Consumer Packaged Goods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

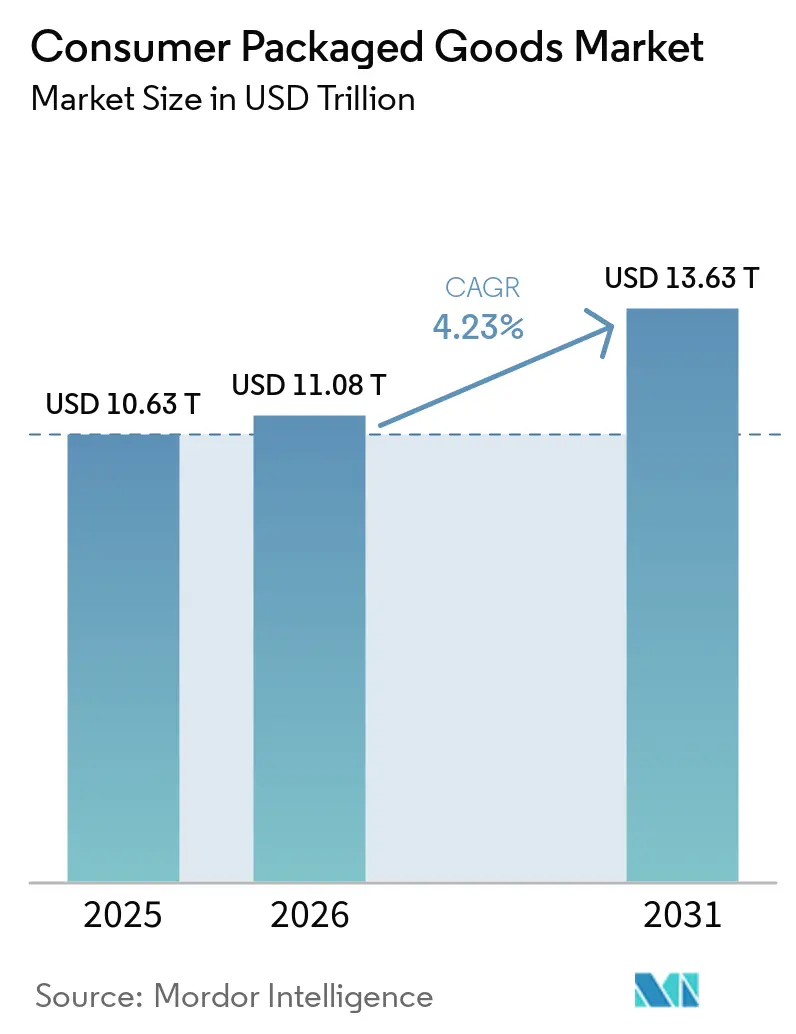

| Market Size (2026) | USD 11.08 Trillion |

| Market Size (2031) | USD 13.63 Trillion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

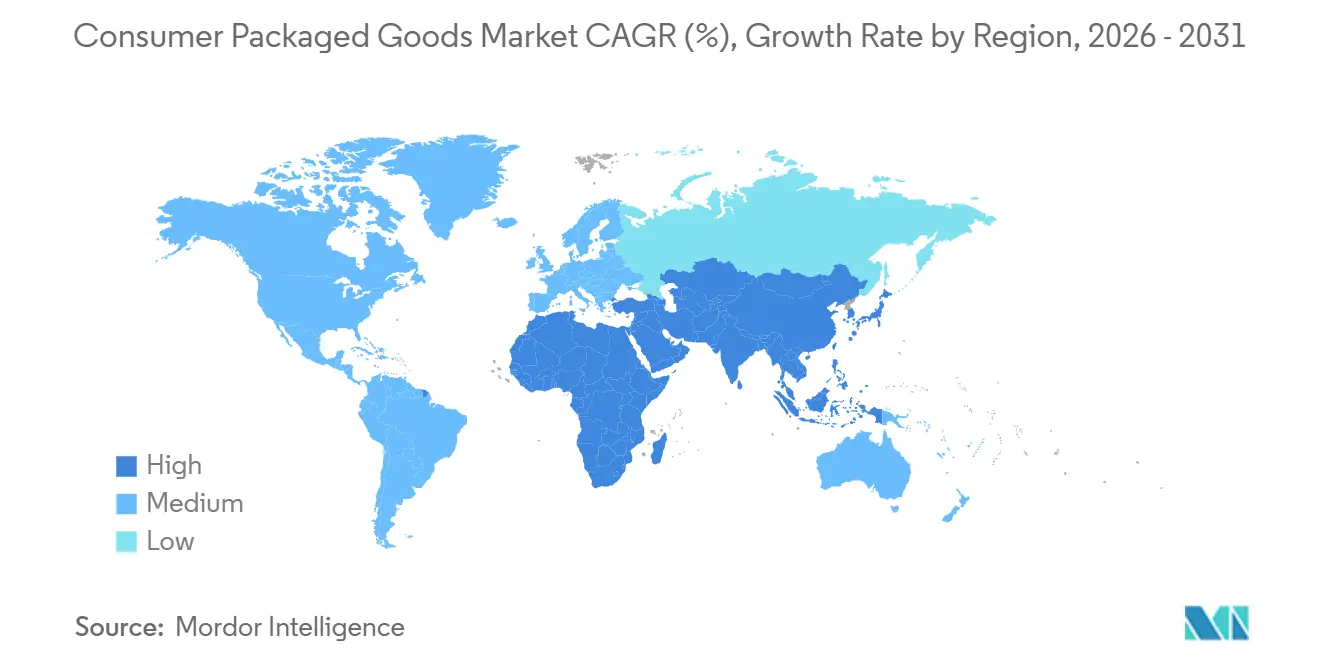

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Consumer Packaged Goods Market Analysis by Mordor Intelligence

The Consumer Packaged Goods Market is projected to grow from USD 10.63 trillion in 2025 to USD 11.08 trillion in 2026, reaching USD 13.63 trillion by 2031, with a CAGR of 4.23% during 2026–2031. This growth is primarily driven by rising demand for convenient, high-quality, and easily accessible products that cater to changing consumer lifestyles and purchasing behaviors. The increasing adoption of ready-to-use solutions, evolving consumption patterns, and the demand for reliable, safe, and user-friendly products are prompting manufacturers to enhance their offerings. Developments in processing technologies, product formulations, and packaging designs have improved product durability, functionality, and convenience, further boosting consumer acceptance.

Key Report Takeaways

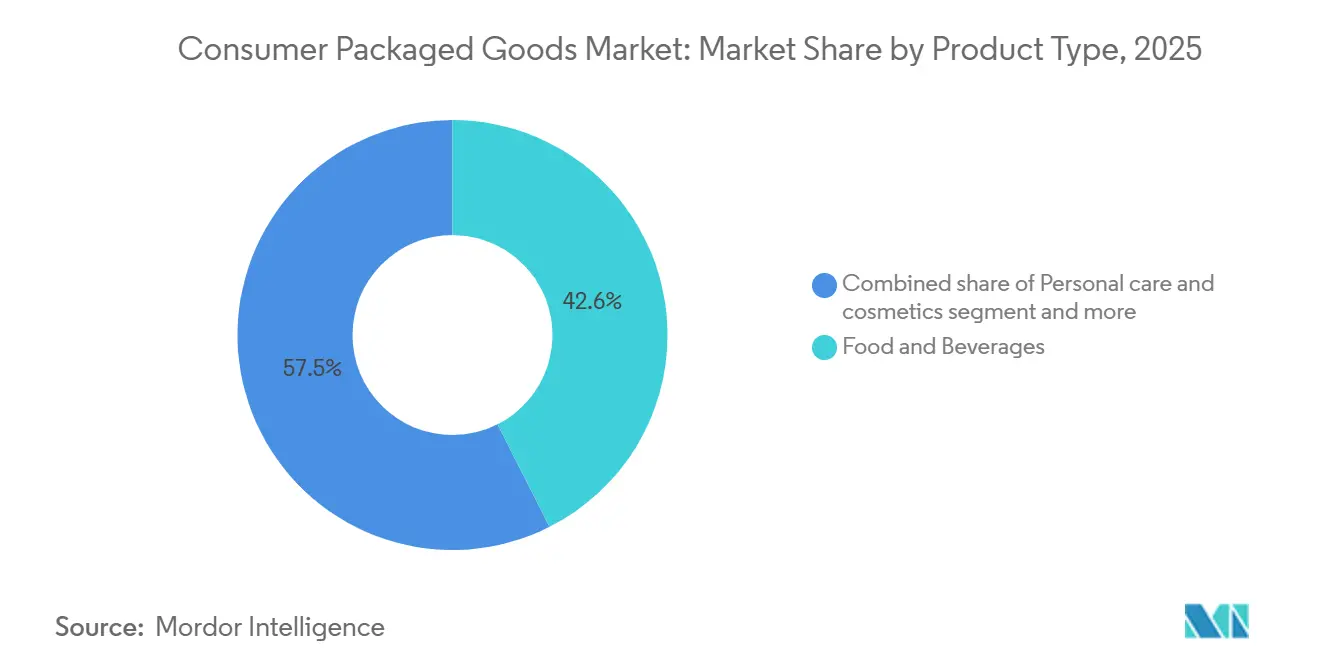

- By product type, Food and Beverages held 42.55% of the consumer packaged goods market share in 2025, while Personal Care and Cosmetics is projected to record the highest CAGR at 5.35% through 2031.

- By packaging type, Bottles led with a 36.81% share in 2025, while Pouches is forecast to grow the fastest at a 4.56% CAGR through 2031.

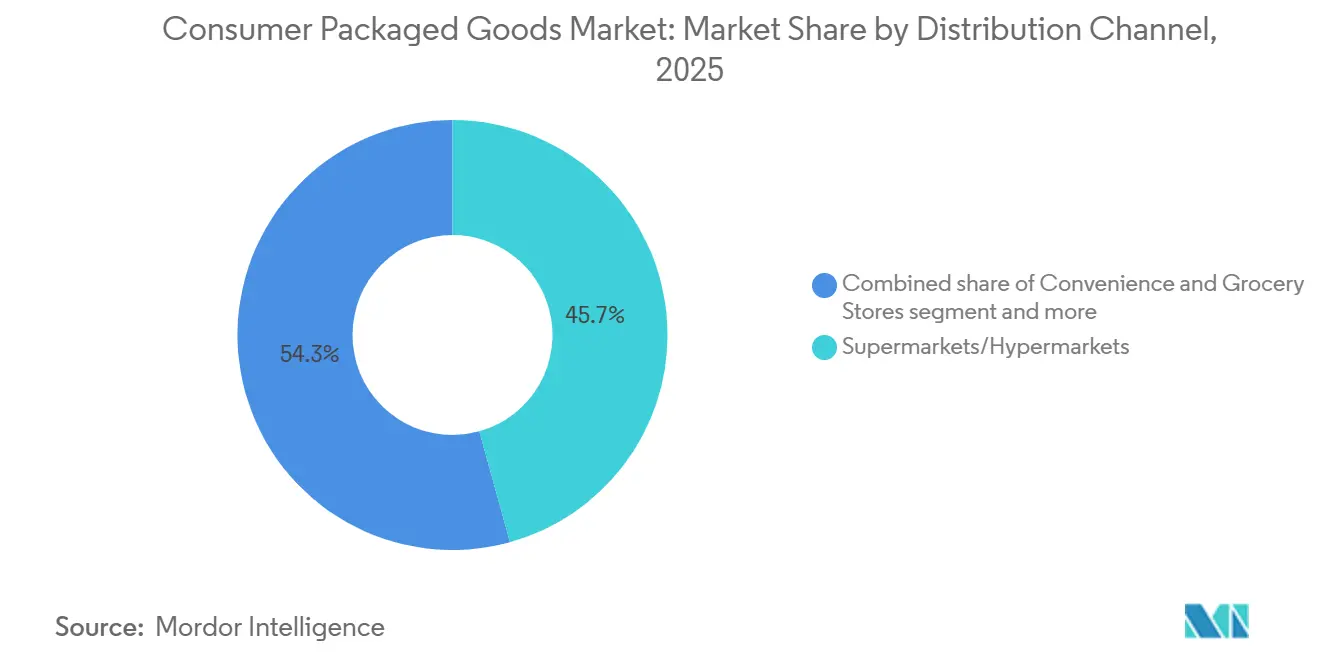

- By distribution channel, Supermarkets and Hypermarkets accounted for 45.69% of the market in 2025, while Online Retail Stores is expected to expand at a 6.13% CAGR through 2031.

- By end-user, Household Consumers represented 71.23% of demand in 2025, while Commercial Users is projected to advance at a 4.81% CAGR through 2031.

- By geography, Asia-Pacific captured 32.32% of the market in 2025 and is also set to post the fastest regional CAGR at 5.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Packaged Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenience and ready-to-use products | +1.1% | Global; strongest in North America and Asia-Pacific core, spill-over to South America | Short term (≤ 2 years) |

| Adoption of e-commerce and digital retail channels | +0.9% | Global; concentrated in Asia-Pacific, North America, and Western Europe | Medium term (2-4 years) |

| Consumer preference for health and wellness products | +0.8% | Global; strongest in North America and Europe, expanding in premium Asia-Pacific markets | Medium term (2-4 years) |

| Product innovation and premiumization trends | +0.7% | Global; early-stage in Middle-East and Africa and South America | Long term (≥ 4 years) |

| Urbanization and rising disposable incomes in emerging markets | +0.6% | Asia-Pacific, South America, and Middle East and Africa; strongest in India, Indonesia, and Sub-Saharan Africa | Medium term (2-4 years) |

| Growing consumer adoption of sustainability and eco-conscious purchasing | +0.5% | Global; strongest in EU and North America, emerging in premium Asia-Pacific segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for convenience and ready-to-use products

The demand for convenience and ready-to-use products is increasing due to changing consumer lifestyles and evolving purchasing preferences. Consumers are prioritizing products that offer ease of use, accessibility, and time efficiency while maintaining quality, reliability, and consistency. This trend has driven manufacturers to develop products with enhanced functionality, extended shelf life, and user-friendly designs. Advances in processing technologies, packaging innovations, and preservation methods have enabled brands to provide products requiring minimal preparation while ensuring freshness, safety, and convenience. The growing use of portable, single-use, resealable, and easy-to-store packaging formats has further improved consumer experiences and encouraged repeat purchases. Moreover, the expansion of digital retail channels and faster delivery services has enhanced access to convenient packaged goods, allowing consumers to shop according to their preferences and schedules.

Adoption of e-commerce and digital retail channels

The increasing adoption of e-commerce and digital retail channels is driving growth in the consumer packaged goods market by reshaping how consumers discover, compare, and purchase products. Enhanced digital connectivity, the rise of mobile commerce, and the expansion of online retail platforms have improved product accessibility and allowed brands to reach a wider audience. According to the International Telecommunication Union (ITU), the number of internet users globally reached six billion in 2025, up from 5.6 billion in the previous year, underscoring the rapid growth of digital access that supports online purchasing behavior [1]Source: International Telecommunication Union (ITU), "Individuals using the Internet ", itu.int. Additionally, the adoption of digital payment solutions, personalized recommendations, subscription-based purchasing models, and direct-to-consumer platforms has increased shopping convenience and strengthened consumer engagement.

Consumer preference for health and wellness products

Consumer preference for health and wellness products is a significant driver of the consumer packaged goods market. Individuals are increasingly prioritizing products that promote healthier lifestyles, enhanced well-being, and preventive care. Rising awareness about ingredient quality, product safety, and long-term wellness benefits has led consumers to favor products with natural ingredients, clean-label formulations, functional benefits, and improved nutritional profiles. This trend is prompting manufacturers to emphasize product innovation, reformulation, and transparency by reducing artificial ingredients and introducing offerings that align with changing consumer expectations. Additionally, the demand for products with added functionality, sustainability, and personalized benefits is accelerating the development of advanced formulations within the consumer goods industry.

Product innovation and premiumization trends

Product innovation and premiumization trends are driving growth in the consumer packaged goods market as consumers increasingly demand high-quality, advanced, and differentiated products that offer enhanced performance, convenience, and experiences. Investments in research, advanced formulations, and new product development have enabled manufacturers to introduce innovative solutions that cater to evolving consumer preferences for functionality, personalization, and quality. Premiumization is further influencing the market, with brands emphasizing superior ingredients, improved designs, sustainable solutions, and value-added features to enhance consumer engagement and product differentiation. For example, in March 2026, Nestlé S.A. launched Compleat Paediatric Oral Blends, an oral nutritional supplement for children with special medical nutrition needs. Packaged in an on-the-go pouch format, this product demonstrates how companies are integrating innovation, convenience, and specialized solutions to address changing consumer demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply chain disruptions and operational challenges | -0.8% | Global; most acute in North America and import-dependent Asia-Pacific supply chains | Short term (≤ 2 years) |

| Fluctuating raw material availability and sourcing challenges | -0.6% | Global; concentrated in markets reliant on single-country sourcing for tariff-sensitive inputs | Medium term (2-4 years) |

| Intensifying private label competition and retailer consolidation | -0.5% | Global; concentrated in EU-11 and North America, expanding into Asia-Pacific organized retail | Medium term (2-4 years) |

| Consumer price sensitivity and structural downtrading pressures | -0.4% | Global; most acute in North America, EU, and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply chain disruptions and operational challenges

Supply chain disruptions and operational challenges significantly constrain the consumer packaged goods market by impacting production efficiency, product availability, and overall business continuity. The industry relies on intricate supply networks encompassing raw material sourcing, manufacturing, packaging, transportation, and distribution, making it susceptible to delays and interruptions at various stages. Issues such as logistics constraints, shortages of essential materials, transportation bottlenecks, and inventory management challenges can result in production delays, reduced product availability, and difficulties in meeting consumer demand. Furthermore, ensuring consistent product quality and timely delivery across multiple retail channels requires effective coordination, which becomes increasingly difficult during periods of supply chain uncertainty. Operational challenges, including limited supplier flexibility, production capacity constraints, and difficulties in responding to sudden demand fluctuations, further hinder market performance.

Fluctuating raw material availability and sourcing challenges

Fluctuating raw material availability and sourcing challenges significantly restrain the consumer packaged goods market. Variations in the supply of essential ingredients, packaging materials, and production inputs can disrupt manufacturing operations and impact product consistency. The industry depends on a diverse range of agricultural commodities, natural resources, and specialized materials, making it vulnerable to supply shortages, climate-related disruptions, changing production conditions, and procurement uncertainties. According to the World Bank, agricultural prices increased by 2.5% in May 2026, with food prices rising by 1.9% and beverage prices by 5.3% [2]Source: World Bank, "Energy prices eased in May", worldbank.org. These fluctuations highlight ongoing challenges in key input categories used in consumer goods production, complicating manufacturers' efforts to maintain stable sourcing strategies, production planning, and supply reliability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food and Beverages Anchor Volume as Personal Care Accelerates

In 2025, Food and Beverages commanded a leading 42.55% share of the consumer packaged goods market. This dominance stemmed from a consistent demand for packaged products that prioritize convenience and quality, aligning with evolving consumer preferences. As consumers increasingly sought products that are easy to store, ready-to-use, and boast a longer shelf life, the appeal of packaged goods surged. Moreover, advancements in processing, preservation, and packaging technologies not only bolstered product availability but also fostered consumer trust. A heightened interest in healthier formulations, ingredient transparency, and diverse product varieties has spurred manufacturers to broaden their portfolios and enhance product differentiation. Eurostat reported that in 2024, the European Union saw its food and beverage service industry enterprises swell to 1.58 million, marking a 60,000 increase from 2021 and underscoring the industry's expansion and rising demand.

Personal Care and Cosmetics emerged as the quickest-growing segment in the consumer packaged goods arena, boasting a 5.35% CAGR from 2026 to 2031. This surge is attributed to a heightened consumer emphasis on grooming, self-care, and wellness. As awareness around hygiene, skincare, and preventive care rises, so does the demand for innovative, high-quality products that cater to these evolving needs. Manufacturers, in response to a growing preference for natural ingredients, clean-labels, sustainability, and ethical sourcing, are channeling investments into advanced formulations and product innovation. Furthermore, the digital age, marked by social media's sway, online interactions, and tailored recommendations, has revolutionized purchasing behaviors, enhancing both product discovery and consumer engagement.

By Packaging Type: Bottles Lead but Flexible Formats Redefine the Market's Growth Edge

In 2025, bottles commanded a 36.81% share of the consumer packaged goods market, solidifying their status as the leading packaging type. Their dominance stems from attributes like durability, convenience, and the ability to maintain product quality during storage and distribution. Bottles are favored across diverse products due to benefits like enhanced protection, extended shelf life, ease of handling, resealability, and user-friendliness. Ongoing innovations in bottle design, lightweight materials, and novel closures have not only boosted functionality but also elevated consumer experience and brand distinction. With an increasing emphasis on sustainable packaging, there's been a surge in the development of recyclable, reusable, and eco-friendly bottle solutions. This shift enables manufacturers to tackle environmental challenges without compromising on performance and safety standards.

Pouches are emerging as the fastest-growing packaging format in the consumer packaged goods arena, boasting a 4.56% CAGR from 2026 to 2031. This growth is fueled by a rising appetite for lightweight, flexible, and user-friendly packaging. Pouches offer distinct advantages over traditional rigid formats, including portability, efficient storage, reduced material consumption, and superior handling. As consumers increasingly gravitate towards resealable, single-serve, and convenient on-the-go options, pouch adoption has surged. Innovations in packaging technology, such as better barrier protection, heightened durability, and advanced closure systems, have been pivotal in preserving product freshness and extending shelf life, bolstering market demand. Furthermore, a heightened focus on sustainability is driving a transition to recyclable, biodegradable, and low-waste pouch materials, as manufacturers pursue eco-friendly packaging solutions.

By Distribution Channel: Supermarkets Retain Primacy While Online Retail Commands Growth

Supermarkets and hypermarkets accounted for a 45.69% share of the distribution channel in 2025, maintaining their leading position in the consumer packaged goods market. This dominance is attributed to their ability to offer wide product availability, convenience, and a comprehensive shopping experience. Their growth is supported by strong consumer preference for organized retail formats that provide extensive product choices, competitive pricing, promotional offers, and the convenience of comparing multiple brands in one location. Features such as well-managed shelf spaces, attractive product displays, and enhanced in-store experiences continue to influence purchasing decisions and strengthen consumer engagement. Additionally, advancements in inventory management systems, supply chain efficiency, and digital integration have improved product availability and operational performance, contributing to higher sales volumes.

Online retail stores represent the fastest-growing distribution channel in the consumer packaged goods market, with a 6.13% CAGR projected for the period 2026–2031. This growth is driven by increasing consumer preference for convenient, flexible, and technology-enabled shopping experiences. The ability to access a wide range of products, compare options, read reviews, and receive doorstep delivery has significantly boosted the adoption of digital purchasing platforms. Innovations in mobile commerce, secure digital payment systems, artificial intelligence-based recommendations, and personalized shopping experiences have enhanced customer engagement and streamlined the purchasing process. Furthermore, the expansion of direct-to-consumer models, subscription-based services, and faster delivery solutions has reinforced the role of online platforms in improving product accessibility and fostering consumer retention.

By End-User: Household Consumers Drive Volume as Commercial Users Emerge as the Next Growth Engine

Household consumers accounted for a 71.23% share of end-user demand in 2025, maintaining their leading position in the consumer packaged goods market. This dominance is attributed to the consistent and frequent consumption of daily-use products. Growth in this segment is driven by an increasing preference for convenient, reliable, and easily accessible packaged solutions that align with modern lifestyles and evolving purchasing habits. The rising demand for products offering enhanced quality, safety, hygiene, and extended usability has further reinforced consumer reliance on packaged goods. Additionally, the growing emphasis on wellness, sustainability, product transparency, and improved user experiences has encouraged the adoption of innovative and differentiated offerings. Advancements in packaging convenience, digital purchasing platforms, personalized product options, and expanded availability through diverse retail networks continue to strengthen consumer engagement and support the strong market position of household consumers.

Commercial users represent the fastest-growing end-user segment in the consumer packaged goods market, with a projected CAGR of 4.81% during 2026–2031. This growth is driven by increasing demand for efficient, standardized, and high-quality packaged solutions across professional and business environments. The segment's expansion is supported by the need for reliable product supply, consistent quality, and convenient purchasing options that enhance operational efficiency. The adoption of bulk purchasing models, digital procurement platforms, and customized product solutions has improved accessibility and streamlined purchasing processes. Furthermore, advancements in supply chain management, product innovation, sustainable solutions, and service-oriented offerings are fostering wider adoption among commercial users, positioning this segment for steady growth throughout the forecast period.

Geography Analysis

Asia-Pacific accounted for a 32.32% share of the consumer packaged goods market in 2025 and is expected to achieve the fastest growth with a 5.91% CAGR during 2026–2031. This growth is driven by the rapid expansion of organized retail networks, increased adoption of digital shopping platforms, and shifting consumer preferences toward convenient, branded, and quality-focused products. Additional factors supporting the region's growth include strong demand for innovative product formats, enhanced packaging solutions, and rising awareness of health, wellness, and sustainability. Expanding manufacturing capabilities, advancements in supply chains, and the growing availability of diverse product choices further reinforce Asia-Pacific's leading position in the market.

North America remains a strategically significant region in the consumer packaged goods market, supported by robust retail infrastructure, advanced supply chain systems, and high adoption of innovation-driven consumer products. The market is fueled by increasing demand for premium, personalized, sustainable, and digitally accessible packaged goods. The integration of technology, including data analytics, automation, and omnichannel retail solutions, has enhanced consumer engagement and product availability. Europe is gaining traction in the consumer packaged goods market due to a growing preference for sustainable solutions, strict quality standards, and a well-established consumer goods ecosystem. For example, according to the National Federation of Italian Pharmacy Owners (Federfarma), there were over 20,195 pharmacies operating in Italy in 2024, highlighting a strong retail and distribution network that ensures wider accessibility of consumer packaged goods [3]Source: National Federation of Italian Pharmacy Owners (Federfarma), "Number of pharmacies in Italy ", federfarma.it.

South America and the Middle East and Africa are emerging as growth regions in the consumer packaged goods market, driven by retail modernization, increased availability of branded products, and improvements in distribution infrastructure. Growing consumer awareness of product quality, convenience, and sustainable packaging solutions is prompting manufacturers and retailers to expand their presence in these regions. The rise of digital commerce platforms, advancements in logistics capabilities, and the adoption of innovative product offerings are expected to create long-term growth opportunities for the consumer packaged goods market in South America and the Middle East and Africa.

Competitive Landscape

The consumer packaged goods market operates in a moderately consolidated competitive environment globally, led by multi-category companies such as Procter & Gamble Company, Unilever PLC, Nestlé S.A., The Coca-Cola Company, and PepsiCo, Inc. These companies maintain their market positions through diverse product portfolios, strong brand equity, extensive distribution networks, and consistent investments in innovation. Market participants are focusing on expanding their portfolios, reformulating products, offering premium options, and adopting consumer-centric strategies to enhance engagement and adapt to shifting preferences. Strategic partnerships, acquisitions, and the expansion of digital capabilities are key approaches employed by leading players to broaden market reach and sustain long-term competitiveness.

Technology-enabled differentiation is emerging as a critical competitive factor in the consumer packaged goods market. Companies are increasingly integrating advanced analytics, artificial intelligence, automation, and digital platforms into their operations. By leveraging data-driven insights, manufacturers are improving product development, personalizing consumer experiences, optimizing supply chains, and enhancing demand forecasting. Digital transformation across e-commerce channels, smart packaging, connected consumer experiences, and targeted marketing strategies is enabling companies to strengthen customer relationships while improving operational efficiency. Furthermore, investments in research and development are facilitating faster innovation cycles, allowing brands to respond more effectively to evolving consumer expectations.

White-space opportunities in the consumer packaged goods market are concentrated in areas such as functional nutrition, science-backed personal care, and sustainable packaging formats. Consumers are increasingly seeking products that combine performance, transparency, and environmental responsibility. Companies are addressing this demand by expanding into value-added offerings focused on wellness, clean ingredients, personalized solutions, and eco-conscious designs. The shift toward recyclable materials, reduced packaging waste, and responsible sourcing is creating avenues for differentiation. Additionally, advancements in formulation science and product technologies are enabling brands to develop innovative solutions. These evolving priorities are expected to intensify competition and influence future growth strategies within the consumer packaged goods industry.

Consumer Packaged Goods Industry Leaders

-

Procter and Gamble Company

-

Unilever PLC

-

Nestlé S.A.

-

The Coca-Cola Company

-

PepsiCo, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Wildflower Naturals has launched on Blinkit, enhancing its presence in the quick commerce market. This initiative aligns with the brand’s omnichannel growth strategy, aiming to improve accessibility to its skincare and wellness products for consumers across India.

- February 2026: PepsiCo introduced a ready-to-heat range of vegetable soups under its Alvalle brand. Produced in Murcia, Spain, these soups are made using 100% Spanish-sourced natural ingredients, including vegetables, olive oil, and salt, without any additives or gluten.

- January 2026: Ghodawat Consumer Limited introduced soya chunks under the STAR brand. These are produced using advanced extrusion technology, which transforms defatted soy flour into textured vegetable protein through high temperature and pressure.

Global Consumer Packaged Goods Market Report Scope

Consumer Packaged Goods (CPG) are everyday items that consumers buy frequently, consume rapidly, and regularly replace. The consumer packaged goods market is segmented by product type, packaging type, distribution channel, end-user, and geography. Based on product type, the market is segmented into food and beverages, personal care and cosmetics, household care products, dietary supplements, and others. Based on packaging type, the market is segmented into bottles, pouches, cans, boxes, and other packaging types. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, convenience and grocery stores, specialty stores, online retail stores, and other distribution channels. Based on end-user, the market is segmented into household consumers, commercial users, institutional buyers, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Food and Beverages |

| Personal care and cosmetics |

| Household Care Products |

| Dietary supplements |

| Others |

| Bottles |

| Pouches |

| Cans |

| Boxes |

| Other Packaging Types |

| Supermarkets/Hypermarkets |

| Convenience and Grocery Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| Household Consumers |

| Commercial Users |

| Institutional Buyers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Food and Beverages | |

| Personal care and cosmetics | ||

| Household Care Products | ||

| Dietary supplements | ||

| Others | ||

| By Packaging Type | Bottles | |

| Pouches | ||

| Cans | ||

| Boxes | ||

| Other Packaging Types | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience and Grocery Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By End-User | Household Consumers | |

| Commercial Users | ||

| Institutional Buyers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and forecast for consumer packaged goods?

The consumer packaged goods market size is projected at USD 10.63 trillion in 2025, USD 11.08 trillion in 2026, and USD 13.6 trillion by 2031, growing at a 4.2% CAGR.

Which product category leads packaged goods demand?

Food and Beverages led with 42.55% share in 2025, supported by frequent household replenishment and broad use across income groups.

Which segment is growing fastest across packaged goods categories?

Personal Care and Cosmetics is projected to grow the fastest among product types at a 5.35% CAGR through 2031.

Which sales channel is gaining the most momentum?

Online Retail Stores is expected to expand at a 6.13% CAGR through 2031 as digital discovery, social commerce, and quick delivery models gain ground.

Page last updated on: