Europe Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

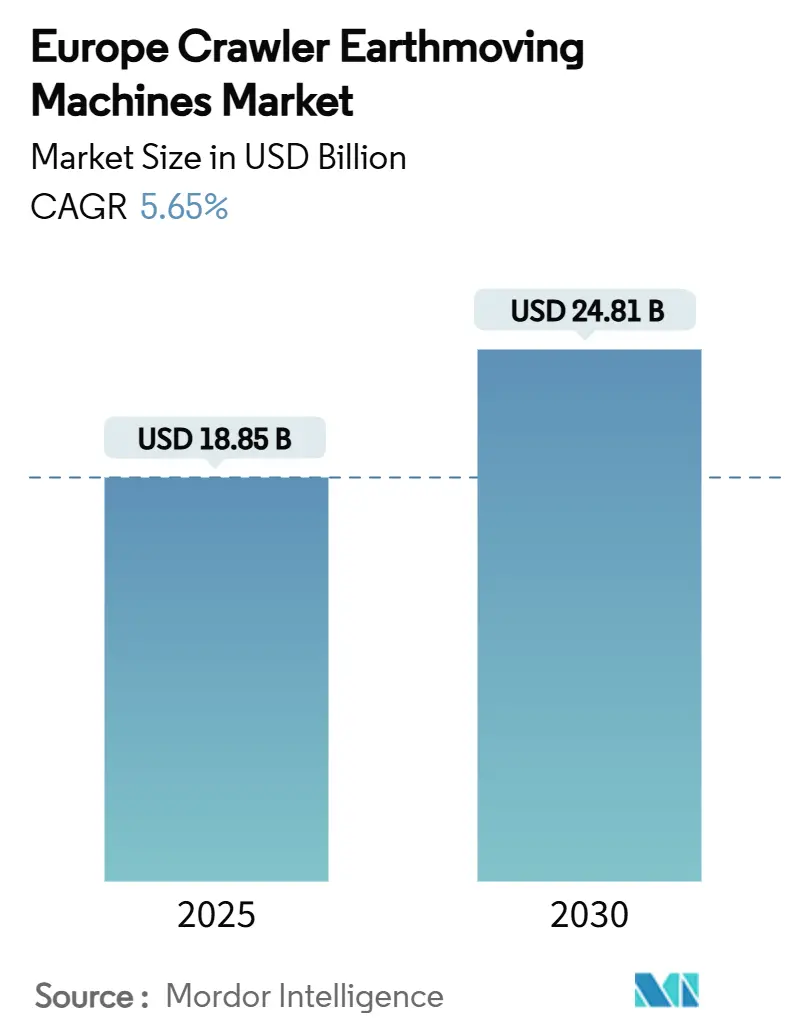

| Market Size (2025) | USD 18.85 Billion |

| Market Size (2030) | USD 24.81 Billion |

| Growth Rate (2025 - 2030) | 5.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

Europe crawler earthmoving machines market size stands at USD 18.85 billion in 2025 and is forecast to register a 5.65% CAGR to reach USD 24.81 billion by 2030. This trajectory is underpinned by the EUR 891.7 billion EU Recovery Fund. Building-energy renovations bolster demand, the rapid modernization of rental fleets, and stringent Stage V emissions rules that accelerate replacement of pre-2019 equipment. Supply chain volatility in steel and critical components elevates input costs, favoring scale players that can hedge raw materials and secure long lead-time parts. The progressive electrification of compact equipment, combined with digital-twin deployments, enhances fleet uptime and lowers total ownership cost, creating a competitive moat for manufacturers that bundle hardware, software, and services.

Key Report Takeaways

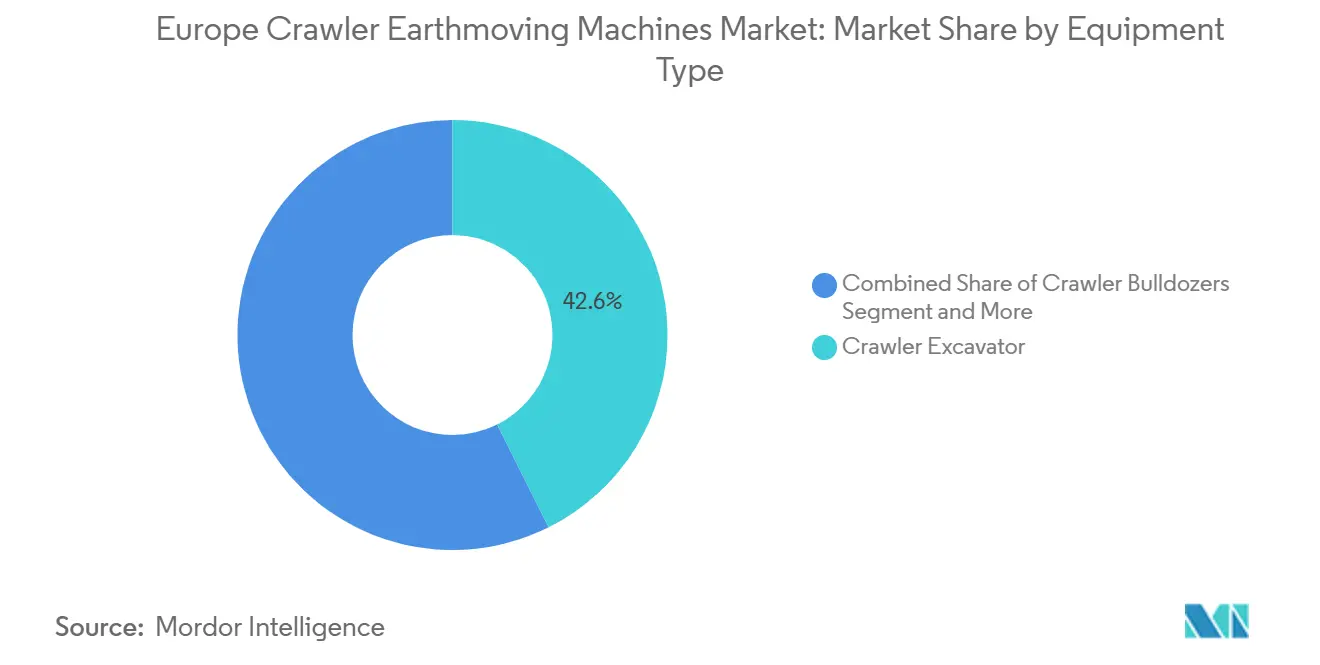

- By equipment type, crawler excavators led with 42.62% revenue share in 2024, while compact track loaders are projected to expand at an 8.79% CAGR to 2030.

- By propulsion, diesel systems accounted for 76.43% share of the Europe crawler earthmoving machines market size in 2024; battery-electric variants are forecast to grow at a 9.56% CAGR through 2030.

- By engine power, the 201–400 HP band commanded 37.27% share of the Europe crawler earthmoving machines market size in 2024, whereas the below-100 HP class is advancing at a 7.49% CAGR to 2030.

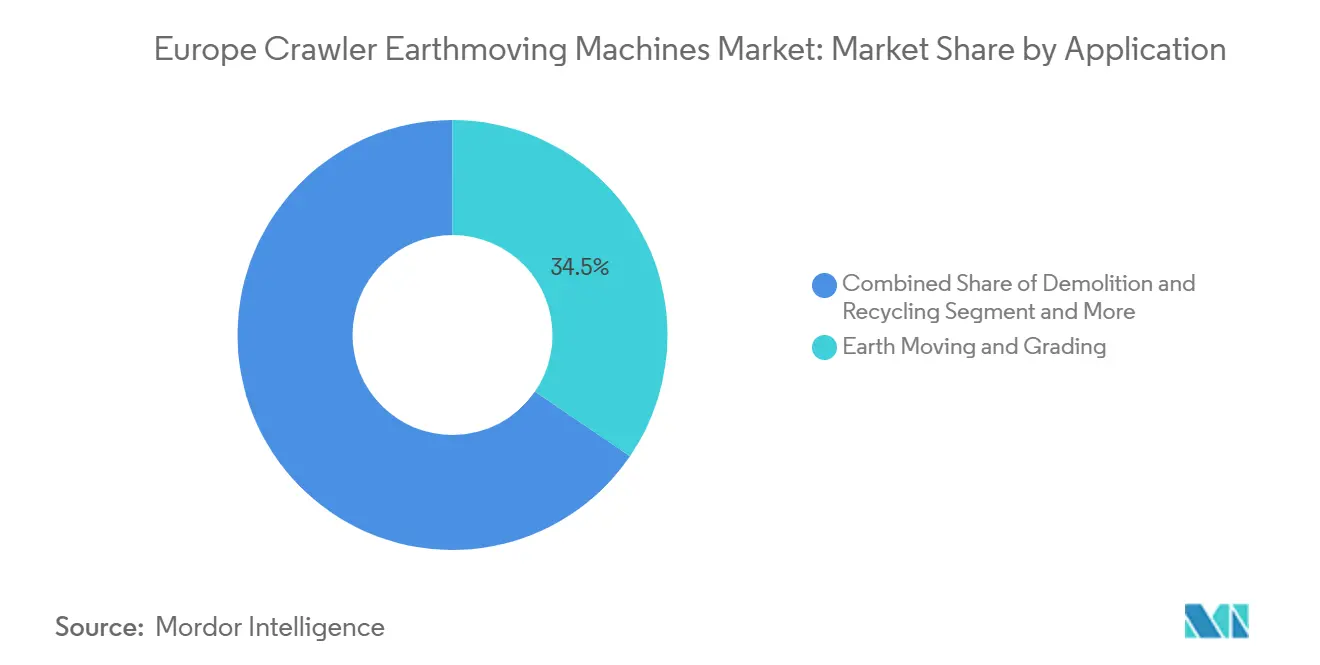

- By application, earthmoving and grading captured 33.18% share of the Europe crawler earthmoving machines market size in 2024; demolition and recycling is the fastest-growing segment at a 7.46% CAGR through 2030.

- By end-user, construction held 46.75% of Europe crawler earthmoving machines market share in 2024, while municipal services record the highest 7.34% CAGR to 2030.

- By distribution channel, authorized dealers maintained 34.86% share in 2024; online and digital marketplaces are projected to rise at a 9.28% CAGR between 2025-2030.

- By geography, Germany dominated with a 24.83% share in 2024, whereas Norway is set to post the fastest 8.94% CAGR through 2030

Proportional positioning is established by comparing regional contributions against the global total, including that of Europe. The crawler earthmoving machines market share in our global report expresses these relative weights.

Europe Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Recovery Fund stimulus | +1.8% | EU-wide, strongest in Germany, France, Italy | Medium term (2-4 years) |

| Fleet replacement cycle | +1.2% | Western Europe, Nordic countries | Short term (≤ 2 years) |

| Stage V and EV incentives | +0.9% | EU-wide, early adoption in Netherlands, Germany | Long term (≥ 4 years) |

| Telematics OPEX savings | +0.7% | Nordic countries, Germany, United Kingdom | Medium term (2-4 years) |

| Circular demolition surge | +0.6% | Netherlands, Belgium, Germany | Long term (≥ 4 years) |

| Rental fleet expansion | +0.5% | Western Europe, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Construction-sector stimulus under EU Recovery Fund

The EU Recovery Fund channels a mandated 37% of its value toward green infrastructure, which keeps public-sector tenders flowing and sustains multi-year crawler equipment orders, especially in Germany, France, and Italy[1]“Recovery and Resilience Facility: Green Transition Targets,”, European Commission, ec.europa.eu. Investments in energy envelope earmarks, building-energy upgrades, and renewable installations have surged, driving the demand for compact electrified machines. These machines are designed to operate in densely populated urban areas, all while producing zero local emissions. Performance-linked disbursements through 2026 ensure a predictable project pipeline that smooths OEM production planning and helps rental houses lock in bulk orders. Contractors favor Stage V-compliant and battery-electric models to secure public contracts tied to sustainability metrics, reinforcing purchase intent well before older fleets reach technical end-of-life.

Stage V and electrification incentives

Stage V standards now cover engines above 560 kW and below 19 kW, forcing OEMs to fit diesel particulate filters and selective catalytic reduction across the crawler range[2]“Stage V Non-Road Mobile Machinery Regulation Overview,”, Committee for European Construction Equipment, cece.eu. Municipalities like Oslo stipulate zero-emission equipment on public works, creating immediate pull for electric compact crawlers. Volvo CE plans to electrify its entire compact excavator roster within the decade. At the same time, CNH has launched an Italian production line dedicated to electric wheel loaders, collectively signalling an irreversible propulsion shift.

Digital-twin and telematics OPEX savings

Platforms such as Trackunit IrisX process 2 billion data points daily, allowing fleet operators to diagnose track wear or hydraulic pressure anomalies days before failure[3]“IrisX Platform Data Milestones,”, Trackunit ApS, trackunit.com. Predictive maintenance translates into 15-20% downtime reduction and up to 10% fuel savings, which offsets the price premium of connected machines in four to five years. Subscription models with high recurring revenue, typified by SmartCraft in the Nordics, embed software into contractor workflows and raise switching costs, giving first-movers a durable competitive edge.

Expansion of rental and leasing fleets

High equipment prices and monetary tightening in 2024 pushed many contractors to asset-light operating models. Rental penetration in some Western European nations has exceeded, and integrated telematics enables rental companies to bill on actual utilisation while guaranteeing uptime. OEMs respond by designing crawler platforms optimised for high-hour-per-year duty cycles and quick attachment swaps, locking in long-term service contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and credit | -1.1% | Southern Europe, Eastern Europe | Short term (≤ 2 years) |

| Supply volatility | -0.8% | EU-wide, acute in Germany, France | Medium term (2-4 years) |

| Fast-charge scarcity | -0.6% | EU-wide, critical in urban centers | Long term (≥ 4 years) |

| Diesel ESG cost | -0.4% | Western Europe, Nordic countries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-material and component supply volatility

European steel demand declined 2.3% in 2024, and anti-dumping quotas under the EU Steel Action Plan reduced import slack, raising volatility[4]“EU Steel Market Report Q1 2025,”, European Steel Association, eurofer.eu. Hydraulic valve lead times peaked at 46 weeks in early 2025, forcing OEMs to overorder and carry inventory at a higher cost. Battery-grade nickel and lithium prices remain susceptible to global EV demand spikes, constraining the ramp-up of large electric crawlers.

ESG-linked cost of owning diesel fleets

Green-bond frameworks and sustainability-linked loans penalize companies with high diesel exposure. Contractors bidding on public tenders must disclose fleet emissions, and higher Scope 1 footprints translate into lower evaluation scores. The incremental financing cost reduces cash available for new diesel purchases, indirectly suppressing market volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators underpin market leadership

The European crawler earthmoving machines market size for crawler excavators measured in 2024, equal to a 42.62% share, and these machines retain dominance due to versatility across trenching, site clearing, and selective demolition. Compact track loaders reach the highest 8.79% CAGR on the back of urban renewal projects that demand maneuverability, with mid-range 2,500-3,000 lb units balancing transport ease and hydraulic power. Europe crawler earthmoving machines market share for crawler bulldozers and loaders remains stable, serving reclamation works and quarry overburden removal. OEM innovation focuses on attachment quick-couplers and grade-control automation that reduce operator skill dependency.

Growth momentum in the “Others” group, including trenchers and drill rigs, links to telecom fibre roll-outs and energy interconnector projects that require narrow trench widths and precise depth control. Komatsu’s Stage V-compliant 4-ton skid-steer launch at Bauma 2025 illustrates how traditional heavy-duty brands pivot toward compact, tech-enabled designs to capture this emerging demand niche.

By Propulsion: Electric gains ground amid diesel prevalence

Diesel engines retained a 76.43% hold over Europe crawler earthmoving machines market share in 2024 thanks to widespread refuelling logistics and high torque density. Yet battery-electric units post a 9.56% CAGR, penetrating compact and mid-size classes where 80-100 kWh battery packs sustain one shift with overnight AC charging. Stage V after-treatment costs and urban low-emission zones raise the total cost of diesel ownership, narrowing the acquisition price gap. OEM concentration on battery modularity, exemplified by CASE’s removable pack concept, enhances fleet utilisation as charged modules can be exchanged in minutes.

Hybrid systems combine downsized diesel engines with 48 V or 600 V battery assistance, yielding up to 25% fuel savings without range anxiety. Hydrogen fuel cells remain pilot-scale due to inadequate hydrogen distribution and high stack costs.

By Engine Power Output: Mid-range retains the sweet spot

Machines rated 201-400 HP controlled 37.27% of the Europe crawler earthmoving machines market size in 2024. They meet most infrastructure excavation demands while conforming to transport regulations on European roads. Below-100 HP crawlers grow fastest at 7.49% CAGR, favoured for inner-city projects where weight-restricted bridges and emission rules apply. Improvement in hydraulic efficiency lets sub-100 HP units tackle tasks once reserved for 150 HP machines, compressing the power curve.

Above-400 HP units remain indispensable for mine overburden removal and large hydro projects. Liebherr’s tie-up with Fortescue for autonomous 360 t battery-electric trucks signals how even ultra-high-power classes will adopt zero-emission propulsion once battery specific energy improves.

By Application: Demolition embodies circular economy goals

Earthmoving and grading stayed dominant at 33.18% of the Europe crawler earthmoving machines market share in 2024, but selective demolition and recycling showed the strongest 7.46% CAGR. EU waste directives require provenance documentation for reclaimed materials, pushing contractors to equip crawlers with shear, pulveriser, and crusher attachments capable of fractionating concrete and rebar on-site. Increased tunnelling, rail expansion, and renewable energy developments keep pipeline excavation and energy infrastructure applications active.

Rental fleet deployment emerges as an application in its own right, as renters push for telematics-ready machines to control utilisation. Forestry and agriculture niches continue to adopt low ground-pressure tracks to navigate soft soil without compaction.

By End-User: Municipal services outpace private demand

Municipal authorities accounted for only 17.9% of 2024 volume but deliver a 7.34% CAGR to 2030, fuelled by climate adaptation works such as flood defences and district heating upgrades that suit compact electric crawlers. Construction firms remain the largest buyers, with 46.75% share, though many outsource ownership to rental partners. Mining and quarrying secure a base-load of demand, while logistics developers invest in larger crawler loaders to build automated fulfilment centres.

By Distribution Channel: Digital marketplaces gain traction

Authorized dealer networks still control 34.86% of unit sales due to on-site service capacity. However, the online channel grows at 9.28% CAGR as buyers use digital configurators and price-comparison portals before placing orders. OEM-owned platforms integrate financing, telematics subscriptions, and over-the-air software updates, blurring the line between sales and after-sales support. Rental portals let contractors schedule equipment, add attachments, and monitor utilisation from a single dashboard.

Geography Analysis

Germany generated 24.83% of the Europe crawler earthmoving machines market size 2024, benefiting from high-value industrial projects and domestic OEM presence. Federal incentives for energy-efficient building retrofits keep crawler demand resilient despite 2024’s construction slowdown. France and the United Kingdom represent over one-quarter of regional volume; political turbulence in France suppressed new project approvals, while the UK relies on large rail and road schemes to sustain fleet renewal.

Italy leverages EUR 68.9 billion in Recovery Fund grants for public works and hosts CNH’s new electric loader line, positioning the country as a technology hub. Spain’s residential rebound lifts compact crawler sales, whereas Russia remains constrained by sanctions that limit Western technology imports. The Netherlands spearheads circular-demolition practice, spurring high attachment demand. Sweden and Finland use forestry and mining to utilise mid-range diesel crawlers with high tractive effort.

Norway posts the fastest 8.94% CAGR through 2030. NOK 46.9 billion earmarked for 2025 road spend and large contracts such as Skanska’s NOK 11.4 billion E10/rv-85 project create a robust equipment pipeline. Government mandates for emission-free machinery on public works tilt purchases to battery-electric compact and hybrid mid-size units. Poland and Czechia show steady growth as EU cohesion funds finance expressway upgrades. Alpine nations Austria and Switzerland maintain demand for narrow-gauge crawlers capable of operating on steep gradients.

Mordor Intelligence examines the crawler earthmoving machines market across diverse other regional markets as well, offering granular country-level perspectives for Indonesia, United States, Thailand, Philippines, Singapore, Australia, South Korea, and Saudi Arabia and more.

Competitive Landscape

The market shows moderate concentration, with Caterpillar, Komatsu, Liebherr, and Volvo CE channeling global scale into R&D, speeding battery and hydrogen prototype deployment. Caterpillar’s deal with CRH to co-develop 70-100 t battery haul trucks illustrates collaborative innovation aimed at aggregate sites using crawler excavators.

Strategic acquisitions reshape the field. Komatsu absorbed GHH Group to deepen underground capability; Fayat’s pending purchase of Mecalac adds compact specialists to its portfolio; Kubota secures Liebherr OEM supply to enter the 9-11 t wheeled excavator class. Chinese entrants XCMG and SANY boost European compliance by integrating Stage V engines and opening parts depots in Germany and Poland.

Data-centric ecosystems have become the new battlefield. Trackunit has grown its installed base to over 1.4 million units, selling analytics that cut renter downtime. OEMs bundle multi-year telematics licenses and predictive maintenance packages, making total lifecycle cost rather than invoice price the primary contracting variable. Market entrants lacking software depth face margin compression as customers demand integrated solutions.

Europe Crawler Earthmoving Machines Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Liebherr-International AG

Volvo Construction Equipment AB

Hitachi Construction Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kubota agreed with Liebherr to source 9 t and 11 t wheeled excavators for the European launch in 2026 to capture infrastructure-led demand.

- December 2024: Zeppelin took over Caterpillar distribution in Norway and the Netherlands, widening its regional footprint.

- July 2024: CNH opened an electric compact loader line in Lecce, Italy, timed to rising zero-emission demand.

Europe Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes & Pipe-layers |

| Compact Tracked Loaders & Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Diesel (Stage III - V) |

| Hybrid Diesel-Electric |

| Battery-Electric |

| Hydrogen Fuel-cell (Pilot) |

| Below 100 HP |

| 100-200 HP |

| 201-400 HP |

| Above 400 HP |

| Earthmoving & Grading |

| Demolition & Recycling |

| Forestry & Agriculture |

| Mining & Quarrying |

| Pipeline & Energy Infrastructure |

| Rental Fleet Operations |

| Construction (Residential, Non-residential) |

| Mining & Quarrying |

| Oil & Gas Infrastructure |

| Industrial & Logistics Parks |

| Municipal Services |

| Agriculture & Forestry |

| Direct OEM Sales |

| Authorised Dealers |

| Rental & Leasing Firms |

| Online / Digital Marketplaces |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Sweden |

| Norway |

| Finland |

| Poland |

| Czech Republic |

| Austria |

| Switzerland |

| Belgium & Luxembourg |

| Denmark |

| Ireland |

| Portugal |

| Greece |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes & Pipe-layers | |

| Compact Tracked Loaders & Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Diesel (Stage III - V) |

| Hybrid Diesel-Electric | |

| Battery-Electric | |

| Hydrogen Fuel-cell (Pilot) | |

| By Engine Power Output | Below 100 HP |

| 100-200 HP | |

| 201-400 HP | |

| Above 400 HP | |

| By Application | Earthmoving & Grading |

| Demolition & Recycling | |

| Forestry & Agriculture | |

| Mining & Quarrying | |

| Pipeline & Energy Infrastructure | |

| Rental Fleet Operations | |

| By End-user | Construction (Residential, Non-residential) |

| Mining & Quarrying | |

| Oil & Gas Infrastructure | |

| Industrial & Logistics Parks | |

| Municipal Services | |

| Agriculture & Forestry | |

| By Distribution Channel | Direct OEM Sales |

| Authorised Dealers | |

| Rental & Leasing Firms | |

| Online / Digital Marketplaces | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Sweden | |

| Norway | |

| Finland | |

| Poland | |

| Czech Republic | |

| Austria | |

| Switzerland | |

| Belgium & Luxembourg | |

| Denmark | |

| Ireland | |

| Portugal | |

| Greece |

Key Questions Answered in the Report

What is the expected CAGR for Europe’s crawler earthmoving machines between 2025 and 2030?

The sector is projected to register a 5.65% CAGR, lifting revenue from USD 18.85 billion in 2025 to USD 24.81 billion by 2030.

Which equipment category shows the highest growth momentum?

Compact track loaders post the strongest outlook with an 8.79% CAGR through 2030, driven by urban-site maneuverability needs.

How quickly is battery-electric propulsion gaining traction?

Although diesel still holds a 76.43% share, battery-electric units are expanding at a 9.56% CAGR thanks to Stage V compliance and zero-emission policies.

Which country is forecast to grow the fastest and why?

Norway leads with an 8.94% CAGR, supported by large-scale road budgets and municipal mandates for emission-free machinery.

How does the shift toward rental fleets influence procurement strategy?

High CAPEX and tighter credit prompt contractors to favor long-term rentals; this accelerates turnover of Stage V-compliant and connected machines within rental inventories.

Page last updated on: