Ambulatory Healthcare Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.4 Billion |

| Market Size (2031) | USD 5.81 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

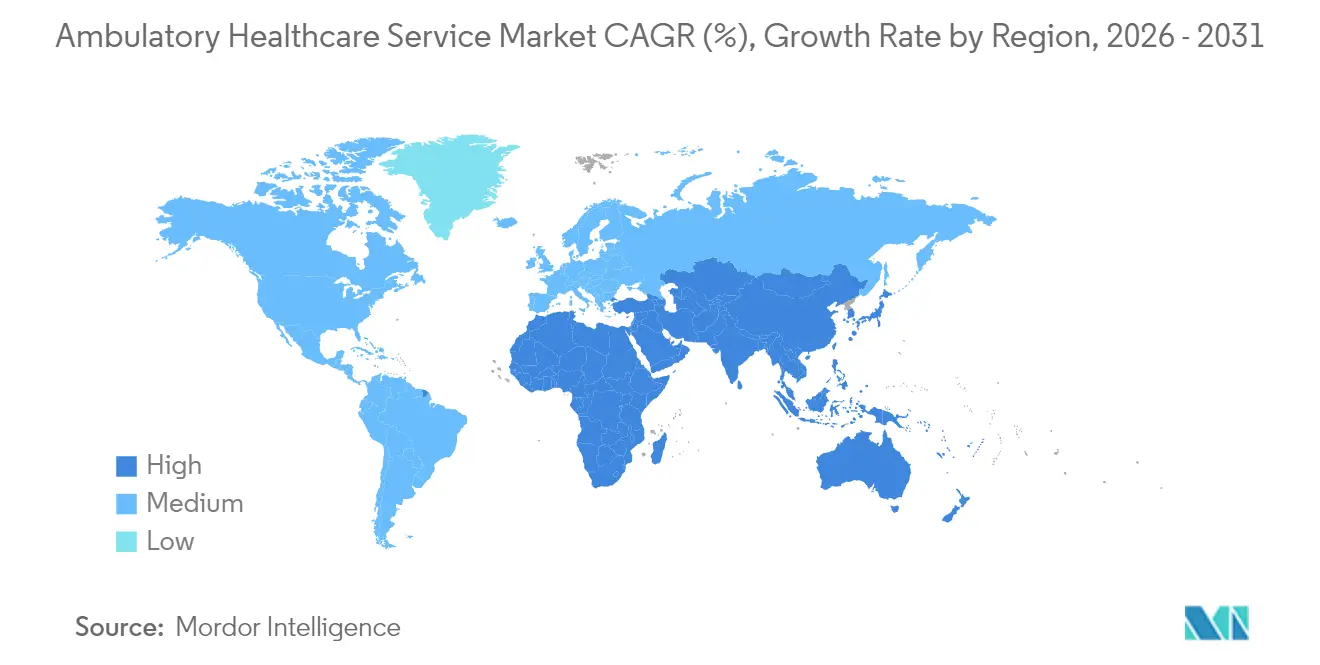

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambulatory Healthcare Service Market Analysis by Mordor Intelligence

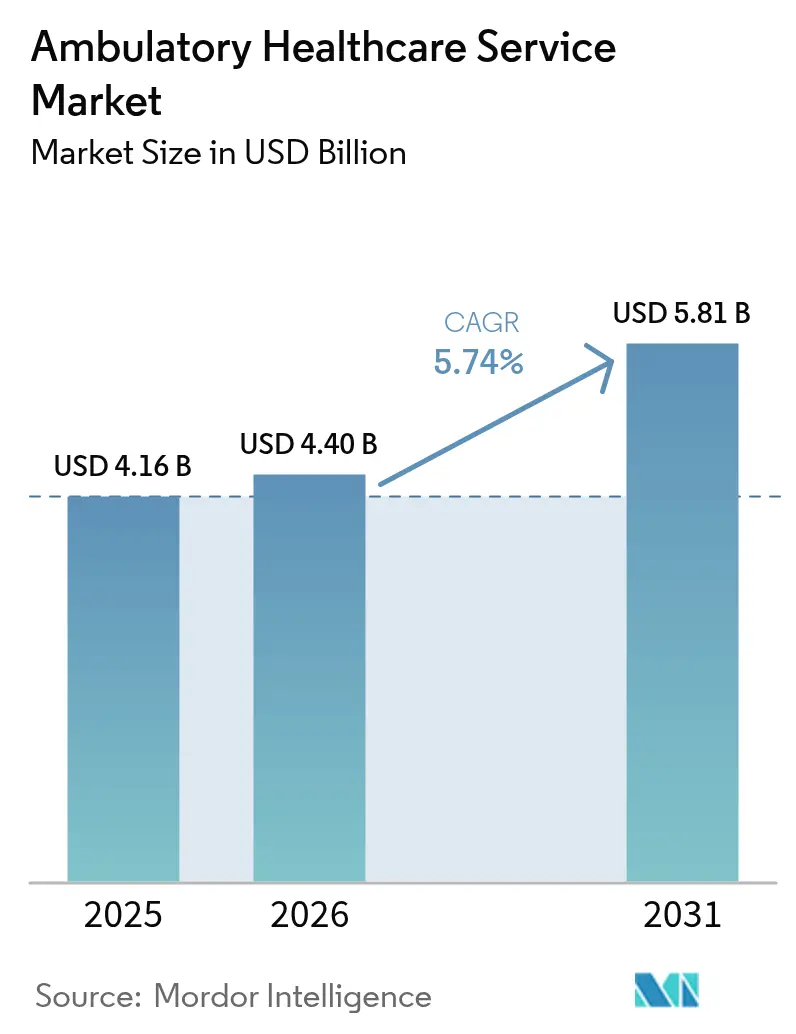

The Ambulatory Healthcare Service Market size was valued at USD 4.16 billion in 2025 and estimated to grow from USD 4.40 billion in 2026 to reach USD 5.81 billion by 2031, at a CAGR of 5.74% during the forecast period (2026-2031).

Expansion is propelled by the steady shift of procedures from inpatient hospitals to cost-efficient outpatient facilities, stronger payer incentives for value-based care, and rising demand for chronic-disease management. North America continues to anchor global revenues on the back of mature reimbursement policies, while Asia-Pacific records the most rapid uptake as governments scale outpatient infrastructure. Technology that supports minimally invasive surgeries, real-time analytics, and remote monitoring further widens the clinical scope of ambulatory centers. Concurrently, labor shortages, cyber threats, and rising urban real-estate costs temper growth momentum by adding operational risk and capital pressure.

Key Report Takeaways

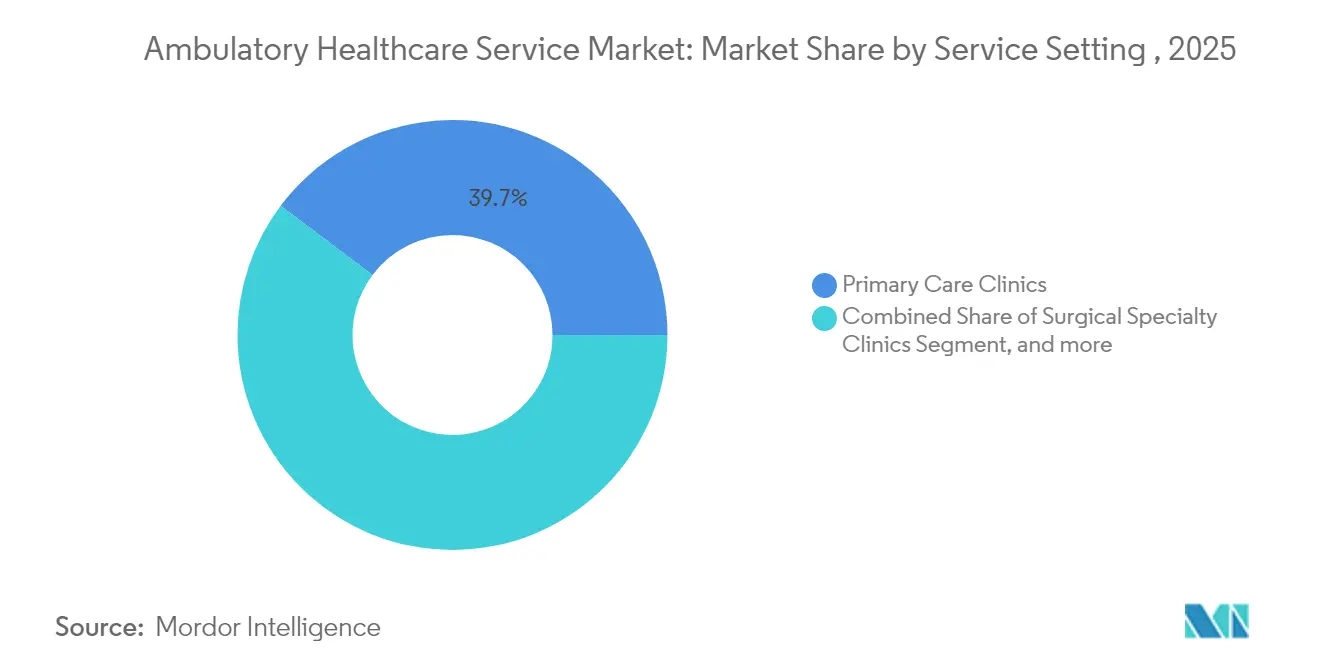

- By service setting, primary care clinics held 39.74% of the ambulatory healthcare service market share in 2025, while telehealth and virtual clinics are projected to expand at a 7.62% CAGR through 2031.

- By specialty, gastroenterology led with 25.02% revenue share in 2025; oncology is forecast to grow at an 8.42% CAGR to 2031.

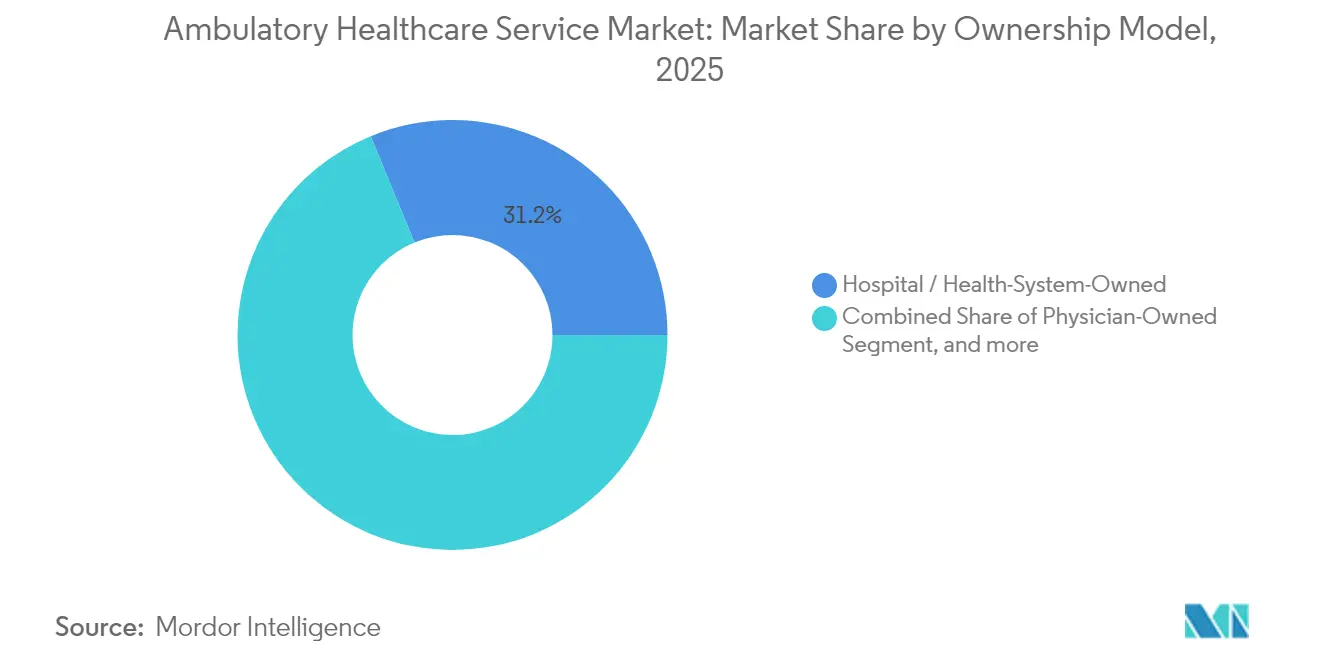

- By ownership model, hospital- and health-system-owned sites accounted for 31.21% share of the ambulatory healthcare service market size in 2025; physician-owned facilities are poised for a 9.33% CAGR between 2026-2031.

- By geography, North America commanded 43.12% of global revenues in 2025, whereas Asia-Pacific registers the fastest regional CAGR at 10.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Ambulatory Healthcare Service Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Chronic Diseases and a Growing Elderly Population | +1.8% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Technological Innovations Enabling Shift Toward Minimally Invasive Surgeries | +1.2% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Policy Initiatives Promoting Favorable Reimbursement and Site-of-Care Mandates | +0.9% | North America primarily, selective EU markets | Short term (≤ 2 years) |

| Entry of Retail Giants and Big-Tech Players Accelerating Digital Innovation | +0.7% | North America & APAC core, spill-over to EU | Medium term (2-4 years) |

| Hybrid ASC-OBL Facilities Supporting Migration of Cardiovascular Procedures | +0.5% | North America, early adoption in select EU markets | Medium term (2-4 years) |

| Adoption of Value-Based Care and Bundled Payment Models | +0.6% | North America & EU, pilot programs in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases and a Growing Elderly Population

Demand for the ambulatory healthcare service market deepens as multimorbidity rates climb among seniors who prefer community-based care. Payers now tie 75% of home- and community-care reimbursements to government programs, embedding outpatient delivery in national health strategies. Community clinics respond by enlarging chronic-disease panels, integrating nutrition services, and deploying point-of-care diagnostics that shorten referral loops. Population-health contracts increasingly include performance metrics for hypertension, diabetes, and COPD management conducted in ambulatory settings. These patterns confirm that outpatient care is becoming a structural component of health-system capacity rather than a discretionary adjunct.

Technological Innovations Enabling Shift Toward Minimally Invasive Surgeries

Advances in robotics, imaging, and AI reduce incision size, operating-room time, and recuperation periods, allowing procedures once limited to hospital theaters to migrate to ambulatory surgery centers. Photon-counting CT and digital SPECT scanners shrink scan sequences and radiation exposure, aligning with outpatient throughput targets. Cardiovascular interventions such as atherectomy and peripheral stenting are increasingly reimbursed for ambulatory venues, expanding procedure mix. Automated image-analysis tools offset shortages of radiologists by triaging scans and flagging anomalies for rapid review. Collectively, these technologies help facilities boost case volumes without proportional increases in clinical manpower.

Policy Initiatives Promoting Favorable Reimbursement and Site-of-Care Mandates

For CY 2025, Medicare boosted ASC payment rates by 2.9%, while updates for hospital outpatient departments remained modest, sharpening the cost differential in favor of ambulatory sites.[1]Centers for Medicare & Medicaid Services, “Advanced Primary Care Management Services Summary,” cms.gov The Physician Fee Schedule adds Advanced Primary Care Management codes that decouple chronic-care billing from time-based documentation, making outpatient workflows more financially viable. Telehealth reimbursement remains extended through September 2025, and bipartisan proposals aim to cement remote-care parity, giving virtual ambulatory clinics durable revenue streams. Several U.S. states have relaxed certificate-of-need laws, enabling faster build-outs of imaging centers and procedure suites. These synchronized measures accelerate procedure migration and incentivize new entrants.

Entry of Retail Giants and Big-Tech Players Accelerating Digital Innovation

Consumer-facing conglomerates deploy AI scribes that cut clinical-note time by 40%, allowing physicians to handle greater visit volumes. Cloud-native EHR modules integrate pharmacy, diagnostics, and remote-monitoring data, creating frictionless hand-offs between bricks-and-mortar sites and virtual platforms. Industry analysts project 25-30% of U.S. ambulatory visits to occur via telemedicine by 2026, with behavioral health commanding the highest mix. Digital retail clinics co-locate urgent care, labs, and chronic-care programs in storefront footprints, challenging traditional primary-care economics. Early adopters secure first-mover brand equity and data networks that create high switching costs for consumers.

Restraints Impact Analysis of Ambulatory Healthcare Service Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Workforce Shortages and Increasing Clinician Burnout | -1.4% | Global, most acute in North America and EU | Short term (≤ 2 years) |

| Rising Cybersecurity Threats and Fragmented Data Systems | -0.8% | Global, highest impact in digitally advanced markets | Medium term (2-4 years) |

| High Real Estate Costs in Urban and High-Growth Corridors Pose Barriers to ASC Expansion | -0.6% | North America & EU urban centers, select APAC metros | Medium term (2-4 years) |

| Operational Complexity from Managing Multispecialty Practices | -0.4% | Global, particularly in fragmented healthcare systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Workforce Shortages and Increasing Clinician Burnout

A projected deficit of up to 139,000 physicians by 2033 tightens labor supply, with only 42.2% of physicians still in private practice as employment shifts toward hospital systems.[2]American Hospital Association, “Health Care Cybersecurity Advisory,” aha.org Burnout rates climb as clinicians juggle high visit counts and electronic documentation, prompting early retirement and reduced hours. Ambulatory centers struggle to staff evening and weekend clinics, limiting throughput during peak periods. Rural areas face compounded shortages because telehealth licensing requirements vary by state, slowing specialist deployment. Workforce gaps elevate salary expenses, pressuring margins that are already thinner than hospital counterparts.

Rising Cybersecurity Threats and Fragmented Data Systems

Healthcare recorded 386 significant cyber incidents in 2024, with average outage costs exceeding USD 2 million per day. The Change Healthcare breach exposed 190 million patient records, underscoring system-wide vulnerabilities. Smaller ambulatory providers often lack mature security operations centers, making them prime ransomware targets. Fragmented data across practice management systems complicates the deployment of end-to-end encryption and unified threat detection. High breach-remediation expenses frequently exceed annual IT budgets, forcing facilities to divert funds from clinical upgrades to cybersecurity safeguards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Ambulatory Healthcare Service Market Segment Analysis

By Service Setting:

Primary Care Anchors GrowthPrimary care clinics generated the largest revenue stream, accounting for 39.74% of the ambulatory healthcare service market in 2025. They serve as gatekeepers for disease prevention, prescription renewals, and referrals, positioning them as indispensable nodes in population-health programs. Continuity of care fosters strong patient relationships, leading to higher adherence and lower downstream costs. Investment in advanced triage tools and chronic-care dashboards enables clinics to manage rising multimorbidity without proportional physician headcount. Telehealth and virtual clinics, though smaller in absolute terms, are on track for a 7.62% CAGR through 2031, reflecting consumer preference for convenient, on-demand access.

Rapid virtual uptake brings fresh competition and raises expectations for 24/7 availability, pushing traditional practices to adopt hybrid models. Urgent care centers, numbering more than 14,000, continue to relieve emergency-room congestion by handling non-life-threatening episodes. Diagnostic imaging hubs prosper as payers shift high-cost scans out of hospital radiology departments. In parallel, home-health agencies leverage remote vitals monitoring to extend the reach of clinicians, particularly for post-acute recovery and palliative support. The segment mosaic underscores how diversified points of care jointly reinforce the ambulatory healthcare service market flow of patients and revenue.

By Specialty:

Gastroenterology Leads, Oncology AcceleratesGastroenterology captured 25.02% of specialty revenue in 2025, aided by procedural efficiencies that allow same-day discharge after colonoscopy or endoscopic retrograde cholangiopancreatography. Bundled-payment programs reward high-volume centers that maintain low complication rates, supporting continuous scale gains. Robust demand also stems from mandated colorectal-cancer screening guidelines beginning at age 45, widening addressable volumes. Oncology, though smaller, is predicted to log the fastest 8.42% CAGR through 2031 as immunotherapy infusions and oral oncolytics migrate to outpatient infusion suites. Favorable safety profiles and shorter chair-time make outpatient cancer care clinically practical and economically compelling.

Ophthalmology sustains momentum via cataract and LASIK procedures, which are highly standardized and benefit from rapid turnover. Orthopedics expands through minimally invasive joint repair with enhanced recovery pathways that minimize inpatient stays. Cardiovascular specialties gain lift from CMS approval of additional cardiac interventions in ambulatory surgery centers, illustrating policy leverage in shaping service mix. Pain management, ENT, dermatology, and urology continue building volumes by integrating image-guided modalities and regenerative therapies that meet rising consumer expectations for quick recovery. Specialty diversification enhances risk mitigation and stabilizes overall revenues within the ambulatory healthcare service market.

By Ownership Model:

Physician Independence ResurgesHospital- and health-system-owned outpatient networks held 31.21% of revenue in 2025, benefiting from referral integration, brand recognition, and centralized purchasing power. These entities capitalize on scale when negotiating supply contracts and payer agreements, preserving margin despite reimbursement headwinds. Yet physician-owned centers are forecast to grow at 9.33% CAGR through 2031, indicating renewed appetite for professional autonomy and equity upside. Clinicians embrace ownership to innovate around scheduling, staffing, and patient-experience design that larger systems sometimes standardize.

Private-equity-backed platforms accelerate roll-up strategies by injecting capital and managerial discipline, often clustering facilities in high-growth urban corridors. Joint-venture models join hospital capital with physician governance, sharing risk while aligning incentives for efficient throughput. Regulatory relaxations in several states are lowering hurdles for independent builds, encouraging new entrants. Competitive tension between scale and personalization continues to shape the ambulatory healthcare service market narrative. Ultimately, survival hinges on an owner’s ability to balance capital access, clinician engagement, and technology adoption.

Geography Analysis

North America Ambulatory Healthcare Service Market

North America controlled 43.12% of global ambulatory revenues in 2025, underpinned by expansive payer coverage, favorable site-of-service differentials, and a mature supply of more than 14,000 urgent care centers. The United States benefits from a 2.9% Medicare payment bump for ASCs, creating immediate cash-flow lift, while Canada’s provincial reforms reward community-based chronic-disease clinics. Mexico’s medical-tourism clusters generate incremental procedure volume that fortifies regional share. Telehealth adoption now touches 23% of encounters, a signal that digital pathways are firmly embedded in the ambulatory healthcare service market.

APAC Ambulatory Healthcare Service Market

Asia-Pacific posts a leading 10.18% CAGR by 2031 as governments fast-track outpatient construction to relieve public-hospital congestion. Singapore’s integrated surgery centers demonstrate best-in-class throughput, China prioritizes domestic production of minimally invasive devices, and Japan subsidizes tele-rehabilitation for seniors. India’s insurance-expansion policies and medical-tourism inflows also funnel capital into multispecialty ambulatory hubs. Demographic aging in the region ensures sustainable demand for cardiovascular, ophthalmic, and orthopedic day surgeries.

EMEA and South America Ambulatory Healthcare Service Market

Europe exhibits steady growth as national health systems tighten budgets and encourage shift-left initiatives. Germany’s gynecology procedures now occur 98% in private free-standing units, and EU-wide value-based frameworks tie reimbursement to care-quality metrics that outpatient sites can meet efficiently. Adoption of teleradiology mitigates radiologist shortages, while relaxed cross-border directives ease patient flow within the bloc. Emerging markets in the Middle East, Africa, and South America invest in private outpatient clusters that complement often overstretched public hospitals, extending the global footprint of the ambulatory healthcare service market.

Competitive Landscape

Competitive intensity is moderate, with fragmentation by service line creating both consolidation plays and niche opportunities. In urgent care, private-equity firms already hold over 30% share in more than 100 U.S. metropolitan areas, illustrating the speed at which institutional capital can aggregate dispersed assets. Large health systems pursue horizontal expansion to retain referrals and capture pre- and post-acute margins, often bolting surgery centers onto existing campus footprints. Physician-led groups differentiate through patient-experience metrics and specialty depth, safeguarding their positions even as capital-heavy players scale.

Digital competencies emerge as a decisive edge. Facilities deploying AI documentation platforms have reported 40% reductions in clerical time, freeing clinicians for extra visits or complex consultations. Cyber-preparedness also influences partnership decisions, as payers and referring providers now screen facilities for security posture before network inclusion. Low-acuity visit sites face encroachment from retail clinics whose extended hours and transparent pricing attract volume. Conversely, high-acuity ambulatory surgery centers defend turf by offering procedural breadth and anesthesia capabilities beyond retail incumbents.

Regulatory moves shape rivalry. CMS expansion of ASC-covered cardiac and orthopedic codes opens lucrative volumes, intensifying competition among multispecialty centers. States diluting certificate-of-need oversight accelerate imaging-center proliferation, tightening spread margins. Yet untapped rural corridors still lack basic outpatient infrastructure, offering whitespace for tele-enabled models. Overall, the ambulatory healthcare service market rewards players that synchronize clinical excellence, cost efficiency, and digital agility.

Ambulatory Healthcare Service Industry Leaders

Medical Facilities Corporation

Surgery Partners

Aspen Healthcare

NueHealth

Sheridan Healthcare

- *Disclaimer: Major Players sorted in no particular order

Ambulatory Healthcare Service Market Companies Covered in this Report

- Aspen Pharmacare

- Healthway Medical Group

- Medical Facilities

- NueHealth

- Envision / Sheridan Healthcare

- Surgery Partners

- SCA Health (Surgical Care Affiliates)

- Terveystalo Healthcare

- United Surgical Partners International (USPI)

- AmSurg

- Tenet Healthcare

- HCA Healthcare

- Community Health Systems

- TeamHealth

- FastMed Urgent Care

- NextCare Urgent Care

- One Medical

- Oak Street Health

- CVS MinuteClinic

- DaVita Kidney Care

- Kaiser Permanente

Recent Industry Developments in Ambulatory Healthcare Service Market

- June 2025: Ascension Health nears completion of USD 3.9 billion AmSurg acquisition, significantly expanding its ambulatory surgery center network and outpatient services capacity. The transaction reflects Ascension's strategic focus on ambulatory care following an 18.1% increase in surgery visits year-over-year.

- January 2025: NeueHealth becomes private following USD 1.3 billion acquisition by New Enterprise Associates affiliate, with stockholders receiving USD 7.33 per share representing a 70% premium. The transaction includes a USD 150 million loan facility from Hercules Capital to support continued growth in value-based care delivery.

- January 2025: Concentra announces USD 265 million acquisition of Nova Medical Centers, expanding its occupational health network to over 770 centers across 42 states. The deal enhances Concentra's position as the largest occupational health provider in the United States.

- January 2024: Ardent Health acquires 18 NextCare urgent care clinics across New Mexico and Oklahoma, strengthening its ambulatory operations in these key markets. The acquisition follows previous urgent care center purchases in East Texas and Kansas during 2024

- January 2024: The Indian Health Service (IHS), under the U.S. Department of Health and Human Services, allocated USD 55 million in funding. This funding was distributed among 15 tribes and tribal organizations. It is part of the Small Ambulatory Program, a competitive initiative that aims to support the development, expansion, or modernization of small ambulatory health care facilities.

Ambulatory Healthcare Service Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the ambulatory health care service market as all revenue earned from organized, same-day medical services delivered in outpatient venues such as primary-care clinics, surgical specialty centers, freestanding emergency departments, diagnostic imaging suites, and virtual visit platforms, while medicines or devices sold separately are excluded. According to Mordor Intelligence, the baseline year 2025 market is valued at USD 4.16 billion and is forecast to reach USD 5.51 billion by 2030.

Scope exclusion: home-based nursing, inpatient hospital wards, and long-term residential facilities remain outside our frame.

Segments Covered in This Report

- By Service Setting

- Primary Care Clinics

- Surgical Specialty Clinics

- Urgent Care Centers

- Freestanding Emergency Departments

- Diagnostic Imaging Centers

- Specialty Clinics

- Home Healthcare Agencies

- Telehealth & Virtual Clinics

- By Specialty

- Ophthalmology

- Orthopedics

- Gastroenterology

- Cardiovascular

- Pain Management

- Dermatology

- ENT

- Oncology

- Others

- By Ownership Model

- Physician-Owned

- Hospital / Health-System-Owned

- Corporate / Private-Equity-Owned

- Joint-Ventures

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts held structured calls and surveys with administrators of multi-site clinic chains, payer medical directors, equipment distributors, and regional health regulators across North America, Europe, and Asia-Pacific. These dialogues clarified real-world case mix, average reimbursement, and adoption pacing of virtual consult models, enabling us to fill data gaps and challenge desk-research assumptions.

Desk Research

We begin with authoritative public datasets, including OECD HealthStats, WHO Global Health Expenditure, CMS Outpatient Prospective Payment System files, American Hospital Association facility counts, and peer-reviewed journals on procedure migration trends, to chart patient volumes and tariff corridors. Company filings and investor decks provide cost-per-case clues, while news feeds from Dow Jones Factiva, plus financial snapshots on D&B Hoovers, keep ownership shifts visible.

Further depth comes from trade associations such as the Ambulatory Surgery Center Association, regional payer bulletins, customs import logs for single-use surgical kits, and patent landscaping via Questel to gauge technology diffusion. This list is illustrative; many other secondary inputs supported data checks and narrative clarity.

Market-Sizing & Forecasting

A blended top-down view reconstructs outpatient activity from national encounter counts and payer spend before being cross-checked with sampled average selling price times volume roll-ups for surgical, diagnostic, and urgent-care episodes.

Key variables feeding the model include: procedure shift rate from inpatient to outpatient settings, chronic-disease prevalence that dictates revisit frequency, payer fee-schedule revisions by CPT code, clinic bed-equivalent capacity additions, and telehealth visit penetration.

Forecasts deploy multivariate regression with scenario analysis, letting elasticity of each driver adjust under conservative, base, and accelerated adoption cases.

Gaps in bottom-up estimates, especially in emerging markets, are bridged using regional utilization proxies aligned to GDP-per-capita health spend bands.

Data Validation & Update Cycle

Outputs undergo variance checks against sentinel metrics (e.g., ASC visit ratios, CMS spend trends), senior-analyst peer review, and client-side sense testing. Reports refresh yearly, and material market events trigger interim model updates before delivery.

How Mordor Intelligence's Ambulatory Healthcare Service Market Size Compares to Other Published Estimates

Published figures often diverge because firms select different service mixes, geographic breadth, and refresh rules. Our disciplined scope focused strictly on organized outpatient facilities and verified tariff streams, plus annual model tuning, keeps estimates tight and traceable.

Key gap drivers versus other publishers include their inclusion of hospital outpatient departments, wellness programs, or home-health revenues, differing currency bases, and less frequent validation with frontline operators.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.16 billion (2025) | Mordor Intelligence | |

| USD 828.1 billion (2023) | Global Consultancy A | Broad service basket covering primary offices, hospital outpatient wings, and diagnostics; largely tariff-top aggregation with limited primary checks |

| USD 881.27 billion (2024) | Industry Journal B | Includes wellness and rehab revenue, mixed currency conversion, and infrequent dataset refresh |

In sum, the smaller yet focused baseline from Mordor Intelligence stems from a clearly bounded scope, double-validated assumptions, and an annual refresh cadence, offering decision-makers a balanced, reproducible yardstick for strategic planning.

Key Questions Answered in the Report

What is the current value of the ambulatory healthcare service market?

The market stands at USD 4.40 billion in 2026 and is projected to reach USD 5.81 billion by 2031.

Which service setting holds the largest share?

Primary care clinics command 39.74% of 2025 revenues, reflecting their central role in care coordination.

Which specialty is expanding fastest?

Oncology services show the highest forecast growth at an 8.42% CAGR through 2031 as more cancer therapies move to outpatient settings.

Why is Asia-Pacific the fastest-growing region?

Rapid infrastructure build-out, supportive government policies, and demographic aging drive the region’s 10.18% CAGR.

How are workforce shortages affecting growth?

Physician deficits and clinician burnout reduce available staffing, subtracting an estimated 1.4 percentage points from the market’s CAGR.

What strategies help providers stay competitive?

Successful operators combine disciplined cost management, technology adoption such as AI documentation, and targeted expansion into underserved geographies.

Page last updated on: