Medical Tapes And Bandages Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.09 Billion |

| Market Size (2031) | USD 11.12 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Tapes And Bandages Market Analysis by Mordor Intelligence

Medical Tapes And Bandages market size in 2026 is estimated at USD 9.09 billion, growing from 2025 value of USD 8.73 billion with 2031 projections showing USD 11.12 billion, growing at 4.12% CAGR over 2026-2031.

Stable growth reflects aging populations, rising surgical volumes, and wider acceptance of advanced wound management technologies. Smart sensors, biodegradable films, and controlled-release antimicrobial layers are shifting demand from passive coverings to interactive dressings that shorten healing time and cut follow-up visits. Cost pressure on hospitals and payers is prompting interest in products that enable earlier discharge and home-based self-care without compromising clinical outcomes. Sustainability mandates are also influencing material choices, guiding manufacturers toward solvent-free adhesives, compostable backings, and reduced packaging waste. The medical tapes and bandages market is therefore evolving along two axes—digital connectivity and environmental stewardship—while maintaining focus on skin-sparing adhesion and broad infection control.

Key Report Takeaways

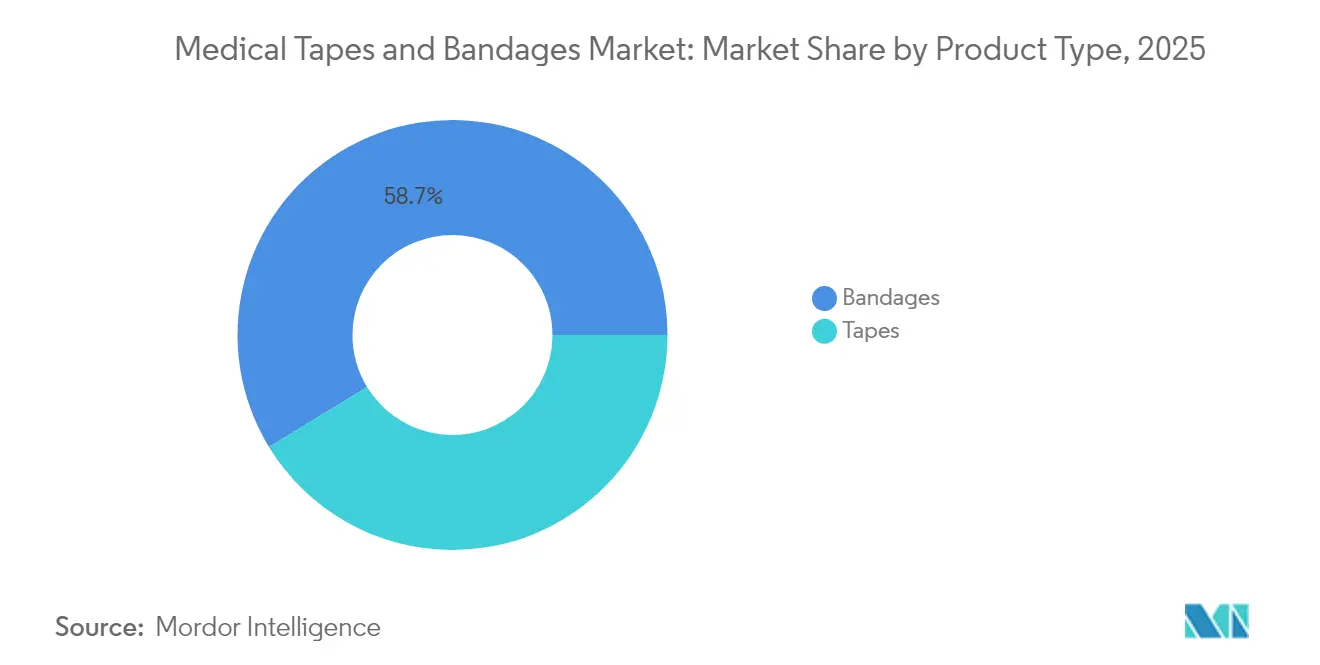

- By product type, bandages led with 58.72% of the medical tapes and bandages market share in 2025, while paper tapes are projected to expand at a 6.02% CAGR through 2031.

- By application, surgical wound care accounted for 34.22% of the medical tapes and bandages market size in 2025; ulcer treatment is set to grow fastest at 4.67% CAGR between 2026 and 2031.

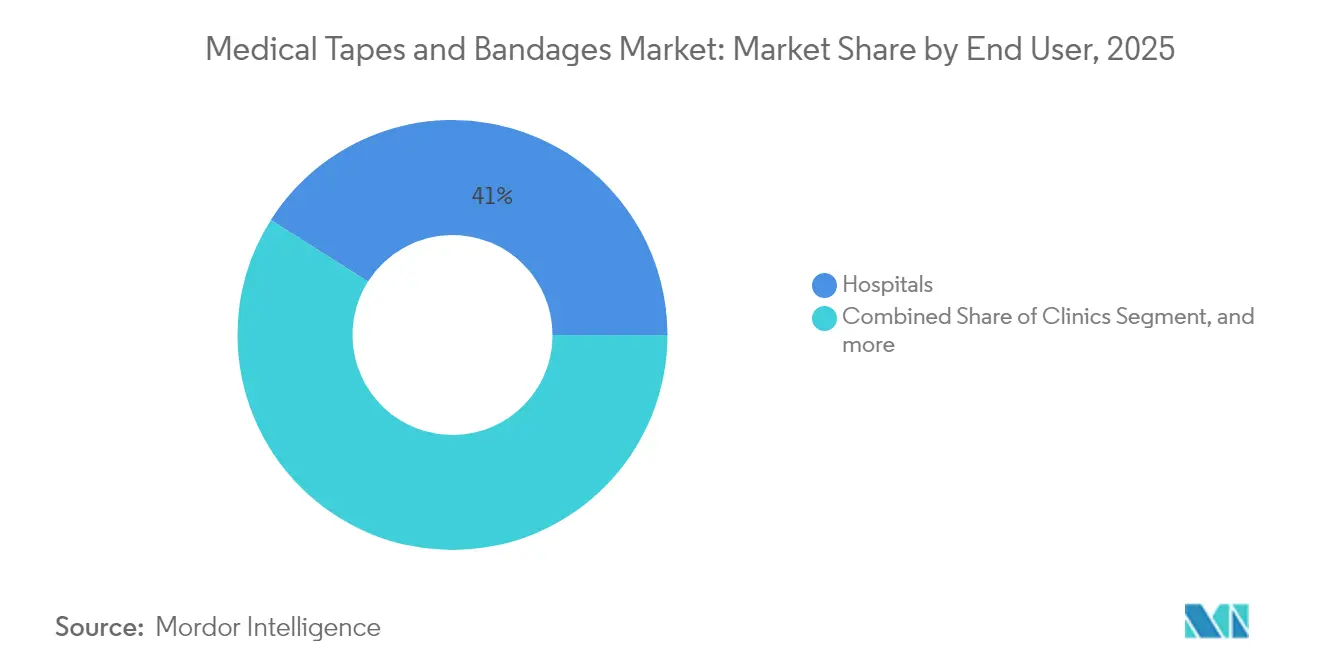

- By end user, hospitals held 41.02% revenue share of the medical tapes and bandages market in 2025, but home care settings are advancing at a 5.62% CAGR to 2031.

- By geography, North America controlled 33.05% of the medical tapes and bandages market in 2025, whereas Asia-Pacific is poised for a 4.83% CAGR, the quickest regional pace.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Medical Tapes And Bandages Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Surgical Volumes Increasing Demand for Post-Operative Wound Dressings | +0.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Growing Prevalence of Chronic Wounds, Including Diabetic Foot Ulcers and Pressure Ulcers | +1.2% | Global, particularly APAC and North America | Long term (≥ 4 years) |

| Expansion of Home-Based Wound Care Supported by Telehealth and Self-Care Kits | +0.9% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Integration of Antimicrobial Agents in Tapes and Bandages | +0.7% | Global | Medium term (2-4 years) |

| Expansion of Aging Population Worldwide | +1.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Emergence of Smart, Sensor-Embedded Tapes Enabling Remote Wound Monitoring | +0.6% | North America & Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Surgical Volumes Increasing Demand for Post-Operative Wound Dressings

Over 300 million procedures are performed worldwide each year, and aging patients increasingly undergo orthopedic, cardiovascular, and minimally invasive surgeries that require robust peri-operative dressings. Post-operative care can cost more than USD 6,000 per day for complex incisions, prompting hospitals to specify longer-wear tapes that maintain seal integrity for up to seven days to avoid excessive change frequency. Bandages with elastic compression and atraumatic removal are now preferred in ambulatory surgery centers, where same-day discharge hinges on patient comfort and the absence of skin stripping. Consequently, procurement teams place adhesion longevity and hypoallergenic performance at the top of evaluation criteria. These imperatives continue to enlarge the medical tapes and bandages market.

Growing Prevalence of Chronic Wounds, Including Diabetic Foot Ulcers and Pressure Ulcers

Roughly 6.7 million Americans live with non-healing ulcers; diabetic foot ulcers alone will affect up to 25% of diabetes patients during their lifetime.[1]M. Bolton et al., “Economic Burden of Chronic Wounds,” mdpi.com Chronic wounds generate USD 50 billion in annual treatment expenditures in the United States, driving demand for moisture-balancing bandages infused with silver or copper nanoparticles that curb biofilm formation. Clinical trials report 87.35% wound-area reduction from copper dressings versus 37.02% for conventional silver foams. Clinicians also favor layered composite tapes that modulate pH and temperature, enabling micro-environmental control and better granulation tissue development. These innovations bolster the medical tapes and bandages market by demonstrating measurable clinical payoff.

Expansion of Home-Based Wound Care Supported by Telehealth and Self-Care Kits

Telehealth reimbursement codes introduced in the 2025 Medicare Physician Fee Schedule allow caregivers to bill for remote wound-care instruction, accelerating adoption of self-service dressing kits.[2]WoundReference Clinical Team, “Telehealth Codes for Wound Care,” woundreference.com Smart-sensor tapes now transmit moisture, temperature, and strain data to cloud dashboards so clinicians can intervene before infection emerges. For patients, simplified packaging and color-changing indicators guarantee correct application without professional supervision. Retail pharmacies are stocking complete ulcer-care bundles, lifting consumer-direct sales channels. Home-care distributors thus represent a growing route-to-market, reinforcing revenue diversification inside the medical tapes and bandages market.

Integration of Antimicrobial Agents in Tapes and Bandages

Silver, copper, and chitosan additives are widely embedded into polyurethane, foam, and hydrogel matrices. Silver nanoparticles offer broad-spectrum efficacy while maintaining low cytotoxicity at controlled release rates.[3]Frontiers Editorial Office, “Silver Nanoparticles in Wound Dressings,” frontiersin.org Newer copper-oxide meshes provide continuous ionic flux, achieving rapid bacterial kill even against resistant strains. Multilayer designs stagger the release of different ions for synergistic activity, and emerging photothermal coatings activate antimicrobial potency under visible light. Regulatory expectations now call for in-vivo evidence of sustained bioburden reduction across diverse patient groups, pushing manufacturers to run multicenter trials. The performance leap widens the medical tapes and bandages market by justifying premium prices in infection-prone settings.

Restraints Impact Analysis of Medical Tapes And Bandages Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Dressings and Silicone-Based Adhesive Tapes | -0.9% | Global, particularly price-sensitive markets | Short term (≤ 2 years) |

| Clinical Concerns over Medical Adhesive-Related Skin Injury (MARSI) | -0.7% | Global, concentrated in vulnerable populations | Medium term (2-4 years) |

| Increasing Competition from Advanced Wound-Care Products | -0.5% | North America & Europe primarily | Medium term (2-4 years) |

| Environmental Sustainability Pressures on Single-Use, and Non-Biodegradable Materials | -0.4% | Europe & North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Dressings and Silicone-Based Adhesive Tapes

Smart dressings can cost 5–10 times more per unit than plain gauze. Although clinical studies reveal 58.6% weekly material-cost savings when foam dressings shorten healing time lww.com, purchasing decisions often focus on sticker price. A Spanish regional audit recorded EUR 34.99 (USD 40.16) million in primary-care wound spending across three years, with EUR 8.46 (USD 9.74) million tied to tapes and bandages sciencedirect.com. Emerging markets with limited reimbursement struggle to absorb these premiums, delaying adoption and slowing the medical tapes and bandages market in low-resource settings. Wider transition to value-based procurement may temper this restraint over the next two years.

Clinical Concerns over Medical Adhesive-Related Skin Injury (MARSI)

Incidence of medical adhesive–related skin injury reaches 11.86% in adult intensive-care units and exceeds 50% among neonates. Mechanical stripping accounts for nearly three-quarters of cases, elevating risk for elderly and immunocompromised patients. Hospitals now mandate staff training on tape selection and removal angles, adding labor time and documentation burdens. Silicone and hydrocolloid tapes mitigate trauma but remain 20–30% costlier than acrylic adhesives. Until hypoallergenic options achieve parity pricing, MARSI fears will curb broader utilization of certain product lines, limiting some high-value niches within the medical tapes and bandages market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Medical Tapes And Bandages Market Segment Analysis

By Product Type:

Versatile Bandages Anchor Demand while Paper Tapes AccelerateBandages retained 58.72% of the 2025 medical tapes and bandages market share by revenue and continue to underpin routine wound protocols for surgical sites, lacerations, and chronic ulcers. Their configuration flexibility from conformable gauze rolls to high-compression elastic wraps allows clinicians to tailor pressure, absorbency, and breathability for each wound stage. Traditional cotton gauze remains ubiquitous due to procurement familiarity, but multi-layer cohesive dressings with viscose and elastic filaments are gaining traction for exudate control in limb ulcers. Hydrogel-impregnated pads embedded within elastic bandages reduce dressing change frequency by maintaining moist environments, vital for autolytic debridement. Consequently, the medical tapes and bandages market continues to leverage bandages as the baseline product family across emergency, inpatient, and home settings.

Paper tapes, though accounting for a smaller revenue base, register the strongest 6.02% CAGR thanks to their hypoallergenic cellulose fibers and gentle, repositionable adhesives that minimize epidermal stripping. Surgeons prefer them for delicate facial incisions, pediatric IV fixation, and ophthalmic dressings where skin trauma risk is elevated. Moreover, antimicrobial-coated paper substrates now incorporate silver salts without compromising tensile strength, positioning the sub-segment as a premium offering in infection-prone wards. Fabric tapes maintain relevance where tensile support and mechanical durability trump breathability, as in orthopedics. Plastic tapes fill waterproof niche demands for shower-safe ostomy and catheter sites. Across categories, solvent-free acrylic chemistries launched by 3M in 2025 illustrate how manufacturers are blending sustainability with high adhesion, reinforcing product-line differentiation inside the medical tapes and bandages market.

By Application:

Ulcer Care Outpaces Surgical MainstaySurgical wound care delivered 34.22% of overall revenue in 2025, validating its role as the historic backbone of the medical tapes and bandages market size. Hospitals issue standardized peri-operative kits specifying elastic compression wraps, transparent IV site dressings, and microporous tapes to ensure hemostasis and early ambulation. Volume growth remains tied to rising orthopedic, cardiovascular, and bariatric surgeries among older adults. Material advances—such as silicone retention strips that peel away without disrupting staples enhance patient comfort and lower re-admission rates tied to dehisced incisions. Consequently, surgical protocols continue to consume large quantities of high-performance tapes and bandages.

Ulcer management, however, achieves the highest 4.67% CAGR because diabetic foot, venous leg, and pressure wounds are mounting alongside global obesity and longevity trends. Multilayer compression systems embedded with zinc and calamine accelerate granulation tissue, while foam-based bandages with micro-channel vapor vents minimize maceration in exuding ulcers. Smart sensors integrated into adhesive patches alert clinicians via Bluetooth when moisture levels exceed preset thresholds, preventing malodor and infection. Traumatic wounds, burns, and sports injuries each occupy smaller yet steady shares, with specialized hydrocolloid island dressings or kinesiology tapes meeting performance demands. Evidence correlating application-specific dressings with 15–20% faster closure times continues to sway payer coverage policies, broadening commercial space for the medical tapes and bandages market.

By End User:

Home Care Climbs on Telehealth MomentumHospitals commanded 41.02% of 2025 revenue, reflecting their gatekeeper status in initial wound evaluation, debridement, and product testing that influences formulary choices. Purchasing consortia negotiate multi-year contracts balancing unit price against outcome metrics such as average length of stay and infection rates. This institutional sway explains why formulary acceptance can catapult a new tape into global prominence within months, underscoring hospitals’ ongoing dominance inside the medical tapes and bandages market.

Yet home-based care represents the fastest 5.62% CAGR segment as payers embrace cost-effective recovery outside clinical walls. Remote monitoring platforms bundle sterilized dressing kits, QR-coded instructions, and live nurse chat, reducing travel costs and encouraging adherence. Clinics remain vital for chronic-wound follow-ups, while ambulatory surgical centers benefit from adhesive sheets designed for same-day discharge. Employers and sports teams increasingly purchase kinesiology and cohesive tapes directly, diversifying demand streams. The shift toward decentralized care thus reinforces multichannel distribution, compelling manufacturers to design packaging, shelf life, and educational materials fit for non-professional users, thereby enlarging long-tail revenue inside the medical tapes and bandages market.

Geography Analysis

North America Medical Tapes And Bandages Market

North America led the medical tapes and bandages market with 33.05% revenue share in 2025, fueled by advanced reimbursement mechanisms, broad clinician acceptance of composite dressings, and robust clinical-trial infrastructure that validates new materials quickly. Hospitals routinely test digital dressings that send real-time data to electronic medical records, fostering early adoption of connected tapes. Material shortages and fluctuating resin prices, however, have prompted local production initiatives to de-risk supply chains.

Europe Medical Tapes And Bandages Market

Europe remained a dependable yet slower-growing region, with public health systems mandating tender processes emphasizing eco-labels and recyclability. Regulatory frameworks such as the European Medical Device Regulation impose extensive post-market surveillance, pushing companies toward thicker clinical evidence packages. Regardless, aging demographics and high prevalence of venous leg ulcers sustain steady consumption of compression bandage systems. Manufacturers must therefore align sustainability narratives with proven healing benefits to win pan-European tenders, maintaining their share of the medical tapes and bandages market.

APAC Medical Tapes And Bandages Market

Asia-Pacific, projected to advance at a 4.83% CAGR, witnesses rapid infrastructure modernization, rising chronic-disease burden, and government incentives for domestic med-tech manufacturing. China boosts local procurement quotas, prompting joint ventures between multinational brands and provincial device makers. India’s national wound-care guidelines published in 2025 emphasize low-trauma adhesives and antimicrobial dressings for diabetic ulcers, opening volume contracts across public hospitals. Southeast Asian nations, meanwhile, adopt telehealth wound platforms to reach remote islands, expanding demand for sensor-enabled tapes capable of transmitting data over low-bandwidth networks. The convergence of policy support and manufacturing capacity places Asia-Pacific at the center of long-term expansion for the medical tapes and bandages market.

Competitive Landscape

The competitive field balances global conglomerates with focused innovators. 3M leverages diversified adhesive expertise to introduce solvent-free tapes that cut greenhouse-gas emissions by 25%, meeting hospital sustainability scorecards while preserving peel force. Johnson & Johnson combines historical brand trust with outpatient-center distribution, pushing cohesive wraps through bundled orthopedic kits. Smith & Nephew recorded 3.8% underlying growth in Advanced Wound Management during Q1 2025 on the back of ALLEVYN Ag+ SURGICAL, an antimicrobial foam dressing targeting post-operative infections.

Start-ups focus on digitization; United States-based Stasis Health markets a patch with embedded flexible electronics that tracks lactate and pH, while South Korea’s BioSensorTech commercializes colorimetric paper tapes for rapid infection screening. Mid-tier firms pursue vertical integration, acquiring non-woven fabric producers to stabilize input costs and shorten development cycles. Meanwhile, contract manufacturers in Malaysia and Mexico raise FDA-audited capacity, lowering barrier-to-entry for private-label owners.

Pricing pressure is intensifying because hospitals award multi-year contracts through competitive tenders. Manufacturers therefore bundle value-added services analytics dashboards, training modules, and waste-takeback programs to secure renewals. Intellectual-property portfolios around polymer formulations and microfluidic channels serve as protective moats, yet patent cliffs on classic acrylic chemistries open room for generic tapes. The resulting landscape is dynamic but not fragmented, characterized by a handful of firms shaping standards while digital entrants chip away at specialty niches of the medical tapes and bandages market.

Medical Tapes And Bandages Industry Leaders

3M Company

B. Braun SE

Johnson & Johnson Services, Inc.

Coloplast A/S

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Medical Tapes And Bandages Market Companies Covered in this Report

- 3M

- Johnson & Johnson

- Smiths Group

- Cardinal Health

- Coloplast

- B. Braun

- Nitto Denko

- Hartmann Group

- Henkel

- Mckesson

- BenQ Materials

- Triage Meditech Pvt. Ltd.

- Medline Industries

- Molnlycke Health Care

- Essity

- Derma Sciences

- Winner Medical Co. Ltd.

- Dynarex

- Lohmann & Rauscher

- Avery Dennison Medical

Recent Industry Developments in Medical Tapes And Bandages Market

- April 2025: Caltech researchers launched the iCares smart bandage system for human patient trials, featuring real-time wound monitoring capabilities and machine learning algorithms that predict healing outcomes with over 98% accuracy. The biocompatible polymer-based system samples wound fluid to analyze biomarkers of inflammation and infection, representing a significant advancement in personalized wound care technology.

- April 2025: Smith & Nephew reported Q1 2025 revenue of USD 1,407 million with 3.8% underlying growth in Advanced Wound Management, driven by successful launches of ALLEVYN Ag+ SURGICAL antimicrobial silver dressing and continued innovation in wound care technologies. The company emphasized its commitment to advancing wound care through product pipeline development and strategic market expansion initiatives.

- March 2025: University of Arkansas researchers developed antimicrobial surfaces using silver nanowires and low electric current technology, creating sterile surfaces that effectively eliminate bacteria like E. coli. The technology shows potential for integration into medical tapes and bandages to enhance pathogen resistance while remaining undetectable to patient touch.

- March 2025: Taipei Medical University introduced ChitHCl-DDA biodegradable tissue adhesive for knee meniscus repair, offering safer alternatives to traditional sutures with enhanced biocompatibility and controlled degradation properties. The natural polymer-based adhesive demonstrates strong tissue adhesion while supporting cell migration and collagen formation.

Medical Tapes And Bandages Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the medical tapes and bandages market as single-use, sterile or semi-sterile fabric or polymer strips and pressure-sensitive tapes that clinicians or patients apply externally to secure dressings, compress tissue, immobilize minor injuries, or shield wounds. Products tracked move through medical supply distributors, hospital tenders, and retail pharmacies.

For clarity, we intentionally exclude advanced hydrogel, foam, alginate, and sensor-enabled 'smart' dressings from the scope.

Segments Covered in This Report

- By Product Type

- Bandages

- Gauze Bandages

- Elastic / Compression Bandages

- Cohesive Bandages

- Adhesive Bandages

- Other Specialized Bandages

- Tapes

- Fabric Tapes

- Paper Tapes

- Plastic (PVC/PE) Tapes

- Silicone & Low-Trauma Tapes

- Hydrocolloid & Specialty Tapes

- Bandages

- By Application

- Surgical Wound Treatment

- Traumatic Wound Treatment

- Ulcer Treatment

- Burn Injury Treatment

- Sports Injury Treatment

- Others

- By End User

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Home Care Settings

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with wound-care nurses, hospital procurement heads, tape converters, and pharmacy buyers across North America, Europe, and Asia-Pacific. These interviews confirmed price bands, utilization rates, and the shift toward silicone low-trauma tapes, helping us align assumptions and close information gaps uncovered during desk work.

Desk Research

We gathered baseline figures from public repositories such as the WHO Global Health Observatory, CDC National Hospital Discharge Survey, European Wound Management Association dashboards, UN Comtrade shipment codes 3005 and 5906, and Questel patent alerts. Annual reports, FDA 510(k) listings, and news archived in Dow Jones Factiva enriched trend mapping, while D&B Hoovers offered revenue snapshots for private converters. This list is illustrative; many additional secondary sources informed data collection, validation, and clarification.

Market-Sizing & Forecasting

We build the model top-down, starting with surgical procedure counts, chronic wound prevalence, sports injury incidence, and population aged 65+, which are then multiplied by tape or bandage usage ratios verified through interviews. Bottom-up cross-checks, sampled supplier shipments, average selling price × volume roll-ups, and retail scanner data calibrate totals. Key variables tracked each year include hospital bed additions, polypropylene price indices, diabetic prevalence, and outpatient surgery share. Five-year forecasts use multivariate regression with ARIMA smoothing, while scenario analysis captures raw-material price shocks. When granular shipment data are missing, we triangulate with proxy countries or prior-year growth deltas.

Data Validation & Update Cycle

Our outputs are compared with trade statistics and independent wound-care revenue disclosures. Any anomaly triggers analyst re-work before sign-off. Reports refresh annually, and interim updates follow recalls, reimbursement changes, or material mergers so clients always receive the latest view.

How Mordor Intelligence's Medical Tapes And Bandages Market Size Compares to Other Published Estimates

We recognize that published estimates often diverge because firms mix advanced dressings, apply dissimilar price references, or anchor forecasts to one region's growth path. Mordor's disciplined scope, refreshed inputs, and dual-path modeling temper both optimism and conservatism.

We see key gap drivers when other studies fold in compression wraps, count veterinary demand, rely on flat average prices, or leave currency shifts unchecked.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.73 B (2025) | Mordor Intelligence | |

| USD 8.18 B (2024) | Global Consultancy A | Omits over-the-counter tapes sold through pharmacies and applies flat ASP assumption |

| USD 9.10 B (2022) | Industry Journal B | Includes compression wraps and projects a straight-line CAGR without new procedure data |

These comparisons show that our balanced, transparent build-up, grounded in procedure counts and validated utilization, offers decision-makers a reliable starting point.

Key Questions Answered in the Report

What is the current value of the medical tapes and bandages market?

The medical tapes and bandages market size stands at USD 9.09 billion in 2026 and is projected to rise to USD 11.12 billion by 2031.

Which product category dominates sales?

Bandages lead, representing 58.72% of 2025 revenue, although paper tapes record the fastest growth rate of 6.02% CAGR.

Why is ulcer care the fastest-growing application?

Diabetic foot and pressure ulcers are increasing globally, and advanced antimicrobial dressings shorten healing time, pushing ulcer treatment to a 4.67% CAGR.

How are smart sensors influencing the market?

Sensor-embedded tapes transmit temperature, moisture, and strain data, enabling remote monitoring that reduces clinic visits and supports home-based care expansion.

Which region will grow quickest through 2031?

Asia-Pacific is forecast to expand at 4.83% CAGR due to infrastructure upgrades, chronic-disease prevalence, and domestic manufacturing incentives.

What is the main restraint facing high-tech dressings?

Premium pricing limits uptake in cost-sensitive health systems, even though long-term studies show advanced materials can lower total treatment costs.

Page last updated on: