South Korea Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

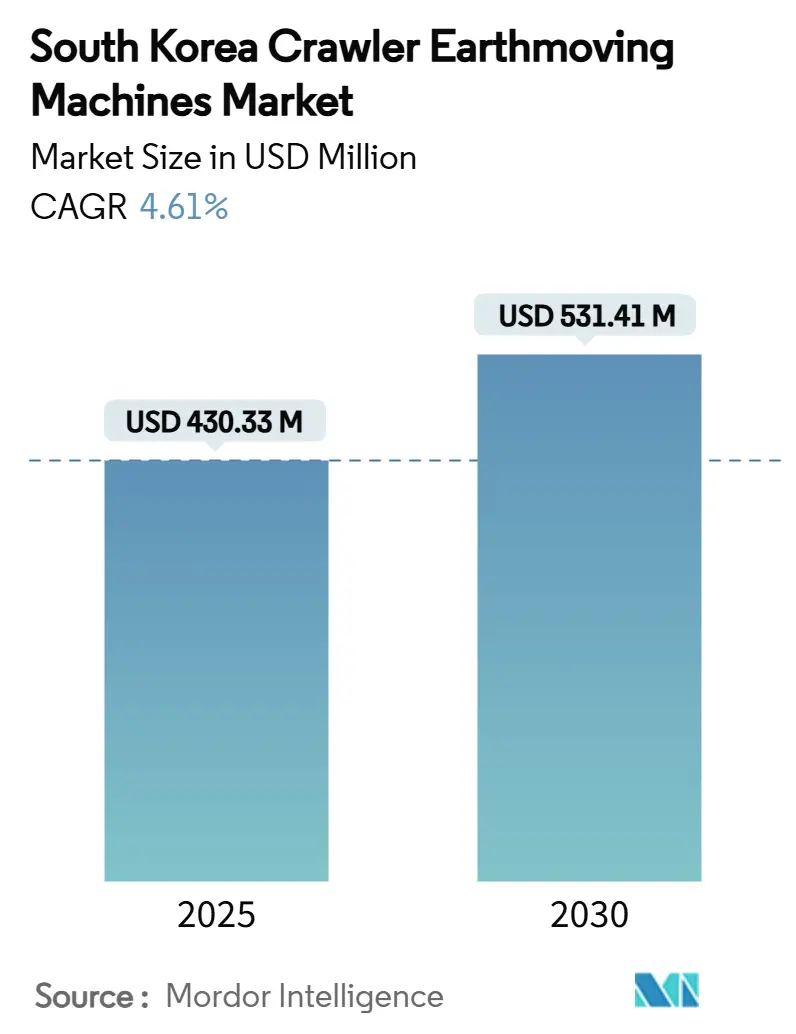

| Market Size (2025) | USD 430.33 Million |

| Market Size (2030) | USD 531.41 Million |

| Growth Rate (2025 - 2030) | 4.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The South Korea crawler earthmoving machines market size reached USD 430.33 million in 2025 and is forecast to grow at a 4.31% CAGR to USD 531.41 million in 2030. This trajectory reflects sustained infrastructure spending, mandatory digital‐construction rules, and rising demand for low-emission machinery. Public budgets tied to the Green New Deal program accelerate electrification, while private contractors adopt telematics to trim operating costs. Compact machines enjoy heightened interest as dense urban sites constrain large earthmovers. Consolidation among domestic manufacturers reshapes competition, but open standards in Building Information Modeling (BIM) create fresh entry points for software-led differentiation. The South Korean crawler equipment market balances traditional hydraulic strength with rapid digital integration, positioning its OEMs for export expansion in Asia.

Key Report Takeaways

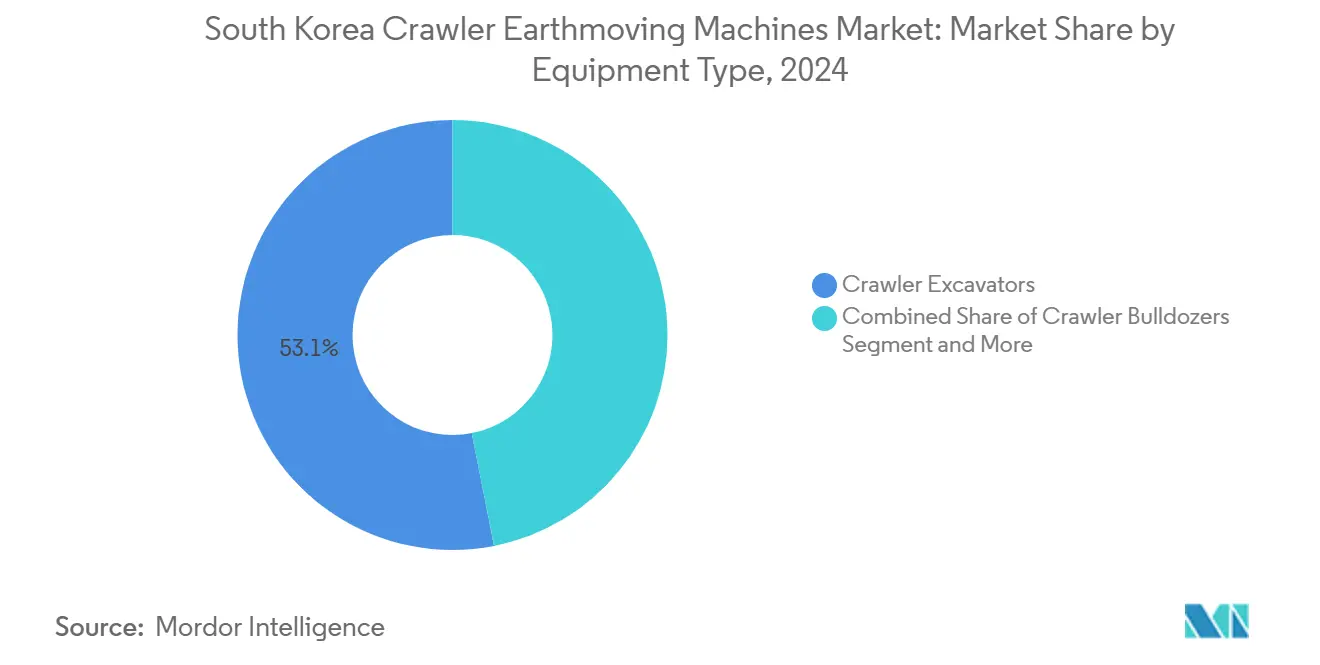

- By equipment type, crawler excavators led with 53.10% of the South Korean crawler equipment market share in 2024, and compact tracked loaders are expanding at an 8.32% CAGR through 2030.

- By propulsion, internal-combustion machines held 79.65% of the South Korean crawler equipment market size in 2024, while electric and hybrid units are projected to advance at an 18.33% CAGR to 2030.

- By engine power output, the 100-200 HP band accounted for 41.87% of the South Korea crawler equipment market size in 2024; units below 100 HP are set to grow the fastest at a 9.12% CAGR between 2025 and 2030.

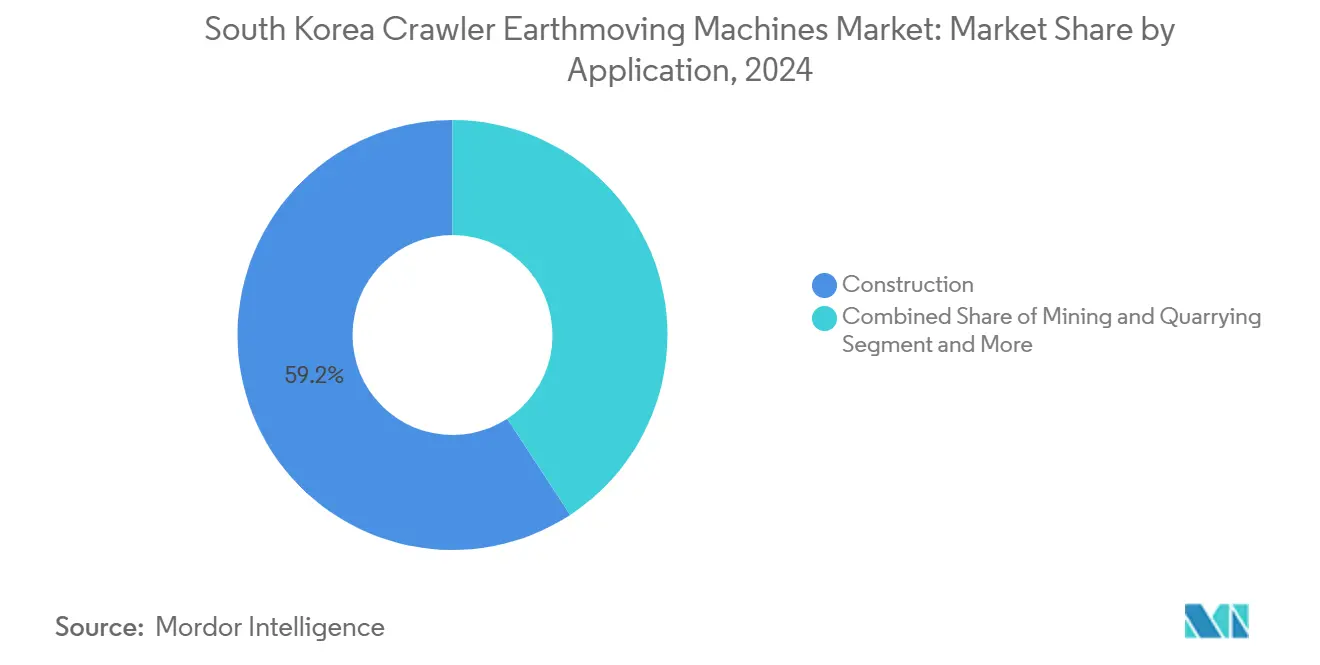

- By application, construction captured 59.22% of the South Korean crawler equipment market share in 2024, and agriculture and forestry are forecast to climb at an 11.45% CAGR through 2030.

- By distribution channel, authorised dealers delivered 55.14% of the South Korean crawler equipment market size in 2024; rental and leasing firms are tracking a 9.61% CAGR over the forecast window.

National developments in South korea connect differently with activity unfolding across other parts of the world. In the global crawler earthmoving machines market coverage, Mordor Intelligence integrates these into a single analytical framework.

South Korea Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Incentives and Emission Mandates | +1.1% | Seoul, Busan, Incheon | Medium term (2-4 years) |

| Digital Twins and OPEX Savings | +0.8% | Gyeonggi-do, Seoul, Daegu | Short term (≤ 2 years) |

| Deconstruction and Circular-Demolition | +0.6% | Seoul, Busan, Ulsan | Medium term (2-4 years) |

| Mandatory BIM Adoption | +0.5% | Seoul, Sejong, Gyeonggi-do | Long term (≥ 4 years) |

| Offshore-Wind Foundation Demand | +0.4% | Busan, Ulsan, Jeollanam-do | Long term (≥ 4 years) |

| Fleet-Electrification Program | +0.3% | Seoul, Gyeonggi-do, Incheon | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification Incentives and Stage-V Emission Mandates

Emissions regulation aligns South Korea with the European Stage-V model and propels a replacement cycle favoring electric and hybrid crawlers. The Green New Deal’s 160 trillion KRW fund channels subsidies into clean-propulsion pilot fleets and offsets the premium pricing of battery-powered units[1]Hae-Ran Lee, “Green New Deal Policy of South Korea: Policy Innovation for a Sustainability Transition,” MDPI Sustainability, mdpi.com. City authorities sharpen particulate-matter limits, making diesel retrofits less viable and nudging contractors toward factory-built zero-tailpipe machines. OEMs react through battery pack sourcing partnerships and hydrogen-ready prototypes that extend runtime beyond eight hours. Financing arms of dealers now market power-train conversion packages together with service contracts, reducing total cost anxiety among mid-size builders. Collectively, these steps lock in a multi-year growth lane for compliant models within the South Korean crawler equipment market.

Digital Twins and Telematics-Driven OPEX Savings

Real-time data services cut idle time and fuel burn, addressing the top risk cited by domestic contractors: insufficient control over equipment budgets[2]Jong-Wook Park, “Risk Factors Affecting Equipment Management in Construction Firms,” Korea Institute of Civil Engineering and Building Technology, koreascience.or.kr. Digital twin platforms overlay BIM files with live sensor feeds, letting site managers simulate trench routes and predict maintenance windows on crawler excavators. The national K-BIM e-Submission system streamlines permit approvals and makes telematics compatibility a bidding prerequisite, further embedding software in procurement logic. HD Hyundai’s remote-monitoring suite illustrates the shift from iron-only selling to lifecycle value propositions. Lower downtime translates into measurable margin gains for fleet owners and underpins greater willingness to pay for connected machines, reinforcing the South Korea crawler equipment market momentum.

Surge In Deconstruction and Circular-Demolition Projects

Selective dismantling gains share over blast-and-clear demolition as policymakers push resource recovery targets. Urban renewal corridors in Seoul and Busan require precision grapples, shear-equipped excavators, and low-noise electric loaders to meet neighborhood regulations. Modular construction uptake expands factory pre-assembly, yet on-site phases still depend on nimble crawlers to move volumetric units into position. These job-site nuances open niches for compact models with higher lift-to-weight ratios, sustaining double-digit growth for specialized attachments. The trend improves revenue mix by lifting accessory sales relative to base hardware in the South Korean crawler equipment market.

Mandatory BIM Adoption for Public Projects

Since 2016, every public project over USD 50 million has been mandated to deploy BIM, and the Ministry of Land, Infrastructure, and Transport plans full BIM coverage by 2025. A majority of domestic design firms already embed 3D models in tenders, pulling equipment specifiers into digital-ready checklists. Crawler excavators equipped with grade-control sensors and cloud APIs score higher in tender evaluations, benefiting incumbents that bankroll firmware upgrades. Smaller importers face integration hurdles, raising entry barriers, and concentrating sales among a handful of tech-savvy OEMs within the South Korean crawler equipment market. Over time, BIM compliance evolves from a differentiator to a baseline, spurring a fresh wave of value-added software services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX And Tightening Credit | -1.1% | Seoul, Gyeonggi-do, Busan | Short term (≤ 2 years) |

| Supply-chain Volatility | -0.8% | Ulsan, Busan, Gyeonggi-do | Medium term (2-4 years) |

| Fast-Charging Infrastructure Scarcity | -0.6% | Seoul, Incheon, Busan | Long term (≥ 4 years) |

| Cost of Ownership for Diesel Units | -0.4% | Seoul, Busan, Daegu | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX And Tightening Credit

Escalating steel and cement prices inflate project budgets and pinch cash flows, delaying fleet renewal among small contractors. Material costs on benchmark smart-city sites climbed by more than 25% between 2024 and 2025, while domestic banks tightened working-capital lines, raising borrowing spreads by 150 basis points[3]International Trade Administration, “South Korea – Construction Services,” trade.gov. Many firms pivot to short-term rentals or lease-backs, slowing direct purchases. OEM finance subsidiaries promote payment holidays and buy-back guarantees, yet adoption lags in rural provinces. The squeeze blunts near-term sales velocity across the South Korean crawler equipment market, although it simultaneously boosts rental penetration.

Raw-Material and Component Supply Volatility

Battery cells, semiconductors, and hydraulic valves suffer periodic shortages tied to geopolitical friction and factory fires. Production lead-times for flagship excavators lengthened from eight to thirteen weeks in 2024, pushing dealers to carry higher inventory buffers. Currency swings against the U.S. dollar amplify imported part costs, complicating price quotes valid for more than thirty days. OEMs nearshore certain castings and sign multi-year lithium contracts, but smaller assemblers lack scale to hedge, exposing them to spot-market shocks. Volatility elevates replacement-part pricing and could dampen secondary-market values, mildly moderating growth in the South Korea crawler equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators Anchor Value While Compact Units Accelerate

Crawler excavators dominated the South Korean crawler equipment market with a 53.10% share in 2024, underscoring their adaptability in South Korea's construction landscape, from urban redevelopment to significant projects such as the Gadeokdo New Airport. This segment's dominance is attributed to hydraulic excavators' flexibility, catering to a range of needs from standard earthmoving to intricate demolition tasks.The segment benefits from a broad attachment ecosystem that reduces idle time and extends asset life.

Compact tracked loaders posted an 8.32% CAGR forecast to 2030, gaining traction in alleyway trenching and high-rise logistics zones. Crawler bulldozers serve port-land reclamation, while pipe-layer variants fill LNG trunk-line assignments. High-visibility bucket cameras and semi-autonomous dig cycles widen productivity gaps, sustaining premium list prices across the South Korea crawler equipment market.

By Propulsion: Electric Momentum Challenges Diesel Dominance

Internal-combustion platforms captured 79.65% of the South Korean crawler equipment market size in 2024, but their share is projected to dip as electric and hybrid alternatives outpace them at an 18.33% CAGR. South Korea's Green New Deal commitment to electric and hydrogen vehicle development extends to construction equipment applications, creating policy support for propulsion system transitions

Electric propulsion offers benefits such as reduced operational costs, lower maintenance needs, and adherence to tightening urban emission regulations impacting construction sites. Yet, the adoption rate faces hurdles due to limited charging infrastructure and the higher initial capital outlay, especially for larger crawler equipment. Hybrid drivetrains bridge range anxiety on provincial highway lots where chargers remain scarce. OEM battery-leasing schemes decouple capital costs from technology obsolescence, enriching service revenue streams inside the South Korean crawler equipment market.

By Engine Power Output: Mid-Range Machines Deliver Optimal Utilization

The 100-200 HP class accounted for 41.87% of the South Korea crawler equipment market size in 2024 due to its sweet-spot balance between fuel efficiency and multi-tool compatibility. Units below 100 HP are projected to rise 9.12% annually through 2030 as city ordinances curb diesel engine displacement downtown. Higher power segments (201-400 HP and above 400 HP) serve specialized applications in major infrastructure projects

Above-400 HP models rely on mega-infrastructure outlays such as offshore-wind foundations, leading to cyclical demand. Electric propulsion faces greater technical challenges in higher power applications due to battery weight and energy density limitations, creating market segmentation between electrified smaller equipment and traditional ICE larger machines. Power-segment granularity helps dealers tailor parts stocking, boosting after-sales margins throughout the South Korean crawler equipment market.

By Application: Construction Leads, Agriculture Gains Ground

Construction activities commanded 59.22% of the South Korean crawler equipment market share in 2024 on the back of subway extensions and expressway maintenance. The segment's leadership reflects crawler equipment's fundamental role in earthmoving, excavation, and material handling across construction phases, from site preparation to final grading operations.

Agriculture and forestry are accelerating at an 11.45% CAGR, spurred by precision-silviculture pilots and state forestry mechanization grants. Quarrying retains steady volume around metropolitan aggregate hubs. Meanwhile, environmental remediation contracts following coal-plant closures open new niches for zero-spill hydraulic crawlers within the South Korean crawler equipment market. Major infrastructure projects like the Gadeokdo New Airport development and ongoing expressway network expansions sustain construction application demand while creating opportunities for specialized equipment applications.

By Distribution Channel: Dealer Networks Dominate Amid Service Integration

In 2024, authorized dealers command a 55.14% market share, capitalizing on their established relationships and comprehensive service capabilities. These dealers also offer crucial financing arrangements, ensuring construction equipment users can maintain operational continuity. Their strength is rooted in local market knowledge, ready parts availability, and technical support, all vital for upholding equipment uptime amidst South Korea's rigorous construction timelines.

Rental and leasing firms expect a 9.61% CAGR because builders prefer variable costs during uncertain rate cycles. Meanwhile, direct OEM sales cater to large fleet operators and niche applications, where customization and direct ties to manufacturers yield significant operational advantages. Channel diversification underpins unit absorption and stabilizes inventory turnover in the South Korean crawler equipment market.

Geography Analysis

Seoul, Gyeonggi-do, and Incheon formed the largest pool of spending in 2024 thanks to nonstop urban regeneration, fourth-generation subway lines, and smart-city pilots that demand BIM-ready fleets. Contractors here prize low-noise electrics to comply with strict particulate rules, reinforcing first-mover marketing advantages in the South Korea crawler equipment market.

Busan, Ulsan, and South Gyeongsang Province follow as the fastest-growing cluster, propelled by the 13.7 trillion-won Gadeokdo New Airport megaproject and adjacent port dredging works. Local shipyards require heavy crawler cranes for dry-dock expansions that feed energy-transition vessel orders. Regional authorities subsidize hydrogen-powered machinery trials, accelerating technology adoption curves across the South Korean crawler equipment market.

Balanced development policies keep demand alive in inland provinces such as North Chungcheong, where logistics parks and high-speed rail track upgrades need mid-range excavators. Mountain tunneling for highway bypasses spurs orders for high-torque bulldozers, while coastal flood-defense jobs spur procurement of amphibious carriers. Geographic dispersion cushions OEM order books against single-region slowdowns.

Mordor Intelligence's coverage of the crawler earthmoving machines market extends across other regions including Europe, while country-specific intelligence is also available for Thailand, Philippines, Indonesia, United States, Singapore, Australia, and Saudi Arabia, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

Domestic consolidation gives HD Hyundai Construction Equipment and Develon a combined edge in 2024 turnover, translating to purchasing scale for steel and battery packs. They leverage unified telematics back-ends to cross-sell parts and analytics subscriptions, locking customers into proprietary ecosystems within the South Korean crawler equipment market.

Global titans Caterpillar and Komatsu sustain share by shipping advanced grade-control sensors and autonomous haul-assist modules honed in overseas mines. Their Korean branches partner with local rental chains to broaden reach without duplicating dealer footprints. High-spec models targeting offshore-wind jackets and LNG terminals carve a profitable niche alongside domestic brands.

Strategic alliances intensify. HD Hyundai and Doosan Bobcat co-market compact electrics in export territories, pooling R&D roadmaps to de-risk platform bets. Volvo CE injects multimillion-dollar capex into its Changwon site to shorten build-to-ship cycles for APAC orders. Competitive emphasis shifts from pure horsepower to software reliability, battery warranty, and lifecycle analytics, redefining leadership metrics in the South Korea crawler equipment market.

South Korea Crawler Earthmoving Machines Industry Leaders

HD Hyundai Construction Equipment

Develon (Doosan)

Caterpillar Inc.

Komatsu Ltd.

Volvo Construction Equipment AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: HD Hyundai Construction Equipment invested EUR 131 million to build a smart factory at its Ulsan campus, automating material flow and quality checks.

- June 2025: Volvo CE earmarked USD 261 million to expand crawler excavator capacity across sites in the United States, South Korea, and Sweden.

- February 2025: Develon unveiled “Real X,” an autonomous control suite enabling its latest crawler excavators to conduct trenching and bulk earthwork without direct operator input.

South Korea Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Internal Combustion Engine (ICE) |

| Electric and Hybrid |

| Below 100 HP |

| 100 to 200 HP |

| 201 to 400 HP |

| Above 400 HP |

| Construction |

| Mining and Quarrying |

| Agriculture and Forestry |

| Others |

| Direct OEM Sales |

| Authorised Dealers |

| Rental and Leasing Firms |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric and Hybrid | |

| By Engine Power Output | Below 100 HP |

| 100 to 200 HP | |

| 201 to 400 HP | |

| Above 400 HP | |

| By Application | Construction |

| Mining and Quarrying | |

| Agriculture and Forestry | |

| Others | |

| By Distribution Channel | Direct OEM Sales |

| Authorised Dealers | |

| Rental and Leasing Firms |

Key Questions Answered in the Report

What is the 2025 value of South Korea’s crawler equipment sector?

The segment is valued at USD 430.33 million in 2025.

How quickly are electric and hybrid crawlers expanding?

They are forecast to post an 18.33% CAGR between 2025 and 2030.

Which machine category controls the greatest share?

Crawler excavators lead with a 53.10% share of 2024 sales.

How fast is the rental and leasing channel growing?

Rental providers are on track for a 9.61% CAGR through 2030.

Where is demand increasing most rapidly outside greater Seoul?

Busan and surrounding southeastern provinces see the highest projected growth, buoyed by the Gadeokdo New Airport build.

Why does BIM compliance matter when buying new crawlers?

Public contracts now mandate BIM-integrated machinery, making digital-ready models a prerequisite for large projects and boosting premium sales.

Page last updated on: