Cord Blood Banking Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

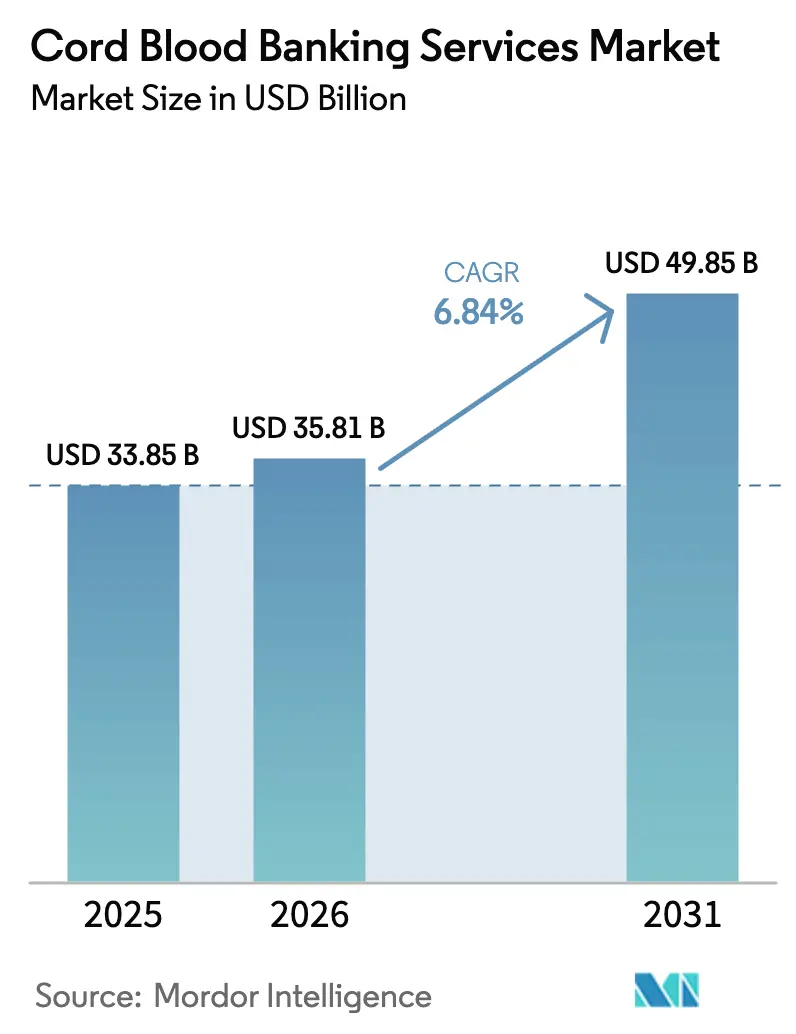

| Market Size (2026) | USD 35.81 Billion |

| Market Size (2031) | USD 49.85 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cord Blood Banking Services Market Analysis by Mordor Intelligence

The Cord Blood Banking Services Market size is expected to grow from USD 33.85 billion in 2025 to USD 35.81 billion in 2026 and is forecast to reach USD 49.85 billion by 2031 at 6.84% CAGR over 2026-2031.

Clinical validation, such as the FDA’s December 2025 approval of the ex-vivo expanded product Omisirge for severe aplastic anemia, is removing long-standing dose constraints and raising physician confidence in cord blood–based transplants.[1] U.S. Food and Drug Administration, “FDA Approves First Ex-Vivo Expanded Cord Blood Product for Severe Aplastic Anemia,” FDA.gov Parents are becoming more aware that private storage can serve as biological insurance against transplant-treatable diseases, a trend reinforced by obstetrician endorsement and targeted digital campaigns. Meanwhile, public banks are benefiting from new government funding that underwrites collection costs and broadens genetic diversity, making publicly donated units more accessible to transplant centers.[2]Health Resources and Services Administration, “National Cord Blood Inventory Contracts,” hrsa.gov Technology upgrades—automated closed-system processing, real-time cryogenic monitoring, and blockchain audit trails—are lowering contamination risk and aligning operations with AABB and FACT-NetCord standards. These combined forces are steering the cord blood banking services market toward steady, mid-single-digit annual expansion while encouraging new hybrid service models that blend public altruism with private optionality.

Key Report Takeaways

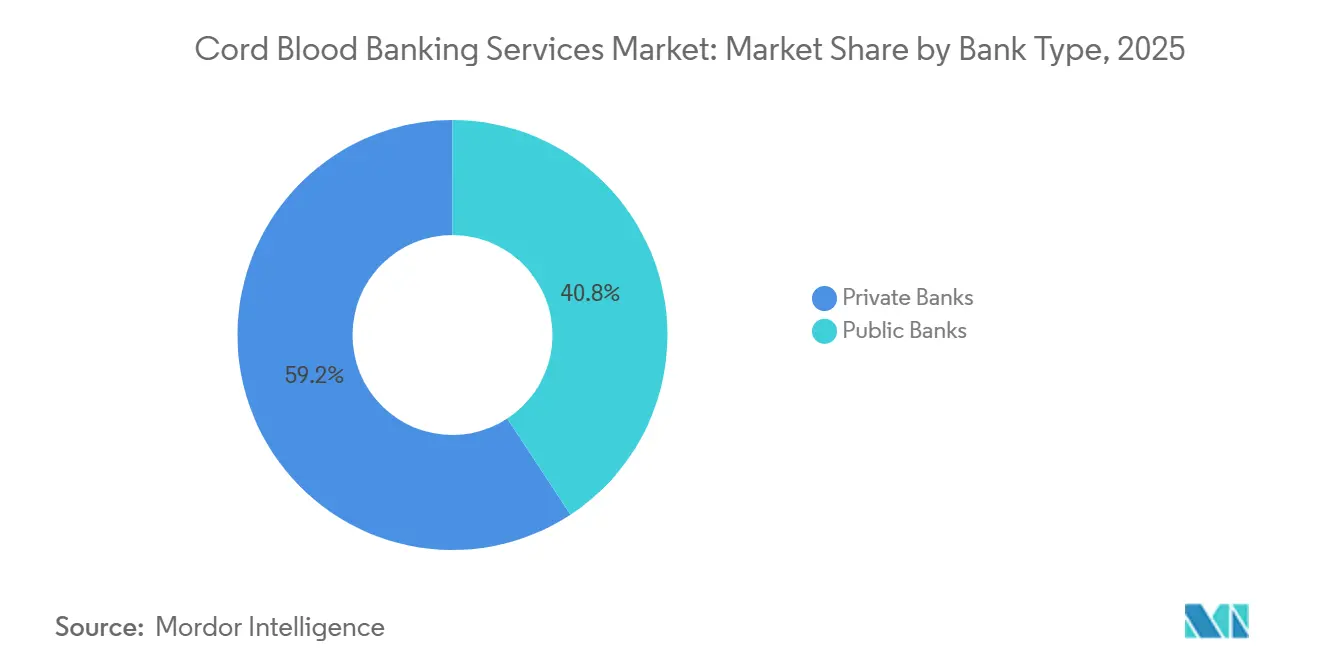

- By bank type, private operators held 59.24% of the cord blood banking services market share in 2025, while public banks are projected to post the highest growth at a 9.14% CAGR through 2031.

- By storage service, combined processing and storage accounted for 47.25% of the cord blood banking services market size in 2025, whereas processing-only contracts are forecast to expand at a 9.53% CAGR over 2026-2031.

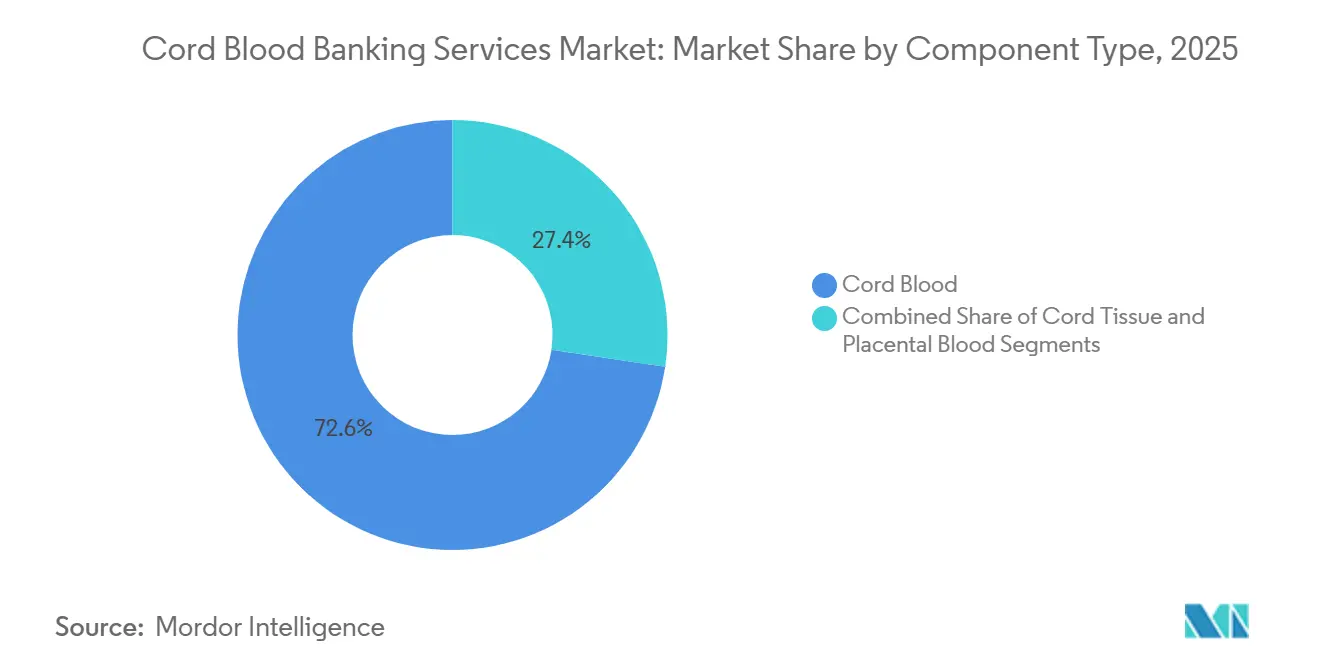

- By component, cord blood led with 72.64% cord blood banking services market share in 2025; cord tissue is set to rise fastest, advancing at a 10.43% CAGR to 2031.

- By application, cancers captured 37.67% of the cord blood banking services market size in 2025, while metabolic disorders are on track for the quickest growth at a 10.32% CAGR through 2031.

- By end user, hospitals and clinics commanded 43.74% cord blood banking services market share in 2025, with research institutes expected to grow at the highest 9.54% CAGR during 2026-2031.

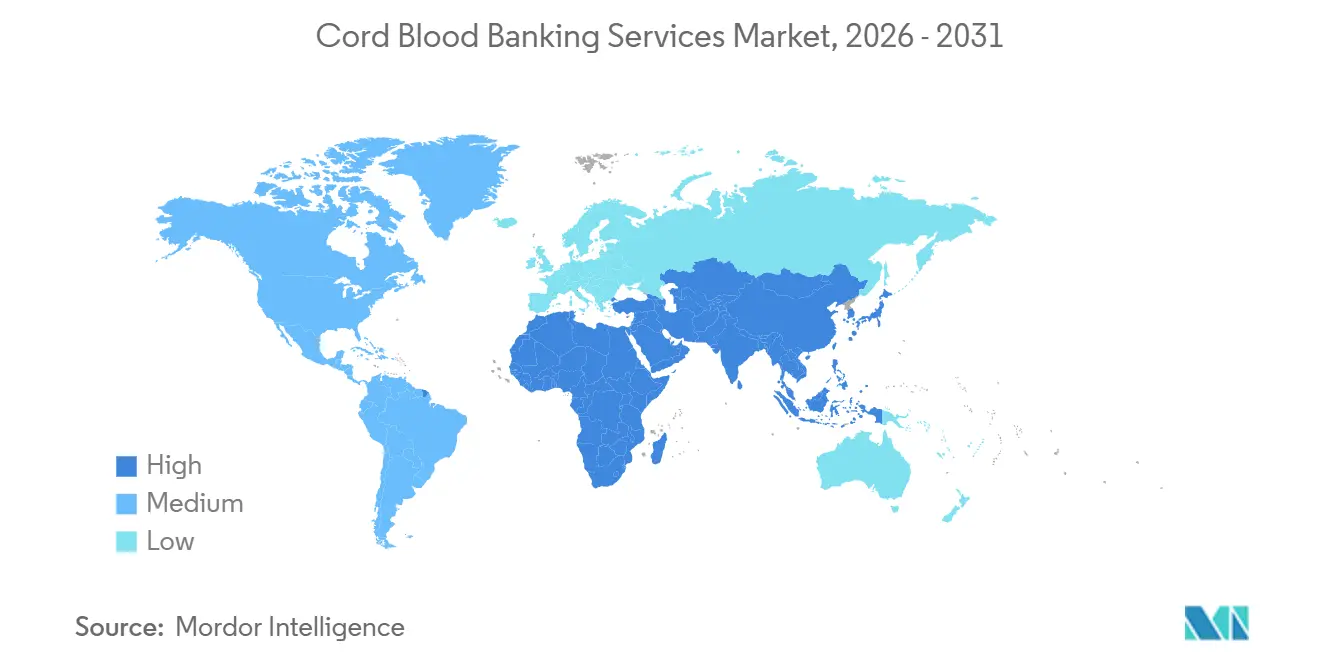

- By geography, North America led with 39.54% cord blood banking services market share in 2025, whereas Asia-Pacific is forecast to register the strongest regional expansion at an 8.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cord Blood Banking Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Incidence of Transplant-Treatable Diseases | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Rising Parental Awareness & Private Bank Uptake | +1.5% | Urban North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Government Funding for Public Banks | +0.9% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| Advances in Cryopreservation & Processing Tech | +1.1% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Ex-Vivo Stem-Cell Expansion Platforms | +1.3% | North America, Europe, Japan | Long term (≥ 4 years) |

| Hybrid Public-Private Cost-Sharing Models | +0.8% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Transplant-Treatable Diseases

Leukemias and inherited anemias continue to lift transplant demand, and cord blood fills critical gaps when matched adult donors are unavailable. Acute lymphoblastic and acute myeloid leukemia account for roughly 60% of pediatric cord blood grafts, while sickle cell disease and beta-thalassemia are accelerating fastest in high-carrier geographies.[3]AMERICAN SOCIETY OF HEMATOLOGY, “Cord Blood Transplantation for Hematologic Malignancies,” American Society of Hematology, hematology.org Expanded newborn screening is also pushing metabolic-disorder transplants earlier when outcomes are best, as five-year survival exceeds 80% for Hurler syndrome treated before nine month. Payers in several European states now reimburse private banking for families with proven genetic risk, reinforcing the medical value proposition.

Rising Parental Awareness & Private Bank Uptake

Parents in major cities increasingly recognize that banked units offer a low-probability but high-value safety net. Up-front fees of USD 1,400–2,300 plus annual storage of USD 125–300 remain palatable to affluent households, and partnerships such as Cord Blood Registry’s whole-exome sequencing bundle allow families to align storage with genetic insights. Autologous use rates stay below 1%, yet the perceived downside of not storing remains a potent motivator, keeping private demand resilient.

Government Funding for Public Banks

Public inventories depend on government grants that subsidize collection and maintain diverse tissue types. In 2024 the U.S. Health Resources and Services Administration awarded USD 16.5 million across five banks, securing a 150,000-unit inventory for unrelated transplant needs. Comparable programs in the EU and Japan link funding to transplant activity, ensuring stable quality yet exposing budgets to policy shifts.

Advances in Cryopreservation & Processing Tech

Automated closed systems now reclaim more cells and cut contamination risk compared with manual methods. New facilities feature redundant liquid-nitrogen supply and unit-level blockchain tracking, as shown by Cryo-Cell International’s 56,000-square-foot Durham site opened in 2024. Vitrification is also gaining ground for cord tissue, where mesenchymal cells respond poorly to slow-freeze methods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Private-Banking Costs | –0.7% | Emerging Asia-Pacific, Latin America | Short term (≤ 2 years) |

| Limited Approved Clinical Applications | –0.5% | Global | Medium term (2-4 years) |

| Regulatory Accreditation Gaps | –0.4% | Asia-Pacific (ex-Japan), Middle East, Latin America | Long term (≥ 4 years) |

| Competition From iPSC Sources | –0.6% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Private-Banking Costs

Prices exclude many households where annual income is below USD 10,000, especially in emerging markets facing currency swings that push fees even higher. Only a handful of insurers pay for storage, restricting penetration outside upper-income tiers.

Limited Approved Clinical Applications

Although about 80 disorders qualify for cord blood treatment, most private-bank marketing stresses potential regenerative uses, such as cerebral palsy, that lack Phase III proof. Consumer-protection bodies in Australia and Canada have warned against overstatement, forcing some firms to tone down advertising.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bank Type: Public Funding Spurs Faster Growth

Public institutions held 40.76% of the cord blood banking services market in 2025 and are set to grow 9.14% annually through 2031 as governments underwrite inventory diversity. Private players retain leadership due to entrenched brands and direct-to-consumer marketing, yet autologous usage below 1% continues to attract scrutiny and fosters new hybrid pricing that preserves consumer choice while enriching public stocks.

Private operators now layer genetic screening, tissue add-ons, and future access to ex-vivo expansion to justify premiums, aiming to limit cannibalization by hybrids. Public banks counter with broader HLA coverage and rising transplant success, positioning altruistic donation as both socially responsible and medically efficient.

By Storage Service: Processing-Only Contracts Accelerate

Hospitals increasingly choose processing-only deals to avoid the capital burden of maintaining large cryogenic vaults, giving this niche a projected 9.53% CAGR. Combined processing and storage still represents 47.25% of 2025 revenue and remains the staple for full-service private banks that promote custody continuity and tighter chain-of-identity.

Banks investing in mega-facilities benefit from lower per-unit costs, yet they must also manage courier times, as cell viability drops when more than 48 hours elapse between collection and freezing. Storage-only agreements, though minor, attract parents who wish to move previously banked units into higher-accredited vaults, often after an international relocation.

By Component Type: Cord Tissue Gains Momentum

Cord blood continues to anchor 72.64% of the cord blood banking services market size, supported by decades of transplant data and new expansion approvals that remove adult-dose issues. Cord tissue, rich in mesenchymal cells, is set to grow 10.43% a year thanks to promising trials in graft-versus-host disease and orthopedic repair. Private banks bundle tissue with blood to raise average revenue per enrolment and hedge therapeutic uncertainty.

Placental blood offers bigger cell doses but adds collection complexity and contamination risk, keeping its adoption moderate. As vitrification protocols improve, tissue banking costs are falling, closing the price gap with standard cord blood storage.

By Application: Metabolic Disorders Rise Fastest

Cancers held 37.67% of 2025 revenue, driven by leukemia and lymphoma transplants, yet metabolic disorders are sprinting ahead at a projected 10.32% CAGR. Early treatment of Hurler syndrome and Krabbe disease shows clear neurologic benefit, prompting broader newborn screening and quicker transplant referral.

Sickle cell disease and beta-thalassemia also expand solidly, aided by gene-editing programs that rely on banked stem cells. Experimental neurological uses remain in clinical limbo after mixed trial outcomes, tempering growth for the “Others” category.

By End User: Research Institutes Expand Inventory Needs

Hospitals and clinics perform most transplants and held 43.74% share in 2025, but research institutes will grow 9.54% annually as they test ex-vivo expansion, gene editing, and iPSC comparators. Each Phase II study can consume hundreds of units, providing public banks with a new revenue stream while sharpening demand for high-quality, protocol-grade material.

Specialty transplant centers retain mid-single-digit growth by adopting haploidentical approaches that rely on T-cell depletion. Home storage remains fringe because regulators warn against at-home dewars that lack validated temperature monitoring.

Geography Analysis

North America led with 39.54% share in 2025 on the strength of mature private banking, FDA-mandated quality controls, and National Cord Blood Inventory funding of USD 16.5 million that preserved 150,000 diverse units. Canada emphasizes units from Indigenous populations to close HLA gaps, while Mexican parents often store across the border to access U.S. oversight. Competition among Cord Blood Registry, ViaCord, and Cryo-Cell squeezes margins and encourages service bundling.

Asia-Pacific should post the fastest regional CAGR at 8.24%. China’s seven-license cap creates quasi-monopolies that drive premium pricing and medical tourism, with China Cord Blood Corporation reporting USD 180 million in 2024 revene. India’s LifeCell and StemCyte expand at 15% a year as middle-class awareness and obstetric endorsements climb. Japan maintains stringent quality through its centralized network, while Australia limits operators to three through Therapeutic Goods Administration licensing.

Europe held roughly one-quarter of 2025 revenue. Robust public networks in the United Kingdom and Germany use performance-based funding to focus on transplant success, while private banking remains below 5% penetration due to cultural preference for public donation. Conditional EMA approval of Zemcelpro places the region at the forefront of expanded cord blood therapies. In the Middle East, Abu Dhabi Biobank’s 100,000-unit vault positions the UAE as a cross-border storage hub, whereas Latin America contends with uneven accreditation; Brazil’s ANVISA imposes GMP rigor, but neighboring countries lag, prompting families to store across borders for better assurance.

Competitive Landscape

The largest companies in the market includes Cord Blood Registry, China Cord Blood Corporation, ViaCord, Cryo-Cell International, and Cordlife, indicating moderate concentration. China Cord Blood leverages limited licenses to maintain regional dominance, while Cryo-Cell pursues scale economies through its automated Durham facility that holds 500,000 units. Cord Blood Registry differentiates through added genetic services and research ties that integrate its inventory into precision-medicine pipelines.

Regional entrants focus on Southeast Asia, the Middle East, and Latin America, where regulatory pathways remain fragmented yet demand is climbing. Hybrid public-private pricing, ex-vivo expansion partnerships, and bundled tissue offerings are the primary levers for newcomers. Switching costs are low once units are banked, yet reputational trust and accreditation status erect meaningful barriers.

Cord Blood Banking Services Industry Leaders

Cord Blood Registry (CBR) |

China Cord Blood Corporation

Cryo-Cell International

FamiCord Group

Revvity

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The Cord Blood Council launched to supply shared resources to FDA-licensed public banks supported by the National Cord Blood Inventory.

- November 2025: StemCyte introduced an insurance-linked public bank matching service in Taiwan with Taishin Life, combining transplant protection with life-cover benefits.

- July 2025: Cryoviva partnered with Life Keep Philippines to build a new storage facility near Manila, expanding service reach across Southeast Asia.

Global Cord Blood Banking Services Market Report Scope

Cord blood banking services refer to the collection, processing, testing, and storage of stem cells from the umbilical cord and placenta at sub-zero temperatures (-196°C) for potential use in treating diseases like cancers, immune deficiencies, and genetic disorders.

The Cord Blood Banking Services Market Report is segmented by Bank Type, Storage Service, Component Type, Application, End User, and Geography. By Bank Type, the market is segmented into Public and Private banks. By Storage Service, the market is segmented into Processing-only, Storage-only, and Combined Processing & Storage services. By Component Type, the market is segmented into Cord Blood, Cord Tissue, and Placental Blood. By Application, the market is segmented into Cancers, Blood Disorders, Metabolic Disorders, and Others. By End User, the market is segmented into Hospitals & Clinics, Specialty Transplant Centers, Research Institutes, and Home Storage Users. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Public |

| Private |

| Processing-only |

| Storage-only |

| Combined Processing & Storage |

| Cord Blood |

| Cord Tissue |

| Placental Blood |

| Cancers |

| Blood Disorders |

| Metabolic Disorders |

| Others |

| Hospitals & Clinics |

| Specialty Transplant Centers |

| Research Institutes |

| Home Storage Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Bank Type | Public | |

| Private | ||

| By Storage Service | Processing-only | |

| Storage-only | ||

| Combined Processing & Storage | ||

| By Component Type | Cord Blood | |

| Cord Tissue | ||

| Placental Blood | ||

| By Application | Cancers | |

| Blood Disorders | ||

| Metabolic Disorders | ||

| Others | ||

| By End User | Hospitals & Clinics | |

| Specialty Transplant Centers | ||

| Research Institutes | ||

| Home Storage Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is expected for the cord blood banking services market through 2031?

The market is projected to grow at 6.84% annually from 2026 to 2031.

Why are public cord blood banks expanding faster than private banks?

Government grants that cover collection expenses and build genetically diverse inventories are driving a 9.14% CAGR for public banks.

Which component type is growing fastest?

Cord tissue is forecast to expand at 10.43% a year due to rising interest in mesenchymal stem-cell therapies.

How does Omisirge affect adult transplantation?

Omisirge’s ex-vivo expansion overcomes historical cell-dose limits, cutting neutrophil-engraftment time by about half.

What factors limit wider private-bank adoption?

High up-front and annual storage fees, along with a limited set of FDA-approved uses, constrain take-up among middle-income families.

Page last updated on: