Crawler Earthmoving Machines Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

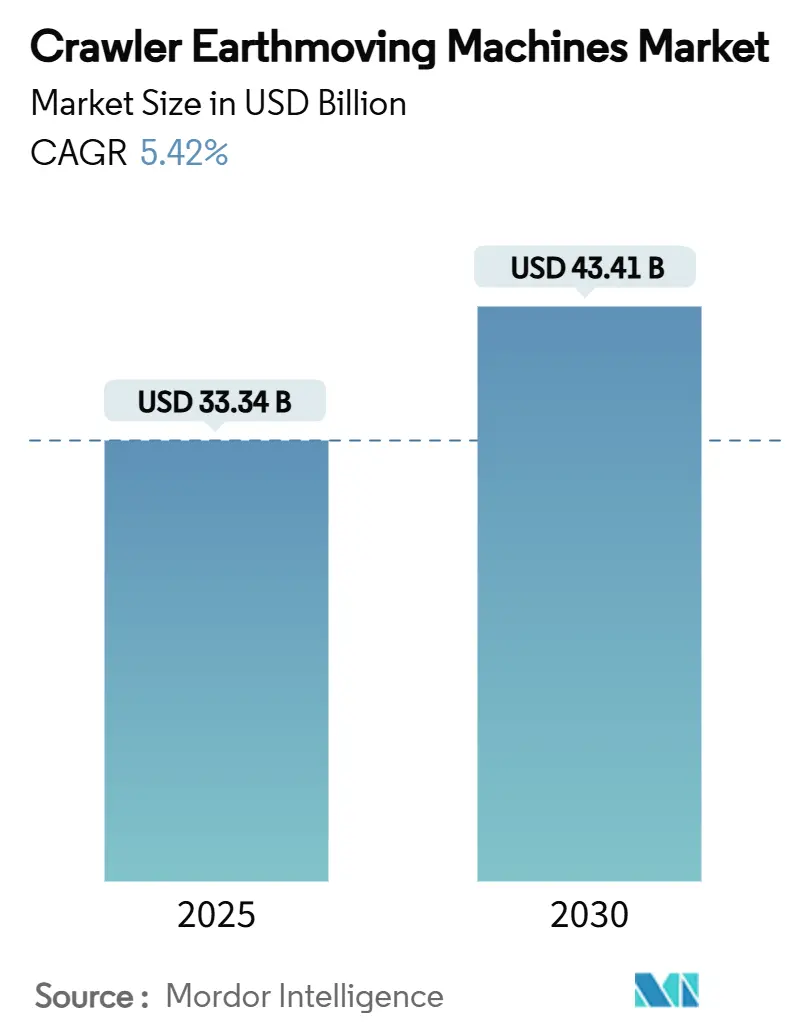

| Market Size (2025) | USD 33.34 Billion |

| Market Size (2030) | USD 43.41 Billion |

| Growth Rate (2025 - 2030) | 5.42% CAGR |

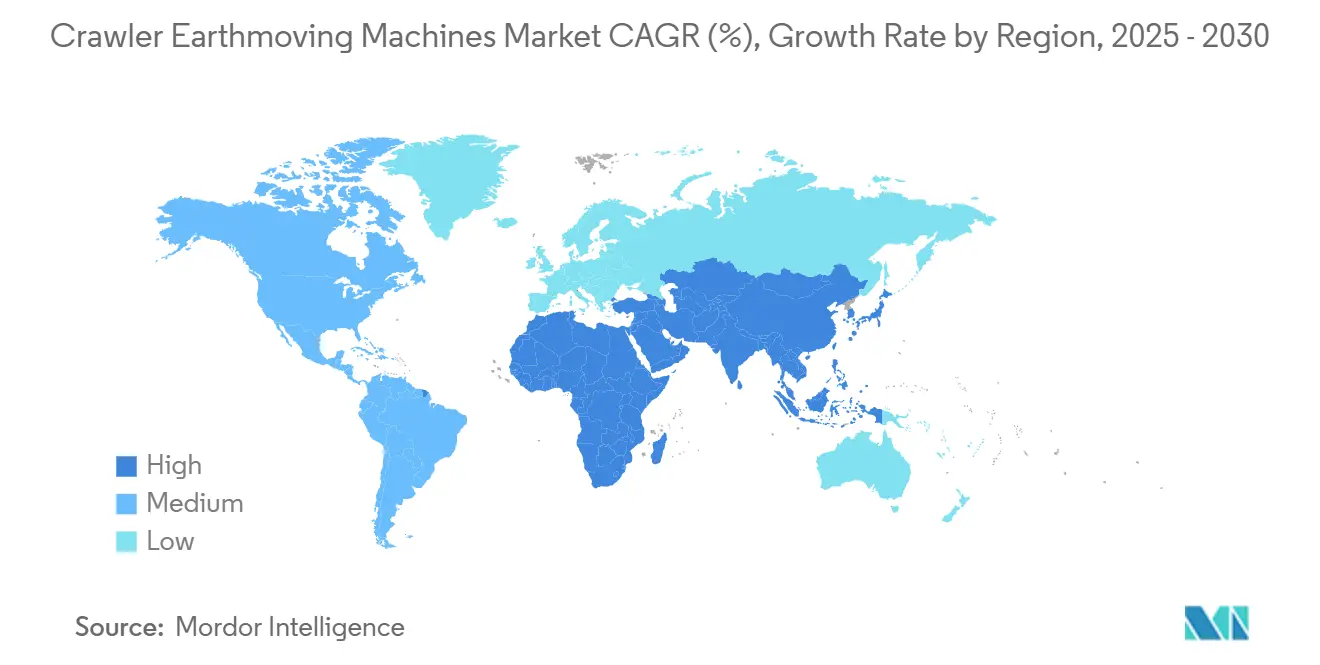

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Crawler Earthmoving Machines Market Analysis by Mordor Intelligence

The crawler earthmoving machines market size stood at USD 33.34 billion in 2025 and is forecast to reach USD 43.41 billion by 2030, advancing at a 5.42% CAGR. Robust public-works pipelines, accelerating electrification of heavy-duty equipment, and adoption of autonomous retrofit technologies underpin this growth momentum. Government infrastructure budgets in the United States, India, and Indonesia are translating into record tender volumes and clear order visibility, while zero-emission regulations in Europe and parts of Asia are pushing demand for battery-electric variants. Medium-weight machines with hybrid powertrains are emerging as the preferred bridge solution between diesel and full electrification, helping contractors curb fuel costs without extensive charging infrastructure. Meanwhile, rental penetration has returned to pre-pandemic levels as fleet owners deploy telematics-enabled asset-management platforms that lower total cost of ownership and improve uptime. Supply-chain exposure to volatile lithium prices and a tightening skilled-operator pool continue to shape procurement criteria, reinforcing the importance of technology integration in the competitive playbook.

Key Report Takeaways

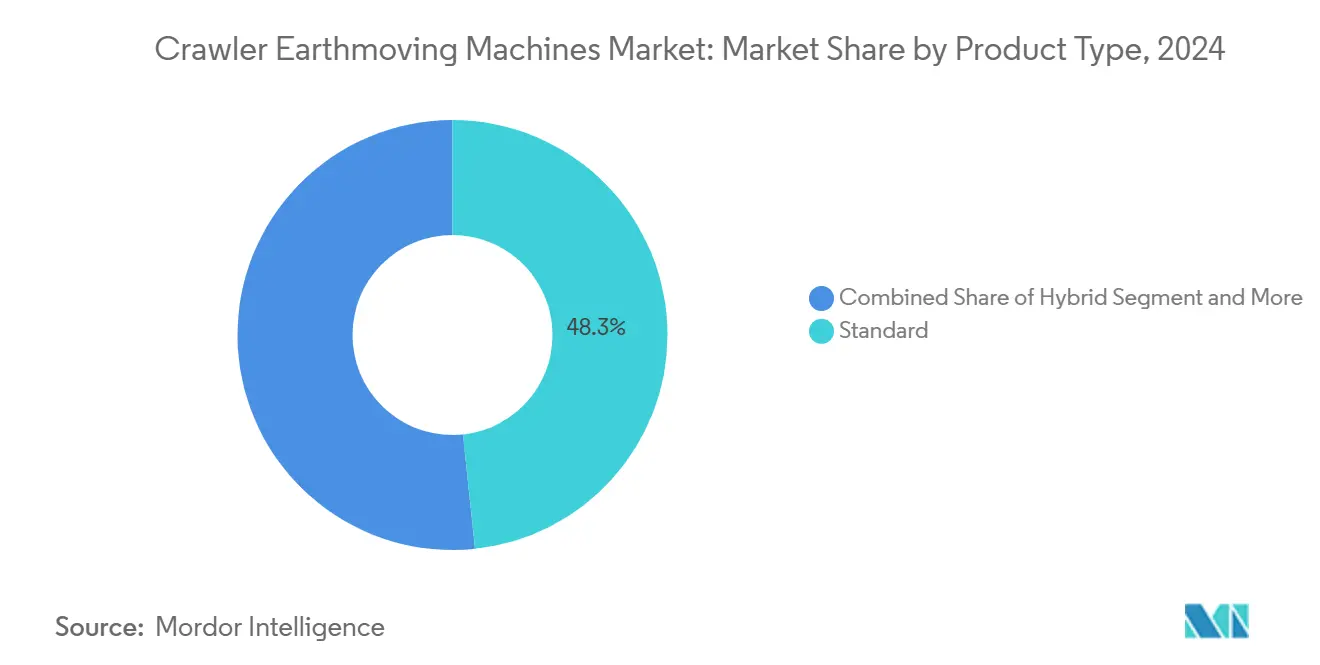

- By product type, standard crawler excavators held 48.33% of crawler earthmoving machines market share in 2024, while hybrid variants are projected to lead with a 10.76% CAGR through 2030.

- By bucket capacity, the 2 to 4 m³ segment captured 40.97% of the crawler earthmoving machines market size in 2024; units below 2.00 m³ are poised for the fastest 8.71% CAGR to 2030.

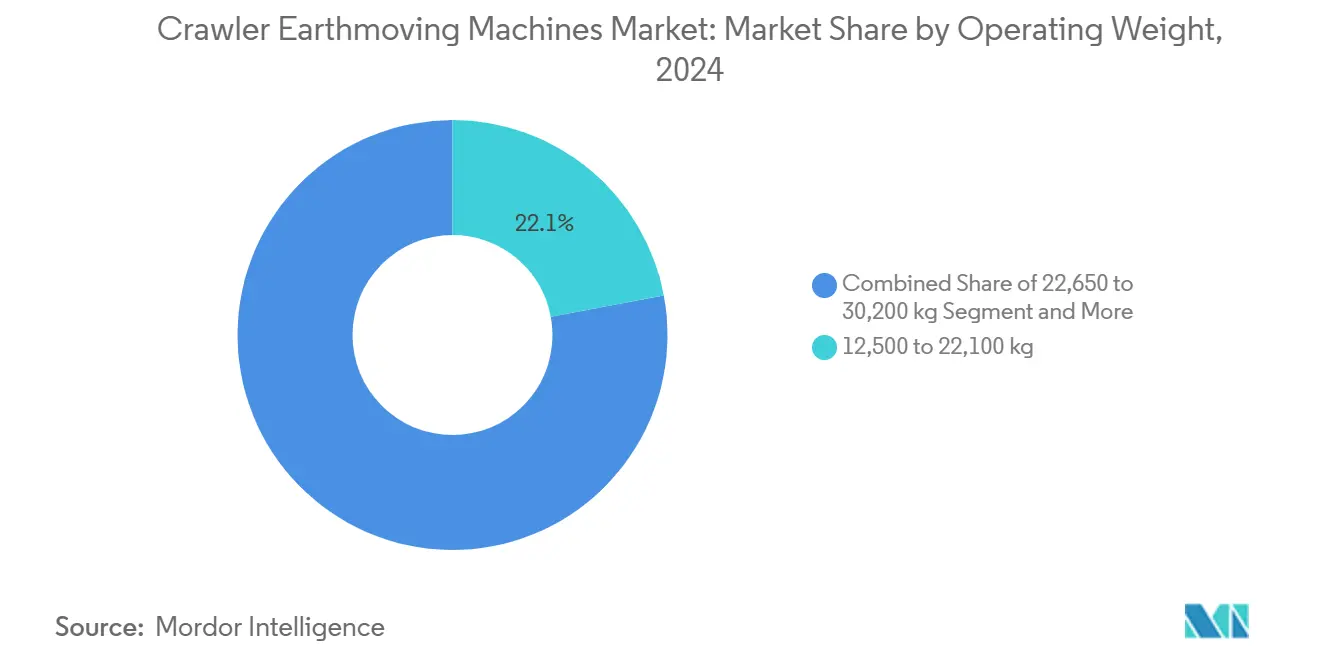

- By operating weight, machines in the 12,500-22,100 kg class accounted for 22.06% share of the crawler earthmoving machines market size in 2024 and are expanding at a 7.84% CAGR.

- By end-use vertical, construction retained 64.09% of the crawler earthmoving machines market size in 2024; mining applications are expected to grow at an 8.34% CAGR through 2030.

- By geography, Asia-Pacific commanded 42.03% of crawler earthmoving machines market share in 2024 and is advancing at a 6.85% CAGR to 2030.

Global Crawler Earthmoving Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewed Infrastructure Stimulus | +1.3% | North America, APAC core, spill-over to global supply chains | Medium term (2-4 years) |

| Rapid Electrification | +1.1% | Global, with early adoption in Europe and China | Long term (≥ 4 years) |

| OEM Telematics Bundles | +0.8% | Global, particularly North America and Europe | Short term (≤ 2 years) |

| Autonomous "Robot-Dig" | +0.6% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Green-Steel Undercarriage | +0.4% | Europe, North America, with gradual APAC adoption | Long term (≥ 4 years) |

| Critical-Minerals Open-Pit Surge | +0.2% | Global, concentrated in resource-rich regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renewed Infrastructure Stimulus in the U.S., India, and Indonesia

More than 56,000 projects funded by the United States Infrastructure Investment and Jobs Act are underway, fuelling a double-digit rise in public highway spending. Similar momentum in India and Indonesia keeps order books full, with contractors reporting minimal cancellations and rising equipment utilization. The current wave prioritizes resilient roads, decarbonized transit, and digital connectivity, thereby requiring higher-precision, technology-ready excavators. Stable multi-year funding horizons also shorten payback periods for hybrid and electric models, accelerating fleet renewal cycles within the crawler earthmoving machines market.[1]"FACT SHEET: Biden-Harris Administration Kicks Off Infrastructure Week by Highlighting Historic Results Spurred by President Biden’s Investing in America Agenda", The White House, bidenwhitehouse.archives.gov

Rapid Electrification of Above-15-T Machines

Battery-electric prototypes exceeding 20 t now match diesel duty cycles in urban projects while cutting operating costs by up to 60%. California’s Advanced Clean Equipment list already cites hundreds of compliant models, signalling regulatory tailwinds[2]“Advanced Clean Equipment,” California Air Resources Board, arb.ca.gov. Improved lithium-ion energy density and rapid-charging solutions reduce range anxiety, making electric heavy excavators viable on congested city sites with strict noise and emission limits. Global OEM roadmaps suggest every major brand will field multiple high-tonnage electric options before 2028, anchoring a new growth vector for the crawler earthmoving machines market.

OEM Telematics Bundles Lowering TCO

Modern excavators ship with factory-installed connectivity that combines geofencing, predictive maintenance, and automated performance reporting. Mixed-fleet standards allow contractors to view disparate brands on one dashboard, slashing administrative overhead. Service revenues linked to data-driven maintenance contracts already exceed product revenue growth, encouraging OEMs to monetize uptime guarantees. The model transforms one-off equipment sales into recurring service relationships, embedding long-term customer lock-in and lifting lifecycle profitability across the crawler earthmoving machines industry.

Autonomous “Robot-Dig” Retrofit Kits

Aftermarket sensor pods and AI modules convert legacy excavators into semi-autonomous diggers capable of trenching or grading without continuous operator input. Investors are pouring capital into these retrofit platforms, attracted by scalable business models that leverage the installed base of millions of machines. Contractors adopt autonomy to mitigate labour shortages, cut rework, and extend operating hours, reinforcing demand for compatible crawler earthmoving machines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight Credit For Loans | -0.8% | Global, particularly affecting small to mid-size contractors | Short term (≤ 2 years) |

| Raw-Material Volatility | -0.6% | Global, with supply chain concentration in China and Indonesia | Medium term (2-4 years) |

| Skilled-Operator Shortages | -0.5% | North America & EU, emerging in APAC urban centers | Long term (≥ 4 years) |

| Wage Inflation | -0.4% | Global, most acute in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight Credit for Construction Loans

Higher interest rates raise hurdle rates for contractors, delaying equipment purchases and shifting preference toward short-term rentals. Small firms feel the pinch most acutely, consolidating demand with larger, better-capitalised players. The financing bottleneck creates a secondary effect where equipment demand shifts toward rental rather than purchase, altering the fundamental demand dynamics in the crawler excavator market.

Lithium-Ion Raw-Material Volatility

Battery-grade lithium metal averaged USD 80,354.23 per metric ton in February 2025, underscoring price swings large enough to erase projected fuel savings on electric crawler excavators[3]"2025 Lithium Pricing Trends: How Emerging Markets Are Shaping Global Supply and Demand", SMM Information & Technology Co., Ltd., metal.com. With more than 70% of global refining capacity clustered in China and Indonesia, any logistical disruption or export curb sends immediate shock waves through cathode and cell producers, pushing costs straight into OEM bill-of-materials. Manufacturers now negotiate multi-year offtake agreements, invest in upstream joint ventures, or pilot sodium-ion chemistries to stabilize input costs, yet price-adjustment clauses in supply contracts still cascade into end-user quotations. Fleet buyers face unpredictable battery surcharges that complicate total-cost-of-ownership models and lengthen payback horizons, especially in rental fleets operating on tight margin thresholds. As a hedge, contractors prolong diesel fleet life or pivot to hybrid excavators until commodity markets cool, tempering near-term adoption of fully electric crawler earthmoving machines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Variants Gain Traction

Standard excavators dominated 2024 with a 48.33% crawler earthmoving machines market share, testament to their proven reliability and universal service support. Hybrid models, however, are climbing at a 10.76% CAGR, providing up to 20% fuel savings without charging downtime. Contractors view hybrids as a low-risk bridge toward full electrification, and OEM retrofit programs further ease adoption. Niche models such as short-tail and super-long-front variants serve tight urban sites and deep-reach demolition, respectively, rounding out diverse application needs.

Hybrid demand illustrates how incremental efficiency wins attract capital even before zero-emission mandates take full effect. Demonstrations of regenerative-swing technology on 20-t platforms confirm performance parity with diesel machines while lowering maintenance intervals. As battery prices fall, hybrids can capture an expanding share, reinforcing their strategic role inside the crawler earthmoving machines market.

By Bucket Capacity: Medium Segment Dominates Applications

Excavators with 2 to 4 m³ buckets accounted for 40.97% of the crawler earthmoving machines market size in 2024, matching mainstream roadbuilding, foundation, and utility tasks. Small-capacity models below 2.00 m³ are registering an 8.71% CAGR, propelled by urban utilities and landscaping where precision and maneuverability trump outright digging volume. Large-capacity machines over 4 m³ remain vital for mining and mega-infrastructure but face longer sales cycles tied to commodity prices.

The growth trajectory of small capacity machines reflects fundamental changes in construction project characteristics, with urban infill development and utility modernization creating demand for compact, maneuverable equipment. Further, the rise in compact electric models underscores the regulatory push for low-noise, zero-emission equipment in dense cities. Longer-arm attachments and quick-coupler systems further boost versatility, ensuring medium buckets retain primacy across mixed-project portfolios within the crawler earthmoving machines industry.

By Operating Weight: Light-Weight Class Leads Growth

Machines in the 12,500-22,100 kg class captured 22.06% of the crawler earthmoving machines market share in 2024 and are projected to expand at a 7.84% CAGR. They deliver optimal transportability, staying within standard trailer limits, while offering enough hydraulic power for most commercial jobs. Contractors favour the lighter class to juggle diverse projects without additional permitting costs, explaining its dual role as both the largest and fastest-growing slice of the crawler earthmoving machines market.

Heavier classes above 34,000 kg skew toward mining and large-scale earthworks, where site logistics can absorb specialised haulage. OEMs accordingly prioritise technological upgrades such as factory-fitted grade control on these models, ensuring high utilisation rates across rental and owner-operated fleets. Komatsu's PC9000 hydraulic mining excavator, representing the company's largest machine at 900-tonne class, demonstrates the end of the weight spectrum designed for efficiency with ultra-class haul trucks.

By End-Use Vertical: Mining Applications Accelerate

Construction retained a commanding 64.09% revenue share in 2024, buoyed by ongoing urbanisation and government stimulus. Mining, though smaller, is climbing at an 8.34% CAGR as the energy transition pushes demand for critical minerals. Procurement roadmaps from leading miners call for fleets of battery-electric or hydrogen-ready excavators to meet decarbonisation targets, fuelling specialised product launches.

The mining segment's acceleration reflects fundamental shifts in global resource demand, with the International Energy Agency projecting an investment rise from USD 45 billion in 2023 to USD 800 billion by 2040 in critical metals. The sector’s capex commitments translate into longer contract tenures and premium aftermarket parts sales, raising the strategic value of mining to OEM revenue mix. Autonomous truck-shovel pairings further strengthen synergies, embedding advanced crawler excavators at the heart of next-generation mine plans and reinforcing their contribution to the crawler earthmoving machines market size.

Geography Analysis

Asia-Pacific commanded 42.03% of the crawler earthmoving machines market share in 2024 and is forecast to grow at a 6.85% CAGR through 2030. China’s infrastructure modernisation and Indonesia’s multi-year capital-spending plans combine to keep utilisation rates high. Regional OEMs leverage short supply chains to offer competitive pricing and quick delivery, solidifying their home-market dominance while expanding export footprints.

North America remains a robust purchaser owing to the USD 1.2 trillion federal infrastructure package, which is now in the full execution phase with highways, bridges, and broadband corridors driving machine hours. The regulatory push for zero-emission construction equipment is most advanced on the West Coast, creating early-adopter niches for 20-t battery-electric excavators. Retrofit autonomy is also scaling quickly as contractors offset labour shortages and rising wages.

Europe, though mature, is transitioning from volume growth to value-added upgrades. Tender documents increasingly stipulate lifecycle carbon limits and digital-twin compatibility, favouring models with green-steel undercarriages and open API telematics. Incentives for low-noise, electric machinery in the Nordic countries enhance adoption rates ahead of broader EU mandates. Collective emphasis on sustainability and digitisation sustains premium pricing and differentiates European demand within the global crawler earthmoving machines market.

Mordor Intelligence provides coverage of the crawler earthmoving machines market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Indonesia, United States, Thailand, Philippines, Singapore, Australia, South Korea, and Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

The crawler earthmoving machines market remains moderately concentrated. Caterpillar leads followed by Komatsu and Hitachi Construction Machinery, yet a cohort of Chinese brands has risen rapidly on competitive pricing and robust domestic volumes. SANY’s ascent to global unit-sales leadership exemplifies this shift, backed by expanding overseas factories that shorten lead times.

Competition is pivoting from pure hardware metrics toward connected-service ecosystems. OEMs are bundling telematics subscriptions, predictive-maintenance contracts, and autonomous-ready interfaces at the point of sale, locking customers into proprietary data platforms. Strategic alliances with software specialists are common, as seen in recent 3D machine-control integrations that simplify operator workflows. The ability to harmonise digital and mechanical competencies is now a core differentiator in the crawler earthmoving machines industry.

Investment also targets emission-free powertrains. Komatsu’s PC9000, the firm’s largest hydraulic excavator, demonstrates readiness for full battery or hydrogen retrofit pathways while pairing with ultra-class haul trucks for mine duty. Similar flagship launches reinforce brand positioning and show how scale OEMs exploit R&D depth to stay ahead even as low-cost entrants expand share. Overall, the landscape balances price-based rivalry with innovation-led repositioning, keeping margins in check yet accelerating technology diffusion.

Crawler Earthmoving Machines Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Hitachi Construction Machinery

-

SANY Heavy Industry

-

Volvo Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Komatsu delivered its 900-t PC9000 hydraulic excavator to a Canadian oil-sand site, extending the ultra-class product family.

- March 2025: Bobcat unveiled 23-t and 25-t models featuring Tier-4 engines and four power modes for fuel efficiency.

- March 2025: Volvo Construction Equipment partnered with a control-technology firm to embed 3D machine guidance in its excavator line.

- March 2025: Caterpillar launched the Cat 395 front-shovel variant aimed at high-productivity mining and quarry applications.

Global Crawler Earthmoving Machines Market Report Scope

| Standard |

| Hybrid |

| Short Tail |

| Super Long Front |

| 0.3 to 2 m³ (Small) |

| 2 to 4 m³ (Medium) |

| Over 4 m³ (Large) |

| 12,500 to 22,100 kg |

| 22,650 to 30,200 kg |

| 34,300 to 45,750 kg |

| 51,000 to 70,650 kg |

| 78,500 to 93,300 kg |

| 95,900 kg and Above |

| Construction |

| Mining |

| Forestry and Agriculture |

| Other Industries |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Saudi Arabia | |

| Rest of Middle East and Africa |

| By Product Type | Standard | |

| Hybrid | ||

| Short Tail | ||

| Super Long Front | ||

| By Bucket Capacity | 0.3 to 2 m³ (Small) | |

| 2 to 4 m³ (Medium) | ||

| Over 4 m³ (Large) | ||

| By Operating Weight | 12,500 to 22,100 kg | |

| 22,650 to 30,200 kg | ||

| 34,300 to 45,750 kg | ||

| 51,000 to 70,650 kg | ||

| 78,500 to 93,300 kg | ||

| 95,900 kg and Above | ||

| By End-Use Vertical | Construction | |

| Mining | ||

| Forestry and Agriculture | ||

| Other Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Saudi Arabia | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the crawler earthmoving machines market today?

The crawler earthmoving machines market size reached USD 33.34 billion in 2025 and is forecast to climb to USD 43.41 billion by 2030.

What is the expected growth rate for crawler excavators over the next five years?

Aggregate demand is projected to rise at a 5.42% CAGR through the 2025-2030 period.

Which region will contribute most to future sales?

Asia-Pacific is set to remain the primary growth engine, expanding at a 6.85% CAGR on the back of sustained public-works spending and rapid urbanisation.

Are battery-electric excavators commercially viable for heavy-duty applications?

Yes. Models above 20 t now match diesel performance in urban projects while benefiting from lower energy and maintenance costs, especially in jurisdictions with zero-emission incentives.

What segment of machines is growing fastest by operating weight?

Units in the 12,500-22,100 kg class lead both market share at 22.06% and forecast growth at 7.84% CAGR, owing to their balance of power and transportability.

How are equipment makers differentiating their offerings?

OEMs increasingly bundle telematics, predictive maintenance, and autonomous-ready capabilities, shifting competition from pure hardware toward integrated service ecosystems.

Page last updated on: