Singapore Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

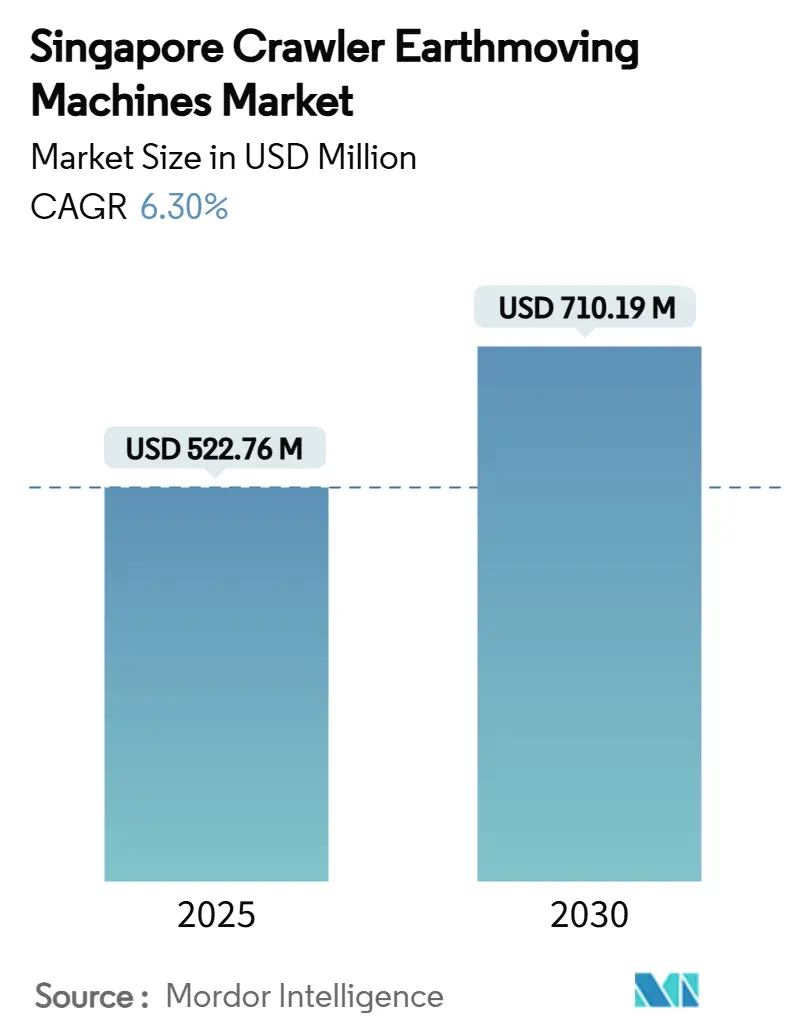

| Market Size (2025) | USD 522.76 Million |

| Market Size (2030) | USD 710.19 Million |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The Singapore crawler earthmoving machines market size is USD 522.76 million in 2025 and is on course to reach USD 710.19 million in 2030, expanding at a 6.30% CAGR. A steady pipeline of mega-projects such as the USD 20 billion Tuas Mega Port build-out and the Cross Island Line Phase 2 rail extension anchors equipment demand, while the Green Plan 2030 tightens Stage V emission compliance and channels spending toward cleaner powertrains. Contractors are upgrading fleets earlier than planned because an aging equipment base collides with aggressive sustainability targets, creating a replacement super-cycle. Digital twin adoption raises the premium on telematics-ready machines, and equipment-as-a-service offerings lower entry barriers for small and mid-size firms. Collectively, these drivers position the Singapore crawler earthmoving machines market for balanced, policy-backed growth through the decade.

Key Report Takeaways

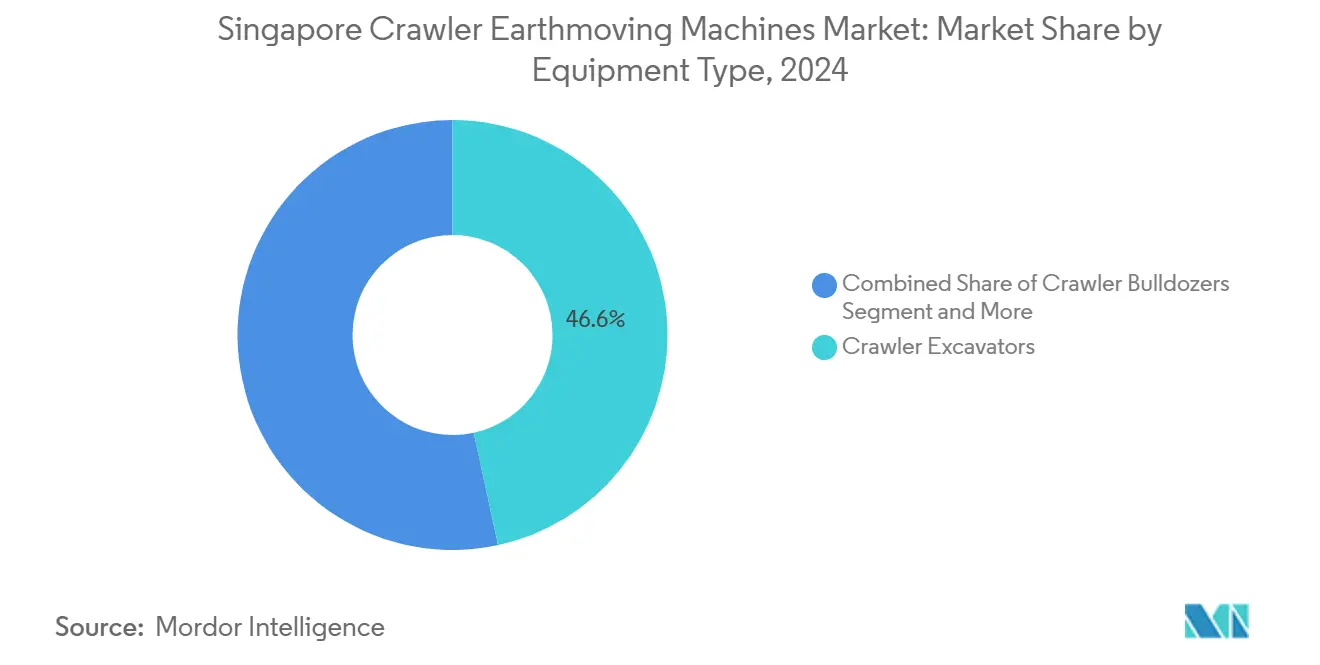

- By equipment type, crawler excavators commanded 46.62% of the Singapore crawler earthmoving machines market share in 2024, whereas compact tracked loaders and skid-steers are projected to register an 11.28% CAGR to 2030.

- By propulsion, diesel units held 67.84% share of the Singapore crawler earthmoving machines market size in 2024, while battery-electric variants are forecast to advance at a 34.17% CAGR through 2030.

- By engine power, the 100–200 HP class accounted for 42.36% of the Singapore crawler earthmoving machines market size in 2024, and sub-100 HP machines are expected to post a 13.22% CAGR to 2030.

- By application, earthmoving and grading led with 38.49% revenue share in 2024; demolition and recycling are projected to grow at a 12.08% CAGR between 2025 and 2030.

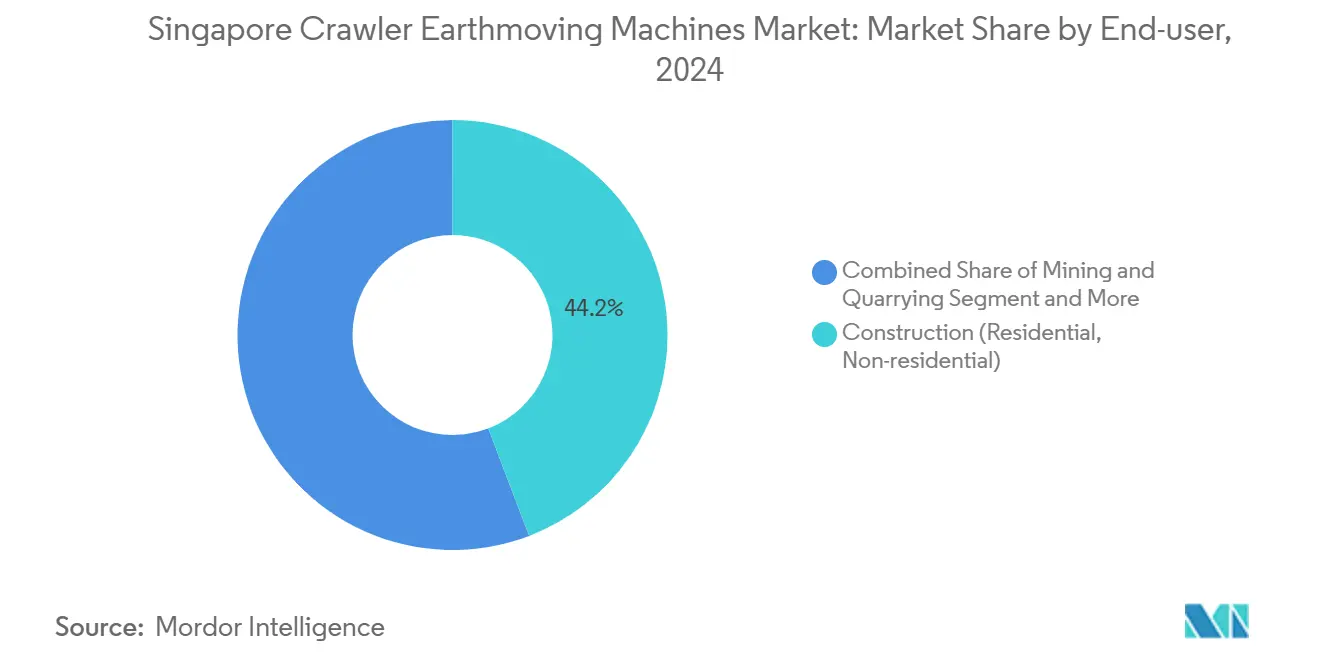

- By end-user, construction activities represented 44.17% of the Singapore crawler earthmoving machines market size in 2024, whereas municipal services are slated to expand at an 11.63% CAGR through 2030.

- By distribution channel, authorized dealers captured 55.42% share in 2024, yet online and digital marketplaces are expected to record a 15.72% CAGR by 2030.

Future direction is shaped by developments occurring across multiple countries and regions, with Singapore contributing to the overall trajectory. The outlook on worldwide crawler earthmoving machines market reflects how these are expected to evolve collectively.

Singapore Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification Incentives & Stage V Mandates | +1.8% | National, with early adoption in industrial zones | Short term (≤ 2 years) |

| Singapore Green Plan 2030 Projects | +1.5% | National, concentrated in western Singapore | Medium term (2-4 years) |

| Aging Fleet Replacement Cycle | +1.2% | National, with priority in urban areas | Medium term (2-4 years) |

| Funding for Autonomous Tuas Port | +0.9% | Western Singapore, spillover to Jurong | Long term (≥ 4 years) |

| Digital Twins & Telematics Savings | +0.7% | National, early gains in smart construction projects | Short term (≤ 2 years) |

| Rise in Circular Demolition Projects | +0.6% | National, concentrated in older districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification Incentives and Stage V Emission Mandates

Singapore's Commercial Vehicle Emissions Scheme extension through March 2027 provides USD 15,000 incentives for electric vehicles while increasing surcharges for diesel units, fundamentally reshaping crawler equipment procurement strategies[1]"Joint News Release by the Land Transport Authority (LTA) & NEA -Commercial Vehicle Emissions Scheme and Early Turnover Scheme Extended," . The National Environment Agency's enforcement of off-road diesel engine standards requires compliance with EU Stage II, US Tier II, or Japan Tier I emissions, creating immediate replacement demand for non-compliant equipment. Pan-United's deployment of Singapore's first electric concrete mixer truck, featuring 350 kWh battery capacity and 2-hour charging capability, demonstrates the commercial viability of electrified heavy machinery. This regulatory framework accelerates the transition from diesel-dominant fleets toward hybrid and battery-electric alternatives, particularly in the sub-200 HP crawler segment where charging infrastructure constraints are less prohibitive. The convergence of environmental compliance costs and electrification incentives creates a compelling economic case for fleet modernization, especially for municipal and infrastructure contractors operating under strict emission monitoring protocols.

Singapore Green Plan 2030 Infrastructure Pipeline

The Green Plan 2030's infrastructure commitments generate sustained demand for specialized crawler equipment across multiple mega-projects, including the USD 20 billion Tuas Port expansion and the 15-kilometer Cross Island Line Phase 2 extension. Construction activity is projected to reach SGD 35-39 billion in 2025, with public sector projects accounting for 65% of demand, creating predictable equipment utilization patterns for crawler machinery. The Building and Construction Authority's target of 80% Green Mark certification by 2030 mandates sustainable construction practices that favor fuel-efficient and low-emission crawler equipment over conventional diesel alternatives[2]Dr Edward Anggadjaja, "Sustainable Building and Construction in Singapore," irbnet.de. . Tuas Port's automated terminal development requires specialized crawler equipment capable of operating in proximity to autonomous systems, driving demand for telematics-enabled and remote-controlled machinery. The infrastructure pipeline's emphasis on sustainability metrics creates a premium market for equipment manufacturers offering carbon footprint tracking and energy-efficient operation modes.

Aging National Construction-Fleet Replacement Cycle

Singapore's construction equipment fleet, predominantly acquired during the 2010-2015 infrastructure boom, approaches end-of-life replacement cycles, coinciding with stricter emission standards and technological obsolescence pressures. The Early Turnover Scheme's extension through December 2025 provides financial incentives for replacing older Heavy Commercial Vehicles, including construction equipment, with approximately 70,000 vehicles already replaced under the program. Fleet replacement decisions increasingly factor in total cost of ownership calculations that favor newer equipment with advanced telematics, predictive maintenance capabilities, and fuel efficiency improvements. The convergence of regulatory compliance requirements and natural replacement cycles creates a concentrated demand window for crawler equipment manufacturers, particularly in the 100-400 HP power range where operational efficiency gains are most pronounced. Construction companies are prioritizing equipment purchases that offer dual compliance with current emission standards and future electrification mandates, driving preference for hybrid-ready platforms over purely diesel alternatives.

Public-Private Funding of Autonomous Tuas Port Logistics

The Tuas Mega Port's development as the world's largest fully automated terminal by 2040 requires specialized crawler equipment capable of operating within autonomous logistics ecosystems, creating niche demand for advanced machinery[3]"Tuas Port to be world's largest fully automated terminal when completed in 2040," The Straits Times, straitstimes.com.. PSA's USD 647.5 million supply chain hub construction, scheduled for completion by Q2 2027, incorporates advanced robotics and automation systems that necessitate precision-grade crawler equipment for infrastructure preparation. The port's 24-hour operational efficiency targets require construction equipment with enhanced durability and minimal maintenance intervals, favoring premium OEM offerings over cost-focused alternatives. Integration with autonomous systems demands crawler equipment equipped with advanced positioning systems, collision avoidance technology, and remote monitoring capabilities that align with the port's intelligent operations framework. The project's phased development approach creates sustained equipment demand through 2040, with each phase requiring increasingly sophisticated machinery as automation levels advance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & Tight Credit | -1.4% | National, affecting SME contractors | Short term (≤ 2 years) |

| Raw Material Supply Volatility | -1.1% | Global supply chains, local assembly impact | Medium term (2–4 years) |

| Limited Fast-Charging for Above 20-Ton Crawlers | -0.9% | National, industrial and mining corridors | Medium term (2–4 years) |

| ESG Costs for Diesel Units | -0.8% | National, amplified by tightening emission norms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Tightening Credit

Construction equipment financing constraints intensify as interest rates remain elevated and banks tighten lending criteria for capital-intensive machinery purchases, particularly affecting small and medium enterprises that comprise 60% of Singapore's construction sector participants. The shift toward electric and hybrid crawler equipment compounds CAPEX pressures, with battery-electric variants commanding 30-50% premiums over diesel equivalents, while charging infrastructure investments add USD 50,000-100,000 per site for heavy machinery compatibility. Rental penetration rates increase as contractors defer ownership decisions, benefiting equipment rental companies like Ashtead Group, which reported 10% rental revenue growth in 2024 despite challenging market conditions. Credit tightening disproportionately impacts crawler equipment purchases in the 201-400 HP segment, where unit costs exceed USD 500,000 and financing terms extend beyond 5 years, creating market opportunities for leasing and equipment-as-a-service models.

Raw-Material and Component-Supply Volatility

Global supply chain disruptions continue affecting construction equipment manufacturing, with aluminum and steel price volatility creating unpredictable cost structures for crawler machinery production and maintenance operations. The Economist Intelligence Unit projects industrial raw material prices will rise through 2025-2026, driven by decarbonization demand for aluminum, copper, and nickel, while weak construction activity in China creates supply-demand imbalances. Component shortages, particularly for electronic control systems and hydraulic components, extend equipment delivery times from 6-8 months to 12-15 months, forcing contractors to maintain older equipment longer than planned. US tariff policies on steel and aluminum imports tighten global supply chains, affecting Singapore-based equipment assembly operations and aftermarket parts availability. Supply volatility drives inventory management costs higher for dealers and rental companies, with some operators maintaining 18-month parts inventories compared to the traditional 6-month buffer, increasing working capital requirements and operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators Drive Automation Integration

Crawler Excavators maintain market leadership with 46.62% share in 2024, driven by their versatility in Singapore's dense urban construction environment and compatibility with emerging automation technologies. The segment benefits from the Housing Development Board's Construction Transformation Project, which incorporates autonomous cranes and robotic systems that require precision excavation support. Compact Tracked Loaders and Skid-steers emerge as the fastest-growing segment at 11.28% CAGR through 2030, reflecting Singapore's shift toward smaller, more maneuverable equipment for urban renewal projects and tight construction sites.

Crawler Bulldozers and Crawler Loaders serve specialized roles in major infrastructure projects like Tuas Port land reclamation, where 294 hectares require extensive earthmoving capabilities. Crawler Cranes and Pipe-layers support Singapore's utility infrastructure upgrades, particularly for the island's transition to hydrogen-ready energy systems. The Others category, encompassing trenchers and drill rigs, benefits from Singapore's extensive underground development, including the 360-kilometer subway network planned for completion by 2030. Equipment manufacturers are integrating IoT sensors and telematics systems across all categories to support Singapore's digital twin infrastructure initiatives, creating differentiation opportunities in the premium market segment.

By Propulsion: Electric Transition Accelerates Despite Infrastructure Gaps

Diesel propulsion systems command 67.84% of the market share in 2024, reflecting the mature technology's reliability and established service networks, yet they face increasing regulatory pressure from Singapore's emission standards enforcement. Battery-Electric variants surge at 34.17% CAGR through 2030, driven by government incentives and successful pilot deployments like Pan-United's electric concrete mixer truck, which demonstrates commercial viability in heavy-duty applications. Hybrid Diesel-Electric systems serve as transitional technology, offering emission reductions without the range limitations that constrain pure electric operation in extended construction projects.

Hydrogen Fuel-cell variants remain in pilot phase, with Singapore's first hydrogen-ready cogeneration plant breaking ground in 2023 as part of the island's decarbonization strategy. The propulsion transition faces infrastructure constraints, with charging networks designed for light vehicles inadequate for heavy construction equipment requiring 350+ kWh battery capacities. Volvo Construction Equipment's introduction of its first commercial electric machine to Asia signals OEM commitment to electrification, despite the challenging economics of battery replacement costs exceeding 40% of equipment value.

By Engine Power Output: Compact Segment Leads Electrification

The 100-200 HP category dominates with 42.36% market share in 2024, optimally suited for Singapore's urban construction requirements and infrastructure maintenance applications. Less than 100 HP equipment experiences the fastest growth at 13.22% CAGR through 2030, driven by electrification feasibility in smaller power ranges and increasing demand for precision work in confined spaces. This segment benefits from Singapore's Smart Nation initiative, which emphasizes technology integration and automated systems requiring compact, maneuverable installation and maintenance equipment.

The 201-400 HP segment serves major infrastructure projects but faces headwinds from electrification challenges and higher financing costs that limit market expansion. Equipment exceeding 400 HP remains niche, primarily serving specialized applications like Tuas Port's deep-water berth construction, which requires heavy-duty machinery for caisson installation and marine engineering. Power output segmentation increasingly correlates with propulsion technology adoption, as battery limitations constrain electric variants to sub-200 HP applications while diesel systems maintain dominance in higher power categories. The trend toward modular construction and prefabrication reduces demand for high-power equipment, as building components are manufactured off-site using factory-based systems rather than traditional on-site assembly methods.

By Application: Demolition Drives Circular Economy Growth

Earthmoving and Grading applications maintain a 38.49% market share in 2024, supported by Singapore's extensive infrastructure development and land reclamation projects that require substantial soil movement and site preparation capabilities. Demolition and Recycling emerges as the fastest-growing application at 12.08% CAGR through 2030, reflecting Singapore's Zero Waste Master Plan and circular economy initiatives prioritizing material recovery over disposal. The Building and Construction Authority's demolition protocol for waste management creates a systematic demand for specialized crawler equipment capable of selective deconstruction and material sorting.

Mining and Quarrying applications remain limited due to Singapore's geographic constraints, while Forestry and Agriculture serve niche roles in the island's urban farming initiatives and park development projects. Pipeline and Energy Infrastructure applications gain prominence as Singapore transitions to hydrogen-ready energy systems and expands its renewable energy infrastructure. Rental Fleet Operations increasingly dominate equipment utilization patterns, with contractors preferring short-term rentals over ownership for project-specific applications. The application mix reflects Singapore's evolution from traditional construction toward smart infrastructure development, where crawler equipment must integrate with digital systems and support sustainable building practices rather than merely providing mechanical capability.

By End-user: Municipal Services Drive Smart City Integration

Construction (Residential/Non-residential) commands 44.17% market share in 2024, driven by Singapore's ambitious public housing program and commercial development projects that support the island's economic diversification strategy. Municipal Services emerges as the fastest-growing end-user at 11.63% CAGR through 2030, reflecting Singapore's Smart Nation initiative and the need for specialized equipment to install and maintain urban technology infrastructure. The Housing Development Board's plan to deploy construction robots at half of Build-To-Order sites from 2025 creates demand for crawler equipment that can operate alongside automated systems.

Mining and Quarrying end-users remain constrained by Singapore's limited land area, while Oil and Gas Infrastructure applications focus on offshore support and marine terminal development. Industrial and Logistics Parks benefit from Singapore's position as a regional distribution hub, requiring specialized equipment for warehouse construction and automated facility development. Agriculture and Forestry end-users serve Singapore's food security initiatives, including vertical farming projects and urban agriculture development that require compact, precision equipment for soil preparation and facility construction. The end-user landscape increasingly emphasizes technology integration and sustainability compliance, with municipal and construction clients prioritizing equipment supporting digital twin development and reducing carbon footprint over purely cost-focused alternatives.

By Distribution Channel: Digital Transformation Reshapes Sales Models

Authorized Dealers maintain 55.42% market share in 2024, leveraging established relationships and comprehensive service networks that remain essential for complex crawler equipment sales and maintenance support. Online/Digital Marketplaces surge at 15.72% CAGR through 2030, driven by digital transformation in equipment procurement and the growing acceptance of virtual demonstrations and remote equipment evaluation capabilities. Direct OEM Sales serve large-scale projects and government contracts, while Rental and Leasing Firms expand their market presence as contractors increasingly prefer equipment-as-a-service models over ownership.

The distribution channel evolution reflects broader changes in customer behavior, with younger procurement professionals comfortable with digital platforms and data-driven equipment selection processes. Caterpillar's extensive Asia-Pacific presence since the 1920s, including Singapore operations focused on parts distribution and customer support, demonstrates the enduring importance of local service capabilities. Digital marketplaces increasingly incorporate augmented reality and virtual reality technologies for equipment demonstrations, reducing the need for physical showrooms while maintaining customer engagement. The channel mix optimization becomes critical as equipment complexity increases and customers demand integrated solutions that combine machinery, software, and service support rather than standalone product transactions.

Geography Analysis

Singapore's compact geography concentrates crawler earthmoving machine demand within distinct zones that reflect the island's strategic development priorities and infrastructure investment patterns. Western Singapore leads market activity, driven by the USD 20 billion Tuas Mega Port development and associated logistics infrastructure that requires extensive earthmoving capabilities for land reclamation and terminal construction. The port's 65 million TEU capacity target by 2040 necessitates sustained crawler equipment deployment across multiple construction phases, with Phase 2 alone involving 227 caissons weighing 13,000 tons each and nearly 400 hectares of land reclamation. Central Singapore experiences concentrated activity from the Cross Island Line Phase 2 construction, which began in July 2025 and extends 15 kilometers with six underground stations, requiring specialized tunnel boring support and station excavation capabilities.

Eastern Singapore's development focuses on residential and mixed-use projects, with the Housing Development Board's plan to launch 100,000 Build-To-Order flats by end-2025 creating sustained demand for compact crawler equipment suitable for urban construction environments. The integration of construction robots for painting and plastering operations requires crawler equipment capable of precise positioning and coordination with automated systems, driving preference for telematics-enabled machinery over conventional alternatives.

Northern Singapore benefits from industrial redevelopment projects, including the Sungei Kadut eco-industrial district revitalization that emphasizes circular economy principles and sustainable construction practices. The geographic distribution pattern reflects Singapore's strategic emphasis on automation, sustainability, and smart infrastructure development, with crawler equipment requirements increasingly specified around digital integration capabilities rather than purely mechanical performance parameters.

Analysis of the crawler earthmoving machines market by Mordor Intelligence spans multiple other regional evaluations across Europe, supported by country-level insights for South Korea, Indonesia, United States, Thailand, Philippines, Australia, and Saudi Arabia, wherein local market conditions keep varying from one country to another.

Competitive Landscape

The Singapore crawler earthmoving machines market exhibits moderate fragmentation with established global OEMs maintaining dominant positions through extensive dealer networks and comprehensive service capabilities, while emerging Chinese manufacturers gain market share through competitive pricing and local assembly strategies. Caterpillar's presence since the 1920s, including Singapore operations focused on parts distribution across Asia-Pacific, demonstrates the enduring importance of regional service hubs and established customer relationships. The competitive intensity increases as traditional equipment sales models transition toward service-oriented offerings, with companies like Ashtead Group reporting USD 10.86 billion global revenue in 2024, primarily from rental operations that emphasize equipment availability over ownership.

Market consolidation accelerates through strategic acquisitions, exemplified by Sumitomo Corporation's purchase of Singapore-based Aver Asia, positioning the Japanese trading group to capitalize on Southeast Asia's construction equipment rental growth. Technology integration becomes a key differentiator, with manufacturers investing in IoT sensors, telematics systems, and autonomous operation capabilities that align with Singapore's Smart Nation initiative and digital twin infrastructure development.

White-space opportunities emerge in electric and hybrid propulsion systems, where established OEMs face competition from new entrants offering specialized battery-electric solutions. At the same time, the charging infrastructure gap creates market potential for integrated equipment-and-energy service providers. The competitive landscape increasingly rewards companies that can deliver comprehensive solutions combining machinery, software, financing, and maintenance support rather than standalone product offerings.

Singapore Crawler Earthmoving Machines Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Volvo Construction Equipment

-

Hitachi Construction Machinery Co., Ltd.

-

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Land Transport Authority commenced construction on Cross Island Line Phase 2, extending 15 kilometers with six underground stations and utilizing Large-Diameter Tunnel Boring Machines, creating sustained demand for specialized crawler equipment support throughout the project's timeline to 2032 completion.

- January 2025: Inchcape+ opened a 2,000 square foot BYD commercial electric vehicle showroom in Singapore, featuring the T9R heavy electric truck suitable for construction applications, signaling mainstream adoption of electric heavy machinery in the construction sector.

- October 2024: PSA broke ground on a USD 647.5 million supply chain hub at Tuas Port, spanning over 185,000 square meters with advanced robotics and automation systems, requiring specialized crawler equipment for infrastructure preparation and scheduled for Q2 2027 completion.

Singapore Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Diesel (Stage III–V) |

| Hybrid Diesel-Electric |

| Battery-Electric |

| Hydrogen Fuel-cell (Pilot) |

| Less than 100 HP |

| 100 to 200 HP |

| 201 to 400 HP |

| More than 400 HP |

| Earthmoving and Grading |

| Demolition and Recycling |

| Forestry and Agriculture |

| Mining and Quarrying |

| Pipeline and Energy Infrastructure |

| Rental Fleet Operations |

| Construction (Residential, Non-residential) |

| Mining and Quarrying |

| Oil and Gas Infrastructure |

| Industrial and Logistics Parks |

| Municipal Services |

| Agriculture and Forestry |

| Direct OEM Sales |

| Authorised Dealers |

| Rental and Leasing Firms |

| Online/Digital Marketplaces |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Diesel (Stage III–V) |

| Hybrid Diesel-Electric | |

| Battery-Electric | |

| Hydrogen Fuel-cell (Pilot) | |

| By Engine Power Output | Less than 100 HP |

| 100 to 200 HP | |

| 201 to 400 HP | |

| More than 400 HP | |

| By Application | Earthmoving and Grading |

| Demolition and Recycling | |

| Forestry and Agriculture | |

| Mining and Quarrying | |

| Pipeline and Energy Infrastructure | |

| Rental Fleet Operations | |

| By End-user | Construction (Residential, Non-residential) |

| Mining and Quarrying | |

| Oil and Gas Infrastructure | |

| Industrial and Logistics Parks | |

| Municipal Services | |

| Agriculture and Forestry | |

| By Distribution Channel | Direct OEM Sales |

| Authorised Dealers | |

| Rental and Leasing Firms | |

| Online/Digital Marketplaces |

Key Questions Answered in the Report

What is the 2025 value of the Singapore crawler earthmoving machines market?

The market is valued at USD 522.76 million in 2025 with a 6.30% CAGR outlook.

Which equipment type leads sales in Singapore?

Crawler excavators lead, commanding 46.62% of 2024 revenue.

How fast is the battery-electric crawler segment growing?

Battery-electric variants are projected to expand at a 34.17% CAGR through 2030.

Why are municipal agencies boosting crawler demand?

Smart-city projects and emission mandates drive municipal purchases, making this the fastest-growing end-user group at 11.63% CAGR.

Which distribution channel is expanding the quickest?

Online and digital marketplaces are growing at 15.72% CAGR as buyers embrace virtual procurement.

What restrains equipment purchases in Singapore?

High upfront CAPEX and tightening bank credit, especially for SMEs, slow outright acquisitions.

Page last updated on: