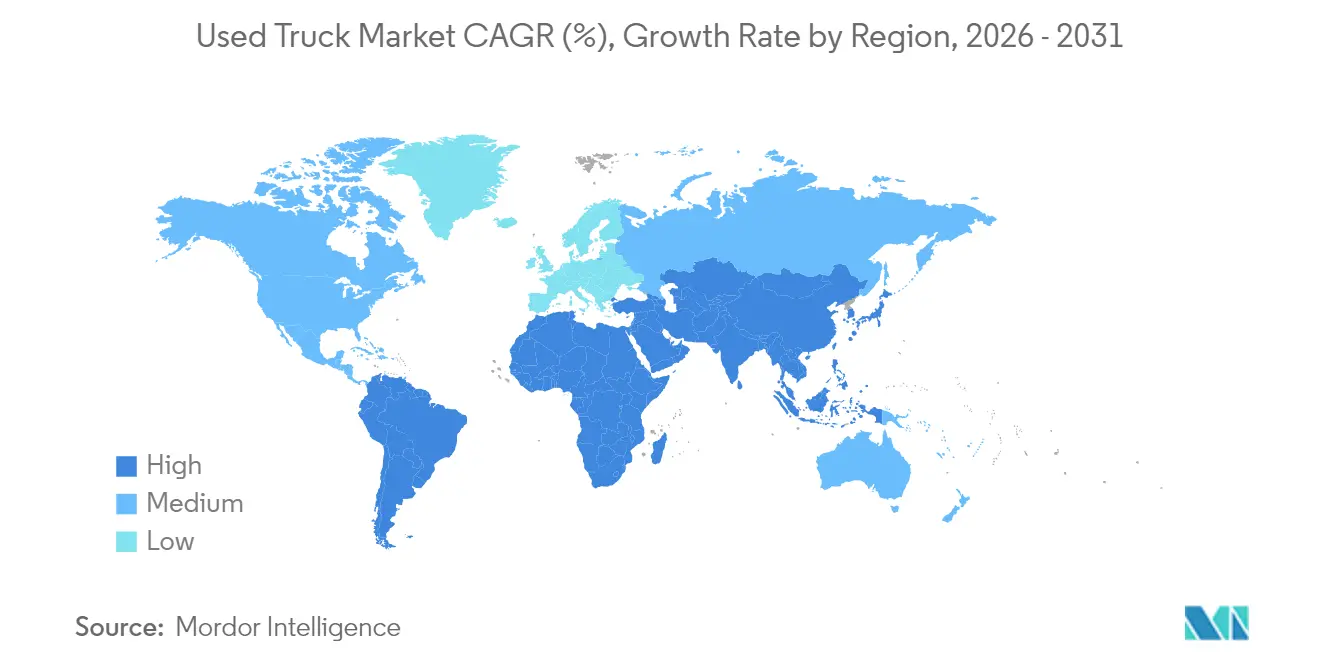

- By geography, Asia-Pacific retains the world’s most extensive regional fleet base, capturing 47.92% market share. In contrast, the Middle East and Africa are expected to lead regional growth, posting a 7.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Used Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure-Led Construction Booms | +1.2% | India, ASEAN core (Indonesia, Vietnam, Thailand) | Medium Term (2-4 Years) |

| E-Commerce Last-Mile Expansion | +1.0% | North America, with spillover to urban Latin America | Short Term (≤ 2 Years) |

| OEM Certified Pre-Owned Programs | +0.8% | Europe (Germany, France, UK, Italy, Spain) | Medium Term (2-4 Years) |

| Digital Wholesale Auctions | +0.7% | Middle East, North Africa, with global digital reach | Short Term (≤ 2 Years) |

| Fleet Electrification Targets | +0.6% | China, with secondary effects in Southeast Asia | Medium term (2-4 years) |

| Tax Incentives on Used Commercial Vehicles | +0.4% | Brazil, with potential extension to Argentina and Chile | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure-Led Construction Booms in India and ASEAN Stimulating Heavy Used-Truck Turnover

The National Infrastructure Pipeline earmarks more than USD 1.4 trillion to transport and logistics projects, which is raising heavy-duty registrations that later flow into the used truck market[1]Ministry of Finance, "A Strong V-Shaped Recovery of Economic Activity", PIB Delhi, pib.gov.in. Large projects such as highway corridors and port expansions shorten ownership cycles because contractors prefer asset-light balance sheets once projects end. Resulting mid-life trucks enter secondary channels in good condition, attracting small builders that cannot finance new equipment. India’s 2024 scrappage policy, offering registration-fee waivers for retiring trucks aged over 15 years, removes aged assets and supports unit values in the 4-to-7-year window[2]"Scrappage policy – significant potential with about 1.1 million medium & heavy commercial vehicles older than 15 years: ICRA", ICRA, icra.in. Comparable public works agendas in Indonesia and Vietnam have similar knock-on effects, ensuring a stable pipeline of compliant, late-model heavy dumpers and tractors.

E-commerce Last-Mile Expansion in North America Triggering Demand for Used Light-Duty Trucks

Rapid parcel growth led carriers to open micro-hubs that rely on Class 3-5 box trucks for same-day delivery. Compliance deadlines under the U.S. Environmental Protection Agency’s Clean Truck Plan, finalized in 2024, encourage fleets to retire diesel models before 2027 NOx ceilings take hold[3]"Final Rule: Multi-Pollutant Emissions Standards for Model Years 2027 and Later Light-Duty and Medium-Duty Vehicles", EPA, epa.gov. Turnover raises the supply of low-mileage units that owner-operators can afford. In parallel, zero-emission pilot zones in several U.S. metros spur early adopters to remarket first-generation electric vans, broadening fuel mix in the secondary channel without sacrificing range for urban drops. Light-truck absorption remains robust because these vehicles require modest capital and deliver quick payback.

OEM Certified Pre-Owned Programs in Europe Enhancing Trust and Residual Values

Truck makers now refurbish returned lease units under standardized checklists and attach multi-year powertrain warranties, strengthening confidence in the Used Truck Market. Buyers gain transparency into mileage, repair history, and telematics data, helping reduce volatility in the total cost of ownership. Demand for certified units rose after the European Commission’s Corporate Sustainability Reporting Directive made Scope 3 disclosures mandatory from 2024. Large shippers thus prefer documented fuel-efficient vehicles over unverified inventory. National development banks in Germany and France extend low-interest lines to small hauliers acquiring Euro VI-E-compliant CPO trucks, reinforcing take-up.

Digital Wholesale Auctions Broadening Buyer Pool, Especially in Middle East

Online bidding removes geographic constraints, enabling Gulf-based firms to source surplus inventory from Europe and North America in real time. Blockchain-backed title tools cut fraud risk and entice banks to underwrite cross-border invoices. The schemes mesh with regional logistics visions that aim to diversify oil economies via freight corridors. Importers value Euro V and Euro VI trucks that comply with local sulfur mandates but still cost less than new purchases. The convenience of door-to-door shipping quotes within auction dashboards further accelerates platform shift.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Euro-VII/Phase-3 NOx Rules | -0.5% | European Union, with spillover to UK and Norway | Medium term (2-4 years) |

| Low-Cost New Chinese Trucks | -0.4% | Sub-Saharan Africa, North Africa | Medium term (2-4 years) |

| Limited Financing Options | -0.3% | ASEAN rural markets (Indonesia, Philippines, Vietnam) | Long term (≥ 4 years) |

| Chip Shortages | -0.2% | Global, with pronounced effects in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Euro-VII/Phase-3 NOx Rules Discouraging Older Diesel Imports in EU

Starting in 2027, the Euro VII framework will prohibit many pre-Euro VI trucks from accessing low-emission corridors, effectively dampening the demand for older diesel vehicles. In Germany and the UK, municipal clean-air zones are penalizing heavy vehicles that don't meet compliance standards, further dissuading potential buyers. Importers are shifting their focus to Eastern Europe and North Africa for liquidating these vehicles. This shift is narrowing the pool of buyers within the EU and driving up prices for compliant Euro VI vehicles.

Low-Cost New Chinese Trucks Compressing Used Price Premiums in Africa

New heavy-duty models from Chinese OEMs are priced significantly lower, around 30-40% less, than their Western counterparts, which limits the resale value of imported trucks aged 4-7 years. In African cities, the improved availability of spare parts has reduced the maintenance benefits that European brands previously offered, thereby tightening profit margins for traditional exporters. To navigate this shift, traders with adaptable logistics strategies are redirecting inventory to markets like Latin America and Southeast Asia. However, these shifts come with challenges, including increased freight costs and extended delivery times, which constrain the growth potential of the used trucks market in these regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Heavy-Duty Trucks Remain Dominant While Light Trucks Accelerate

Heavy-duty trucks captured 43.57% of the used-truck market share in 2025, underscoring their entrenched role in long-haul freight and infrastructure hauling. They remain the preferred choice for fleets that prioritize payload capacity, durability, and an extensive service network. Yet tightening emission rules and shifting delivery patterns are prompting operators to reassess fleet composition, opening space for lighter formats that better suit urban corridors. Manufacturers are responding by broadening certified pre-owned programs that include turnkey maintenance bundles, raising buyer confidence in previously owned heavy rigs. Against this backdrop, residual values for well-maintained heavy-duty units stay resilient even as buyers diversify into smaller classes.

Light trucks in the Class 3–5 band are projected to expand at a 7.69% CAGR through 2031, the fastest pace among all weight classes. This surge reflects last-mile e-commerce growth, municipal clean-air initiatives, and lower capital hurdles for independent owner-operators. Fleets cycling out of first-generation electric vans are releasing late-model diesel and battery-electric light trucks into secondary channels, offering budget-minded buyers multiple propulsion choices. Urban delivery contracts often specify tight turning radii and low curb weights, making light trucks the logical selection for same-day routes. Digital auction houses expand access to these assets by publishing telematics data and inspection reports, thereby shortening due diligence cycles.

By Fuel Type: Diesel Dominates but Electrification Momentum Builds

Diesel engines retained 93.36% of the used truck market share in 2025, supported by ubiquitous fueling infrastructure and proven reliability in high-torque duty cycles. Operators value the established parts ecosystem and the predictable maintenance intervals associated with diesel powertrains. Even as zero-emission mandates tighten, many carriers hedge compliance risk by refreshing to newer, cleaner diesel models rather than switching to propulsion entirely. Certified pre-owned channels reinforce this trend by bundling extended engine warranties and advanced telematics for mileage verification. Consequently, diesel continues to anchor price discovery across dealer lots and digital platforms alike.

Hybrid and battery-electric trucks are scaling at a 22.55% CAGR through 2031, the swiftest rate across the fuel type spectrum. Early adopters who trialed first-wave electric rigs now release them into resale pools, creating an emerging inventory stream for smaller fleets eager to test zero-tailpipe technology. Government incentives, such as scrappage credits or clean-transport rebates, further tilt economics in favor of electrified options. Buyers weigh the lower operating costs of electricity against the uncertainty of battery health, making OEM-issued battery-warranty transfers a critical differentiator. Over time, improved charging networks and standardized diagnostics are expected to normalize valuation models for used electric trucks.

By Age Bracket: 4–7 Years Remain the Sweet Spot

Trucks aged 4 to 7 years accounted for 38.39% of transactions in 2025, setting the benchmark for liquidity in the secondary market. These assets typically fall just outside factory warranty yet carry complete service histories, allowing buyers to balance price against remaining life. Leasing companies and large corporate fleets often rotate vehicles at this interval to maintain uptime targets, feeding a steady pipeline into independent dealerships. Dealers recondition these units and append limited warranties that mimic new-truck assurances, reinforcing mid-cycle value. For buyers in emerging markets, this bracket offers a combination of modern emissions compliance and manageable acquisition costs.

Units under 3 years old are advancing at a 9.23% CAGR through 2031, the fastest growth inside the age matrix. OEM buy-back schemes accelerate this flow by guaranteeing remarketing outlets and stabilizing residual values. Younger equipment often comes bundled with transferable telematics subscriptions, enabling predictive maintenance that appeals to data-driven fleets. Financial institutions view low-mileage assets as lower-risk collateral, expanding financing availability for small operators. The combination of technology features, remaining warranty coverage, and favorable loan terms supports rapid turnover in this segment.

By Vehicle Class: Class 8 Leads, Class 4 Moves Fastest

Class 8 tractors accounted for 39.42% of the used truck market share in 2025, reflecting their indispensability to bulk freight corridors and cross-border commerce. Long-distance hauliers rely on the payload advantages and aerodynamic refinements of these heavy rigs to optimize cost per mile. A robust dealer network keeps downtime to a minimum through readily available parts and trained technicians. Even as lighter classes gain traction in urban delivery, Class 8 units continue to anchor the resale ecosystem for fleet renewal strategies. Their dominance also encourages auction houses to curate specialized lanes for this class, thereby improving price transparency.

Class 4 trucks are forecast to register the quickest uptick at a 7.18% CAGR through 2031. Urban logistics firms favor narrower frames and compliance with evolving low-emission zone regulations. Municipal authorities often grant Class 4 vehicles preferential access and parking permits, reinforcing demand. Refurbishers can upfit these chassis with refrigerated boxes, flatbeds, or utility booms, broadening end-use appeal. Digital marketplaces expedite cross-country sourcing of Class 4 units, matching surplus fleet inventory with emerging last-mile operators.

By End-use Industry: Logistics and E-commerce Dominate

Logistics and e-commerce delivery captured 35.27% of the used-truck market share in 2025, mirroring continued online retail expansion and consumer expectations for faster fulfillment. Parcel carriers rotate assets frequently to maintain service reliability, enriching the secondary pool with relatively young, well-spec’d trucks. Telematics-enabled route optimization favors vehicles that integrate seamlessly with fleet-management software, a factor now common in used-truck listings. Warehousing networks sited near urban centers amplify short-haul demand that lighter trucks efficiently meet. Consequently, logistic operators remain the primary price-setters across multiple weight classes.

Construction and infrastructure projects are projected to grow at a 9.02% CAGR, the highest among end-use categories. Governments in Asia and Latin America are allocating substantial budgets for roads, ports, and public facilities, prompting contractors to acquire rugged tippers and concrete mixers. These buyers appreciate the cost advantages of reliable mid-life trucks over new units that face immediate depreciation. Seasonal project cycles ensure a recurring flow of equipment back into resale lanes once work concludes, supporting a circular market dynamic. The segment also benefits from favorable lending programs for small subcontractors, keeping demand buoyant through economic cycles.

By Sales Channel: Independent Dealers Hold Ground, Digital Marketplaces Surge

Independent dealers controlled 53.94% of the used truck market share in 2025, underscoring their pivotal role in localized asset remarketing. They cultivate community relationships, tailor payment schedules, and often package trade-in deals that resonate with small fleet owners. In-house service bays enable quick turnaround for reconditioning, shortening the time assets sit idle. Face-to-face negotiation remains a cultural norm in many regions, preserving the relevance of brick-and-mortar yards. Dealer consortia are also investing in online storefronts to widen geographic reach without diluting relationship capital.

Online peer-to-peer and auction platforms are set to climb at a 12.31% CAGR, outpacing all other channels. Transparent pricing dashboards and remote inspection tools reduce information asymmetry, drawing in first-time buyers who value convenience. Cross-border logistics integration lets Middle Eastern and African importers source compliant Euro-standard trucks without travel, shrinking procurement cycles. Blockchain-anchored title verification builds lender confidence, unlocking new financing avenues. As platform algorithms refine asset matching, digital channels are expected to capture greater mindshare among tech-savvy operators.

Geography Analysis

Asia-Pacific accounted for 47.92% of global volume in 2025, cementing its position as the nucleus of the used truck market. Infrastructure megaprojects in India and Southeast Asia keep heavy-duty units circulating swiftly between primary and secondary owners. China’s electrification trajectory is prompting fleets to sell diesel stock earlier in the lifecycle, enriching export pipelines across the region. Digital auction hubs in Singapore and Bangkok simplify cross-border trade, tightening regional price spreads. Collectively, these factors reinforce Asia-Pacific’s standing as both the largest demand center and an increasingly sophisticated supply hub.

North America sustains steady activity as e-commerce networks grow denser and carriers pre-empt stricter EPA rules by refreshing assets. The easing of semiconductor bottlenecks improves new-truck availability, but many smaller fleets still gravitate toward used alternatives to conserve capital. State-level incentives for low-emission trucks create a selective appetite for late-model diesel and emerging electric units. Auction facilities across the Midwest and Southeast now livestream events, attracting buyers well beyond local markets. The region’s mature financing infrastructure further lubricates transaction velocity.

The Middle East and Africa region is poised for the fastest expansion, with a 7.41% CAGR through 2031. Gulf logistics visions emphasize multimodal freight corridors, driving appetite for heavy tractors that meet Euro V and Euro VI benchmarks. Online auctions connect regional buyers with surplus inventory in Europe and North America, compressing historical supply gaps. In Africa, the influx of competitively priced trucks strengthens trade routes that serve mining and agriculture. These dynamics collectively elevate the region from a peripheral participant to a focal growth frontier.

Competitive Landscape

The competitive environment is moderately concentrated, anchored by five global truck makers that operate certified pre-owned programs spanning inspection, warranty, and telematics. Such programs stabilize residual values and funnel repeat customers back into OEM ecosystems for parts and service. Auction giants add liquidity by offering real-time bidding and secured payment rails, making cross-border purchases routine. Independent dealers maintain relevance through community ties and bespoke financing, countering margin pressure with value-added reconditioning. Telematics vendors further empower buyers by surfacing asset-health data previously limited to primary owners.

Digital disruption continues to redraw boundaries among stakeholders. Auction platforms integrate blockchain-based title verification, lowering fraud risk and drawing institutional capital into floorplan financing. OEMs experiment with subscription-style aftercare on sold units, prolonging customer engagement beyond the point of sale. Dealers respond by forming alliances with fintech start-ups to streamline loan approvals and extend reach into underserved regions. As data transparency rises, price discovery tightens, leaving service quality as a chief differentiator in buyer decision-making.

Sustainability mandates are also shaping strategy. Manufacturers emphasize fuel-efficient powertrains and predictive maintenance packages to align with transport decarbonization targets. Fleets pursuing scope-based emissions reporting increasingly favor certified units whose fuel economy and service records are verifiable. Auction houses collaborate with environmental agencies to tag listings with emission-standard badges, easing compliance checks for buyers. Collectively, these moves underscore how regulatory forces, technology integration, and shifting customer expectations converge to shape competitiveness in the used-truck arena.

Used Truck Industry Leaders

-

Scania AB

-

Daimler AG

-

PACCAR Inc.

-

Navistar International Corporation

-

AB Volvo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Schneider National rolled out a complimentary third-party warranty for purchasers of pre-owned trucks. This warranty extends coverage for 90 days or up to 25,000 miles, covering the engine and aftertreatment systems of the most-used trucks sold by Schneider.

- October 2025: Renault Trucks showcased the newest iteration of its celebrated special edition: the Renault Trucks T 01 Racing. This model stands out with its sleek design, unparalleled customization options, and cutting-edge technology.

- April 2025: Thompson Truck Group acquired Lee-Smith Dealer Group, extending its regional footprint and service density.

- January 2025: John Deere showcased its first autonomous articulated dump truck (ADT) at CES 2025, aimed at mining and quarry environments.

Global Used Truck Market Report Scope

Used trucks are pre-owned commercial vehicles designed to transport materials and goods. These vehicles are available for resale in the secondary market.

The Used Truck market is segmented by vehicle type, fuel type, age bracket, vehicle class, end-use industry, sales channel, and geography. By vehicle type, the market is segmented into Light Trucks (Class 3-5), Medium-Duty Trucks (Class 6-7), and Heavy-Duty Trucks (Class 8 and Over 15 t). By fuel type, the market is segmented into Diesel, Gasoline, Natural Gas, LPG, and Hybrid and Battery-Electric. By age bracket, the market is segmented into 0 to 3 Years, 4 to 7 Years, 8 to 12 Years, and 12+ Years. By vehicle class, the market is segmented into Class 3, Class 4, Class 5, Class 6, Class 7, and Class 8. By end-use industry, the market is segmented into Construction and Infrastructure, Logistics and E-commerce Delivery, Mining and Quarrying, Agriculture and Forestry, Municipal and Utilities, and Others. By sales channel, the market is segmented into Independent Dealer, Franchised Dealer, OEM-Backed Certified Pre-Owned, and Online Peer-to-Peer and Auction. By geography, the market is segmented into North America (United States, Canada, and Rest of North America), South America (Brazil, Argentina, Chile, and Rest of South America), Europe (Germany, United Kingdom, France, Italy, Spain, Russia, and Rest of Europe), Asia-Pacific (China, India, Japan, South Korea, and Rest of Asia-Pacific), and Middle East (United Arab Emirates, Saudi Arabia, Qatar, South Africa, and Rest of Middle East).

Market forecasts are provided in terms of Value (USD) and Volume (Units).

By Vehicle Type

| Light Trucks (Class 3-5) |

| Medium-Duty Trucks (Class 6-7) |

| Heavy-Duty Trucks (Class 8 and Over 15 t) |

By Fuel Type

| Diesel |

| Gasoline |

| Natural Gas and LPG |

| Hybrid and Battery-Electric |

By Age Bracket

| Up to 3 Years |

| 4 to 7 Years |

| 8 to 12 Years |

| Above 12 Years |

By Vehicle Class

| Class 3 |

| Class 4 |

| Class 5 |

| Class 6 |

| Class 7 |

| Class 8 |

By End-use Industry

| Construction and Infrastructure |

| Logistics and E-commerce Delivery |

| Mining and Quarrying |

| Agriculture and Forestry |

| Municipal and Utilities |

| Others |

By Sales Channel

| Independent Dealer |

| Franchised Dealer |

| OEM-Backed Certified Pre-Owned |

| Online Peer-to-Peer and Auction |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Light Trucks (Class 3-5) | |

| Medium-Duty Trucks (Class 6-7) | ||

| Heavy-Duty Trucks (Class 8 and Over 15 t) | ||

| By Fuel Type | Diesel | |

| Gasoline | ||

| Natural Gas and LPG | ||

| Hybrid and Battery-Electric | ||

| By Age Bracket | Up to 3 Years | |

| 4 to 7 Years | ||

| 8 to 12 Years | ||

| Above 12 Years | ||

| By Vehicle Class | Class 3 | |

| Class 4 | ||

| Class 5 | ||

| Class 6 | ||

| Class 7 | ||

| Class 8 | ||

| By End-use Industry | Construction and Infrastructure | |

| Logistics and E-commerce Delivery | ||

| Mining and Quarrying | ||

| Agriculture and Forestry | ||

| Municipal and Utilities | ||

| Others | ||

| By Sales Channel | Independent Dealer | |

| Franchised Dealer | ||

| OEM-Backed Certified Pre-Owned | ||

| Online Peer-to-Peer and Auction | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the growth outlook for the used truck market through 2031?

It is projected to expand from USD 55.38 billion in 2026 to USD 70.74 billion by 2031, equating to a 5.02% CAGR.

Which vehicle type is expected to grow fastest in the secondary channel?

Light trucks in the Class 3-5 window are set to advance at about 7.69% CAGR on last-mile demand.

How are emissions rules shaping resale values in Europe?

Forthcoming Euro VII NOx limits narrow the buyer pool for older diesels, pushing up prices for Euro VI-compliant units.

Why are digital auctions important for Middle East buyers?

They provide direct access to Euro V and Euro VI inventory from Europe and North America, shortening procurement cycles and enhancing price discovery.

What role do certified pre-owned programs play?

CPO schemes add inspections and warranties, boosting buyer confidence and supporting residual values for 3-to-7-year-old trucks.

Page last updated on: