Tajikistan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

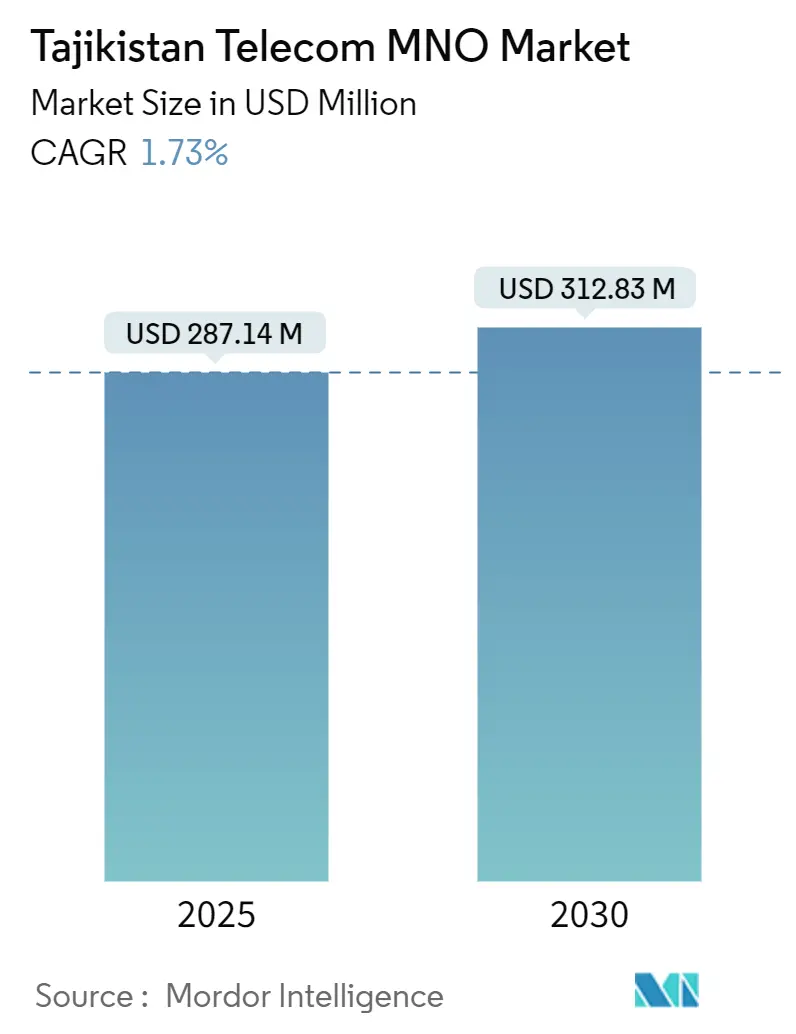

| Market Size (2025) | USD 287.14 Million |

| Market Size (2030) | USD 312.83 Million |

| Growth Rate (2025 - 2030) | 1.73% CAGR |

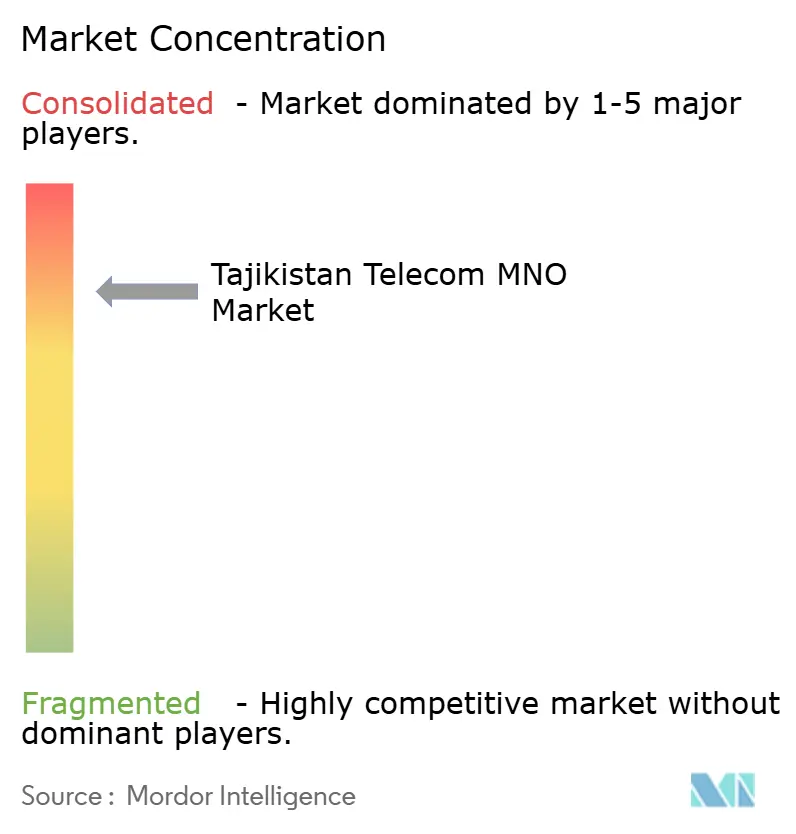

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tajikistan Telecom MNO Market Analysis by Mordor Intelligence

The Tajikistan Telecom MNO Market size is estimated at USD 287.14 million in 2025, and is expected to reach USD 312.83 million by 2030, at a CAGR of 1.73% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 10.80 million Subscribers in 2025 to 12 million Subscribers by 2030, at a CAGR of 2.26% during the forecast period (2025-2030). Rising smartphone ownership among the country’s 9.7 million inhabitants, remittance-supported consumer spending, and selective 5G roll-outs in Dushanbe, Khujand, and Kulob drive incremental revenue, yet the persistence of 2G coverage across 95% of the landmass tempers growth. Elevated data prices, mandatory surveillance spending, and the single-gateway regime further restrain profitability despite expanding urban demand for mobile financial services. Competitive intensity remains moderate, with four network operators sharing a 42% penetration rate amid gradual policy moves that now allow MegaFon and Tcell to bypass the state-controlled gateway for international bandwidth.[1]Eurasianet, “Tajikistan’s Patchwork Leap to 5G,” eurasianet.org Chinese-financed fibre backbones and base stations continue to underpin capacity upgrades, but reliance on one supplier raises long-term technology-sovereignty questions.

Key Report Takeaways

- By service type, data and internet services held 45.67% of the Tajikistan telecom MNO market share in 2024; OTT and PayTV services are poised to expand at a 1.74% CAGR through 2030.

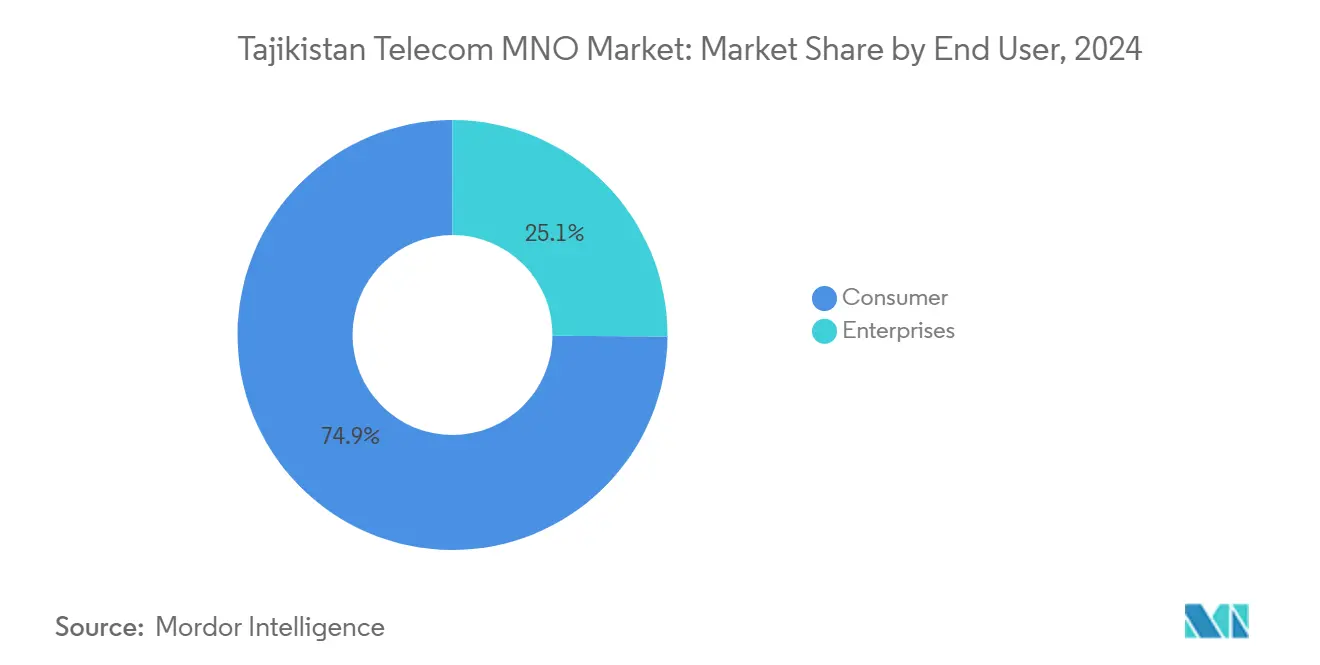

- By end user, consumer services accounted for 74.89% share of the Tajikistan telecom MNO market size in 2024, while enterprise services are projected to grow at a 2.12% CAGR over 2025-2030.

Tajikistan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government 4G/5G spectrum roadmap and license renewals | +0.4% | National, early gains in Dushanbe, Khujand, Kulob | Medium term (2-4 years) |

| Rapid smartphone uptake among under-30 population | +0.3% | National, urban centres | Short term (≤ 2 years) |

| Remittance-fuelled rise in data-centric ARPU | +0.2% | National, strongest in Sughd and Khatlon | Medium term (2-4 years) |

| Chinese-financed national fibre backbone rollout | +0.3% | National infrastructure backbone | Long term (≥ 4 years) |

| Cross-border Afghan transit traffic boosting leased-line sales | +0.1% | Border regions, Badakhshan | Medium term (2-4 years) |

| CASA-1000 towers repurposed as rural mobile backhaul | +0.1% | Rural transmission corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government 4G/5G Spectrum Roadmap and Licence Renewals

Structured spectrum auctions since 2019 have enabled Tcell to stage 5G trials that exceeded 1 Gbps download speeds in Dushanbe.[2]Developing Telecoms, “Tcell Conducts 5G Trials in Dushanbe,” developingtelecoms.com The roadmap obliges licensees to achieve minimum rural coverage, nudging operators to extend beyond profit-rich urban footprints. Huawei’s 7,600-site build-out provides the physical layer for compliance, though elevated capital outlays tied to mandatory interception gear burden balance sheets. Predictable licence terms nonetheless sharpen investment planning and encourage long-term vendor financing. The policy ultimately narrows the urban–rural digital divide without diluting the Tajikistan telecom MNO market’s competitive neutrality.

Rapid Smartphone Uptake Among Under-30 Population

A youthful demographic base propels device adoption; an IMEI registration scheme logged 757,000 imported handsets between October 2023 and June 2024, generating USD 2.4 million in fees.[3]Asia-Plus, “Device Registration Fees Collected by Net Solutions,” asiaplustj.info Source: International Monetary Fund, “Article IV Consultation 2024,” imf.orgRemittance inflows from Russia and Kazakhstan furnish disposable income that offsets high data tariffs. The resulting demand for video streaming, social media and mobile wallets reallocates revenue from voice to bandwidth, compelling operators to speed up 4G capacity upgrades. Enterprises mirror consumer behaviour, using mobile apps to reach young customers and employees. This demographic momentum keeps the Tajikistan telecom MNO market firmly on a data-centric growth path.

Remittance-Fuelled Rise in Data-Centric ARPU

GDP expanded 8.3% in 2023 on the back of stronger remittances, and digital wallets reached 10.4 million users by mid-2024, up 16.2% year on year. Migrants boost average revenue per user by purchasing larger data bundles and paying for cross-border transfers embedded in operator apps. Seasonal volatility persists, but flexible add-on plans help smooth revenue swings. Operators also monetise diaspora connections through roaming packages and tiered international call minutes. While remittance-backed consumption supports the Tajikistan telecom MNO market, dependence on external labour markets exposes earnings to geopolitical risk.

Chinese-Financed National Fibre Backbone Rollout

Long-haul fibre routes supplied under vendor-financing agreements with Huawei reduce backhaul bottlenecks and create enterprise-grade service opportunities. By linking power substations, schools and clinics, the backbone aligns with government e-services targets while giving operators scalable capacity. Yet single-vendor reliance concentrates supply-chain risk and raises data-sovereignty concerns. Successful rural spurs will decide how far the Tajikistan telecom MNO market can stretch beyond city limits. Over the long run, diversified funding and multivendor procurement could ease strategic vulnerabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-gateway policy inflating bandwidth prices | -0.3% | National | Short term (≤ 2 years) |

| Low disposable income suppressing premium-data uptake | -0.2% | National, severe in rural areas | Medium term (2-4 years) |

| Chronic power-grid outages curbing rural tower uptime | -0.1% | Remote valleys | Long term (≥ 4 years) |

| Mandatory surveillance gear raising operator capex | -0.1% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Single-Gateway Policy Inflating International Bandwidth Prices

Recent rules allow MegaFon and Tcell to procure bandwidth outside the Unified Electronic Communications Switching Center, but wholesale rates remain high during the transition. Uncertain pricing and interconnection terms deter aggressive retail discounting, keeping average data at USD 1.65 per GB versus USD 0.60 in Uzbekistan. Enterprises requiring cloud connectivity face latency and cost challenges that can delay digitalisation. Clarity on service-level standards and cost-sharing will determine how quickly the Tajikistan telecom MNO market reaps the benefits of competition in the international segment.

Low Disposable Income Suppressing Premium-Data Uptake

Informal employment covers 57% of workers, especially in agriculture, creating volatile cash flows that constrain spending on large data bundles. Operators tailor micro-packs and daily validity plans, but these arrest ARPU expansion. Rural households often resort to shared devices, which limits per-SIM consumption. Government efforts to formalise jobs and raise wages could enlarge the addressable base for higher-tier packages. Until then, affordable entry-level tariffs remain essential for sustaining subscriber growth in the Tajikistan telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Anchor Revenue Momentum

Data and internet services captured 45.67% of the Tajikistan telecom MNO market size in 2024, underscoring the pivot away from legacy voice. Urban youths stream music, video and gaming content, while SMEs adopt cloud-based accounting and messaging tools. Voice revenues slide as over-the-top apps cannibalise traditional minutes, and message volumes stagnate amid social media dominance. IoT uptake in logistics corridors and hydropower monitoring begins, though coverage gaps curb scale. OTT and PayTV products lead growth at a 1.74% CAGR to 2030 as falling handset prices broaden smartphone ownership. Operators bundle video subscriptions with mid-range data plans to lift stickiness and reduce churn within the Tajikistan telecom MNO market.

A modest but rising enterprise appetite for M2M services prompts pilot projects in smart metering and agro-monitoring, leveraging CASA-1000 tower backhaul. International roaming and inbound transit traffic add incremental revenue through Afghanistan links along the Wakhan corridor. While constrained by income levels, product diversification positions operators to defend margins as regulatory fees climb.

By End User: Enterprise Adoption Gains Traction

Consumer lines dominated 74.89% of the Tajikistan telecom MNO market size in 2024 thanks to remittance-backed smartphone purchases and a digitally native under-30 cohort. Operators use gamified loyalty apps to sustain engagement, and mobile wallets process rising remittance inflows, converting financial transactions into fee income. Rural uptake remains hamstrung by intermittent power and higher data costs, prompting seasonal churn cycles. Flexible validity extensions seek to maintain rural SIM activity.

Enterprise connections, though only 25.11% of active SIMs, are set to grow at a 2.12% CAGR through 2030 as cross-border traders, banks and public agencies require secure virtual-private networks and cloud access. The World Bank-funded Digital CASA initiative subsidises backhaul to government offices, stimulating demand for managed services. Operators bundle leased lines, cybersecurity and mobile device management to capture higher-margin contracts and diversify cash flows in the Tajikistan telecom MNO industry.

Geography Analysis

Urban clusters drive revenue concentration. Dushanbe alone accounts for more than one-third of total data traffic, buoyed by university campuses and rising fintech uptake. Khujand and Kulob follow as 5G testbeds where early adopters trial cloud gaming and ultra-HD streaming. These cities benefit from denser tower grids and fibre rings financed under vendor-credit schemes, enabling operators to market premium 20 GB monthly bundles.

Rural Khatlon and Sughd provinces present latent demand but suffer from chronic power outages that keep tower uptime below 85%. Operators deploy solar-hybrid energy and repurpose CASA-1000 pylons for microwave backhaul to trim costs. Nevertheless, low disposable income limits average monthly spend, locking many users into sub-USD 2 starter packs. Expanding fibre spurs and off-grid power solutions will be critical to unleash rural growth in the Tajikistan telecom MNO market.

Border regions, particularly Gorno-Badakhshan, offer strategic transit revenue from Afghanistan. A July 2024 fibre optic link aligned with the TAPI pipeline enhances redundancy, attracting data transit from Central to South Asia. Geopolitical volatility remains a risk, yet the corridor positions Tajikistan as a land-bridge, diversifying operator income beyond saturated domestic segments.

Competitive Landscape

Four mobile network operators jostle for share in a moderately concentrated arena. Tcell leads with 3.301 million subscribers on the strength of early 5G trials and a nationwide 4G footprint. ZET Mobile and Babilon-Mobile chase value-conscious segments, leveraging aggressive top-up bonuses and local language apps. MegaFon’s Russian shareholder ties deliver roaming alliances that appeal to migrant workers.

State-owned Tojiktelecom retains wholesale dominance in fixed backhaul and controls inter-city ducts, shaping lease pricing and competitive neutrality. Foreign vendors remain central: Huawei supplies most RAN equipment, while recent memoranda with Russian firm Tsifra aim to diversify supply, possibly lowering costs and mitigating sanctions exposure. Operators also partner with fintech firms to embed payments, with Net Solutions managing the IMEI registry that generates device verification fees. Disruptive entrants face high capex, a spectrum shortfall and compliance hurdles, but could exploit rural coverage obligations through infrastructure-sharing models to carve niches in the Tajikistan telecom MNO market.

Operators pursue three notable strategic moves. First, Tcell secured 3500 MHz spectrum and committed to rural coverage percentages that unlock tax incentives. Second, ZET Mobile pilots an e-SIM onboarding journey to cut distribution costs. Third, MegaFon introduced cross-border data bundles targeting Tajik migrants in Russia, lifting its roaming revenue by double digits in 2024. Such targeted strategies illustrate how incumbents navigate margin pressure while expanding service depth.

Tajikistan Telecom MNO Industry Leaders

Tcell

Babilone-Mobile

MegaFon Tajikistan

ZET-Mobile

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: The Communications Service under the Government of Tajikistan signed a memorandum of cooperation with Russian company “Tsifra” to enhance telecommunications infrastructure and digital service capabilities, extending supplier diversification.

- April 2024: MTS subsidiary Irteya announced plans to start production of 4G and 5G base stations, potentially lowering equipment costs for Central Asian operators.

- April 2024: Afghanistan’s Ministry of Communications unveiled a fibre optic project alongside TAPI, opening future transit possibilities for Tajik operators.

- April 2024: The government formalised cooperation frameworks with multiple international technology companies to broaden infrastructure options.

Tajikistan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the value of the Tajikistan telecom MNO market in 2025?

The market is valued at USD 287.14 million in 2025.

How fast is the market expected to grow by 2030?

It is projected to expand to USD 312.83 million, translating to a 1.73% CAGR through 2030.

Which service type currently generates the most revenue?

Data and internet services lead with a 45.67% share of total revenue in 2024.

Which segment shows the fastest growth potential?

OTT and PayTV offerings are forecast to rise at a 1.74% CAGR over 2025-2030.

How significant is the enterprise opportunity?

Enterprise services are expected to grow at a 2.12% CAGR, supported by government digitisation and cross-border trade.

Why do data prices remain high in Tajikistan?

A legacy single-gateway regime keeps international bandwidth costs elevated, which inflates retail data tariffs.

Page last updated on: