Global Adhesive Bandages Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

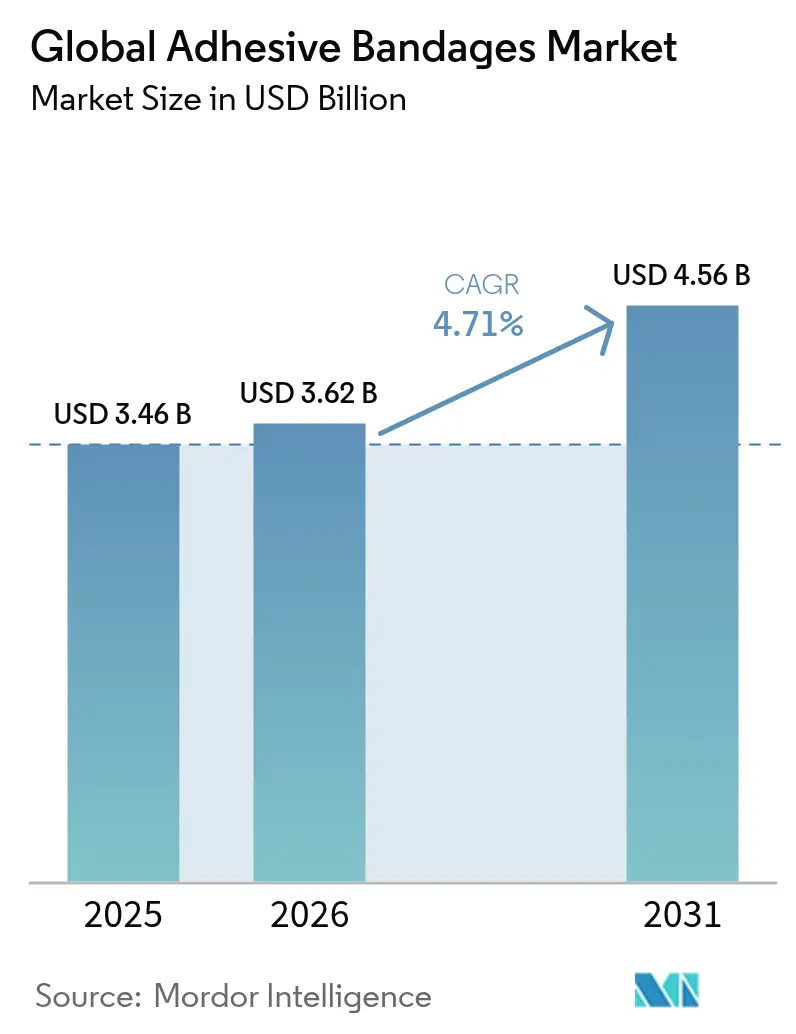

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 4.56 Billion |

| Growth Rate (2026 - 2031) | 4.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Adhesive Bandages Market Analysis by Mordor Intelligence

The adhesive bandages market size is expected to grow from USD 3.46 billion in 2025 to USD 3.62 billion in 2026 and is forecast to reach USD 4.56 billion by 2031 at 4.71% CAGR over 2026-2031. Demand holds steady as healthcare systems confront the rising costs of chronic wound care, which drain Medicare of USD 28.1 billion–USD 31.7 billion each year. Medicated formats sustain current volume leadership, while digital health convergence spurs adoption of sensor-enabled dressings that record temperature, pH, and moisture. Parallel advances in breathable, waterproof, and biodegradable materials keep non-medicated lines competitively relevant, reflecting policy moves that mandate greener packaging and reduced volatile organic compounds. E-commerce platforms reshuffle go-to-market models, driving rapid uptake of home-care-oriented micro-packs, and North America preserves its lead because of robust reimbursement and regulatory clarity that accelerates smart-bandage approvals. Competitive pressure intensifies as smart-bandage innovators claim they can trim hospital therapy costs by 41% and reduce application time 61% relative to standard dressings.

Key Report Takeaways

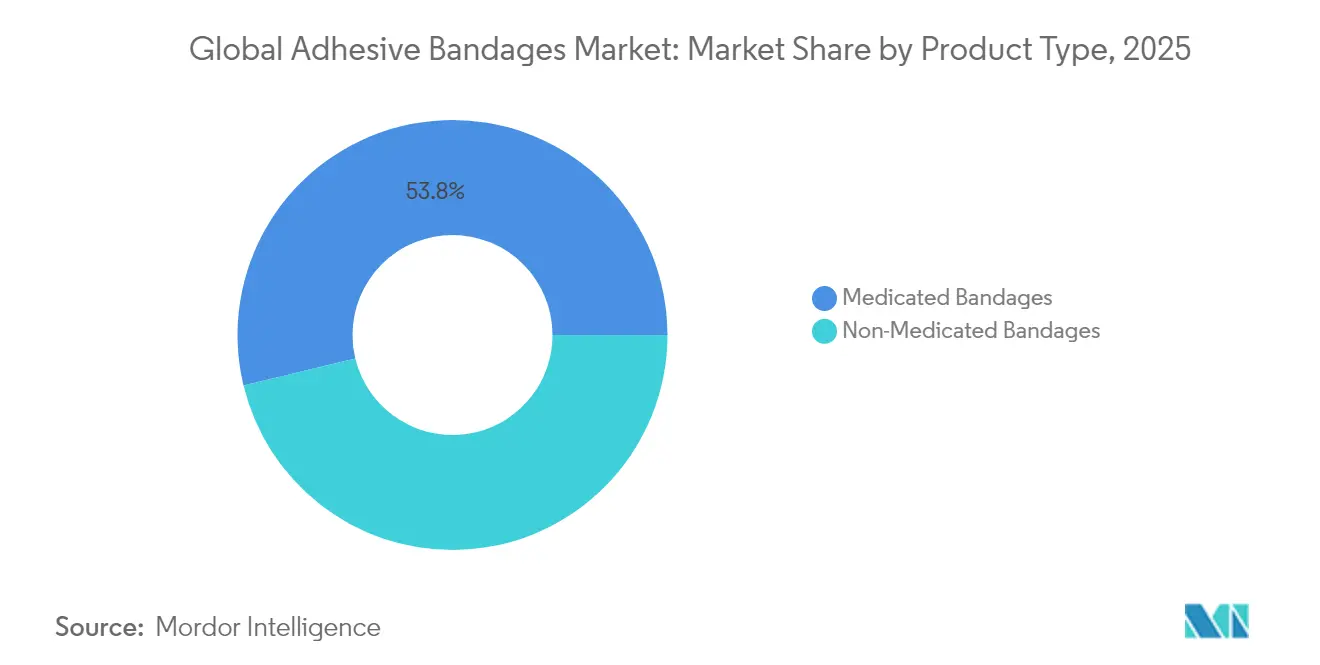

- By product type, medicated bandages held 53.78% of adhesive bandages market share in 2025, whereas non-medicated variants post the fastest 5.49% CAGR through 2031.

- By application, wound management captured 46.68% revenue in 2025, while first-aid and home care outpace the field at a 5.67% CAGR to 2031.

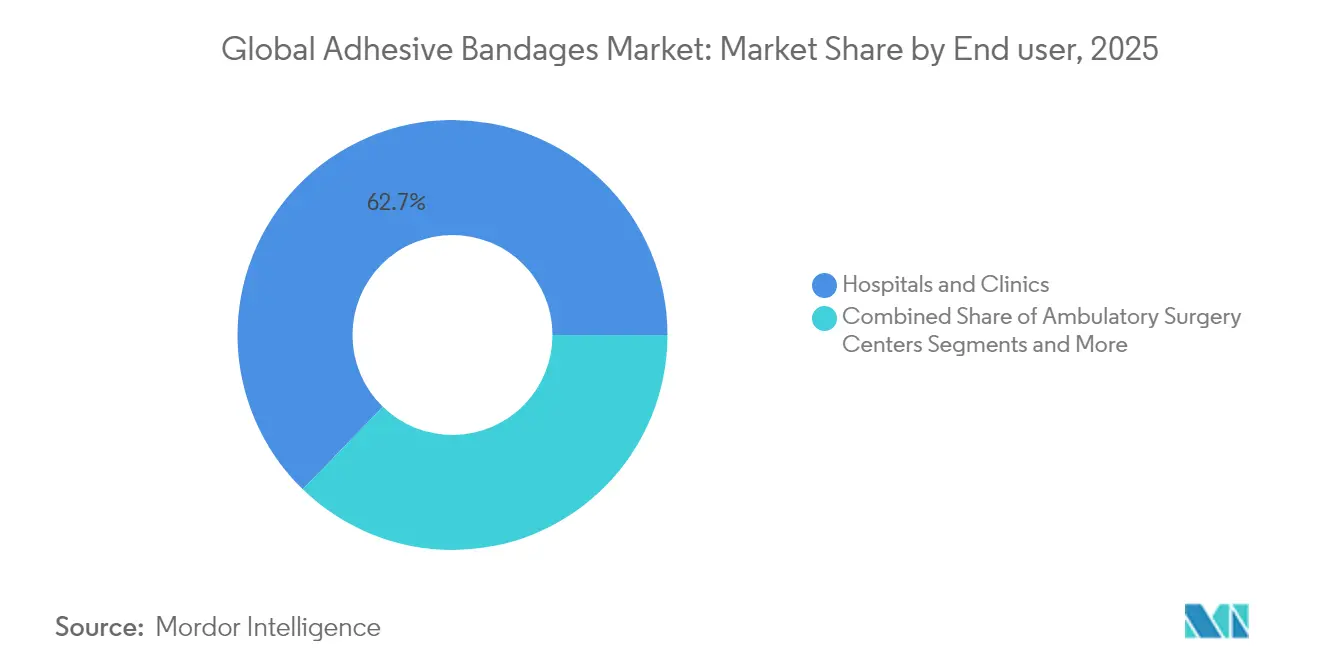

- By end user, hospitals and clinics accounted for 62.74% share of the adhesive bandages market size in 2025, yet home healthcare is set to expand 6.98% CAGR between 2026–2031.

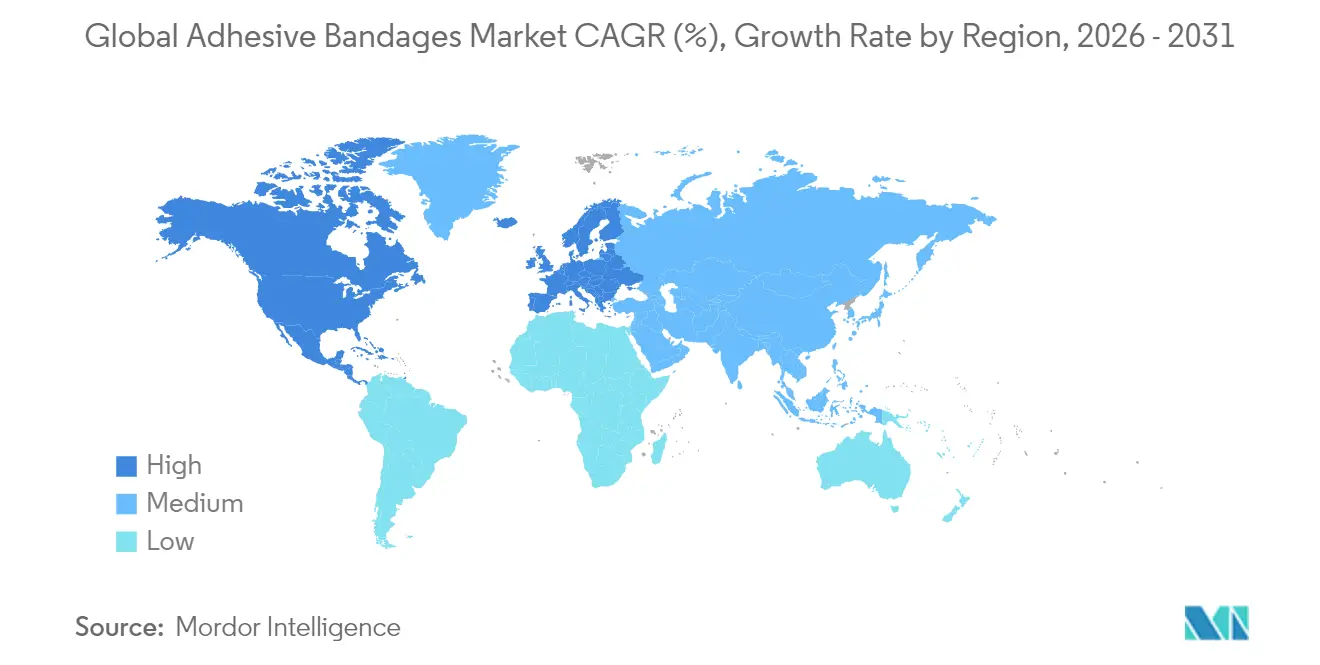

- By region, North America led with 42.33% revenue share in 2025; Asia-Pacific registers the fastest 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adhesive Bandages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Surgical Procedures & Trauma-Related Injuries | +1.2% | Global, with North America & Europe leading | Medium term (2-4 years) |

| Rising Incidence Of Chronic Wounds & Diabetic Ulcers | +1.8% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Increasing Sports Injuries & Active Lifestyle Demand | +0.7% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Technological Advances In Breathable & Waterproof Materials | +0.9% | Global, led by developed markets | Medium term (2-4 years) |

| Surge In Home First-Aid & E-Commerce Micro-Packs | +1.1% | Global, accelerated in Asia-Pacific | Short term (≤ 2 years) |

| Emergence Of Smart Sensor-Enabled Bandages | +0.6% | North America, Europe early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Surgical Procedures & Trauma-Related Injuries

Expanding surgical volumes boost the adhesive bandages market as outpatient and ambulatory centers rely on extended-wear dressings that preserve sterile barriers and enable early discharge. National Collegiate Athletic Association surveillance shows lower-extremity trauma represents more than 50% of collegiate injuries, underscoring sustained demand for precision athletic strips [1]National Center for Biotechnology Information, “Epidemiology of Collegiate Sports Injuries,” ncbi.nlm.nih.gov. Minimally invasive techniques favor thin, highly conformable films that manage exudate without secondary fixation. Incorporating silver nanoparticles within substrate layers supports surgical-site infection prevention goals, an increasingly critical quality metric for payers.

Rising Incidence of Chronic Wounds & Diabetic Ulcers

In the United States, 6.7 million individuals face chronic wounds each year, with direct treatment costs topping USD 50 billion. Diabetic foot ulcers alone trigger USD 6.2 billion–USD 6.9 billion in annual Medicare spending. Smart dressings such as Caltech’s iCares platform analyze nitric oxide and hydrogen peroxide biomarkers in real time and predict healing trajectories via machine-learning algorithms. Hydrocolloid matrices retain dominance in chronic settings despite raw-material supply squeezes, while hydrogel constructs with self-healing clay nanosheets promise up to 90% structural recovery within 4 hours.

Increasing Sports Injuries & Active Lifestyle Demand

Global participation in organized athletics stimulates specialty wraps that flex under stress, expel moisture, and cling through sweat. Bandage contact lenses for corneal abrasions permit direct return to play without depth-perception loss. Retail shelves now feature cohesive fabrics and elastic cloth strips aligned to dynamic movement, widening the consumer base beyond professional teams.

Surge in Home First-Aid & E-Commerce Micro-Packs

Telehealth growth and direct-to-consumer logistics lift at-home care. Digital storefronts accounted for USD 309.62 billion medical supply purchases in 2022 and may reach USD 732.3 billion by 2027. Medicare’s 2025 caregiver-training codes (G0541-G0543) reimburse structured wound-care coaching, prompting broader use of self-service dressing kits.

Emergence of Smart Sensor-Enabled Bandages

Wireless dressings with pH, temperature, and impedance sensors provide continuous data flow to clinicians, cutting unnecessary clinic visits. Caltech’s prototype demonstrated expert-level healing forecasts while delivering on-demand electrical stimulation. Spiral stainless-steel electrode designs accelerate closure rates and support machine-learning decision tools that refine treatment intervals. Regulatory approval, mass-manufacturing economics, and price parity versus legacy dressings remain critical adoption hurdles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin irritation & allergic reaction risk | -0.8% | Higher in developed markets | Short term (≤ 2 years) |

| Competition from advanced wound-closure devices | -1.1% | North America & Europe | Medium term (2-4 years) |

| Sustainability rules driving bio-material costs | -0.6% | Europe & North America | Long term (≥ 4 years) |

| Raw-material supply volatility | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skin Irritation & Allergic Reactions to Latex/PU

Dermatitis concerns narrow product acceptance among increasingly informed consumers. A class-action suit filed in 2024 claims certain Band-Aid lines contain per- and polyfluoroalkyl substances, raising health-equity issues for products marketed to people of color. Latex allergies affect up to 6% of the general population, pushing producers toward hypoallergenic silicone and polyurethane blends, but trade-offs emerge around breathability and cost.

Competition From Advanced Wound-Closure Solutions

Cyanoacrylate tissue adhesives exhibit comparable tensile strength to sutures and eliminate post-operative dressing changes, eroding share in surgical channels. The United States FDA issued guidance that clarifies approval routes for tissue adhesives combined with adjunct devices, accelerating market entry for alternatives that bypass traditional dressings [2]U.S. Food and Drug Administration, “Tissue Adhesive Guidance for Industry,” fda.gov. Solventum’s V.A.C. Peel and Place disposable kit demonstrated a 61% reduction in application time and 41% cost savings, illustrating the economic argument that challenges legacy adhesive strips.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Medicated Solutions Extend Clinical Edge

Medicated variants controlled 53.78% of adhesive bandages market size in 2025 courtesy of embedded antimicrobials that answer hospital-acquired infection mandates. Silver nanoparticle and PHMB matrices log 98.5% bacterial elimination against Staphylococcus aureus, reinforcing clinical trust. Low-trauma silicone coatings protect geriatric and pediatric skin, while cohesive fabrics suit high-motion athletic injuries. As reimbursement trends reward infection-prevention proof points, producers escalate evidence generation to defend pricing.

Non-medicated strips, although smaller in revenue today, expand at a 5.49% CAGR as sustainable PLA and solvent-free adhesives dovetail with regulatory carbon targets. Elastic cloth and waterproof PE films satisfy consumer preference for breathable and aquatic-safe dressings. Retailers promote value packs through online storefronts, widening access across emerging economies where discretionary healthcare buys gain traction. Such momentum keeps the adhesive bandages market firmly diversified across price tiers.

By Application: Wound Management Retains Leadership Amid Home-Care Expansion

Clinical wound management remains the core use, commanding 46.68% of adhesive bandages market share in 2025 as chronic ulcers, pressure injuries, and post-operative incisions demand specialty dressings. Hospitals integrate smart patches that relay moisture and temperature data, trimming manual inspection labor. Orthopedic support tapes carve a stable niche, whereas analgesic patches hint at crossover opportunities with pain-management therapeutics.

Conversely, first-aid and home-care kits log the quickest 5.67% CAGR. Pandemic-era self-sufficiency boosted demand for household dressings capable of handling minor cuts and scrapes. Sports wraps exploit the global fitness boom, and veterinary uses inch upward alongside rising pet ownership. Direct-to-consumer portals streamline stock replenishment, and curated packs for parents, hikers, and cyclists amplify segmentation depth.

By End User: Institutional Dominance Meets Decentralized Care Momentum

Hospitals and clinics held 62.74% of adhesive bandages market size in 2025 thanks to bulk procurement and evidence-backed formularies. Ambulatory surgery centers widen institutional demand by shifting procedures out of inpatient settings, reinforcing order volumes for high-performance dressings. Incumbent suppliers leverage technical service teams that guide product selection and protocol alignment.

Home healthcare races ahead at a 6.98% CAGR through 2031 as telehealth monitoring normalizes remote dressing changes. Medicare’s caregiver-training reimbursement removes a major barrier to at-home wound management, making advanced strips practical outside clinical walls. E-commerce channels facilitate one-click replenishment, and subscription models introduce reliable revenue pipelines for manufacturers able to cultivate direct consumer relationships.

Geography Analysis

North America generated 42.33% of global revenue in 2025, cementing leadership through high per-capita spend, rigorous reimbursement, and early adoption of smart sensor technologies. Chronic wounds cost the United States healthcare system more than USD 50 billion annually, driving continuous demand for premium dressings. Canada funds nationwide digital-health pilots that integrate wireless bandages into chronic-disease management, while Mexico expands manufacturing corridors that shorten regional supply chains.

Asia-Pacific produces the fastest 7.18% CAGR through 2031. China combines large-scale export capacity with rising domestic consumption as diabetes prevalence climbs. Japan’s super-aged demographic spurs uptake of atraumatic hydrogels suited for fragile skin, and India’s hospital build-out under Ayushman Bharat pushes rural penetration. Regional procurement increasingly favors CE-marked or US-FDA-cleared products, prompting multinationals to invest in localized assembly.

Europe shows stable expansion under Medical Device Regulation (EU 2017/745), which tightens clinical-evidence and traceability obligations . Sustainability incentives encourage biodegradable substrates; Beiersdorf registered 6.5% organic growth in 2024 by launching plastic-free patches under its Leukoplast line. Germany, the United Kingdom, and France anchor demand, while Eastern European markets improve access via EU structural funds.

Competitive Landscape

The adhesive bandages market is moderately fragmented. Solventum, Johnson & Johnson, and Beiersdorf hold entrenched channel relationships and complete portfolios covering commodity and premium dressings. Solventum posted high healthcare sales in 2024, flooding operating-room funnels with bundled wound-care kits.

Smith+Nephew and ConvaTec focus on advanced foams and hydrocolloids, capturing premium hospital procedures that justify higher margins. Patent filings reveal sector priorities shift toward multifunctional bandages incorporating silver, hemostatic agents, and pressure-sensing circuits.

Technology start-ups orbit academic hubs like Caltech and the University of Southern California, translating lab prototypes into pilot-scale manufacturing. Though still subscale, these disruptors influence feature roadmaps for incumbents that partner or license intellectual property to close capability gaps. Vertical integration strategies strengthen supply surety as raw-material volatility remains top-of-mind; Solventum’s internal adhesive line and Beiersdorf’s in-house cotton processing exemplify moves to lock in input quality and negotiate cost stability.

Global Adhesive Bandages Industry Leaders

B. Braun Melsungen AG

Cardinal Health, Inc

Johnson and Johnson

Smith & Nephew Pty Ltd

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Caltech began human trials of its iCares smart bandage, a microfluidic “lab on skin” platform that analyzes wound biomarkers and applies tailored electrotherapy.

- September 2024: SUGAMA released an elastic adhesive bandage engineered for medical and athletic use, featuring enhanced stretch retention and breathable backing.

- August 2024: FibroBiologics filed a United States patent on fibroblast-based adhesive bandages aimed at accelerating tissue regeneration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

At Mordor Intelligence, we define the adhesive bandages market as factory-produced, single-use strip dressings, medicated and plain, that shield minor wounds; revenues capture shipments through hospitals, retail outlets, and e-commerce platforms worldwide.

Scope Exclusion: We exclude elastic compression wraps, surgical drapes, liquid skin adhesives, and closure strips.

Segmentation Overview

- By Product Type

- Medicated Bandages

- Cohesive Fabric Bandages

- Flexible Fixation Bandages

- Hydrocolloid Adhesive Bandages

- Antimicrobial (Silver/PHMB) Bandages

- Silicone-based Low-Trauma Bandages

- Non-Medicated Bandages

- Cohesive Fabric Bandages

- Flexible Fixation Bandages

- Waterproof PE/PVC Strips

- Elastic Cloth Strips

- Biodegradable PLA Strips

- Medicated Bandages

- By Application

- Wound Management

- Acute (Surgical & Traumatic)

- Chronic (Diabetic, Pressure, Venous Ulcers)

- Orthopedic Support

- Pain Management (Analgesic patches)

- Sports & Athletic Wraps

- First-Aid & Home Care

- Veterinary Use

- Wound Management

- By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Home Healthcare

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Targeted interviews with wound-care nurses, sports trainers, pharmacy buyers, and production managers across North America, Europe, and Asia helped us validate usage rates, discount structures, and adoption curves, letting our analysts reconcile desk findings with real-world practice.

Desk Research

We pulled treated-wound incidence from WHO and US CDC dashboards, surgical counts from Eurostat, and HS 300590 trade flows from UN Comtrade to size demand. Retail scanner panels cited by the National Association of Chain Drug Stores refined average pack volumes and prices. Material-shift signals came from Questel patent analytics, industry papers of the American Wound Care Association, and company 10-Ks reviewed through D&B Hoovers and Dow Jones Factiva. This list is indicative, not comprehensive.

Market-Sizing & Forecasting

Our model begins with a top-down prevalence-to-demand build: population × injury and surgical ratios × strips per episode × blended ASP. Select bottom-up supplier roll-ups and channel checks test the totals. Key variables like aging index, e-pharmacy penetration, cotton and hydrocolloid price shifts, latex-allergy prevalence, and sustainability mandates feed a multivariate regression that projects 2025-2030 growth.

Data Validation & Update Cycle

We run variance screens against customs exports and hospital spend, followed by a two-stage analyst review. Models refresh every twelve months, with mid-cycle updates when recalls, tariffs, or mergers materially change assumptions.

Credibility Corner - Why Mordor's Adhesive Bandages Baseline Stands Apart

Published figures often diverge because some providers mix tapes, apply list prices, or extend pandemic spikes.

Our disciplined scope, yearly refresh, and blended top-down/bottom-up cross-checks minimize such skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.46 B | Mordor Intelligence | - |

| USD 0.51 B | Global Consultancy A | Excludes unit packs; applies 2019 price list unchanged |

| USD 8.35 B | Trade Journal B | Pools elastic bandages and tapes with adhesive strips |

| USD 3.79 B | Regional Consultancy C | Uses 2024 base and linear CAGR without injury normalization |

These contrasts show that Mordor's stepwise validation delivers a balanced, transparent baseline decision makers can rely on.

Key Questions Answered in the Report

What is the current Global Adhesive Bandages Market size?

The adhesive bandages market size reached USD 3.62 billion in 2026 and is projected to climb to USD 4.56 billion by 2031.

Who are the key players in Global Adhesive Bandages Market?

B. Braun Melsungen AG, Cardinal Health, Inc, Johnson and Johnson, Smith & Nephew Pty Ltd and 3M are the major companies operating in the Global Adhesive Bandages Market.

Which product type leads revenue generation

Medicated bandages dominate with 53.78% market share in 2025 thanks to built-in antimicrobial performance.

Which region has the biggest share in Global Adhesive Bandages Market?

In 2025, the North America accounts for the largest market share in Global Adhesive Bandages Market.

Page last updated on: