U.S. Capnography Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

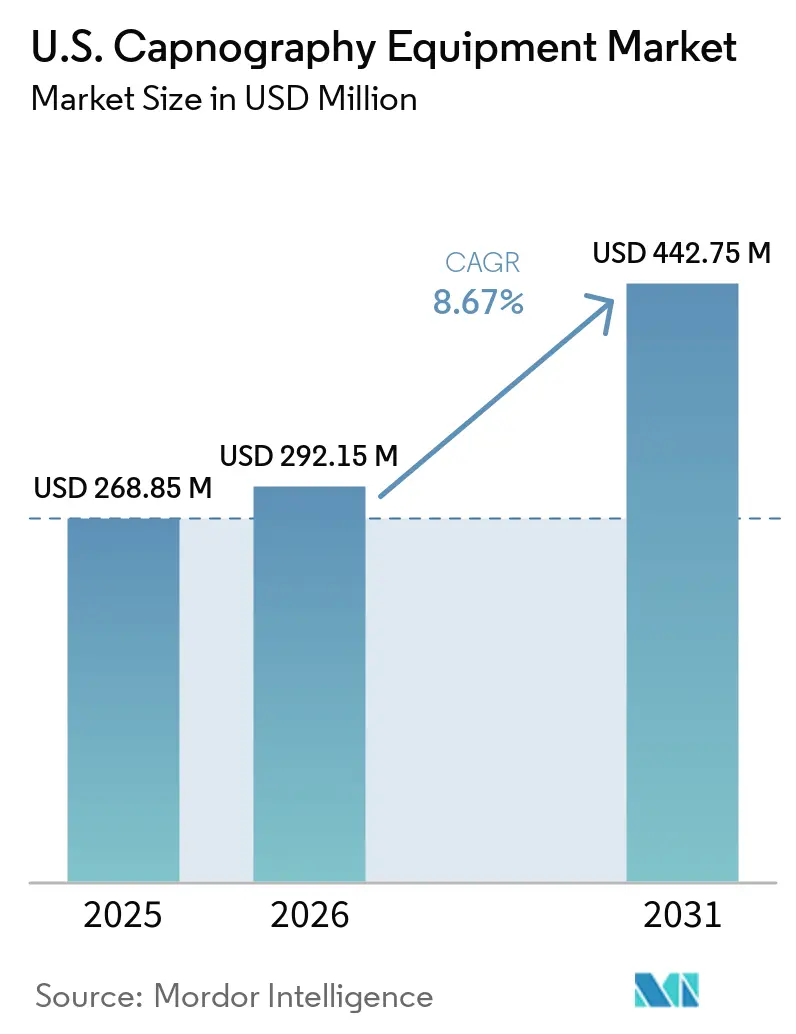

| Base Year Market Size (2025) | USD 268.85 Million |

| Market Size (2026) | USD 292.15 Million |

| Market Size (2031) | USD 442.75 Million |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Capnography Equipment Market Analysis by Mordor Intelligence

The U.S. Capnography Equipment Market size is expected to increase from USD 268.85 million in 2025 to USD 292.15 million in 2026 and reach USD 442.75 million by 2031, growing at a CAGR of 8.67% over 2026-2031.

The expansion of the United States capnography equipment market signifies a shift from its use as a specialized operating room tool to a broader patient safety standard across settings involving sedation, ventilation, or airway management. COPD remains a key driver of demand, influencing hospital care, respiratory monitoring, and long-term disease management. The care pathway is also extending from inpatient settings to ambulatory and home-based environments. Procedural sedation protocols, emergency care standards, and increased monitoring requirements in non-operating room settings are further driving the adoption of capnography equipment across the United States market. Product innovations, including portable monitors, integrated multiparameter systems, wireless connectivity, and advanced alarm management, are enhancing deployment in transport, wards, ambulatory, and home settings. However, factors such as capital budgets, recurring consumable costs, and uncertain reimbursement outside acute care continue to influence purchasing decisions, prompting vendors to focus on balancing clinical value with cost efficiency.

Key Report Takeaways

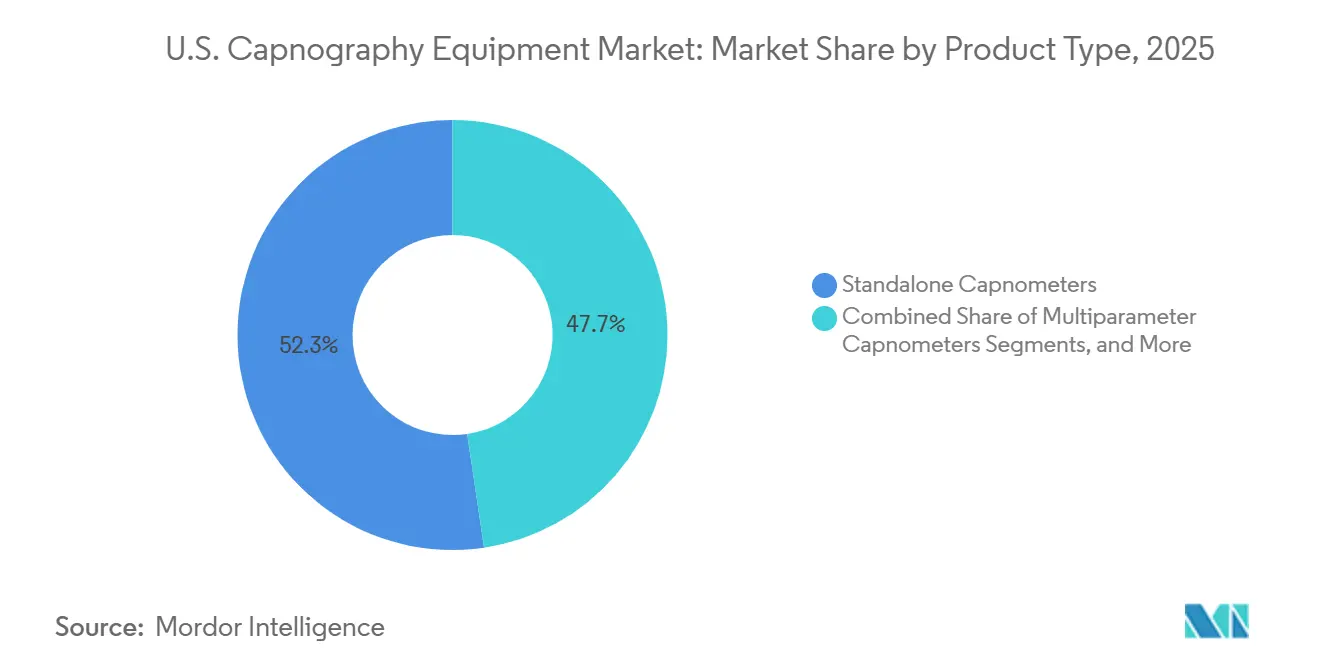

- By product type, standalone capnometers accounted for 52.35% of the US capnography equipment market size in 2025, while handheld capnography devices are forecasted to expand at a 9.65% CAGR through 2031.

- By component, equipment led with 45.65% of revenue in 2025, while consumables are projected to expand at a 9.55% CAGR through 2031.

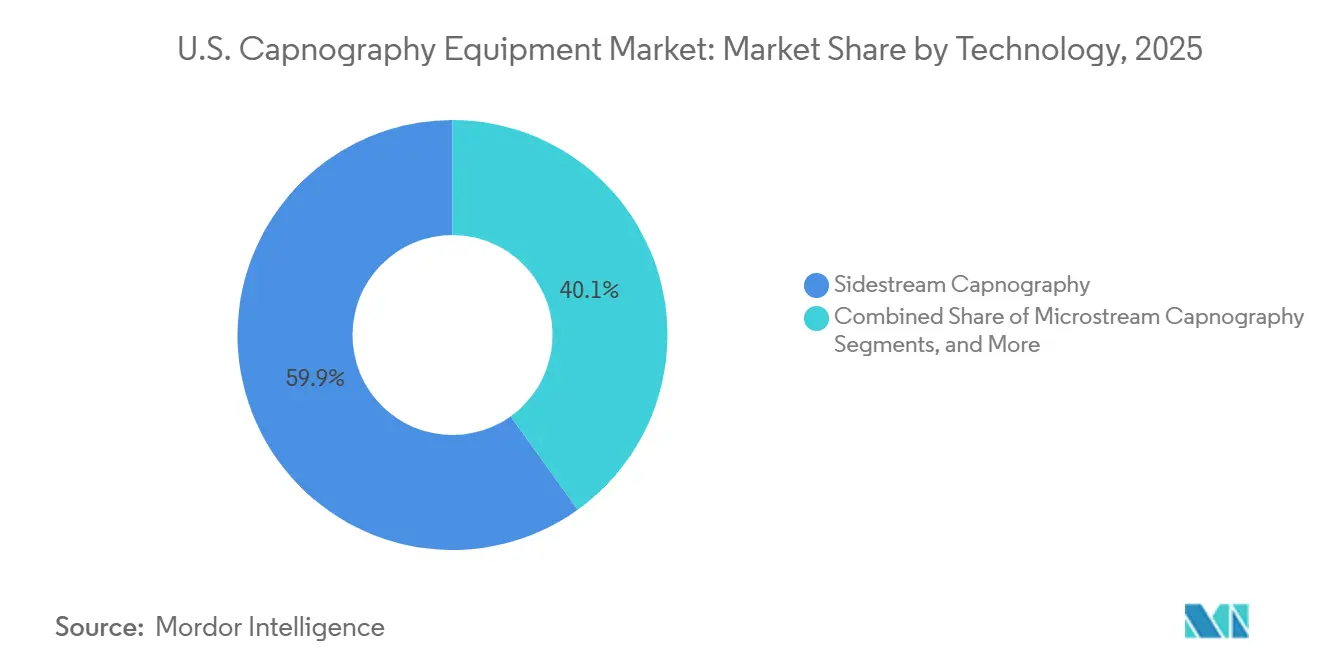

- By technology, sidestream capnography held 59.87% of the US capnography equipment market share in 2025, while microstream capnography is projected to grow at an 8.98% CAGR through 2031.

- By application, anesthesia monitoring captured 34.77% of revenue in 2025, while emergency medicine is expected to grow at a 10.25% CAGR through 2031.

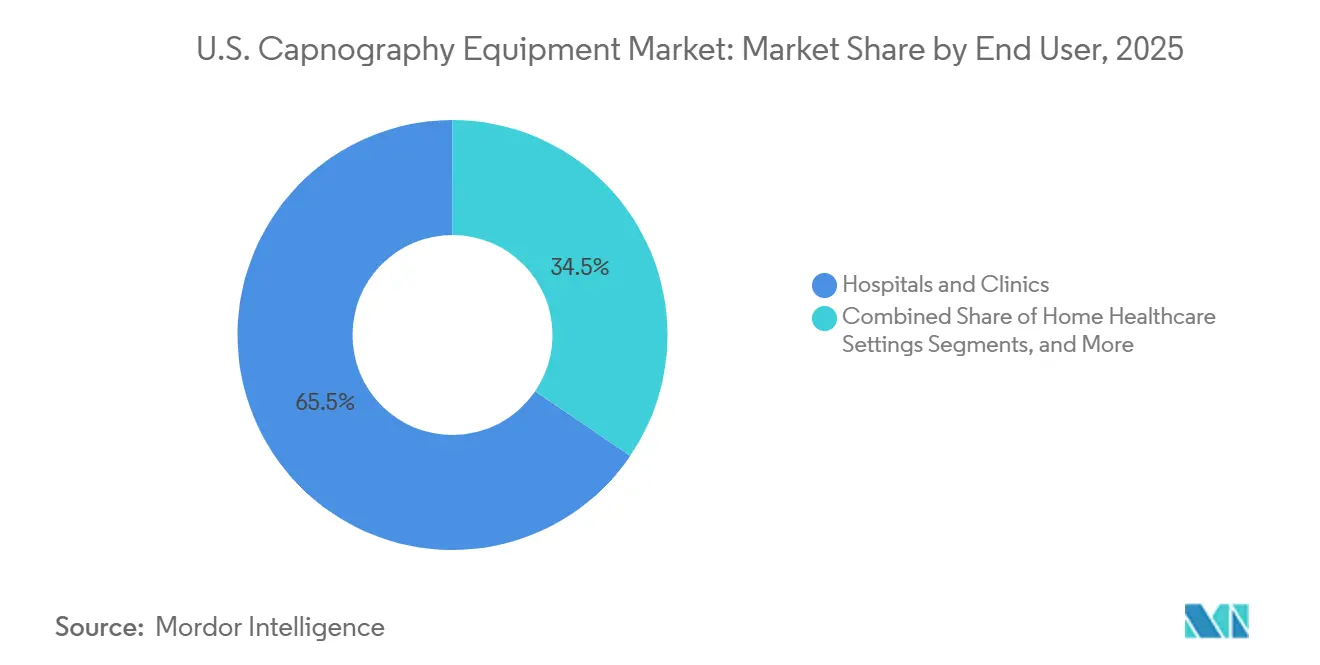

- By end user, hospitals and clinics held 65.47% of revenue in 2025, while home healthcare settings are projected to grow at a 9.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Capnography Equipment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of COPD and other chronic respiratory conditions | +2.0% | National, with highest burden in the South and Midwest | Medium term (2-4 years) |

| Higher use of capnography in anesthesia and procedural settings | +1.7% | National, with early uptake in academic medical centers | Short term (≤ 2 years) |

| Expansion of emergency and critical care monitoring protocols | +1.5% | National, driven by EMS mandates and trauma care requirements | Short term (≤ 2 years) |

| Migration toward portable and workflow-integrated monitors | +1.2% | National, especially in ambulatory surgery and home healthcare corridors | Medium term (2-4 years) |

| Greater focus on early detection of hypoventilation | +0.9% | National, with emphasis on surgical and ICU settings | Medium term (2-4 years) |

| Increasing adoption of capnography in non-operating room settings | +0.8% | National, across endoscopy, pain management, and procedural radiology suites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of COPD and Other Chronic Respiratory Conditions

The United States capnography equipment market benefits from the growing clinical burden of COPD and related respiratory disorders. In 2024, the age-adjusted COPD prevalence rate in the United States was 3.8%, with higher rates of 10.5% among adults aged 75 and older and 8.9% among those aged 65-74. Approximately 11.7 million insured individuals had a COPD diagnosis, leading to 1.8 million COPD-related acute inpatient hospitalizations. Regional disparities show higher prevalence in the South and Midwest (4.2%) compared to the West (3.1%), creating opportunities for suppliers with strong community hospital and rural system networks.[1]Centers for Disease Control and Prevention, National Center for Health Statistics, “Chronic Obstructive Pulmonary Disease in Adults Age 18 and Older: United States, 2023,” NCHS Data Brief No. 529, cdc.gov The shift toward ambulatory and home settings further supports sustained demand for capnography equipment.

Higher Use of Capnography in Anesthesia and Procedural Settings

Anesthesia monitoring remains a key driver in the United States capnography equipment market, contributing 34.77% of application revenue in 2025. While operating rooms are the primary demand center, growth is expanding into recovery workflows and procedural areas requiring moderate sedation. Standards for general anesthesia and airway confirmation reinforce the importance of end-tidal carbon dioxide monitoring. Additionally, the adoption of capnography by gastroenterologists, pulmonologists, radiologists, and emergency physicians broadens its demand, favoring vendors with multispecialty sales capabilities.

Expansion of Emergency and Critical Care Monitoring

Capnography is increasingly utilized in emergency department care, procedural sedation, prehospital airway confirmation, and cardiopulmonary resuscitation. Updated guidelines from the American Board of Emergency Medicine in 2025 emphasized continuous capnography for adult deep sedation, boosting its adoption in emergency departments and EMS systems.[2]American Board of Emergency Medicine, “Key Advances, Practice Advance, Procedural Sedation, Adult,” American Board of Emergency Medicine, abem.org EMS agencies, often purchasing through stable multi-year programs, provide a consistent demand channel as protocols standardize further.

Migration Toward Portable and Workflow-Integrated Monitors

Portability is a key trend shaping the United States capnography equipment market. In 2026, the FDA cleared Medtronic’s Capnostream 35 Portable Respiratory Monitor, designed for transport and ward use with multiparameter capabilities like EtCO₂, SpO₂, ECG, and noninvasive blood pressure. Masimo’s 2025 plans for 2026-2028 include moisture-wicking cannulas and enhanced OEM connectivity, highlighting a focus on portability and workflow integration. Purchasing decisions now prioritize monitors that fit seamlessly into transport, ward, ambulatory, and connected-care workflows, emphasizing integration and multiparameter functionality over standalone hardware.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Capital cost and recurring consumables burden | -0.8% | National, with strongest pressure in rural hospitals and smaller ambulatory surgery centers | Short term (≤ 2 years) |

| Reimbursement and billing friction in non-acute care settings | -0.7% | National, especially in endoscopy, pain management, and interventional radiology suites | Medium term (2-4 years) |

| Staff training and alarm-management requirements | -0.6% | National, with higher impact where non-anesthesiologist sedation volumes are high | Short term (≤ 2 years) |

| Device integration challenges across mixed-vendor healthcare IT environments | -0.5% | National, especially in multi-system hospital networks with mixed monitoring fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital Cost and Recurring Consumables Burden

The United States capnography equipment market faces a commercial challenge as its model relies on upfront hardware investments and recurring disposable purchases. Vendor-specific accessories like Microstream™ filter lines and NomoLine sampling sets increase the total cost of ownership beyond the initial device purchase. This creates difficulties for rural hospitals and smaller facilities, which struggle to manage fleet upgrades and ongoing consumable costs compared to larger systems. Outside the operating room, limited direct billing pathways and reliance on the unlisted 94799 code, which requires case-by-case approval, further complicate adoption. Additionally, training and alarm management add operational burdens, slowing deployment in cost-sensitive settings.

Reimbursement and Billing Friction in Non-Acute Care Settings

Reimbursement challenges limit the expansion of the United States capnography equipment market into non-acute settings. Facilities like ambulatory endoscopy centers and pain clinics recognize the clinical value but face administrative hurdles due to unlisted billing codes, complicating capital planning. Mixed-vendor IT environments further hinder seamless integration of new devices with existing systems. Buyers increasingly prefer equipment with lower consumable costs, better interoperability, and easier deployment, driving the market toward solutions focused on workflow efficiency and cost predictability alongside clinical performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Standalone Devices Dominant, Handheld Segment Reshaping Reach

Standalone capnometers accounted for 52.35% of revenue in 2025, maintaining their leadership in the United States capnography equipment market. Their dominance is driven by extensive use in operating rooms, intensive care units, and emergency departments, where waveform visibility, stable performance, and monitor compatibility are critical. Hospitals prefer these devices for their seamless integration into existing monitoring systems and minimal interoperability concerns.

Handheld capnography devices are projected to grow at a 9.65% CAGR through 2031, making them the fastest-growing segment in the United States capnography equipment market. Their growth is linked to EMS procurement, ambulatory surgery use, and the adoption of continuous respiratory monitoring in home care. As portability improves and disposable designs become more user-friendly, the focus is shifting to how quickly care protocols will adapt to these advancements.

By Component: Hardware Revenue Dominant, Consumables Compounding Fastest

Equipment contributed 45.65% of component revenue in 2025, highlighting the importance of capital device purchases in the United States capnography equipment market. Standalone and multiparameter devices dominate, forming the core monitoring footprint in hospitals and procedural settings. Software and connectivity modules are increasingly influencing purchasing decisions due to their role in integrating with broader patient monitoring systems.

Consumables are expected to grow at a 9.55% CAGR through 2031, making them the fastest-growing component category. This growth reflects the rising installed base in hospitals, emergency departments, and ambulatory sites, driving demand for nasal cannulas, sampling lines, and airway adapters. Recurring accessory demand significantly impacts margins and customer retention, complementing the role of hardware in the market.

By Technology: Sidestream Entrenched, Microstream Accelerating on Precision and Adaptability

Sidestream capnography held 59.87% of revenue in 2025, securing its leadership in the United States capnography equipment market. Its versatility with both intubated and non-intubated patients and adaptability across various clinical settings make it the preferred platform in many health systems. This broad usability ensures its continued dominance.

Microstream capnography is forecasted to grow at an 8.98% CAGR through 2031, making it the fastest-growing technology segment. Its precision, moisture handling capabilities, and ease of use for non-specialists make it ideal for diverse clinical environments. While sidestream remains dominant, microstream is rapidly gaining traction in use cases requiring higher accuracy and workflow adaptability.

By Application: Anesthesia Monitoring Anchors Revenue, Emergency Medicine Expanding Fastest

Anesthesia monitoring accounted for 34.77% of application revenue in 2025, maintaining its position as the largest application in the United States capnography equipment market. Its integral role in general anesthesia workflows and ventilatory monitoring ensures its continued demand, particularly in hospitals where quality and reliability are paramount.

Emergency medicine is projected to grow at a 10.25% CAGR through 2031, making it the fastest-growing application. The increasing use of capnography in prehospital care and moderate sedation outside traditional anesthesia settings is driving demand. Portable monitors designed for rapid deployment and rugged conditions are further supporting this growth.

By End User: Hospital Dominance Stable, Home Healthcare Emerging as Structural Growth Engine

Hospitals and clinics represented 65.47% of end-user revenue in 2025, reaffirming their role as the primary buyers in the United States capnography equipment market. Intensive care units and operating rooms drive demand, while emergency departments and medical-surgical floors contribute to refresh cycles. Established procurement cycles and infrastructure favor large-scale deployments in this segment.

Home healthcare is expected to grow at a 9.12% CAGR through 2031, emerging as the fastest-growing end-user segment. This growth is driven by unmet clinical needs and advancements in device capabilities, particularly for older COPD patients. As the market expands into home healthcare, protocol adoption and reimbursement support are becoming key challenges rather than hardware feasibility.

Geography Analysis

The United States capnography equipment market is the largest single-country demand base, supported by a robust hospital infrastructure, high patient safety standards, and diverse clinical applications requiring respiratory monitoring. The Northeast and West Coast lead in equipment density and early adoption of advanced monitoring technologies due to their concentration of academic medical centers, trauma facilities, and integrated health systems, which also influence policy and protocol development.

The South and Midwest face a higher respiratory disease burden, with COPD prevalence reaching 4.2% in 2023 compared to 3.1% in the West. States like West Virginia reported 203 COPD-related emergency department encounters per 1,000 insured patients. However, rural and critical-access hospitals in these regions often operate under tighter budgets and inconsistent reimbursement structures, leading to strong but uneven demand for capnography equipment.

Sun Belt states such as Texas, Florida, Arizona, and Georgia are emerging as growth hubs due to older populations, expanding ambulatory care, and a developed home healthcare sector. Portable monitors are gaining traction in these regions as care delivery extends beyond acute care to ambulatory, transport, and remote monitoring pathways. Home-based capnography, though nascent, aligns well with metropolitan areas equipped with remote patient monitoring infrastructure, making these states key expansion zones for the United States capnography equipment market.

Competitive Landscape

The United States capnography equipment market is moderately concentrated, with Medtronic, Masimo, Philips, and GE HealthCare holding strong positions through hospital partnerships, integrated monitoring portfolios, and proprietary consumable ecosystems. Their competitive advantage arises from a combination of installed base depth, product familiarity, OEM collaborations, and broad clinical coverage across acute care settings. Medtronic leads in Microstream-based monitoring and partnerships that extend its technology across patient monitoring platforms. Masimo has built its position with capnography and gas monitoring solutions designed for portable and integrated use cases, focusing on rapid deployment and flexibility. Philips and GE HealthCare remain key players due to their monitoring platforms, which influence the distribution of third-party sensing technologies in hospitals.

A significant strategic development is Danaher’s February 2026 agreement to acquire Masimo for approximately USD 9.9 billion. This acquisition, once finalized, will integrate Masimo’s sensor portfolio and monitoring pipeline into Danaher’s diagnostics franchise, potentially reshaping competitive dynamics and pricing leverage in the United States capnography market. In July 2025, Medtronic announced a strategic partnership with Philips to integrate Microstream™ capnography, Nellcor™ pulse oximetry, and BIS brain monitoring into the IntelliVue portfolio. Furthermore, in May 2026, Medtronic received FDA clearance for its Capnostream35 Portable Respiratory Monitor, strengthening its position in transport, ward, and portable monitoring applications. These developments highlight the competition among leading companies in connected monitoring ecosystems and clinical workflow coverage.

U.S. Capnography Equipment Industry Leaders

Koninklijke Philips N.V.

Masimo Corporation

Medtronic plc

Drägerwerk AG and Co. KGaA

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The FDA granted a substantially-equivalent decision (K253030) for Medtronic's Capnostream 35 Portable Respiratory Monitor. Classified under product code CCK (Analyzer, Gas, Carbon-Dioxide, Gaseous-Phase) by the Anesthesiology review panel, this clearance strengthens Medtronic's capnography portfolio. It enables real-time multiparameter respiratory monitoring, expanding its application beyond the ICU and OR.

- February 2026: Danaher Corporation announced a definitive agreement to acquire Masimo Corporation for approximately USD 9.9 billion, representing about 18 times the estimated 2027 EBITDA. Under Danaher's ownership, Masimo is expected to achieve high-single-digit core revenue growth.

- July 2025: Medtronic entered into a multi-year strategic partnership with Philips to integrate Microstream capnography into Philips' IntelliVue monitoring portfolio, alongside Nellcor pulse oximetry and BIS brain monitoring.

U.S. Capnography Equipment Market Report Scope

As per the scope of the report, Capnography equipment continuously measures and displays the concentration of carbon dioxide (CO2) in a patient's exhaled breath. It provides a real-time, noninvasive readout of both a numerical value (End-Tidal (CO2) and a graphical waveform (capnogram), allowing medical professionals to instantly assess ventilation, circulation, and metabolism.

The U.S. capnography equipment market is segmented by product type, component, technology, application, and end-user. By product type, the market includes multiparameter capnometers, standalone capnometers, and handheld capnography devices. By component, the market is segmented into equipment, capnometers, monitors, accessories and consumables (nasal cannulas, sampling lines, airway adapters, and related consumables), and software and connectivity. By technology, the market is categorized into mainstream capnography, sidestream capnography, and microstream capnography. By application, the market includes anesthesia monitoring, critical care monitoring, emergency medicine, procedural sedation, pain management, respiratory monitoring, and other applications. By end-user, the market is segmented into hospitals and clinics, ambulatory surgery centers, home healthcare settings, and other end users. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Multiparameter Capnometers |

| Standalone Capnometers |

| Handheld Capnography Devices |

| Equipment |

| Capnometers |

| Monitors |

| Accessories and Consumables |

| Nasal Cannulas |

| Sampling Lines |

| Airway Adapters and Related Consumables |

| Software and Connectivity |

| Mainstream Capnography |

| Sidestream Capnography |

| Microstream Capnography |

| Anesthesia Monitoring |

| Critical Care Monitoring |

| Emergency Medicine |

| Procedural Sedation |

| Pain Management |

| Respiratory Monitoring |

| Other Applications |

| Hospitals and Clinics |

| Ambulatory Surgery Centers |

| Home Healthcare Settings |

| Other End Users |

| By Product Type | Multiparameter Capnometers |

| Standalone Capnometers | |

| Handheld Capnography Devices | |

| By Component | Equipment |

| Capnometers | |

| Monitors | |

| Accessories and Consumables | |

| Nasal Cannulas | |

| Sampling Lines | |

| Airway Adapters and Related Consumables | |

| Software and Connectivity | |

| By Technology | Mainstream Capnography |

| Sidestream Capnography | |

| Microstream Capnography | |

| By Application | Anesthesia Monitoring |

| Critical Care Monitoring | |

| Emergency Medicine | |

| Procedural Sedation | |

| Pain Management | |

| Respiratory Monitoring | |

| Other Applications | |

| By End User | Hospitals and Clinics |

| Ambulatory Surgery Centers | |

| Home Healthcare Settings | |

| Other End Users |

Key Questions Answered in the Report

What is the size of the US capnography equipment market in 2026 and 2031?

The US capnography equipment market size stands at USD 292.15 million in 2026 and is forecast to reach USD 442.75 million by 2031, growing at a CAGR of 8.67% over the forecast period.

Which technology segment leads and which one grows the fastest in the United States?

Sidestream capnography led with 59.87% of revenue in 2025, while microstream capnography is projected to record the fastest growth at an 8.98% CAGR through 2031.

Why are handheld capnography devices gaining traction in the United States?

Handheld systems are expanding at a 9.65% CAGR because they fit EMS use, ambulatory settings, and emerging home monitoring needs, while newer designs also support portability, Bluetooth connectivity, and longer battery life.

Which application is growing fastest for capnography equipment in the country?

Emergency medicine is the fastest-growing application at a 10.25% CAGR through 2031, supported by wider procedural sedation protocols and stronger emergency monitoring guidance.

What is driving home healthcare adoption for capnography equipment?

Home healthcare is projected to grow at a 9.12% CAGR as older COPD patients, remote patient monitoring programs, and compact NDIR-based devices make continuous EtCO monitoring more practical outside hospitals.

What are the biggest barriers to wider capnography use outside hospitals?

The main barriers are capital cost, recurring consumables expense, reimbursement uncertainty in non-acute settings, and integration challenges across mixed monitoring fleets.

Page last updated on: