Uzbekistan Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

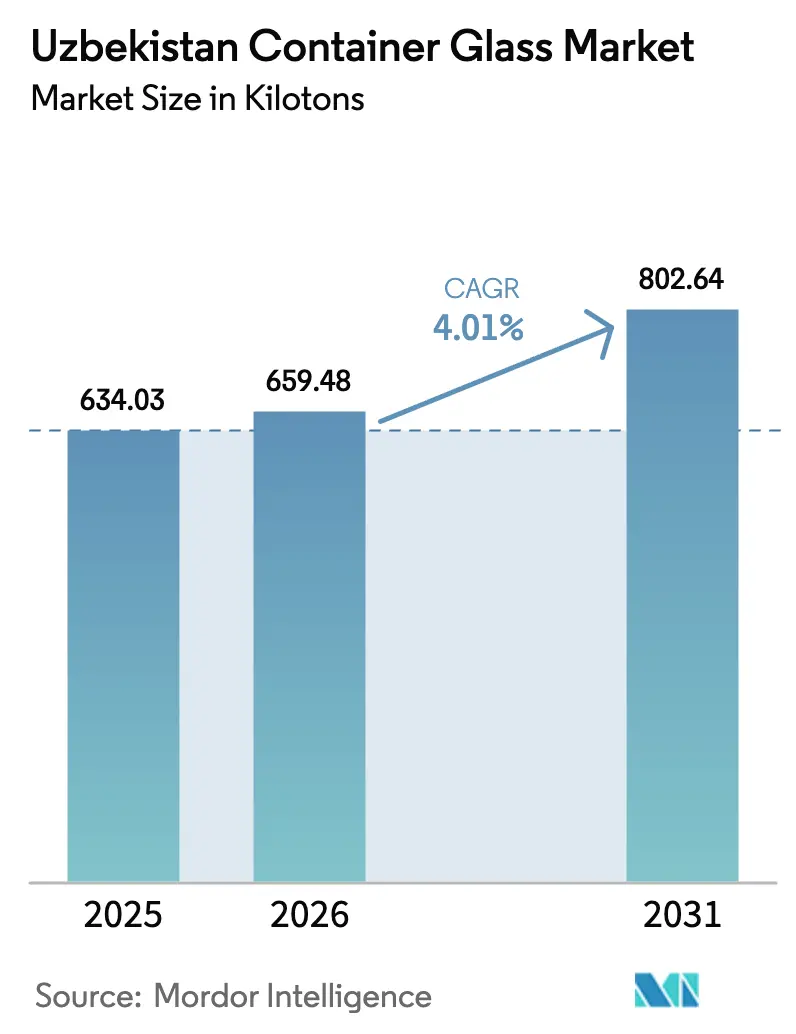

| Base Year Market Size (2025) | 634.03 kilotons |

| Market Volume (2026) | 659.48 kilotons |

| Market Volume (2031) | 802.64 kilotons |

| Growth Rate (2026 - 2031) | 4.01% CAGR |

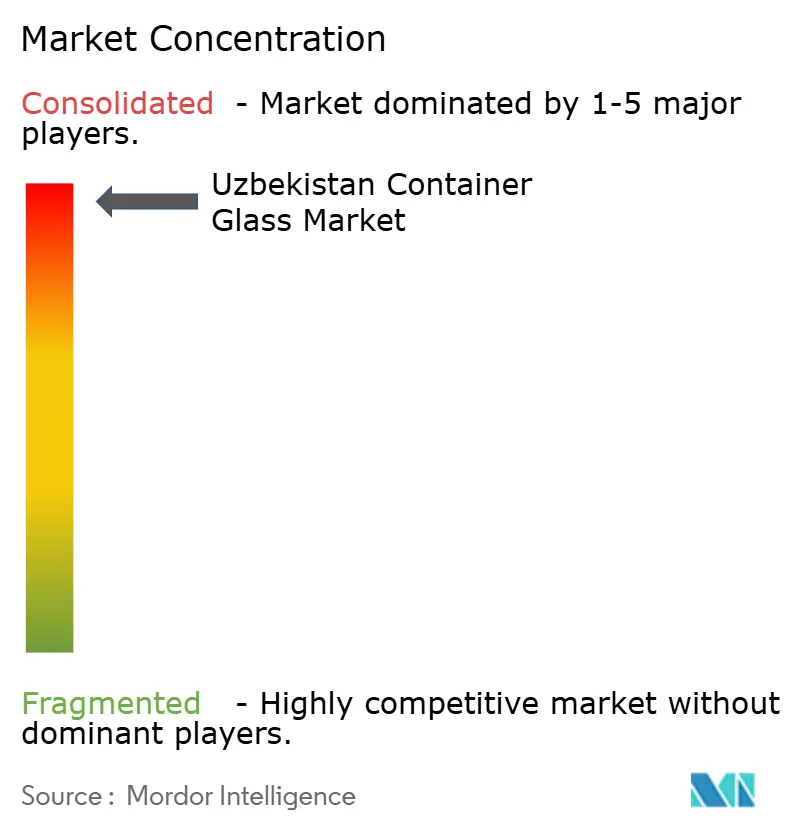

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Uzbekistan Container Glass Market Analysis by Mordor Intelligence

The Uzbekistan container glass market size is expected to grow from 634.03 kilotons in 2025 to 659.48 kilotons in 2026 and is forecast to reach 802.64 kilotons by 2031 at 4.01% CAGR over 2026-2031. This steady trajectory is anchored in strong demand from the beverage sector, a national industrialization push, and duty-free access to the European Union under the GSP+ scheme, all of which channel fresh capital into furnace upgrades and greenfield plants.[1]European Commission, “GSP+ assessment of the Republic of Uzbekistan,” eur-lex.europa.eu Domestic manufacturers benefit from quartz-sand deposits in Sirdaryo and Jizzakh, as well as rising halal-certified food exports, and government tax holidays that shield foreign joint ventures from profit tax for up to seven years. At the same time, the Uzbekistan container glass market faces intensifying competition from domestic PET and aluminum can investments, higher gas tariffs, and the logistics premium that accompanies a double-landlocked geography. Strategic responses include greater cullet utilization, amber-glass capacity for UV-sensitive pharmaceuticals, and export-oriented product lines with EU-compliant safety markings.

Key Report Takeaways

- By end-user, beverages captured 62.09% of Uzbekistan container glass market share in 2025.

- By color, the Uzbekistan container glass market for amber glass is projected to grow at a 5.31% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Uzbekistan Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eco-friendly packaging preference | +0.8% | National; Central Asian export spillover | Medium term (2-4 years) |

| Food and beverage sector growth | +1.2% | Tashkent and Samarkand regions | Short term (≤2 years) |

| State-backed furnace capacity expansion | +0.9% | Sirdaryo, Jizzakh, and Tashkent clusters | Short term (≤2 years) |

| EU-GSP+ export opportunity for glass-packed foods | +0.6% | National; EU-compliant facilities | Medium term (2-4 years) |

| Halal-compliance push for inert containers | +0.4% | Domestic and Muslim-majority export markets | Long term (≥4 years) |

| Local soda-ash self-sufficiency | +0.3% | National raw-material chain | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Food and beverage sector growth

Food and beverage manufacturers increased their output value by 26.3% in Fergana during 2024, underpinned by a USD 200 million credit line reserved for construction materials and packaging companies. These policy funds enable breweries, juice houses, and dairy processors to commit to long-term glass supply contracts, thereby underpinning baseline furnace utilization across the Uzbekistan container glass market. Sector leaders are also integrating halal certification to meet export compliance in Gulf and South-Asian markets, where inert glass is favored over PET for premium positioning. Parallel upgrades in cold-chain logistics expand the shelf-life benefits that glass provides. As a result, volume off-take agreements from beverage fillers are lengthening to five-year horizons, improving cash-flow predictability for container manufacturers. Bottle design collaborations, often executed with Czech mold makers, further differentiate local brands in growing craft-beer and artisanal-juice sub-segments.

State-backed furnace capacity expansion

Sirdaryo Universal Oyna scaled to 102 million containers annually by adopting triple-gob IS machines procured from Germany, while Sirdaryo Glass will add another 136.1 million units of colored pharmaceutical ware when it comes on-stream in late 2025. The adjacent quartz-sand beneficiation line removes iron-oxide impurities, allowing low-E cobalt-free coloration that meets EU heavy-metal thresholds. Government-guaranteed loans from Asaka Bank keep interest costs below 6%, and customs exemptions slash capex by 8-10%. This policy cocktail shortens payback periods, attracts Chinese FDI such as Mingyuan Silu’s USD 150 million Jizzakh expansion, and drives the Uzbekistan container glass market toward economies of scale. Capacity additions translate into bulk-melting cost efficiencies that partly offset the April 2025 gas-tariff hike, preserving gross margins for export consignments.

EU-GSP+ export opportunity for glass-packed foods

The 92.7% utilization rate of Uzbekistan’s GSP+ allowances in 2022 confirms exporters' ability to capture tariff-free EU niches. Glass-packed cherries, pickles, and honey occupy premium supermarket shelves in Germany, Italy, and the Baltic states, where single-origin produce commands higher price points. EU zero-tariff access also accelerates investments in BRC and ISO 22000 certification among Uzbek fillers, which in turn lifts demand for traceability-compliant glass bottles and jars. Still, overland transit via the Middle Corridor adds four to five days to lead times; therefore, producers favor lighter, high-value amber containers that maximize revenue per kilogram. To hedge against logistics volatility, firms are increasingly using bonded rail depots in Georgia and Azerbaijan for cross-docking, an emerging model that reshapes distribution patterns in the Uzbekistan container glass market.

Eco-friendly packaging preference

Consumer polls conducted in Tashkent supermarkets indicate that 42% of shoppers in 2025 actively choose glass over plastic when price differentials are within 12%. This sentiment aligns with the 2020 Tashkent waste-segregation law, which mandates color-coded bins, thereby boosting cullet recovery from 20% in 2018 toward a 35% mid-term target. The Uzbekistan container glass industry capitalizes on marketing infinite recyclability and migration-free storage. KPMG’s local circular-economy roadmap recommends standardizing bottle dimensions to simplify in-store returns, a policy that could inject an additional 28 kilotons of cullet annually into furnace batches.[2]Abdullakhanov Farrukh, “Circular economy in consumer goods,” kpmg.com Firms respond by retrofitting optical sorters that are compatible with green and amber shards, prompting cullet ratios to climb past 30%, thereby reducing melting energy by roughly 2.5% per 10% cullet increment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PET and lightweight packaging substitution | -1.1% | Urban centers nationwide | Short term (≤2 years) |

| High inland freight cost in double-landlocked country | -0.7% | National export lanes | Medium term (2-4 years) |

| Rising energy prices and gas-diversion policies | -0.9% | Energy-intensive factories | Short term (≤2 years) |

| Stricter safety-regulation compliance costs | -0.4% | Food-contact applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PET and lightweight packaging substitution

Uzbekistan’s first methanol-to-olefins complex in Bukhara will produce 1.1 million tonnes of polymers annually, including PET preforms that undercut glass on delivered cost per unit. Simultaneously, East Can Solutions’ 2.2 billion-unit aluminum line provides beverage brands with a lighter container that offers superior cube efficiency, eroding glass’s share in mass-market sodas. The weight penalty also magnifies freight costs, a pressing concern because logistics absorb 16.5% of the GDP. Glass producers counter by promoting shelf-life advantages, flavor neutrality, and the premium aura associated with clear or amber flint; yet, substitution risk remains highest in single-serve segments. Niche differentiators such as laser-etched logos and smart barcodes triggered by EU traceability rules help defend market share, but price-sensitive consumers in provincial cities continue to migrate toward cheaper PET bottles, especially for still water.

Rising energy prices and gas-diversion policies

The April 2025 tariff hike, which raised gas prices to 1,000 UZS/m³, inflates melting costs by roughly USD 5.8 per tonne of glass, thereby slashing EBITDA for smaller furnaces operating on outdated recuperative technology. Planned cost-recovery tariffs could increase rates by another 25-30% by 2027, aligning Uzbekistan with regional parity but potentially squeezing the Uzbekistan container glass market during the transition. Producers experiment with oxy-fuel burners and batch pre-heaters to reduce specific energy consumption, while others negotiate renewable power purchases aligned with the national 40% renewable energy target for 2030. Unplanned gas curtailments compound the issue; a day-long furnace shutdown can trigger cold-repair costs exceeding USD 400,000, forcing mills to keep buffer LPG inventories. The diversion of gas to higher-margin MTO petrochemical plants further tightens the supply, compelling manufacturers to lobby for protected industrial quotas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Volume, Cosmetics Lead Growth

The beverages segment dominated with 62.09% of Uzbekistan container glass market share in 2025, backed by rising per-capita soft-drink consumption and robust beer exports to Kazakhstan. High-volume fillers in Tashkent sign multi-year offtake deals that ensure base-load furnace utilization, making beverages the anchor customer group. The segment also absorbs color-variant demand, from flint for premium vodkas to emerald green for sparkling wines aimed at Russian tourists. Going forward, beverage glass demand will trail a 4.08% CAGR, mirroring national GDP projections and steady urbanization.

The cosmetics and personal-care category, although smaller, is forecast to outpace the market at a 5.19% CAGR, benefiting from e-commerce beauty sales and local influencer brands that favor upscale flint jars. Urban millennials perceive glass droppers as a symbol of safety, countering microplastics linked to PET. The Uzbekistan container glass market size for cosmetics containers is projected to increase from 19.56 kilotons in 2026 to 25.23 kilotons by 2031, driven by duty-free EU access that enables local contract fillers to serve Italian niche perfumes. Pharmaceutical demand, especially for amber syrups and ophthalmic bottles, adds a defensive layer because these products face stricter migration limits that glass easily meets.

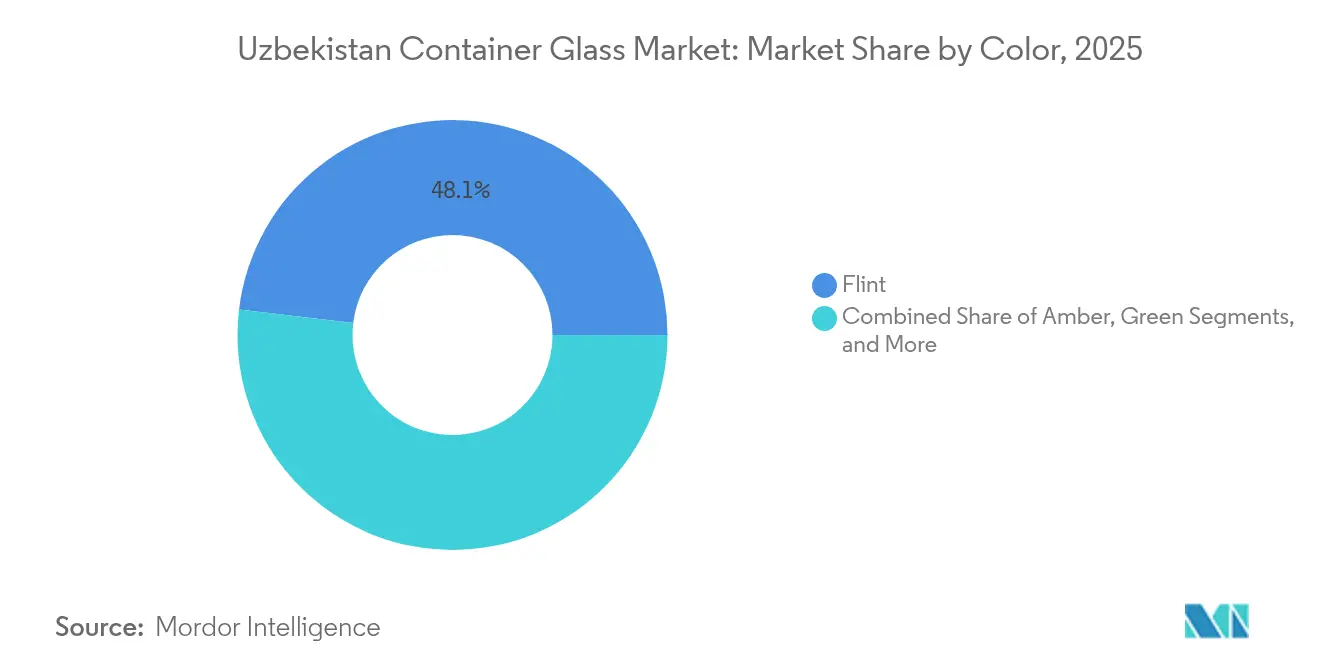

By Color: Flint Dominates, Amber Accelerates

Flint owned 48.10% of the Uzbekistan container glass market in 2025, propelled by its versatility, visual clarity, and compatibility with laser-engraved branding. Clear bottles remain the default for vodkas, juices, and laboratory reagents. High-quality silica inputs from Navoi deposits keep iron content below 0.026%, assuring near-water-white clarity for premium applications. As a result, Uzbek flint exports find receptive buyers in Tajikistan and Afghanistan, where local furnace technology struggles to achieve the same level of brightness.

Amber is projected to clock the fastest 5.31% CAGR through 2031 as pharma bottlers migrate to UV-shielding containers for light-sensitive antibiotics. Sirdaryo Glass dedicates an entire furnace to amber flux, utilizing selenium-free formulations to meet EU heavy metal ceilings. Research by the Uzbek Academy of Sciences confirms that substituting enriched coal ash for 8% of batch weight yields comparable chromaticity at 6% lower cost. The Uzbekistan container glass market thus gains a cost-effective path to premium, export-friendly amber with a sustainability narrative rooted in waste-ash valorization.

Geography Analysis

Uzbekistan’s eastern industrial belt, stretching from Tashkent to Fergana, accounts for 65% of the country's national freight volumes and concentrates 56.72% of the demand for container glass. Proximity to grain and fruit belts supports integrated agro-processing hubs, while rail links to Kazakhstan’s Almaty region enable two-day door-to-door beer shipments. The Middle Corridor’s throughput jumped from 600,000 tons in 2021 to 2.7 million tons in 2023, shortening lead times to Georgian ports and nudging European buyers to trial Uzbek glass jars for pickled vegetables. In contrast, western Karakalpakstan remains an underserved demand pocket, constrained by sparse transport and higher delivered glass prices.

Kazakhstan emerges as the top export destination: Kyzylorda’s own glass plant still supplies 30% of its output to Uzbekistan, Kyrgyzstan, and Tajikistan, indicating reciprocal trade flows. Uzbek producers compete by offering shorter lead times, an advantage during seasonal beverage peaks. Meanwhile, EU demand, although still below 8% of the total volume, is increasing under the GSP+ umbrella. Hot-filled cherry juice in 370-ml flint jars captured shelf space in German organic chains during 2025, validating the export pivot. Yet the double-landlocked handicap inflates freight; exporters dedicate 2%-3% of invoice value to trans-Caspian insurance surcharges, a cost partly offset by higher unit margins in value-added amber pharma bottles bound for Baltic repackaging hubs. Southern corridors toward Afghanistan show promise for halal-certified glass, but political risk keeps volumes modest. Nonetheless, traders in Termez report a 14% increase in small-lot shipments in 2024, primarily consisting of honey jars and spice grinders. Government investments in the Termez–Mazar-e-Sharif railway could unlock larger flows, allowing the Uzbekistan container glass market to diversify beyond overland CIS lanes. Domestically, Sirdaryo’s central location underpins balanced east-west distribution, with multi-modal depots enabling 48-hour truck-rail combinations that serve both Samarkand confectioners and Bukhara pharma plants.

Competitive Landscape

The Uzbekistan container glass market exhibits moderate fragmentation, with state-aligned champions and foreign joint ventures consolidating their positions. The top five producers account for roughly 62% of installed capacity, driven by policy incentives that favor them in bidding and land allocation. Sirdaryo Universal Oyna exemplifies vertical integration: an on-site sand-washing plant feeds two float-line furnaces while waste heat powers a greenhouse cluster, anchoring a micro-industrial ecosystem. German IS machines assure 425 bph efficiency on 330-ml beer formats, enabling competitive unit costs even after the April 2025 gas hike.

Chinese entrant Mingyuan Silu leverages preferential credit from the Export-Import Bank of China, integrating low-interest financing with equipment sourced domestically to undercut Western vendors by 8-10%. In contrast, legacy player Kvartz relies on its reputation, shipping flint to five neighboring states and operating a private rail spur that reduces transit time to the Kazakh border to 18 hours. Product differentiation revolves around color capability, embossing technology, and WRI performance. Local SMEs attempt to carve out niches in the artisanal food market, but they face hurdles in procuring raw materials because soda ash allocations favor larger furnaces under government prioritization lists.

Non-glass investments amplify competitive pressure: East Can Solutions and Arnest’s USD 190 million can lines produce 3.7 billion units annually.[3]AL Circle, “Uzbekistan’s aluminium cans manufacturing unit,” alcircle.com To fight back, glass makers are embarking on ESG branding and marketing life-cycle carbon analyses, which show a 20% footprint reduction at 30% cullet content. Technology upgrades, such as forehearth blending that allows for color changes within 6 hours, also enable producers to chase short-run niche orders. Strategic OEM alliances with Czech mold makers enable proprietary embossing; combined with e-commerce cosmetics, these boutique formats secure higher margins and insulate against fluctuations in PET prices. Market consolidation is likely as private-equity investors scour furnace assets for turnaround opportunities once cost-recovery tariffs stabilize.

Uzbekistan Container Glass Industry Leaders

ASL OYNA LLC

IP Campalia LLC

Kvarts Aksiyadorlik Jamiyati

Sirdaryo Universal Oyna

Exclusive Glass Bottles LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Uzbekistan and Belarusian KUVO initiated talks on laminated-glass cooperation to expand automotive glazing capabilities.

- May 2025: UET Invest purchased a 100% stake in the Avtooyna automotive glass plant for 200.5 billion soums (USD 16.7 million)

- May 2025: President Mirziyoyev inaugurated the USD 5 billion methanol-to-olefins complex in Bukhara, producing 1.1 million t of polymers annually, adding competitive pressure on glass.

- April 2025: The EU-Uzbekistan strategic partnership on critical raw materials was signed, streamlining access to specialty glass inputs

Uzbekistan Container Glass Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

The Uzbekistan container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Uzbekistan container glass market today?

The Uzbekistan container glass market size reached 659.48 kilotons in 2026 and is forecast to exceed 802.64 kilotons by 2031 at a 4.01% CAGR.

Which end-use segment dominates demand for containers?

Beverages hold 62.09% of volume, anchoring furnace utilization through long-term supply contracts with breweries and soft-drink fillers.

What is the fastest-growing container glass segment by color?

Amber glass is projected to expand at a 5.31% CAGR through 2031, propelled by demand from pharmaceuticals and premium foods.

How do energy tariffs affect glass producers?

The April 2025 gas-price hike to 1,000 UZS/m³ raised melting costs by about USD 5.8 per tonne, prompting investments in energy-saving furnaces and cullet use.

What export advantages does Uzbekistan enjoy in the EU market?

Duty-free GSP+ access covers two-thirds of tariff lines, enabling Uzbek glass-packed foods and cosmetics to enter Europe without import duties.

Who are the major new competitors to glass packaging?

Domestic PET polymer capacity from the new methanol-to-olefins complex and large-scale aluminum can plants by East Can Solutions and Arnest introduce lighter, cost-efficient substitutes.

Page last updated on: