Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

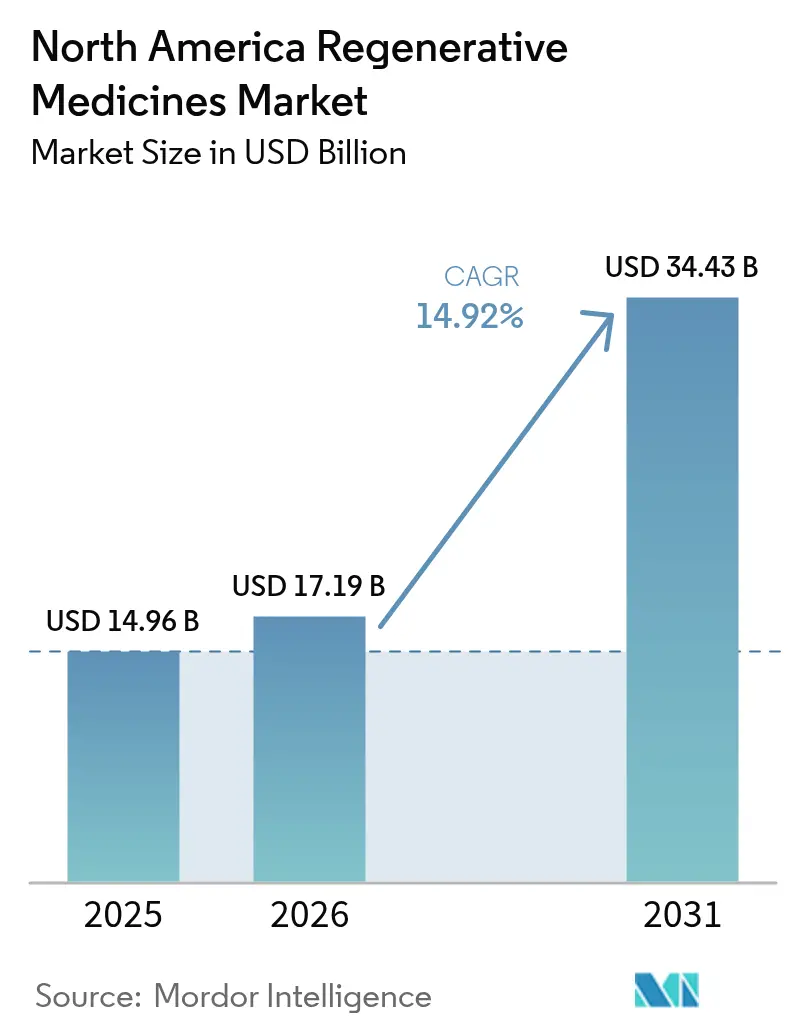

| Base Year Market Size (2025) | USD 14.96 Billion |

| Market Size (2026) | USD 17.19 Billion |

| Market Size (2031) | USD 34.43 Billion |

| Growth Rate (2026 - 2031) | 14.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Regenerative Medicines Market Analysis by Mordor Intelligence

North America Regenerative Medicines Market size in 2026 is estimated at USD 17.19 billion, growing from 2025 value of USD 14.96 billion with 2031 projections showing USD 34.43 billion, growing at 14.92% CAGR over 2026-2031.

Commercial adoption is accelerating as therapies that were once confined to academic settings now secure reimbursement for high-burden conditions such as osteoarthritis, hemophilia A and relapsed multiple myeloma. The United States accounts for 84.11% of total 2024 revenue, while Mexico delivers the highest growth trajectory on the continent as regulatory modernization and medical-tourism flows converge. Cell therapies retain leadership on volume, yet gene therapies deliver the steepest revenue ramp as manufacturing economies of scale materialize, particularly in viral-vector production. Heightened strategic investment in in-house manufacturing, spurred by the need for batch-control and intellectual-property protection, is reshaping site-selection patterns throughout the North America regenerative medicine market.

Key Report Takeaways

- By product type, cell therapies led with 42.13% North America regenerative medicine market share in 2025; gene therapies are advancing at a 23.82% CAGR through 2031.

- By origin of cells, allogeneic approaches commanded 55.22% of the North America regenerative medicine market size in 2025, while autologous therapies are forecast to grow at 20.61% CAGR to 2031.

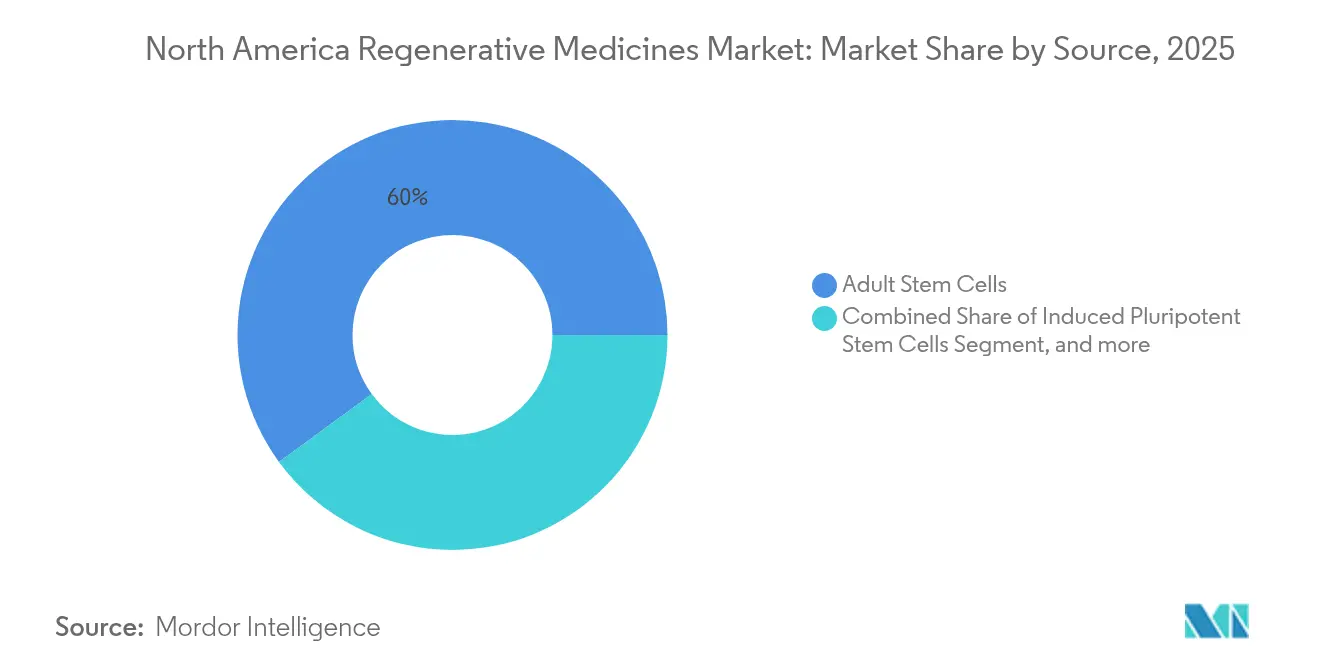

- By source, adult stem cells held 60.05% revenue share in 2025; the induced pluripotent stem-cell segment is expanding at a 26.10% CAGR.

- By application, orthopedics and musculoskeletal indications captured 31.12% of the market in 2025; oncology applications exhibit the fastest growth at 25.27% CAGR.

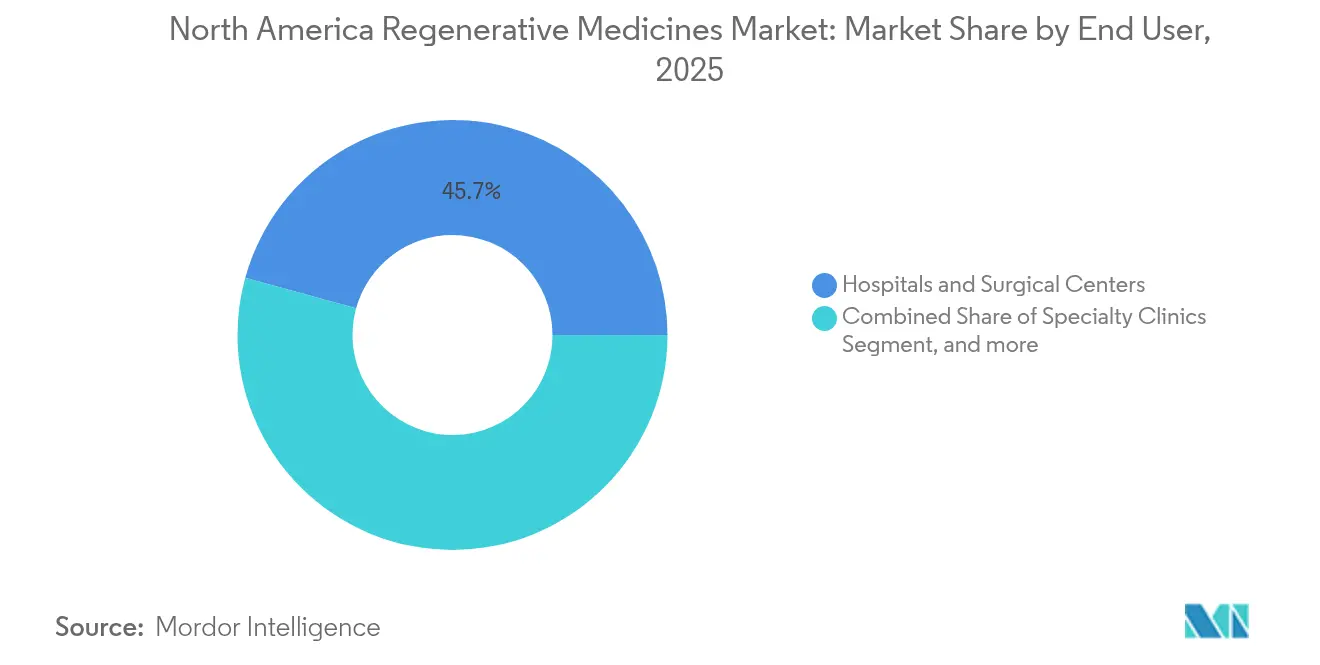

- By end user, hospitals and surgical centers accounted for 45.71% of 2025 revenue; biobanks and cell banks register the quickest rise at 18.15% CAGR.

- By country, the United States dominated with an 83.64% share in 2025, whereas Mexico is forecast to accelerate at an 17.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Regenerative Medicines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of chronic degenerative & age-related disorders | +3.2% | United States, Canada | Medium term (2–4 years) |

| Robust government & private funding for advanced therapies | +2.8% | United States, Canada | Short term (≤2 years) |

| Expanded FDA expedited pathways fueling pipeline | +2.1% | Primarily United States; spillover to Canada | Short term (≤2 years) |

| Big-pharma–biotech alliances accelerating commercialization roadmaps | +1.9% | U.S. biotech hubs; expanding impact in Canada | Medium term (2–4 years) |

| Increasing adoption of stem-cell technology | +1.7% | Pan-regional | Long term (≥4 years) |

| Advancements in 3D bioprinting and tissue-engineering technologies | +1.5% | U.S. research clusters; emerging capacity in Canada | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Chronic Degenerative & Age-Related Disorders

An expanding cohort of older adults is amplifying the clinical urgency behind regenerative solutions. More than 54 million Americans live with arthritis, and projections place the figure at 78 million by 2040, driving orthopedic demand within the North America regenerative medicine market.[1]Centers for Disease Control and Prevention, “Arthritis Prevalence Statistics,” cdc.gov Parallel surges in cardiovascular and neurodegenerative conditions add to the therapeutic backlog, prompting sponsors to pursue FDA’s Regenerative Medicine Advanced Therapy (RMAT) designation for age-related indications. The cumulative economic burden, measured in lost productivity and direct medical expenditure, intensifies payer willingness to underwrite curative options that offset lifetime costs. Collectively, these epidemiological factors add substantial momentum to pipeline activity across cell, gene and tissue-engineered modalities.

Robust Government & Private Funding for Advanced Therapies

Funding velocity underscores the maturing innovation cycle. The National Institutes of Health allocated USD 2.8 billion to regenerative-medicine projects for fiscal-year 2024, a 23% budgetary rise over 2023.[2]National Institutes of Health, “FY 2024 Budget for Regenerative Medicine,” nih.gov Simultaneously, Canada’s Strategic Innovation Fund committed CAD 1.2 billion (USD 890 million) to construct three advanced-therapy manufacturing hubs, a move designed to anchor domestic capacity and attract technology transfer agreements.[3]Government of Canada, “Strategic Innovation Fund—Advanced Therapeutics,” canada.ca Venture investors are mirroring the trend by preferentially channeling capital toward late-stage assets with defined regulatory pathways, signaling confidence in near-term revenue realization within the North America regenerative medicine market.

Expanded FDA Expedited Pathways Fueling Pipeline

The U.S. Food and Drug Administration granted 27 new RMAT designations during 2024, a 42% increase versus the prior year, trimming median review time for qualifying cell therapies from 12.8 months to 7.3 months. Faster agency feedback loops lower development risk and have enticed non-traditional entrants, including technology firms building data-infrastructure platforms to support cell-and-gene therapy logistics. These dynamics strengthen the competitive tempo inside the North America regenerative medicine market and reduce time-to-clinic for high-unmet-need indications.

Big-Pharma–Biotech Alliances Accelerating Commercialization

Thirty-seven partnership transactions worth more than USD 28 billion were executed in 2024, targeting manufacturing technology transfer rather than traditional royalty structures. Pharmaceutical majors seek end-to-end control over viral-vector and cell-processing know-how, while smaller biotechs retain higher program equity in exchange for sharing later-stage risk. The collaboration trend lifts aggregate production capacity and supports faster scale-up milestones, directly benefitting growth prospects for the North America regenerative medicine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost & complex GMP manufacturing infrastructure | −2.5% | United States, Canada, Mexico | Medium term (2–4 years) |

| Stringent & evolving regulatory compliance for ATMPs | −1.8% | Primarily United States | Short term (≤2 years) |

| Limited long-term clinical evidence and outcome data | −1.6% | Pan-regional | Long term (≥4 years) |

| Ethical and public-perception challenges around cell-based therapies | −1.2% | United States, Canada | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Cost & Complex GMP Manufacturing Infrastructure

Specialized clean-room construction averages USD 2,000 per square foot, quadruple that of conventional biologics facilities, and skilled-labor shortages persist, with two-thirds of regenerative-medicine firms citing hiring difficulties in 2024. Manual processing steps amplify batch variability; industry surveys place 15% of runs outside release specifications, five-times the failure rate observed for monoclonal antibodies. While automation is advancing, capital intensity remains a formidable hurdle stifling wider roll-out across the North America regenerative medicine market.

Stringent & Evolving Regulatory Compliance for ATMPs

Between trial readout and biologics license application, regenerative-medicine sponsors spend an average 14.7 months navigating documentation requirements—nearly double that for traditional drugs. Eleven new FDA guidance documents in 2024 alone underscore the fluid nature of regulatory expectations. Post-approval, Risk Evaluation and Mitigation Strategies frequently mandate 15-year patient follow-up. Such extended surveillance elevates operating costs for smaller firms, raising entry barriers across the North America regenerative medicine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gene Therapies Disrupting Treatment Paradigms

Cell therapies led the revenue tables in 2025 with 42.13% North America regenerative medicine market share, benefitting from established reimbursement in oncology and orthopedics. Gene therapies, however, post a 23.82% CAGR outlook, propelled by manufacturing efficiencies that have trimmed viral-vector costs by 35% since 2023.

Across 2024 pipelines, 43% of candidates now blend multiple regenerative modalities, reflecting a strategic pivot toward combination constructs. Three such hybrid products gained FDA clearance in early 2025, confirming regulatory openness to category-blurring solutions that will likely enlarge the North America regenerative medicine market.

By Origin of Cells: Autologous Momentum Building

Allogeneic therapies commanded 55.22% of the North America regenerative medicine market size in 2025, aided by off-the-shelf scalability and established distribution chains. Autologous approaches are closing the gap, advancing at 20.61% CAGR as process optimization compresses vein-to-vein timelines from 28 days in 2023 to 14 days in early 2025.

Efficacy differentials remain indication-specific: autologous CAR-T retains a clinical edge in hematologic malignancies, whereas allogeneic constructs offer rapid deployment in cardiovascular emergencies. Hybrid sourcing models, marrying autologous targeting with allogeneic manufacturing, received their first approval in March 2025, further diversifying the North American regenerative medicine market.

By Source: iPSCs Reshaping Development Economics

Adult stem cells dominated 2025 revenue with a 60.05% share, supported by safety track records across graft-versus-host and cartilage repair. Yet induced pluripotent stem cells are the growth engine, expanding at 26.10% CAGR through process-control advances that have sliced production costs by 45% since 2023.

ClinicalTrials.gov lists 11 new CRISPR-edited stem-cell protocols launched during 2024, underscoring a convergence of gene editing and pluripotent biology. These innovations enhance differentiation fidelity and could push the North American regenerative medicine market toward broader organ-repair indications.

By Application: Oncology Catalyzing Innovation

Orthopedics retained 31.12% revenue share in 2025, anchored by high-volume cartilage and disc-repair procedures. Oncology, however, exhibits the sharpest ascent with a 25.27% CAGR forecast, as CAR-T and gene-edited NK-cell platforms expand from hematologic to solid-tumor settings.

Regulators have launched an indication-expansion pilot that lowers evidentiary thresholds for follow-on approvals, cutting supplemental timelines by up to 40%. Sponsors are now running an average 3.7 expansion trials per approved therapy, intensifying competitive jockeying inside the North America regenerative medicine market.

By End User: Specialized Centers Setting Adoption Pace

Hospitals and surgical centers contributed 45.71% of 2025 revenue owing to entrenched referral networks and established payer contracts. Biobanks and cell banks represent the quickest-growing customer group at 18.15% CAGR, reflecting their evolution from storage utilities to value-added processing hubs.

Twenty-seven U.S. hospital systems opened dedicated cell-and-gene therapy centers during 2024, creating procedural learning curves that cut administration time by 32% and ancillary costs by 28%. Such efficiencies widen patient access and sustain momentum within the North America regenerative medicine market.

Geography Analysis

The United States underpins the North America regenerative medicine market, holding 83.64% of 2025 revenue, driven by 27 fresh RMAT designations that shortened median regulatory review by 5.5 months. Regional footprints are diversifying as 14 GMP facilities broke ground in the Southeast and Midwest during 2024, catalyzed by state incentive programs in Texas, North Carolina and Indiana. These geographic shifts mitigate bottlenecks traditionally concentrated in coastal biotech hubs and further embed the North America regenerative medicine market across the national landscape.

Canada’s contribution, although smaller in absolute terms, is strategically amplified by CAD 1.2 billion in federal backing for three new advanced-therapy plants announced in March 2024. Universal healthcare financing simplifies reimbursement negotiations, and the pan-Canadian Pharmaceutical Alliance is piloting value-based contracts for one-time gene therapies. Patent filings originating from Canadian universities rose 37% year over year in 2024 CIPO, confirming upstream innovation strength that feeds the continental pipeline of the North America regenerative medicine market.

Mexico provides the highest growth vector at an 17.93% CAGR outlook to 2031. Regulatory modernization by COFEPRIS in late 2024 clarified clinical trial and commercial pathways, triggering five foreign direct-investment projects in allogeneic manufacturing during the same year. Lower labor costs make the country an attractive production base, while CENETEC’s new regenerative-medicine assessment unit, launched January 2025, institutionalizes evidence-based adoption for public hospitals. These shifts bolster demand and reinforce the trilateral ecosystem that defines the broader North America regenerative medicine market.

Competitive Landscape

Competitive structure in the North America regenerative medicine market is barbell-shaped: multinational pharmaceutical groups and early-stage biotechs dominate, leaving a sparse mid-tier. Gene-therapy commercialization is relatively concentrated; the top five players control major share in marketed vectors, whereas tissue-engineering remains fragmented. Intellectual-property focus has moved downstream into manufacturing science; USPTO data show a 67% rise in processing-oriented filings during 2024, outpacing therapeutic-mechanism patents.

Vertical integration is now the prevailing strategy. Seventy-three percent of companies owning commercial assets announced internal capacity expansions during 2024 to overcome vector shortages and to maintain proprietary cell-handling protocols. These moves effectively realign supply-chain power dynamics, embedding production knowledge inside corporate walls and strengthening competitive moats across the North America regenerative medicine market.

White-space opportunities lie at modality junctions, particularly in combining gene-editing precision with off-the-shelf cell constructs. Oncology remains the fiercest battleground, with 43 developers pursuing overlapping hematologic indications, while neurodegeneration attracts fewer entrants but offers high-value upside. Market participants differentiate less on scientific novelty and more on consistent, cost-efficient release specifications, underlining manufacturing excellence as the principal lever for sustained leadership in the North America regenerative medicine market.

North America Regenerative Medicines Industry Leaders

Integra Lifesciences

Abbvie Inc (Allergan Plc)

Cook Medical (Cook Biotech Incorporated)

Organogenesis Holdings Inc.

Smith & Nephew plc (Osiris Therapeutics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Poseida Therapeutics obtained RMAT designation from the FDA for P-BCMA-ALLO1, an allogeneic TSCM-based CAR-T therapy targeting relapsed or refractory multiple myeloma.

- August 2024: Organogenesis Holdings secured Medicare coverage for ReNu, an amniotic suspension indicated for knee osteoarthritis, broadening reimbursement reach.

- July 2024: Sangamo Therapeutics and Pfizer reported positive Phase 3 data for their hemophilia A gene therapy, with 94% of patients maintaining therapeutic factor VIII expression for over three years.

North America Regenerative Medicines Market Report Scope

As per the scope of the report, regenerative medicines are used to repair, replace, and regenerate the tissues and organs affected by injury, disease, or the natural ageing process. These medicines restore the functionality of cells and tissues and are used in several degenerative disorders, such as dermatology, neurodegenerative diseases, cardiovascular, and orthopaedic applications. The North America Regenerative Medicine Market is segmented by type of technology application and geography.

By Product Type

| Cell Therapies |

| Gene Therapies |

| Tissue-Engineered Products |

| Biomaterials |

| Acellular Regenerative Products |

By Origin of Cells

| Autologous |

| Allogeneic |

| Xenogeneic |

By Source

| Adult Stem Cells |

| Induced Pluripotent Stem Cells |

| Embryonic Stem Cells |

| Hematopoietic Stem Cells |

By Application

| Orthopedics & Musculoskeletal |

| Dermatology & Wound Care |

| Cardiovascular |

| Neurology |

| Oncology |

| Ophthalmology |

| Others (Endocrine, Renal etc.) |

By End User

| Hospitals & Surgical Centers |

| Specialty Clinics |

| Academic & Research Institutes |

| Biobanks & Cell Banks |

By Country

| United States |

| Canada |

| Mexico |

| By Product Type | Cell Therapies |

| Gene Therapies | |

| Tissue-Engineered Products | |

| Biomaterials | |

| Acellular Regenerative Products | |

| By Origin of Cells | Autologous |

| Allogeneic | |

| Xenogeneic | |

| By Source | Adult Stem Cells |

| Induced Pluripotent Stem Cells | |

| Embryonic Stem Cells | |

| Hematopoietic Stem Cells | |

| By Application | Orthopedics & Musculoskeletal |

| Dermatology & Wound Care | |

| Cardiovascular | |

| Neurology | |

| Oncology | |

| Ophthalmology | |

| Others (Endocrine, Renal etc.) | |

| By End User | Hospitals & Surgical Centers |

| Specialty Clinics | |

| Academic & Research Institutes | |

| Biobanks & Cell Banks | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North America regenerative medicine market?

The North America regenerative medicine market size is USD 17.19 billion in 2026 and is set to climb to USD 34.43 billion by 2031.

Which segment is growing the fastest?

Gene therapies show the highest growth, advancing at a 23.82% CAGR through 2031 due to improved manufacturing and pivotal clinical results.

Why is Mexico the fastest-growing geography?

Regulatory modernization, cost-efficient manufacturing and expanding medical tourism will propel Mexico at an 17.93% CAGR over the forecast period.

How are FDA expedited pathways influencing the market?

RMAT, Breakthrough Therapy and Fast-Track programs have reduced median review times by up to 5.5 months, accelerating time-to-market for innovative therapies.

What are the main challenges to large-scale manufacturing?

High capital costs for GMP facilities, skilled-labor shortages and batch variability impose significant hurdles, especially for smaller developers.

Page last updated on: