US Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

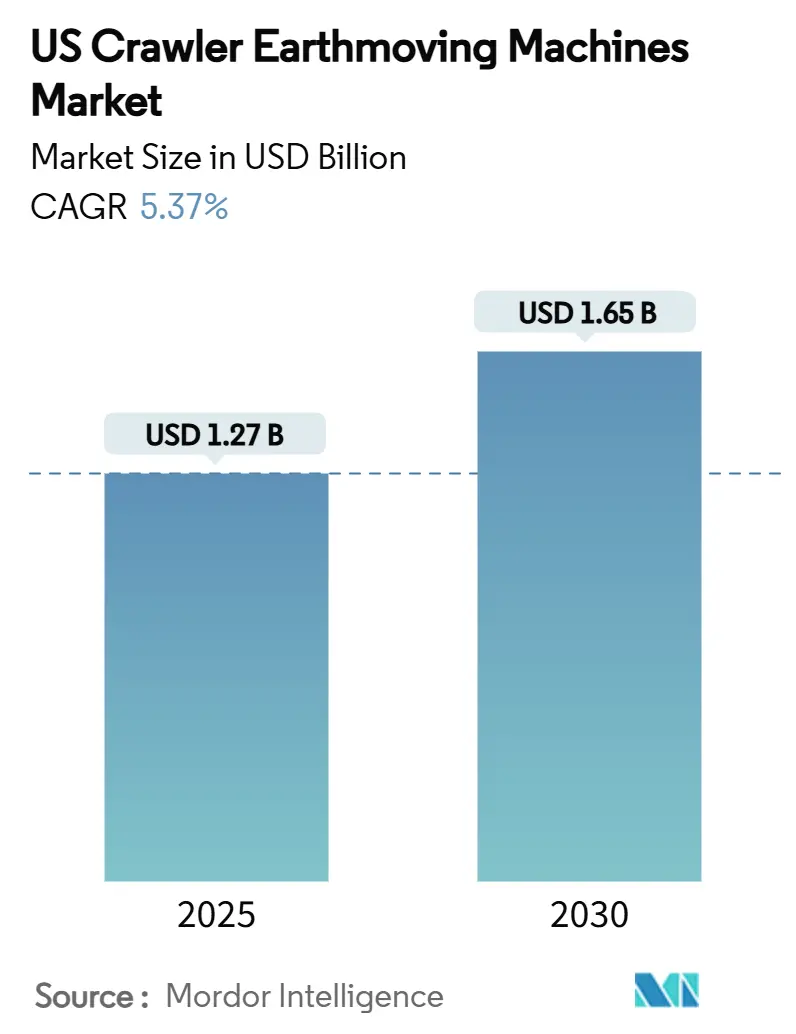

| Market Size (2025) | USD 1.27 Billion |

| Market Size (2030) | USD 1.65 Billion |

| Growth Rate (2025 - 2030) | 5.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The US crawler earthmoving machines market size is pegged at USD 1.27 billion in 2025 and is projected to reach USD 1.65 billion by 2030, reflecting a 5.37% CAGR over the forecast period. Market expansion is anchored in federal infrastructure legislation, rising wildfire-mitigation spending, and accelerating adoption of electric and hybrid drivetrains. Contractors continue to favor multi-functional excavators that lower fleet complexity, while rental penetration rises in response to labor scarcity and higher borrowing costs. OEM investment in zero-emission powertrains and predictive telematics differentiates product offerings, even as steel price volatility and Tier-4 compliance costs present profit headwinds. Competitive intensity is shaped by supply-chain realignment toward domestic sourcing and by strategic partnerships that hasten technology commercialization.

Key Report Takeaways

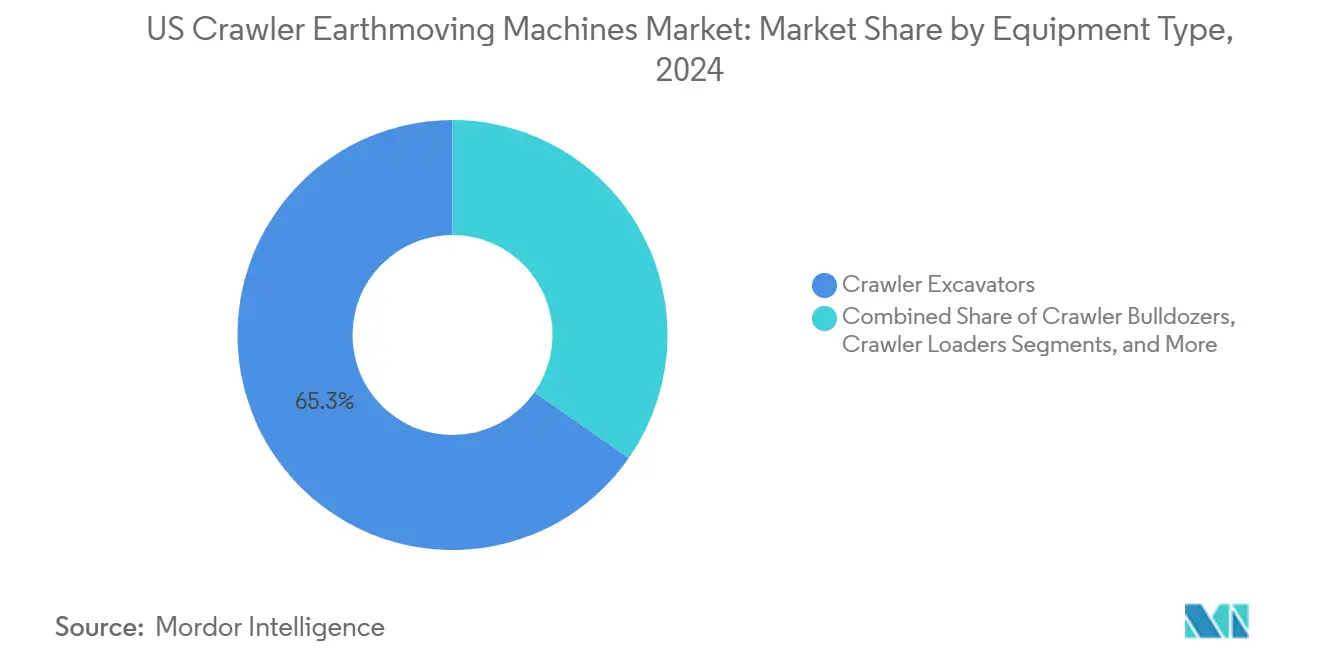

- By equipment type, crawler excavators led with 65.33% revenue share in 2024, while compact tracked loaders and skid-steers are projected to expand at 6.15% CAGR through 2030.

- By propulsion, internal combustion engines accounted for an 85.41% share in 2024, whereas electric and hybrid variants are forecast to grow at a 7.83% CAGR.

- By engine power output, the 100–200 HP category commanded 48.19% share in 2024; below 100 HP machines exhibit the fastest growth at 5.81% CAGR.

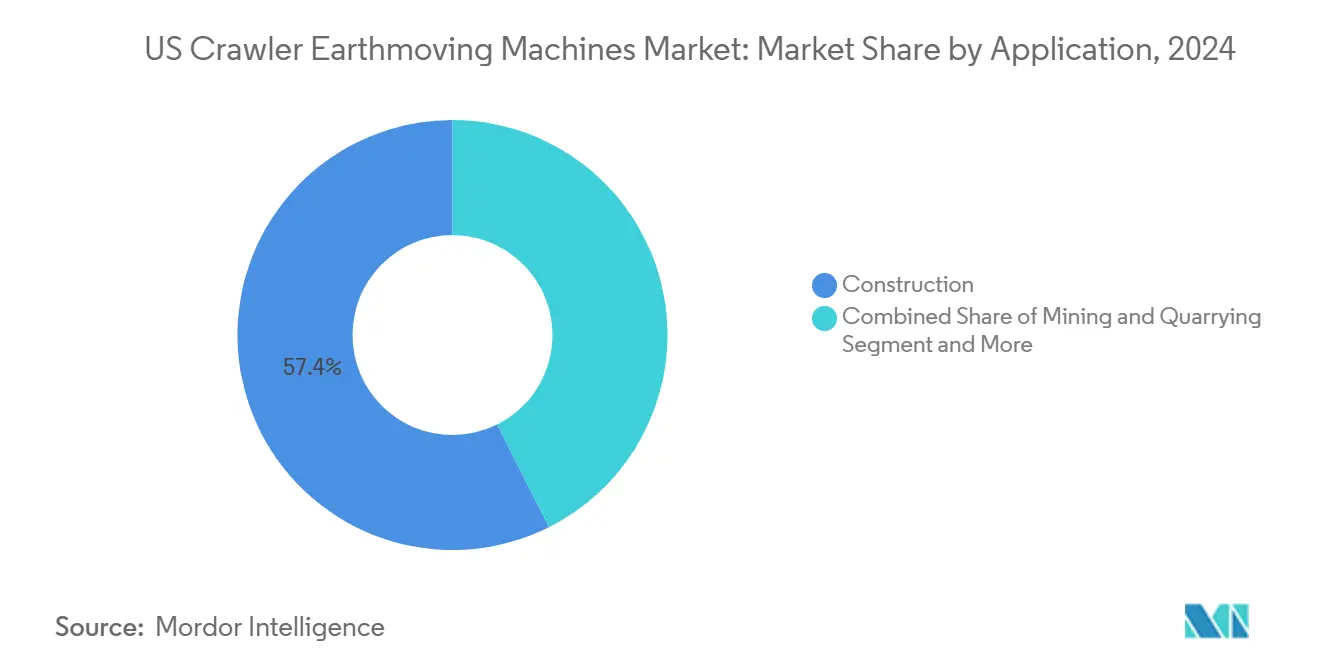

- By application, construction captured a 57.44% share in 2024 and is advancing at a 6.84% CAGR.

- By distribution channel, authorized dealers held a 72.35% share in 2024, while rental and leasing firms are anticipated to rise at a 7.26% CAGR.

- By geography, the South region controlled a 36.72% share in 2024, and the West is growing at a 6.11% CAGR.

United states contributes to a system defined not by any single country or region but by the interaction of many. The global crawler earthmoving machines market data by Mordor Intelligence represents that combined structure.

US Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Boom in Federal Infrastructure Funding (IIJA, IRA) | +1.8% | National; South and West lead | Long term (≥ 4 years) |

| Accelerated Urban-Renewal Projects in Tier-2 Cities | +0.9% | Midwest and Northeast core | Medium term (2-4 years) |

| Rise of Electrified and Hybrid Excavator Models | +0.7% | West Coast and Northeast | Long term (≥ 4 years) |

| Labor Scarcity Driving Equipment-Rental Penetration | +0.6% | National; South and West acute | Short term (≤ 2 years) |

| Digitized Job-Site Management and Telematics Integration | +0.5% | National, urban focus | Medium term (2-4 years) |

| Forestry Wildfire-Mitigation Incentives | +0.4% | West region primary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Boom in Federal Infrastructure Funding (IIJA, IRA)

The Infrastructure Investment and Jobs Act allocates USD 550 billion through 2026, creating a visible project pipeline across all states. “Buy America” sourcing rules favor domestic manufacturing, supporting localized component production and limiting low-cost imports. Highway and bridge upgrades dominate early outlays, yet manufacturing facility construction linked to the CHIPS and Inflation Reduction Acts widens demand for earthmoving fleets [1]Federal Highway Administration, “Obligation of Highway Infrastructure Programs,” fhwa.dot.gov. As mega-projects clear permitting, OEMs scale production capacity, and dealers extend inventories to match multi-year equipment schedules. Regional allocations channel the largest share to aging assets in the South, reinforcing that region’s equipment demand leadership.

Accelerated Urban-Renewal Projects in Tier-2 US Cities

Secondary metropolitan areas such as Cleveland and Kansas City advance billion-dollar mixed-use redevelopments financed through tax-increment mechanisms that cushion higher interest rates [2]Associated General Contractors of America, “The Construction Inflation Alert,” agc.org. Compact job sites within these districts need crawler equipment with low ground pressure and enhanced maneuverability. Public-private partnerships embed affordable-housing quotas that stretch build-out timelines, lengthening equipment utilization periods. Workforce and land-cost advantages sustain Tier-2 project viability even as prime urban centers face affordability constraints. Infrastructure renewal efforts dovetail with broader utility upgrades, elevating demand for mid-range earthmoving capacity able to interchange attachments rapidly.

Rise of Electrified and Hybrid Excavator Models

Manufacturers intensify investment in battery-electric drivetrains, spurred by emission restrictions in California and Northeast low-emission zones [3]U.S. Environmental Protection Agency, “Emission Standards for New Nonroad Engines,” epa.gov. Caterpillar demonstrated a hybrid retrofit that maintains diesel-like power while trimming fuel use, signaling a bridge technology before full electrification. Volvo CE confirmed USD 261 million for US excavator production, aligning capacity with anticipated electric uptake. Compact loaders shift first, as battery mass penalties remain manageable; however, battery energy density improvements progressively expand feasible duty cycles in the 100–200 HP class. Government purchase incentives and fleet-average emission targets accelerate fleet turnover, rewarding early adopters with preferential bid scoring on public projects.

Labor Scarcity Driving Equipment-Rental Penetration

According to data released by the Bureau of Labor Statistics, U.S. construction recorded 236,000 open, unfilled jobs at the end of January, marking a 42% decline from January 2024, intensifying competition for skilled operators. Contractors under-staffed for multi-year infrastructure jobs adopt rental models to match fleet size with variable labor availability. The American Rental Association forecasts USD 78.7 billion in 2024 rental revenue, up 8.9%, confirming heightened preference for variable equipment costs. Rental houses respond by expanding premium machine inventories and offering operator training packages. Flexible short-term contracts mitigate the burden of higher financing costs and free up cash for wage premiums that attract scarce labor.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steep Increases in Equipment-Financing Rates Post-2023 | -0.8% | National; small contractors hardest hit | Short term (≤ 2 years) |

| Tight Tier-4 Emission-Compliance Costs for OEMs | -0.6% | National; specialized units sensitive | Medium term (2-4 years) |

| Supply-Chain Fragility for Hydraulic Components | -0.4% | National; pockets of supplier concentration | Short term (≤ 2 years) |

| Volatile Steel Prices Impacting OEM Margins | -0.3% | National; domestic producers most exposed | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Steep Increases in Equipment-Financing Rates Post-2023

Federal Reserve tightening doubled typical construction-equipment loan rates for prime borrowers, elongating payback horizons and dampening outright purchases. The SBA Optional Peg Rate climbed to 4.38% for Q1 2025, constraining small businesses reliant on government-backed credit. Higher debt service obligations force contractors to postpone fleet renewal or switch to leasing structures. Dealers absorb inventory, carrying costs longer, and pressuring working capital. Although borrowing costs are expected to plateau by late 2025, elevated rates have shifted contractor attitudes toward flexible fleet strategies emphasizing rental over ownership.

Tight Tier-4 Emission-Compliance Costs for OEMs

EPA Tier-4 Final rules require a 90% cut in particulate matter and NOx relative to Tier-3 engines, compelling diesel particulate filters and selective catalytic reduction systems that lift production cost by as much as 20%. Contractors shoulder higher acquisition prices and commit to diesel exhaust fluid logistics. California’s accelerated fleet-turnover mandate forces early retirement of older units, tightening used-equipment supply and amplifying capital needs. OEMs with broad engine portfolios spread R&D burden, but specialized manufacturers face proportionally higher compliance expense.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavator Dominance Anchors Growth

Crawler excavators generated 65.33% of the US crawler earthmoving machines market share in 2024, reinforcing their status as versatile workhorses for digging, lifting, and loading tasks across construction and mining. Contractors value the segment’s attachment compatibility, which reduces fleet size and simplifies logistics. Compact tracked loaders and skid-steers are forecast to grow at a 6.15% CAGR, contingent on rising infill development and infrastructure retrofits in confined urban footprints. Crawler bulldozers sustain demand for large-scale site grading, while crawler cranes and pipe-layers serve niche energy and utility projects spawned by federal spending.

Manufacturers broaden tonnage offerings; Bobcat’s 23- and 25-ton E-series excavators target mid-range jobs previously ceded to larger incumbents. Electric actuation begins with compact loaders that benefit from hydraulic elimination, translating into higher efficiency and lower maintenance. Meanwhile, crawler loaders experience muted uptake as excavators substitute traditional loading roles. Specialized trenchers and drill rigs inside the “Others” class find opportunity in broadband and renewable-energy installations. The segment mix collectively underpins revenue resilience even when individual project pipelines fluctuate.

By Propulsion: Electric Momentum Builds on Regulatory Pull

Internal-combustion models still account for 85.41% of the US crawler earthmoving machines market size in 2024, but electric and hybrid alternatives are expanding at a 7.83% CAGR as urban emission zones tighten. Early adoption centers on equipment below 100 HP, where battery mass is manageable, yet hybrid retrofits extend fuel savings to mid-range units without charging infrastructure dependency. Caterpillar’s battery-electric haul-truck pact with CRH underlines heavy-equipment decarbonization commitments. California’s renewable-diesel mandate accelerates regional electric interest, with the West serving as a proving ground before national diffusion.

Doosan Bobcat’s autonomous electric concepts highlight convergence between electrification and automation, signaling a shift toward software-defined construction machinery. The propulsion transition attracts new battery suppliers and power-management specialists, reshaping the value chain. Hybrid diesel-electric systems bridge current operational requirements and future zero-emission targets, smoothing contractors’ capital planning and fueling the gradual yet persistent displacement of purely diesel fleets.

By Engine Power Output: Mid-Range Flexibility Rules

Machines rated 100–200 HP hold 48.19% share of the US crawler earthmoving machines market size, balancing torque needs with manageable fuel burn across varied job conditions. This sweet spot aligns with federal road-building tasks and mixed-use developments that demand both muscle and maneuverability. Units below 100 HP are projected to grow fastest at 5.81% CAGR as city infill and forestry programs require smaller footprints and lighter ground impact. The 201–400 HP cohort underpins heavy civil and mining operations, while above-400 HP remains limited to large-scale extraction.

Tier-4 emissions compliance raises complexity sharply beyond 200 HP, incentivizing contractors to maximize productivity within lower power brackets. Battery energy density advances will progressively enable electric entries in the 100–200 HP class, though grid charging logistics remain a hurdle for remote sites. Fleet managers optimize total cost of ownership by matching power precisely to task rather than defaulting to oversize equipment, reinforcing mid-range volume dominance.

By Application: Construction Leads, Mining Steady

Construction activities represented 57.44% of the US crawler earthmoving machines market share in 2024 and are advancing at a 6.84% CAGR through 2030. Federal outlays for highways, bridges, and public transit converge with Tier-2 city renewal projects, buoying demand for excavators and compact loaders. Mining and quarrying maintain consistent equipment pull as domestic minerals support renewable-energy supply chains. Agriculture and forestry uptake benefits from wildfire-mitigation contracts and precision land-management programs emphasizing low ground disturbance.

Manufacturing plant construction, up 156% since 2019 amid CHIPS Act incentives, injects additional demand for site-prep machines suited to large pad foundations. Mega-projects in excess of USD 1 billion require sustained multi-year fleet commitments, elevating equipment utilization rates and aftermarket parts revenue. Utility and environmental remediation projects inside the “Others” category provide steady specialty demand, such as trenchers for broadband rollout and dredging rigs for water-quality restoration.

By Distribution Channel: Dealers Retain Primacy While Rental Surges

Authorized dealers supplied 72.35% of units in 2024, reflecting entrenched service infrastructure and financing support that sustain client loyalty. In parallel, rental and leasing firms are rising at 7.26% CAGR, propelled by contractor preference for flexible cost structures and by acute labor shortages that push demand for turnkey equipment-with-operator packages. The American Rental Association projects rental penetration nearing 56.4%, close to its pre-pandemic zenith.

Dealer networks respond by launching subscription-based maintenance plans and short-duration “try-and-buy” programs, blurring lines with rental houses. OEM direct sales remain limited to large fleet owners and government buyers who negotiate specification consistency. Equipment-as-a-service pilots grant manufacturers real-time machine data, informing product improvements and predictive parts stocking. Yet high capital intensity and service obligations preserve dealer relevance in the near term.

Geography Analysis

The South accounted for 36.72% of the US crawler earthmoving machines market in 2024, buoyed by robust population inflows, petrochemical expansion along the Gulf Coast, and major interstate upgrades. Texas captures sizable IIJA allocations for highway modernization, while Florida’s high-growth metropolitan corridors sustain residential and commercial site demand. Warm climate extends construction seasons, lifting annual machine utilization compared to colder regions. Energy projects ranging from LNG terminals to utility-scale solar farms add specialized heavy-lift and grading needs.

The West is the fastest-growing region at 6.11% CAGR through 2030, catalyzed by wildfire mitigation initiatives and aggressive decarbonization policies. California and Colorado channel USFS grants into vegetation management that specifies low-impact crawler designs. Urban reinvestment in Seattle, San Diego, and Denver favors compact electrified loaders capable of operating within emission-regulated downtown cores. Renewable-energy buildouts across desert and mountain terrains further diversify demand, requiring equipment adapted to steep gradients and abrasive conditions.

The Northeast and Midwest post steady growth as legacy infrastructure reaches end-of-life. The Northeast’s dense urban context drives adoption of smaller footprints and telematics-enabled safety features for subterranean transit upgrades. Projects such as New York’s Gateway rail tunnel deliver multi-year earthmoving requirements allied to strict environmental controls. The Midwest benefits from on-shored manufacturing corridors spanning Ohio to Michigan, where greenfield electronics plants necessitate expansive earthworks. Seasonal weather variability steers contractors toward rental units for peak activity periods, reinforcing channel diversification.

The crawler earthmoving machines market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Europe. This is complemented by country-specific insights for Indonesia, Thailand, Philippines, Singapore, Australia, South Korea, and Saudi Arabia, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The US crawler earthmoving machines market remains moderately concentrated. Market leaders—Caterpillar, John Deere, Komatsu, Volvo CE, and Liebherr—are pivoting from diesel-centric portfolios to mixed fleets that incorporate hybrid and fully electric models while bolstering dealer service capacity to defend after-sales revenue streams. Investment in proprietary telematics, autonomous-ready control systems, and over-the-air software updates differentiates premium offerings and raises switching costs for fleet owners. Supply-chain localization is gaining importance as “Buy America” provisions steer component procurement toward domestic plants, a shift that favors incumbents with established US manufacturing footprints. At the same time, pricing pressure from Chinese entrants keeps margins tight on low-spec machines, compelling incumbents to focus on value-added features rather than price plays.

Strategic capital deployment underscores the technology race. Volvo CE earmarked USD 261 million to establish crawler excavator production in Shippensburg, Pennsylvania, enhancing regional capacity and reducing logistics risk while preparing for higher electric-machine demand from West Coast emission-control zones. Liebherr entered a USD 2.8 billion partnership with Fortescue to co-develop zero-emission mining machines, broadening its battery and hydrogen know-how and locking in anchor customers willing to pilot large-format electric crawlers. These moves signal an arms race in power-train flexibility, where OEMs hedge between incremental hybrids and clean-sheet battery designs as regulations tighten through 2030.

Channel leverage and aftermarket strength round out competitive positioning. Dense dealer networks allow incumbents to guarantee 24-hour parts delivery and remote diagnostics, critical advantages when rental penetration climbs and equipment uptime dictates contract profitability. Rental majors increasingly demand telematics integration to optimize fleet utilization, pushing OEMs toward open-API architectures that can feed third-party dashboards without compromising data security. Electrification blurs traditional boundaries as battery suppliers and software firms become co-creators of performance; successful OEMs are those that translate these collaborations into seamless customer experiences rather than discrete hardware upgrades. Consequently, brand loyalty is migrating from machine horsepower toward total-lifecycle value measured in fuel savings, predictive maintenance, and regulatory compliance assurance, reinforcing the primacy of full-service ecosystems over stand-alone equipment sales.

US Crawler Earthmoving Machines Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

John Deere

Volvo CE

Hitachi Construction Machinery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Volvo Construction Equipment (Volvo CE) is investing USD 261 million globally to expand crawler excavator production and address supply chain risks. Shippensburg, Pennsylvania, is one of the sites planned for expansion, and production will start in 2026.

- June 2025: CASE Construction Equipment launches the CX380E crawler excavator in North America at 268 HP and 37,700 kg operating weight.

- October 2024: John Deere integrates SmartGrade 3D machine-control into 450, 550, and 650 P-Tier crawler dozers.

- July 2024: HD Hyundai Construction Equipment North America debuts the HX355A LCR 35.5-ton compact-radius excavator.

US Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Internal Combustion Engine (ICE) |

| Electric and Hybrid |

| Below 100 HP |

| 100-200 HP |

| 201-400 HP |

| Above 400 HP |

| Construction |

| Mining and Quarrying |

| Agriculture and Forestry |

| Others |

| Direct OEM Sales |

| Authorized Dealers |

| Rental and Leasing Firms |

| Northeast |

| Midwest |

| South |

| West |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric and Hybrid | |

| By Engine Power Output | Below 100 HP |

| 100-200 HP | |

| 201-400 HP | |

| Above 400 HP | |

| By Application | Construction |

| Mining and Quarrying | |

| Agriculture and Forestry | |

| Others | |

| By Distribution Channel | Direct OEM Sales |

| Authorized Dealers | |

| Rental and Leasing Firms | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current value of the US crawler earthmoving machines market?

The market stands at USD 1.27 billion in 2025 with a 5.37% CAGR outlook to 2030.

Which equipment type leads US crawler earthmoving machine sales?

Crawler excavators dominate, capturing a 65.33% share in 2024.

How fast is electric propulsion growing in US crawler earthmoving machines?

Electric and hybrid variants are expanding at a 7.83% CAGR through 2030, outpacing diesel growth.

Why is rental demand rising for crawler earthmoving machines?

Labor shortages and higher financing costs make flexible rental contracts attractive to contractors.

Page last updated on: