Kazakhstan Telecom MNO Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

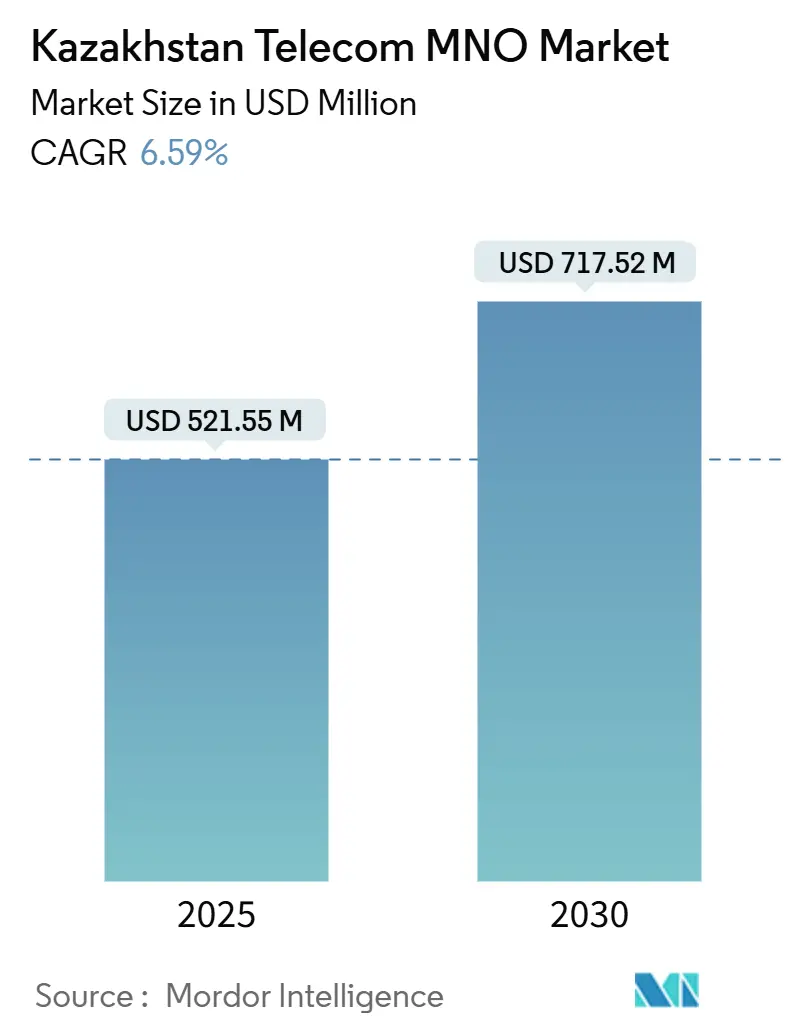

| Market Size (2025) | USD 521.55 Million |

| Market Size (2030) | USD 717.52 Million |

| Growth Rate (2025 - 2030) | 6.59% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kazakhstan Telecom MNO Market Analysis by Mordor Intelligence

The Kazakhstan Telecom MNO Market size is estimated at USD 521.55 million in 2025, and is expected to reach USD 717.52 million by 2030, at a CAGR of 6.59% during the forecast period (2025-2030). In terms of subscriber volume, the market is expected to grow from 26.30 million Subscribers in 2025 to 32.90 million Subscribers by 2030, at a CAGR of 4.57% during the forecast period (2025-2030).

Rising mobile-data usage, rapid 5G pilot launches, and large-scale fiber roll-outs under the Digital Kazakhstan program are broadening addressable revenue pools. Operators also benefit from robust urban demand for OTT video and cloud gaming, stronger wholesale earnings from new Eurasian fibre corridors, and government commitments to deliver universal 4G along national highways. At the same time, elevated network-upgrade costs and currency-driven equipment inflation force operators to migrate subscribers to higher-value bundles and prioritize CAPEX efficiency. Heightened foreign participation, illustrated by Power International Holding’s 2025 acquisition of Altel, injects fresh capital and innovation know-how, intensifying competition around network quality and digital-service portfolios. [1]Ministry of Digital Development, “Digital Kazakhstan Programme Status Update 2025,” gov.kz

Key Report Takeaways

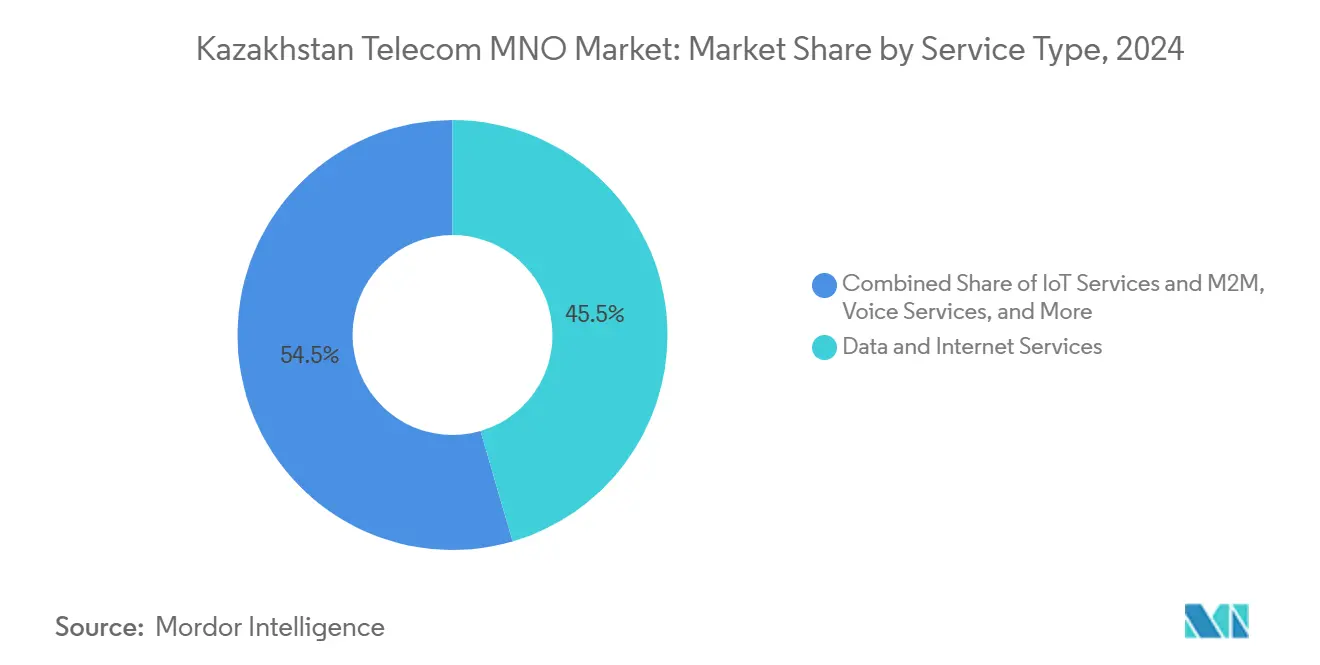

- By service type, Data and Internet Services led with 45.48% revenue share in 2024, whereas IoT & M2M Services are forecast to expand at a 6.68% CAGR through 2030.

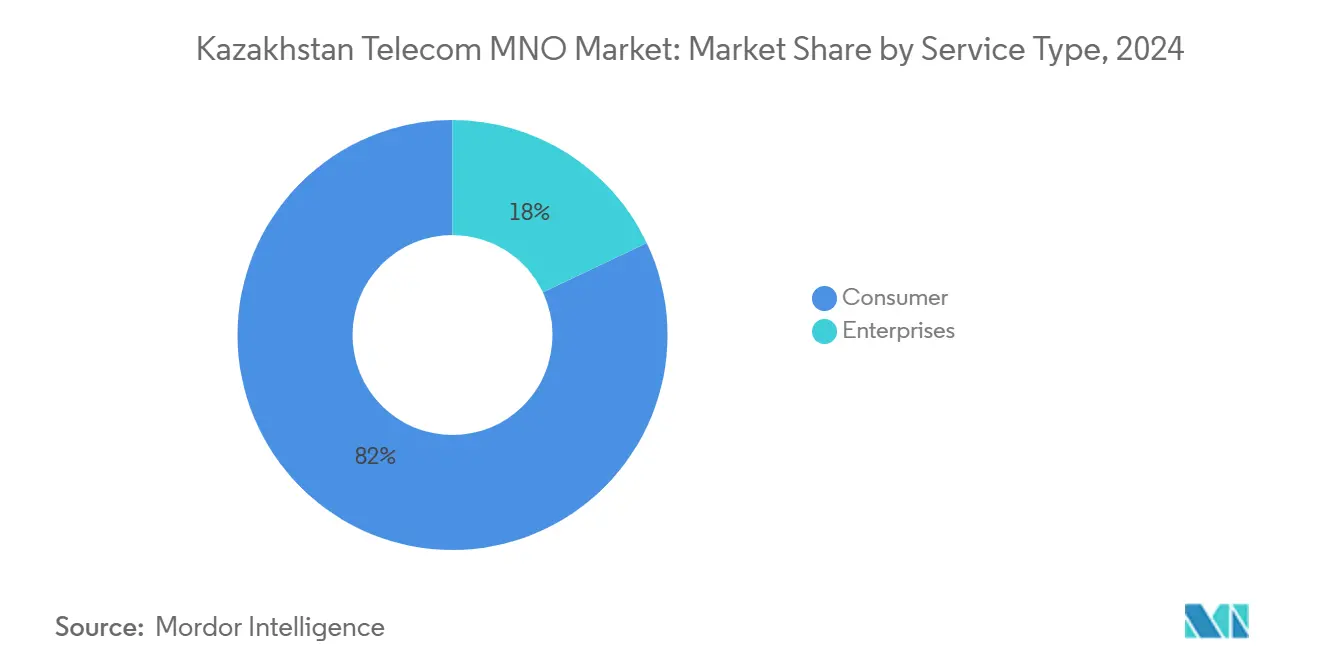

- By end-user, consumer services accounted for 82.04% of the Kazakhstan telecom MNO market share in 2024, while enterprise services are projected to grow at a 7.16% CAGR over 2025-2030.

Kazakhstan Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G spectrum auction & rollout under Digital Kazakhstan | 1.8% | National, with early deployment in Almaty, Nur-Sultan | Medium term (2-4 years) |

| Soaring mobile-data traffic from OTT video & gaming | 2.1% | National, concentrated in urban areas | Short term (≤ 2 years) |

| Accelerated FTTH build-out via PPP financing | 1.5% | National, priority in rural regions | Long term (≥ 4 years) |

| Enterprise digital-transformation (cloud / IoT) projects | 1.2% | National, concentrated in Almaty, Nur-Sultan business districts | Medium term (2-4 years) |

| Cross-border fibre corridors boosting wholesale income | 0.9% | Regional, Trans-Caspian route via Aktau-Siyazan | Long term (≥ 4 years) |

| LEO-satellite backhaul opening remote-area demand | 0.7% | National, focused on remote and rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

5G spectrum auction & rollout under Digital Kazakhstan

Limited commercial 5G services launched by Kcell and Tele2-Altel in early 2025 showcased throughput improvements exceeding 1 Gbps in dense-traffic zones, encouraging early enterprise trials for factory automation and smart-city sensor grids. The government intends to release additional spectrum blocks in the 6425-7125 MHz band, which remains largely unallocated, creating pricing headroom and service-tier differentiation for operators that accelerate deployment. With current 5G coverage touching 38.2% of the population, incremental roll-outs in transport corridors and industrial parks are expected to unlock premium ARPU streams from latency-sensitive applications. [2] Ministry of Industry & Infrastructure Development, “5G Spectrum Roadmap,” gov.kz

Soaring mobile-data traffic from OTT video & gaming

Kazakhstan’s mobile-data load surged from 356 PB in 2018 to nearly 1,000 PB in 2022 as video now represents the bulk of downstream traffic. Peak-hour congestion in Almaty prompts regulatory scrutiny and pushes operators to densify sites, refarm spectrum, and deploy AI traffic-management tools. Although heavier usage supports data-bundle upselling, it also lifts backhaul and power costs, compelling MNOs to negotiate favourable tower-leasing terms and embrace energy-efficient radio units.

Accelerated FTTH build-out via PPP financing

Kazakhtelecom spearheads fibre-to-the-home expansion through joint-investment schemes that share risk with state development funds, targeting 95% household fibre availability by 2025. Deeper fibre penetration shrinks mobile backhaul expenses, supports Wi-Fi-offload strategies, and provides a platform for converged 5P play bundles. Rural residents benefit from symmetrical broadband links, enabling MNOs to cross-sell fixed-wireless access plans where trenching costs remain prohibitive.

Enterprise digital-transformation (cloud/IoT) projects

Large miners, refiners, and energy producers increasingly deploy private LTE and 5G slices to automate heavy-equipment fleets, predictive-maintenance workflows, and asset-tracking systems. Beeline’s AI-driven forest-fire detection solution, built on its mobile core, illustrates monetisable use cases that blend connectivity and analytics services. Rising cloud adoption among banks and e-commerce platforms further elevates demand for low-latency, high-availability MPLS and SD-WAN connectivity, reinforcing enterprise ARPU momentum.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising 5G & fibre CAPEX burden on operator ROI | -1.4% | National, concentrated in urban deployment areas | Medium term (2-4 years) |

| Tenge depreciation inflating imported equipment costs | -1.1% | National, affecting all operators equally | Short term (≤ 2 years) |

| Data-localisation mandates raising OPEX | -0.8% | National, compliance requirements for all operators | Long term (≥ 4 years) |

| Scarcity of Kazakh-language digital content curbing usage | -0.6% | National, particularly affecting rural populations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising 5G & fibre CAPEX burden on operator ROI

Layering 5G NR on top of an already dense 4G grid, while simultaneously trenching fibre to base-station and household clusters, doubles capital commitments. Beeline’s Giga City program encapsulates this pressure, adding 1,800 Massive-MIMO sites yet only gradually converting that capacity into revenue as ARPU growth trails data-traffic expansion. Operators respond by trimming legacy copper assets, rationalising overlapping tower portfolios, and lobbying regulators for longer spectrum-licence tenors to smooth depreciation schedules.[3]ZTE Corporation, “Massive-MIMO Deployment Case Study Kazakhstan,” zte.com.cn

Tenge depreciation inflating imported equipment costs

Radio units, antennas, and core-network servers are largely priced in USD or EUR, making total project budgets highly sensitive to FX swings. The tenge’s weakening against major currencies between 2024-2025 lifted landed equipment prices and caused mobile-tariff hikes averaging 25%, inviting consumer-advocacy scrutiny. Smaller regional carriers lacking hedging tools face the harshest margin squeeze and risk postponing rural roll-outs, thereby delaying nationwide coverage targets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Anchor Revenue Momentum

Data and Internet Services captured 45.48% of the Kazakhstan telecom MNO market in 2024, signalling the clear transition from voice-centric bundles to gigabyte-driven propositions. In absolute terms, this service line generated USD 237 million, and its contribution to the Kazakhstan telecom MNO market size is set to widen as video, cloud gaming, and ultra-HD sports streams dominate usage patterns. Operators now bundle unlimited social-media buckets, zero-rate video portals, and multi-device sharing to lock in higher-tier subscribers. Complementing this, the IoT & M2M category is forecast to grow at 6.68% CAGR, underwritten by industrial telematics deployments in mining belts and sensor grids in smart-irrigation schemes. Although legacy SMS volumes keep sliding, A2P messaging for two-factor authentication moderately cushions the decline.

Voice illustrates a managed-decline profile, still important for regulator-mandated universal-service metrics and inbound roaming margins. OTT and PayTV tie-ups—ranging from local cinema libraries to regional sports packages—extend operators’ relevance inside the living room, spawning new bundles that lift viewer engagement and dampen churn. Enhanced enterprise packages that merge fixed broadband, managed SD-WAN, and private LTE segments are set to add close to USD 36 million to the Kazakhstan telecom MNO market size by 2030, supported by favourable spectrum-leasing policies.

By End-User: Enterprise Uptake Accelerates

Consumer traffic will keep dominating total gigabytes, yet incremental revenue growth increasingly comes from B2B use cases. The consumer slice accounted for 82.04% of the Kazakhstan telecom MNO market share in 2024, but its five-year revenue CAGR trails that of enterprises because subscriber penetration is nearing saturation in urban clusters. Enterprise services are on course to post a 7.16% CAGR, translating into an extra USD 72 million in annual revenue by 2030 for the Kazakhstan telecom MNO market size. Demand comes from cloud-native SMEs as well as industrial conglomerates modernising SCADA networks. Private 5G in rail yards and ports offers deterministic latency, while secure APN configurations position MNOs as partners in financial-services data-centre replication strategies.

Historically conservative state-owned entities now fast-track digitisation to meet e-procurement and e-tax mandates, lifting MPLS upgrades and managed security orders. Edge-cloud zones being built near Almaty reduce round-trip latency, enabling computer-vision quality control on assembly lines. As wholesale price caps fall along the Eurasian fibre route, global hyperscalers co-locate equipment in carriers’ data centres, further diversifying operator income streams.

Geography Analysis

Nationwide 4G footprint already covers 89.2% of residents, yet performance gaps persist between metropolitan and rural zones. Almaty and Nur-Sultan together account for roughly half of all 5G compatible devices in service and host pilot industrial-IoT campuses supported by network-slicing. Western coastal regions around Aktau leverage new submarine linkages under the Trans-Caspian project, tapping transit fees from Europe-Asia data flows. These corridors help monetise spare backbone capacity, boosting wholesale revenue and elevating Kazakhstan telecom MNO market size at the national level.

In semi-arid central provinces, fibre build-outs lag because of longer trenching distances. Operators therefore trial LEO-satellite backhaul, which lowers latency versus GEO systems and grants residents 50-100 Mbps service tiers. Government grants tied to the “Digital Partner in the Village” initiative offset some deployment risk, encouraging carriers to roll advanced LTE-Advanced Pro features even in low-density districts. Road-coverage mandates to 2027 further spur tower infill along key logistics arteries, unlocking incremental roaming receipts.

Eastern border areas benefit from cross-border trade with the Xinjiang economic zone, and latency-sensitive traffic exchanges with Chinese cloud platforms demand resilient routes. New 100G upgrades on the RETN TRANSKZ backbone furnish extra capacity headroom, ensuring seamless traffic hand-off and reducing packet loss during peak hours. Collectively, these geographical dynamics yield a balanced market-expansion pattern, enriching the Kazakhstan telecom MNO market while narrowing the urban-rural digital divide.

Competitive Landscape

Four nationwide operators shape market outcomes. Beeline Kazakhstan held 45% subscriber share in 2024 and exploits VEON’s global digital-app stack to differentiate. Its Janymda super-app bundles payments, streaming, and cloud storage, lifting non-connectivity revenues to more than 14% of local turnover. Kcell follows at 42% share, harnessing parent Kazakhtelecom’s dense fibre plant to accelerate 5G outdoor small-cell roll-outs and serve enterprise VPN contracts. Tele2/Altel, now controlled by Qatar-based Power International Holding, commands 13% share and positions itself as a value challenger emphasising superior download speeds that averaged 69.91 Mbps in 2025, marginally ahead of rivals.

Network-quality metrics have emerged as a decisive churn driver. Ookla’s latest study shows Tele2’s user-satisfaction index topping 85.3%, prompting Beeline to modernise 1,800 sites with FDD Massive-MIMO arrays in partnership with ZTE. Kcell focuses on indoor-coverage gains through spectrum-aggregation and voice-over-NR roll-outs in modern office towers. Outside traditional cellular footprints, Starlink and OneWeb add a nascent competitive dimension in remote communities, nudging MNOs to push cheaper fixed-wireless offers. Intensifying rivalry encourages spectrum-sharing discussions and tower-co-tenancy schemes that lower cost per megabyte and keep Kazakhstan telecom MNO market dynamics attractive for investors.

Regulatory oversight remains pragmatic, with licences extended to 2035 to protect ROIC, while wholesale fixed-line tariffs are gradually liberalised to foster cross-border traffic. The foreign-ownership ceiling in telecoms was relaxed in 2025 for operators contributing to Digital Kazakhstan milestones, encouraging further capital injections and technology transfers.

Kazakhstan Telecom MNO Industry Leaders

Beeline Kazakhstan

Kcell

Altel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Power International Holding completed the acquisition of 100% interest in Mobile Telecom-Service LLP (Tele2/Altel), broadening foreign investment in domestic networks.

- December 2024: OneWeb signed an LoI with Ghalam LLP for local satellite component manufacturing, advancing LEO-broadband localization.

- October 2024: The Cabinet approved the National Infrastructure Plan 2029, budgeted for 10 flagship digital-connectivity projects.

- June 2024: Beeline and ZTE finalized the “Giga City” RAN modernization across Akmola and Turkestan, switching on 1,800 Massive-MIMO sites.

Kazakhstan Telecom MNO Market Report Scope

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

What is the current value of the Kazakhstan telecom MNO market?

The market was valued at USD 521.55 million in 2025 and is forecast to reach USD 717.52 million by 2030.

How fast is mobile-data traffic growing in Kazakhstan?

Total mobile-data volume rose nearly threefold between 2018 and 2022, driven mainly by OTT video and cloud gaming consumption.

Which service segment is expanding the quickest?

IoT & M2M connectivity is projected to grow at a 6.68% CAGR between 2025-2030.

What drives enterprise demand for telecom services?

Enterprise cloud migration, private 5G networks in heavy industry, and wider adoption of IoT analytics platforms fuel B2B connectivity spending.

How will 5G coverage evolve by 2030?

Additional spectrum auctions and ongoing infrastructure build-outs are expected to lift 5G population coverage well beyond the current 38.2%, supporting nationwide smart-city and industrial-automation projects.

Page last updated on: