Thailand Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

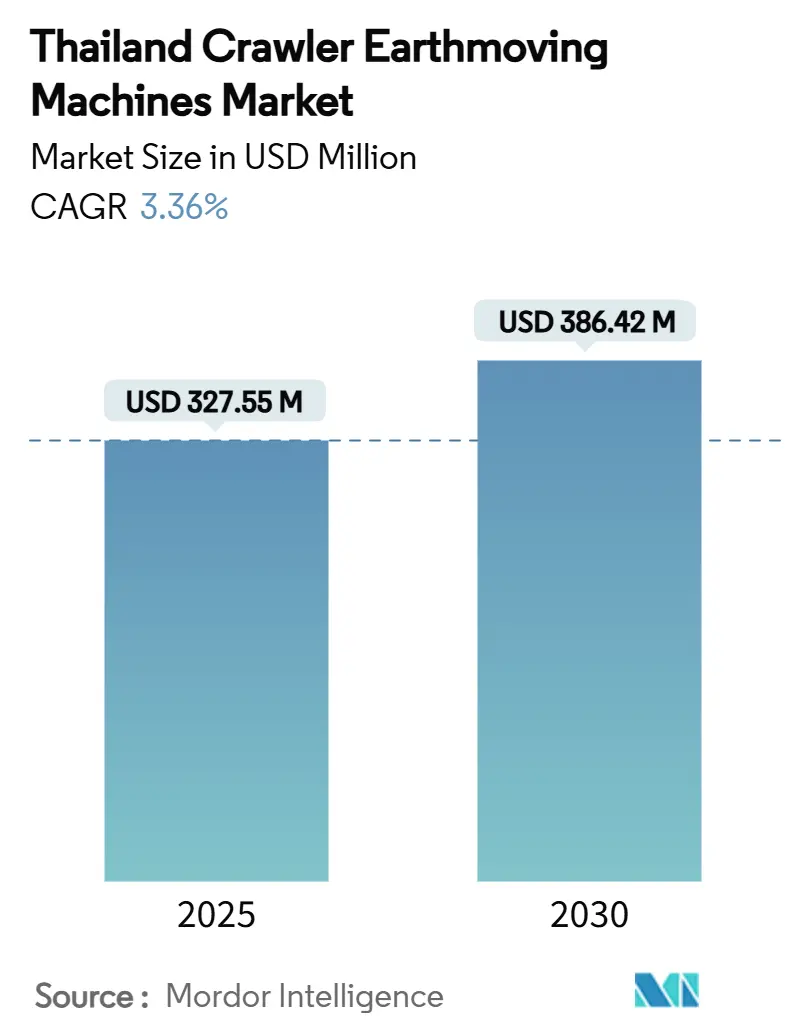

| Market Size (2025) | USD 327.55 Million |

| Market Size (2030) | USD 386.42 Million |

| Growth Rate (2025 - 2030) | 3.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The Thailand crawler earthmoving machines market size stands at USD 327.55 million in 2025 and is forecast to reach USD 386.42 million by 2030, reflecting a 3.36% CAGR over the period. Growth pivots on sustained public-sector infrastructure outlays, particularly the Eastern Economic Corridor program, rising industrial-estate construction, and an accelerating transition toward electrified and digitally connected equipment fleets. OEMs strengthen domestic assembly and parts support to cut lead times, while rental providers scale fleets to meet contractors’ preference for asset-light execution models. Competitive intensity rises as China-based brands expand dealer coverage and leverage cost advantages, even as established Western and Japanese suppliers defend share through advanced telematics and automation packages. Supply-chain volatility and upfront capital costs temper growth but do not stall long-run demand given Thailand’s commitment to large-scale logistics, transport, and smart-city developments.

Key Report Takeaways

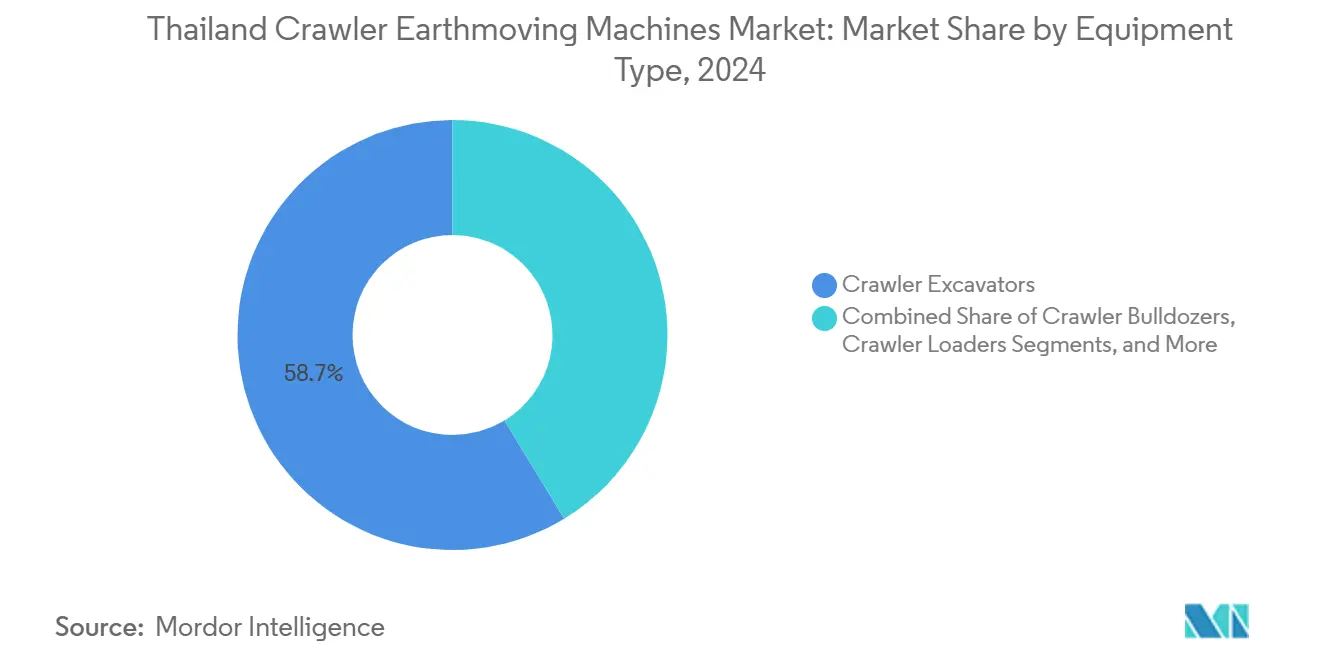

- By equipment type, crawler excavators led with 58.71% of the Thailand crawler earthmoving machines market share in 2024, while compact tracked loaders and skid-steers record the fastest projected 4.25% CAGR through 2030.

- By propulsion, internal-combustion models retained an 88.36% share in 2024; electric and hybrid variants posted the strongest 23.14% CAGR.

- By engine power, the 201–400 HP band accounted for 40.17% of the Thailand crawler earthmoving machines market size in 2024; sub-100 HP models expand at a 5.01% CAGR to 2030.

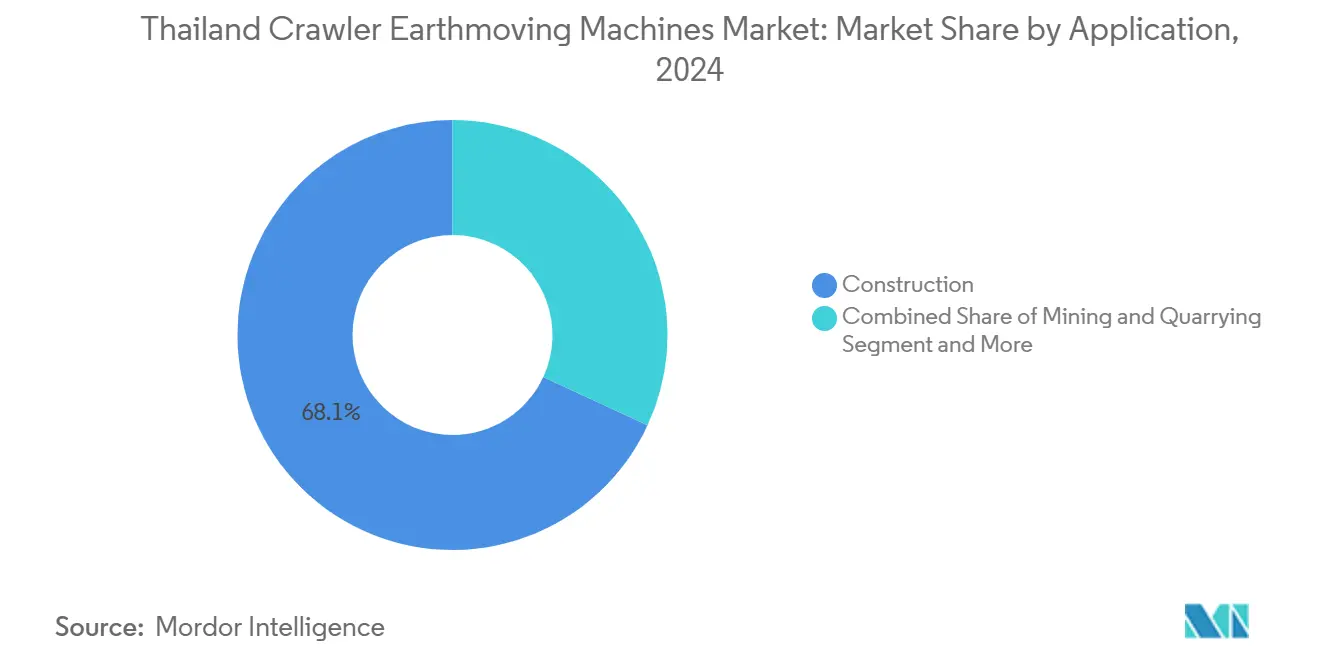

- By application, construction captured 68.13% revenue share in 2024 and is advancing at a 4.55% CAGR on the back of public-works spending.

- By distribution, authorized dealers controlled 48.55% in 2024, while rental and leasing channels will accelerate at a 7.13% CAGR amid tightening credit.

Global valuation is built by aggregating outputs from multiple countries and regions, with Thailand being one of the contributors. Our global crawler earthmoving machines market size represents that cumulative total.

Thailand Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure Build-Out Under Thailand's Eastern Economic Corridor Plan | +1.2% | Eastern provinces | Long term (≥ 4 years) |

| Accelerated Replacement of Ageing Crawler Fleets for Safety and Efficiency | +0.8% | National | Medium term (2-4 years) |

| Electrification Incentives and Stage V Emission Mandates | +0.6% | National | Long term (≥ 4 years) |

| Emergence of Modular Industrial Parks Needing Low-Ground-Pressure Crawlers | +0.5% | Eastern and central corridors | Medium term (2-4 years) |

| Digital Twins and Telematics-Driven OPEX Savings | +0.4% | National | Medium term (2-4 years) |

| Surge in Deconstruction and Circular-Demolition Projects | +0.3% | Major cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Build-Out Under Thailand’s Eastern Economic Corridor Plan

Government approval of THB 652 billion for EEC mega-projects anchors multi-year crawler demand. Earthmoving spiked on U-Tapao International Airport’s second runway project, while Laem Chabang Port Phase 3 requires extensive dredging and land reclamation. High-speed rail packages between Bangkok and Rayong entail long viaduct sections that rely on precision grading and piling. Smart-city initiatives around Huai Yai further boost low-ground-pressure crawler requirements for sensitive soil preparation. The clustering of projects permits contractors to redeploy fleets efficiently across contiguous sites, supporting steady unit turnover for dealers and rental firms.

Accelerated Replacement of Ageing Crawler Fleets for Safety and Efficiency

Thai contractors operate crawler machines averaging 8.4 years of service life, well beyond efficiency optima [1]Epiroc, “Epiroc Annual and Sustainability Report 2024,”epirocgroup.com. Large highway builders bring forward replacement cycles to avoid costly downtime, whereas SMEs prolong asset use or purchase lower-priced used units. Rising public-works budgets lift overall machine utilization, intensifying the cost of unplanned failures and foregrounding the value of reliable, fuel-efficient models. Newer crawler platforms integrate falling-object guards, improved cab ergonomics, and telematics, helping contractors comply with updated safety codes and insurance requirements. Financing barriers persist, but rental options ease the transition to modern fleets for smaller firms lacking balance-sheet headroom.

Electrification Incentives and Stage V Emission Mandates

Thailand’s EV 3.5 package cuts import duties on electric heavy equipment and offers excise rebates, widening the business case for battery-powered crawlers. A 2050 carbon-neutrality pledge aligns with Stage V engine rules already applied to new registrations in urban zones. Limited charging infrastructure for >20-ton machines slows widespread adoption, so OEMs prioritize hybrid drivelines that pair downsized diesels with power-assist batteries. Contractors in Bangkok pilot fully electric mini-excavators on short-shift urban jobs, while port operators evaluate hybrid crawler cranes where shore-power links exist. Supply-chain partnerships emerge to co-develop high-capacity chargers tailored for construction sites.

Emergence of Modular Industrial Parks Needing Low-Ground-Pressure Crawlers

Thailand’s fast-growing modular industrial parks require earthmoving machines that can move across partially prepared plots without over-compressing sub-grade soils. Developers in the Eastern Economic Corridor phase of construction so contractors prefer compact tracked loaders and sub-100 HP excavators equipped with extra-wide rubber tracks that distribute weight evenly. This preference underpins the 4.25% CAGR projected for the compact crawler segment through 2030 as each new factory pad, utility trench, and drainage channel calls for repeat deployment of low-impact equipment. Industrial-estate land sales in Chachoengsao, Chonburi, and Rayong rise 18-20% annually, translating into steady orders for these specialized crawlers as successive tenants erect logistics hubs and light-assembly plants. Short job durations make outright purchase uneconomic for many subcontractors, so rental fleets rapidly add low-ground-pressure units to capture demand from rotating work crews.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX and Tightening Credit | -0.7% | National | Short term (≤ 2 years) |

| Raw-Material and Component Supply Volatility | -0.5% | Global supply chains | Medium term (2-4 years) |

| ESG-Linked Cost of Ownership for Diesel Units | -0.4% | National | Long term (≥ 4 years) |

| Scarcity of Fast-Charging Infrastructure for Above 20-ton Crawlers | -0.3% | Outside Bangkok | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Tightening Credit

Rising policy rates push finance costs to five-year highs, narrowing contractor access to working capital. Smaller builders postpone purchases or shift to rental agreements that preserve liquidity. Budget delays trim construction-materials demand, indirectly depressing crawler-unit orders. OEMs counteract by extending warranty periods and partnering with banks to craft step-up repayment plans pegged to project milestones. Yet higher-spec machines equipped with Stage V engines and integrated telematics carry premium price tags, reinforcing bifurcation between cash-rich tier-one firms buying top-end models and SME contractors opting for basic configurations.

Raw-Material and Component Supply Volatility

Fluctuating steel and semiconductor prices raise production costs for undercarriage assemblies, control modules, and hydraulic systems. Delivery lead times stretch during peak construction seasons, compelling dealers to stock larger buffer inventories. Chinese inward investment increases local content sourcing but also heightens dependency on single-country supply chains vulnerable to external trade tensions. OEMs localize cylinder and track-shoe fabrication in Rayong and Chonburi to reduce currency risk, though doing so lifts working-capital requirements. Contractors hedge exposure by cross-leasing equipment among consortium partners to ensure smooth availability across project portfolios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators Anchor Infrastructure Transformation

Crawler excavators held 58.71% of the Thailand crawler earthmoving machines market share in 2024, owing to versatility across trenching, foundation, and demolition tasks. Continued EEC build-out secures baseline demand while Bangkok redevelopment sustains mid-size classes. Compact tracked loaders and skid-steers, recording a 4.25% CAGR, suit modular factory builds and warehouse expansions on industrial-estate plots where ground pressure limits apply. Bulldozers remain critical on road-bed preparation and coastal-reclamation jobs, whereas crawler cranes fill heavy-lift roles on port extensions and elevated-rail columns. Digitally enabled machine control spreads across equipment lines, improving accuracy and reducing rework rates.

In parallel, OEMs bundle grade-control sensors and quick-coupler systems that boost utilization rates across varied attachments. Contractors use telematics dashboards to redeploy idle excavators to adjacent projects, raising fleet turnover. Hybrid drive crawlers debut in the 20-25-ton size class for municipal night work requiring low noise. Rental firms prioritize compact loaders and 13-ton diggers given broad demand elasticity. The product mix, therefore, mirrors Thailand’s shift toward space-constrained industrial and urban builds alongside endurance-driven highway projects.

By Propulsion: Electrification Gains Momentum

Internal-combustion models dominated at 88.36% in 2024, yet the electric and hybrid cohort posts a 23.14% CAGR as government duty cuts and corporate ESG targets converge. Bangkok’s elevated-rail contractors deploy battery mini-excavators for tunnel interior work due to zero exhaust. Port operators trial hybrid crawler cranes that cut diesel burn in idling cycles. Diesel remains indispensable for 30-ton-plus excavators working double shifts on remote greenfield sites lacking grid access. The Thailand crawler earthmoving machines market size attributable to electric units could exceed USD 60 million by 2030 if the charger rollout meets the 12,000-station target.

Hybrid drive bridges the gap; regenerative swing systems recover boom-slew energy, trimming fuel by up to 15%. Dealers ramp technician training on high-voltage systems while second-life battery providers explore stationary storage uses for end-of-life packs. Manufacturers collaborate with utilities on job-site microgrids powered by mobile battery containers, easing power delivery for large-frame electric crawlers during pilot deployments.

By Engine Power Output: Mid-Range Dominance with Compact Upside

The 201–400 HP tier accounted for 40.17% of the Thailand crawler earthmoving machines market size in 2024, thanks to suitability for most EEC earthworks. Models in this band balance digging power with transport ease on 10-wheel trailers navigating provincial roads. Sub-100 HP units, growing at 5.01% CAGR, underpin industrial-estate utility installation and urban smart-city landscaping where maneuverability is paramount. Above-400 HP machines occupy niche demand on port reclamation and open-pit mining, yet face stricter emission fees within city limits.

Contractors adopt telematics-enabled power-mode management that auto-selects engine maps matching load, reducing fuel per cubic meter moved. Higher-pressure common-rail systems increase hydraulic breakout force even on mid-horsepower engines, extending the effective job envelope of 20-25-ton machines. Conversely, mini-crawlers integrate tilt-rotators, enhancing task productivity in confined spaces, extending value-add beyond raw engine output.

By Application: Construction Supremacy with Mining Support

Construction sites consumed 68.13% of units in 2024 and will expand at a 4.55% CAGR on the back of THB 253.45 billion worth of nationwide public-works projects. Residential high-rise programs and e-commerce fulfillment centers drive demand for mid-size excavators and compact loaders. Mining and quarrying, though smaller, remain vital suppliers of aggregates feeding the EEC concrete and road-base supply chain. Agriculture and forestry segments order low-ground-pressure crawlers for plantation drainage and land clearing, especially in the central plains rice-belt modernization schemes.

Circular-demolition projects in Bangkok boost specialized multi-processor excavators with high-reach booms suitable for selective deconstruction. Environmental-remediation jobs along industrial corridors need auger-drilling rigs and vacuum-excavators classified under the “others” application group, diversifying crawler demand. Contractors increasingly value machines pre-wired for grade-control sensors, easing redeployment from infrastructure to vertical construction.

By Distribution Channel: Dealers Lead, Rentals Surge

Authorized dealers, equipped with parts depots and finance desks, retained a 48.55% share in 2024. They anchor OEM brand presence, provide warranty service, and coordinate technician certification. Rental and leasing operators, expanding at a 7.13% CAGR, cater to contractors facing tight credit lines or intermittent project pipelines. Large rental fleets leverage telematics to monitor machine health across dispersed job-sites, reducing downtime and securing repeat business. Direct OEM sales to top-tier builders remain significant for bulk orders tied to turnkey EPC contracts.

Dealers respond to the rental upswing by launching branded short-term hire programs and certified pre-owned exchanges. Digital platforms list real-time crawler availability, allowing contractors to match fleet capacity with peak demand windows during mass-earthwork stages. Financing subsidiaries introduce pay-per-use models that blend ownership and rental attributes, reflecting fluid equipment-utilization strategies.

Geography Analysis

Eastern provinces of Chachoengsao, Chonburi, and Rayong anchor demand, buoyed by THB 652 billion in EEC project allocations and industrial-estate land sales rising 18-20% each year [2]Board of Investment, “Industrial Estate Land Sales 2025,” boi.go.th. Fleet density reaches the highest national levels as logistics parks, airports, and deep-sea ports require ongoing foundation and grading work. Contractors rotate equipment between contiguous mega-projects, enhancing machine utilization and accelerating replacement cycles to maintain uptime targets.

Bangkok and its surrounding metropolitan region remain the second-largest cluster, driven by mass-transit extensions, mixed-use redevelopment, and healthcare facility upgrades. Urban density favors compact crawlers and electric mini-excavators that tackle trenching beneath elevated rail structures. Strict emission zones incentivize hybrid and Stage V diesel adoption sooner than in other regions, shaping dealer inventory strategies.

Central provinces outside the capital experience steady, moderate growth as spillover manufacturing relocates along upgraded motorway corridors linking Bangkok to the EEC. Northern and southern regions post slower uptake yet exhibit niche demand from mining, agro-processing and tourism infrastructure. Government allocation of THB 253.45 billion across 287 projects through 2026 injects crawler demand into provincial highway widening and bridge rehabilitation, ensuring nationwide equipment deployment. Cross-border trade routes to Laos, Cambodia and Malaysia further increase crawler utilization in border logistics hubs, positioning Thailand-based rental fleets to service neighboring markets.

Coverage of the crawler earthmoving machines market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, alongside detailed country-level intelligence for Singapore, Australia, Indonesia, United States, Philippines, South Korea, and Saudi Arabia, each shaped by local operating conditions.

Competitive Landscape

Global incumbents such as Caterpillar, Komatsu, and Hitachi Construction Machinery collectively hold significant shares, while Chinese firms SANY, XCMG, and Zoomlion expand aggressively on price competitiveness and quicker delivery. Caterpillar’s USD 300 million Rayong expansion enhances localized hydraulic-cylinder and undercarriage production, trimming lead times for regional orders [3]Caterpillar Inc., “Rayong Facility Expansion Press Release,” cat.com. Komatsu responds with dealer-installed Smart Construction kits that upgrade legacy fleets with 3D-machine-control, safeguarding installed-base loyalty.

HD Hyundai promotes the Xite Transformation suite, enabling semi-autonomous excavation modes, differentiating in productivity amid chronic skilled-labor shortages. Chinese brands pair economical unit prices with extended warranty terms, pressuring rivals on the total cost of ownership. Rental giants form purchasing alliances to negotiate bulk discounts, diluting OEM pricing power yet guaranteeing high-volume absorption for new-model launches. Strategic white-space emerges in electric crawler niches where Western and Japanese suppliers retain a technology edge, though Chinese battery sourcing prowess narrows time-to-market gaps.

Dealer consolidation accelerates as family-owned distributors seek scale to finance telematics infrastructure and technician training on high-voltage systems. Joint-venture finance arms offer variable-rate leasing pegged to project duration, improving customer stickiness. Competition increasingly shifts from bare-metal sales to lifecycle service packages encompassing predictive-maintenance subscriptions and operator-training modules, raising switching costs for fleet owners eyeing lower-cost imports.

Thailand Crawler Earthmoving Machines Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery Co., Ltd.

Volvo Construction Equipment AB

XCMG Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Shantui delivered its SE550LC crawler excavator to a Thai mine, marking a milestone in eco-friendly heavy-duty deployment.

- January 2025: Volvo Construction Equipment introduced the New Generation EC210 excavator in Bangkok through its newly appointed dealer CHAIRATCHAKARN (Bangkok) Co., Ltd.

Thailand Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Internal Combustion Engine (ICE) |

| Electric and Hybrid |

| Below 100 HP |

| 100-200 HP |

| 201-400 HP |

| Above 400 HP |

| Construction |

| Mining and Quarrying |

| Agriculture and Forestry |

| Others |

| Direct OEM Sales |

| Authorized Dealers |

| Rental and Leasing Firms |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric and Hybrid | |

| By Engine Power Output | Below 100 HP |

| 100-200 HP | |

| 201-400 HP | |

| Above 400 HP | |

| By Application | Construction |

| Mining and Quarrying | |

| Agriculture and Forestry | |

| Others | |

| By Distribution Channel | Direct OEM Sales |

| Authorized Dealers | |

| Rental and Leasing Firms |

Key Questions Answered in the Report

What is the 2025 value of the Thailand crawler earthmoving machines market?

The market stands at USD 327.55 million in 2025.

How fast is the market projected to grow through 2030?

It is forecast to record a 3.36% CAGR over 2025-2030.

Which equipment type currently leads to unit demand?

Crawler excavators, holding 58.71% share in 2024.

Why are rental and leasing channels expanding?

Contractors favor asset-light models amid higher borrowing costs, driving a 7.13% CAGR for rentals.

Page last updated on: