Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

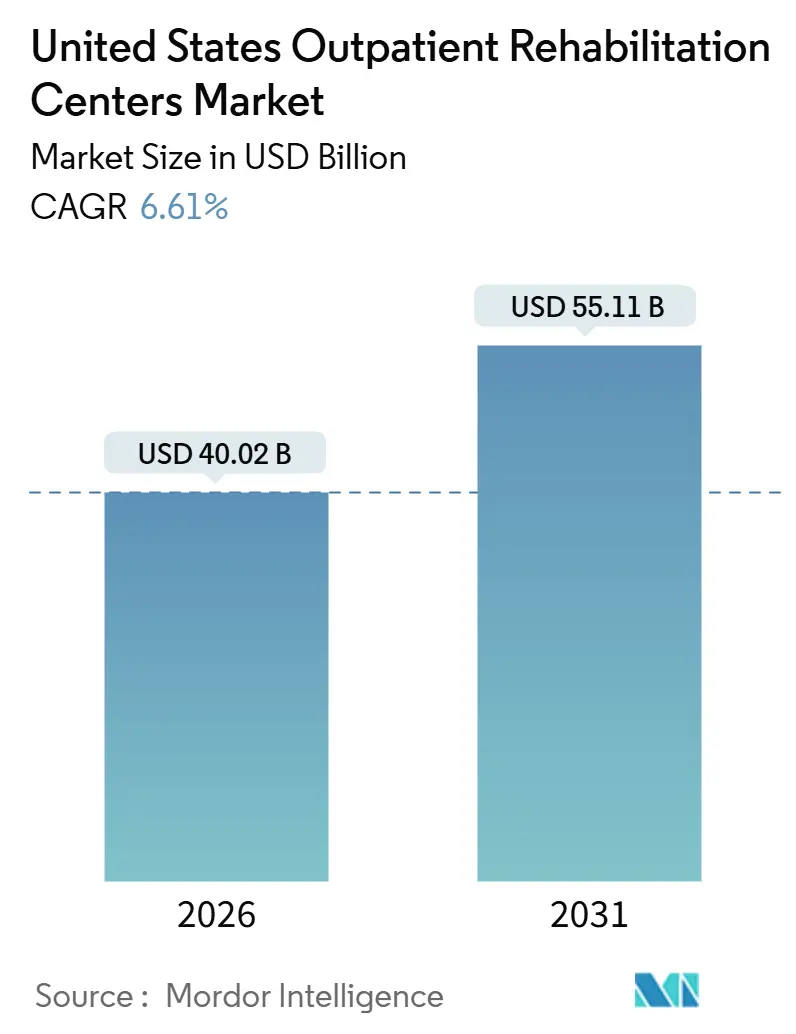

| Market Size (2026) | USD 40.02 Billion |

| Market Size (2031) | USD 55.11 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Outpatient Rehabilitation Centers Market Analysis by Mordor Intelligence

The United States Outpatient Rehabilitation Centers Market size is estimated at USD 40.02 billion in 2026, and is expected to reach USD 55.11 billion by 2031, at a CAGR of 6.61% during the forecast period (2026-2031).

Extensions of hospital-at-home waivers, surging Medicare Advantage enrollment, and employer-sponsored onsite clinics are steering patient volumes away from inpatient facilities and toward community-based therapy. Physical therapy dominates the revenue mix, yet tele-rehab platforms that blend in-person and virtual visits are posting double-digit growth as sensor-based motion tracking lifts adherence and expands therapist panel capacity. Musculoskeletal disorders remain the largest caseload driver, but neurological rehabilitation is the fastest-expanding condition segment as longer survival after stroke and Parkinson’s disease lengthens therapy timelines. Reimbursement headwinds from consecutive CMS fee-schedule cuts are pressuring independent operators, spurring consolidation and accelerating technology adoption that lowers per-episode costs. Workforce shortages and uneven clinic density - especially in rural Sun Belt and Midwest counties - continue to shape expansion strategies and capital allocation in the United States outpatient rehabilitation centers market.

Key Report Takeaways

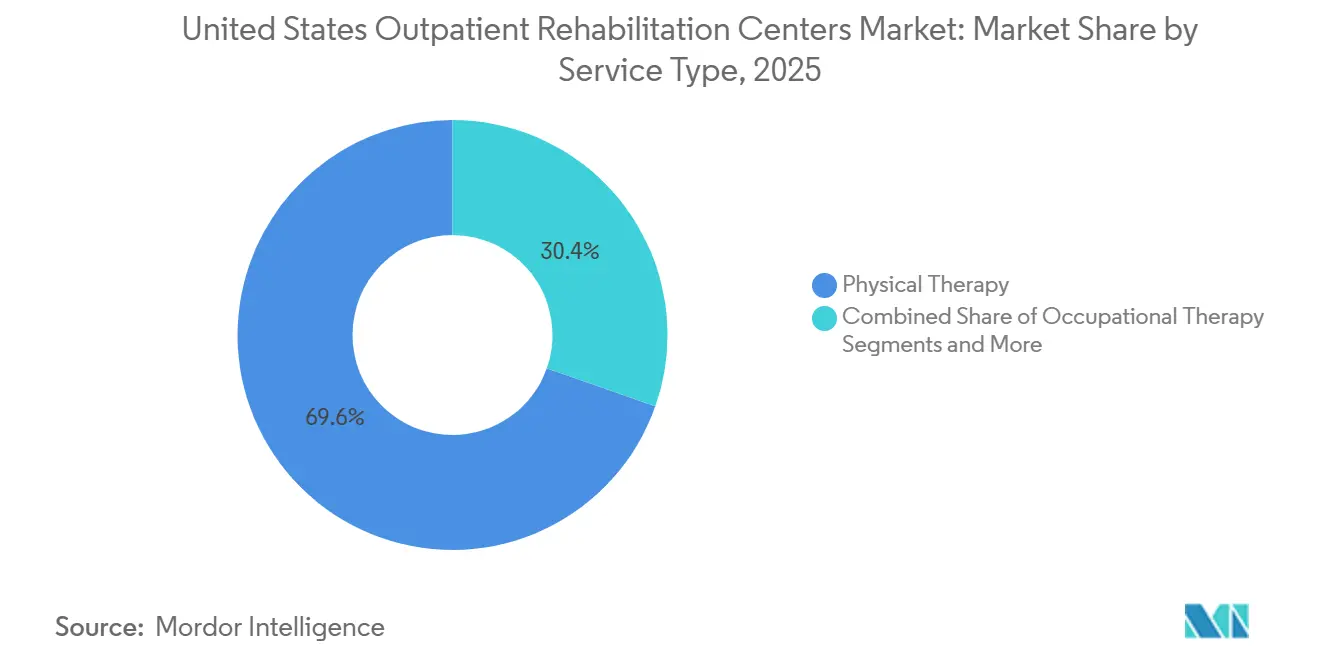

- By service type, physical therapy captured 69.62% of revenue in 2025, while tele-rehab physical therapy is on track for a 10.52% CAGR to 2031.

- By rehabilitation condition, musculoskeletal disorders commanded 58.56% of 2025 case volume; neurological rehabilitation is projected to expand at 9.24% through 2031.

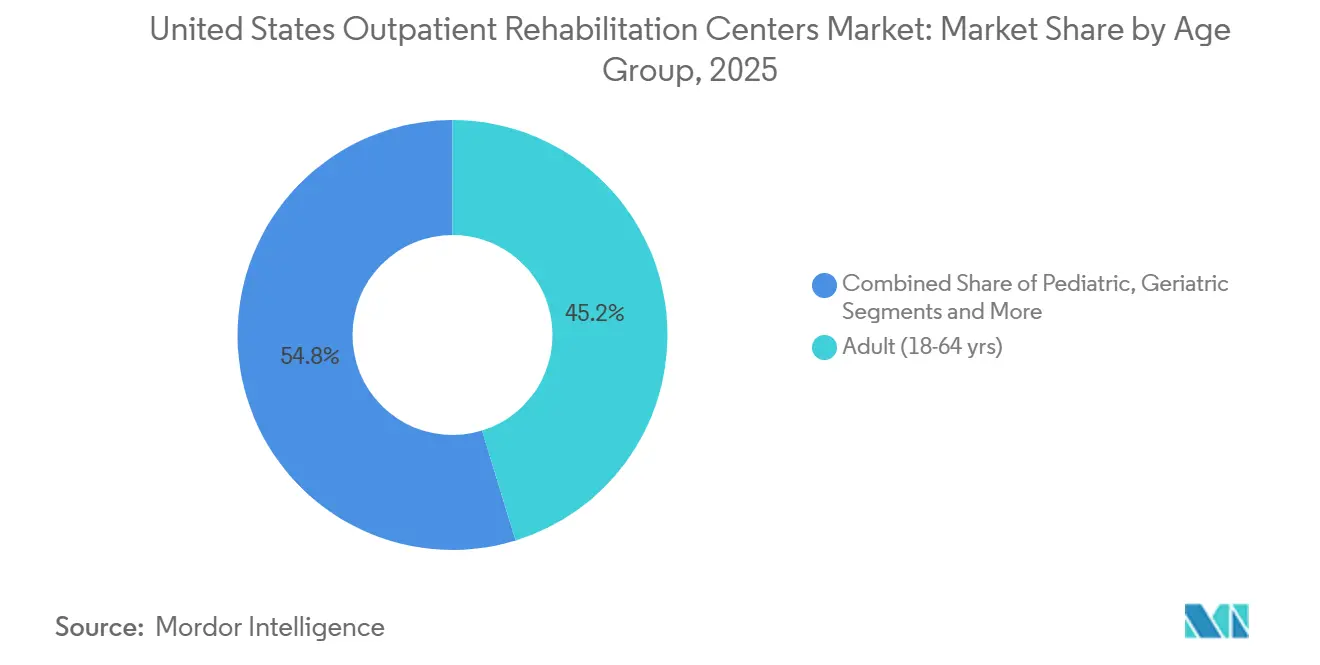

- By age group, geriatric visits are forecast to grow at an 8.32% CAGR, outpacing the adult segment that still represented 45.24% of visits in 2025.

- By payer type, private insurance held 39.22% of the United States outpatient rehabilitation centers market share in 2025; Medicare Advantage is the fastest-growing channel at 8.73% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Outpatient Rehabilitation Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & chronic musculoskeletal burden | +1.8% | Florida, Arizona, Texas | Long term (≥ 4 years) |

| Shift to value-based outpatient care models | +1.2% | California, New York, Pennsylvania | Medium term (2–4 years) |

| Rising sports injuries & active-lifestyle demand | +0.9% | Colorado, Oregon, Washington, North Carolina | Short term (≤ 2 years) |

| Hospital-at-home codes enabling hybrid rehab | +0.7% | New York, Massachusetts, Illinois | Medium term (2–4 years) |

| Employer-sponsored onsite rehab clinics | +0.5% | Texas, California, Georgia | Medium term (2–4 years) |

| AI-driven motion tracking boosts adherence | +0.6% | California, Washington, Massachusetts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic Musculoskeletal Burden

The 65-plus cohort climbed 3.1% to 61.2 million in 2024 and is projected to reach 78 million by 2040, a shift that dovetails with higher arthritis, chronic back pain, and fall-related injuries.[1]Jennifer D. Ortman, “2024 Population Estimates: 65 and Older Population,” U.S. Census Bureau, census.gov Arthritis affects 53.2 million adults, chronic back pain is reported by 39% of adults, and falls result in 3 million emergency visits annually, prompting Medicare to reimburse evidence-based fall-prevention therapy that saves USD 3 in acute-care costs for every rehabilitation dollar spent.[2]Charles G. Helmick, “Arthritis Prevalence and Chronic Pain Statistics, 2024,” Centers for Disease Control and Prevention, cdc.gov Sun Belt states show the steepest senior growth yet remain below median clinic density, stretching wait times beyond three weeks in suburban Phoenix and Tampa. As the geriatric population accumulates multiple chronic conditions, the United States outpatient rehabilitation centers market increasingly relies on multi-modal programs that target strength, balance, and pain management within one care plan.

Shift to Value-Based Outpatient Care Models

Medicare Advantage enrollment hit 33.8 million in 2024, or 54% of eligible beneficiaries, and many plans now pay for additional physical therapy visits beyond fee-for-service limits.[3]Meredith Freed, “Medicare Advantage Enrollment 2024 Data Spotlight,” Kaiser Family Foundation, kff.org Bundled payment models covering joint replacement and cardiac episodes delivered 18% more outpatient therapy visits in the first 90 days post-discharge than fee-for-service cohorts, rewarding clinics that can share real-time outcomes data with accountable care organizations. Providers adept at risk-sharing are securing preferred-network status, especially in California, New York, and Pennsylvania, where value-based contracts tie up to 15% of revenue to quality metrics such as functional-outcome scores and 90-day readmission rates. The United States outpatient rehabilitation centers market thus favors operators with interoperable EHRs and analytics that quantify therapy’s economic returns.

AI-Driven Motion Tracking Boosts Adherence

FDA-cleared digital therapeutics that employ smartphone cameras or wearable sensors now guide home exercises, logging repetitions and flagging risky compensations. Studies published in 2024 show patients using AI-guided platforms complete 72% of prescribed exercises, versus 48% on paper programs, resulting in superior functional-gain scores. Clinics integrating these tools expand therapist panels from 12 to 18 patients per full-time equivalent, trimming facility costs by 35% per episode while maintaining outcomes. However, only half of commercial payers reimburse remote monitoring codes as of early 2026, creating uneven adoption across the United States outpatient rehabilitation centers market.

Hospital-at-Home Codes Enabling Hybrid Rehab

CMS extended its Acute Hospital Care at Home waiver through December 2025, allowing more than 300 hospitals to deliver inpatient-level care - and accompanying rehabilitation - inside patients’ homes. Early evidence shows 30–40% lower episode costs and satisfaction scores above 90%. Urban health systems in New York, Massachusetts, and Illinois have already captured up to 12 percentage points of post-surgical rehab share in active ZIP codes, compelling freestanding centers to form joint ventures that maintain continuity when patients transition from acute home care to community-based therapy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CMS fee-schedule reimbursement cuts | -0.8% | National, rural emphasis | Short term (≤ 2 years) |

| Licensed therapist workforce shortage | -0.6% | Rural Midwest, Appalachia, non-metro South | Long term (≥ 4 years) |

| Rising urban clinic real-estate costs | -0.3% | New York, San Francisco, Boston, Seattle, Los Angeles | Medium term (2–4 years) |

| Data-privacy friction for sensor monitoring | -0.2% | California and biometric-law states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

CMS Fee-Schedule Reimbursement Cuts

The Medicare physician fee schedule reduced payment for core evaluation and therapeutic exercise codes by 3.37% in 2024 and a further 2.83% in 2025, slicing already thin 8–12% EBITDA margins for independent clinics. Rural operators, unable to leverage large commercial payer contracts, face disproportionate pressure and are either consolidating or exiting the United States outpatient rehabilitation centers market. National chains are downsizing footprints, shortening visit lengths, and shifting to group sessions to offset lost revenue while lobbying continues for multi-year phase-ins.

Licensed Therapist Workforce Shortage

Physical therapist employment is forecast to grow 14% from 2022 to 2032, yet only 10,200 new graduates entered the workforce in 2024, while turnover in outpatient settings tops 18%. Rural counties average fewer than 0.5 clinics per 10,000 residents, and sign-on bonuses exceed USD 15,000. Telehealth offers partial relief, but licensure reciprocity remains incomplete, with 12 states still outside the Physical Therapy Compact. Unless graduate program capacity rises or international credentialing accelerates, staffing constraints will temper clinic expansion across the United States outpatient rehabilitation centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Physical Therapy Anchors Revenue, Tele-Rehab Accelerates

Physical therapy held 69.62% of 2025 revenue in the United States outpatient rehabilitation centers market, while tele-rehab PT is growing at 10.52% annually through 2031. Occupational therapy leverages Medicare’s expanded fall-prevention benefits, speech therapy meets rising post-stroke aphasia needs, and respiratory therapy gains traction from long-COVID cases. Hybrid care models typically start and finish in clinic but shift six to eight mid-episode visits online, cutting facility costs by 35%. Reimbursement parity is improving; Medicare pays 95% of in-person rates, but commercial discounts of up to 30% still challenge aggressive virtualization.

Continued tele-rehab adoption is supported by 2024 competency standards that make virtual-care skills mandatory for new graduates. Yet interoperability gaps and payer variability keep in-person visits dominant for occupational therapy that requires environmental assessments and for speech therapy nuances best captured face-to-face. Providers balance modality mix to sustain margins across the United States outpatient rehabilitation centers market size.

By Rehabilitation Condition: Musculoskeletal Volume Meets Neurological Growth

Musculoskeletal disorders accounted for 58.56% of 2025 cases, reflecting 53.2 million arthritis sufferers, chronic back pain prevalence, and 120,000 ACL repairs. Neurological rehabilitation is set to grow 9.24% through 2031 as 7.6 million stroke survivors and 1 million Parkinson’s patients demand extended therapy. Cardiopulmonary programs benefit from CMS expansion to 36 covered sessions, and post-operative pathways thrive under bundled payments that reward early mobilization.

Constraint-induced movement therapy and LSVT BIG protocols require 20–40 visits, boosting revenue per episode versus routine orthopedic cases. Medicare Advantage plans accept the cost because robust neurological programs cut nursing-home placements, lowering long-term spend. Operators diversify into these higher-acuity lines to cushion CMS fee-schedule cuts, sustaining the United States outpatient rehabilitation centers market share.

By Age Group: Geriatric Surge Reshapes Demand

Geriatric visits are expanding at an 8.32% CAGR as the senior population surges, even though adults aged 18–64 still generated 45.24% of 2025 clinic volume. Pediatric cases grow modestly via early-intervention mandates but suffer from lower Medicaid reimbursement. Clinics are redesigning schedules to accommodate geriatric needs—longer evaluations, caregiver coordination—and extending evening hours for working adults.

Preventive fall-prevention programs now reimbursed by Medicare lower acute admissions, aligning with capitated Advantage incentives. Meanwhile, minimally invasive procedures shorten adult rehab timelines and remote work reduces workplace injuries, tempering growth in the younger cohort within the United States outpatient rehabilitation centers market.

By Payer Type: Medicare Advantage Gains Share

Private insurance delivered 39.22% of 2025 revenue, yet Medicare Advantage is the fastest-rising payer at 8.73% CAGR as enrollment climbs past half of all beneficiaries. Advantage plans reward clinics capable of real-time outcome reporting and accept lower per-visit rates in exchange for steady volume. Traditional Medicare lags due to beneficiary migration and fee-schedule cuts, while Medicaid continues to reimburse at 60–70% of Medicare, leading many providers to cap volume.

Workers’ compensation declines with safer workplaces, and self-pay remains niche amid USD 75–150 visit costs. Risk-based contracts and supplemental benefits position Medicare Advantage as the pivotal growth engine for the United States outpatient rehabilitation centers market size over the forecast.

Geography Analysis

Regional disparities influence expansion. Sun Belt states show the fastest senior growth yet sub-median clinic density, prompting de novo builds in Phoenix, Tampa, and Austin. California, New York, and Pennsylvania lead Medicare Advantage penetration, enabling value-based networks that capture referrals. Rural Midwest and Appalachian counties wrestle with therapist shortages, where sign-on incentives are highest.

Urban coastal hubs face medical office rents topping USD 55 per square foot, compelling footprint downsizing or relocations to secondary submarkets. Hospital-at-home programs thrive in these same metros, diverting post-operative cases from freestanding centers unless joint ventures secure downstream therapy. Tele-rehab scalability is limited in 12 non-compact states, further segmenting the United States outpatient rehabilitation centers market geographically.

Competitive Landscape

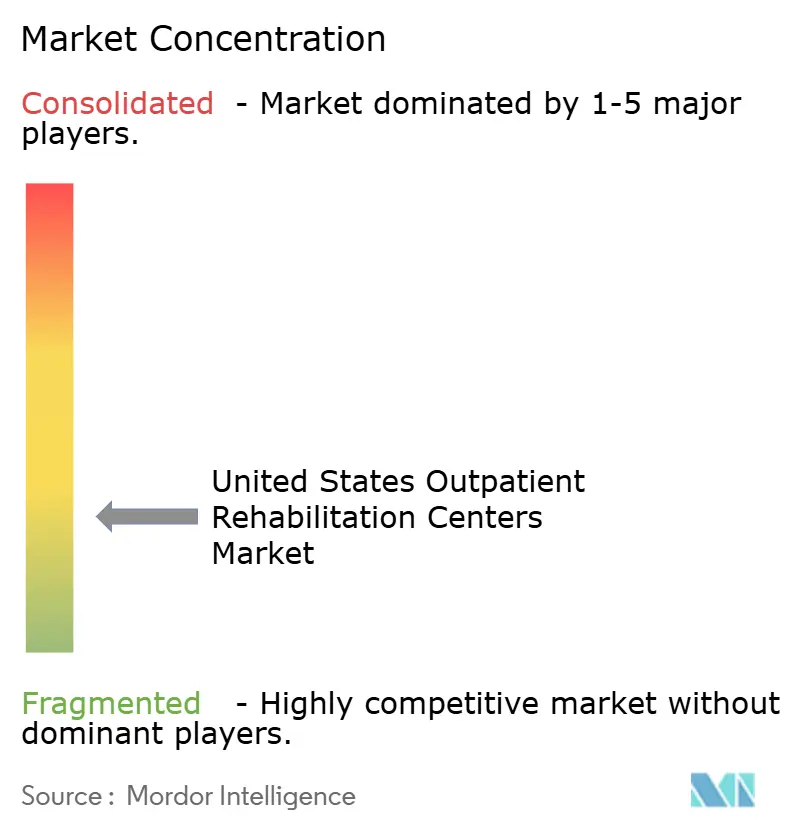

The five largest providers include Encompass Health, Select Medical, U.S. Physical Therapy, ATI Physical Therapy, and Athletico, underscoring fragmentation. Private-equity roll-ups and public chains are executing de novo builds in growth corridors and acquiring single-site clinics to aggregate share. Competitive edge now rests on technology integration, outcomes-based contracting, and payer diversification.

Chains deploying AI motion tracking expand therapist capacity while cutting costs, positioning themselves for Medicare Advantage preferred-network status. Rural markets offer whitespace but require creative staffing models, whereas urban systems leverage hospital-at-home programs to internalize rehab revenue. Select Medical grew its outpatient footprint 6.2% in 2024, focusing on Advantage-dense metros and orthopedic ASC partnerships that funnel high-margin post-surgical cases. Consolidation and technology-enabled efficiency will define strategy across the United States outpatient rehabilitation centers market.

United States Outpatient Rehabilitation Centers Industry Leaders

Select Medical Corporation

Encompass Health Corp.

U.S. Physical Therapy Inc.

ATI Physical Therapy

Kindred Rehabilitation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: R & R Health launched expanded sober-living and outpatient addiction treatment services in Redondo Beach, California.

- December 2025: Nemours Children’s Health opened the Lisa Dean Moseley Foundation Institute for Cancer and Blood Disorders Outpatient Services and Day Hospital in the Delaware Valley.

- November 2025: TIRR Memorial Hermann inaugurated a new outpatient clinic in Cypress, California.

United States Outpatient Rehabilitation Centers Market Report Scope

As per the scope of the report, outpatient rehabilitation is an effective form of therapy for those with conditions that don't require intensive care. It has a lower cost and offers a greater degree of freedom compared to inpatient therapy. Outpatient rehab is needed after many surgeries. As part of the recovery process, the patient may begin receiving care at a hospital. Depending on the nature or extent of the injury, the treatment might be given by physical therapists.

The United States outpatient rehabilitation centers market is segmented by service type, rehabilitation condition, age group, and payer type. By Service Type, the market is segmented into Physical Therapy, Occupational Therapy, speech and language therapy, and Respiratory Therapy. By Rehabilitation Condition, the market is segmented into Musculoskeletal Disorders, Neurological Disorders, Cardiopulmonary Conditions, Post-Operative Recovery, and sports and orthopedic injuries. By Age Group, the market is segmented into Pediatric, Adult, and Geriatric. By Payer Type, the market is segmented into Private Insurance, Medicare, Medicaid, Workers' Compensation, and Self-Pay.

. The report offers the value (in USD) for the above segments.

By Service Type

| Physical Therapy |

| Occupational Therapy |

| Speech & Language Therapy |

| Respiratory Therapy |

By Rehabilitation Condition

| Musculoskeletal Disorders |

| Neurological Disorders |

| Cardiopulmonary Conditions |

| Post-Operative Recovery |

| Sports & Orthopedic Injuries |

By Age Group

| Pediatric (0-17 yrs) |

| Adult (18-64 yrs) |

| Geriatric (65+ yrs) |

By Payer Type

| Private Insurance |

| Medicare |

| Medicaid |

| Workers’ Compensation |

| Self-Pay / Out-of-Pocket |

| By Service Type | Physical Therapy |

| Occupational Therapy | |

| Speech & Language Therapy | |

| Respiratory Therapy | |

| By Rehabilitation Condition | Musculoskeletal Disorders |

| Neurological Disorders | |

| Cardiopulmonary Conditions | |

| Post-Operative Recovery | |

| Sports & Orthopedic Injuries | |

| By Age Group | Pediatric (0-17 yrs) |

| Adult (18-64 yrs) | |

| Geriatric (65+ yrs) | |

| By Payer Type | Private Insurance |

| Medicare | |

| Medicaid | |

| Workers’ Compensation | |

| Self-Pay / Out-of-Pocket |

Key Questions Answered in the Report

How fast is the United States outpatient rehabilitation centers market expected to grow?

The market is forecast to expand at a 6.61% CAGR, rising from USD 40.02 billion in 2026 to USD 55.11 billion by 2031.

Which service category leads revenue?

Physical therapy accounts for 69.62% of 2025 revenue, sustained by musculoskeletal and post-operative demand.

Why is Medicare Advantage pivotal for outpatient rehab providers?

Advantage plans are growing at 8.73% CAGR and reward clinics that can furnish real-time outcomes and accept risk-based payments.

Where are clinic shortages most acute?

Rural Midwest and Appalachian counties average fewer than 0.5 clinics per 10,000 residents, constraining access and fueling sign-on bonuses.

What technology trends are reshaping outpatient rehabilitation?

FDA-cleared AI motion-tracking tools raise home-exercise adherence, expand therapist capacity, and support hybrid in-person/virtual care models.

Page last updated on: