Uzbekistan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 0.96 Billion |

| Market Size (2030) | USD 1.29 Billion |

| Growth Rate (2025 - 2030) | 6.42% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uzbekistan Telecom MNO Market Analysis by Mordor Intelligence

The Uzbekistan Telecom MNO Market size is estimated at USD 0.96 billion in 2025, and is expected to reach USD 1.29 billion by 2030, at a CAGR of 6.42% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 36.60 million Subscribers in 2025 to 47.70 million Subscribers by 2030, at a CAGR of 5.43% during the forecast period (2025-2030).

Robust public-sector funding under the Digital Uzbekistan 2030 programme, rising mobile‐data consumption, rapid 5G roll-outs in major cities and the removal of foreign-investment barriers collectively underpin this expansion. Operators are prioritising fibre back-bone upgrades and AI-driven network optimisation to capture surging demand for social-video traffic while maintaining quality of service. Competitive intensity is escalating as the upcoming privatisation of Mobiuz is expected to unlock fresh capital and international know-how, further accelerating network modernisation. Although blended ARPU remains below USD 3, operators see upside in enterprise digitisation and premium OTT offerings that can lift margins over the medium term. [1]United Nations Development Programme, “Analytical Report on Internet Development in Uzbekistan,” undp.org

Key Report Takeaways

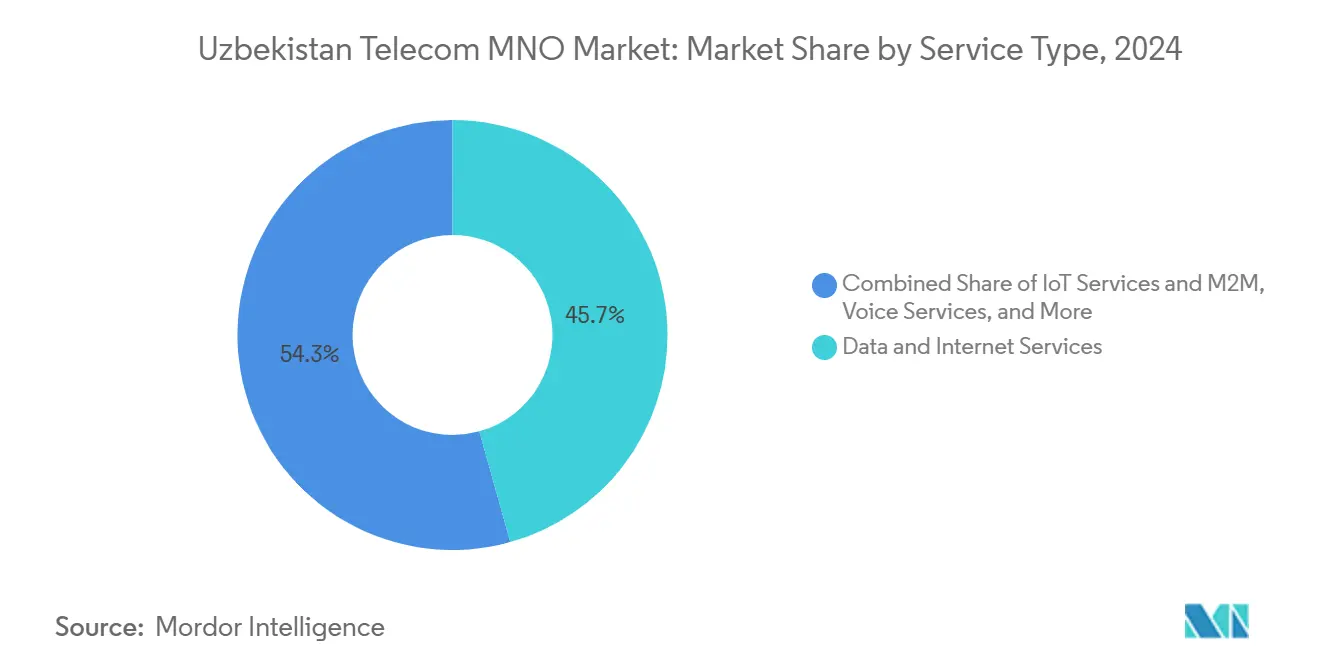

- By service type, data and internet services led with 45.67% revenue share in 2024, while OTT and PayTV services are projected to expand at a 6.28% CAGR through 2030.

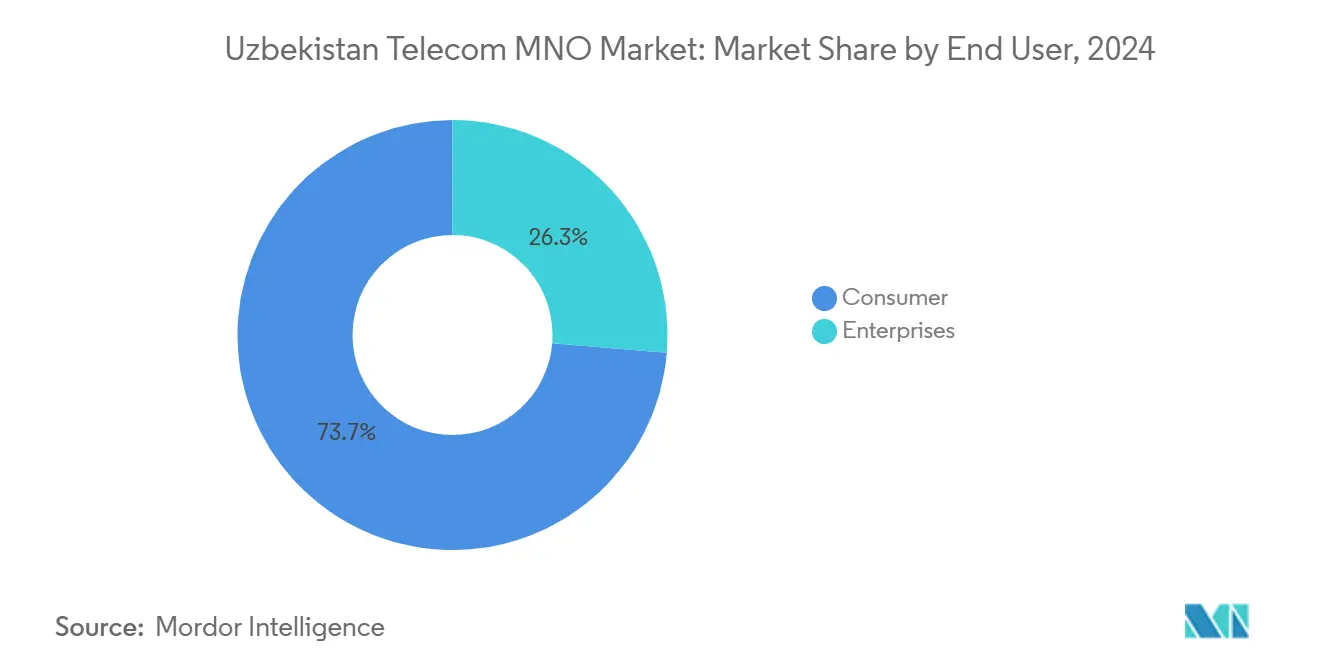

- By end user, the consumer segment accounted for 73.69% of the Uzbekistan Telecom MNO market share in 2024; enterprise services are advancing at a 6.63% CAGR through 2030.

Uzbekistan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G roll-outs concentrated in Tashkent and regional hubs | +1.2% | National, with early gains in Tashkent, Samarkand, Namangan | Short term (≤ 2 years) |

| Government "Digital Uzbekistan - 2030" fibre-backbone subsidies | +0.9% | National | Medium term (2-4 years) |

| Explosive mobile data usage driven by social-video apps | +1.1% | National | Short term (≤ 2 years) |

| Privatization of Mobiuz attracting fresh capex and know-how | +0.8% | National | Medium term (2-4 years) |

| Removal of Uztelecom's international gateway monopoly slashing IP-transit costs | +0.7% | National | Short term (≤ 2 years) |

| AI-driven network optimisation boosting ARPU and NPS for operators | +0.6% | National, concentrated in urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G roll-outs in Tashkent and regional hubs

Uzbektelecom activated non-stand-alone 5G across all regional centres, upgrading more than 3,500 base stations, while Perfectum’s alliance with Nokia positions the challenger for future stand-alone deployment. [2]VEON Ltd., “Beeline Uzbekistan to Deploy Predictive AI,” veon.com Operators initially focus on dense urban clusters to maximise spectrum returns and ARPU uplift before expanding to rural zones. Early adopters in Tashkent and Samarkand exhibit higher data-bundle uptake, validating the hub-and-spoke strategy. The learning curve gained in metropolitan cells lowers deployment risk for second-wave roll-outs. Incremental traffic from premium subscribers has already improved capacity-utilisation ratios, encouraging continued spectrum investment.

Digital Uzbekistan 2030 fibre-backbone subsidies

State funding expanded national fibre length from 36,600 km in 2019 to 68,600 km in 2020, reducing backbone CAPEX for private operators and accelerating nationwide coverage. Savings are redirected to customer-facing technologies, improving service innovation. Rural districts benefit disproportionately as public subsidies mitigate low-density economics, enabling smaller operators to extend footprints. Enhanced backhaul lowers latency, supporting OTT video quality and enterprise cloud adoption. The subsidy model also attracts foreign partners keen to leverage a ready‐made transport network. [3]World Bank, “Central Asia’s Digital Future,” worldbank.org

Explosive mobile-data usage driven by social-video apps

Mobile internet users nearly doubled to 27.2 million, driven by bandwidth-intensive video platforms that now dominate traffic mixes. Operators respond with capacity upgrades and tiered unlimited plans that lift data ARPU. While consumption growth boosts revenues, it also accelerates network-investment cycles, testing cash-flow resilience. Usage patterns favour larger data bundles, gradually shifting pricing away from pay-as-you-go models. Rising video engagement supports upselling of value-added subscriptions such as mobile TV and cloud gaming.

Privatization of Mobiuz attracting fresh capex and know-how

The sale of Universal Mobile Systems LLC (Mobiuz) is being run by Rothschild & Co with KPMG diligence, targeting foreign operators with both technical expertise and financial muscle. The transaction signals reduced state control and a welcoming stance toward external investors. New ownership is expected to modernise 4G/5G networks, inject AI analytics and upgrade customer-care platforms. Competitive pressure will rise as the acquirer pursues rapid subscriber gains and service differentiation. The deal also sets a precedent for further asset divestitures, reinforcing market liberalisation momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price wars keeping blended ARPU under USD 3 | -0.8% | National | Short term (≤ 2 years) |

| High 700 MHz and 3.5 GHz spectrum reserve prices raising debt loads | -0.6% | National | Medium term (2-4 years) |

| Deep-packet inspection regime curbing OTT and Pay-TV uptake | -0.4% | National | Medium term (2-4 years) |

| Rural power-grid instability causing >7% annual BTS downtime | -0.5% | Rural areas, secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying price wars keeping ARPU under USD 3

Average mobile-data cost stands at USD 0.60 per GB, among the lowest in Central Asia, squeezing operator margins. Deep-discount bundles win subscribers but undermine long-term cash generation needed for 5G build-outs. Promotional churn is rising as customers hop between short-term offers. Operators counter with bundled digital services and loyalty programmes to reduce price sensitivity. Sustained ARPU compression could delay rural expansion and slow quality-of-service upgrades.

High 700 MHz and 3.5 GHz spectrum reserve prices raising debt loads

Beeline paid USD 5.8 million for spectrum usage plus USD 4 million in licence fees in 2023, illustrating the heavy capital burden of high-demand bands. Smaller rivals face balance-sheet stress, potentially entrenching incumbent dominance. Elevated debt service limits flexibility to invest in power backups and AI tools. Staggered payment schedules ease near-term pressure but extend liabilities over the licence term, impacting credit ratings. Elevated spectrum costs might slow competitive entry, reducing consumer choice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Drive Market Evolution

Data and internet services commanded 45.67% of the Uzbekistan Telecom MNO market size in 2024, equating to roughly USD 437 million in service revenues. Changing consumption patterns favour streaming video, cloud gaming and digital payments, consolidating data-centric models at the expense of legacy voice. Operators monetise growth through tiered unlimited plans and sponsored-data partnerships with social platforms. OTT and PayTV services, although starting from a lower base, are forecast to grow at a 6.28% CAGR, propelled by widening smartphone ownership and improved 4G/5G coverage. Bundling content subscriptions into core tariffs has become a key churn-reduction tool. Voice and SMS revenues continue to decline, prompting operators to sunset copper infrastructure and repurpose spectrum for LTE and 5G. IoT and M2M remain nascent but strategically vital for enterprise solutions spanning logistics, agriculture and utilities. As average video bitrates rise, back-haul upgrades and edge caching become essential to sustain quality of experience and contain network operating costs.

OTT adoption underscores the shift from connectivity to platform economics. VEON’s digital revenue surged 50% year-on-year in 1Q25, validating the strategy of embedding content and financial services within an integrated app ecosystem VEON.COM. Operators that secure compelling local-language content libraries are best positioned to convert free users into paid subscribers. The success of data-centric segments will therefore hinge on partnerships with media producers, fintechs and cloud providers as well as continued investment in low-latency transport networks.

By End User: Enterprise Acceleration Reshapes Market Dynamics

Consumers still accounted for 73.69% of the Uzbekistan Telecom MNO market size in 2024, but enterprise services delivered the fastest revenue trajectory at a 6.63% CAGR. Industry 4.0 projects within mining, textiles and agribusiness are driving demand for private LTE, IoT telemetry and secure cloud connectivity. Government incentives under Digital Uzbekistan 2030 include tax breaks and co-financing for enterprise digitisation, lowering adoption barriers and expanding addressable spend. Early movers among operators are establishing dedicated B2B sales units and partnering with global cloud hyper-scalers to bundle connectivity with SaaS offerings. Longer contract tenures and lower churn improve revenue visibility compared with consumer prepaid plans. Vertical-specific solutions such as smart-irrigation and connected energy meters illustrate first-wave deployments shaping use-case playbooks.

Scaling enterprise uptake requires robust SLAs, converged fixed-mobile propositions and cybersecurity overlays that go beyond vanilla connectivity. Operators are piloting network slicing on 5G to guarantee latency and throughput for mission-critical applications. Meanwhile, consumer markets continue to migrate toward higher-bandwidth bundles but are reaching saturation in urban centres, pushing operators to tap rural demographics through aggressive handset financing and targeted digital-literacy campaigns. The dual-track strategy of retaining consumer scale while capturing enterprise value will shape revenue diversification over the next decade.

Geography Analysis

Uzbekistan’s telecommunications footprint is heavily urban-weighted, with Tashkent and other regional hubs accounting for the majority of data traffic and premium ARPU. Internet penetration stood at 55% in 2024, leaving substantial headroom for expansion, particularly in sparsely populated rural districts. Achieving universal coverage is estimated to require USD 6 billion in additional infrastructure spend by 2030, much of it earmarked for tower rollout and fibre back-haul in remote areas. The government’s hub-and-spoke investment strategy prioritises high-density corridors to accelerate payback cycles while layering subsidies to improve rural economics.

Power-grid instability outside major cities causes nearly 7% annual base-station downtime, prompting operators to deploy hybrid solar-diesel solutions and lithium-ion storage to improve uptime. Reliable rural connectivity is critical for e-government initiatives and cross-border trade corridors, positioning telecom infrastructure as a cornerstone of regional integration. Uzbekistan’s location offers the potential to act as a data transit node linking China, Europe and the Middle East once the state-owned international gateway monopoly is dismantled. Lower IP-transit costs could stimulate wholesale revenue streams and enhance affordability of international voice and data products for domestic users.

Regulatory obligations such as content filtering and lawful-intercept requirements impose compliance costs that are proportionally higher for smaller operators. Nonetheless, gradual liberalisation is improving the investment climate: the simplified licencing regime introduced in 2024 reduced permit-issuance times by 60%, supporting new market entry and niche service providers. Secondary cities like Namangan and Samarkand now attract targeted 5G pilots, reflecting rising local economic activity and the government’s decentralisation agenda. Over the long term, geographic revenue composition is expected to converge as rural broadband projects gain momentum and enterprise digitisation spreads to provincial industrial clusters.

Competitive Landscape

Uzbekistan’s mobile market hosts five nationwide operators, resulting in moderate concentration but intense rivalry. Beeline (VEON) leads with 8.2 million subscribers, closely followed by state-controlled Uztelecom brands and Mobiuz, the latter serving 7.8 million users ahead of its planned privatisation. Perfectum differentiates through early adoption of standalone 5G and premium data bundles targeting high-end segments. Competitive levers are shifting from price to network quality and digital-service ecosystems as operators deploy AI for predictive maintenance and personalised offers.

The impending sale of Mobiuz is likely to introduce an international strategic investor, accelerating technology infusion and tariff innovation. Market participants are therefore scaling fibre back-haul and piloting Open RAN to keep pace. Operators also partner with fintechs to embed mobile wallets and micro-credit within super-apps, aiming to deepen customer stickiness and monetise data traffic beyond mere megabytes delivered. VEON’s relocation to Tashkent IT Park underscores the strategic pivot toward digital-first operations and in-house product development capacity.

Regulatory guardrails on spectrum caps and infrastructure-sharing aims to balance competition while avoiding duplication. Joint-venture tower-cos are on the policy agenda, offering capex relief and faster rural roll-out. Industry 4.0 use-cases present a white-space opportunity where early partnerships with manufacturing conglomerates could establish first-mover advantages. Given the pace of liberalisation and technology uptake, competitive dynamics are expected to intensify, with differentiation anchored in network intelligence, customer experience and value-added ecosystem play.

Uzbekistan Telecom MNO Industry Leaders

Beeline

Ucell

UZmobile

Mobiuz

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Uzbekistan's State Assets Management Agency initiated the international privatisation of 100% state-owned telecom operator MobiUz (Universal Mobile Systems LLC), appointing Rothschild & Co as lead strategic advisor with KPMG conducting due diligence.

- May 2025: Beeline Uzbekistan relocated its headquarters to Tashkent's IT Park, accommodating 2,000 employees including specialised teams for digital services and fintech development.

- March 2025: Beeline Uzbekistan deployed predictive AI analytics in partnership with P.I. Works for customer-experience management, enabling proactive network issue resolution.

- September 2024: Uztelecom launched non-stand-alone 5G networks across all regional centers, modernizing over 3,500 base stations since Mar 2022.

Uzbekistan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Uzbekistan Telecom MNO market in 2025?

It stands at USD 956.07 million and is forecast to grow at a 6.24% CAGR to 2030.

What drives short-term revenue growth?

Rapid 5G roll-outs in major cities and surging video-streaming data consumption lift ARPU in high-traffic clusters.

Which service category grows the fastest through 2030?

OTT and PayTV services, supported by higher smartphone penetration and bundled streaming offers, expand at a 6.28% CAGR.

Why is the Mobiuz privatisation significant?

The sale is expected to inject foreign capital and expertise, intensifying competition and accelerating network modernisation.

What challenges limit profitability?

Price wars keep blended ARPU under USD 3 and high reserve prices for 700 MHz and 3.5 GHz spectrum bands elevate operator debt loads.

Which customer segment offers higher-margin upside?

Enterprise clients, growing at a 6.63% CAGR, demand value-added IoT and cloud services with longer-term contracts.

Page last updated on: