United States Home Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

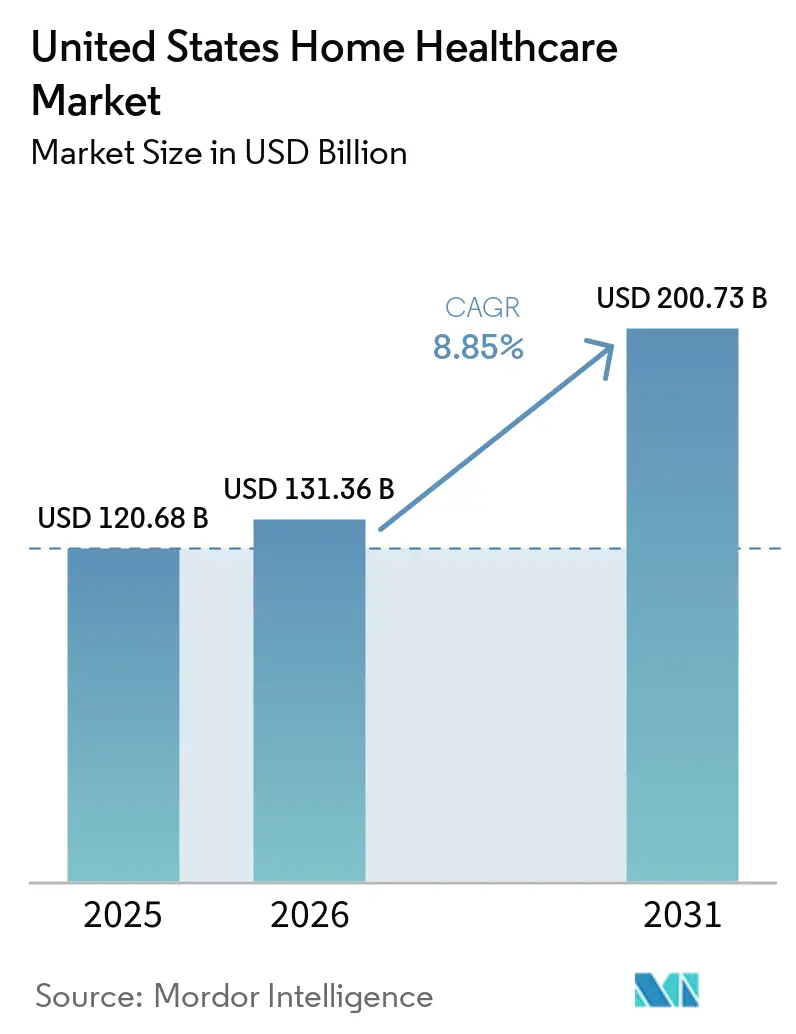

| Base Year Market Size (2025) | USD 120.68 Billion |

| Market Size (2026) | USD 131.36 Billion |

| Market Size (2031) | USD 200.73 Billion |

| Growth Rate (2026 - 2031) | 8.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Home Healthcare Market Analysis by Mordor Intelligence

The United States Home Healthcare Market size is expected to increase from USD 120.68 billion in 2025 to USD 131.36 billion in 2026 and reach USD 200.73 billion by 2031, growing at a CAGR of 8.85% over 2026-2031.

The market is moving into a more durable growth phase as payers direct more acute and chronic care into the home, while health systems respond to stronger evidence on outcomes and post-discharge cost control. CMS reported that Medicare beneficiaries treated through Acute Hospital Care at Home experienced lower 30-day mortality and lower Medicare spending in the 30 days after discharge than comparable inpatient cases, which has strengthened the case for broader deployment of home-based models. This is pushing insurers and health systems to invest more heavily in remote monitoring, home-based post-acute care pathways, and hospital-at-home logistics, which is steadily changing where care is delivered and how providers compete. Near-term pressure remains concentrated in reimbursement compression under the CY 2026 Home Health Prospective Payment System final rule and in the nationwide Medicare enrollment moratorium for new home health agencies that took effect on May 13, 2026. Those conditions favor scaled providers with stronger compliance systems, payer access, workforce depth, and digital infrastructure, while the core demand base remains resilient because older and clinically complex patients continue to require recurring care.

Key Report Takeaways

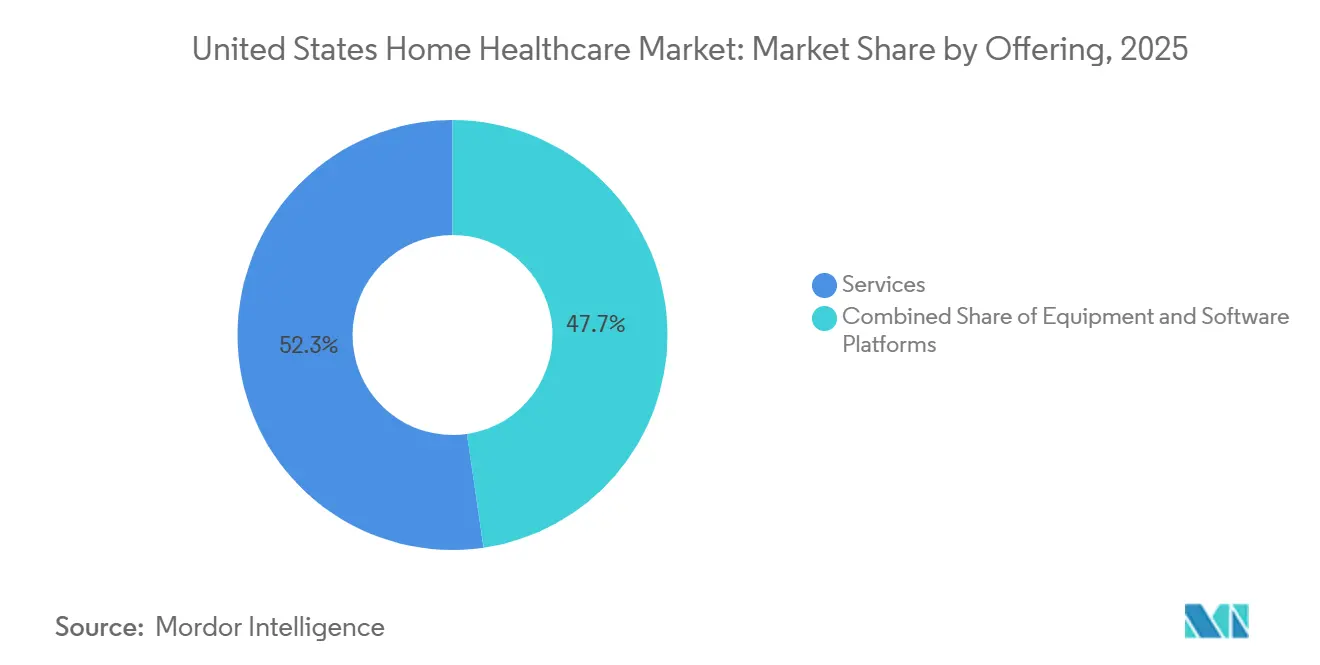

- By offering, services held 52.31% of market value in 2025, while equipment is projected to grow at a 9.38% CAGR from 2026 to 2031.

- By indication, cardiovascular disorders and hypertension accounted for 38.24% of the market in 2026, while renal disorders are forecast to expand at a 9.52% CAGR through 2031.

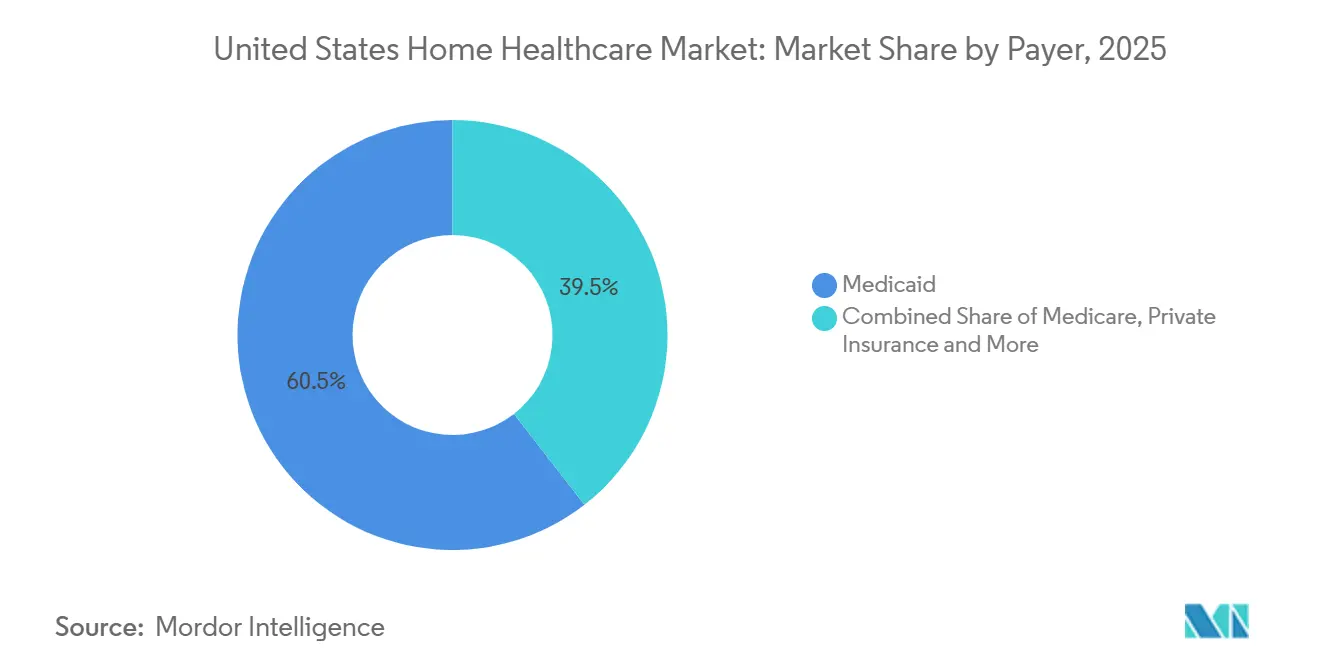

- By payer, Medicaid held 60.52% share in 2025, while commercial and private insurance is projected to advance at a 9.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Home Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Multi-Morbidity Burden | +2.8% | National, with highest concentration in Florida, Arizona, California, and the Southeast | Long term (≥ 4 years) |

| Chronic-Care Migration to Lower-Cost Home Settings | +2.0% | National, with early intensity in markets with high institutional care cost pressure | Medium term (2-4 years) |

| Telehealth and Remote Monitoring Reimbursement Support | +1.1% | National, with outsized impact in rural and low-access markets | Short term (≤ 2 years) |

| Hospital-at-Home and Post-Acute-at-Home Adoption | +1.2% | National, with acceleration in markets near major health systems | Medium term (2-4 years) |

| Home Dialysis Coverage Expansion for AKI Patients | +0.6% | National, with higher impact in ESRD-prevalent regions, including the Southeast and Midwest | Short term (≤ 2 years) |

| Home-Administered Immunotherapy and Specialty Infusion Migration | +0.8% | National, with early adoption in high-density oncology markets, including the Northeast and West Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Multi-Morbidity Burden

Older adults remain the core demand base for the United States home healthcare market, which gives the sector a steady flow of recurring need across skilled nursing, monitoring, therapy, infusion, and personal care. This demand profile is stronger than in many consumer-led healthcare categories because utilization is tied less to discretionary spending and more to age, frailty, and coexisting chronic conditions. Multi-morbidity also raises revenue intensity per patient because cardiovascular disease, diabetes, renal disease, and mobility limits often need several services and devices at the same time. That combination makes volume more predictable and makes home-based care more attractive to payers looking for clinically manageable alternatives to facility use. As the older patient pool deepens, providers with broader service breadth are better positioned to capture a larger share of the United States home healthcare market.

Chronic-Care Migration to Lower-Cost Home Settings

The cost gap between institutional and home-based chronic care remains a powerful reason for payers to move more treatment into the home. The Federal Reserve Bank of Richmond reported that a private nursing-home room costs 3.8 times the annual cost of a home health aide at median rates, which keeps the economic case for home-based care clear when patients are clinically stable[1]Federal Reserve Bank of Richmond, “Home Health Care and Aging in Place,” Economic Brief EB-26-02, richmondfed.org. The National Home Infusion Association reported that immune globulins were the fastest-growing category in home infusion claims during 2025, which shows that migration is strongest in higher-value specialty therapy rather than in every service line equally. March 2025 bipartisan legislation to preserve patient access to home infusion signaled that reimbursement support for serious home-treated conditions continues to draw policy attention. CareCentrix's expansion of Oncology at Home to include 30 immunotherapy drugs also showed that managed care organizations are actively designing benefit pathways around treatment at home rather than simply responding to it.

Telehealth and Remote Monitoring Reimbursement Support

Telehealth and remote monitoring are giving the United States home healthcare market a more technology-enabled operating model, especially in follow-up care and lower-access settings. KFF noted that Medicare Advantage plans can continue to include select telehealth services in basic benefit packages through at least December 2027, which protects an important part of the reimbursement base from immediate policy uncertainty. That flexibility matters because home care providers need durable payment pathways before they scale remote physiological monitoring and remote therapeutic monitoring programs. In practical terms, monitoring is becoming both a clinical management tool and a commercial retention tool inside the United States home healthcare market.

Hospital-at-Home and Post-Acute-at-Home Adoption

Hospital-at-home is becoming one of the clearest structural growth channels for the United States home healthcare market. The American Medical Association reported that Congress extended the CMS Acute Hospital Care at Home waiver through September 30, 2030, which removed a major barrier that had previously limited long-term capital commitment by health systems. The American Hospital Association stated that 366 hospitals across 139 health systems in 37 states were approved under the waiver as of February 2026, and the program had served more than 48,500 fee-for-service Medicare and Medicaid patients since 2020. The same source highlighted stronger outcomes at leading systems, including a 7% 30-day readmission rate at Mass General Brigham versus 23% for traditional inpatient care, and a 9.2% rate at Ohio State compared with 16% for inpatient comparators in fiscal 2025. Penn Medicine's April 2026 launch confirms that more health systems are now building the logistics, command-center workflows, and care-at-home infrastructure needed to support this model at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled Clinician and Aide Shortages | -1.5% | National, most acute in rural markets and high-density urban centers with wage competition | Long term (≥ 4 years) |

| PDGM-Related Reimbursement Pressure and Rate Uncertainty | -1.2% | National, with disproportionate impact on smaller independent agencies | Medium term (2-4 years) |

| Smart-Home IoT Cybersecurity and HIPAA Compliance Burden | -0.4% | National, with operational burden highest for hospital-at-home deployments | Medium term (2-4 years) |

| Fragmented Referral-to-Start-of-Care Workflows | -0.4% | National, most severe in markets with high acute-care discharge volumes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled Clinician and Aide Shortages

Workforce availability remains the hardest operating constraint in the United States home healthcare market because service demand can rise faster than agencies can staff visits safely and on time. Homecare Homebase reported that more than 4.2 million patients in 2024 did not receive physician-recommended home health services because of workforce and operational capacity constraints[2]Homecare Homebase, “Home Health Staffing Shortages, Why Time, Not Hiring, Is the Real Constraint in 2026,” Homecare Homebase, hchb.com. The same source also highlighted that demand for home health and personal care aides is expected to keep increasing for years, which means access pressure is not likely to ease quickly. Administrative workload further reduces effective staffing capacity, and KFF has shown that prior authorization remains a heavy operational burden across post-acute services in Medicare Advantage. These conditions are especially damaging in rural and high-density urban markets where travel time, wage competition, and paperwork all make it harder to convert referrals into timely starts of care.

PDGM-Related Reimbursement Pressure and Rate Uncertainty

PDGM-related payment pressure is limiting how aggressively providers can expand in the United States home healthcare market. CMS finalized a net aggregate 1.3% reduction, or USD 220 million, in Medicare payments to home health agencies for CY 2026 compared with 2025. The final rule included a permanent -1.023% adjustment and a temporary -3.0% adjustment tied to the ongoing recoupment framework under. This adds to the rate pressure already seen since 2023 and makes smaller agencies more cautious about hiring, branch expansion, and technology investment. The nationwide enrollment moratorium that began in May 2026 adds another supply-side restriction, which supports further consolidation among better-capitalized incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Revenue Anchors the Market, Equipment Growth Accelerates

Services held 52.31% of the United States home healthcare market share in 2025, which kept them clearly ahead of equipment and software in total revenue. That lead reflects the recurring and labor-intensive nature of skilled nursing, therapy, hospice, personal care, and home infusion delivered in the residence. Skilled nursing remains the central service because it supports post-acute transitions, medication oversight, chronic disease management, and repeated patient contact over time. Therapy is also benefiting from the expansion of hospital-at-home and post-acute-at-home programs, which create more patients who leave acute episodes but still need rehabilitation and home follow-up.

Equipment is projected to record the fastest growth in the United States home healthcare market size at a 9.38% CAGR from 2026 to 2031, supported by rising demand for CPAP and BiPAP devices, home dialysis systems, remote multi-parameter monitors, and continuous glucose monitors. Demand is strengthening because payers and providers both have stronger incentives to intervene earlier at home and to generate more real-time patient data outside the hospital. CMS's January 2025 expansion of Medicare coverage for home dialysis in acute kidney injury added a direct reimbursement pathway that supports equipment uptake in renal care. Software remains the smallest offering type, yet it is becoming more strategic as agencies seek better documentation, referral automation, hospitalization-risk prediction, and revenue cycle control within the United States home healthcare industry. WellSky's 2025 and 2026 product releases in AI-enabled intake, medication reconciliation, ambient documentation, and personal care summarization show that digital tools are moving from support functions to operating infrastructure in the United States home healthcare market.

By Indication: Cardiovascular Dominance Masks a Renal Inflection Point

Cardiovascular disorders and hypertension held 38.24% of the United States home healthcare market share in 2025, which made them the largest indication group. Their scale reflects both disease prevalence and the wide care stack needed at home, including blood pressure monitoring, rhythm tracking, wound support after cardiac procedures, skilled nursing, and heart-failure management. These patients often require several services at once, which raises revenue intensity per patient and supports demand across both services and equipment. Diabetes and respiratory disease also remain major contributors because continuous glucose monitoring, CPAP, BiPAP, and respiratory therapy fit naturally into long-duration home management pathways.

Renal disorders are projected to post the fastest growth in the United States home healthcare market size at a 9.52% CAGR from 2026 to 2031. The main trigger is the CMS policy that took effect on January 1, 2025, which expanded Medicare-covered home dialysis services to patients with acute kidney injury and aligned payment with in-center treatment[3]Kidney News, “2025 CMS ESRD PPS Final Rule Released,” Kidney News, kidneynews.org. That decision creates a new addressable pool for dialysis providers, equipment manufacturers, and nursing teams that handle training and follow-up. It also turns what had been a clinically obvious use case into a reimbursable growth category, which materially improves the scaling outlook for renal care in the United States home healthcare market. Cancer and wound care remain smaller than cardiovascular care, yet both support high-value utilization through home infusion, compression and wound therapy equipment, and closer supervision for complex patients.

By Payer: Medicaid Dominance Faces Policy Risk, Commercial Coverage Grows Fastest

Medicaid financed 60.52% of the United States home healthcare market in 2025, which made it the clear revenue anchor among payer groups. Its dominance reflects the central place of home and community-based services in long-term support for older adults and people with disabilities who would otherwise rely more heavily on institutional care. KFF reported that 46 states maintained at least 1 Medicaid waiver for adults aged 65 and older or those with physical disabilities, which shows how strongly state waiver design underpins current access. This concentration keeps a large share of provider revenue tied to state policy design, waiver administration, and public program budgeting rather than to broad consumer choice alone.

Commercial and private insurance is projected to expand at a 9.25% CAGR in the United States home healthcare market size through 2031, which makes it the fastest-growing payer segment. Much of that growth is coming from employer-sponsored coverage and Medicare Advantage benefit designs that include more telehealth, remote monitoring, and home-based acute care pathways. AdaptHealth's five-year exclusive home medical equipment agreement covering more than 10 million members illustrates how commercial relationships are moving toward broader managed contracts rather than simple fee-for-service transactions. Providers with geographic reach, reporting capability, and operating efficiency are better placed to win these arrangements because payers increasingly want fewer vendors and tighter oversight within the United States home healthcare industry. Self-pay remains the smallest payer category and is used mainly by households that purchase private-duty services or supplemental support beyond covered benefits.

Geography Analysis

The United States home healthcare market showed its heaviest demand concentration in the South and Southeast in 2026, where aging populations, Medicaid waiver use, and post-acute care demand keep referral volumes elevated. Florida stands out as a bellwether because CMS identified South Florida as a high-fraud-risk zone when it imposed the national enrollment moratorium in May 2026, which points to both dense demand and intense oversight. Texas remains a large demand center because Medicaid-funded home and community-based services continue to support broad in-home care utilization across a large eligible population. California also contributes major scale through its population base and large provider ecosystem, which keeps it central to service capacity, equipment deployment, and payer contracting. Taken together, these conditions keep the South and adjacent Sun Belt states at the front of the United States home healthcare market through the forecast period.

The Northeast has a different growth profile, shaped less by volume alone and more by high institutional care costs, dense health system networks, and early adoption of hospital-at-home pathways. The American Hospital Association cited Mass General Brigham as reaching more than 80% of eligible patients in its service area through its hospital-at-home program, which shows how mature referral integration can lift utilization. Penn Medicine launched its Hospital at Home program in April 2026 at 2 Philadelphia hospitals and plans to expand across all Penn Medicine acute-care sites during the year. New York also remains important because large-state demand, dense provider networks, and policy scrutiny now move together in regions where home-based care is scaling quickly.

The Midwest and Mountain West operate from a smaller installed base, but they are gaining importance as rural hospital strain and technology-enabled care make treatment at home more feasible. Remote physiological monitoring and tele-homecare coordination are helping providers extend reach in lower-density markets, where travel time and staffing have historically limited access. Ohio State's hospital-at-home model reported a 9.2% 30-day readmission rate and 95% patient satisfaction in fiscal 2025, which supports wider adoption in Midwest systems. On the West Coast, Kaiser Permanente's Northern California program treats more than 1,000 patients annually at home, which reflects the region's stronger Medicare Advantage penetration and integrated care structures. These regional patterns show that the United States home healthcare market is not advancing evenly, yet the common growth factors remain payer alignment, health-system readiness, and better use of connected care tools.

Competitive Landscape

The United States home healthcare market remains fragmented across local agencies and specialized providers, even as consolidation accelerates among national platforms. Scale is becoming more valuable because reimbursement pressure, compliance demands, and technology spending are all rising at the same time. UnitedHealth's acquisition of Amedisys proceeded only after DOJ-mandated divestitures, which shows that large strategic buyers still view home care assets as critical when they improve payer reach, referral access, and care coordination depth. Kinderhook Industries completed its take-private acquisition of Enhabit in May 2026, which underlines continued private equity interest in established providers with scalable clinical footprints. This combination of fragmentation at the lower tier and consolidation at the upper tier gives the United States home healthcare market a two-speed competitive structure.

Strategy now differs clearly by operating model. Large platforms are investing in AI-enabled documentation, referral automation, cybersecurity controls, and payer contracting infrastructure so they can protect margins and manage broader geographic networks. WellSky launched new AI capabilities for referral intake in January 2026, expanded ambient documentation deployment across more than 400 home health agencies, and introduced summarization tools for personal care workflows, which together raise switching costs and improve labor productivity. Mid-sized regional operators are competing more on geographic density, clinician relationships, and specialization in higher-acuity service lines where local responsiveness still matters.

The clearest white-space remains in rural care, specialty infusion, and models that connect personal care with clinical monitoring under a single contract. NIST's December 2025 smart-home telehealth guidance raised the bar for cybersecurity and privacy governance, which will favor operators that manage connected devices and home-based data through standardized systems rather than scattered point solutions. Penn Medicine's April 2026 launch also shows that health systems which once hesitated under annual waiver uncertainty are now committing real operating infrastructure to hospital-level care at home. AdaptHealth's five-year exclusive home medical equipment agreement covering more than 10 million members is another example of how payer and provider relationships are shifting toward broader managed-risk structures. As a result, the United States home healthcare market is likely to reward organizations that combine compliance strength, clinical breadth, digital workflow control, and payer relevance in a single operating model.

United States Home Healthcare Industry Leaders

Maxim Healthcare Services

CenterWell Home Health

Amedisys (UnitedHealth Group)

Enhabit Inc.

AccentCare Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: CMS implemented a nationwide six-month moratorium on all new Medicare enrollments for home health agencies and hospices, effective May 13, 2026, as part of Vice President Vance's Anti-Fraud Task Force. The action covers all states, territories, and DC, bars new HHA branch expansions, and may be extended in six-month increments. Existing enrolled agencies are unaffected, but the moratorium immediately constrains supply growth and concentrates competitive advantage in current providers.

- April 2026: Penn Medicine officially launched its Hospital at Home program at the Hospital of the University of Pennsylvania and Penn Presbyterian Medical Center, with a phased expansion planned to all Penn Medicine acute-care hospitals through 2026. The launch followed four days of clinical simulation exercises and represents one of the larger academic health system hospital-at-home programs in the Mid-Atlantic region.

United States Home Healthcare Market Report Scope

As per the scope of the report, Home healthcare refers to medical and supportive services provided to individuals in their own homes to manage illness, recover from surgery, or maintain health and well-being. These services are delivered by healthcare professionals such as nurses, therapists, and home health aides, and can include medical treatments, medication management, physical therapy, and assistance with daily activities.

The segmentation for the United States home healthcare market is categorized by offering, indication, and payer. By offering, the market includes equipment, services, and software platforms. The equipment segment is further divided into therapeutic equipment, diagnostic and monitoring equipment, and mobility and daily living assist equipment. Therapeutic equipment includes insulin delivery devices, home IV pumps and infusion equipment, home dialysis equipment, ventilators and nebulizers, CPAP and BiPAP devices, and compression and wound therapy equipment. Diagnostic and monitoring equipment comprises blood-glucose monitors and CGM, blood pressure monitors, pulse oximeters, ECG and Holter monitors, digital thermometers, and multi-parameter remote monitoring devices. Mobility and daily living assist equipment includes wheelchairs, walkers and rollators, mobility scooters, patient lifts and transfer aids, and home medical furniture and safety aids. The services segment covers skilled nursing, physical therapy, occupational therapy, speech therapy, hospice and palliative care, personal care or home health aide services, respiratory therapy, home infusion services, and tele-homecare or virtual care coordination.

The software platforms segment includes agency management and scheduling, clinical or EHR platforms, remote patient monitoring platforms, and revenue cycle and referral management. By indication, the market is segmented into cardiovascular disorders and hypertension, diabetes, respiratory diseases, renal disorders, cancer, wound care, and other indications. By payer, the market is divided into Medicare, Medicaid, commercial or private insurance, self-pay or out-of-pocket, and others. For each segment, the market size and forecast are provided in terms of value (USD).

| Equipment | Therapeutic Equipment | Insulin Delivery Devices |

| Home IV Pumps & Infusion Equipment | ||

| Home Dialysis Equipment | ||

| Ventilators & Nebulizers | ||

| CPAP & BiPAP Devices | ||

| Compression & Wound Therapy Equipment | ||

| Diagnostic & Monitoring Equipment | Blood-Glucose Monitors & CGM | |

| Blood Pressure Monitors | ||

| Pulse Oximeters | ||

| ECG & Holter Monitors | ||

| Digital Thermometers | ||

| Multi-parameter Remote Monitoring Devices | ||

| Mobility & Daily Living Assist Equipment | Wheelchairs | |

| Walkers & Rollators | ||

| Mobility Scooters | ||

| Patient Lifts & Transfer Aids | ||

| Home Medical Furniture & Safety Aids | ||

| Services | Skilled Nursing | |

| Physical Therapy | ||

| Occupational Therapy | ||

| Speech Therapy | ||

| Hospice & Palliative Care | ||

| Personal Care / Home Health Aide Services | ||

| Respiratory Therapy | ||

| Home Infusion Services | ||

| Tele-homecare / Virtual Care Coordination | ||

| Software Platforms | Agency Management & Scheduling | |

| Clinical / EHR Platforms | ||

| Remote Patient Monitoring Platforms | ||

| Revenue Cycle & Referral Management | ||

| Cardiovascular Disorders & Hypertension |

| Diabetes |

| Respiratory Diseases |

| Renal Disorders |

| Cancer |

| Wound Care |

| Other Indications |

| Medicare |

| Medicaid |

| Commercial / Private Insurance |

| Self-pay / Out-of-pocket |

| Others |

| By Offering | Equipment | Therapeutic Equipment | Insulin Delivery Devices |

| Home IV Pumps & Infusion Equipment | |||

| Home Dialysis Equipment | |||

| Ventilators & Nebulizers | |||

| CPAP & BiPAP Devices | |||

| Compression & Wound Therapy Equipment | |||

| Diagnostic & Monitoring Equipment | Blood-Glucose Monitors & CGM | ||

| Blood Pressure Monitors | |||

| Pulse Oximeters | |||

| ECG & Holter Monitors | |||

| Digital Thermometers | |||

| Multi-parameter Remote Monitoring Devices | |||

| Mobility & Daily Living Assist Equipment | Wheelchairs | ||

| Walkers & Rollators | |||

| Mobility Scooters | |||

| Patient Lifts & Transfer Aids | |||

| Home Medical Furniture & Safety Aids | |||

| Services | Skilled Nursing | ||

| Physical Therapy | |||

| Occupational Therapy | |||

| Speech Therapy | |||

| Hospice & Palliative Care | |||

| Personal Care / Home Health Aide Services | |||

| Respiratory Therapy | |||

| Home Infusion Services | |||

| Tele-homecare / Virtual Care Coordination | |||

| Software Platforms | Agency Management & Scheduling | ||

| Clinical / EHR Platforms | |||

| Remote Patient Monitoring Platforms | |||

| Revenue Cycle & Referral Management | |||

| By Indication | Cardiovascular Disorders & Hypertension | ||

| Diabetes | |||

| Respiratory Diseases | |||

| Renal Disorders | |||

| Cancer | |||

| Wound Care | |||

| Other Indications | |||

| By Payer | Medicare | ||

| Medicaid | |||

| Commercial / Private Insurance | |||

| Self-pay / Out-of-pocket | |||

| Others | |||

Key Questions Answered in the Report

What is the 2026 size and 2031 outlook for United States home healthcare?

The United States home healthcare market stands at USD 131.36 billion in 2026 and is forecast to reach USD 200.73 billion by 2031 at a CAGR of 8.85%.

Why do services still lead revenue in home healthcare across the United States?

Services held 52.31% of revenue in 2025 because skilled nursing, therapy, hospice, personal care, and home infusion require recurring labor and ongoing reimbursement support.

Which indication is growing fastest in United States home healthcare?

Renal disorders are the fastest-growing indication, with a 9.52% CAGR through 2031, supported by Medicare coverage expansion for home dialysis in acute kidney injury.

How important is Medicaid to home healthcare funding in the United States?

Medicaid accounted for 60.52% of market revenue in 2025, making it the largest funding channel because home and community-based services remain central to long-term support delivery.

How are hospital-at-home programs changing demand for home-based care?

They are expanding demand for skilled nursing, rehabilitation, monitoring, and equipment by shifting selected acute and post-acute episodes into the home. CMS waiver extension through 2030 gives health systems more confidence to invest.

What are the biggest risks facing providers through 2031?

The main risks are workforce shortages, PDGM-related payment pressure, cybersecurity demands tied to connected care, and the May 2026 Medicare enrollment moratorium that limits new agency growth.

Page last updated on: