Cardiac Safety Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

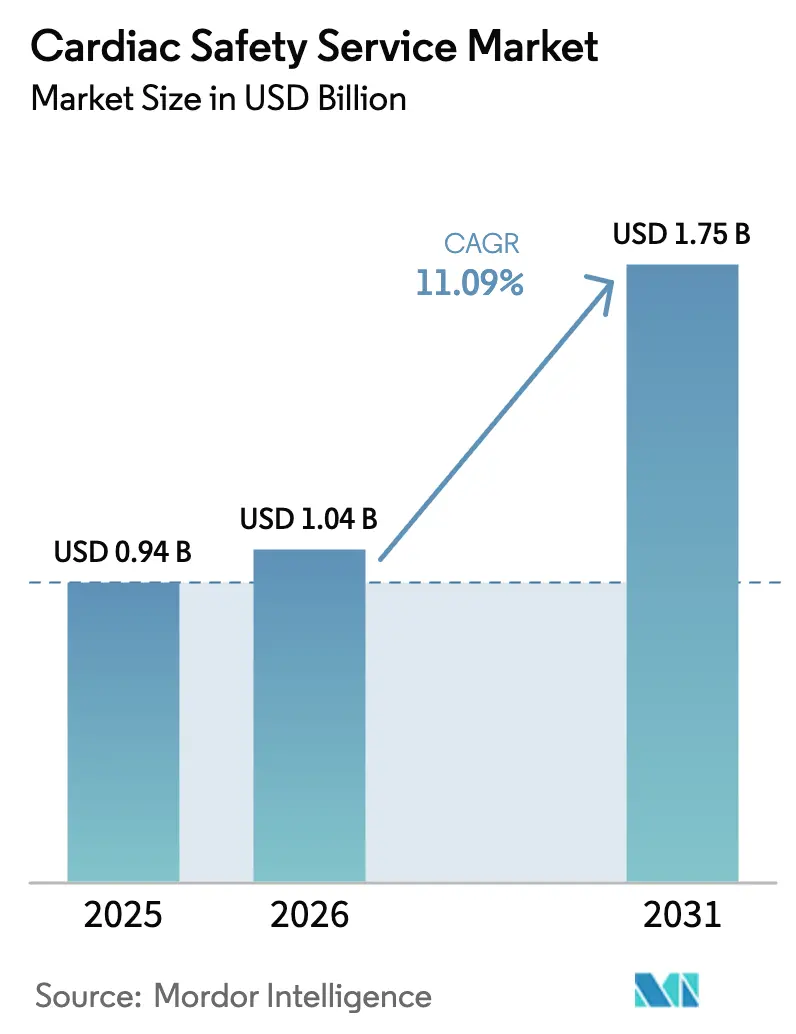

| Market Size (2026) | USD 1.04 Billion |

| Market Size (2031) | USD 1.75 Billion |

| Growth Rate (2026 - 2031) | 11.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiac Safety Service Market Analysis by Mordor Intelligence

The Cardiac Safety Service Market size is projected to expand from USD 0.94 billion in 2025 and USD 1.04 billion in 2026 to USD 1.75 billion by 2031, registering a CAGR of 11.09% between 2026 to 2031.

Stricter ICH E14/S7B mandates now compel real-time proarrhythmia screening in every first-in-human dose group, while decentralized and hybrid trial designs accelerate adoption of cloud ECG telemetry across oncology, rare-disease, and gene-therapy pipelines.[1]European Medicines Agency, “Clinical Trials Regulation Drives Cloud ECG Adoption,” EMA.europa.eu Investment in AI-enabled analytics shortens the interval from ECG capture to dose-escalation decisions, cutting early-phase timelines by up to 15%. Sponsors also face a rising burden of cardiovascular adverse events linked to tyrosine-kinase inhibitors and immune checkpoint therapies, expanding service demand beyond small-molecule programs.[2]Robert L. McNamara et al., “Cardiovascular Adverse Events in Cancer Trials,” ASCOPubs.org Outsourced cardiac safety providers continue to dominate multicountry pivotal studies, yet large pharmaceutical companies are internalizing analytics platforms to protect proprietary ECG datasets and mitigate GDPR, PIPL, and DPDP compliance risk.

Key Report Takeaways

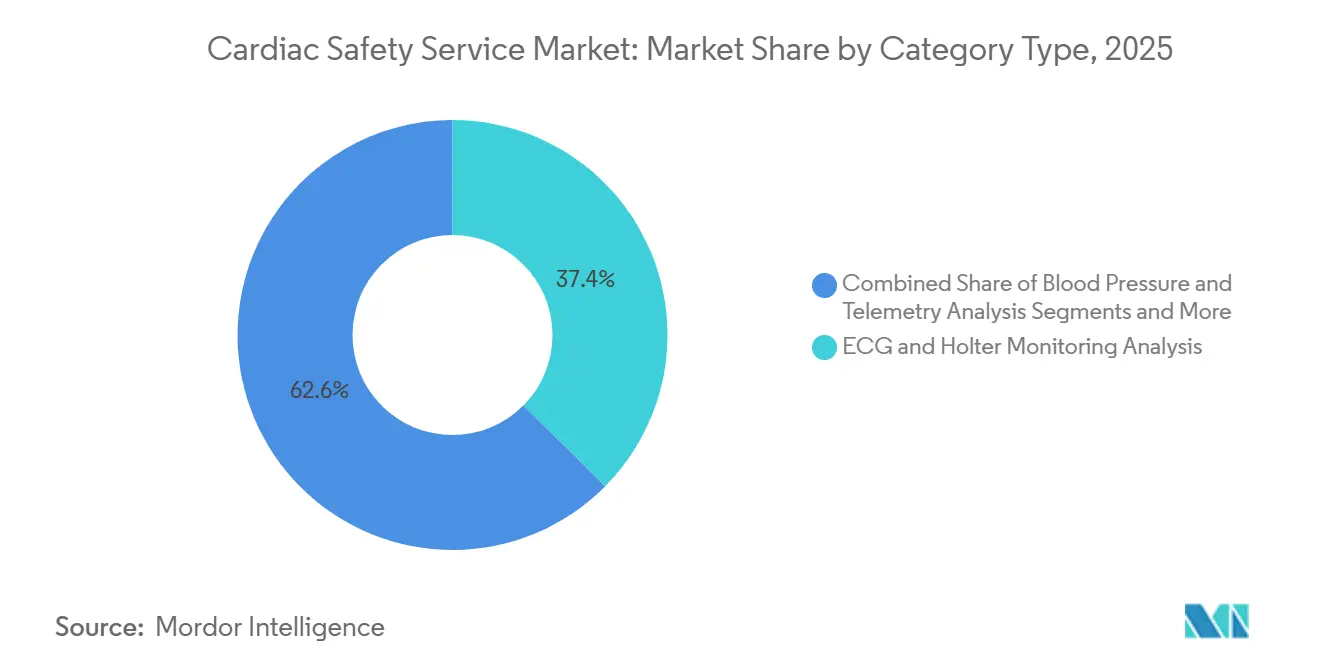

- By service type, ECG & Holter monitoring analysis led with 37.42% of the cardiac safety service market share in 2025, whereas real-time data analytics & reporting is advancing at a 14.24% CAGR through 2031.

- By service delivery model, outsourced vendors captured 72.53% revenue share in 2025, while in-house operations are projected to grow at 12.52% over 2026-2031.

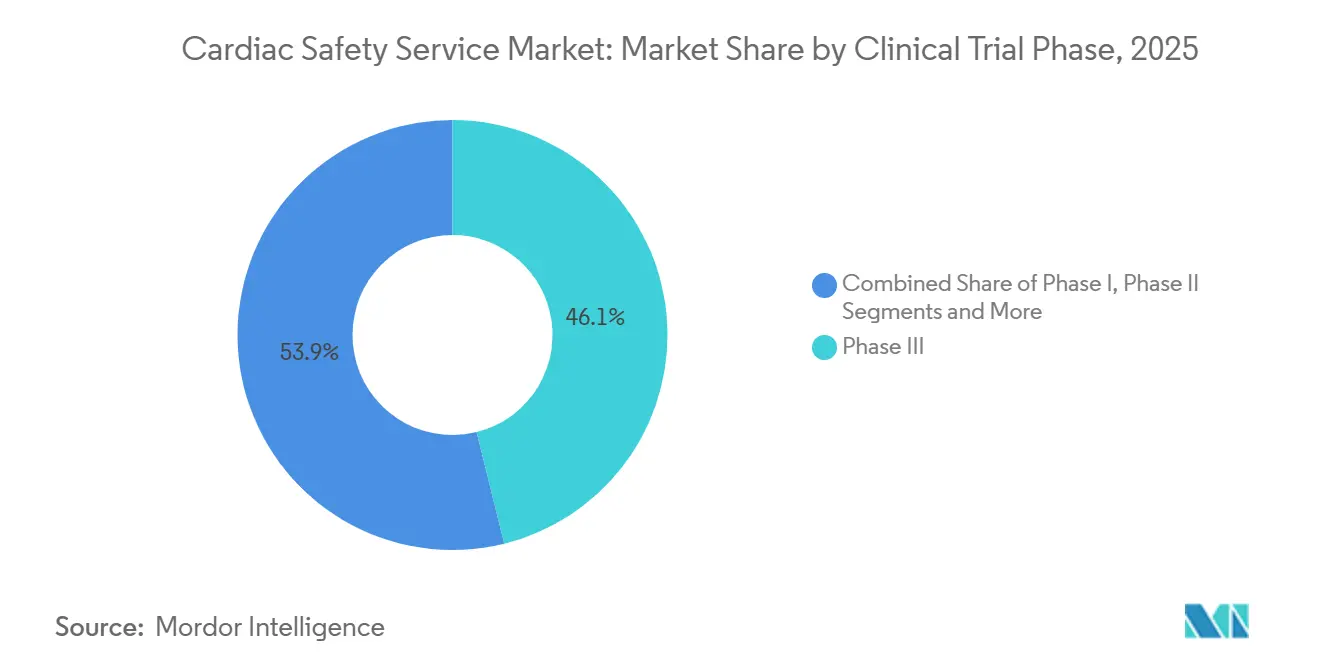

- By clinical trial phase, Phase III trials accounted for 46.13% of the cardiac safety service market size in 2025, yet Phase I services are expanding at a 12.84% CAGR to 2031.

- By end user, pharmaceutical companies held 56.22% share of the cardiac safety service market size in 2025, whereas biotechnology firms post the fastest 13.04% CAGR through 2031.

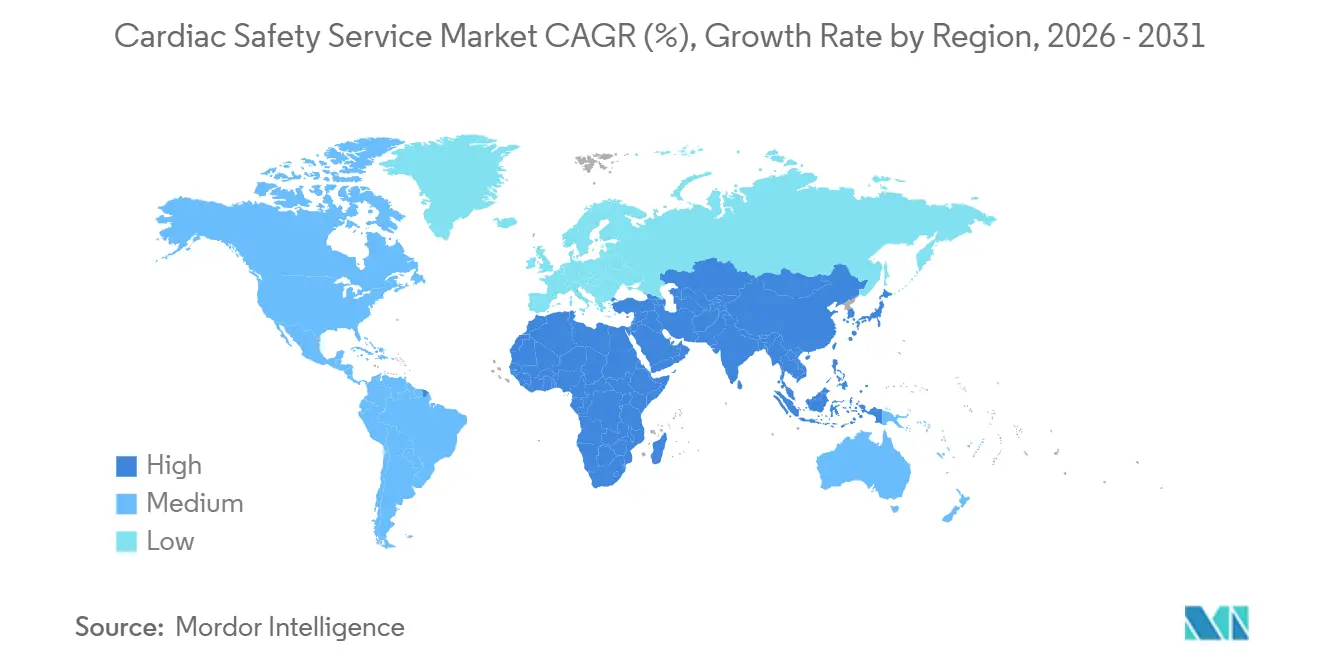

- By geography, North America dominated with 39.14% revenue share in 2025; Asia-Pacific is forecast to post a 13.63% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiac Safety Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Adoption of Decentralized & Hybrid Trials | +2.1% | North America, Western Europe, emerging uptake global | Medium term (2-4 years) |

| Rising Incidence of Cardiovascular Adverse Events in Oncology Trials | +1.8% | North America and Europe core | Short term (≤ 2 years) |

| Stricter ICH E14/S7B 2022 Addendum Implementation | +1.5% | Global, led by FDA and EMA | Short term (≤ 2 years) |

| Growth of Real-Time Cloud-ECG Analytics Platforms | +1.9% | North America, Europe, spill-over to APAC | Medium term (2-4 years) |

| AI-Enabled Arrhythmia Prediction Reducing Late-Stage Failures | +1.6% | Global early adopters | Medium term (2-4 years) |

| Integration of In-Silico Proarrhythmia Models into Safety Workflows | +1.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Adoption of Decentralized & Hybrid Trials

Decentralized cardiac safety workflows grew from 12% of cardiovascular studies in 2023 to 28% in 2025.[3]IQVIA Institute for Human Data Science, “Decentralized Trial Adoption Accelerates Cardiac Safety Monitoring,” IQVIA.com Remote Holter patches transmit encrypted ECG streams to cloud servers that flag QTc drift within hours, satisfying the FDA’s 2024 digital-health guidance. Hybrid approaches blend at-home telemetry with site-based echocardiography, lowering patient travel costs by 40% while preserving imaging rigor. Vendors such as Clario fielded 15,000 wearable devices across oncology protocols in 2025, using machine-learning algorithms to escalate arrhythmia alerts automatically. Centralized over-reads mitigate regional cardiologist shortages, enabling multicountry enrollment without sacrificing data quality.

Rising Incidence of Cardiovascular Adverse Events in Oncology Trials

Cardiovascular toxicities ranked second among serious adverse events in cancer trials during 2024. Tyrosine-kinase inhibitors and immune checkpoint agents prolong QT or provoke myocarditis, prompting FDA safety communications that now require intensified ECG surveillance in early-phase oncology protocols. Updated 2025 European Society of Cardiology guidelines recommend pairing ECG monitoring with biomarkers and imaging, raising per-patient costs by 35% but cutting late-stage attrition. Real-time telemetry detects silent arrhythmias during dose escalation cohorts, a differentiator cited by Charles River in recent oncology contract wins. The resulting demand surge broadens the cardiac safety service market beyond traditional small-molecule programs.

Stricter ICH E14/S7B 2022 Addendum Implementation

The addendum allows sponsors to replace stand-alone thorough-QT studies with exposure-response modeling, provided assay sensitivity is demonstrated. FDA and EMA guidance in 2023 made this pathway mainstream, yet only 38% of 2024 Phase I trials leveraged it, reflecting lingering uncertainty. Certara reported a 42% jump in cardiac-modeling consulting revenue during 2025 as sponsors sought expertise in concentration-QTc statistics. Clinical holds for inadequate cardiac monitoring rose to 17 in 2024, underscoring regulatory pressure to pre-specify QTc plans. CiPA-aligned in-silico assays now complement early modeling, trimming animal studies and expediting IND submissions.

Growth of Real-Time Cloud-ECG Analytics Platforms

Cloud ECG hubs supported more than 400 trials in 2025, up from 120 in 2023. Automated QTc algorithms cut over-read time from 48 hours to under 6 hours, enabling same-day dose decisions and shrinking Phase I cycle times by 15%. Platforms trained on two million annotated waveforms detect subtle T-wave changes, boosting early arrhythmia detection rates. IEEE 11073 standards updated in 2024 improved data interoperability, though legacy Holter systems still require middleware bridges. EMA’s 2025 qualification opinion on algorithmic QTc tools signaled growing regulator confidence in AI-assisted endpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Global Harmonization of QT/QTc Assessment Standards | -0.8% | APAC and Latin America most affected | Medium term (2-4 years) |

| High Capital Cost for 12-Lead Telemetry Infrastructure | -0.6% | Global, acute for small CROs and emerging-market sites | Short term (≤2 years) |

| Data-Privacy Restrictions on Cross-Border ECG Transfer | -0.7% | Europe, China, India with spill-over to multinationals | Medium term (2-4 years) |

| Scarcity of Certified Cardiac Safety Cardiologists in Emerging Markets | -0.9% | APAC (ex-Japan), Latin America, Middle East & Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Limited Global Harmonization of QT/QTc Assessment Standards

Regional regulators apply different QTc correction formulas and risk thresholds, forcing sponsors to run duplicate analyses that can delay approvals by up to three months. China still favors Bazett correction while the FDA and EMA prefer Fridericia, and Japan demands ethnic-sensitivity studies in Japanese volunteers, adding USD 1.5-2 million per program. Divergent cut-off values—480 ms in some jurisdictions versus 500 ms elsewhere—create uncertainty for data-safety boards and complicate dose-escalation decisions. The ICH working group began drafting unified correction guidance in 2025, yet final text is unlikely before 2028. Until then the cardiac safety service market will continue to bear redundant statistical costs that erode trial budgets and elongate timelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and complexity of comprehensive cardiac safety studies | −1.4% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Shortage of skilled electrophysiologists for data interpretation | −1.1% | Global, acute in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Limited validation of wearables for regulatory-grade cardiac endpoints | −0.9% | Global, regulatory lag in emerging markets | Short term (≤ 2 years) |

| Data-privacy hurdles in cloud ECG telemetry across borders | −0.7% | EU and Asia-Pacific cross-border studies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost & Complexity of Comprehensive Cardiac Safety Studies

Building a real-time core laboratory requires FDA-cleared hardware, compliant cloud storage, and redundant connectivity, with start-up spend ranging from USD 500,000 to USD 3 million depending on trial scale. Smaller contract research organizations cannot amortize these investments across many studies, so they cede share to large vendors and drive consolidation within the cardiac safety service market. Emerging-market sites face unreliable internet, making batch uploads the default and extending Phase II timelines by up to six weeks. Wearable Holter patches lower site hardware spend, yet device, training, and support still cost USD 800-1,200 per patient. Without reimbursement pathways, biotechnology sponsors shoulder the cost, limiting uptake despite proven efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Real-Time Analytics Outpace Traditional Monitoring

The real-time data analytics and reporting segment grew to 14.24% CAGR, the fastest within the cardiac safety service market, as sponsors now expect same-day arrhythmia alerts for dose-escalation decisions. ECG and Holter monitoring maintained a 37.42% revenue lead in 2025 because 12-lead Holters remain mandatory in pivotal protocols. Thorough-QT study services contributed about 22% but lag due to the E14/S7B addendum that lets exposure-response modeling replace dedicated crossover trials. Blood-pressure telemetry posted 10.8% growth as oncology programs pair hemodynamic data with ECG to profile VEGF inhibitor risk. Cardiovascular imaging accounted for roughly 15% and climbs steadily because cardio-oncology guidelines call for serial left-ventricular ejection fraction checks.

Sponsors view real-time analytics as central to adaptive trial designs that modify dosing on the fly, something retrospective batches cannot support. Clario reports its machine-learning triage trims cardiologist review time 35%, underscoring why the cardiac safety service market favors algorithm-enabled workflows. Crossover thorough-QT remains vital for compounds with unknown ion-channel profiles, yet its USD 1.2 million price tag pushes many biotechnology firms toward integrated Phase I monitoring instead. Hybrid devices now combine blood-pressure cuffs and ECG patches in one transmitter, cutting procurement spend 20% and easing subject compliance. Imaging growth is tempered by the site-visit requirement, but the FDA’s cardio-oncology draft in 2024 guarantees baseline and on-treatment scans for high-risk drugs, sustaining volume within the cardiac safety service market

By Service Delivery Model: In-House Capabilities Gain Ground

Outsourced providers controlled 72.53% revenue in 2025, yet in-house units are set to expand 12.52% over 2026-2031 as large pharmaceutical companies install subscription software behind their firewalls. Internalization protects raw ECG files, eases GDPR and PIPL compliance, and lowers unit costs across long portfolios, fueling a shift within the cardiac safety service market. Eli Lilly’s internal core lab now processes data from 20 concurrent studies and saves USD 8 million annually, a model other multinationals will likely mirror.

Outsourcing remains dominant for small biotechnology firms that lack cardiology staff or capital to buy hardware. Multicountry Phase III trials depend on vendors with 24-hour multilingual support, a scale only the largest contract research organizations provide. Smaller CROs form alliances to stay relevant; PSI and Richmond Pharmacology teamed up in 2025 to share cardiologist networks and broaden reach. Regulators scrutinize sponsor-run labs closely: twelve FDA inspection findings in 2024 cited inadequate QC, reminding smaller companies why outsourced oversight still matters. Hybrid models blending sponsor data capture with independent over-reads may become the norm as the cardiac safety service market balances cost, speed, and compliance.

By Clinical Trial Phase: Early-Phase Spend Accelerates

Phase I services are forecast to rise at 12.84% CAGR as regulators insist on comprehensive QT screens at first-in-human dosing, redirecting spend upstream in the cardiac safety service market. Phase III held 46.13% of 2025 revenue but grows a slower 10.2% because exposure-response models satisfy many QT requirements before pivotal enrollment. Phase II captures adaptive protocol demand where sponsors refine dose and explore exposure-safety curves, while Phase IV sees double-digit growth from wearable post-marketing surveillance.

Biotechnology firms integrate intensive ECG telemetry into Phase I dose-escalation cohorts, bypassing standalone crossover studies and trimming four to six months off timelines. The shift requires 24-hour cardiologist access and feeds demand for AI triage that filters normal tracings automatically. Phase III still commands the largest budgets because enrollment numbers drive monitoring volume, although its share of the cardiac safety service market is set to decline as earlier phases shoulder more safety analytics. Real-world wearables in Phase IV flag unanticipated QT prolongations, demonstrated when IQVIA monitoring identified alerts in 3.2% of patients on a new oncology agent, leading to a labeling update in 2025.

By End User: Biotechnology Drives Outsourced Demand

Pharmaceutical companies generated 56.22% of 2025 revenue, yet biotechnology firms will post 13.04% CAGR through 2031 and thus reshape the cardiac safety service market. Venture-backed oncology and gene-therapy developers lack cardiology infrastructure and outsource 95% of assessments to specialist providers. Medical device manufacturers contribute an 8% slice, driven by ISO 14155 demands on implantable stimulators, and contract research organizations procure the remaining share while negotiating bulk discounts.

Large pharmas internalize AI platforms; Pfizer expanded its cardiology staff 30% in 2025 to retain proprietary datasets and shorten decision cycles. Smaller biotech firms prefer turnkey packages that bundle wearable device logistics, cloud analytics, and independent cardiologist reads. Their funding surged to USD 42 billion in 2025, guaranteeing a healthy project pipeline for service vendors. CROs respond with integrated cardiac offerings; Parexel now markets combined ECG, imaging, and blood-pressure telemetry suites, mirroring sponsor appetite for single-vendor simplicity. As capital remains plentiful, biotechnology clients will keep shaping pricing power and innovation cycles within the cardiac safety service market.

Geography Analysis

North America commanded 39.14% of 2025 revenue because FDA enforcement of the E14/S7B addendum anchors first-in-human activity, yet its growth moderates to 10.45% as sponsors diversify early-phase work into cost-efficient regions. Europe after adoption of Regulation (EU) 536/2014 streamlined cross-border ECG exchange, though GDPR amendments extend start-up paperwork and temper its expansion.EU. Asia-Pacific is the fastest mover, projected at 13.63% CAGR, propelled by China’s 2024 cardiac safety guidance that aligns with Fridericia correction and India’s investment in ISO 13485 core labs.

Middle East and Africa will grow as Gulf Cooperation Council nations invest USD 500 million in compliant research centers, aiming to diversify beyond oil. South America held 8% and expands 11.7% after Brazil’s regulator aligned QT rules with ICH standards, while Argentina’s economic stabilization revives Buenos Aires as a trial hub. Data-sovereignty laws in Europe, China, and India fragment telemetry workflows, forcing redundant infrastructure that raises per-patient costs and redistributes spend within the cardiac safety service market.

Asia-Pacific’s large treatment-naive population lets Phase II and III trials finish six to nine months faster than in Western regions, a benefit WuXi Clinical highlights to multinational sponsors. North America remains the regulatory bellwether; FDA draft guidance on AI biomarkers issued in 2024 has shaped global adoption curves, keeping many pilot studies domestic despite cost concerns. European share is influenced by Brexit fragmentation that forces dual submissions to EMA and the UK regulator, adding administrative load and tilting some Phase I volumes toward the Netherlands and Belgium. Sub-Saharan Africa’s potential is constrained by bandwidth and cardiologist shortages, yet tele-reading partnerships with European labs gradually open new recruitment corridors.

Competitive Landscape

The cardiac safety service market shows moderate concentration. Leaders chase vertical integration, acquiring wearable device makers and cloud analytics firms to offer devices, data collection, AI triage, and cardiologist over-reads in one contract. Certara’s CiPA in-silico models won 18 new contracts in 2025 by letting sponsors predict torsades risk preclinically, cutting IND timelines by months.

Technology patents accelerate competition; the USPTO granted 47 AI-ECG patents during 2024-2025, signaling rapid innovation cycles. Vendors active in IEEE and CDISC standards bodies gain early insight into regulatory requirements and tailor product roadmaps accordingly. Niche firms differentiate through therapeutic focus; Ncardia specializes in cardio-oncology, combining stem-cell assays with imaging protocols that large generalists have yet to match.

Strategic moves include Labcorp’s 2025 purchase of a telemetry middleware company to solve legacy device interoperability, and ICON’s partnership with a cloud cybersecurity vendor to harden ECG data pipelines against GDPR fines. Heartstream’s 2026 spin-out of Philips Emergency Care expands AED and monitor manufacturing, giving the group standing inventory it can bundle with trial services. Emerging alliances such as Frontage-Banook pair telemedicine platforms with core labs to address hybrid decentralized protocols. Competitive intensity will rise as AI tools commoditize baseline ECG reads, shifting value to predictive analytics, regulatory consulting, and integrated device logistics within the cardiac safety service market.

Cardiac Safety Service Industry Leaders

Clario

IQVIA

Labcorp Drug Development

ICON plc

Medpace

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: CardioOne launched CardioOne Connect, a cloud platform that joins ambulatory diagnostics, chronic-care management, and remote monitoring into one EMR-integrated ecosystem.

- January 2026: Heartstream began operations as an independent emergency-care company after acquiring Philips Emergency Care, retaining AED and monitor production under a multi-year brand license.

- June 2025: Alphaiota and Powerful Medical expanded their partnership to roll out PMcardio, the first AI-powered heart-attack diagnostic, across Saudi Arabia.

Global Cardiac Safety Service Market Report Scope

Cardiac safety services are clinical, medical, and technical solutions designed to monitor and assess the cardiovascular effects of drugs, devices, or therapies during clinical trials (Phase I-IV) while ensuring compliance with regulatory standards.

The Cardiac Safety Service Market Report is segmented by Service Type, Service Delivery Model, Clinical Trial Phase, End User, and Geography. By Service Type, the market is segmented into Thorough QT/QTc Study Services, ECG & Holter Monitoring Analysis, Blood Pressure & Telemetry Analysis, Cardiovascular Imaging, and Real-Time Data Analytics & Reporting. By Service Delivery Model, the market is segmented into In-house and Outsourced services. By Clinical Trial Phase, the market is segmented into Phase I, Phase II, Phase III, and Phase IV. By End User, the market is segmented into Pharmaceutical Companies, Biotechnology Firms, Medical Device Manufacturers, and CROs. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Thorough QT/QTc Study Services |

| ECG & Holter Monitoring Analysis |

| Blood Pressure & Telemetry Analysis |

| Cardiovascular Imaging (Echocardiography, MUGA) |

| Real-Time Data Analytics & Reporting |

| In-house (Sponsor-run) |

| Outsourced (CRO & Specialist Vendors) |

| Phase I |

| Phase II |

| Phase III |

| Phase IV / Post-marketing |

| Pharmaceutical Companies |

| Biotechnology Firms |

| Medical Device Manufacturers |

| Contract Research Organisations (CROs) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Thorough QT/QTc Study Services | |

| ECG & Holter Monitoring Analysis | ||

| Blood Pressure & Telemetry Analysis | ||

| Cardiovascular Imaging (Echocardiography, MUGA) | ||

| Real-Time Data Analytics & Reporting | ||

| By Service Delivery Model | In-house (Sponsor-run) | |

| Outsourced (CRO & Specialist Vendors) | ||

| By Clinical Trial Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV / Post-marketing | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Firms | ||

| Medical Device Manufacturers | ||

| Contract Research Organisations (CROs) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will cardiac safety service spending be by 2031?

It is projected to reach USD 1.75 billion, rising at an 11.09% CAGR from 2026 to 2031.

Which service line is expanding the fastest?

Real-time data analytics and reporting is advancing at a 14.24% compound rate as sponsors prioritize same-day arrhythmia alerts.

Why are decentralized and hybrid trials important for cardiac monitoring?

They let volunteers transmit Holter data from home, cut site visits by 40%, and still comply with FDA digital‐health guidance.

What is driving early-phase demand for cardiac telemetry?

Regulators now expect full QT assessments in first-in-human studies, pushing Phase I outlays up 12.84% a year.

Which region shows the strongest growth outlook?

Asia-Pacific leads with a forecast 13.63% CAGR, helped by China’s harmonized QT guidance and India’s investment in ISO 13485 labs.

Page last updated on: