Saudi Arabia Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

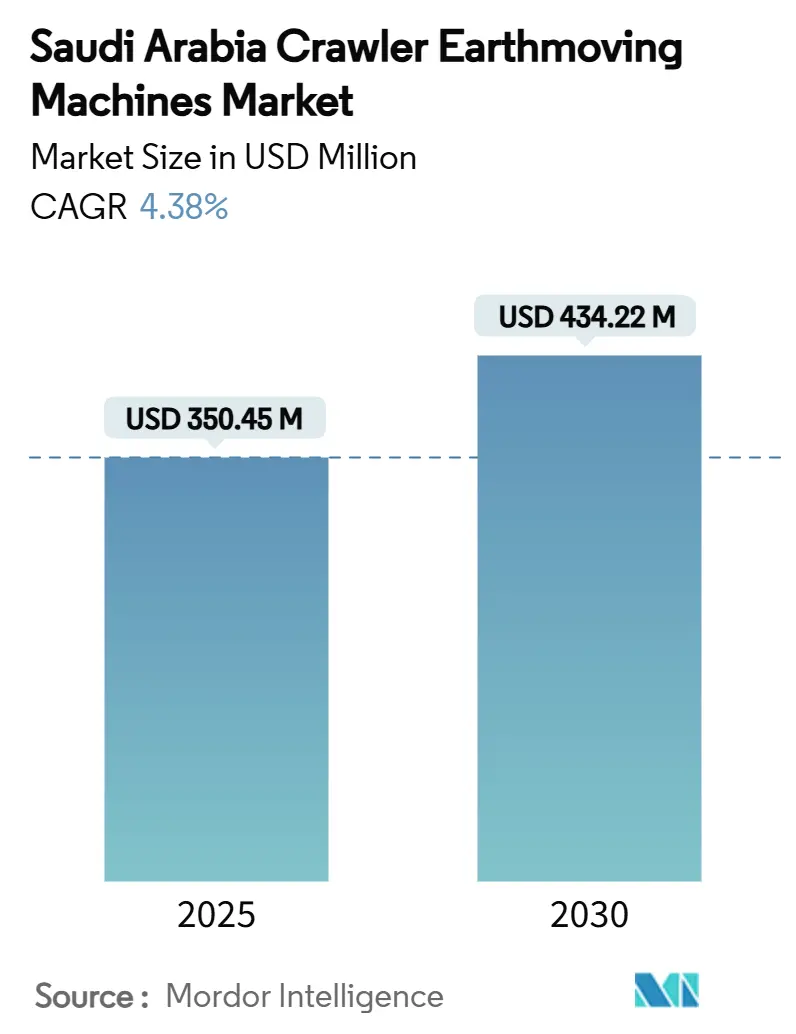

| Market Size (2025) | USD 350.45 Million |

| Market Size (2030) | USD 434.22 Million |

| Growth Rate (2025 - 2030) | 4.38% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The Saudi Arabia crawler earthmoving machines market size stands at USD 350.45 million in 2025 and is forecast to reach USD 434.22 million by 2030, advancing at a 4.38% CAGR. Expansion flows directly from Vision 2030, which directs more than USD 1.25 trillion of public and private capital into giga-projects, transport links, and energy infrastructure. Mega-programs such as NEOM, Diriyah, and the Red Sea tourism corridor compress construction timelines, lifting equipment utilization rates, and supporting premium pricing for high-spec crawlers. Energy infrastructure upgrades led by Saudi Aramco’s USD 25 billion Jafurah and Master Gas System packages reinforce demand for heavy-duty pipe-layers and cranes. At the same time, local-content rules under the IKTVA program channel a growing share of component sourcing and assembly into domestic factories, creating cost and lead-time advantages for in-Kingdom buyers.

Key Report Takeaways

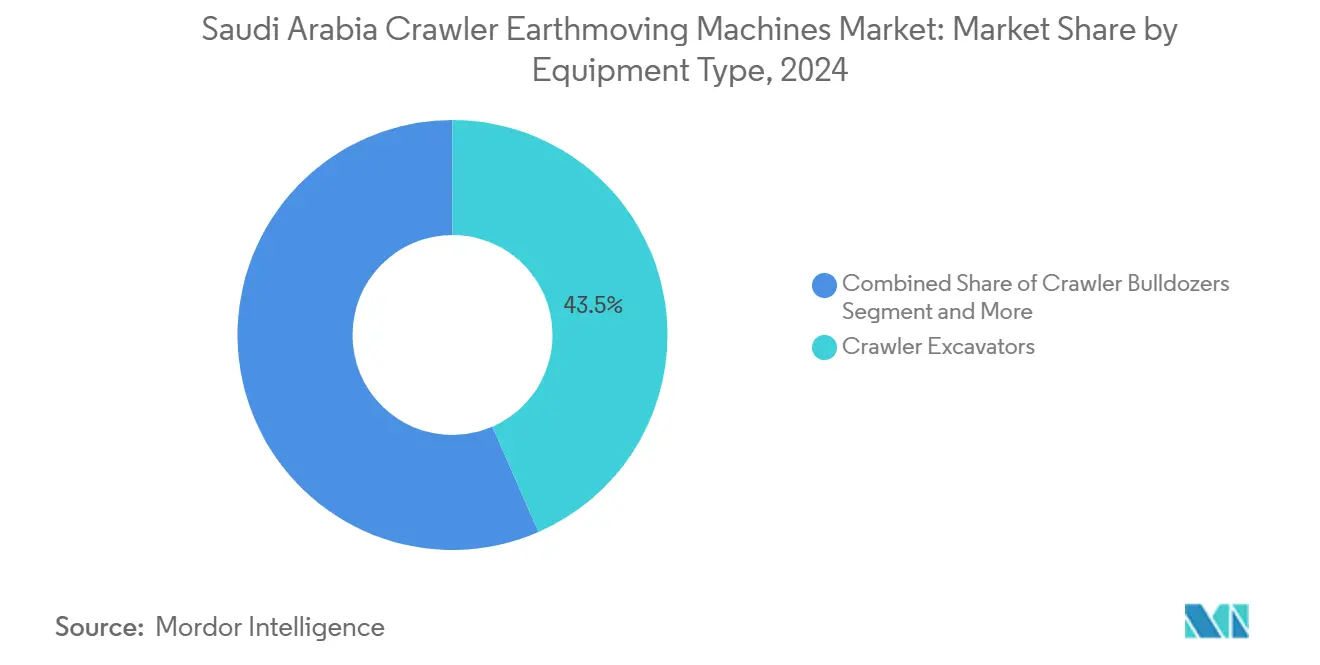

- By equipment type, crawler excavators led with 43.45% of Saudi Arabia's crawler earthmoving machines market share in 2024; compact tracked loaders and skid-steers are poised for the fastest 12.15% CAGR through 2030.

- By propulsion, diesel units accounted for 91.86% of the 2024 base, while battery-electric systems will post the highest 16.64% CAGR to 2030.

- By engine power output, the 201–400 HP band captured 46.05% share in 2024; sub-100 HP machines will expand at a 16.54% CAGR.

- By application, earthmoving and grading dominated with a 49.12% share in 2024; demolition and recycling will grow most quickly at a 10.93% CAGR.

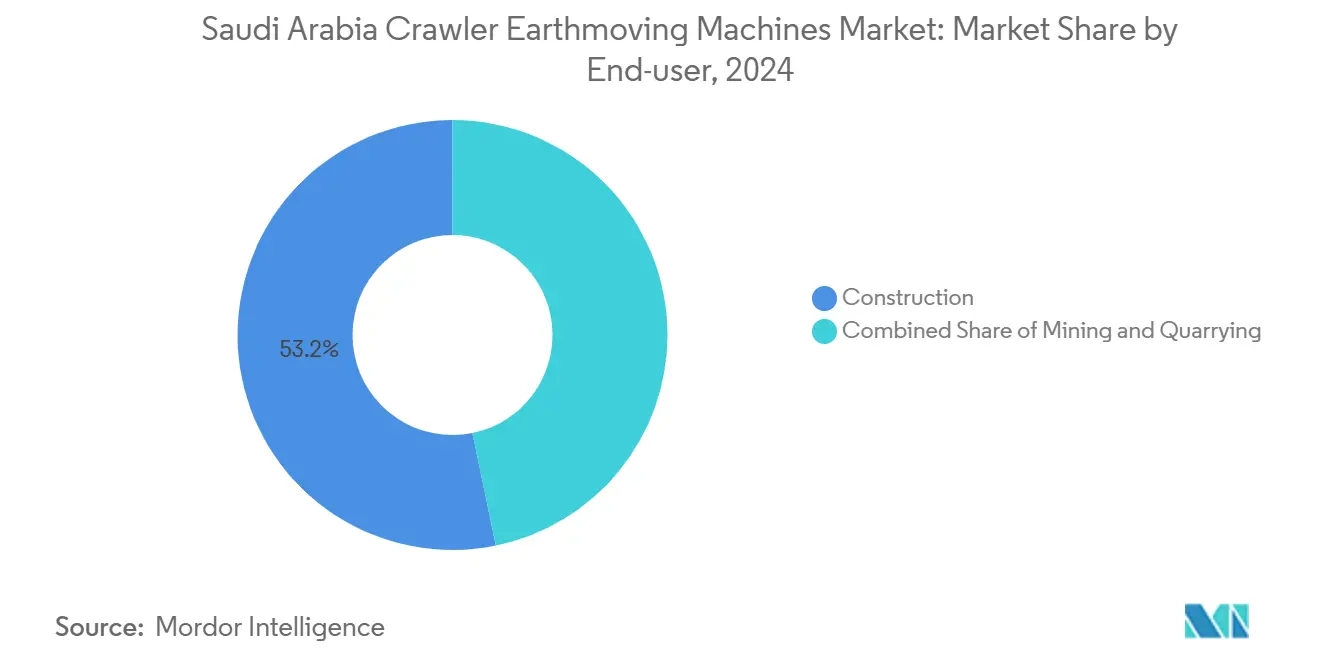

- By end-user, construction commanded 53.22% of 2024 revenue, while municipal services posted the fastest 9.29% CAGR through 2030.

- By distribution channel, authorized dealers held 51.17% share in 2024; online marketplaces are forecast to climb at an 11.74% CAGR.

- By province, the Eastern Province led with 26.61% share in 2024 and will outpace all regions with a 7.76% CAGR through 2030.

Figures recorded within Saudi arabia feed into a worldwide estimate while studying the global industry. Mordor Intelligence's crawler earthmoving machines market size captures this aggregation.

Saudi Arabia Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Giga-Projects Pipeline | +1.1% | Riyadh, Tabuk, Eastern Province | Long term (≥ 4 years) |

| EPC Awards and Midstream CAPEX | +0.9% | Eastern Province, Riyadh | Medium term (2-4 years) |

| Local-Content Mandates | +0.7% | Eastern Province, Riyadh, Makkah | Medium term (2-4 years) |

| Digital-Twin and OPEX Optimisation | +0.5% | Riyadh, Eastern Province, Makkah | Short term (≤ 2 years) |

| Site Rehabilitation and Circular-Demolition | +0.4% | Riyadh, Madinah, Tabuk | Long term (≥ 4 years) |

| Quarry and Mining Leases Privatization | +0.4% | Eastern Province, Tabuk | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vision-2030 Giga-Projects Pipeline (NEOM, Red Sea, Qiddiya)

The USD 500 billion NEOM development alone requires roughly 20,000 cranes and a vast fleet of crawler excavators, bulldozers, and pipe-layers, with the first 23 specialized cranes already mobilized for early civil works[1]“23 Cranes for Construction of NEOM,” Crane Weihua Global, craneweihuaglobal.com. Complementary programs—Diriyah’s USD 63.2 billion cultural rebuild and the Red Sea tourism corridor—intensify nationwide earthmoving demand, elevating rental rates and pushing contractors to lock in multi-year equipment supply agreements. NEOM’s all-renewables mandate also turns it into a live testbed for autonomous machines scheduled for port operations in 2026[2]“Port of NEOM Strengthens Role in Global Supply Chain Connectivity,” NEOM, neom.com. Compressed delivery schedules through 2030 lift operating hours well above historic norms, accelerating replacement cycles and fueling aftermarket parts revenue.

Surging Aramco EPC Awards and Midstream CAPEX

Saudi Aramco’s USD 25 billion contract wave for the Jafurah shale gas development and Master Gas System expansion covers 16 EPC packages that rely heavily on tracked earthmovers for trenching, backfilling, and compressor-station foundations. Offshore programs in Safaniyah and Marjan further extend demand to onshore yards that pre-assemble platform modules. Guaranteed capital spending of USD 48–52 billion a year to 2027 grants OEMs long-range volume visibility, encouraging them to localize component machining and undercarriage refurbishment lines.

Local-Content Mandates (IKTVA) Boosting OEM Assembly

The IKTVA threshold requiring around 70% in-Kingdom spend has tripled local purchases since 2020, prompting global brands to joint-venture with Saudi partners for crawler chassis welding, engine pack-up, and cab assembly. Tower-crane production in Dammam and new transmission plants in Jubail are early outcomes, shrinking import lead times from 6 months to 8 weeks, and anchoring a regional export hub. Domestic suppliers gain from volume certainty, which in turn reduces the total cost of ownership for fleet operators through quicker parts availability and lower logistics charges.

Digital-Twin and Telematics Driven OPEX Optimisation

AI-enabled telematics platforms such as Tenderd use IoT sensors to track run-hours, idle time, and fuel burn across more than 5,000 units, helping contractors cut operating costs by up to 20%. Rising diesel prices magnify savings from smart idling and predictive maintenance. Digital twins fed by 5G networks now simulate job-site progress in real time, enabling dispatchers to match crawler size with load and soil conditions and thereby improve productivity per liter of fuel.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX | -0.7% | Riyadh, Eastern Province, Makkah | Short term (≤ 2 years) |

| Supply-chain Volatility | -0.5% | Eastern Province, Riyadh | Medium term (2-4 years) |

| Scarce Fast-Charging Infra | -0.4% | Riyadh, Eastern Province | Long term (≥ 4 years) |

| Diesel Fleet Ownership Cost | -0.3% | Riyadh, Makkah, Eastern Province | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX Amid Tighter Project Finance

Financial institutions have tightened lending criteria, raising the cost of capital for mid-sized contractors and squeezing cash flows allocated to fleet renewal. Although the Public Investment Fund’s deep reserves offset sovereign budget pressures, disbursement timing mismatches can delay purchase orders for crawler units. Rental penetration is therefore climbing, with hourly rates edging up in 2025 as demand outpaces fleet growth.

Component and Raw-Material Supply Volatility

Global supply chain disruptions are impacting the availability of construction equipment. In the Kingdom, a swift acceleration of projects has led to a demand that surpasses the supply capacity of components from international manufacturers. Heavy machinery production is especially hampered by shortages in steel and semiconductors. These shortages result in extended lead times for manufacturers, potentially delaying project timelines and inflating equipment costs. Moreover, fluctuations in raw material prices, especially for steel and rare earth elements vital for electronic components, introduce cost uncertainties. These uncertainties, in turn, influence pricing and procurement decisions throughout the construction sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators Lead Infrastructure Surge

The crawler excavator segment accounted for 43.45% of Saudi Arabia's crawler earthmoving machines market share in 2024, reflecting its versatility across giga-projects, pipeline corridors, and urban renewal zones. Utilization peaks between 2026 and 2028 when NEOM’s linear city trenching, Diriyah’s heritage landscaping, and Jafurah’s gas-gathering systems converge. Compact tracked loaders, boosted by municipal road widening and utilities trenching, will log the fastest 12.15% CAGR.

Semi-autonomous control kits gain traction, enabling night-shift operation with skeletal crews and lowering safety-related downtime. Additionally, demand in the “Others” bucket, trenchers, drill rigs, and specialist graders, rises as utility corridors extend into second-tier cities. Heavy lift crawlers above 600 tons see steady call-offs for modular refinery builds and petrochemical expansions along the Gulf coast. Digital work-order integration across fleet management systems reduces idle-time spread between equipment classes, maximizing job-site productivity.

By Propulsion: Diesel Dominance Faces Electric Challenge

Diesel units retained a 91.86% of Saudi Arabia's crawler earthmoving machines market share in 2024 as fueling logistics and power-to-weight ratios favor internal-combustion engines for 20-to-100 ton machines. Yet battery-electric crawlers, mainly in the 8-to-15 ton class, will post a 16.64% CAGR through 2030 owing to lower noise limits in dense urban precincts and ESG compliance tender scoring. Hybrid drivetrains bridge the gap, cutting fuel burn by up to 18% without range anxiety.

Charging infrastructure remains the pacing factor. Permanent 600 kW chargers cluster at Riyadh and Jeddah depots, yet remote project camps still rely on diesel gensets, undercutting full-cycle emission gains. Technology roadmaps signal 400 kWh battery packs and swappable modules by 2027 that could push electric penetration well beyond compact classes. Market adoption timing depends on charging infrastructure development and battery technology improvements for heavy-duty applications exceeding 20 tons operational weight.

By Engine Power Output: Compact Segment Accelerates

Mid-range 201–400 HP machines captured 46.05% Saudi Arabia's crawler earthmoving machines market share in 2024, satisfying mainline earthworks on mixed-use giga-projects. Equipment under 100 HP, ideal for alleyway utility work and parkland grading, will outpace all others at a 16.54% CAGR as municipal spending broadens beyond the three largest cities. Above-400 HP crawlers preserve a niche in mining overburden removal and coastal land reclamation, retaining a critical role despite their lower unit volumes.

As diesel costs rise, operators are gravitating towards smaller engines for their superior fuel economy. However, larger engines remain the go-to choice for heavy-duty tasks, especially in mining and energy sectors. This shift in preferences underscores a growing market sophistication, with operators now prioritizing equipment tailored to specific applications over the traditional tendency to opt for oversized machinery. Telematics dashboards now benchmark fuel burn per cubic meter, encouraging fleet owners to redeploy under-utilized power bands where appropriate.

By Application: Earthmoving Dominates Diversified Demand

Earthmoving and grading secured 49.12% of Saudi Arabia's crawler earthmoving machines market share in 2024, anchored by mass excavation for new city platforms and logistics corridors. Demolition and recycling activities will enjoy a 10.93% CAGR on the back of heritage-site revival programs and urban densification that replaces obsolete structures with mixed-use towers. Integrated crushers and on-site material sorters enable contractors to hit circular-economy targets while trimming trucking costs.

Pipeline and energy infrastructure remain a stable second-tier application given continuous midstream investment, while quarrying benefits from the licensing of new extraction blocks that feed giga-project concrete plants. Forestry and agriculture segments stay modest but gain traction through land-rehabilitation and green-corridor initiatives baked into Vision 2030.

By End-User: Construction Sector Leads Diversification

Residential construction (Residential, Non-residential) commanded a 53.22% of Saudi Arabia's crawler earthmoving machines market share in 2024, driven by large-scale housing targets and mega-malls integrated into flagship projects such as New Murabba. Municipal services will post the fastest 9.29% CAGR as provinces outside Riyadh upgrade drainage, street-lighting, and green-space infrastructure. Oil-and-gas installations, industrial parks, and mining operations round out end-user breadth, each adding steady baseline demand for 300 HP-plus crawlers and specialized attachments.

Saudi Arabia's economic shift away from oil dependency is evident in its diversified end-user sectors, all of which are fueling a consistent demand for tracked equipment. Notably, Industrial and Logistics Parks are capitalizing on the IKTVA localization mandates, which necessitate significant site preparations and facility constructions, thereby boosting the use of tracked equipment. Contractors increasingly switch to rental or rental-purchase hybrids to align fleet size with project pipelines, a trend that accelerates aftermarket service revenues for dealers who provide uptime guarantees through telematics-driven preventive maintenance.

By Distribution Channel: Dealers Maintain Dominance

Authorized dealers handled 51.17% of the 2024 market share, leveraging parts stocks and field-technician coverage indispensable to desert job sites. Online platforms will expand at an 11.74% CAGR as contractors use smartphone apps to match idle inventory with real-time demand across projects. Rental and leasing firms pivot to “equipment-as-a-service” bundles that fold in fuel management and operator training, boosting stickiness with EPC contractors striving for cost visibility.

The distribution landscape evolution reflects market maturation and changing customer preferences, with digital platforms offering enhanced equipment utilization tracking and transparent pricing models. Direct OEM sales remain strong for marquee projects where warranty and customization requirements favor factory-level engagement. Dealer networks respond by co-locating service bays inside giga-project zones, shrinking downtime tied to long haulbacks for overhaul work.

Geography Analysis

Eastern Province retained the largest single-region footing in the Saudi Arabia crawler earthmoving machines market in 2024, capturing 26.61% of revenue while expanding at a 7.76% CAGR through 2030. The cluster of gas processing plants, petrochemical hubs, and privately operated quarries sustains year-round equipment utilization. Aramco’s Jafurah field development alone underwrites multiyear purchase agreements for high-horsepower pipe-layers and bulldozers, while Master Gas System upgrades extend demand to compressor-station earthworks and trunk-line corridors. Intensive industrial activity spurs local fabrication of undercarriage assemblies, cutting lead times and logistics costs, and making Eastern Province a natural launchpad for dealer expansion into the wider Gulf.

Riyadh commands a substantial slice of the market by virtue of its administrative clout and mega-project density. The USD 63.2 billion Diriyah renewal and the sprawling New Murabba mixed-use district generate overlapping excavation phases that demand simultaneous deployment of large fleets. Urban projects such as the Sports Boulevard emphasize low-emission compact crawlers for park construction and utility installations. The capital’s role as headquarters for top EPC firms and finance houses creates procurement synergies that feed national fleet rotation and resilience.

Western and northern regions deliver a more project-specific pattern. Makkah, Madinah and the Red Sea corridor benefit from religious tourism expansions and heritage preservation that require precision demolition and low-ground-pressure machines. Tabuk’s NEOM platform, valued at USD 500 billion, calls for relentless earthmoving as it shapes the 170-km linear city footprint. Southern provinces, including Asir and Jazan, tap into refinery builds, port expansions and cross-border road links that diversify crawler utilization profiles. Together, these regions reinforce balanced national growth, ensuring that no single demand center dictates capacity planning for OEMs or dealers.

Mordor Intelligence evaluates the crawler earthmoving machines market across all key regional markets, including Europe, with deeper country-level insights covering Indonesia, United States, Thailand, Philippines, Singapore, Australia, and South Korea.

Competitive Landscape

The Saudi Arabia crawler earthmoving machines market exhibits moderate concentration. Caterpillar leads, leveraging an extensive product suite and dealer service standards designed for harsh environments. European suppliers Liebherr and Volvo position themselves around specialty lifts and high-capacity articulated cranes, capturing niche but profitable segments. Chinese entrant XCMG accelerates penetration by combining aggressive pricing with localized inventory hubs. Technology platforms such as Tenderd compress idle rates through AI-based fleet matching, challenging traditional ownership economics and nudging OEMs to embed telematics across product lines.

Parts and service revenue approaches a significant portion of dealer turnover as project owners demand uptime guarantees. Consequently, leading dealers invest in 24/7 mobile workshops and predictive diagnostics that trigger component replacement before failure. Price competition stays intense for baseline 20-ton excavators, yet total-cost-of-ownership packages increasingly influence purchase decisions, with warranty extensions and operator-training bundles tipping bids.

Innovation race shifts toward sustainable power trains. Diesel-electric hybrids roll off pilot lines, promising up to 18% fuel savings without infrastructure dependencies, while battery-electric crawlers in the 10-ton class ready for commercial release in 2026. OEMs partner with energy utilities to pilot 2 MW charging hubs near giga-project campuses. The supplier field remains open for disruption, but entrenched dealer networks and high switching costs for parts inventories preserve moderate concentration.

Saudi Arabia Crawler Earthmoving Machines Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Liebherr-International AG

Volvo Construction Equipment AB

XCMG Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Weir signed a joint venture with Olayan to supply equipment and services to the Kingdom’s burgeoning mining sector, bolstering localized support capabilities.

- January 2025: Amhec ordered 100 Tadano GR-800EX rough-terrain cranes, signaling robust fleet expansion among domestic rental firms.

- September 2024: MDS appointed Abdul Latif Jameel Machinery as its first Middle East distributor, broadening access to materials-processing equipment.

Saudi Arabia Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Diesel (Stage III–V) |

| Hybrid Diesel-Electric |

| Battery-Electric |

| Hydrogen Fuel-cell (Pilot) |

| Below 100 HP |

| 100 to 200 HP |

| 201 to 400 HP |

| Above 400 HP |

| Earthmoving and Grading |

| Demolition and Recycling |

| Forestry and Agriculture |

| Mining and Quarrying |

| Pipeline and Energy Infrastructure |

| Rental Fleet Operations |

| Construction (Residential, Non-residential) |

| Mining and Quarrying |

| Oil and Gas Infrastructure |

| Industrial and Logistics Parks |

| Municipal Services |

| Agriculture and Forestry |

| Direct OEM Sales |

| Authorised Dealers |

| Rental and Leasing Firms |

| Online / Digital Marketplaces |

| Riyadh |

| Makkah |

| Eastern Province |

| Madinah and Tabuk |

| Asir, Jazan and Najran |

| Al-Qassim and Northern Borders |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Diesel (Stage III–V) |

| Hybrid Diesel-Electric | |

| Battery-Electric | |

| Hydrogen Fuel-cell (Pilot) | |

| By Engine Power Output | Below 100 HP |

| 100 to 200 HP | |

| 201 to 400 HP | |

| Above 400 HP | |

| By Application | Earthmoving and Grading |

| Demolition and Recycling | |

| Forestry and Agriculture | |

| Mining and Quarrying | |

| Pipeline and Energy Infrastructure | |

| Rental Fleet Operations | |

| By End-user | Construction (Residential, Non-residential) |

| Mining and Quarrying | |

| Oil and Gas Infrastructure | |

| Industrial and Logistics Parks | |

| Municipal Services | |

| Agriculture and Forestry | |

| By Distribution Channel | Direct OEM Sales |

| Authorised Dealers | |

| Rental and Leasing Firms | |

| Online / Digital Marketplaces | |

| By Province | Riyadh |

| Makkah | |

| Eastern Province | |

| Madinah and Tabuk | |

| Asir, Jazan and Najran | |

| Al-Qassim and Northern Borders |

Key Questions Answered in the Report

What is the current value of the Saudi Arabia crawler earthmoving machines market?

The market is valued at USD 350.45 million in 2025 and is projected to reach USD 434.22 million by 2030.

Which equipment type holds the largest share?

Crawler excavators lead with 43.45% of sales in 2024 thanks to their versatility across giga-projects and energy infrastructure.

Which propulsion technology is growing fastest?

Battery-electric crawlers will register the highest 16.64% CAGR through 2030, driven by ESG mandates and lower operating costs.

Why is Eastern Province the largest regional market?

Intensive energy projects such as the Jafurah gas field and a concentration of petrochemical plants push equipment demand, giving the province 26.61% of 2024 revenue.

What is the main restraint on market growth?

High upfront CAPEX amid tighter project-finance terms temporarily slows equipment procurement, especially for smaller contractors.

Page last updated on: