Indonesia Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

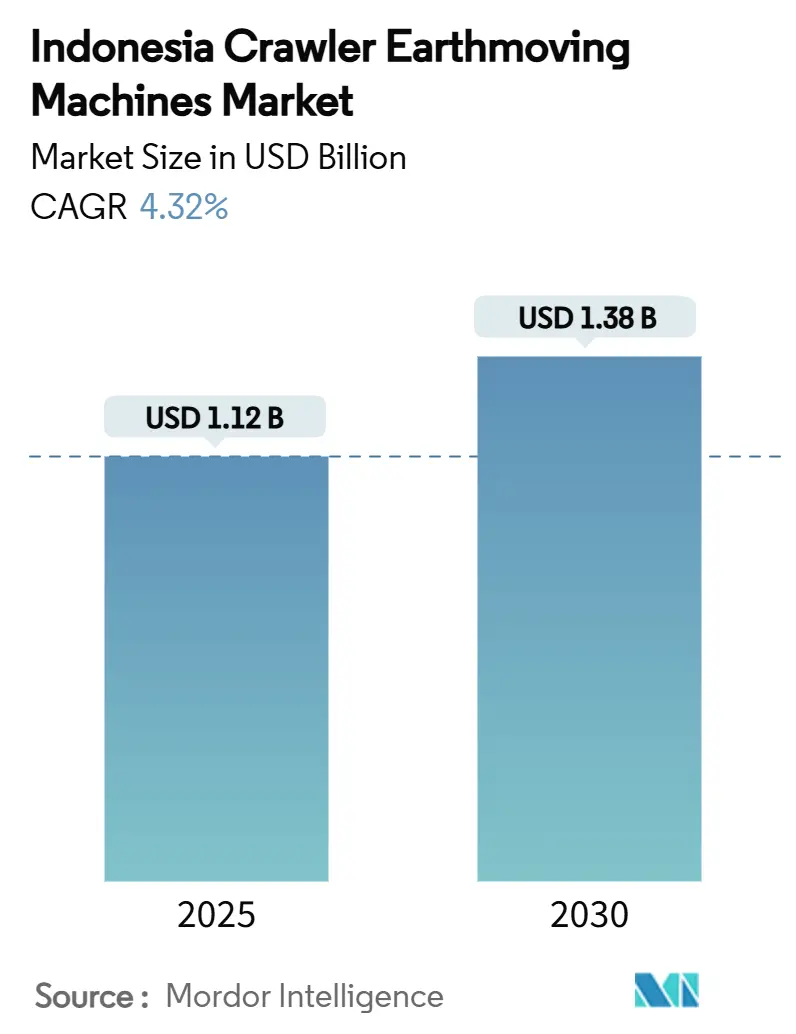

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 1.38 Billion |

| Growth Rate (2025 - 2030) | 4.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The Indonesia crawler earthmoving machines market size is USD 1.12 billion in 2025 and is forecast to expand to USD 1.38 billion by 2030 at a 4.32% CAGR. Solid public-sector infrastructure spending, the Nusantara capital city earthworks, and expanding nickel and copper mining operations underpin this trajectory. Steady annual construction growth keeps urban real-estate developments on schedule, while government outlays are budgeted to provide predictable project pipelines. At the same time, Indonesia has approximately a 50% share of global nickel output, and downstream processing mandates lift crawler equipment demand at Sulawesi and Papua mine sites. OEMs benefit from telematics-enabled maintenance, financing innovations, and rental penetration that lower entry barriers for SME contractors. Carbon pricing adds cost pressure yet accelerates electrification, encouraging battery-electric crawler adoption in regulated urban zones.

Key Report Takeaways

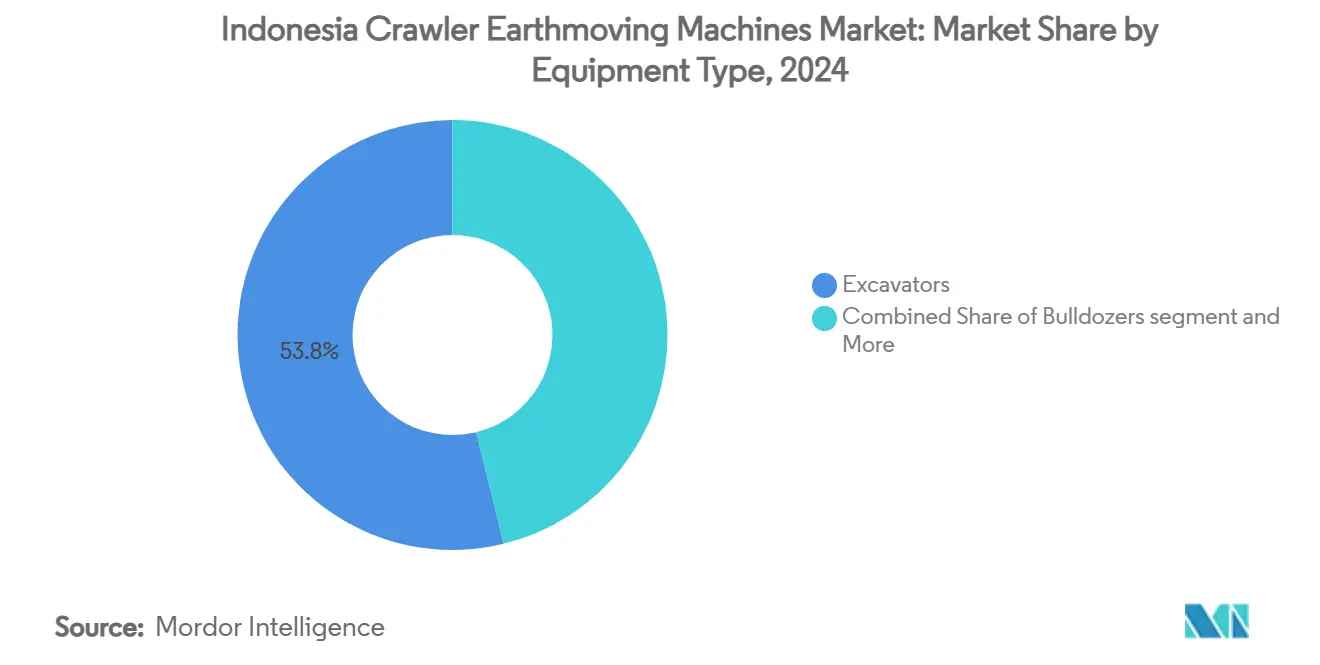

- By equipment type, excavators led with 53.82% Indonesia crawler earthmoving machines market share in 2024, while dozers recorded the highest CAGR at 7.76% through 2030.

- By propulsion, internal combustion engines held 86.43% of the Indonesia crawler earthmoving machines market size in 2024; battery-electric variants are advancing at an 8.42% CAGR to 2030.

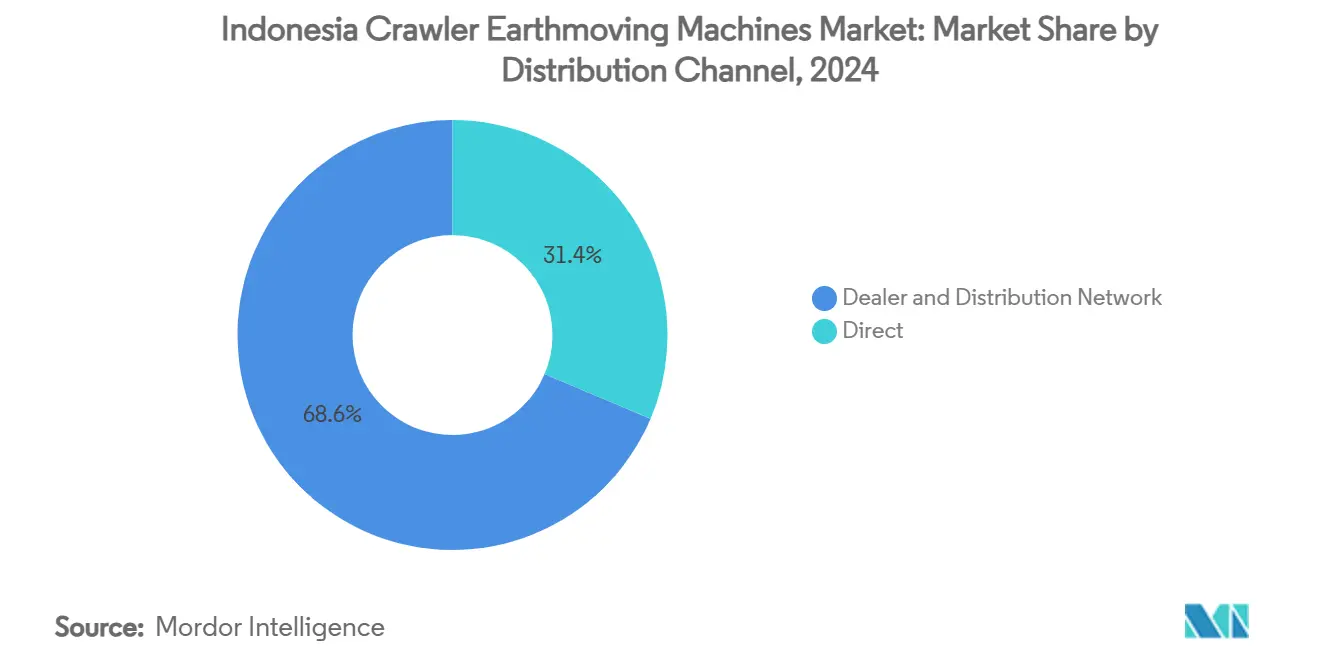

- By distribution channel, dealer networks commanded 68.63% share of the Indonesia crawler earthmoving machines market in 2024, whereas direct sales are projected to expand at 7.47% CAGR up to 2030.

- By end-use industry, construction accounted for 62.73% share of the Indonesia crawler earthmoving machines market size in 2024 and mining and quarrying is progressing at a 7.34% CAGR through 2030.

Indonesia Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infra pipeline | +1.8% | East Kalimantan primary, Java secondary | Long term (≥ 4 years) |

| Mine expansions | +1.2% | Sulawesi core, spill-over to Kalimantan | Medium term (2-4 years) |

| Urbanization projects | +0.9% | Greater Jakarta, Surabaya, Medan metro areas | Medium term (2-4 years) |

| Dealer-credit & rental | +0.6% | National, with early gains in Jakarta, Surabaya | Short term (≤ 2 years) |

| Telematics-Enabled Predictive Maintenance | +0.4% | Mining regions first, construction sites follow | Medium term (2-4 years) |

| Carbon-Pricing Drives | +0.3% | National, accelerated in urban areas | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Massive Public-Sector Infrastructure Pipeline

As of January 2024, Indonesia's ambitious USD 35 billion Nusantara project, covering 256,000 hectares in East Kalimantan, has surpassed its phase 1 target, achieving 71.47% of the set milestone[1]“Nusantara Progress Update January 2024,”, Nusantara Capital Authority, iglc.net. Crawler excavators and dozers remain essential for land clearing, grading, and foundation work on the capital’s core government district. Toll-road extensions such as the Karangjoang–Kariangau link multiply equipment demand by unlocking adjoining industrial corridors. Digital monitoring applied on-site has already cut idle time and lifted utilization, steering procurement toward telematics-ready machines. Dealers are racing to open service outposts near Balikpapan and Penajam in anticipation of multi-year fleet support requirements. The long-term scale of Nusantara provides durable visibility for OEM order books, cushioning cyclical dips in private construction.

Accelerated Nickel and Copper Mine Expansions

Indonesian nickel producers are solidifying their status as pivotal players on the global stage. The U.S. Geological Survey (USGS) reported in 2023 that Indonesia boasted 42% of the world's nickel reserves and accounted for 51% of global nickel production. The country is home to four publicly listed nickel companies: PT Aneka Tambang (Antam), Merdeka Battery Materials (MBMA), Trimegah Bangun Persada (TBP Harita), and PT Vale Indonesia (Vale). These companies, witnessing significant growth in both scale and profitability, have set ambitious targets to more than double their production within the next 3-5 years. Collectively, these four firms produced 353,000 tonnes of nickel metal in 2023[2]“Indonesia’s nickel companies: The need for renewable energy amid increasing production”, INSTITUTE FOR ENERGY ECONOMICS AND FINANCIAL ANALYSIS, ieefa.org. This forces continuous mine stripping and waste removal that favors high-capacity crawler excavators. PT Freeport Indonesia’s Grasberg smelter expansion exceeded 90% completion in 2023, illustrating how downstream mandates double equipment needs by adding plant-site earthworks[3]“Form 10-K 2023”, FCX Investor Relations, fcx.com. Larger class-70-ton excavators with reinforced undercarriages are increasingly specified to endure abrasive lateritic soils prevalent in Sulawesi.

Rapid Urbanization Fueling Real-Estate Projects

Greater Jakarta’s population now exceeds 34 million, and ongoing annual construction growth keeps residential towers, transit-oriented developments, and mixed-use complexes on tight timelines. Cement consumption in Kalimantan rose 18.8% in June 2024, spotlighting spill-over demand from Nusantara works. Developers prefer crawler excavators to wheeled alternatives for basement excavation and pile cap digouts due to superior stability on saturated clay soils typical in Java. Environmental regulations that limit onsite emissions push contractors in Jakarta’s low-emission zones toward hybrid or fully electric 20-ton models. Public-private partnership frameworks covering 35 transport and housing projects simplify access to long-dated work packages, giving equipment owners revenue visibility. Urban land scarcity further raises demand for compact radius crawler excavators capable of swinging within restrained footprints.

OEM Dealer-Credit and Rental Penetration

SME contractors comprise 99.6% of Indonesia’s enterprises, yet bank lending to MSMEs equals only 7% of GDP, creating apparent financing gaps[4]“MSME Financing in Indonesia 2024,”, Asian Development Bank, adb.org. United Tractors launched flexible leasing and rent-to-own schemes that bundle service contracts, easing the acquisition of 30-ton class excavators. Multi-finance companies add factoring options so contractors can collateralize receivables and release liquidity for fleet expansion. Rental uptake is most substantial in Java’s metro rail and commercial high-rise trades, where project phases last 6–12 months. OEMs benefit from higher lifecycle margins through genuine parts and telematics subscriptions tied to rental contracts. Dealer-credit programs now reach Eastern Indonesia, lifting crawler penetration among provincial contractors building feeder roads to resource projects.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity price volatility | -1.4% | Mining regions, particularly Sulawesi and Kalimantan | Short term (≤ 2 years) |

| SME financing gap | -0.8% | National, acute in outer islands | Medium term (2-4 years) |

| Operator shortage | -0.6% | National, severe in remote mining areas | Long term (≥ 4 years) |

| EV-parts duty uncertainty | -0.4% | National, affecting electrification timeline | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility Suppresses Capex Cycles

Heavy equipment demand remained sluggish in 2023, with sales dropping 13% to 18,123 units from 20,546 units in 2022, according to PAABI. Coal and nickel prices likely contributed to the decline. Smaller contractors struggle to service equipment loans during downturns, often liquidating crawler assets and shrinking the used-machine value pool. The volatility encourages tier-one miners to seek versatile excavator-dozer combinations that can be redeployed across ore bodies, yet overall spend remains closely tied to commodity price outlooks. OEMs hedge by diversifying into construction rentals where demand correlates with government budgets rather than export earnings.

Shortage of Certified Machine Operators

Only 7.4% of Indonesia’s construction workforce holds competency certificates, and awareness of legal requirements remains low. Remote mining sites in Papua and Kalimantan face the most acute shortfall, prompting firms to import operators or accept lower productivity from on-the-job trainees. Vocational centers have limited crawler simulators, constraining annual graduate throughput despite worker interest in certification. The skills gap restricts the adoption of advanced electro-hydraulic controls and semi-autonomous functions because operators cannot exploit the full machine capability. Government TVET reforms embed green-construction curricula, yet industry expects results only after 2027. OEMs respond with on-site training modules and teleoperation packages that allow experienced operators in Java to control machines at distant mines.

Segment Analysis

By Equipment Type: Excavators Set the Pace in Mining and Infrastructure

Excavators accounted for 53.82 of % Indonesian crawler earthmoving machines market share in 2024, reflecting their versatility across mining, road building, and urban projects. Large-capacity units dominate laterite nickel pits, while 20-ton models flourish in Jakarta basement digs. The segment benefits from rising demand for integrated quick-couplers and Grade Control systems that shorten cycle times. Dozers register a 7.76% CAGR to 2030 as massive land-grading requirements at Nusantara and toll road corridors lift ripping and fill-spreading work. Dozers are increasingly factory-fitted with slope-assistance packages to raise operator productivity amid skills shortages. Graders see stable demand for national highway upkeep, and specialized amphibious excavators gain niche traction in mangrove rehabilitation projects. The equipment mix underlines the primacy of excavators and dozers as dual pillars of the Indonesia crawler earthmoving machines market size.

OEM innovation centers on electric mini excavators for emissions-sensitive urban pockets and on high-horsepower dozers with remote blade control for mining benches. Import tariffs on undercarriage assemblies keep localization economics favorable for domestic fabrication of frames and track groups. Rental fleets skew toward 30-ton excavators because they balance transportability with broad job applicability, minimizing idle days. Meanwhile, mining firms acquire 70-ton and above models outright, leveraging longer payback horizons tied to long-life ore bodies. This dichotomy sustains tiered demand across weight classes within the Indonesia crawler earthmoving machines market.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion: ICE Dominance Meets Regulatory Pressure

Internal combustion engines held 86.43% share of the Indonesia crawler earthmoving machines market in 2024 due to mature fueling networks and familiarity among operators. Tier 3 and Tier 4 interim engines remain prevalent, though carbon pricing since 2022 has introduced direct operating-cost penalties that sharpen interest in alternative powertrains. Battery-electric units exhibit an 8.42% CAGR, led by 20-ton excavators inside emission-restricted urban zones. However, uncertain import duties on traction batteries hinder upfront affordability, causing some contractors to defer purchases until policy clarity emerges. Hybrid systems occupy the middle ground by offering 15–20% fuel savings without a charging infrastructure.

State-owned utilities plan pilot charging yards at Nusantara that can service crawler equipment during shift breaks, signaling future scalability. OEMs such as Komatsu and Hyundai propose swappable battery packs to mitigate charging downtimes on remote mining benches. Even so, long-cycle jobs in Kalimantan’s overburden removal still favor diesel due to energy density and refueling speed. Therefore, the Indonesia crawler earthmoving machines market size is expected to remain ICE-heavy through 2030, with electrification proceeding first in regulated urban clusters.

By Distribution Channel: Dealers Anchor After-Sales Reach

Dealer networks captured 68.63% share in 2024 because Indonesia’s 17,000 islands require localized parts depots and rapid technician dispatch. Flagship dealers in Jakarta, Surabaya, and Balikpapan stock critical undercarriage components and hydraulic pumps, cutting downtime for fleet owners. Direct sales grow at 7.47% CAGR as large miners negotiate factory-spec fleets bundled with telematics dashboards and long-term maintenance contracts. OEM e-commerce portals allow contractors to order wear parts online and schedule service calls, yet field support still routes through regional dealers for final execution.

Digital platforms now integrate machine data feeds so dealers can propose predictive maintenance kits before failures occur. This enhances parts revenue and cements dealer value, especially in remote eastern provinces. Fleet customers increasingly sign availability-guarantee agreements under which dealers incur penalties for extended downtime, incentivizing proactive service. Taken together, hybrid distribution models position both channels to scale alongside the Indonesia crawler earthmoving machines market.

By End-Use Industry: Construction Leads While Mining Accelerates

Construction projects generated a 62.73% share of the Indonesia crawler earthmoving machines market size in 2024, with steady workstreams from road building, airports, housing, and industrial parks. Government-backed PPP structures reduce payment risk, encouraging contractors to refresh fleets regularly. Mining and quarrying post a 7.34% CAGR as nickel, copper, and gold expansions crowd order books for large crawler excavators and bulk dozers. The segment also demands specialized slope stabilization and tailings-pond equipment, widening SKU requirements.

Oil and gas pipeline installations contribute consistent yet niche crawler purchases for trenching and right-of-way clearing in Sumatra and Kalimantan. Plantation agriculture employs mid-size dozers for land preparation in palm oil estates, while forestry concessions deploy crawler harvesters on steep terrain. As downstream processing zones proliferate, combined industrial-construction complexes will further blur the line between traditional end-use categories, enlarging the Indonesia crawler earthmoving machines market over the outlook period.

Geography Analysis

Java represents the most significant regional slice of the Indonesia crawler earthmoving machines market in 2024 because Greater Jakarta alone absorbs dozens of rail, highway, and high-rise packages yearly. Contractors in West Java maintain the nation’s densest rental fleets, ensuring quick swaps that keep project schedules on target. Sumatra follows owing to coal logistics corridors and palm plantation expansions that require robust earthmoving for roadbeds and drainage canals. However, Kalimantan shows the fastest 2025-2030 growth due to the colossal Nusantara land-development program that spans greenfield drainage, grading, and embankment works over multiple phases.

Sulawesi’s spotlight rises as PT Vale, Tsingshan, and Huayou intensify nickel-processing clusters around Morowali and Pomalaa, necessitating continuous overburden removal and site leveling. Papua hosts low-volume yet high-value demand tied to the Grasberg underground ramp-up and potential Wabu gold mine development. Market penetration on Maluku and Nusa Tenggara islands remains thinner because limited logistics inflate equipment support costs. Nonetheless, new maritime highway links and port upgrades promise to improve accessibility, unlocking latent crawler requirements. The geographic spread underscores Indonesia’s policy shift from Java-centric to archipelagic development, broadening the Indonesia crawler earthmoving machines market base over the forecast horizon.

Competitive Landscape

Global OEMs dominate Indonesia through a blend of local assembly, deep dealer roots, and incremental technology localization. Caterpillar operates plants in Jakarta and Batam that produce key crawler models tailored to tropical conditions, such as reinforced cooling systems for 40 °C ambient temperatures. Komatsu leverages its Gresik factory to supply 20- and 30-ton excavators under the CKD scheme, reducing import duties and shortening lead times. Hitachi Construction Machinery Indonesia assembles ZX-series excavators with indigenized undercarriages, catering to both domestic buyers and ASEAN exports.

Competition centers on technology differentiation. Komatsu’s 2024 launch of battery-electric WX04B underground loaders and teleoperable D475A-8 dozers highlights the race to automate and decarbonize fleets. Liebherr’s USD 2.8 billion deal with Fortescue for 360 autonomous electric trucks signals the scale potential that could spill over to crawler offerings. Local state-owned PT Pindad introduces amphibious crawler excavators for peatland restoration, showcasing niche innovation capacity.

Pricing rivalry intensifies in mid-range excavators where Chinese entrants seek a share via aggressive financing. Yet after-sales depth and residual value keep premium brands in a strong position. United Tractors, Trakindo Utama, and Intraco Penta anchor parts distribution, operator training, and certified rebuild programs, creating high switching costs for fleet owners. As Indonesian carbon policy stiffens, players offering electric and hybrid portfolios plus charging ecosystems are expected to edge ahead in the Indonesia crawler earthmoving machines market.

Indonesia Crawler Earthmoving Machines Industry Leaders

Komatsu Ltd.

Caterpillar Inc.

Hitachi Construction Machinery

SANY

Volvo CE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Nusantara capital investments reached USD 4 billion across 42 projects, backed by IDR 48.8 trillion in government funding.

- February 2025: PT Superior Prima Sukses broke ground on a Rp 250 billion ceramic plant in Banjarnegara, widening construction materials capacity.

- October 2024: Central Java’s Batang integrated industrial estate secured Rp 16 trillion from 21 multinationals, spurring crawler demand for site works.

Indonesia Crawler Earthmoving Machines Market Report Scope

| Excavators |

| Bulldozers |

| Graders |

| Dump Trucks |

| Skid-Steer Loaders and Others |

| Internal-Combustion Engine |

| Hybrid |

| Battery-Electric |

| Direct |

| Dealer and Distributor Network |

| Construction |

| Mining and Quarrying |

| Oil and Gas Infrastructure |

| Others (Agriculture, Forestry) |

| By Equipment Type | Excavators |

| Bulldozers | |

| Graders | |

| Dump Trucks | |

| Skid-Steer Loaders and Others | |

| By Propulsion | Internal-Combustion Engine |

| Hybrid | |

| Battery-Electric | |

| By Distribution Channel | Direct |

| Dealer and Distributor Network | |

| By End-Use Industry | Construction |

| Mining and Quarrying | |

| Oil and Gas Infrastructure | |

| Others (Agriculture, Forestry) |

Key Questions Answered in the Report

What is the current value of the Indonesia crawler earthmoving machines market?

The market is valued at USD 1.12 billion in 2025 and is projected to reach USD 1.38 billion by 2030.

Which equipment type holds the largest share of crawler machines sold in Indonesia?

Excavators lead with 53.82% market share due to their versatility in mining and construction.

Why is Kalimantan considered the fastest-growing regional market?

Kalimantan hosts the 256,000-hectare Nusantara capital city project that requires multi-year earthmoving fleets.

Which end-use sector is expanding quickest for crawler equipment?

Mining and quarrying applications are growing at a 7.34% CAGR due to Indonesia’s nickel and copper expansions.

How are Indonesian dealers supporting SME contractors?

Dealers offer lease-to-own and rental programs that lower upfront costs and include bundled maintenance services.