United Arab Emirates Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

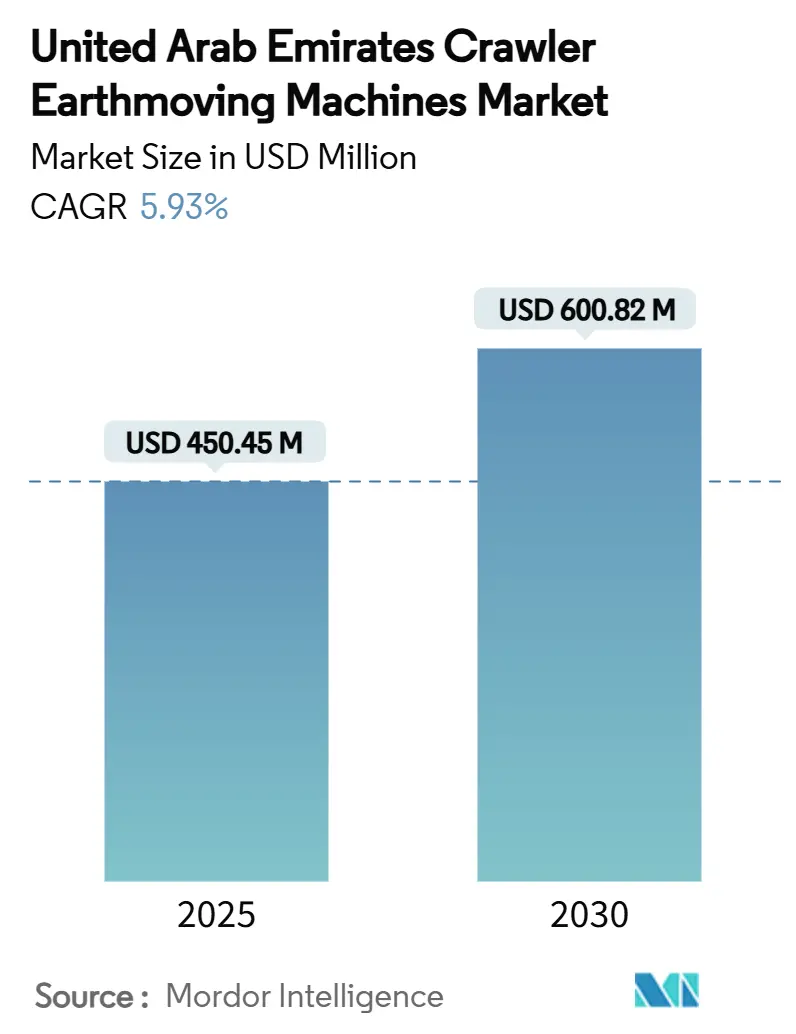

| Market Size (2025) | USD 450.45 Million |

| Market Size (2030) | USD 600.82 Million |

| Growth Rate (2025 - 2030) | 5.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The united arab emirates crawler earthmoving machines Market size is valued at USD 450.45 million in 2025 and is projected to reach USD 600.82 million by 2030, advancing at a 5.93% CAGR over the forecast period. Sustained government capital spending, a robust project pipeline under the Dubai 2040 Urban Master Plan, and ongoing diversification initiatives in Abu Dhabi have solidified an environment where earth-moving machinery is indispensable. The UAE crawler equipment market benefits from the speed at which mega-projects transition from concept to ground-breaking, requiring immediate access to mid- and high-horsepower units that can handle large-scale trenching, grading, and soil compaction. Contractors increasingly favor connected machines that deliver telematics data to help manage fuel consumption and operator productivity, while electrification incentives begin to shift perceptions of lifecycle costs. Rental penetration continues to rise as builders hedge against credit tightening and raw-material price swings by trading ownership for access, ensuring the UAE crawler equipment market maintains steady utilization rates.

Key Report Takeaways

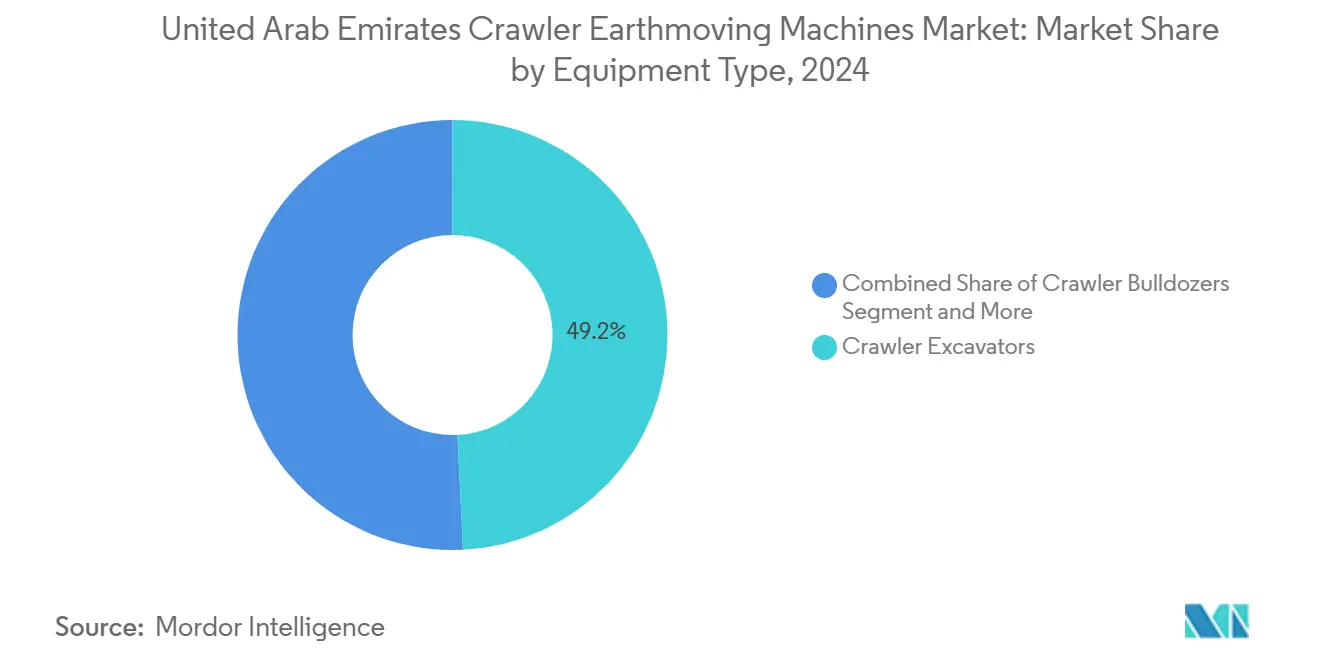

- By equipment type, crawler excavators led with 49.22% of the UAE crawler equipment market share in 2024, while compact tracked loaders and skid-steers are forecast to expand at a 9.51% CAGR through 2030.

- By propulsion, internal combustion engines held 86.24% of the UAE crawler equipment market size in 2024, whereas electric and hybrid models are projected to advance at an 18.23% CAGR to 2030.

- By engine power output, the 201-400 HP class accounted for 37.94% of the UAE crawler equipment market size in 2024; sub-100 HP units are poised to grow at a 12.12% CAGR during the same horizon.

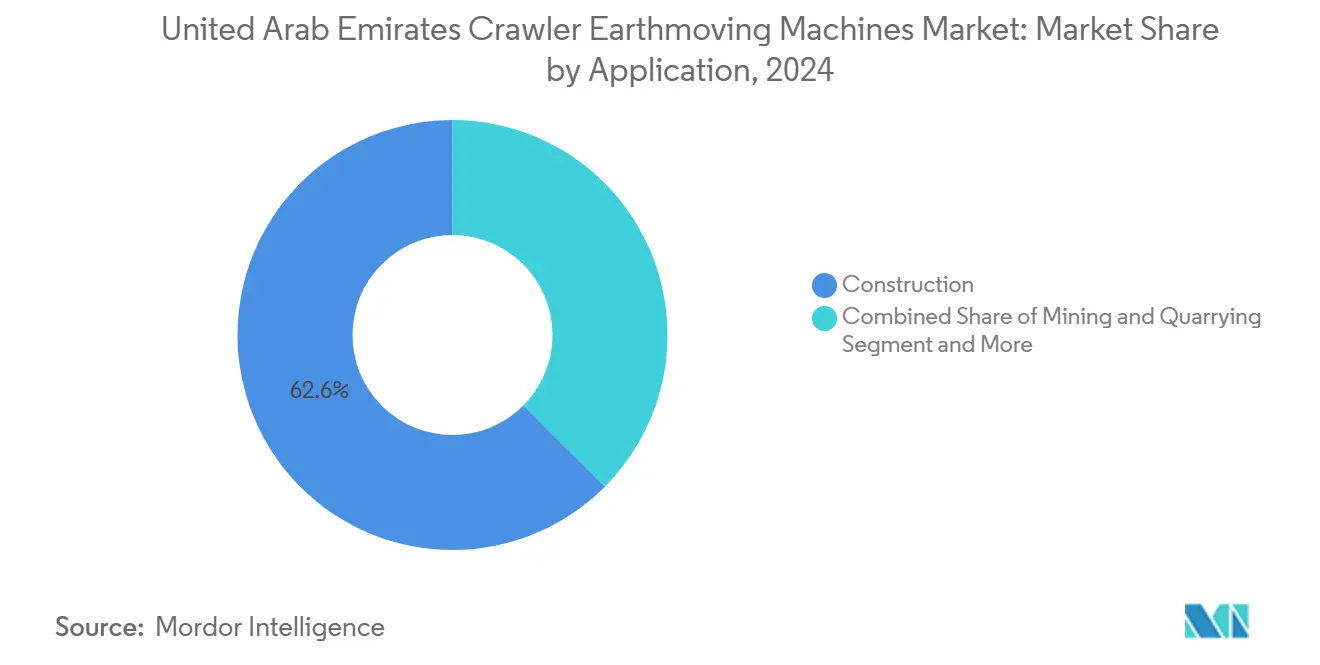

- By application, construction captured 62.56% of the UAE crawler equipment market share in 2024, while agriculture and forestry are on track for a 9.15% CAGR up to 2030.

- By distribution channel, authorized dealers commanded 50.25% of the UAE crawler equipment market size in 2024; rental and leasing firms are projected to log an 11.81% CAGR through 2030.

- By region, Abu Dhabi contributed 34.87% of the UAE crawler equipment market share in 2024, whereas Dubai is forecast for the fastest 9.62% CAGR over the period.

United Arab Emirates Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-Sector Stimulus | +1.5% | Abu Dhabi, Dubai, Sharjah | Medium term (2-4 years) |

| Dubai 2040 Urban Master Plan | +1.1% | Dubai, Sharjah and Ajman | Long term (≥ 4 years) |

| Fleet Replacement Cycle | +0.9% | Abu Dhabi, Dubai, Ras Al Khaimah | Short term (≤ 2 years) |

| Electrification Incentives | +0.7% | Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Digital-Twin OPEX Savings | +0.6% | Dubai, Abu Dhabi | Short term (≤ 2 years) |

| Circular-Demolition Surge | +0.4% | Dubai, Abu Dhabi, Sharjah | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction-Sector Stimulus Under UAE Dirham-Pegged Public-Spending Plans

Record federal and emirate-level budgets continue to anchor the UAE crawler equipment market, creating high-visibility demand that encourages dealers to maintain larger inventories. Public entities allocate multi-year funds across housing, drainage, and transport corridors, giving contractors the confidence to commit to fresh fleet orders. The currency peg to the US dollar stabilizes import pricing for OEMs, simplifying financing arrangements on long-lead items. As spending targets sustainable urban mobility and renewable energy parks, crawler excavators and dozers with grade-control systems see immediate deployment. The spillover into private mixed-use projects amplifies equipment cycles once tender packages move downstream to subcontractors[1]“Law No. (20) of 2023 Approving the General Budget Cycle of the Government of Dubai for the Financial Years 2024 to 2026,” Dubai Government, dlp.dubai.gov.ae.

Dubai 2040 Urban Master Plan Earthworks Pipeline

The emirate’s blueprint to house 5.8 million residents intensifies excavation needs for metro extensions, utility galleries, and reclaimed parkland. Each development phase sets out detailed land-preparation schedules that help dealers synchronize maintenance capacity with demand peaks. Mixed-use towers require deep-pit foundation work, encouraging contractors to deploy high-reach excavators with quick-coupler attachments. Doubling planned green areas compels landscaping contractors to lease compact loaders that can maneuver through tight urban parcels. The plan’s 16 billion AED transport docket through 2027 alone signals steady machine run-hours and parts throughput, reinforcing the long-term growth outlook for the UAE crawler equipment market.

Accelerated Replacement of Ageing Crawler Fleets for Safety and Efficiency

Equipment exceeding operational life thresholds faces stricter inspection regimes, prompting contractors to retire non-compliant units rapidly. Updated municipal safety codes require automated boom-angle limiters and enhanced operator protection, specifications typically absent from pre-2015 machines. Heat, sand, and extended shift patterns accelerate component fatigue, increasing unplanned downtime that erodes project margins. Telematics dashboards quantify maintenance backlogs and fuel over-consumption, providing data-backed justification for trade-ins. Dealers respond by bundling buy-back guarantees and service-inclusive leases, further supporting replacement volumes within the UAE crawler equipment market.

Electrification Incentives and Stage V Import Mandates

Emissions regulations narrow the total cost-of-ownership gap between diesel and battery machines. Subsidized registration fees and preferential parking for electric vehicles lower entry barriers for early adopters. Stage V compliance adds particulate filters and SCR systems, raising ICE purchase prices and complexity, which improves the payback profile of zero-tailpipe alternatives. Abu Dhabi’s fast-charging network roll-out reassures contractors about mid-shift top-ups for compact models. Additionally, silent operation enables night-time work in dense neighborhoods, a significant advantage in Dubai’s 24-hour construction culture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX And Credit | -1.4% | Abu Dhabi, Dubai, Sharjah | Short term (≤ 2 years) |

| Supply Chain Volatility | -0.8% | Dubai, Abu Dhabi, Ras Al Khaimah | Medium term (2-4 years) |

| Fast-Charging Infrastructure Scarcity | -0.5% | Dubai, Abu Dhabi | Long term (≥ 4 years) |

| ESG Diesel Ownership Cost | -0.3% | Abu Dhabi, Dubai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX And Tightening Credit

Benchmark lending rates have risen in line with global monetary policy, inflating lease costs and pushing some small contractors toward second-hand markets. Banks request larger down-payments, lengthening approval cycles for asset-backed loans. Elevated steel and hydraulic-component prices further increase invoice values, prolonging payback horizons. As a result, many builders pivot to rental fleets to preserve working capital. The central bank’s temporary repayment moratorium in 2024 highlighted systemic sensitivity to liquidity shocks.[2]“Quarterly Economic Review September 2024,” Central Bank of the UAE, centralbank.ae

Raw-Material and Component Supply Volatility

Global steel price swings and electronics shortages complicate OEM production schedules, producing sporadic delivery delays of three to six months. Contractors seeking fleet expansion struggle to align equipment arrival with project mobilization, leading to higher standby costs. Suppliers pass on surcharges through variable-price clauses, eroding contractor margins built on fixed-rate bids. Importers hedge exposure by stocking larger inventories, tying up warehouse space and working capital. Persistent supply uncertainty encourages project owners to incorporate escalation provisions, increasing contract complexity across the UAE crawler equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators Anchor Diverse Use-Cases

In UAE crawler equipment market, crawler excavators accounts 49.22% of market share owing to their broad applicability in trenching, bulk excavation, and demolition. Mid-size units between 20 and 35 tons remain the core of most urban job sites because they balance reach, dig depth, and transport ease. Contractors maximize utilization by switching between buckets, hammers, and grapples through hydraulic quick couplers, extending working hours without machine changeovers. Compact tracked loaders and skid-steers recorded the highest 9.51% CAGR outlook as tower cranes and high-rise basements constrain maneuvering space, favoring agile machines that can operate under low overhead clearances. Demand for crawler bulldozers remains steady on highway corridors and utility trenches where continuous pushing power is essential. Pipe-layers and crawler cranes serve energy-sector projects that require heavy lift capability and precise placement of long-run piping.

Manufacturers continually upgrade cab ergonomics, integrating 360-degree cameras and fingertip joysticks that reduce operator fatigue during 12-hour shifts common on regional megaprojects. Autonomous dig-assist features calibrate bucket angles in real time, reducing over-dig and rework. The proliferation of Grade Control 3D systems means earth-moving tolerances tighten, lowering backfill volumes and minimizing survey expenses. Sustained work on drainage tunnels, airport runways, and tourism islands ensures excavator rental utilisation throughout the forecast period, reinforcing the dominant role of this segment in the broader UAE crawler equipment market.

By Propulsion: Electric Gains Momentum

Internal combustion units accounts 86.24% of the UAE crawler equipment market, but their share is set to decline as battery-electric and hybrid entrants achieve double-digit penetration. Diesel models retain a service-network advantage, with every emirate hosting multiple refueling points and mobile fuel bowser fleets. Yet escalating fuel costs and Stage V after-treatment complexity have closed the operational-expenditure gap, making electrified alternatives attractive on urban night shifts where noise restrictions apply. Electric mini-excavators under 6 tons prove popular for utility trenching inside city blocks. Hybrid drive trains employing regenerative swing motors improve efficiency on trench-and-dump cycles typical to drainage works.

OEMs coordinate with utility providers to pre-wire fast-charge bays at project sites, reducing the need to transport batteries off-site. Battery rental models emerge, allowing contractors to swap depleted packs, mirroring forklift-exchange services present in the logistics sector. Government fleet procurement targets stipulate minimum electric content, prompting early deployment within municipal maintenance departments, which then provides demonstration spots for private contractors. The UAE crawler equipment market thus stands at an inflection point where diesel dominance gradually yields to a more diverse propulsion mix that aligns with national decarbonization goals.

By Engine Power Output: Mid-Range Retains Sweet Spot

Machines rated 201-400 HP captured 37.94% of the UAE crawler equipment market share in 2024 due to their versatility on mid-depth excavations and roadbed preparation. Power-to-weight optimization achieved through turbocharged engines and load-sensing hydraulics enables these units to deliver high breakout force while staying within transport axle-load limits on local highways. Sub-100 HP models, while smaller in dollar value, chart the fastest 12.12% CAGR as township developments and villa compounds emphasize compact equipment that can pass under height-restricted parking podiums. The 100-200 HP bracket serves contractors who seek higher productivity than mini-class machines can offer yet still need low ground pressure for desert sand mobility.

Above-400 HP crawlers fulfill specialized roles in quarry ripping and bulk earthmoving on greenfield industrial parks in Al Dhafra and Jebel Ali. Technology spillovers such as variable-geometry turbos and high-pressure common-rail fuel injection have pushed specific power higher, allowing manufacturers to package greater output in smaller frames. Operators appreciate upgraded HVAC systems that protect against 45 °C summer heat and dust ingress. The UAE crawler equipment market rewards those OEMs that can deliver power density without compromising serviceability, ensuring that mid-range machines will remain the first choice for most general contractors.

By Application: Construction Dominates Demand

Construction segment accounts for 62.56% of 2024 United Arab Emirates crawler earthmoving machines market share, reflecting the country’s commitment to transport corridors, medical complexes, and hospitality developments. High-rise basements require deep excavation supported by secant piling, tasks ideally suited to crawler excavators equipped with long arms and rotational grabs. The sector also consumes crawler loaders during backfill and site cleanup phases, driving continuous demand for medium-horsepower equipment. Agriculture and forestry, though starting from a low base, exhibit the fastest 9.15% CAGR, supported by vertical-farming clusters and desert-greening initiatives that call for light tracked tractors and multipurpose diggers.

Mining and quarrying, especially limestone and gabbro operations in the northern emirates, sustain steady orders for high-power bulldozers and loaders that withstand abrasive conditions. Circular-economy programs open fresh niches such as onsite concrete crushing, raising utilization of hybrid excavators that can switch between demolition and reclamation attachments during a single shift. The UAE crawler equipment market thus mirrors the wider economy’s diversification, with construction remaining the anchor yet newer applications adding incremental volume.

By Distribution Channel: Services Drive Dealer Value

By distribution channel, authorized dealers register 50.25% of the UAE crawler equipment market share in 2024, by bundling financing, extended warranties, and on-call maintenance. Telematics portals allow dealers to schedule service trucks in advance, minimizing machine downtime for customers on cost-plus contracts. Rental and leasing firms accelerate at an 11.81% CAGR as developers request shorter mobilisation periods and variable equipment fleets that mirror project phases. Dealer branches increasingly operate rental sub-divisions, blurring boundaries between ownership and access models.

Direct OEM sales remain the preferred route for government entities procuring standardized fleets under framework agreements. Digital marketplaces emerge, listing live inventory with hourly rates and delivery windows, giving project managers real-time visibility on fleet costs. Remote diagnostics agreements embedded in rental contracts help optimize fleet rotation and reduce idle time. Such contracting sophistication ensures the UAE crawler equipment market remains resilient even when credit conditions tighten.

Geography Analysis

Abu Dhabi, with a commanding 34.87% share of the United Arab Emirates crawler earthmoving machines market revenue in 2024, is bolstered by its ambitious multibillion-dollar industrial and cultural projects, all of which necessitate a consistent demand for earth-moving services. The Strategic Tunnel Enhancement Program serves as a testament to the pivotal role of deep-bore excavation, which in turn fuels prolonged operations for high-horsepower crawlers. Investments in petrochemicals and manufacturing, particularly in Al Ruwais and the Khalifa Industrial Zone, further cement the need for mid-range machines adept at material handling. Additionally, the planned EV charging corridors signal the emirate's commitment to the rollout of electrified heavy machinery.

Dubai is on a rapid ascent, boasting a 9.62% CAGR, driven by the 2040 Urban Master Plan's directives on land-use and transport enhancements. Projects like the drainage system overhaul and airport expansion have paved the way for numerous sub-contracts, focusing on deep excavation, pile cap trimming, and utility trenching. Within the city's constrained downtown areas, contractors are leaning towards agile mid-size excavators and tele-handler fleets for efficient material logistics. Furthermore, Dubai's stature as a re-export hub accelerates lead times for replacement parts, bolstering fleet availability.

Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain are emerging as a secondary growth corridor. Here, economic diversification is manifesting in industrial zones, port expansions, and agricultural ventures. Coastal dredging activities in Fujairah, alongside breakwater projects in Ras Al Khaimah, are drawing in specialized crawler cranes and dozers, particularly those adept at soft ground operations. Smaller municipalities are increasingly turning to rentals, allowing them the agility to pilot electric mini-excavators in green-infrastructure initiatives. This polycentric development approach not only diversifies demand but also shields the UAE's crawler equipment market from potential downturns in any single city.

Competitive Landscape

The UAE crawler equipment market reflects moderate consolidation, with the top five suppliers holding a majority of 2024 revenue. Caterpillar leads, leveraging its Dubai parts hub and in-country technical-training center that shortens repair cycles and builds operator loyalty. Komatsu emphasizes fuel efficiency and packaged service agreements that appeal to cost-sensitive mid-tier contractors. Volvo holds 14%, capitalizing on proven safety features and Stage V-ready engines that align with tightening import rules.

Technological capability now outweighs pure horsepower as a differentiator. Local start-ups such as TENDERD integrate multi-brand telematics into cloud dashboards, giving fleet owners a unified view of productivity and emissions. OEMs respond by embedding API-ready data gateways, ensuring equipment can feed third-party analytics platforms. Chinese entrants like XCMG target share gains via aggressive pricing and localized inventory financing, using the UAE as a launchpad for wider GCC expansion strategies. Electric crawler prototypes showcased at regional expos indicate accelerating competition in the zero-tailpipe segment.

Dealer networks invest in mobile workshops and parts vending machines located near major project clusters, aiming to offer sub-two-hour response times for critical breakdowns. Extended warranty packages now include remote software updates, reducing the need for on-site technicians. Competitive intensity is expected to rise as rental specialists add technology overlays such as utilization-based invoicing, further blurring distinctions between OEM capability and service innovation within the UAE crawler equipment market.

United Arab Emirates Crawler Earthmoving Machines Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Volvo Construction Equipment AB

Hitachi Construction Machinery Co., Ltd.

XCMG Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Undercarriage parts for Hitachi Sumitomo SCX550EN crawler cranes arrived in the UAE, covering track rollers, idlers, sprockets, and chains.

- November 2024: Falcon Motors LLC became the exclusive UAE dealer for XCMG, granting access to mobile cranes, bulldozers, aerial platforms, and crawler equipment.

United Arab Emirates Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trenchers, Drill Rigs, etc.) |

| Internal Combustion Engine (ICE) |

| Electric and Hybrid |

| Below 100 HP |

| 100 to 200 HP |

| 201 to 400 HP |

| Above 400 HP |

| Construction |

| Mining and Quarrying |

| Agriculture and Forestry |

| Others |

| Direct OEM Sales |

| Authorised Dealers |

| Rental and Leasing Firms |

| Abu Dhabi |

| Dubai |

| Sharjah and Ajman |

| Ras Al Khaimah |

| Fujairah |

| Umm Al Quwain |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trenchers, Drill Rigs, etc.) | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric and Hybrid | |

| By Engine Power Output | Below 100 HP |

| 100 to 200 HP | |

| 201 to 400 HP | |

| Above 400 HP | |

| By Application | Construction |

| Mining and Quarrying | |

| Agriculture and Forestry | |

| Others | |

| By Distribution Channel | Direct OEM Sales |

| Authorised Dealers | |

| Rental and Leasing Firms | |

| By Region | Abu Dhabi |

| Dubai | |

| Sharjah and Ajman | |

| Ras Al Khaimah | |

| Fujairah | |

| Umm Al Quwain |

Key Questions Answered in the Report

What is the 2025 value of the UAE crawler equipment market?

The UAE crawler equipment market is worth USD 450.45 million in 2025.

How fast is the market expected to grow through 2030?

The market is forecast to expand at a 5.93% CAGR, reaching USD 600.82 million by 2030.

Which equipment type currently generates the largest revenue?

Crawler excavators lead with 49.22% of 2024 revenue.

Which propulsion technology shows the highest growth potential?

Electric and hybrid crawler machines are projected to post an 18.23% CAGR through 2030.

Why are rental and leasing channels gaining traction?

Contractors are turning to rental and leasing to conserve capital amid higher borrowing costs and supply-chain price volatility.

Which region is forecast to grow the fastest by 2030?

Dubai is expected to record the highest CAGR at 9.62% due to its 2040 Urban Master Plan and large infrastructure budget.

Page last updated on: