Philippines Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

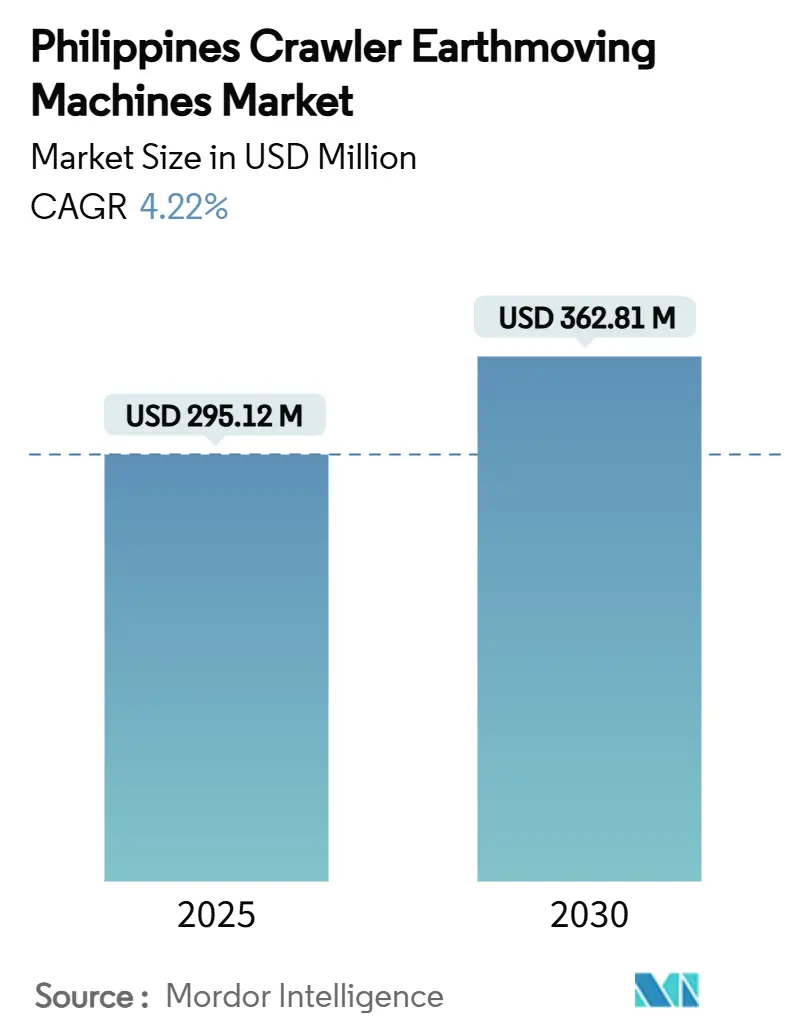

| Market Size (2025) | USD 295.12 Million |

| Market Size (2030) | USD 362.81 Million |

| Growth Rate (2025 - 2030) | 4.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Philippines Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The Philippines crawler earthmoving machines market size stands at USD 295.12 million in 2025 and is forecast to reach USD 362.81 million by 2030, translating into a 4.22% CAGR over the five-year horizon. Government outlays on bridges, expressways, rail lines, and disaster-mitigation projects continue to anchor demand, while revived large-scale mining in Mindanao adds a counter-cyclical boost. Equipment owners are accelerating fleet renewal to improve safety, reduce unscheduled downtime, and trim fuel bills that can swallow 35-40% of operating costs. At the same time, electrification mandates and Stage V-equivalent emission rules are nudging buyers toward hybrid and battery-electric models despite infrastructure gaps. Dealer networks remain the primary route to market, yet a fast-growing rental channel offers capital-constrained contractors flexible access to the latest machines amid tighter credit and volatile project pipelines.

Key Report Takeaways

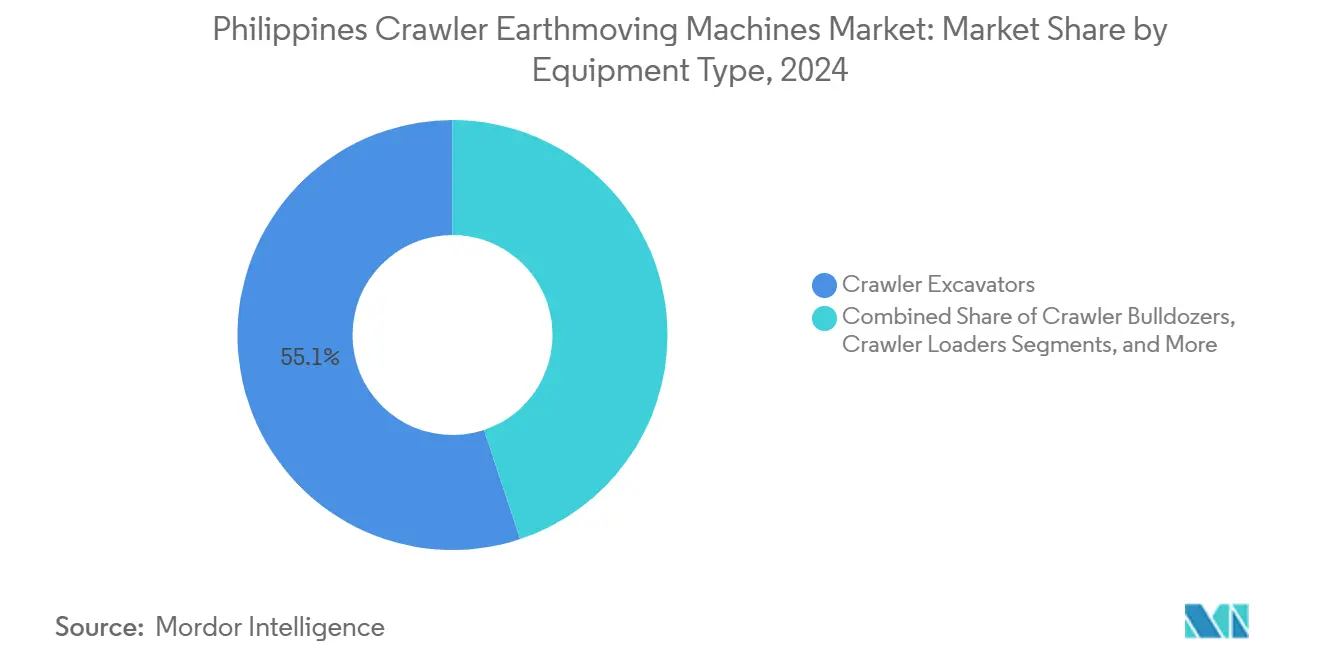

- By equipment type, crawler excavators led with 55.12% of the Philippines crawler earthmoving machines market share in 2024; compact tracked loaders and skid-steers are projected to expand at a 4.88% CAGR through 2030.

- By propulsion, internal combustion engines commanded 96.91% share of the Philippines crawler earthmoving machines market size in 2024, while electric and hybrid units are advancing at a 21.78% CAGR to 2030.

- By engine power output, the 201–400 HP class represented 39.61% of the Philippines crawler earthmoving machines market size in 2024, and below 100 HP machines are rising at a 5.12% CAGR up to 2030.

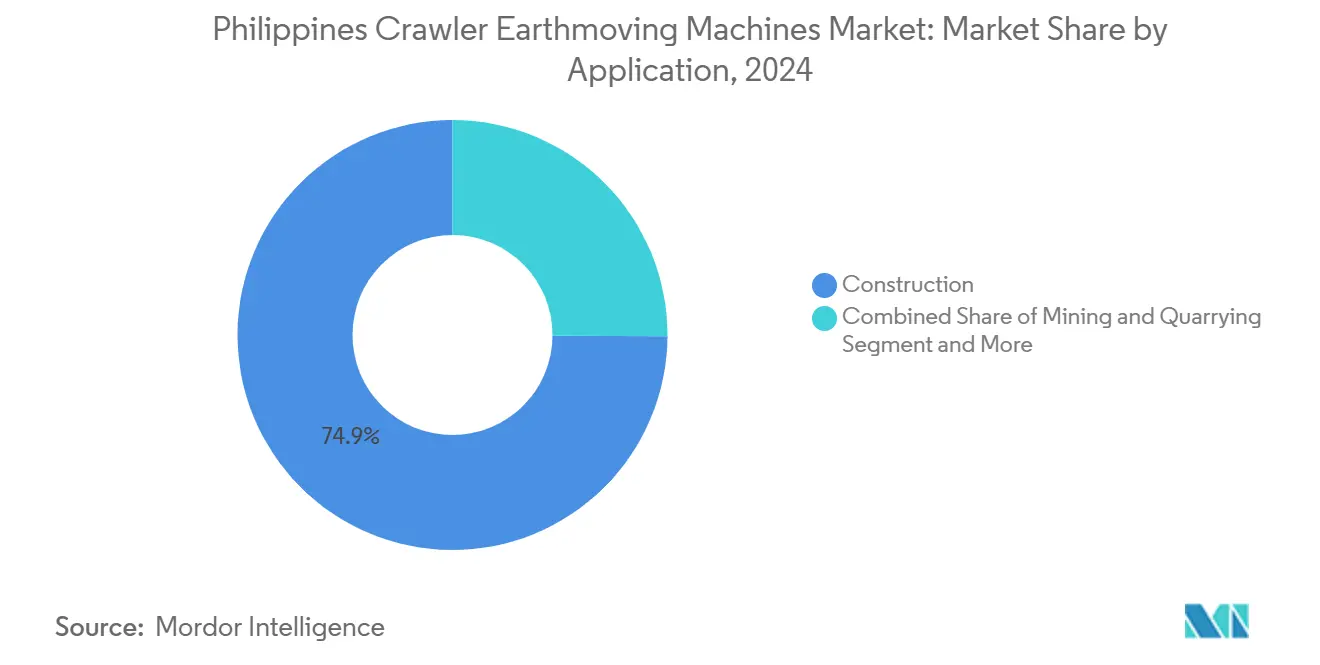

- By application, construction accounted for a 74.94% share of the Philippines crawler earthmoving machines market size in 2024, and mining activities are moving ahead at a 6.35% CAGR through 2030.

- By distribution channel, authorized dealers held 49.76% of the Philippines crawler earthmoving machines market share in 2024, whereas rental and leasing services are climbing at a 7.96% CAGR during the forecast period.

Competitive positioning in Philippines includes both locally based firms and those operating across multiple regions. The market landscape in the global crawler earthmoving machines industry research shows how these players are arranged internationally.

Philippines Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Backed “Build Build Build 2.0” Pipeline | +1.2% | Priority corridors in Luzon and Mindanao | Medium term (2-4 years) |

| Accelerated Replacement of Ageing Crawler Fleets | +0.8% | Metro Manila, Cebu and other growth corridors | Medium term (2-4 years) |

| Revival of Large-Scale Mining Projects | +0.7% | Mindanao with spillover to national suppliers | Long term (≥ 4 years) |

| Electrification Incentives and Stage V Mandates | +0.6% | Early-adopter cities nationwide | Long term (≥ 4 years) |

| Digital Twins and Telematics Savings | +0.4% | Large contractors across the archipelago | Short term (≤ 2 years) |

| Surge in Circular-Demolition Projects | +0.3% | Metro Manila and key urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-backed “Build Build Build 2.0” Infrastructure Pipeline

The PHP 9-trillion Build Better More program spans 194 flagship assets, from the Luzon Spine Expressway to the Metro Manila Subway. Infrastructure disbursements topped PHP 1.545 trillion in 2024, equal to 5.8% of GDP, and the 2025–2030 budget keeps annual spending above 5% of GDP. Large earthmoving packages for bridges, flood-control structures, and elevated rail lines require a continuous supply of excavators, bulldozers, and cranes. Public-private partnership reforms under the new PPP Code shorten procurement cycles, giving contractors visibility to invest in higher-capacity fleets. Sustained public spending shields equipment demand from private-sector cycles and anchors the market CAGR.

Accelerated Replacement of Ageing Crawler Fleets for Safety and Efficiency

Operators are retiring units older than 10–15 years as stricter site-safety rules and insurance clauses penalize breakdowns that halt critical path activities. Modern machines cut fuel use by up to 20% and embed ROPS/FOPS cabins plus 360-degree cameras, reducing accident risk and insurance premiums. Penalty clauses tied to downtime on flagship expressway and railway projects intensify the push to refresh fleets. Government agriculture mechanization schemes such as PhilMech’s PHP 59.6 million farm-equipment rollout further reinforce a culture of machinery renewal [1]Philippine News Agency, “PhilMech Distributes Farm Machines Worth PHP 59.6 Million,” pna.gov.ph. The resulting uptick in replacement cycles positions dealers and rental fleets to capture premium pricing on high-spec equipment.

Revival of Large-scale Mining and Quarrying Projects in Mindanao

Environmental clearances issued in 2024 reopened billion-dollar deposits such as King-king and Tampakan. Combined capital commitments exceed USD 4 billion and extend out to 2040, requiring mass excavation, haul-road construction, and tailings-dam reinforcement. Crawler excavators fitted with rock-bucket attachments and dozers upgraded with multi-shank rippers are in strong demand. Global commodity prices for copper and gold support project economics, and operators are stipulating the latest-generation machinery with tier-four compliant engines to satisfy lender ESG covenants. Suppliers able to mobilize support teams in Davao Region and South Cotabato enjoy a first-mover edge [2]Mines and Geosciences Bureau, “Mining Projects in Mindanao,” mgb.gov.ph.

Electrification Incentives and Stage V Emission Mandates

Clean-air regulations are tightening as Euro 4 norms for heavy vehicles expand toward Stage V-equivalent limits for off-road machinery. The Electric Industry Development Act stipulates 5% EV adoption across government fleets, nudging public-works contractors toward battery-electric or hybrid crawlers. Early pilots rely on mobile charging rigs and battery-swap packs to circumvent limited grid capacity on jobsites. Manufacturers such as Komatsu have launched battery-electric drilling and bolting rigs, while local distributor ACMobility fields “Power-on-Wheels” chargers for urban projects. Adoption remains niche today, but cumulative incentives, lower noise levels, and ESG compliance requirements are expected to accelerate take-up after 2027[3]Department of Environment and Natural Resources, “Clean Air Act Implementation Updates,” denr.gov.ph.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX and Tightening Credit | -0.7% | Nationwide; acute for micro and small contractors | Short term (≤ 2 years) |

| Raw-Material and Component Supply Volatility | -0.5% | Global supply shocks felt across Philippine market | Medium term (2-4 years) |

| Scarcity of Fast-Charging Infrastructure | -0.3% | Urban hubs progressing faster than rural zones | Long term (≥ 4 years) |

| ESG-Linked Cost of Ownership for Diesel Units | -0.4% | Strictest enforcement in major metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Tightening Credit

Crawler excavator prices have climbed 15-25% since 2024, pushing a 25-ton unit beyond PHP 15 million. Philippine banks flag higher non-performing loan ratios in construction, prompting stricter collateral and shorter tenors. The Personal Property Security Act seeks to unlock movable-asset lending, yet full implementation and lender confidence could take two years. In the interim, contractors pivot to rental agreements that shift capital costs to operators with stronger balance sheets. Rental penetration is particularly high among subcontractors on expressway packages who must mobilize quickly but hand machines back once earthworks finish.

Raw-material and Component Supply Volatility

Lead times on hydraulic pumps, undercarriage assemblies, and electronic control modules have stretched to nine months, forcing dealers to stock deeper inventories. Logistics surcharges tied to container shortages and rerouted shipping lanes inflate delivered costs. Manufacturers diversify by sourcing steel castings from domestic foundries in Batangas and Pampanga, yet quality consistency remains a hurdle. Higher safety stocks tie up working capital, feeding into end-user prices. Contractors often delay purchases or scale machinery specifications downward when quoted lead times threaten project schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Excavators Retain Scale as Compact Loaders Accelerate

Crawler excavators accounted for 55.12% of the Philippines crawler earthmoving machines market share in 2024, underpinned by their adaptability across trenching, slope-cutting, and mining overburden removal. High utilization rates on Luzon expressway packages keep resale values buoyant, reinforcing buyer preference for established models with wide parts support. Compact tracked loaders and skid-steers, although smaller in absolute volume, are forecast to grow at a 4.88% CAGR as urban infill projects demand agile machines capable of working within narrow lots and under elevated rail viaducts. Rental houses expand fleets of these compact units because a single tilt-tray truck can move several machines in one run, lowering logistics costs. Bulldozers, the second-largest category, secure steady orders for mine pre-stripping and expressway embankment works, whereas crawler cranes and pipe-layers fill specialist niches on bridge pylons and LNG terminals. OEMs address each pocket of demand with tailored configurations—long-reach excavators for dredging, mass-excavation booms for quarrying, and low-clearance cab versions for tunnel headings—helping sustain equipment diversity even as excavators dominate core spending.

The lower barriers to entry for compact equipment invite new Asian brands, intensifying price competition at the smaller end of the spectrum. In contrast, heavy excavators above 40 tons rely on established dealer service networks and advanced telematics, elements harder for late entrants to replicate. As a result, the premium segment remains relatively consolidated. Across categories, contractors increasingly evaluate total life-cycle cost rather than capital outlay, placing a premium on fuel-efficiency, machine-health alerts and resale liquidity. Such criteria favor brands with proven uptime records, reinforcing the entrenched positions of Caterpillar, Komatsu and Hitachi in the most revenue-rich slices of the market.

By Propulsion: Diesel Dominates Today, Hybrids Bridge to an Electric Future

Internal-combustion models represented 96.91% of the Philippines crawler earthmoving machines market size in 2024, reflecting familiar service practices, ubiquitous diesel supply, and depreciation schedules aligned to conventional financing. Dealers maintain stocked parts depots that guarantee next-day delivery for high-wear items, an advantage difficult to replicate for emerging electric lines. Even so, electric and hybrid machines are racing ahead at a 21.78% CAGR, albeit from a small base, aided by import-duty exemptions and growing ESG clauses in PPP projects. Komatsu, Caterpillar, and Sany have each unveiled 20- to 28-ton battery excavators with swappable packs, and early adopters cite near-silent night-shift operations as a benefit in noise-sensitive urban sites.

Charging remains the chief bottleneck. Portable battery containers and solar-augmented microgrids appear on pilot projects but add logistical complexity. Hybrid drives, therefore, serve as an interim solution, blending regenerative swing motors with downsized diesels to deliver 15% fuel savings without plug-in needs. Contractors bidding on Build Better More rail packages, which impose strict nighttime noise limits, see hybrids as an immediate compliance tool. ICE may continue to rule provincial infrastructure and mine sites through 2030, yet the narrative has shifted decisively toward partial or full electrification, signaling a coming inflection point once charging networks mature and battery densities climb.

By Engine Power Output: Mid-range Machines Command, Compacts Gain Momentum

Mid-range machines in the 201–400 HP bracket controlled 39.61% of the Philippines crawler earthmoving machines market size in 2024, aligning with typical cut-and-fill volumes on road and rail packages. These units balance reach, breakout force, and transportability on standard low-bed trailers. However, sub-100 HP machines are climbing at a 5.12% CAGR as contractors tackle drainage, fiber-optic trenching, and townhouse basement excavation that bigger models cannot physically enter. OEMs add quick-hitch hydraulic couplers and multifunction joysticks, letting one operator switch from bucket to breaker within minutes, boosting small-unit productivity.

Equipment above 400 HP retains relevance in mine pre-strip and dam construction, where push rates and bulk rock movement trump maneuverability. Demand here correlates with the mining revival in Mindanao and large flood-control reservoirs planned in Central Luzon. The 100–200 HP window caters to utilities and rural road maintenance, offering solid performance in mixed terrain without the transport permits sometimes required for heavier gear. As provincial governments procure disaster-relief fleets, this segment gains incremental support. Collectively, the spread of jobs from tight city lots to sprawling mineral leases underpins a broad horsepower mix, though mid-range units remain the undisputed workhorses.

By Application: Construction Dominates While Mining Rebounds

Construction activities absorbed 74.94% of the Philippines crawler earthmoving machines market size in 2024, driven by expressway corridors, urban rail, and mixed-use real-estate build-outs. Continuous public spending helps shield contractors from private-sector volatility, assuring utilization levels attractive to financers. Earthmoving peaks during early project phases, but later works—piling, slope protection, and landscaping—still rely on specialized crawler attachments, prolonging machine demand beyond bulk excavation.

Mining and quarrying is the fastest-rising slice at 6.35% CAGR, riding on renewed policy clarity and high global metals pricing. Copper-gold projects in Davao de Oro and South Cotabato need fleets of 90- to 120-ton excavators, D11-class dozers and drill rigs, opening a lucrative revenue pool for OEMs with hard-rock expertise. Agriculture and forestry attract funding through mechanization grants, yet remain a modest share of value owing to lower horsepower needs and seasonal usage. Waste-management, deconstruction, and environmental-remediation jobs inch upward, reflecting tighter landfill rules and circular-economy targets. Although smaller in absolute terms, these emerging applications drive product innovation such as high-reach demolition booms and hybrid powertrains suited for closed-loop urban sites.

By Distribution Channel: Dealers Hold Ground as Rentals Accelerate

Authorized dealers accounted for 49.76% of the Philippines crawler earthmoving machines market share in 2024 by bundling sales, service, parts, and financing into one interface. Customers value guaranteed parts availability and factory-trained technicians, especially on island provinces where downtime can halt ferry schedules and blow project budgets. Dealer capture of preventive-maintenance contracts also secures recurring revenue and machine telemetry data that feed future spec improvements.

Rental and leasing firms, scaling at 7.96% CAGR, fulfill demand spikes on projects with compressed schedules or uncertain funding. The rental model frees contractors from large capital outlays and depreciation exposure. Larger players such as T1 Rentals import niche cranes and tunneling rigs unavailable from OEM branches, carving a technological edge. Direct OEM sales persist among mining majors who negotiate fleet-wide discounts and bespoke specs, but the channel’s share is smaller owing to logistic complexities across the archipelago. Over the forecast period, dealers and rental specialists are expected to cooperate through buy-back guarantees and shared telematics platforms, ensuring customer uptime while optimizing fleet rotations.

Geography Analysis

Luzon is the largest regional buyer, absorbing the bulk of machines deployed on the North–South Commuter Railway, the 1,200 km Luzon Spine Expressway Network, and Metro Manila’s subway and bridge retrofits. Dense dealer grids in Manila, Bulacan, and Pampanga shorten service response times, a decisive factor for contractors facing liquidated damages on delayed works. Proximity to Subic and Batangas ports simplifies heavy-equipment import clearance, further entrenching Luzon’s lead position.

Mindanao delivers the fastest growth thanks to its USD 4 billion pipeline of copper-gold projects and complementary infrastructure such as access roads, ports, and transmission corridors. Security concerns have eased, permitting OEM technicians to support equipment deep inside Davao de Oro and South Cotabato. Government commitments to responsible mining and social-development programs bolster investor confidence, triggering multiyear purchase contracts for high-capacity excavators, dozers, and haulage support gear. Ancillary industries—explosives, maintenance services, and fuel logistics—are expanding in tandem, reinforcing a virtuous investment cycle.

The Visayas region maintains a steady share through mixed tourism, agriculture and port-expansion activities. Projects such as the Cebu–Cordova Link Expressway underline the need for precision crawler cranes and large vibratory hammers during pylon construction. Mechanized rice programs across Bohol and Negros Oriental drive sales of sub-100 HP compact crawlers suited for irrigation-canal upkeep. Inter-island logistics dictate that dealers retain parts stocks in Cebu City and Iloilo, thereby reducing vessel-borne lead times and supporting higher machine utilization.

Mordor Intelligence tracks the crawler earthmoving machines market across other major regions such as Europe, with additional country-level coverage spanning Australia, South Korea, Indonesia, United States, Thailand, Singapore, and Saudi Arabia, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Global OEMs compete fiercely with technology, after-sales support, and financing assistance. Caterpillar underscores autonomy and electrification, unveiling the Cat 395 Front Shovel excavator and integrating real-time health dashboards that cut unexpected breakdowns by 30%. A centennial-edition equipment line launched in 2025 strengthens brand visibility, while Cat Financial tailors peso-denominated leases to mitigate foreign-exchange risk for local clients.

Komatsu pursues margin expansion through calibrated price hikes while rolling out Smart Construction drone-survey suites that optimize cut-and-fill sequencing. A recent acquisition of GHH Group boosted underground mining offerings, matching Mindanao’s long-term equipment needs. Komatsu’s battery-swap concept for load-haul-dump machines illustrates a pragmatic approach to electrification in grid-constrained sites.

Hitachi Construction Machinery leverages a remanufacturing push and value-chain services to lift revenue and net income year-on-year. The firm partners with Philippine universities on operator-training simulators, building a pipeline of skilled manpower crucial to sustaining rising equipment sophistication. Chinese brands Zoomlion and Sany make inroads through heavy-lift crawler cranes, exemplified by the 150-ton SCE1500TB introduced by T1 Rentals. Their competitive pricing challenges incumbents, yet long-term buyer loyalty appears tied to robust parts ecosystem and residual values, domains still dominated by Japan- and US-based leaders.

Philippines Crawler Earthmoving Machines Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery Co., Ltd.

Sumitomo Construction Machinery

SANY Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: T1 Rentals, the equipment arm of First Balfour, added the 150-ton SANY SCE1500TB telescopic crawler crane, becoming the first Philippine provider of this model.

- January 2024: Zoomlion delivered its 800-ton ZCC11800 crawler crane, the heaviest ever exported to the Philippines, widening high-capacity lifting options for local contractors.

Philippines Crawler Earthmoving Machines Market Report Scope

| Crawler Excavators |

| Crawler Bulldozers |

| Crawler Loaders |

| Crawler Cranes and Pipe-layers |

| Compact Tracked Loaders and Skid-steers |

| Others (Trencher, Drill Rig, etc.) |

| Internal Combustion Engine (ICE) |

| Electric and Hybrid |

| Below 100 HP |

| 100-200 HP |

| 201-400 HP |

| Above 400 HP |

| Construction |

| Mining and Quarrying |

| Agriculture and Forestry |

| Others |

| Direct OEM Sales |

| Authorized Dealers |

| Rental and Leasing Firms |

| By Equipment Type | Crawler Excavators |

| Crawler Bulldozers | |

| Crawler Loaders | |

| Crawler Cranes and Pipe-layers | |

| Compact Tracked Loaders and Skid-steers | |

| Others (Trencher, Drill Rig, etc.) | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric and Hybrid | |

| By Engine Power Output | Below 100 HP |

| 100-200 HP | |

| 201-400 HP | |

| Above 400 HP | |

| By Application | Construction |

| Mining and Quarrying | |

| Agriculture and Forestry | |

| Others | |

| By Distribution Channel | Direct OEM Sales |

| Authorized Dealers | |

| Rental and Leasing Firms |

Key Questions Answered in the Report

What is the current value of the Philippines crawler earthmoving machines market?

In 2025 the market is valued at USD 295.12 million and is projected to reach USD 362.81 million by 2030.

Which equipment type holds the largest share of spending?

Crawler excavators lead with 55.12% of 2024 spending because they fit both construction and mining tasks.

How fast is electric adoption expected to grow?

Electric and hybrid crawler models are forecast to expand to 21.78% CAGR between 2025 and 2030, albeit from a low base.

Why are rental and leasing services growing quickly?

Tighter bank credit and volatile project pipelines push contractors toward rentals, which are growing at a 7.96% CAGR.

Page last updated on: