Afghanistan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

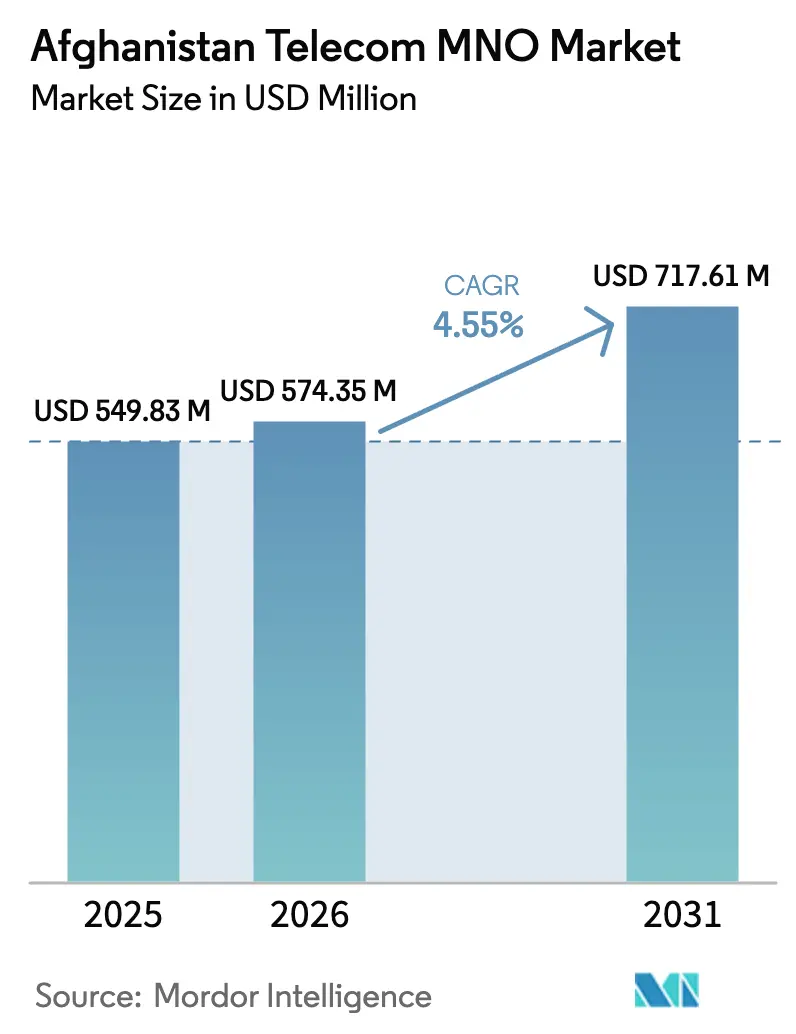

| Base Year Market Size (2025) | USD 549.83 Million |

| Market Size (2026) | USD 574.35 Million |

| Market Size (2031) | USD 717.61 Million |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

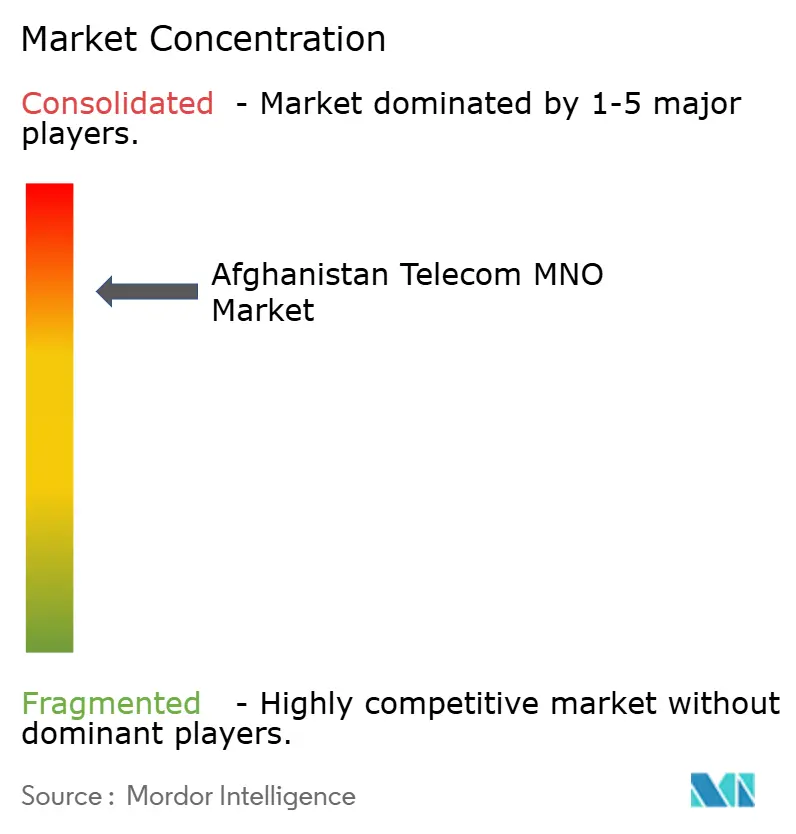

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Afghanistan Telecom MNO Market Analysis by Mordor Intelligence

Afghanistan Telecom MNO Market size in 2026 is estimated at USD 574.35 million, growing from 2025 value of USD 549.83 million with 2031 projections showing USD 717.61 million, growing at 4.55% CAGR over 2026-2031.

Rising demand for mobile broadband, sustained population growth, and the absence of viable fixed-line substitutes keep overall usage levels high even as the operating environment remains complex. Rollouts of 4G-ready spectrum in the 1800 MHz band, cross-border fiber routes that lower international bandwidth costs, and policy support for universal access collectively underpin the next phase of network expansion. [1]TOLO News, “Govt-Owned Telecom Company Wins Spectrum Assignment Auction,” toloNews.com Operators continue to prioritize investment in urban nodes where average revenue per user (ARPU) is higher, but regulatory subsidies are pushing coverage deeper into underserved provinces. [2]Ariana News, “450 New Telecom Sites to Be Built in the Country,” ariananews.af Mounting demand for data-centric applications, coupled with affordable Chinese smartphones and bundled financing plans, is reshaping usage patterns away from legacy voice and SMS toward high-bandwidth services. The Afghanistan telecom MNO market, therefore, enters the forecast window positioned for steady, supply-constrained growth rather than demand-side saturation.

Key Report Takeaways

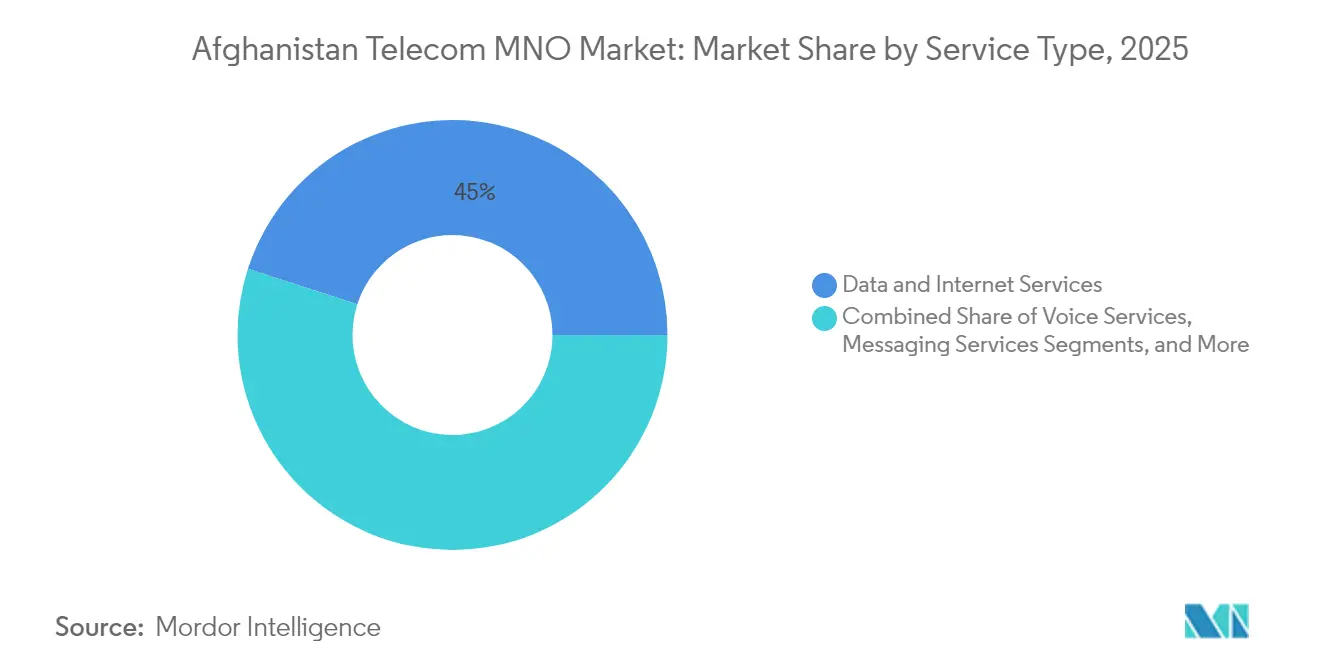

- By service type, Data and Internet services led with 45.02% of Afghanistan telecom MNO market share in 2025, while IoT and M2M services are projected to expand at a 4.58% CAGR to 2031.

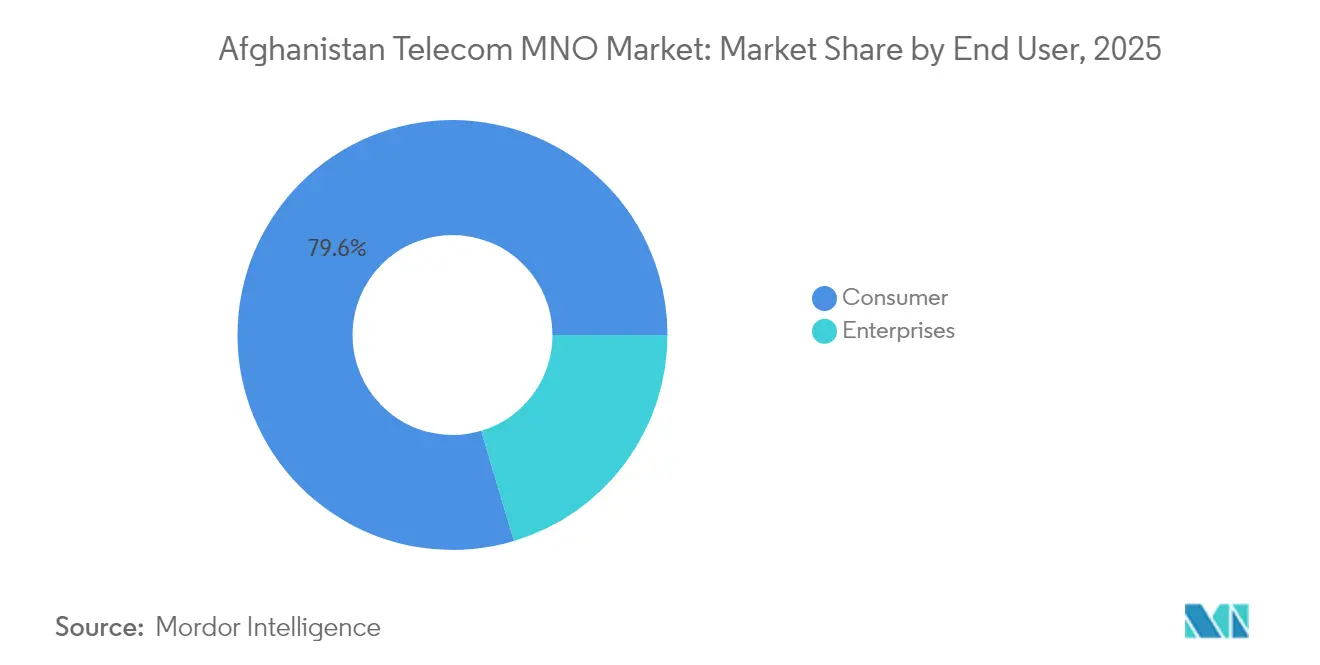

- By end user, the Consumer segment accounted for 79.62% of the Afghanistan telecom MNO market size in 2025, whereas the Enterprise segment records the fastest growth at 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Afghanistan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 4G/5G-ready spectrum releases accelerate mobile broadband uptake | +1.2% | National, with early gains in Kabul, Herat, Kandahar | Medium term (2-4 years) |

| Smartphone affordability and Chinese OEM bundling drives data usage | +0.8% | Urban centers expanding to semi-urban areas | Short term (≤ 2 years) |

| Government Universal Access Fund subsidies for rural sites | +0.6% | Rural provinces, particularly in northern and eastern regions | Long term (≥ 4 years) |

| Enterprise digitization and cloud adoption boost dedicated connectivity | +0.5% | Major cities with commercial activity concentration | Medium term (2-4 years) |

| Cross-border fiber links to Pakistan and CARs slash international transit costs | +0.4% | Border provinces with spill-over to national backbone | Long term (≥ 4 years) |

| LEO satellite backhaul trials open remote coverage white-spots | +0.3% | Remote mountainous regions and conflict-affected areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

4G/5G-ready spectrum releases accelerate mobile broadband uptake

Afghan Telecom’s USD 17.2 million purchase of 2×5 MHz in the 1800 MHz band set a benchmark for future auctions that will unlock additional 2100 MHz and 2600 MHz blocks required for LTE-Advanced services. [3]TOLO News, “Afghanistan, China To Connect Through Fiber Optic Network,” toloNews.com Extra capacity allows operators to migrate heavier traffic to spectrum better suited for broadband, improving speeds and reducing congestion in Kabul, Herat, and Kandahar. Higher network quality feeds directly into data monetization because 80.9% of connections are already classified as broadband capable. Competitive pressure also intensifies; Etisalat Afghanistan, backed by its parent e&, now holds 15 MHz across the two prime bands, compelling rivals to match quality and coverage. Collectively, spectrum releases increase service differentiation potential, lift ARPU ceilings in urban centers, and de-risk capital outlays for rural rollouts by boosting per-site capacity.

Smartphone affordability and Chinese OEM bundling drives data usage

Aggressive pricing by Vivo, Xiaomi, Huawei, and Oppo has pushed average retail prices of 4G-capable models down to AFN 39,130 (USD 450) and below. Operators overlay the hardware push with financing plans and prepaid data packs that encourage immediate broadband adoption once devices are activated. The result is a 6.3% year-on-year jump in mobile internet users to 13.2 million in 2025, significantly widening the addressable pool for value-added digital services. The shift also accelerates migration away from USSD-based transactions toward app-based mobile money platforms, enlarging revenue opportunities in financial services. As penetration rises beyond Kabul into semi-urban districts, data and Internet services consolidate their lead within the Afghanistan telecom MNO market, strengthening the revenue mix against voice-heavy competition.

Government Universal Access Fund subsidies for rural sites

ATRA’s subsidy program has earmarked 450 new base-station rollouts with priority in districts lacking any signal, reducing the payback period on towers that would otherwise never break even. Capital support offsets security-driven construction premiums, especially in mountainous northern provinces where transport and protection costs exceed regional averages. Early rounds have already extended fibre to 16 districts that previously had no telephony at all, widening the potential customer base for every operator that co-locates on subsidized masts. Rural connectivity stimulates ancillary economic benefits such as agricultural price discovery and remote education, indirectly reinforcing subscription affordability. Over the long term, subsidy-driven site density narrows the urban-rural performance gap, positioning nationwide 4G coverage as a realistic objective rather than an aspirational policy statement.

Enterprise digitization and cloud adoption boost dedicated connectivity

Enterprise traffic rises in tandem with Afghanistan’s growing role as a corridor linking Central and South Asia, increasing the need for dependable connectivity across logistics, finance, and business-process outsourcing. Etisalat Afghanistan’s carrier-wholesale division now packages private APNs, content-delivery nodes, and flexible billing to corporate buyers who demand guaranteed uptime. [4]Etisalat Afghanistan, “Carrier & Wholesale,” etisalat.af These premium offerings tap a customer segment that tolerates higher ARPU in exchange for symmetrical bandwidth and service level agreements. As local firms migrate back-office workloads to cloud infrastructure, the need for stable, high-capacity links pushes take-up of leased lines and dedicated LTE. The enterprise share of the Afghanistan telecom MNO market, therefore, expands consistently and creates counter-cyclical revenue streams that are less exposed to consumer price competition, underpinning the 5.11% CAGR forecast for the segment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent security risks inflate network OPEX and CAPEX | -1.8% | Nationwide, with severe impact in southern and eastern provinces | Short term (≤ 2 years) |

| Ultra-low ARPU limits ROI for new technology roll-outs | -1.1% | Rural and low-income urban areas | Medium term (2-4 years) |

| Gender-based usage restrictions shrink addressable base | -0.7% | Conservative rural areas and Taliban-controlled regions | Long term (≥ 4 years) |

| Sanctions-linked equipment import delays and cost over-runs | -0.9% | National infrastructure projects and network expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent security risks inflate network OPEX and CAPEX

ATRA recorded 28 towers destroyed in one quarter of 2024, following 301 tower losses valued at USD 1 million the previous year. Each incident forces operators to budget for duplicate hardware, armed guards, and rapid-response repair teams, pushing site operating costs far above regional benchmarks. Capital deepening consequently slows because funds are diverted to replacement instead of green-field expansion. Protracted outages also erode consumer trust, heightening churn and pressuring margins. While security conditions fluctuate by province, the net effect is a structural cost-overhang that drags on the Afghanistan telecom MNO market CAGR.

Ultra-low ARPU limits ROI for new technology roll-outs

Five national operators compete in a price-sensitive environment where disposable income is among the lowest in Asia. Tariff wars hold ARPU below levels needed to justify widespread 5G adoption, especially in sparsely populated districts. Limited revenue headroom curtails the ability to subsidize handsets or deploy small-cell densification, slowing the migration from legacy 3G layers. The pattern is self-reinforcing: lower network quality suppresses willingness to pay, further constraining reinvestment capacity. Until purchasing power rises materially or service bundling uncovers new value pools, ARPU weakness will continue to moderate the Afghanistan telecom MNO market size expansion trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: data-centric usage reshapes revenue mix

Data and Internet services delivered 45.02% of Afghanistan telecom MNO market share in 2025, reflecting the nation’s accelerated pivot toward mobile broadband. Consumers gravitate to social media, video streaming, and mobile wallets that require robust packet-switched connections, driving steady traffic growth and underpinning network upgrade rationales. Voice minutes remain essential in rural regions but are plateauing in value terms as over-the-top (OTT) applications siphon off traditional usage. Messaging revenue also contracts as users prefer app-based solutions with richer features. In enterprise contexts, IoT deployments for agriculture monitoring, fleet tracking, and energy metering emerge as the fastest-growing service subset at a 4.58% CAGR, albeit from a small base. The Afghanistan telecom MNO market size for IoT connectivity remains modest but signals future diversification potential once device ecosystems mature and provincial data regulations stabilize.

The incoming pipeline of OTT and PayTV platforms positions premium video as a niche but rising revenue line, constrained principally by content localization deficits and last-mile bandwidth variability. Operators, therefore, experiment with partner-bundled streaming passes that minimize data charges during off-peak windows to manage congestion. Other services, including international roaming and enterprise-grade security overlays, benefit from Afghanistan’s new cross-border fiber corridors that slash transit latency and cost. Collectively, the evolving service mix moderates revenue volatility by balancing high-volume consumer data with low-volume, higher-margin enterprise connectivity, reinforcing the sustainability of the Afghanistan telecom MNO market.

By End User: shifting enterprise demand underpins premium tiers

The Consumer segment represented 79.62% of Afghanistan telecom MNO market size in 2025, anchored by essential voice and rapidly growing data requirements among 22.3 million SIM connections. Household adoption rises fastest in Kabul, Herat, and Mazar-e-Sharif, where smartphone affordability has significantly improved. Yet, revenue elasticity remains constrained because prepaid plans dominate, and price points must align with limited income levels. As a result, operators seek margin relief in the Enterprise segment, which is expanding at 5.03% CAGR through 2031 as Afghan firms digitize supply chains and customer engagement channels.

Within enterprises, verticals such as logistics and retail embrace dedicated connectivity, prioritizing low latency for inventory management and contactless payment acceptance. Cross-border trade organizations depend on reliable links to neighboring markets, leveraging Afghanistan’s enhanced transit-hub status to negotiate regional data routes. Managed services bundles that integrate cloud access, cybersecurity, and unified communications lift average spend well above consumer levels. Consequently, the Afghanistan telecom MNO market share of enterprise services inches upward year after year, mitigating ARPU compression elsewhere and encouraging carriers to continue CAPEX in fiber backhaul and metro ethernet overlays.

Geography Analysis

Urban districts, led by Kabul, Herat, and Kandahar, enjoy near-universal 3G and rapidly expanding 4G coverage that delivers data speeds competitive within South Asia. These hubs account for a disproportionate share of the Afghanistan telecom MNO market because they host dense populations, higher per-capita incomes, and a concentration of enterprise customers. Operators therefore deploy carrier-grade redundancy and spectrum refarming in these cities first before extending upgrades to tier-two towns. In contrast, rural districts, especially in the southern and eastern belts, still depend on ageing 2G/3G layers or lack service altogether, reinforcing a digital divide that suppresses national average ARPU.

Cross-border fibre integrations materially shift Afghanistan’s geographic relevance. The USD 50 million Wakhan corridor link to China and the 700 km TAPI route toward Turkmenistan, Uzbekistan, and Pakistan lower transit costs for international bandwidth by up to 60%, creating fresh wholesale revenue channels that accrue directly to national carriers. Estimates suggest transit fees could top USD 60 million annually, a figure meaningful relative to current domestic subscription revenue. Provinces traversed by these cables, notably Badakhshan and Kandahar, gain ancillary benefits through improved last-mile capacity, boosting service quality for local users and stimulating small-business adoption of e-commerce.

However, security-related outages skew provincial performance metrics. Ghazni illustrates the challenge, with adequate mobile service recorded in only 2 of 18 districts despite several subsidy-driven towers coming online. Operators weigh CAPEX against elevated risk premiums, limiting expansion in conflict-heavy zones unless direct government support offsets the threat. This variable risk calculus generates a patchwork of connectivity levels that map less to population density than to security intensity. The resulting geography-led segmentation places a ceiling on near-term market penetration rates and keeps the Afghanistan telecom MNO market reliant on universal-access funds and public-private partnerships to close the gap.

Competitive Landscape

Five nationwide operators, Afghan Wireless Communication Company (AWCC), Roshan, Etisalat Afghanistan, Afghan Telecom, and ATOMA, compete across broadly overlapping footprints, though each pursues distinct positioning levers. AWCC leverages USD 750 million in accumulated infrastructure spend to offer the widest rural reach, while Roshan differentiates through social-impact branding after securing B-Corp certification. Etisalat Afghanistan, buoyed by e&’s 15 MHz spectrum purchase, targets metropolitan users with higher-throughput 4G and enterprise-centric solutions. Afghan Telecom retains state backing and a universal-service mandate that facilitates access to subsidy pools, allowing it to push coverage into remote districts at lower effective cost.

Market structure tightened when MTN divested its 40% share and transferred assets to ATOMA in April 2025. The reconstituted operator inherits a sizable spectrum but must rebrand and restore customer confidence under a new management regime. Consolidation reduced the field yet maintained five players, fostering a balance of competition sufficient to curb price hikes while retaining scale economies needed for network modernization. Strategic focus converges on three themes: accelerating 4G rollout, monetizing cross-border wholesale routes, and scaling mobile financial services into a quasi-banking platform for the unbanked.

Operational resilience remains central to competitive advantage. Carriers that harden sites with renewable energy backups and remote tower monitoring technologies reduce downtime and enhance quality-of-service metrics that consumers increasingly track via crowdsourced speed-test apps. The Afghanistan telecom MNO market, therefore, rewards operators capable of blending cost discipline with differentiated service layers, ensuring that leadership hinges on execution speed rather than on sheer capital outlay alone.

Afghanistan Telecom MNO Industry Leaders

Afghan Wireless Communication Company (AWCC)

Roshan (TDCA)

Etisalat Afghanistan

Salaam Telecom (Afghan Telecom)

ATOMA (MTN Afghanistan)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: MTN formally exited Afghanistan and transferred its network to ATOMA, signaling the end of an 18-year presence and inaugurating a new competitive era under local stewardship.

- February 2024: Afghanistan cleared USD 627 million in electricity arrears to neighboring suppliers, improving grid stability essential for continuous telecom operations.

Afghanistan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Afghanistan telecom MNO market?

The market is valued at USD 574.35 million in 2026.

How fast is the market expected to grow?

It is forecast to expand at a 4.55% CAGR between 2026 and 2031.

Which service type currently leads revenue share?

Data and Internet services lead with 45.02% share.

Which end-user segment is expanding the fastest?

The Enterprise segment is growing at 5.03% CAGR.

What factor most constrains network expansion costs?

Persistent security risks that drive up CAPEX and OPEX.

Which recent cross-border project cuts international transit costs?

The fiber-optic link through the Wakhan corridor to China.

Page last updated on: