Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.43 Billion |

| Market Size (2026) | USD 4.57 Billion |

| Market Size (2031) | USD 5.36 Billion |

| Growth Rate (2026 - 2031) | 3.22% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iran Telecom MNO Market Analysis by Mordor Intelligence

Iran Telecom MNO Market size in 2026 is estimated at USD 4.57 billion, growing from 2025 value of USD 4.43 billion with 2031 projections showing USD 5.36 billion, growing at 3.22% CAGR over 2026-2031.

The measured growth path shows how operators are sustaining revenues despite sanctions that limit equipment imports and foreign partnerships. Domestic infrastructure programs, particularly the National Information Network, now route most traffic inside the country and lower transit costs.[1] “In-house adaptation sustains growth,” tejaratnews.com Government fiber-to-the-home subsidies aimed at 20 million premises stimulate broadband demand even as rial volatility inflates capital expenses. Mobile internet penetration surpassed 109% in 2024, so growth hinges on higher-value data, IoT, and enterprise services rather than new subscriber additions. Operators also gain revenue momentum from domestic video streaming, cloud hosting, and super-app partnerships that deepen customer engagement.

Key Report Takeaways

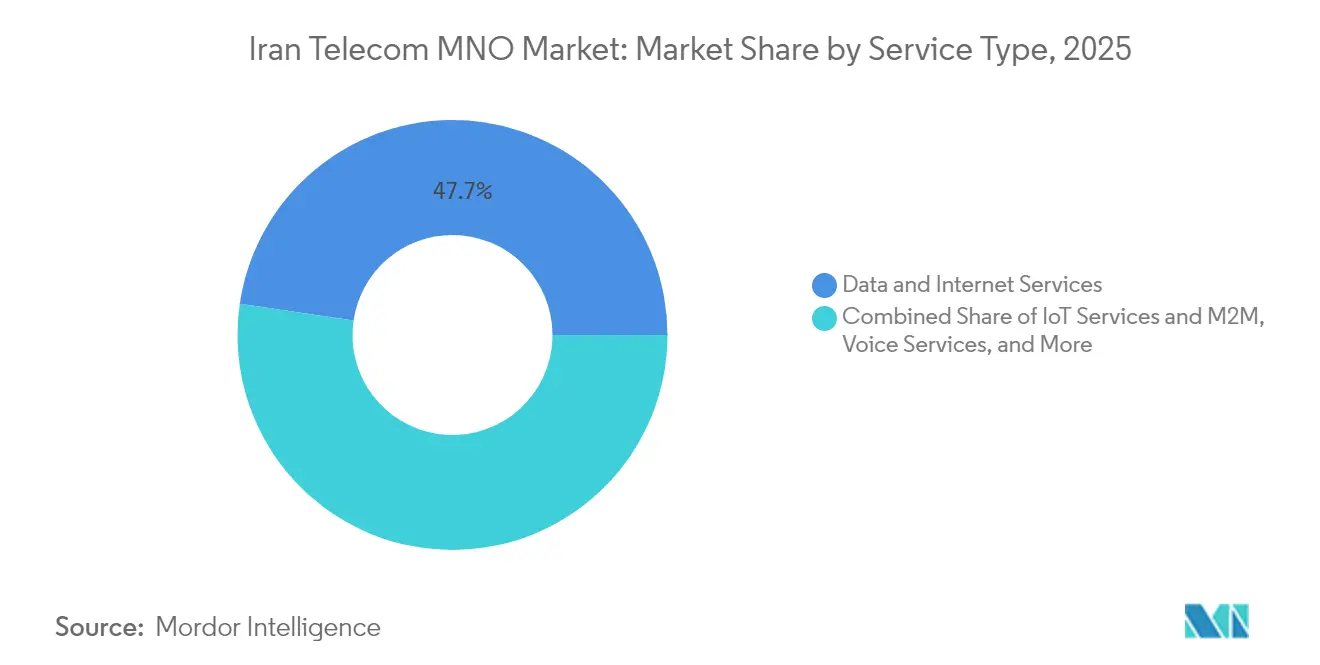

- By service type, data and internet services led with 47.68% of the Iran Telecom MNO market share in 2025; IoT and M2M services are projected to expand at a 3.35% CAGR through 2031.

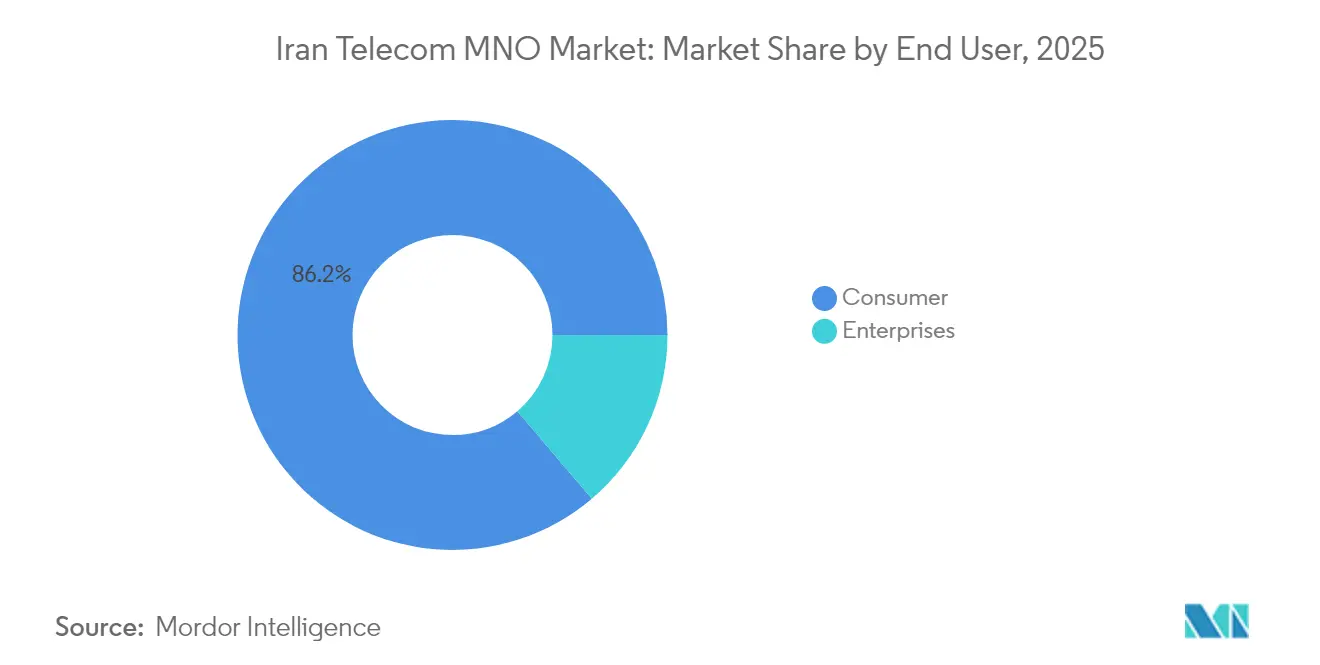

- By end user, the consumer segment accounted for 86.22% share of the Iran Telecom MNO market size in 2025, while enterprise services are advancing at a 3.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iran Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G spectrum acceleration | +0.8% | National with early gains in Tehran, Isfahan, Mashhad | Medium term (2-4 years) |

| Gov-backed FTTH subsidy scheme | +0.6% | National, prioritizing rural and underserved areas | Long term (≥ 4 years) |

| Domestic video-streaming boom | +0.4% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Sanction-driven domestic cloud buildout | +0.5% | National, enterprise-focused in major cities | Medium term (2-4 years) |

| IoT uptake in oil and gas monitoring | +0.3% | Khuzestan and offshore fields | Long term (≥ 4 years) |

| FinTech super-app partnerships | +0.2% | National, urban uptake | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G spectrum acceleration

The communications ministry awarded the 3,600 MHz and 3,700 MHz bands in early 2025, clearing a regulatory hurdle that had slowed migration to 5G technology. [2]Iran Daily Editors, “5G Frequency Auction Results,” iran daily.ir Chinese vendors now supply most radio access equipment because U.S. sanctions block European suppliers; their integrated hardware–software stacks shorten roll-out timelines and cut procurement costs, enabling operators to light up 5G in Tehran, Isfahan, and Mashhad before March 2025. First-phase coverage targets 20 million users, with enterprise use cases in oil, gas, and manufacturing validating premium tariffs. Early adopters benefit from lower latency for industrial monitoring and high-resolution video, while operators gain a differentiated value proposition that eases price competition in saturated 4G segments. Success of the pilot zones will guide the nationwide expansion plan now scheduled for completion by 2027.

Gov-backed FTTH subsidy scheme

The USD 2.1 billion (≈ 50 trillion rial) subsidy program reduces household installation fees from 3.5 million tomans (≈ USD 70) to levels affordable for middle-income subscribers. [3]Business Desk, “Rural Fiber Subsidy Details,” donya-e-eqtesad.comMore than 98% of villages with at least 20 households already have high-speed access, positioning Iran ahead of several regional peers in rural broadband penetration. Subsidized fiber stimulates take-up of premium data bundles, online gaming, and over-the-top TV services that lift average revenue per user. Operators also monetize wholesale dark-fiber leases to cloud providers building domestic data centers. The program dovetails with the National Information Network’s goal of routing sensitive traffic locally, thereby conserving scarce international bandwidth and lowering peering costs for carriers.

Domestic video-streaming boom

Restrictions on global platforms such as Netflix channel demand toward local services like Filimo and Namava, whose combined paying user base climbed above 14 million in 2024. Irancell now bundles unlimited access to domestic video catalogs with high-speed data tiers, adding content-driven stickiness that reduces churn. Local hosting means traffic remains inside Iran, trimming international transit fees and easing pressure on congested gateways. Advertisers follow audiences to domestic platforms, providing operators with incremental revenue through targeted video ad insertion. The content partnership model will expand as rights holders see higher monetization potential within a sovereign digital ecosystem.

Sanction-driven domestic cloud buildout

Enterprises migrating from AWS, Azure, and Google Cloud to domestic providers such as Abr Arvan increased domestic IaaS demand by 46% year-over-year in 2024. Telecom operators supply the secure fiber cross-connects, leased lines, and managed security layers that corporate customers require for data residency compliance. Because reliability is paramount, enterprises accept higher local pricing, giving operators a rare opportunity to expand margins even while the consumer business commoditizes. New data centers in Tehran, Qom, and Tabriz generate wholesale backhaul demand that absorbs excess network capacity. The cloud shift also anchors large-volume contracts, helping carriers hedge against price-sensitive prepaid mobile segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| US sanctions on network imports | -0.7% | National | Long term (≥ 4 years) |

| Rial volatility raising CAPEX costs | -0.5% | National | Medium term (2-4 years) |

| High energy costs and grid outages | -0.3% | Industrial regions | Short term (≤ 2 years) |

| OTT cannibalization of international voice | -0.2% | Urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

US sanctions on network imports

Broad U.S. export controls continue to bar Ericsson, Nokia, and Cisco from shipping critical gear to Iranian carriers. Operators rely on Chinese suppliers whose product roadmaps do not always match Western standards, reducing interoperability and complicating multi-vendor optimization. Spare-parts lead times stretch to several months, raising the risk of service degradation after equipment failures. Financial sanctions also freeze dividends owed to foreign shareholders; MTN Group has been unable to repatriate USD 1 billion since 2018, limiting its flexibility to reinvest. Together these factors lengthen payback periods on 5G and fiber builds, curbing the pace of network modernization.

Rial volatility raising CAPEX costs

The rial lost over 30% of its value against the U.S. dollar between 2023 and 2024, inflating prices of imported radios, servers, and optical modules. Budget uncertainty forces operators to renegotiate vendor contracts in shorter cycles and to hold larger inventories of spare parts. Smaller carriers with thin cash reserves postpone upgrades, risking quality gaps that accelerate subscriber migration to the two largest operators. Currency swings also deter foreign investors whose returns would be exposed to rapid depreciation; this restricts outside capital that could otherwise accelerate 5G scale-up. To mitigate risk, carriers hedge by sourcing more components domestically, although local manufacturing capacity remains limited to passive infrastructure and low-end devices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data services anchor growth while IoT accelerates

Data and internet services captured 47.68% of the Iran Telecom MNO market share in 2025, and the segment’s solid usage growth positions it as the central pillar of operator revenue streams. The Iran Telecom MNO market size tied to data plans is forecast to compound at 3.05% through 2031 as video streaming, mobile gaming, and remote work sustain bandwidth demand. Operators bundle zero-rated access to domestic content platforms, balancing higher per-gigabyte prices with perceived value. The shift toward bigger data packages offsets the slow erosion in voice and SMS revenues that continues under OTT pressure. Consumer appetite for rich media also drives investments in content delivery networks located inside Iran, improving latency for end users and slashing peering costs for carriers.

IoT and M2M revenue grows from a small base at a 3.35% CAGR, making it the fastest-expanding service category. Oil and gas operators deploy sensor networks across wellheads and pipelines in Khuzestan, transmitting telemetry via NB-IoT links that demand ultra-reliable connectivity. The launch of Hatef and Keyhan satellites in 2024 furnishes narrowband coverage to remote deserts and offshore platforms, allowing operators to package hybrid terrestrial-satellite solutions. Municipalities in Tehran, Mashhad, and Shiraz pilot smart-parking and traffic-light projects that could scale nationally once proof of value is demonstrated. Although IoT currently generates less than 5% of sector revenue, high gross margins and multi-year contracts give it outsize strategic importance for ARPU stability. Operators develop proprietary IoT management portals and cyber-security layers as differentiators, reinforcing their move from pure connectivity providers to managed-service partners.

By End User: Massive consumer base funds enterprise ambition

The consumer segment delivered 86.22% of 2025 revenue, reflecting Iran’s 109% mobile penetration and strong smartphone replacement cycle. Ongoing fiber subsidies raise the ceiling for fixed-mobile convergence bundles that include IPTV, cloud gaming, and smart-home security feeds. Tiered unlimited plans help operators monetize heavy video users while limiting network congestion through speed throttling above preset thresholds. Competitive differentiation now centers on value-added apps such as e-wallets, ride-hailing integrations, and exclusive drama series. Churn remains moderate because number portability adoption is low, although Rightel leverages digital-only onboarding and youth-oriented branding to lure urban prepaid users.

Enterprise services, while smaller in absolute terms, advance at a 3.95% CAGR to 2031, outpacing the consumer side and lifting blended ARPU for the Iran Telecom MNO industry. Banks, insurers, and payment processors require secure private APNs for their mobile workforces, a niche that commands double the per-SIM revenue of mass-market plans. Manufacturers in Isfahan deploy 5G private networks to automate quality control via machine-vision cameras, driving incremental spectrum-leasing income for carriers. The Iran Telecom MNO market size attached to enterprise verticals will climb steadily as sanctions keep public-cloud options limited and motivate firms to source end-to-end solutions locally. Operators tailor bundled offers that weave in fixed connectivity, managed security, cloud storage, and IoT dashboards, creating sticky multi-year contracts with predictable cash flows.

Geography Analysis

Regional disparities are narrowing as national infrastructure priorities push fiber and 4G/5G coverage deep into rural districts. Tehran remains the largest revenue pool, accounting for an estimated 30.65% of Iran Telecom MNO market revenue in 2025 on the back of higher ARPU and dense enterprise clusters. Early 5G deployments across Tehran’s business corridors catalyze demand for ultra-low-latency applications such as real-time stock trading and cloud CAD. Isfahan and Mashhad follow, sharing in the first wave of 5G roll-outs thanks to their sizable university populations and tourism activity.

Rural provinces witness a step-change in broadband quality as the FTTH subsidy program connects villages larger than 20 households. Universal service obligations compel operators to install base stations powered by renewable micro-grids in mountainous terrain where grid power is unreliable. For users in Kohgiluyeh-Boyer Ahmad and Sistan-Baluchestan, the leap from 2G voice to 4G data unlocks e-learning and telemedicine options previously inaccessible. This inclusivity aligns with the National Information Network, which now handles 99% of domestic traffic, lowering cross-border data exposure and reducing peering costs.

Border regions such as West Azerbaijan leverage improved mobile coverage to boost cross-border e-commerce with Turkey and Iraq. Coastal provinces along the Persian Gulf benefit from enhanced maritime connectivity for port logistics and offshore oil rigs, bolstering IoT use cases in asset tracking. The Iran Telecom MNO market size associated with these industrial corridors will increase as operators integrate 5G standalone cores that support network slicing, enabling dedicated logical networks for petrochemical complexes or free-trade zones. Overall, geographical expansion follows a mosaic of economic hubs, resource sites, and government inclusion mandates, ensuring balanced growth across divergent socio-economic landscapes.

Competitive Landscape

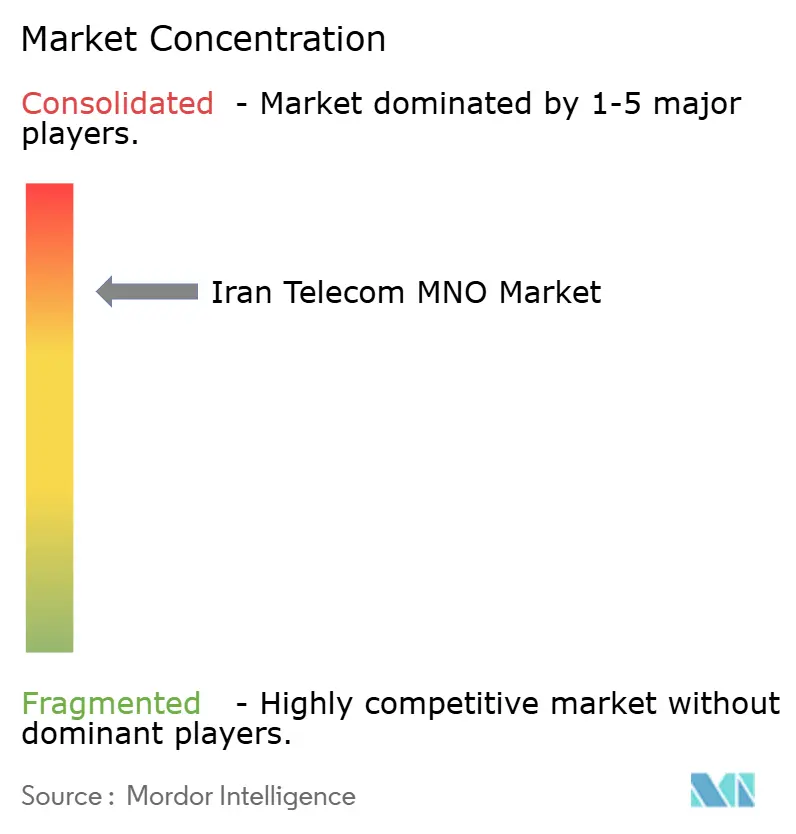

Market concentration is moderate, with three nationwide operators dividing the subscriber base. Hamrah-e Aval (MCI) commands leadership by virtue of its 75 million subscribers and deepest rural footprint, leveraging scale economies to negotiate favorable vendor pricing. MTN Irancell delivered 49% service-revenue growth in H1 2024 after repricing data bundles and upselling enterprise VPNs, signaling its intent to erode MCI’s dominance. Rightel positions itself as the digital challenger, bundling Filimo streaming access and unlimited social-media data to target youth and professionals seeking premium experiences.

Strategic moves skew toward alliances that leverage domestic technology ecosystems. Irancell signed a framework agreement with Abr Arvan to co-locate edge data centers, marrying connectivity with cloud compute for latency-sensitive applications. Hamrah-e Aval invests in AI-enabled customer-care chatbots that lower operating costs while improving resolution times, setting a customer-experience benchmark in a competitively tight marketplace. Rightel cooperates with fintech giant Digipay to embed micro-lending in its self-care app, expanding beyond connectivity into financial services.

Equipment sourcing gravitates toward Huawei and ZTE under long-term supply agreements that include training and local assembly. While Chinese solutions ease sanction risk, they constrain multi-vendor flexibility, prompting carriers to develop in-house integration expertise. Energy-efficient radios and liquid-cooling data centers help operators cap rising electricity costs during peak demand periods. Regulatory oversight remains firm but supportive of innovation: the ICT Ministry green-lighted a sandbox for 5G private networks that lets industrial customers test use cases before commercial launch. The evolving landscape rewards carriers that balance network quality, digital service breadth, and compliance with sovereign data mandates.

Iran Telecom MNO Industry Leaders

Mobile Communications of Iran (MCI)

MTN Irancell

Rightel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Iran’s ICT Minister outlined plans to attract USD 20–25 billion in foreign telecom investment under new bilateral agreements with Malaysia covering cybersecurity, AI, and space communications technologies.

- May 2025: The government launched six AI megaprojects aimed at balancing national energy supply and demand, with telecom infrastructure earmarked for smart-grid data backhaul.

- March 2025: Ride-hailing platform Snapp recorded 5.9 million daily trips, illustrating the scale advantages unlocked by pervasive mobile broadband; MTN Irancell retains a 43% stake via its holding company.

- January 2025: The revised Foreign Investment Promotion and Protection Act opened select ICT segments to 100% foreign ownership, a milestone for capital inflows.

Iran Telecom MNO Market Report Scope

Telecom or telecommunication is the long-range transmission of information by electromagnetic means.

Iran's Telecom MNO Market includes in-depth trend analysis based on connectivity like Fixed Networks, Mobile Networks, and Telecom Towers. The telecom services are divided into Voice Services (Wired and Wireless), Data and Messaging Services, OTT, and PayTV Services. Several factors, including an increasing demand for 5G, likely drive the adoption of telecom services.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-User

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-User | Enterprises |

| Consumer |

Key Questions Answered in the Report

How big is the Iran Telecom MNO market in 2026?

The sector generated USD 4.57 billion in 2026 and is on course to reach USD 5.36 billion by 2031.

What is driving revenue growth for Iranian mobile operators?

Higher-value data bundles, 5G roll-outs, domestic cloud hosting, and IoT demand in oil-and-gas and smart-city projects underpin revenue expansion.

Which service category is growing fastest?

IoT and M2M connections are expanding at a 3.35% CAGR through 2031 thanks to industrial monitoring and municipal smart-infrastructure projects.

How do sanctions affect telecom equipment sourcing?

U.S. sanctions block European vendors, so operators procure most 4G and 5G gear from Chinese suppliers, leading to longer lead times and limited vendor diversity.

Why is the enterprise segment attractive to carriers?

Enterprise contracts bundle connectivity with cloud, security, and IoT services, yielding higher ARPU and long-term cash-flow stability.

What role does the National Information Network play?

The network routes 99% of domestic traffic inside Iran, cutting international transit fees and reinforcing data-sovereignty compliance for operators.

Page last updated on: