United States Patient Engagement Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

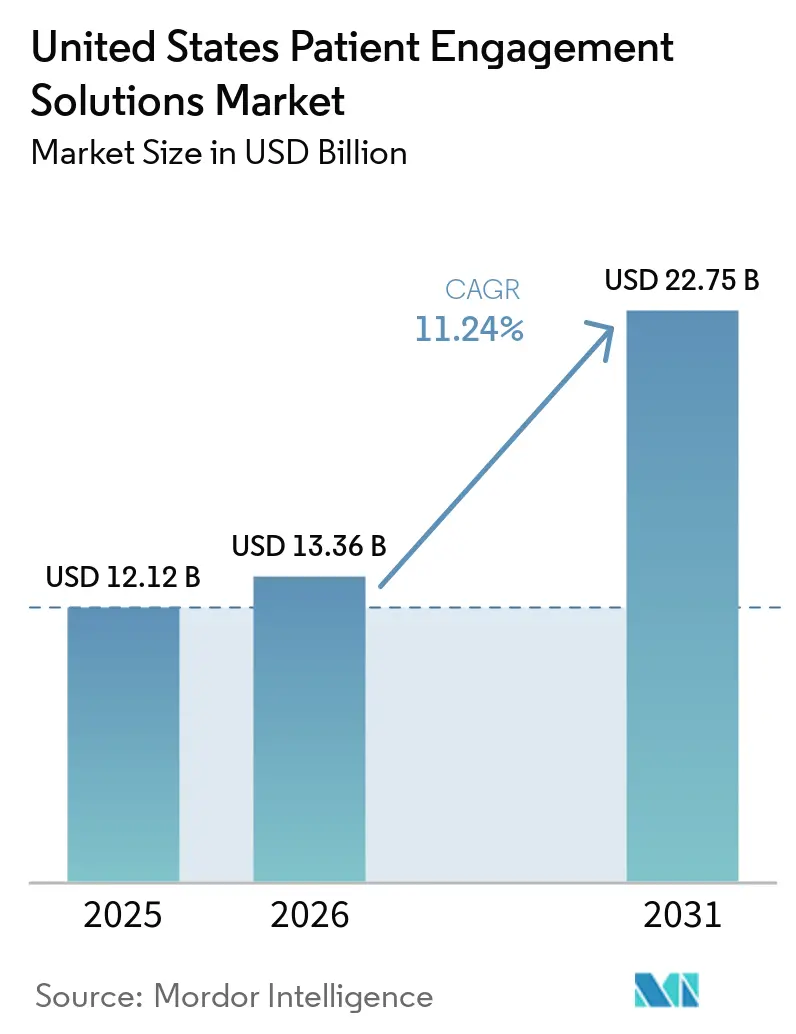

| Base Year Market Size (2025) | USD 12.12 Billion |

| Market Size (2026) | USD 13.36 Billion |

| Market Size (2031) | USD 22.75 Billion |

| Growth Rate (2026 - 2031) | 11.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Patient Engagement Solutions Market Analysis by Mordor Intelligence

The United States Patient Engagement Solutions Market size is projected to be USD 12.12 billion in 2025, USD 13.36 billion in 2026, and reach USD 22.75 billion by 2031, growing at a CAGR of 11.24% from 2026 to 2031.

The United States patient engagement solutions market is expanding as value-based reimbursement continues to tie financial performance more closely to measurable patient outcomes and consistent follow-up. CMS reduced the Medicare Alternative Payment Model incentive payment rate to 1.88% in 2026 from 5% in earlier years, which is pushing health systems to depend more on digital engagement tools that support care coordination, reporting, and adherence tracking. The United States patient engagement solutions market is also supported by the chronic care burden, with the CDC stating that 90% of the nation’s USD 4.9 trillion in annual healthcare spending is tied to chronic and mental health conditions. Cloud migration, AI-enabled communication, and CMS interoperability requirements are reshaping vendor selection, as buyers now prefer platforms that support both patient access and standards-based data exchange. The United States patient engagement solutions market still faces execution risk from fragmented system architectures and cyber exposure, but those issues are also favoring larger vendors that can prove stronger integration and compliance readiness.

Key Report Takeaways

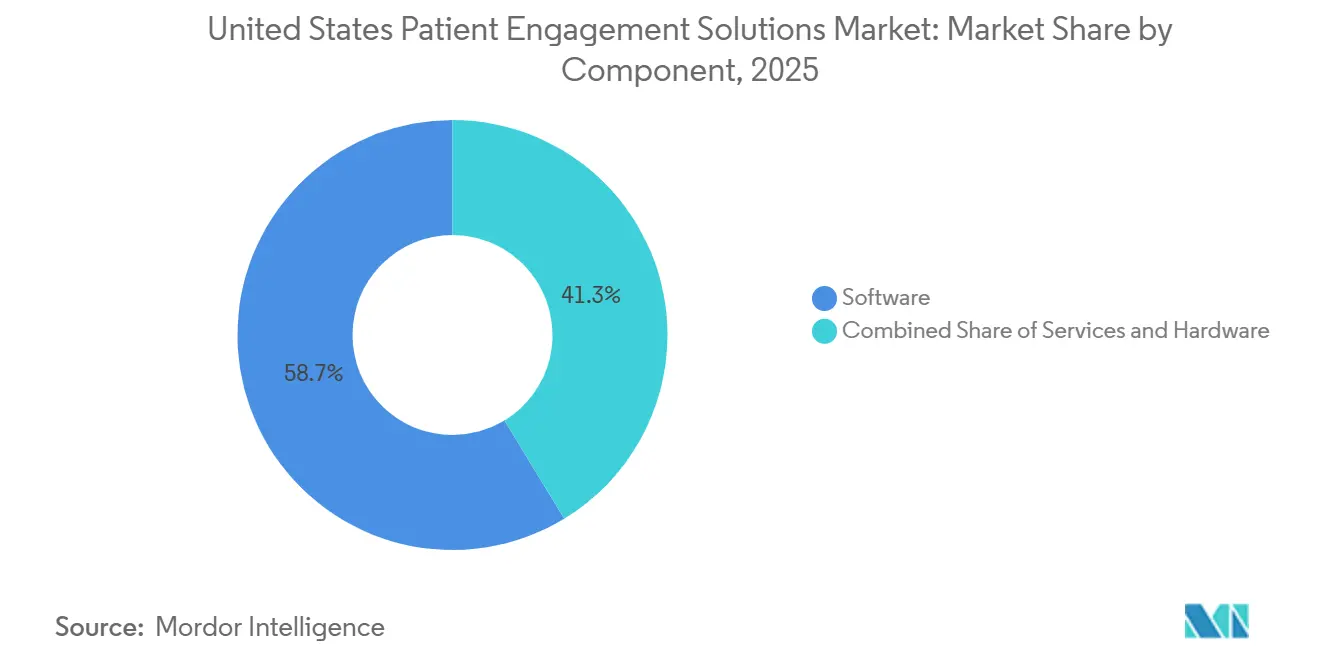

- By component, software held 58.66% of revenue in 2025, while services is projected to grow at a 12.39% CAGR through 2031.

- By solution type, AI-driven engagement led with 30.51% share in 2025, while remote patient monitoring is forecast to expand at an 11.95% CAGR through 2031.

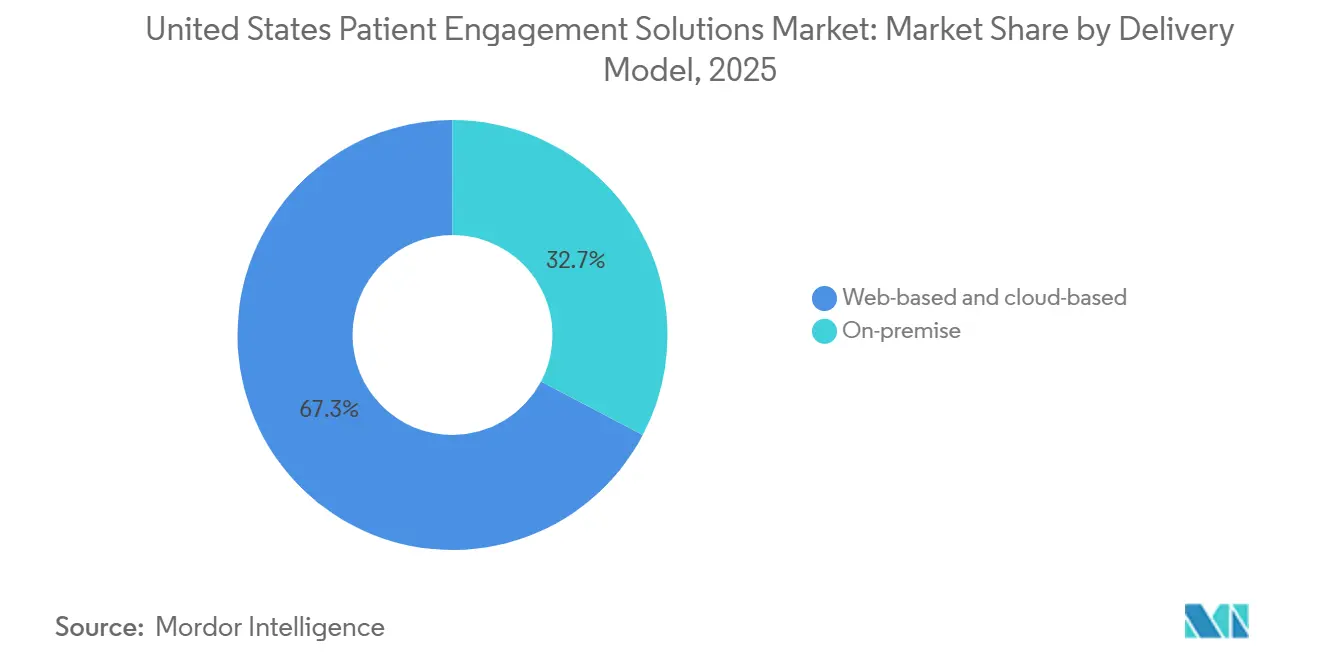

- By delivery model, web-based and cloud-based delivery accounted for 67.35% of the market in 2025 and is also advancing at a 13.33% CAGR through 2031.

- By functionality, communication and messaging represented 28.98% of revenue in 2025, while financial and administrative workflow functionality is growing at a 15.09% CAGR through 2031.

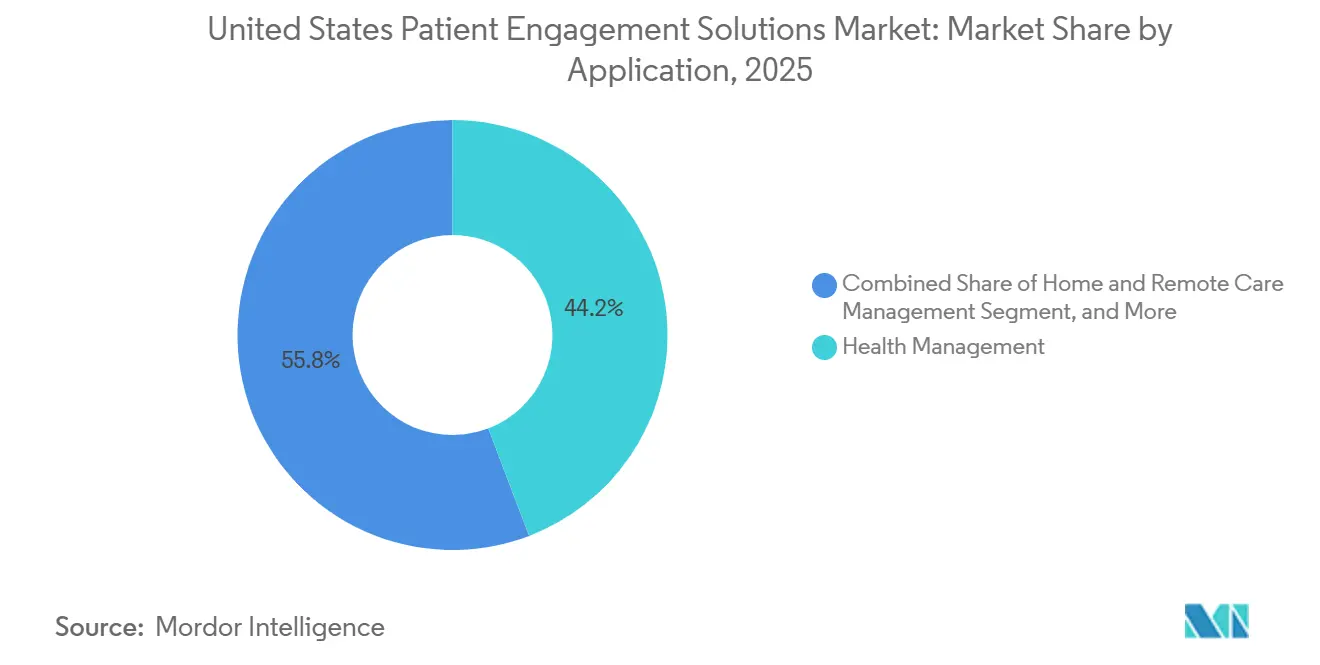

- By application, health management captured 44.21% share in 2025, while home and remote care management is projected to expand at a 13.82% CAGR through 2031.

- By therapeutic area, chronic diseases held 34.85% share in 2025, while behavioral and mental health is forecast to record the highest CAGR at 16.71% through 2031.

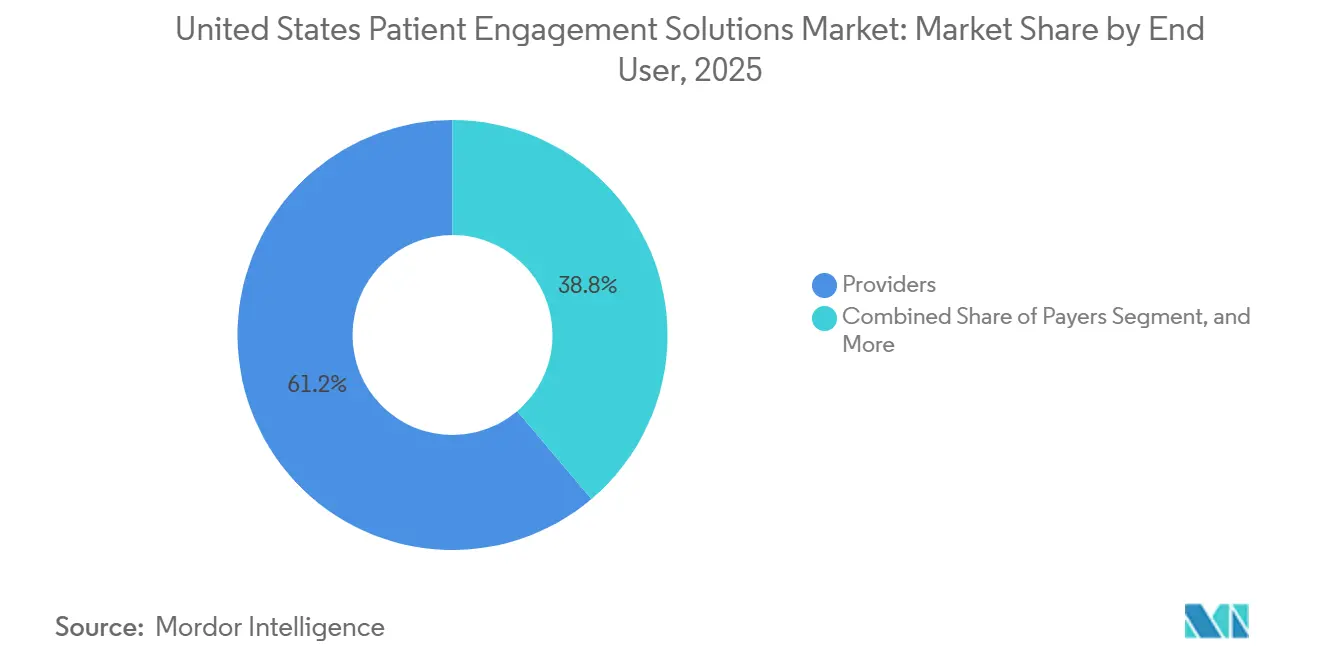

- By end user, providers held 61.23% of the United States patient engagement solutions market share in 2025, while payers are projected to grow at a 15.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Patient Engagement Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift To Value-Based And Patient-Centric Care | +2.0% | National, with stronger early gains in states with advanced Medicaid managed care programs such as Massachusetts, California, and Minnesota | Medium term (2-4 years) |

| High Chronic Disease And Aging Burden | +2.1% | National, with stronger relevance in Sun Belt and rural Midwest states with older and multi-morbid populations | Long term (≥ 4 years) |

| Rapid Digital Front-Door And AI Engagement Adoption | +2.5% | National, led by large integrated delivery networks in Northeast and West Coast markets | Short term (≤ 2 years) |

| Consumer Demand For Self-Service Access And Communication | +1.3% | National, with urban and suburban markets leading adoption and rural areas becoming gap-closure targets | Medium term (2-4 years) |

| CMS Interoperability And Prior Authorization API Rollout | +1.5% | National, across CMS-regulated payer categories, with stronger early effect in Medicare Advantage-heavy states such as Florida, Texas, and Pennsylvania | Short term (≤ 2 years) |

| CMS Healthtech Ecosystem And Medicare App Library Discovery Layer | +0.8% | National, with more visible impact in markets with high Medicare Advantage enrollment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Value-Based and Patient-Centric Care

The United States patient engagement solutions market is benefiting from value-based payment structures that reward providers and payers for measurable clinical improvement rather than visit volume alone. The Medicare Alternative Payment Model incentive payment rate fell to 1.88% in 2026 from 5% in earlier program years, which reduced the financial cushion that once made inefficient care coordination easier to absorb.[1]Centers for Medicare & Medicaid Services, “42 CFR § 414.1450 APM Incentive Payment,” Legal Information Institute, law.cornell.edu That change is making digital outreach, care plan follow-up, adherence tracking, and patient-reported engagement records more important for contract performance and reporting. CMS’s ACCESS model also supports outcome-aligned payments for technology-enabled care when providers achieve measurable targets such as blood pressure reduction or pain management. The United States patient engagement solutions market is also drawing stronger payer investment, as digital engagement now supports member navigation, care gap closure, and retention. UnitedHealthcare launched Avery in March 2026 as a generative AI companion inside its member app, showing that large payers now treat engagement capability as part of core benefit delivery.

High Chronic Disease and Aging Burden

The United States patient engagement solutions market has a durable demand base because chronic and mental health conditions continue to shape how care is financed, delivered, and monitored. CDC states that 90% of the nation’s USD 4.9 trillion in annual healthcare spending is attributable to people with chronic and mental health conditions, which keeps pressure on health systems to improve between-visit management.[2]Centers for Disease Control and Prevention, “Fast Facts Health and Economic Costs of Chronic Conditions,” CDC, cdc.gov Patients managing multiple long-duration conditions typically require more reminders, more education, more follow-up, and more documentation than episodic care populations. That pattern increases the strategic value of platforms that can keep outreach continuous across medication use, symptom monitoring, and care plan updates. The United States patient engagement solutions market, therefore, benefits not just from disease prevalence, but from the recurring interaction frequency that chronic care creates inside provider and payer workflows.

Rapid Digital Front-Door and AI Engagement Adoption

The United States patient engagement solutions market is moving quickly toward AI-enabled communication because manual scheduling, intake, and inquiry handling are too labor-intensive for large enterprise networks. athenahealth launched agentic patient communication tools inside athenaOne in February 2026, adding AI-powered text and voice functions across a provider network that serves 1 in 5 Americans. Oracle Health reported in March 2026 that its Clinical AI Agent had already saved physicians more than 200,000 hours across U.S. provider users within its first year, which strengthened the ROI case for AI-enabled patient-facing workflows.[3]Oracle Health, “Oracle Health Demonstrates Interoperability Leadership, Achieves CMS Aligned Network Status,” Oracle, oracle.com As more EHR vendors embed AI features directly inside their core platforms, standalone engagement vendors are being pushed to compete on cross-EHR portability, narrower workflow depth, or faster deployment. The digital front door is also widening beyond portals, since health plans, providers, and specialty service vendors are all building app-based guidance, intake, and self-service tools. The United States patient engagement solutions market is therefore shifting from feature-led competition toward workflow automation that reduces staff effort while keeping patients active.

CMS Interoperability and Prior Authorization API Rollout

The United States patient engagement solutions market is gaining from a regulatory environment that is expanding the usable data layer for patient-facing applications. CMS published the Interoperability and Prior Authorization Final Rule in January 2024, and key operational provisions became effective on January 1, 2026, including required denial reasons and patient access API usage reporting. Full patient access, provider access, payer-to-payer, and prior authorization API requirements carry January 1, 2027, compliance dates, which gives engagement platforms a wider standards-based integration surface. CMS also proposed in April 2026 to extend electronic prior authorization requirements to drugs and align decision timelines, with urgent requests proposed at 24 hours and standard requests at 72 hours. These rules make prior authorization status, access barriers, and payer decisions easier to expose inside patient-facing tools, which turns compliance work into a transparency feature. Oracle Health’s April 2026 CMS Aligned Network designation shows how vendors are using standards-based exchange readiness as a patient engagement differentiator rather than only a back-office requirement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability Gaps Across EHR, Payer, And Point-Solution Stacks | -1.1% | National, with the strongest effect in fragmented community hospital and rural provider markets | Long term (≥ 4 years) |

| Data Privacy, Cybersecurity, And HIPAA Compliance Burden | -0.9% | National, with stronger effect in states with added data protection rules beyond federal HIPAA requirements | Medium term (2-4 years) |

| Portal And App Fragmentation Reducing Longitudinal Engagement | -0.7% | National, with concentrated impact in multi-system urban markets where patients use several provider networks | Medium term (2-4 years) |

| AI Governance And ROI Scrutiny Slowing Enterprise Rollouts | -0.6% | National, with the strongest effect in large academic medical centers and complex enterprise organizations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Across EHR, Payer, and Point-Solution Stacks

The United States patient engagement solutions market still faces a structural limit because patient data often sits across disconnected provider, payer, and specialized workflow systems. A 2025 systematic review in Frontiers in Health Services found persistent barriers, including semantic misalignment across HL7 FHIR and SNOMED CT implementations, limited cross-system exchange, and weak integration of patient-generated health data. That means standards adoption alone does not guarantee a usable longitudinal record inside patient engagement platforms. HHS leadership wrote in a 2025 JAMA article that unlocking the potential of EHR data for patient experience improvement still requires a more unified approach to exchange and implementation. When information appears incomplete or inconsistent across portals, reminders, and payer touchpoints, patients are less likely to trust the digital channel. The United States patient engagement solutions market, therefore, remains constrained by operational integration quality, not just by the number of interfaces a vendor can claim to support.

Data Privacy, Cybersecurity, and HIPAA Compliance Burden

The United States patient engagement solutions market operates under heavy cyber and privacy pressure because platforms handle highly sensitive clinical, financial, and behavioral data. IBM reported that the average healthcare data breach cost reached USD 7.42 million in 2024, and average breach containment took 279 days, which kept healthcare as the costliest sector for breaches for the 14th straight year. HHS OCR confirmed through July 2025 that the Change Healthcare ransomware incident affected the protected health information of 192.7 million individuals, which reset enterprise expectations for vendor risk management. The American Hospital Association also noted that by year-end 2024, 259 million Americans had experienced PHI exposure and that many attacks combined data theft with operational disruption. These events raise deployment costs because vendors must invest more in encryption, access controls, audit trails, third-party risk reviews, and breach response planning. The burden is especially relevant for AI-driven communication tools, since patient-facing behavior and message content must be handled within strict privacy and minimum-necessary rules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates, Services Becoming Strategic Infrastructure

Software accounted for 58.66% of the United States patient engagement solutions market in 2025, which kept it well ahead of services and hardware in the spending mix. That lead reflects the scale of platform demand for communication, scheduling, intake, reminders, education, and care coordination inside one digital layer. Integrated suites remain the preferred choice for large health systems because they reduce vendor sprawl and fit more easily inside established clinical workflows. Standalone applications still hold an important role in narrower use cases such as intake optimization, patient financing, and behavioral outreach, where buyers often want deeper configuration. The United States patient engagement solutions market continues to reward software vendors that can combine workflow breadth with faster implementation and easier clinician adoption.

Services are projected to record the fastest component growth at a 12.39% CAGR through 2031, which shows that deployment complexity is rising with platform sophistication. Health systems increasingly need implementation support, integration work, staff training, ongoing optimization, and compliance guidance as AI agents and FHIR-based connectivity become more common. Phreesia stated in its FY2026 stakeholder letter that it enabled more than 180 million patient visits in 2025 and expanded its scope through the AccessOne acquisition, which added patient financing capability to its platform offering. Hardware remains a supporting layer rather than the core spending center, but kiosks, bedside devices, tablets, and identity tools still matter in ambulatory and inpatient settings. Oracle Health’s CLEAR integration shows how identity verification is being folded into digital intake and paper-free check-in workflows, which keeps certain hardware-linked functions relevant even as software takes the largest share.

By Solution Type: AI-Driven Engagement Leads While RPM Accelerates

AI-driven engagement held 30.51% of the solution type segment in 2025, making it the largest category inside the United States patient engagement solutions market. Its lead comes from intelligent outreach, conversational scheduling, triage support, and care gap closure tools that are now moving into routine enterprise use. Platforms with larger installed bases also build richer behavioral datasets over time, which improves personalization and makes the product more useful with each new interaction. That advantage matters because patient response patterns, channel preferences, and timing behavior can shape outreach quality in ways that are difficult for newer entrants to replicate quickly. The United States patient engagement solutions market is, therefore, seeing solution competition move from isolated features toward data-backed workflow performance.

Remote patient monitoring is forecast to expand at an 11.95% CAGR through 2031, which makes it the fastest-growing solution type over the forecast period. Its growth is tied to chronic disease prevalence, wider use of between-visit monitoring, and reimbursement support for remote physiologic monitoring activities in higher-risk populations. Patient portals still account for a meaningful share of solution demand, but ONC data shows that adoption and capability use remain uneven among lower-resourced hospitals. Telehealth solutions also remain embedded in the engagement stack because virtual care now supports access, follow-up, and convenience expectations across many care settings. Population health tools, medication reminders, intake platforms, and financial engagement systems continue to sell alongside one another, which is encouraging multi-solution purchasing inside broader platform ecosystems.

By Delivery Model: Cloud-Native Delivery Captures Both Share and Growth

Web-based and cloud-based delivery held 67.35% share in 2025 and is also the fastest-growing model at a 13.33% CAGR through 2031. That combination shows that the dominant delivery model in the United States patient engagement solutions market is still gaining ground rather than moving into a slow-growth phase. Health systems favor cloud deployment because it supports faster upgrades, more flexible scaling, and easier rollout of AI-enabled features across multiple sites. The Change Healthcare attack pushed many organizations to review infrastructure resilience, vendor dependencies, and recovery preparedness with greater urgency after 2024. Frequent release cycles also suit cloud environments better, since modern engagement platforms need regular workflow tuning, security updates, and model changes.

On-premise delivery still retains a role in federal settings, highly regulated specialty environments, and organizations with stricter network isolation requirements. Some providers continue to prefer local control over deployment and data flows when internal governance is more conservative or when legacy infrastructure remains deeply embedded. Procurement standards such as HITRUST and FedRAMP have also raised the bar for cloud vendors serving sensitive or publicly funded programs, which can slow smaller entrants. Oracle Health’s QHIN and CMS Aligned Network activity shows that interoperability expectations and delivery architecture are increasingly being planned together rather than separately. The United States patient engagement solutions market is therefore moving toward cloud-first deployment as the default, even though on-premise options still matter in selected enterprise environments.

By Functionality: Financial Tools Outpace Clinical Enablement in Growth

Communication and messaging represented 28.98% of the market in 2025, giving it the largest functional share in the United States patient engagement solutions market. This position reflects how basic outreach functions remain essential across nearly every care setting, payer workflow, and patient journey. SMS, email, secure messaging, and voice reminders still form the basic layer on which more advanced scheduling, intake, and care management tools are built. The segment is mature, but it remains central because patients still judge digital access first through timely responses and simple communication. TeleVox’s April 2025 launch of Insights360 showed that vendors are now adding more analytics depth even inside this established category.

Financial and administrative workflow functionality is projected to grow at a 15.09% CAGR through 2031, making it the fastest-growing functional category. Providers want tools that simplify estimates, billing communication, payment options, and administrative follow-up because those steps now carry more direct revenue consequences. Cedar reported that ApolloMD improved overall collection rates by 42% within the first year of implementation, with 92% of collections coming from patients who engaged digitally. Scheduling and access, clinical enablement, and analytics and personalization continue to fill out the functional stack across enterprise procurement decisions. Analytics is becoming more valuable because interaction data can now support population stratification, workflow tuning, and reporting needs tied to value-based contracts. The patient engagement solutions industry is therefore placing more weight on tools that can prove measurable workflow and revenue improvement, not only communication volume.

By Application: Health Management Anchors the Market, Home Care Accelerates

Health management held 44.21% of the application segment in 2025, which gave it the largest role in the United States patient engagement solutions market by use case. That strength comes from chronic disease management, preventive care support, wellness programs, and ongoing education workflows that require repeated patient contact. These programs remain important because they support patients who need monitoring and follow-up over longer time horizons rather than during one isolated episode. Providers also rely on health management functions to keep patients connected between visits through reminders, care plans, and status checks. The United States patient engagement solutions market continues to depend on this application area because it links directly to both utilization management and long-term clinical engagement.

Home and remote care management is forecast to grow at a 13.82% CAGR through 2031, which makes it the fastest-expanding application segment. Growth is being supported by remote monitoring, hospital-at-home models, post-discharge outreach, and care plan follow-up that can be delivered outside the clinic. Asynchronous models are also becoming more commercially useful because they allow clinical teams to maintain oversight without requiring every interaction to happen in person. Care coordination and communication, social and behavioral management, and financial health management remain relevant across the broader application landscape. CMS’s 2025 MIPS Value Pathways framework added more attention to patient activation and care planning measures, which support broader use of structured engagement workflows in these adjacent applications. The patient engagement solutions industry is therefore seeing home-centered models become more central as providers look for scalable ways to manage patients outside traditional visit settings.

By Therapeutic Area: Chronic Disease Remains Dominant, Behavioral Health Accelerates

Chronic diseases accounted for 34.85% of the therapeutic area segment in 2025, giving this category the leading position in the United States patient engagement solutions market. Diabetes, cardiovascular disease, respiratory disease, oncology, and obesity all require repeated communication, follow-up, monitoring, and care plan reinforcement. That makes chronic care programs a natural fit for digital engagement platforms that can sustain interaction over time rather than only during intake or discharge. Cardiovascular and respiratory pathways are also adding more device-linked engagement, which expands the role of reminders, alerts, and education. Oncology remains a distinct use case because navigation and symptom tracking are high-frequency needs during active treatment.

Behavioral and mental health is projected to grow at a 16.71% CAGR through 2031, which makes it the fastest-growing therapeutic area in the report. The segment is benefiting from persistent demand, growing comfort with digital-first interaction, and provider interest in keeping contact active between appointments. Talkiatry announced an oversubscribed USD 210 million Series D in 2025 to expand its full-stack psychiatry platform, which shows that behavioral care engagement continues to attract capital and operational scale. Women’s health and other therapeutic areas are also drawing attention, where discreet access, app-based navigation, and tailored communication are becoming more important. The United States patient engagement solutions market is, therefore, seeing the fastest therapeutic momentum in categories where trust, continuity, and regular low-friction touchpoints can materially influence care adherence. This part of the patient engagement solutions industry is likely to stay active because behavioral care still has access gaps that digital platforms can help narrow.

By End User: Providers Lead, Payers Emerge as the High-Growth Segment

Providers held 61.23% of the patient engagement solutions market size in 2025, keeping them as the largest end-user group across the United States patient engagement solutions market. Their lead is supported by the deep placement of communication, portal, scheduling, and care management tools inside provider workflows. Hospitals and physician groups continue to spend because patient engagement has shifted from a helpful add-on to a core part of access, retention, and follow-up operations. Even so, many provider organizations have already covered basic portal and reminder use cases, which means newer budgets are moving toward AI-driven automation and patient finance tools. The United States patient engagement solutions market is therefore seeing provider demand become more selective, with a stronger focus on measurable deployment outcomes rather than broad feature lists.

Payers are forecast to grow at a 15.06% CAGR through 2031, making them the fastest-growing end-user category. Their investment logic centers on care gap closure, member navigation, Star Ratings, HEDIS quality performance, and risk-adjusted reimbursement rather than only customer service. Washington State’s 2025 value-based payment survey reported improved patient outcomes, more timely interventions, and better care coordination among organizations using these models, which supports the case for payer-led engagement spending. Pharmacies are also becoming more active buyers as specialty programs and adherence workflows require stronger patient communication outside standard dispensing. Other buyer groups, including accountable care organizations, employer health plans, and federally qualified health centers, are creating additional demand pockets with different integration and pricing needs. The United States patient engagement solutions market is broadening on the demand side as these non-provider buyers seek tools that fit their own workflow and reimbursement realities.

Geography Analysis

The United States patient engagement solutions market is a single-country market, but adoption is not uniform across regions and provider types. The Northeast and West Coast remain the strongest early-adoption clusters because they have more large integrated delivery networks, academic medical centers, and technology-forward payer organizations. These areas are often quicker to implement AI-enabled front-door tools, enterprise remote monitoring, and standards-based data exchange. ONC’s 2021 to 2024 brief showed that lower-resourced hospitals still lag in patient engagement capability adoption, which explains why growth remains uneven across the country. The United States patient engagement solutions market, therefore, reflects a two-speed pattern, with stronger enterprise-led deployment in well-funded systems and slower expansion in resource-constrained settings.

The Sun Belt states represent the largest volume opportunity inside the United States patient engagement solutions market because they combine aging populations, high chronic disease burden, and heavy Medicare Advantage presence. Florida, Texas, Arizona, and the broader Southeast stand out as important payer-side engagement zones where care gap closure and member activation have clear reimbursement value. These states also align well with home-based care, remote monitoring, and hospital-at-home models that depend on continuous patient contact. CDC projects that the number of adults aged 85 and older will reach 13.7 million by 2040, which supports a long-duration demand outlook for remote care and caregiver communication tools. State-specific privacy rules, including stricter protections in some jurisdictions, also add operational complexity for national vendors that need consistent consent and data-handling controls.

Midwest rural markets remain an important white-space opportunity in the United States patient engagement solutions market because distance, provider shortages, and chronic disease prevalence all support stronger remote engagement use cases. These areas can benefit from remote monitoring and digital follow-up, but broadband constraints and smaller IT budgets still slow implementation in many organizations. Sanford Health partnered with Cedar in 2025 to improve financial engagement across rural care settings, which shows that rural systems are also prioritizing administrative patient experience where revenue pressure is more immediate. Federal connectivity support and stable telehealth policy should help narrow the rural-urban adoption gap over the forecast period.

Competitive Landscape

The United States patient engagement solutions market shows moderate concentration, with a small group of large EHR-platform vendors holding strong embedded positions while specialized vendors compete around them. Epic, Oracle Health, and athenahealth benefit from workflow proximity because their engagement tools sit close to the clinical record and routine provider operations. Oracle Health strengthened its positioning in April 2026 by achieving CMS Aligned Network status and integrating CLEAR for identity-enabled, paper-free patient intake. Athenahealth also expanded its competitive posture in February 2026 by launching agentic patient communication tools across athenaOne. The United States patient engagement solutions market remains open to specialists because many buyers still want faster deployment, deeper workflow control, or better cross-EHR compatibility than broad EHR suites can offer.

Phreesia remains an important specialist, and its FY2026 stakeholder letter showed more than 180 million patient visits enabled in 2025, together with a broader reach into patient financing through AccessOne. Luma Health expanded its Operational AI capabilities in 2026 to automate no-show rescheduling, results follow-up, and fax-to-workflow conversion, which moved the company further beyond messaging into workflow execution. Cedar also demonstrated measurable financial engagement value through ApolloMD, where digital interaction supported a 42% increase in collection rates within the first year. These moves show that specialist vendors are expanding horizontally across adjacent functions instead of defending only one narrow product area. The United States patient engagement solutions market is, therefore, rewarding vendors that can turn engagement into operational and financial outcomes, not just improved user interfaces.

There is still room for newer entrants in audit-ready AI, behavioral engagement between appointments, and rural-focused financial workflows. Vendors that can prove secure integration, policy alignment, and rapid deployment should be better placed to win large enterprise deals. Smaller players can also compete where large platforms remain slower to configure or less flexible across mixed EHR environments. The United States patient engagement solutions market remains competitive, but vendor advantage is increasingly tied to scale, interoperability readiness, and evidence of measurable workflow improvement.

United States Patient Engagement Solutions Industry Leaders

athenahealth

eClinicalWorks

Epic Systems Corporation

Oracle

Veradigm LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Oracle Health achieved CMS Aligned Network status and integrated CLEAR's IAL2-certified identity platform for QR-code-based, paper-free patient check-in, supporting CMS's "Kill the Clipboard" initiative. AtlantiCare (NJ) deployed the solution across ambulatory check-in workflows, positioning Oracle as a standards-based interoperability infrastructure provider for patient intake.

- April 2026: Luma Health released its Spring 2026 Operational AI update, expanding autonomous care-related task handling to cover no-show rescheduling, clinical results follow-up, and automated fax-to-workflow transformation via Fax Transform. The release builds on a platform that had already saved 2.5 million staff hours across health systems.

- March 2026: Oracle Health made Clinical AI Agent note generation available for inpatient and emergency department settings in the US. In its first year of availability, the solution saved physicians more than 200,000 hours across all US provider users.

- February 2026: athenahealth launched its next-generation agentic patient communication suite within athenaOne, including AI-powered text and voice scheduling and inquiry resolution across its provider network serving 1 in 5 Americans.

United States Patient Engagement Solutions Market Report Scope

The patient engagement solutions market encompasses the digital health technologies and platforms designed to facilitate communication and collaboration between patients and healthcare providers. These solutions, such as patient portals, telehealth systems, and mobile health apps, aim to improve health literacy, treatment adherence, and the overall patient experience.

The United States Patient Engagement Solutions Market Report is segmented across multiple dimensions that define its scope and structure. By component, it includes software, services, and hardware. By solution type, the market covers AI-driven platforms, patient portals, telehealth solutions, remote patient monitoring (RPM), and population health tools. In terms of delivery model, solutions are offered through web/cloud-based systems as well as on-premise deployments. Segmentation by functionality and application reflects the diverse use cases across healthcare settings. By therapeutic area, the report highlights solutions tailored for chronic conditions, women’s health, behavioral and mental health, and other specialties. Finally, by end user, the market encompasses providers, payers, pharmacies, and other healthcare stakeholders. Market forecasts are provided in terms of value (USD), illustrating the financial scale and growth potential of the patient engagement solutions market.

| Software | Integrated patient engagement platforms |

| Standalone patient engagement applications | |

| Services | Implementation and integration services |

| Training and education services | |

| Support and maintenance services | |

| Consulting and optimization services | |

| Hardware | Bedside engagement devices |

| Self-service kiosk and check-in devices | |

| Patient tablets and remote devices |

| AI-driven engagement |

| Patient portals |

| Telehealth solutions |

| Remote patient monitoring solutions |

| Population health and outreach solutions |

| Appointment and medication reminder solutions |

| Patient intake and registration solutions |

| Financial engagement solutions |

| Web-based and cloud-based |

| On-premise |

| Communication and messaging |

| Scheduling and access |

| Clinical enablement |

| Financial and administrative workflow |

| Analytics and personalization |

| Health management |

| Home and remote care management |

| Care coordination and communication |

| Social and behavioral management |

| Financial health management |

| Chronic diseases | Diabetes |

| Cardiovascular diseases | |

| Respiratory diseases | |

| Oncology | |

| Obesity and metabolic disorders | |

| Other chronic diseases | |

| Women’s health | |

| Behavioral and mental health | |

| Other therapeutic areas |

| Providers |

| Payers |

| Pharmacies |

| Other End Users |

| By Component | Software | Integrated patient engagement platforms |

| Standalone patient engagement applications | ||

| Services | Implementation and integration services | |

| Training and education services | ||

| Support and maintenance services | ||

| Consulting and optimization services | ||

| Hardware | Bedside engagement devices | |

| Self-service kiosk and check-in devices | ||

| Patient tablets and remote devices | ||

| By Solution Type | AI-driven engagement | |

| Patient portals | ||

| Telehealth solutions | ||

| Remote patient monitoring solutions | ||

| Population health and outreach solutions | ||

| Appointment and medication reminder solutions | ||

| Patient intake and registration solutions | ||

| Financial engagement solutions | ||

| By Delivery Model | Web-based and cloud-based | |

| On-premise | ||

| By Functionality | Communication and messaging | |

| Scheduling and access | ||

| Clinical enablement | ||

| Financial and administrative workflow | ||

| Analytics and personalization | ||

| By Application | Health management | |

| Home and remote care management | ||

| Care coordination and communication | ||

| Social and behavioral management | ||

| Financial health management | ||

| By Therapeutic Area | Chronic diseases | Diabetes |

| Cardiovascular diseases | ||

| Respiratory diseases | ||

| Oncology | ||

| Obesity and metabolic disorders | ||

| Other chronic diseases | ||

| Women’s health | ||

| Behavioral and mental health | ||

| Other therapeutic areas | ||

| By End User | Providers | |

| Payers | ||

| Pharmacies | ||

| Other End Users | ||

Key Questions Answered in the Report

What is driving growth in patient engagement solutions in the United States through 2031?

Growth is being supported by value-based care, chronic disease burden, AI-enabled digital front-door adoption, and CMS interoperability rules. The report projects expansion from USD 13.36 billion in 2026 to USD 22.75 billion by 2031 at an 11.24% CAGR.

Which component category leads spending in this space?

Software leads spending with 58.66% share in 2025 because providers and payers continue to prioritize platforms that combine communication, scheduling, intake, and care coordination.

Which solution type is growing the fastest?

Remote patient monitoring is the fastest-growing solution type, with an 11.95% CAGR through 2031, supported by chronic disease management and between-visit care needs.

Why are payers increasing investment in digital engagement tools?

Payers are using these platforms to improve member navigation, close care gaps, support Star Ratings and HEDIS measures, and strengthen risk-adjusted reimbursement performance.

What is the biggest operational risk for vendors and buyers?

The largest operational risks are interoperability gaps and cyber exposure. Fragmented data environments reduce continuity, while healthcare breach costs reached USD 7.42 million on average in 2024.

Page last updated on: