Medical Devices Cuffs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

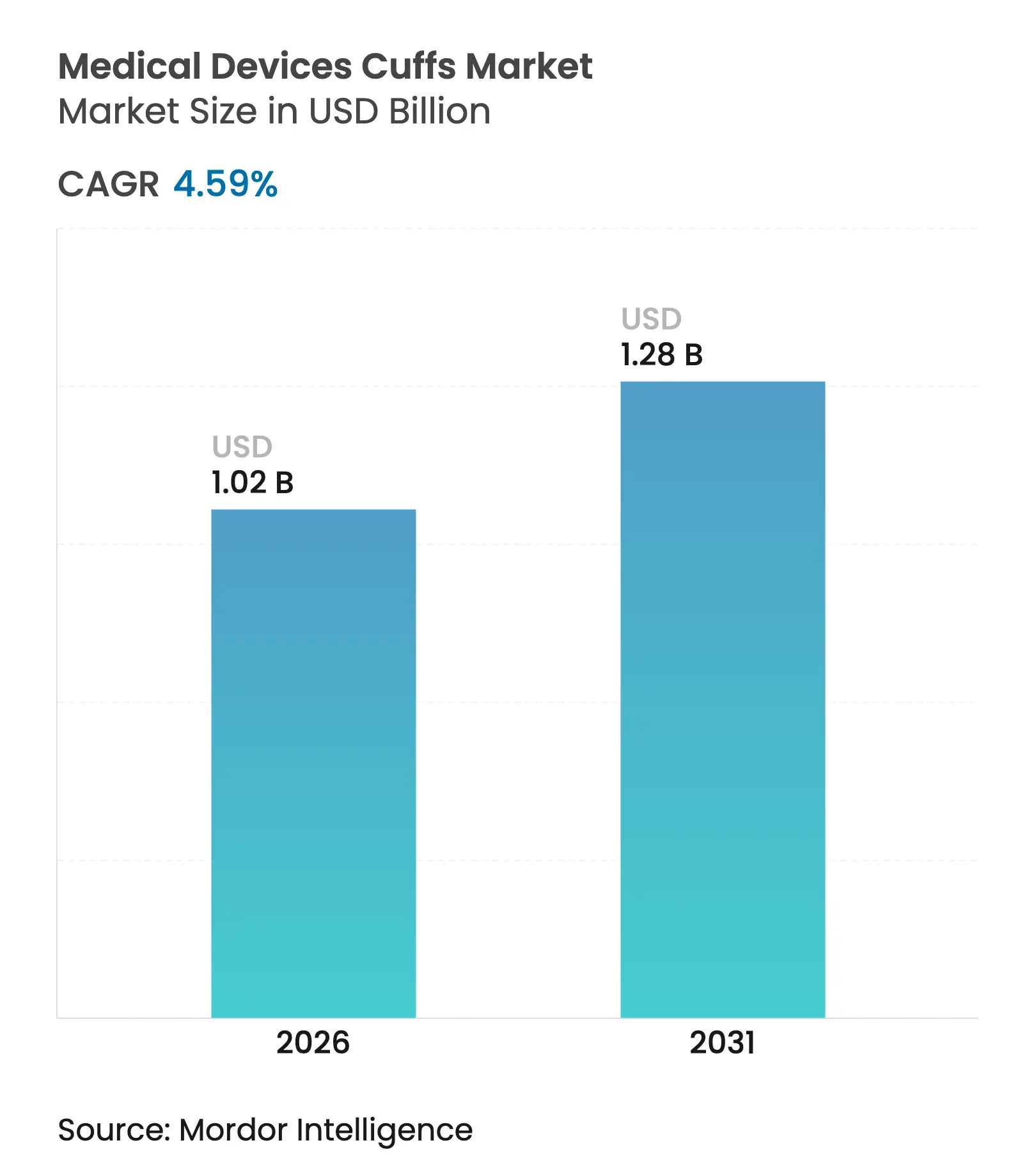

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 4.59 % CAGR |

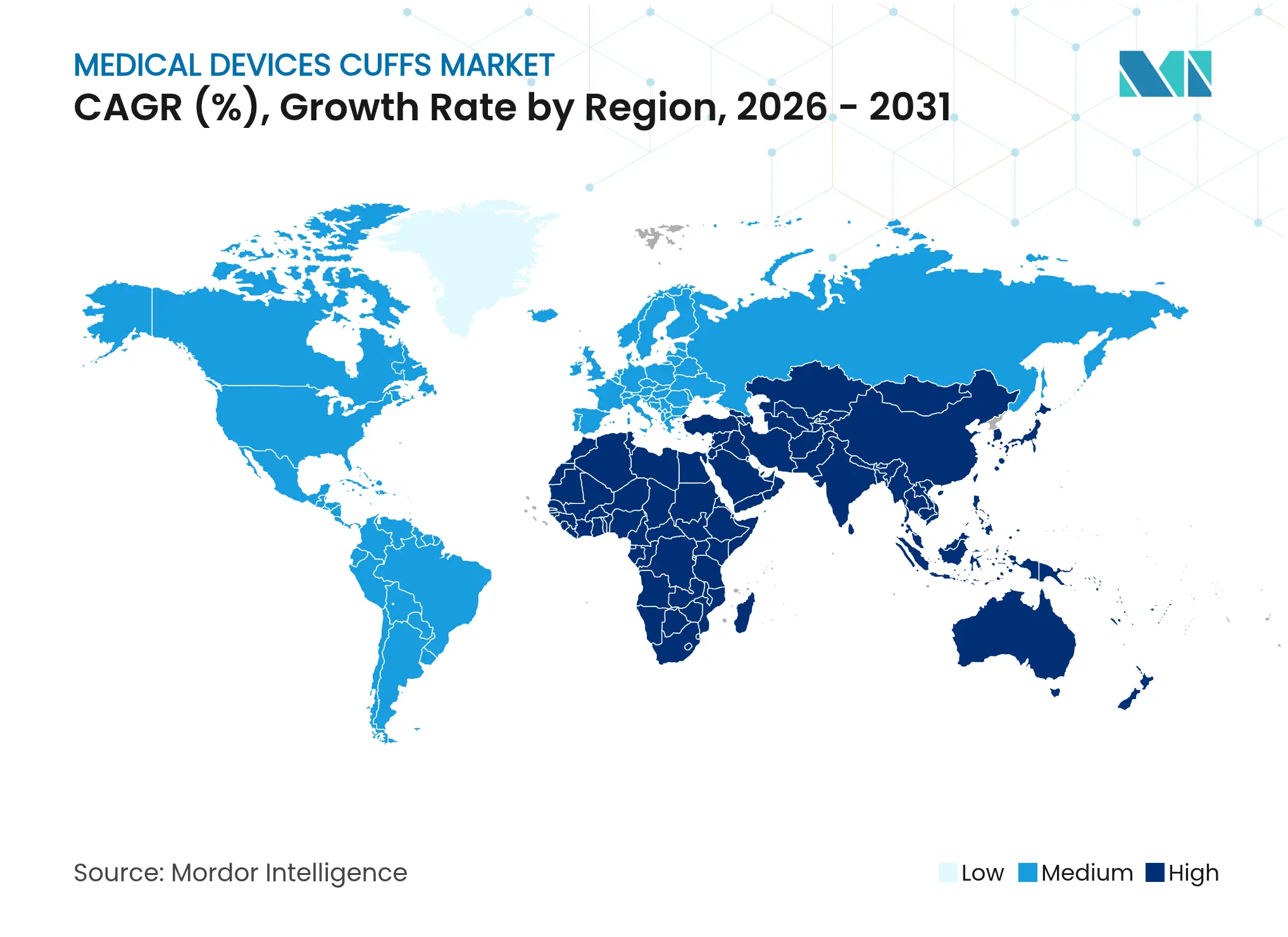

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Medical Devices Cuffs Market Analysis by Mordor Intelligence

Adoption accelerates as hypertension screening programs broaden, AI-capable cuffs enter routine clinical practice, and remote care models shift monitoring beyond hospital walls. Demand concentrates in blood pressure cuffs, where software-driven diagnostic features now differentiate brands, and in disposable formats that align with strict infection-prevention rules. Rapid unit growth from home healthcare and Asia’s expanding middle class offsets structural threats from cuff-less technologies, while reshoring moves protect supply continuity amid geopolitical tension. Competitive positioning increasingly hinges on ISO 81060-2 validation, environmental compliance, and the ability to bundle cloud analytics with hardware, factors that are reshaping the medical devices cuffs market landscape.

Key Report Takeaways

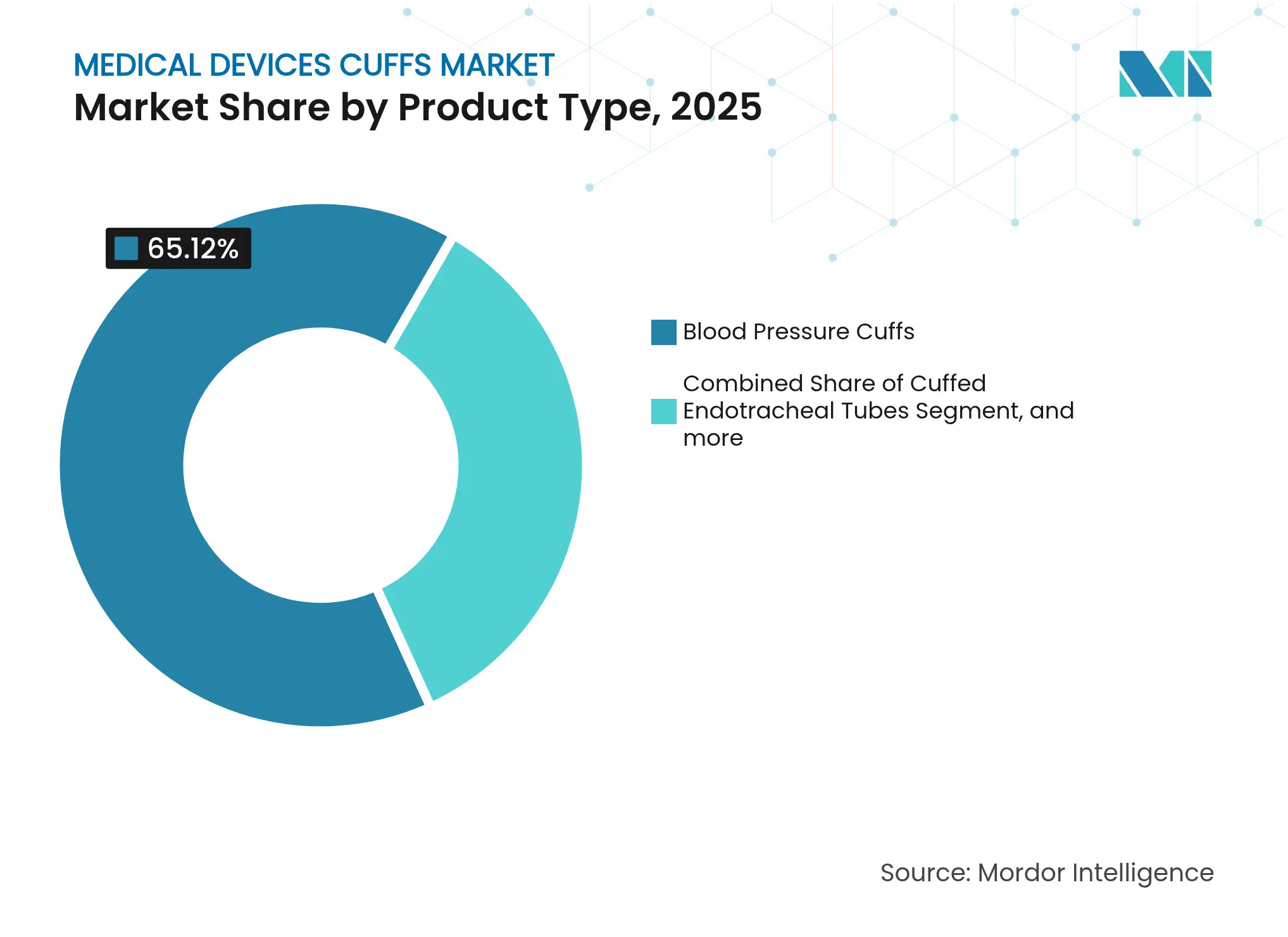

- By product type, blood pressure cuffs held 65.12% of the medical devices cuffs market share in 2025 and are projected to grow at 6.6% CAGR through 2031.

- By usability, disposable cuffs captured 55.74% of the medical devices cuffs market size in 2025 and are advancing at 6.92% CAGR to 2031.

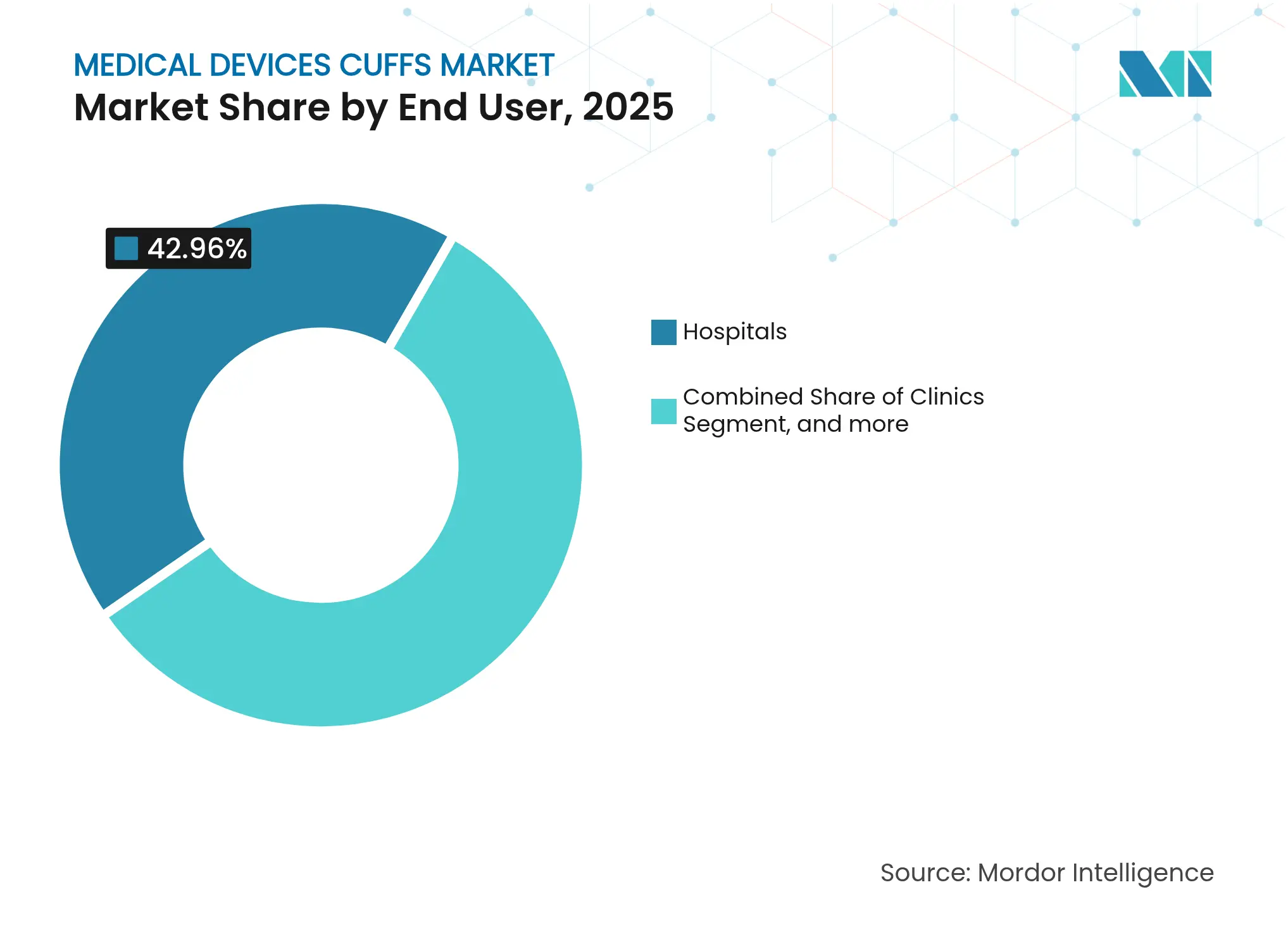

- By end user, hospitals accounted for 42.96% revenue share of the medical devices cuffs market in 2025, while home healthcare is set to post the fastest 7.08% CAGR through 2031.

- By geography, Asia Pacific posted the highest 7.95% CAGR for 2026-2031, whereas North America remained the most significant revenue contributor with 37.12% share of the medical devices cuffs market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Medical Devices Cuffs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Global

Hypertension and Cardiovascular Disease Burden

Rising Global

Hypertension and Cardiovascular Disease Burden

| +1.2% | Global, with highest impact in Asia-Pacific and developing markets | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+1.2%

|

Geographic

Relevance

:

Global, with

highest impact in Asia-Pacific and developing markets

|

Impact

Timeline

:

Long term (≥

4 years)

|

Growth in

Home-Based Care and Remote Patient Monitoring

Growth in

Home-Based Care and Remote Patient Monitoring

| +0.9% | North America & EU leading, expanding to APAC | Medium term (2-4 years) | |||

Infection

Control Protocols Favoring Disposable Cuffs

Infection

Control Protocols Favoring Disposable Cuffs

| +0.7% | Global, particularly acute in hospital-dense urban markets | Short term (≤ 2 years) | |||

Regulatory

Push: ISO 81060-2 Compliance Cycle

Regulatory

Push: ISO 81060-2 Compliance Cycle

| +0.5% | Global, with EU and North America driving initial adoption | Medium term (2-4 years) | |||

Reshoring and

Localization of Cuff Manufacturing

Reshoring and

Localization of Cuff Manufacturing

| +0.4% | North America, EU, with spillover to allied markets | Long term (≥ 4 years) | |||

Emergence of

AI-Enabled Smart Cuffs

Emergence of

AI-Enabled Smart Cuffs

| +0.8% | North America & EU early adoption, Asia-Pacific scale deployment | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Global Hypertension and Cardiovascular Disease Burden

Hypertension afflicts more than 1 billion adults, yet only 21% achieve controlled readings, according to the 2023 WHO report.[1]World Health Organization, “Global Hypertension Report 2023,” who.int Widening screening programs and HEARTS guidelines that champion at-home measurement keep the medical devices cuffs market on a long-run growth path. Clinical studies show home users gain superior risk control versus clinic-only measurement, prompting payers to reimburse home cuffs. Coupled with ageing populations in high-income economies, these factors cement demand for accurate, validated cuffs across care settings.

Growth in Home-Based Care and Remote Patient Monitoring

Remote patient monitoring now serves nearly 50 million U.S. users, reflecting a structural migration of chronic-disease management into the home.[2]Harvard Health, “Home Blood Pressure Monitoring: Why It’s Helpful,” health.harvard.edu Smartphone-connected cuffs and cloud analytics deliver continuous data flows that bolster clinical insight and cut follow-up visits. Reimbursement expansions by Medicare and private insurers lock in economic incentives, while AI triage algorithms push the medical devices cuffs market toward predictive, not reactive, care delivery. Device makers that merge intuitive design with secure data pipelines capture this rising home-healthcare spend.

Infection Control Protocols Favoring Disposable Cuffs

CDC guidelines issued post-pandemic emphasize reprocessing reusable gear, a process many facilities circumvent by adopting single-use cuffs.[3]Centers for Disease Control and Prevention, “Core Infection Prevention and Control Practices,” cdc.gov Hospitals report lower cross-transmission risk and reduced labour tied to sterilisation when shifting to disposables. FDA-cleared antimicrobial cuffs further boost safety profiles.[4]U.S. Food and Drug Administration, “Antimicrobial Blood Pressure Cuffs 510(k) Summary,” fda.gov While supply-chain disruptions highlighted the logistical simplicity of disposables, sustainability pressures now compel manufacturers to explore biodegradable polymers without sacrificing barrier protection.

Regulatory Push: ISO 81060-2 Compliance Cycle

The Lancet Commission and the European Society of Hypertension require blood-pressure devices to pass ISO 81060-2:2018 validation, impacting more than 3,000 models. Non-compliant products are rapidly losing market access as tenders and guidelines list validated devices only. Although rigorous testing raises costs, compliant manufacturers secure competitive moats and reassure clinicians of accuracy, driving purchasing preference inside the medical devices cuffs market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited

Awareness and Access in Low-Income Regions

Limited

Awareness and Access in Low-Income Regions

| -0.6% | Sub-Saharan Africa, rural Asia, Latin America | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

-0.6%

|

Geographic

Relevance

:

Sub-Saharan

Africa, rural Asia, Latin America

|

Impact

Timeline

:

Long term (≥

4 years)

|

High Cost of

Smart and Digital Cuff Technologies

High Cost of

Smart and Digital Cuff Technologies

| -0.5% | Global, particularly acute in price-sensitive emerging markets | Medium term (2-4 years) | |||

Rapid

Adoption of Cuff-less Monitoring Alternatives

Rapid

Adoption of Cuff-less Monitoring Alternatives

| -0.8% | North America & EU early adoption, Asia-Pacific following | Medium term (2-4 years) | |||

Environmental

Regulations Targeting Single-Use Plastics

Environmental

Regulations Targeting Single-Use Plastics

| -0.4% | EU leading, expanding to North America and developed markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Awareness and Access in Low-Income Regions

Only 54% of hypertensive adults in resource-constrained countries are diagnosed, underscoring access gaps. Capital scarcity keeps manual devices in circulation, while electricity and internet deficits curb smart-cuff uptake. Training shortages hamper correct use and data interpretation, limiting the immediate reach of the medical devices cuffs market despite latent epidemiological need.

Environmental Regulations Targeting Single-Use Plastics

The EU Packaging and Packaging Waste Regulation mandates recyclability from 2026 and phases out PFAS in medical devices, forcing redesign of disposable cuffs. Extended-producer requirements raise lifetime costs and push hospitals to trial reusable or hybrid solutions. Manufacturers must innovate sustainable materials without compromising clinical performance, injecting uncertainty into long-term demand for single-use cuffs.

Segment Analysis

By Product Type: Blood Pressure Cuffs Drive Innovation

Blood pressure cuffs captured 65.12% of the medical devices cuffs market share in 2025 and are projected to expand at 6.6% CAGR through 2031. Their central role in cardiovascular care positions them as the focal point for AI feature integration, as shown by Omron’s AFib-detecting device. Cuffed endotracheal and tracheostomy tubes continue steady uptake within surgical and critical-care pathways, yet they trail the pace set by blood-pressure products.Demand for validated, algorithm-ready devices shields the blood-pressure segment from immediate disruption while cuff-less wearables finalise ISO 81060-2 pathways. Hybrid designs that blend periodic cuff readings with continuous sensors provide a transition strategy and preserve share inside the medical devices cuffs market. These dynamics maintain the blood-pressure category as both volume and value engine for global suppliers.

Note: Segment shares of all individual segments available upon report purchase

By Usability: Disposable Solutions Gain Momentum

Disposable formats commanded 55.74% of the medical devices cuffs market size in 2025 and will grow 6.92% CAGR to 2031 as infection-prevention protocols remain non-negotiable in high-throughput settings. Lower reprocessing labour and avoidance of cross-contamination underpin hospital preference for single-use products.

Environmental legislation complicates this trajectory, especially in Europe where recyclability rules intensify scrutiny of plastics use. Vendors respond by developing biodegradable fabrics and reusable electronics married to single-use sleeves. These designs aim to balance infection control with sustainability targets, a critical selling point as purchasing committees evaluate total-life costs within the medical devices cuffs market.

By End User: Home Healthcare Transformation

Hospitals retained 42.96% revenue share in 2025, underpinned by high-acuity monitoring needs and bulk purchasing capacity. Yet home healthcare settings are forecast to record 7.08% CAGR, the quickest among end users, as payers reimburse remote monitoring and ageing populations prefer in-home management. Portable, app-linked cuffs now dominate new product pipelines, reflecting manufacturers focus on usability for non-clinical persons.

Clinics and ambulatory surgery centres remain steady purchasers, valuing cost-effective yet validated devices. Nonetheless, rising consumer literacy and expanded coverage for remote services shift the centre of gravity toward patient residences, a structural change that steadily enlarges the medical devices cuffs market nexus beyond institutional walls.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 37.12% of global revenue in 2025, buoyed by Medicare’s expanding reimbursement for remote monitoring and an installed base of AI-cleared devices led by GE HealthCare’s 80 authorisations. Federal incentives for reshoring saw Becton Dickinson inject USD 10 million into domestic lines, boosting security of supply for critical disposables. The forthcoming Quality Management System Regulation aligning FDA with ISO 13485 is expected to streamline post-2026 exports for compliant U.S. manufacturers.

Asia-Pacific is the fastest-advancing territory, registering 7.95% CAGR as urbanising populations intensify hypertension screening. Japan’s USD 40 billion device market grows 5.5% annually as its ageing society requires frequent cardiovascular monitoring. China’s push for indigenous innovation and broader insurance coverage pulls multinational and domestic brands deeper into tier-2 and tier-3 cities, expanding the addressable medical devices cuffs market.

Europe posts stable mid-single-digit growth, underwritten by MDR enforcement that favours thoroughly validated cuffs. Environmental statutes add cost layers yet spur innovation in recyclable packs. PFAS bans force material re-engineering, creating openings for suppliers of compliant polymers. Emerging regions such as South America and the Middle East & Africa remain underpenetrated but have begun adopting remote patient monitoring pilots, indicating long-run upside.

Competitive Landscape

Market Concentration

The medical devices cuffs market is moderately consolidated, with prominent manufacturers accounting for significant global sales. Omron Healthcare leverages FDA-cleared AFib detection to command premium positioning and deepen patient engagement outside hospitals. Teleflex’s EUR 760 million acquisition of BIOTRONIK’s vascular intervention unit broadens its cardiovascular footprint and cross-selling synergies. Becton Dickinson expands syringe and IV-line capacity in Utah to shore up North American availability and align with public-sector sourcing criteria.

Technology edge increasingly defines competitive hierarchy—firms marrying hardware with cloud analytics vault ahead on subscription revenue opportunities and clinician loyalty. ISO 81060-2 validation remains a high barrier to entry, while sustainability credentials emerge as a tie-breaker in tenders, pushing incumbents to invest in green materials. Meanwhile, start-ups in cuff-less wearables attract venture capital yet face lengthier regulatory pathways, allowing established cuff vendors to defend their share even as modality shifts unfold within the medical devices cuffs market.

Medical Devices Cuffs Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex announced acquisition of BIOTRONIK's Vascular Intervention business for approximately EUR 760 million (USD 825 million), enhancing its interventional portfolio with coronary and peripheral vascular devices. This strategic acquisition strengthens Teleflex's position in the USD 10 billion interventional cardiology market and is expected to drive 6% revenue CAGR starting in 2026.

- November 2024: OMRON Healthcare received FDA De Novo authorization for blood pressure monitors featuring AI-powered AFib detection, achieving 95% sensitivity and 98% specificity in clinical trials. The company plans to launch these monitors in early 2025, representing a significant advancement in home cardiovascular monitoring capabilities.

- May 2024: Gerresheimer announced USD 180 million expansion of its Peachtree City, Georgia facility for medical systems production, adding 18,000 square meters of production space and creating over 400 jobs. This investment underscores the company's commitment to North American market expansion and drug delivery system manufacturing.

- April 2024: OMRON Healthcare received a grant for developing a blood pressure monitor with double cuff structure, representing innovation in measurement accuracy and reliability for clinical applications.

Table of Contents for Medical Devices Cuffs Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Global Hypertension and Cardiovascular Disease Burden

- 4.2.2Growth in Home-Based Care and Remote Patient Monitoring (RPM)

- 4.2.3Infection Control Protocols Favoring Disposable Cuffs

- 4.2.4Regulatory Push: ISO 81060-2 Compliance Cycle

- 4.2.5Reshoring and Localization of Cuff Manufacturing

- 4.2.6Emergence of AI-Enabled Smart Cuffs

- 4.3Market Restraints

- 4.3.1Limited Awareness and Access in Low-Income Regions

- 4.3.2High Cost of Smart and Digital Cuff Technologies

- 4.3.3Rapid Adoption of Cuff-less Monitoring Alternatives

- 4.3.4Environmental Regulations Targeting Single-Use Plastics

- 4.4Regulatory Landscape

- 4.5Porter’s Five Forces Analysis

- 4.5.1Bargaining Power of Suppliers

- 4.5.2Bargaining Power of Buyers

- 4.5.3Threat of New Entrants

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry Intensity

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Product Type

- 5.1.1Blood Pressure Cuffs

- 5.1.2Cuffed Endotracheal Tubes

- 5.1.3Tracheostomy Tubes

- 5.1.4Other Specialty Cuffs

- 5.2By Usability

- 5.2.1Disposable Cuffs

- 5.2.2Reusable Cuffs

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Clinics

- 5.3.3Ambulatory Surgery Centers

- 5.3.4Home Healthcare Settings

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Omron Healthcare, Inc.

- 6.3.2GE HealthCare

- 6.3.3Cardinal Health

- 6.3.4SunTech Medical, Inc.

- 6.3.5Teleflex Incorporated

- 6.3.6Smiths Medical

- 6.3.7Baxter (Hillrom)

- 6.3.8A&D Company

- 6.3.9Philips Healthcare

- 6.3.10Welch Allyn

- 6.3.11Microlife

- 6.3.12Beurer GmbH

- 6.3.13Withings SA

- 6.3.143M Company

- 6.3.15Becton, Dickinson & Co.

- 6.3.16ICU Medical

- 6.3.17Medtronic

- 6.3.18ConvaTec Group

- 6.3.19Cook Medical

- 6.3.20Pulmodyne

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Product Type

- Blood Pressure Cuffs

- Cuffed Endotracheal Tubes

- Tracheostomy Tubes

- Other Specialty Cuffs

- Blood Pressure Cuffs

- By Usability

- Disposable Cuffs

- Reusable Cuffs

- Disposable Cuffs

- By End User

- Hospitals

- Clinics

- Ambulatory Surgery Centers

- Home Healthcare Settings

- Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's Medical Devices Cuffs Baseline Commands Reliability

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 0.98 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 0.95 B (2025) | Regional Consultancy A | omits home-care channels and assumes slower disposable shift | ||

USD 0.91 B (2024) | Trade Journal B | older base year and limited airway cuff coverage | ||

USD 0.70 B (2025) | Global Consultancy C | focuses on blood-pressure cuffs only, excludes airway products |