Australia Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

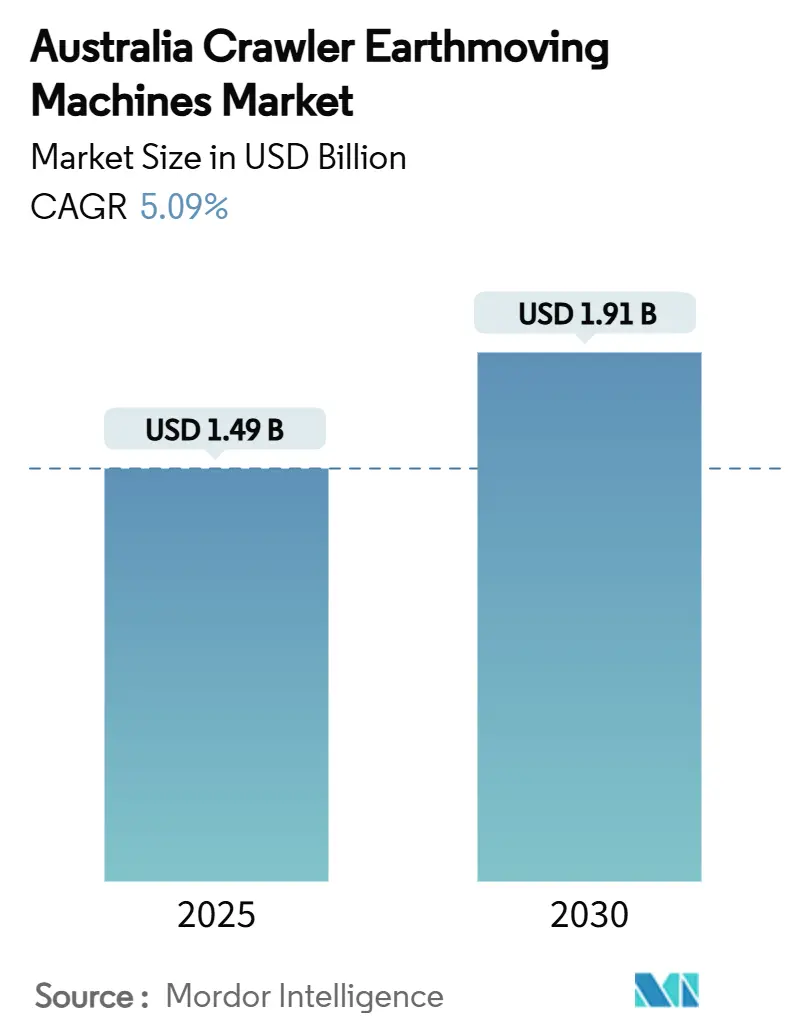

| Market Size (2025) | USD 1.49 Billion |

| Market Size (2030) | USD 1.91 Billion |

| Growth Rate (2025 - 2030) | 5.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The Australia crawler earthmoving machines market size stood at USD 1.49 billion in 2025 and, supported by a 5.09% CAGR, is forecast to reach USD 1.91 billion by 2030. The expansion reflects steady public‐sector spending, a buoyant mining pipeline, and the ongoing replacement of aging fleets, even as equipment costs have climbed more than 30% since the COVID-19 shock. Strong project backlogs in road, rail, and renewable energy underpin demand, while Western Australia’s and Queensland’s iron-ore and lithium investments extend the order cycle for heavy‐duty machines. Electric and hybrid crawlers are gaining ground as Stage V rules tighten procurement criteria, yet diesel platforms still dominate remote mine sites where refueling infrastructure is entrenched. Financing hurdles and supply chain delays temper growth, pushing some contractors toward rentals and usage-based contracts. OEMs that combine telematics, autonomous functions, and robust after-sales networks are capturing the most predictable revenue streams in the consolidating value chain.

Key Report Takeaways

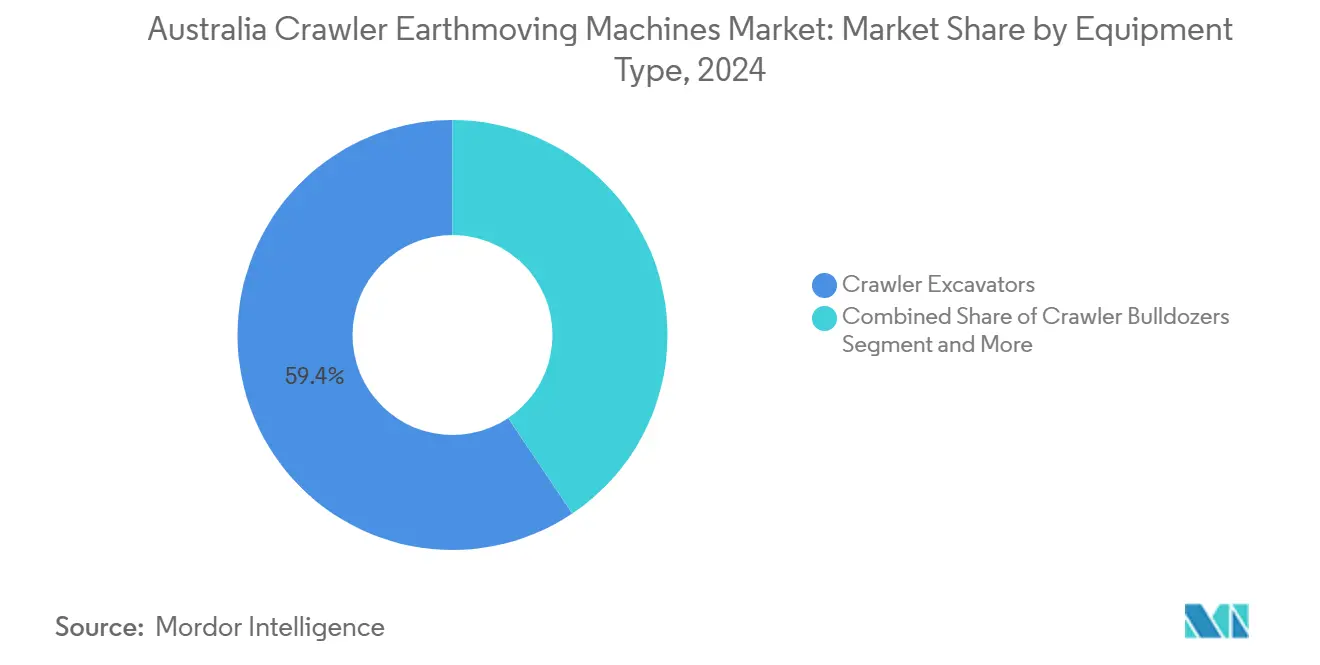

- By equipment type, crawler excavators controlled 59.44% of the Australia crawler earthmoving machines market share in 2024, whereas tracked loaders and skid-steers are projected to expand at a 5.73% CAGR through 2030.

- By propulsion, internal combustion engines held 93.16% share of the Australia crawler earthmoving machines market size in 2024, while electric and hybrid variants are forecast to advance at a 17.46% CAGR between 2025-2030.

- By engine power, the 100-200 HP bracket accounted for 42.65% of the Australia crawler earthmoving machines market size in 2024; sub-100 HP units register the fastest 6.07% CAGR to 2030.

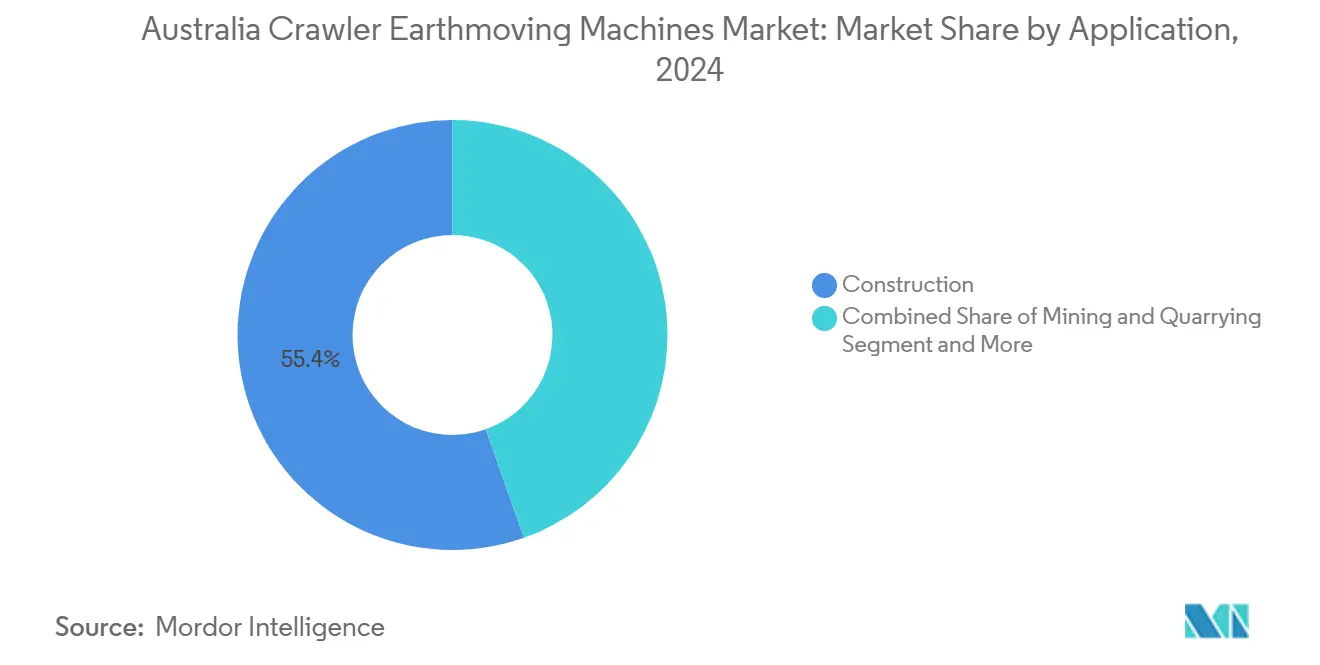

- By application, construction captured 55.42% revenue in 2024, and mining is set to record the highest 6.65% CAGR during the outlook period.

- By distribution channel, authorized dealers commanded 59.25% share in 2024, whereas rental and leasing firms are expanding at a 7.44% CAGR to 2030.

Australia operates as part of an interconnected international environment rather than as a self-contained country level unit. The crawler earthmoving machines market research by Mordor Intelligence places together all major developments across the globe within that wider frame.

Australia Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID Infrastructure Rebound | +1.5% | NSW, VIC, QLD corridors | Short term (≤ 2 years) |

| Aging Crawler Fleet Replacement | +1.2% | WA and QLD mining hubs | Medium term (2-4 years) |

| Mining CAPEX Growth in WA & QLD | +1.1% | Pilbara and QLD resource belts | Medium term (2-4 years) |

| Electrification Incentives & Stage V Mandates | +0.8% | National | Long term (≥ 4 years) |

| Digital Twins & Telematics Savings | +0.6% | National, large mines | Long term (≥ 4 years) |

| Circular Demolition Project Surge | +0.4% | Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rebound in Public Infrastructure Spending Post-COVID Stimulus

Federal commitments of AUD 107.1 billion over four years have revitalized state transport programs, creating predictable loads for crawlers on road, rail, and utility corridors. Infrastructure Australia lists AUD 237 billion in major projects, with 63% in transport, translating into high demand for tracked machines able to traverse uneven terrain [1]Infrastructure Australia, “2025 Infrastructure Market Capacity Report,” infrastructureaustralia.gov.au. Equipment is deployed longer per shift, encouraging contractors to invest in automated grade control to offset skilled-operator shortages. Sign-on bonuses nearing AUD 10,000 for excavator operators illustrate a tightening labor supply that further supports semi-autonomous crawler adoption. Public packages also cushion the market from residential softness, smoothing equipment utilization rates.

Accelerated Replacement of Ageing Crawler Fleets for Safety and Efficiency

Fleet renewal programs have intensified because many units in Western Australia’s iron-ore operations exceed 10 years of service and operate more than 20 hours daily. Safety rules now call for collision avoidance packages, fatigue monitoring, and tighter emission bands that are hard to retrofit on legacy machines. BHP and Rio Tinto are retiring diesel workhorses in phases and pairing replacements with dynamic energy transfer systems that cut idle time [2]BHP Group, “BHP and Caterpillar to Accelerate Zero-Emission Mining Trucks,” bhp.com. Equipment loans have stabilized, allowing operators to justify capital outlays that raise hydraulic efficiency and intelligent machine control by 15-20%. Rental houses mirror this trend, rotating older fleets into secondary markets and stocking late-model crawlers that meet new contract specifications.

Mining CAPEX Upswing in WA and QLD Iron-Ore/Lithium Projects

Western Australia recorded AUD 2.58 billion in mineral exploration outlays during 2023-24, and fresh iron-ore expansions such as the USD 2 billion Western Range mine are sustaining heavy crawler demand. Queensland’s lithium corridor shows similar momentum, with suppliers reporting full order books for high-horsepower dozers and excavators. Rio Tinto alone spent AUD 10.3 billion with local vendors in 2024, much of it on earthworks and haulage units. Large mines favor multi-purpose crawlers that integrate autonomous haulage and telematics to reduce downtime across vast sites. As ore grades decline, higher material movement intensifies replacement cycles and supports mid-single-digit volume growth.

Electrification Incentives and Stage V Emission Mandates

The national adoption of Stage V standards is reshaping bid documents across construction and mining. New South Wales now restricts government purchases to Tier 4 or Stage IV engines, foreshadowing nationwide tightening [3]New South Wales Environment Protection Authority, “Cleaner Construction Procurement Policy,” epa.nsw.gov.au. Mining majors face higher ESG-linked lending spreads for diesel fleets, pushing them toward zero-emission pilots. Fortescue, for example, logged 1 million tonnes moved with an electric excavator and is scaling a 475-unit deal that includes 360 autonomous trucks. Volvo has rolled out battery models suited to urban sites, but a lack of high-capacity chargers in remote pits still limits heavy electric crawler adoption. Equipment managers must weigh compliance against the operational continuity delivered by mature diesel platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX & Tight Credit | -1.8% | National, SMEs are most affected | Short term (≤ 2 years) |

| Raw Material Supply Volatility | -1.2% | Nationwide | Medium term (2-4 years) |

| ESG Costs for Diesel Units | -0.9% | Large mines and public contracts | Medium term (2-4 years) |

| Limited Fast-Charging for >20-Ton Crawlers | -0.7% | Remote WA and QLD | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Tightening Credit

Nearly 2,000 Australian builders entered administration between July 2022 and July 2023, exposing the fragility of fixed-price contracts as equipment and material bills soared. Interest rates remain above pre-pandemic norms, and banks scrutinize collateral quality, restricting access for smaller contractors. These pressures channel demand toward rentals, a segment tracking 7.44% CAGR, because usage fees can be passed through to project owners more easily than capital costs. Rental houses leverage scale to negotiate bulk purchases, keeping fleet age low and compliance high, which erodes OEM direct sales margins.

Raw-Material and Component Supply Volatility

Infrastructure Australia notes that construction material prices widened by 24% year on year in 2024, while OEMs cite lead times of up to 18 months for certain crawler components. Queensland contractors paid 9-12% more for Gyprock and up to 5% more for tools, exemplifying broad inflation. Scarcity forces operators to run equipment longer, boosting demand for predictive maintenance software and stocking of critical spares. OEMs with vertically integrated supply chains, or those that dual-source castings and hydraulics, maintain an edge. However, elevated inventories raise working-capital needs, a risk that smaller importers struggle to absorb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators Dominate Amid Compact Growth

Crawler excavators held a 59.44% Australia crawler earthmoving machines market share in 2024, underscoring their versatility in digging, lifting, and precision grading. Contractors rely on quick couplers and grade-assist systems that cut rework and fuel burn. The Australia crawler earthmoving machines market size for excavators will keep pace with civil packages and mine stripping volumes through 2030. Tracked loaders and skid-steers, though smaller, post a 5.73% CAGR as urban infill and rental fleets demand agile gear.

In heavy mines, bulldozers remain relevant for high-volume push operations, yet their growth trails versatile excavators that now feature 3D machine control. Crawler cranes and pipe-layers serve niche applications such as renewable transmission towers and gas pipelines. OEMs prioritize multi-functionality because equipment buyers aim to shrink fleet variety and training overhead. Advanced attachments, including tiltrotators and screening buckets, broaden task ranges without extra chassis investment, preserving share in a mildly slowing capital cycle.

By Propulsion: Electric Transition Accelerates Despite ICE Dominance

Internal combustion platforms commanded 93.16% of the Australia crawler earthmoving machines market size in 2024, supported by established diesel logistics and high duty cycles. The segment’s stability rests on proven uptime in arid and remote conditions. Nevertheless, battery-electric and hybrid variants post 17.46% CAGR as miners set net-zero deadlines and cities enforce emission ceilings.

OEMs price electric crawlers at premiums of 30-40%, yet SRK Consulting shows lifetime unit cost per tonne can fall 65% where power is renewable and charging docks are close to pits. Fortescue’s AUD 2.8 billion agreement with Liebherr signals credible long-range demand and boosts supplier confidence. The Australia crawler earthmoving machines market size tied to electric propulsion will still hinge on charger rollouts and grid stability, particularly beyond major grids. Until then, dual-fuel and hybrid genset systems will bridge practical gaps.

By Engine Power Output: Mid-Range Dominance with Compact Growth

Machines in the 100-200 HP band accounted for 42.65% of the Australia crawler earthmoving machines market share during 2024, balancing tractive effort and fuel economy for most civil and mine-service missions. Contractors favor this range for its transportability under common axle limits and adaptability to multiple attachments.

The sub-100 HP class records the fastest 6.07% CAGR, fed by suburban utility corridors and horticulture projects where axle pressure and maneuverability matter. High-power units above 400 HP remain indispensable in Pilbara iron-ore operations, but their steep price cap overall demand. Data analytics guides buyers to right-size power, minimizing excess capacity and raising utilization across fleets that increasingly blend owned and rented units.

By Application: Construction Leads While Mining Accelerates

Construction contributed 55.42% of revenue in 2024 as federal and state infrastructure packages triggered continuous call-offs for earthworks, foundation excavation, and trenching. Long project durations raise utilization rates, justifying ownership of high-spec crawlers with semi-autonomous functions.

Mining posts the quickest 6.65% CAGR, driven by Western Australia’s iron-ore expansions and Queensland’s lithium build-outs. Large pits require robust undercarriages and sealed-for-life pins that endure abrasive conditions, prompting OEMs to introduce heavy-duty variants. Agriculture and forestry absorb modest volumes for land clearing, yet renewables corridors add new tasks such as wind-farm access roads that benefit midsize machines.

By Distribution Channel: Dealers Dominate as Rental Gains Momentum

Authorized dealers represented 59.25% of the Australia crawler earthmoving machines market share in 2024, leveraging deep parts inventories, credit programs, and certified service technicians. Their ability to roll out over-the-air updates and warranty refurbishments cements loyalty.

Rental and leasing, however, expands 7.44% CAGR as contractors hedge capital risk and align fleet size with fluctuating workloads. Telemetry from rental fleets allows pay-as-used billing, heightening transparency. Direct OEM ordering remains prevalent among Tier 1 miners purchasing bespoke configurations, but small and medium enterprises now view rentals as a strategic alternative that compresses balance-sheet exposure while guaranteeing Stage V compliance.

Geography Analysis

Western Australia and Queensland dominate crawler demand because iron-ore and critical-minerals mines replace fleets on five-year cycles and often expand capacity. Western Australia’s mineral exploration spend hit AUD 2.58 billion in 2023-24, fostering stable annual tenders for 200-plus-ton excavators and high-horsepower dozers. Queensland’s coal and lithium corridors echo this pattern, underwritten by Asian steel and battery material appetite.

New South Wales and Victoria supply large volumes of construction work, ranging from Sydney’s AUD 21.6 billion rail tunnels to Melbourne’s AUD 10.2 billion underground arterial road. These Megaprojects specify tracked machines for confined urban digs where ground pressure needs tight control. Urban planners also enforce low-emission zones, making electric compact crawlers attractive despite the cost premium.

South Australia, Tasmania, and the Northern Territory furnish smaller slices of demand, mostly tied to wind, hydrogen, and defense infrastructure. Their projects still favor mid-range diesel crawlers due to logistical constraints. Geographic fragmentation means OEMs must stage parts depots near both seaports and inland mining districts, while rental chains calibrate inventories to the contrasting jobsite profiles of coastal cities and remote resource basins.

The crawler earthmoving machines market is assessed by Mordor Intelligence through a multi-layered geographic lens, covering other regions such as Europe, along with detailed country-level analysis for Indonesia, Thailand, United States, Philippines, Singapore, South Korea, and Saudi Arabia.

Competitive Landscape

Global OEMs anchor the Australia crawler earthmoving machines market with well-entrenched dealer networks. Caterpillar leads, having logged more than 1 million autonomous drilling meters at Australian coal operations, which evidences technology maturity and consistent productivity gains. Komatsu strengthens its foothold through local manufacturing, parts warehousing, and recognition for workplace excellence, further underlining customer trust.

Liebherr raised its profile by securing Fortescue’s record AUD 2.8 billion zero-emission order, indicating that the supplier’s electric strategy resonates with majors seeking decarbonization. Hitachi Construction Machinery’s AUD 10 million stake in Envirosuite flags the growing role of environmental monitoring and data science in equipment value propositions.

Market rivalry extends from hardware to integrated services. OEMs bundle uptime guarantees, remote diagnostics, and operator training to lock in multi-year contracts. Dealers retrofit legacy fleets with smart kits to slow attrition. Independent rental firms, headlined by Coates, wield large telemetry-equipped inventories that challenge OEM leasing arms. As sustainability pressures mount, contenders capable of complete life-cycle support—covering financing, energy infrastructure and digital optimization—are poised to outpace rivals focused solely on iron.

Australia Crawler Earthmoving Machines Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery Co., Ltd.

Volvo Construction Equipment AB

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Select Plant Australia deployed Western Australia’s first 250-ton electric crawler crane on the Swan River Crossings project, advancing zero-emission lifting capacity.

- April 2025: A D65EXi dozer expanded an Australian contractor’s Komatsu fleet to 23 units, positioning the firm to tackle Hunter Region subdivisions and remediation programs.

- May 2024: Caterpillar previewed redesigned compact track loader models set to replace the 259D3, 279D3, and 289D3 ranges.

- May 2024: Liebherr-Australia delivered five PR 776, 70-ton dozers to Western Plant Hire for immediate deployment at a Western Australian mine.

Australia Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Internal Combustion Engine (ICE) |

| Electric and Hybrid |

| Below 100 HP |

| 100-200 HP |

| 201-400 HP |

| Above 400 HP |

| Construction |

| Mining and Quarrying |

| Agriculture and Forestry |

| Others |

| Direct OEM Sales |

| Authorized Dealers |

| Rental and Leasing Firms |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric and Hybrid | |

| By Engine Power Output | Below 100 HP |

| 100-200 HP | |

| 201-400 HP | |

| Above 400 HP | |

| By Application | Construction |

| Mining and Quarrying | |

| Agriculture and Forestry | |

| Others | |

| By Distribution Channel | Direct OEM Sales |

| Authorized Dealers | |

| Rental and Leasing Firms |

Key Questions Answered in the Report

How big is Australia’s crawler earthmoving machines space in 2025?

The value is USD 1.49 billion, reflecting steady demand from public works and mining projects.

What compound annual growth rate is expected for these machines through 2030?

A 5.09% CAGR is projected, taking total value to USD 1.91 billion by the end of the forecast period.

Which equipment category holds the highest share of demand?

Crawler excavators lead with 59.44% share thanks to their versatility across construction and mining tasks.

Why are electric crawlers gaining traction on Australian jobsites?

Stage V emission rules and net-zero targets are pushing buyers toward battery-electric options that promise lower operating costs and easier compliance.

Page last updated on: