United States Practice Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

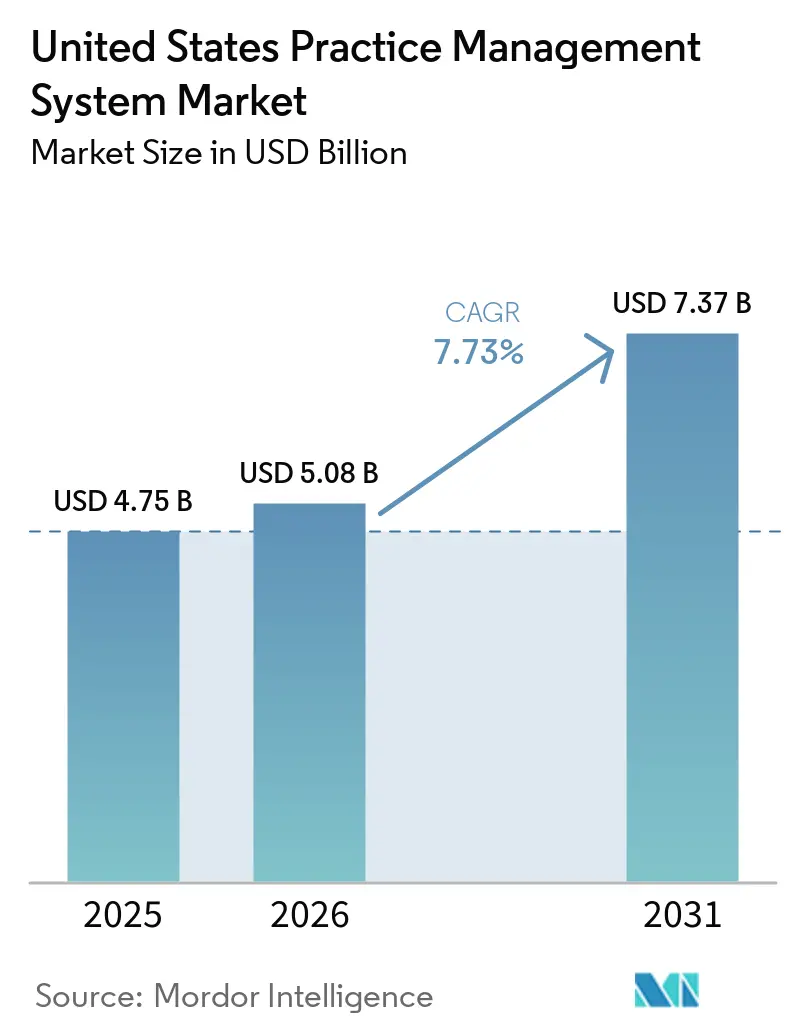

| Base Year Market Size (2025) | USD 4.75 Billion |

| Market Size (2026) | USD 5.08 Billion |

| Market Size (2031) | USD 7.37 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Practice Management System Market Analysis by Mordor Intelligence

The United States Practice Management System Market size is projected to expand from USD 4.75 billion in 2025 and USD 5.08 billion in 2026 to USD 7.37 billion by 2031, registering a CAGR of 7.73% between 2026 to 2031.

The United States practice management system market is being pushed by mounting pressure to reduce denied claims, recover patient balances, and automate administrative work that still absorbs a large share of provider resources. Hospitals tracked by Kodiak Solutions lost USD 48.4 billion in net revenue in 2025 from final claim denials and uncollected patient balances, up from USD 38.6 billion in 2024, which keeps billing efficiency at the center of software spending decisions. The 2025 CAQH Index reported that electronic transactions avoided USD 258 billion in administrative costs in 2024 and identified another USD 21 billion savings opportunity from fuller automation, which continues to strengthen the case for replacing legacy systems with workflow-driven platforms. Regulatory deadlines are also compressing purchase timelines because CMS has already activated prior authorization response and reporting provisions, and full FHIR API compliance is required by January 1, 2027. The United States practice management system market is also seeing competition shift away from broad feature lists and toward clean-claim improvement, denial avoidance, interoperability readiness, and operating resilience as vendors embed AI, cloud delivery, and stronger redundancy into core platform offers.

Key Report Takeaways

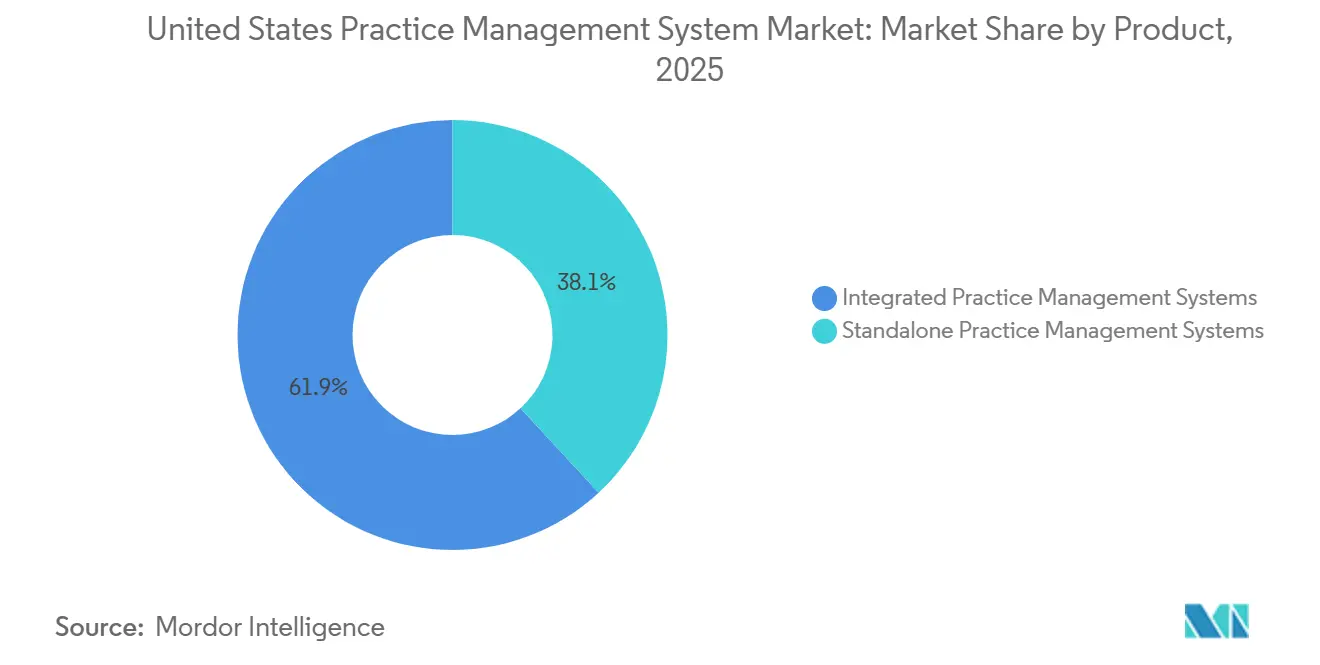

- By product, integrated practice management systems held 61.87% of 2025 revenue in the United States practice management system market share, and the same segment is projected to expand at 8.25% CAGR through 2031.

- By component, software accounted for 63.83% of revenue in 2025, while services recorded the highest projected CAGR at 9.34% through 2031.

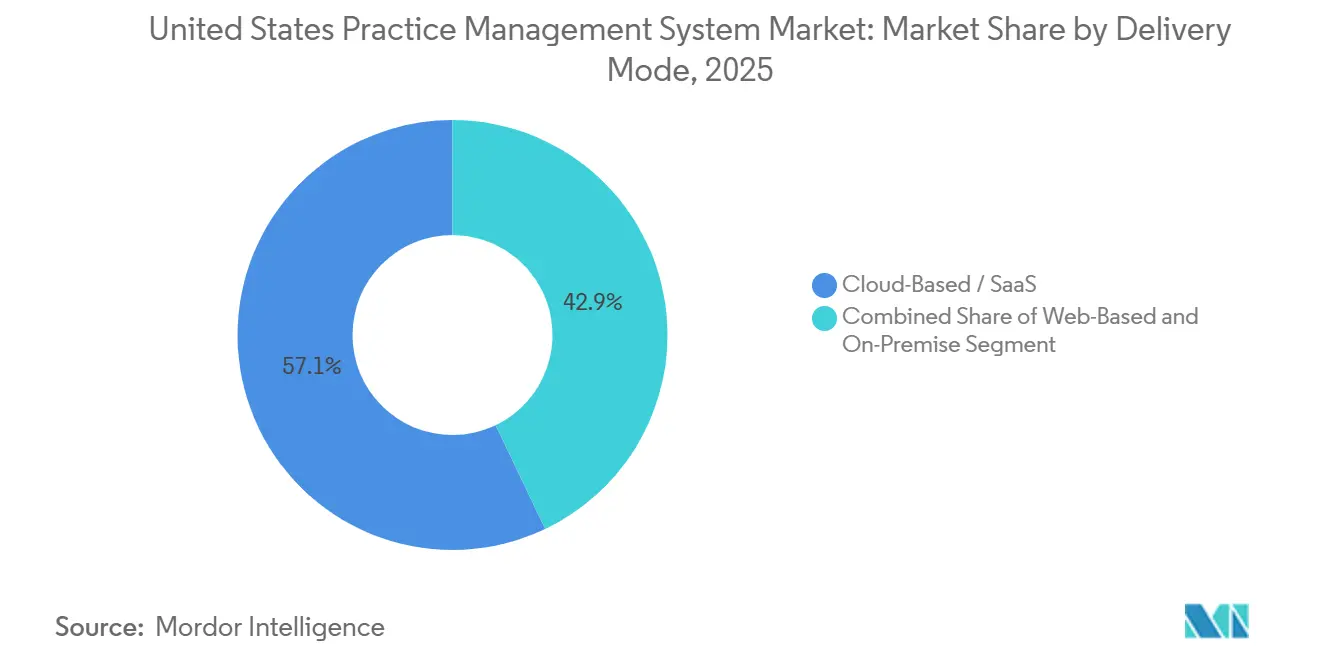

- By delivery mode, cloud-based/SaaS represented 57.12% of revenue in 2025, while the same segment is forecast to grow fastest at 8.69% through 2031.

- By functionality, billing, coding, and claims management captured 33.28% of revenue in 2025, while telehealth coordination is projected to advance at 9.02% CAGR through 2031.

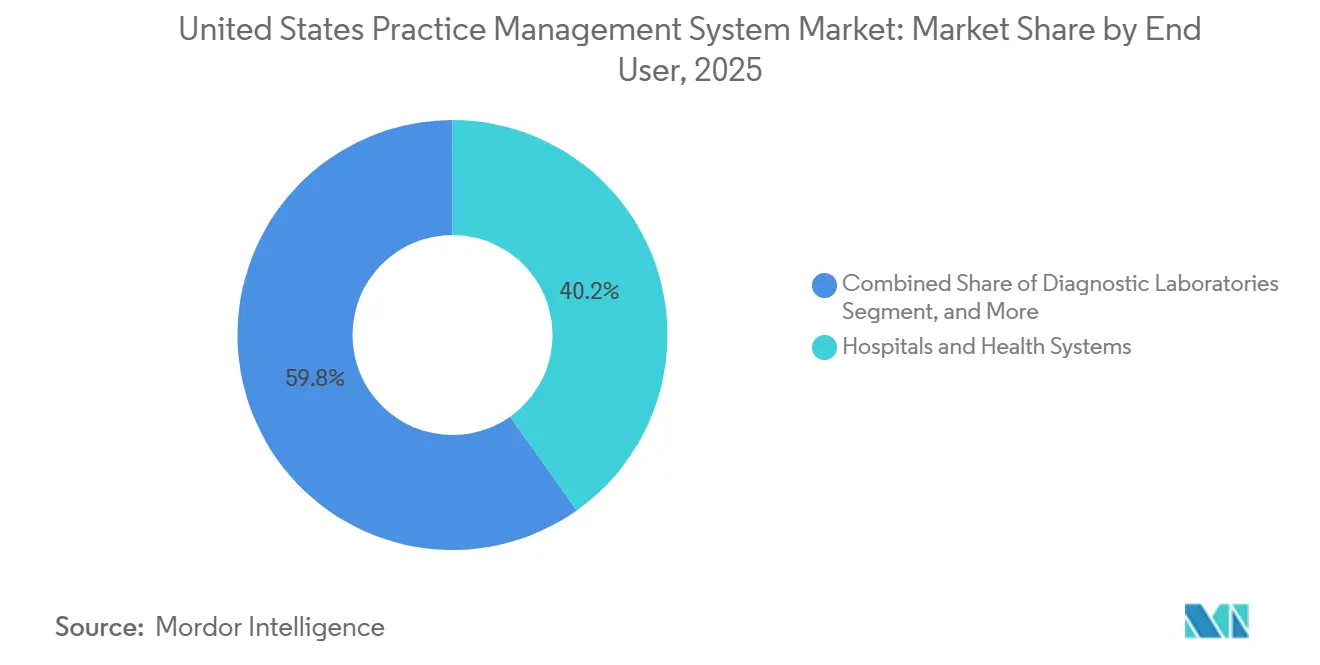

- By end user, hospitals and health systems led with 40.23% of revenue in 2025, while pharmacies are forecast to expand at 8.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Practice Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Administrative Cost and Claim-Denial Reduction Imperative | +1.8% | Global, with peak impact in high-density payer markets, Northeast US, Midwest, Southeast | Short term (≤ 2 years) |

| Shift To Integrated EHR-PM-RCM Suites | +1.5% | National, accelerating in large-group and multi-specialty practices across all regions | Medium term (2-4 years) |

| Cloud Migration for Multi-Site and Hybrid Workflows | +1.4% | National, leading in Sun Belt and suburban multi-site ambulatory groups | Medium term (2-4 years) |

| FHIR-Based Interoperability and E-Prior-Authorization Compliance | +1.2% | National, with early gains in markets with highest payer API readiness, West Coast, Northeast | Short term (≤ 2 years) |

| TEFCA / QHIN Connectivity Becoming a Buying Criterion | +0.8% | National, with spill-over to rural and critical access settings | Medium term (2-4 years) |

| AI-Native Denial Prevention and Staff-Capacity Extension | +1.7% | National, with highest uptake in enterprise organizations and growing use in independent practices | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Administrative Costs and Claim Denials Make Status Quo Unsustainable

The United States practice management system market is being shaped by a billing environment that has become materially harder for providers to manage with fragmented tools. Kodiak Solutions reported that net revenue leakage from final denials and bad debt reached USD 48.4 billion across U.S. hospitals in 2025, up from USD 38.6 billion in 2024, while the median final denial rate rose from 2.5% to 2.7%. Premier also reported that claims adjudication costs providers USD 25.7 billion and that USD 18 billion of that spend is potentially unnecessary expense, which shows how much avoidable rework remains in the payment cycle.[1]Premier Inc., “Claims Adjudication Costs Providers 25.7 Billion, 18 Billion Is Potentially Unnecessary Expense,” Premier Inc., premierinc.com As a result, practices are giving higher priority to eligibility checks, pre-submission claim scrubbing, coding support, and denial prevention functions that can be tied directly to cash collection. This is why billing, coding, and claims management remain the largest functionality block in the United States practice management system market and why vendors are increasingly positioning measurable revenue recovery as the central value proposition.

Integrated EHR-PM-RCM Suites Redefine the Platform Buying Unit

The United States practice management system market is moving toward unified administrative and clinical platforms because providers now want fewer data handoffs and fewer reconciliation delays across scheduling, documentation, and revenue cycle activity. Integrated practice management systems controlled 61.9% of revenue in 2025, which confirms that buyers are already favoring broader suites over isolated point products. Epic showed the direction of travel at HIMSS 2026 with Penny for billing and denial avoidance, alongside agent-driven workflow tools that sit inside the main platform rather than outside it. athenahealth also expanded embedded revenue cycle improvements in its Spring 2026 athenaOne release, reinforcing the same shift toward connected workflows and regular platform-level upgrades.[2]athenahealth, “athenaOne Updates, Spring 2026 Release,” athenahealth, athenahealth.com In practical terms, the integrated model reduces duplicate entry, keeps patient and billing data in one operating layer, and makes interoperability readiness easier to evaluate during procurement.

Cloud Migration Extends Beyond Cost Savings Into Operational Resilience

The United States practice management system market is also being pushed toward SaaS delivery because cloud deployment now supports both day-to-day administration and continuity planning. Cloud-based/SaaS held 57.12% of revenue in 2025 and is projected to grow at 8.69% through 2031, which shows that providers increasingly prefer subscription access over local infrastructure in multi-site settings. CAQH reported that more than 50% of health plans and 25% of provider organizations are now using AI tools in administrative workflows, and those workloads are easier to roll out and update in cloud environments. AdvancedMD’s 2025 product release added a new clearinghouse partnership and framed it as part of a more resilient operating setup, which shows how vendor messaging has broadened from cost reduction to service continuity and risk mitigation. That combination of scalability, faster feature deployment, and redundancy support is keeping cloud migration firmly in the core growth story for the United States practice management system market.

FHIR-Based Interoperability Moves From Optional to Contractually Mandated

The United States practice management system market is facing a clear interoperability timetable rather than an open-ended policy signal. CMS finalized rule CMS-0057-F in January 2024 and requires Medicare Advantage organizations, Medicaid and CHIP managed care plans, and qualified health plan issuers on the federally facilitated exchanges to implement four FHIR-based APIs by January 1, 2027.[3]athenahealth, “athenaOne Updates, Spring 2026 Release,” athenahealth, athenahealth.com The same rule already activated non-technical prior authorization response time and reporting provisions from January 1, 2026, which means compliance work is no longer a future item for payers and providers. Vendors that can support prior authorization workflows, payer connectivity, and API-driven information exchange are therefore gaining a stronger sales position in provider evaluations. ONC also reported that TEFCA’s designated QHINs now connect more than 9,200 organizations across 41,000 unique endpoints, which is making broad exchange capability a practical buying requirement rather than a secondary feature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Costly Migration, Onboarding, and Workflow Disruption | -0.9% | National, most pronounced in independent practices and small rural groups | Medium term (2-4 years) |

| Cybersecurity and HIPAA Exposure in Cloud-Connected Environments | -0.8% | National, with highest risk in under-resourced rural and independent settings | Short term (≤ 2 years) |

| Payer Data Quality and API-Readiness Gaps | -0.6% | National, with spill-over to Medicaid-heavy markets in the South and Midwest | Medium term (2-4 years) |

| Vendor Consolidation and Legacy-Platform Uncertainty | -0.5% | National, concentrated in mid-market practices on discontinued or private equity acquired platforms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Migration Costs and Workflow Disruption Weigh on Replacement Cycles

The main brake on faster replacement remains the time and disruption involved in moving live administrative operations from one system to another. Implementation now goes beyond software installation because practices often need data cleansing, workflow redesign, staff retraining, payer rule alignment, and a parallel operating period before a full switch can happen. That burden is especially difficult for independent practices and community operators that do not have internal project teams or spare billing capacity during go-live periods. The rapid expansion of services, which is projected to grow at 9.3% through 2031, shows that many buyers are paying for outside implementation, training, and managed revenue cycle support instead of relying only on internal teams. This slows purchasing in the short run, even as it supports recurring vendor revenue inside the United States practice management system market.

Cybersecurity Exposure Reshapes Cloud Vendor Selection Criteria

Cybersecurity remains a real restraint because buyers now treat resilience and audit readiness as part of the product decision rather than as separate IT matters. HHS Office for Civil Rights announced a 2025 HIPAA ransomware settlement with a neurology practice, which reinforced that enforcement exposure extends to smaller providers and not only to large hospital systems. This environment is pushing practices to ask for SOC 2 Type II controls, isolated tenant architecture, business continuity commitments, and clearer clearinghouse backup arrangements before they sign new contracts. That extra diligence raises selling costs for vendors and slows some cloud migrations, especially in organizations with limited internal security review resources. Even so, the restraint is not stopping adoption in the United States practice management system market, but it is changing which vendors can win larger accounts and how long the decision cycle takes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Integrated Suites Consolidate the Market, Standalone Finds Refuge in Simplicity

Integrated practice management systems held 61.87% of revenue in 2025 and are projected to expand at 8.25% CAGR through 2031, which gives them both the largest base and the strongest momentum among product options. In product terms, this segment now represents the clearest center of gravity in the United States practice management system market because providers want one system to handle scheduling, documentation links, billing flow, and patient communication. EHR and EMR integrated systems remain the largest volume layer inside this group because health systems and larger physician organizations still favor single-vendor operating environments. Revenue-cycle integrated products are also gaining ground because providers want charge capture, edits, and denial management connected more tightly to front-end registration and back-end collections. Patient engagement integrated tools are becoming more relevant as digital intake, payment estimation, and self-service workflows move from optional features to normal administrative practice. E-prescribing integration is also shifting toward baseline functionality as broader interoperability expectations continue to rise across provider settings.

This direction supports the view that the United States practice management system industry is becoming less tolerant of disconnected software stacks. Epic, athenahealth, eClinicalWorks, and Veradigm are all leaning into broader workflow coverage because providers increasingly judge value by whether a platform reduces handoffs and missed revenue opportunities, not by how many separate modules can be purchased. Standalone systems still retain a meaningful share of demand, at near 38% of product revenue in 2025, because smaller physician offices and specialty clinics often want simpler scheduling and billing tools without the full complexity of a larger suite. Those buyers still value lower switching friction, easier configuration, and lower perceived operating burden, especially when clinical systems are already in place or when the office wants to avoid a full platform conversion. Over time, modular SaaS packaging is narrowing that gap, and that is gradually shifting more of the United States practice management system market toward integrated offers even in smaller practice settings.

By Component: Software Anchors Revenue, Services Signal Where Complexity Lives

Software accounted for 63.83% of component revenue in 2025, which reflects the central role of licensing, subscriptions, and core application access across provider organizations of every size. That installed software base remains the commercial foundation of the United States practice management system market because no practice can operate its scheduling, registration, billing, and reporting processes without a system of record and workflow control layer. Software revenue also stays elevated because buyers are adding AI-assisted coding, workflow orchestration, analytics, and patient communication capabilities inside the platform rather than through outside tools. As vendors bundle more functions into unified suites, software becomes harder to replace module by module, which supports retention and deeper account value. This is one reason the leading vendors continue to widen their product scope even when buyers say they want simpler technology estates.

Services are growing faster, at 9.34% CAGR through 2031, and that growth says more about implementation difficulty than about a reduced need for software. Managed revenue cycle services are expanding because many providers want direct support with claims workflows, denial management, collections, and operational change rather than a technology-only handoff. Training and support are also taking on a larger role because new AI and automation features alter work routines for front-desk staff, billers, and managers instead of merely adding another screen to the system. AdvancedMD, Veradigm, and CareCloud have all emphasized workflow-enhancing releases in 2026, which shows that successful deployment now depends on operating support as much as on technical availability. In effect, the United States practice management system industry is generating more service revenue because platform sophistication is rising faster than internal administrative capacity in many provider organizations.

By Delivery Mode: SaaS Becomes the Default, On-Premise Manages the Decline

Cloud-based/SaaS accounted for 57.12% of 2025 revenue and is projected to expand at 8.69% CAGR through 2031, which means this model leads on both scale and growth. That gives cloud delivery a strong claim on the United States practice management system market size because most new investments now prioritize recurring access, regular updates, and remote administration rather than local infrastructure. The appeal is strongest in multi-site physician groups, ambulatory networks, and hybrid-workflow organizations that need standardized operations across dispersed locations. CAQH’s findings on administrative AI adoption also reinforce this direction because cloud environments are better suited to rapid model updates, workflow changes, and shared configuration across sites. Vendors are also using cloud architecture to package redundancy, security controls, and faster deployment into the core offer rather than treating them as add-ons.

Web-based systems still retain a practical role where providers want browser access and lighter technical overhead without a deeper move into a broader SaaS operating model. On-premise deployments continue to lose share, but they have not disappeared because some integrated delivery networks still have existing server investments, and some specialties remain cautious about keeping certain workflows offsite. In behavioral health, reproductive medicine, and other privacy-sensitive settings, some buyers still prefer tighter local control over administrative and patient records even when that choice slows feature adoption. Even so, the replacement path is increasingly clear because vendor roadmaps, AI releases, and interoperability improvements are now being built first for cloud environments. The result is that the United States practice management system market is no longer debating whether SaaS will be the default model, but how quickly the remaining on-premise base will move once cost, security review, and workflow readiness align.

By Functionality: Billing Anchors Revenue but Telehealth Coordination Races Ahead

Billing, coding and claims management captured 33.28% of revenue in 2025, giving it the largest role across platform functions. That share reflects where provider pain is most visible because cash flow, denial recovery, and claim quality still determine whether a practice experiences administrative stability or daily revenue disruption. Kodiak Solutions and Premier both show why this remains the anchor function, with large and avoidable costs still tied to denials, adjudication, and rework. Appointment scheduling and registration, insurance eligibility and prior authorization workflow, and patient record tracking continue to matter because errors in those early steps often surface later as billing delays or payment denials. Reporting and analytics are also rising in importance because practices want easier visibility into denial trends, staff productivity, and payer bottlenecks. As a result, functionality breadth matters, but revenue still concentrates most heavily around claims-related operations.

Telehealth coordination is projected to grow at 9.02% CAGR through 2031, making it the fastest-expanding function in the report. CMS extended major Medicare telehealth flexibilities through December 31, 2027, which keeps virtual care scheduling, billing eligibility, and code management relevant to platform planning. Vendors are therefore embedding video visit launch, telehealth coding support, patient communication, and follow-up workflows directly into the administrative system instead of leaving them in separate tools. This is important for the United States practice management system market because telehealth coordination now sits closer to core office management than to a temporary pandemic-era add-on. In usage terms, the fastest-growing functions are no longer only those that process claims, but also those that connect virtual visits, patient communication, and documentation-ready billing workflows in one operating path.

By End User: Hospitals Lead, Pharmacies Accelerate, Physicians Hold the Volume Base

Hospitals and health systems held 40.23% of end-user revenue in 2025, which reflects their larger contract values, more complex scheduling structures, and wider payer management requirements. That level also represents a large share of the United States practice management system market size because enterprise accounts buy more modules, more services, and more interoperability support than smaller offices do. These organizations were also among the earliest adopters of embedded AI for denial prevention, documentation support, and workflow automation, which gives the enterprise tier outsized influence over vendor roadmaps. Epic’s Penny, athenahealth’s continuing athenaOne improvements, and Veradigm’s network architecture launch all align with the needs of larger buyers that want measurable operating outcomes from one vendor environment. Physician offices and physician back offices still form the broad account base by number of customers, but their per-site spending is lower and more sensitive to ease of use, price, and implementation burden.

Pharmacies are projected to expand at 8.94% CAGR through 2031, making them the fastest-growing end-user segment. Outcomes reported more than 6.5 million medication therapy management services in the first half of 2025 across the Outcomes network, up 21%, which helps explain why pharmacy-linked scheduling, eligibility verification, and claims workflows are becoming more relevant. Diagnostic laboratories and ambulatory settings continue to add steady demand as outpatient care volumes and specialized service models expand, but the standout growth signal is the movement of more clinical activity into pharmacy channels. athenahealth also found that physician comfort with AI reached 54% in 2026, up from 46% in 2025, which supports broader acceptance of automation-rich administrative tools across provider settings. That shift matters because adoption in the United States practice management system market depends not only on financial pressure, but also on whether end users trust the workflow changes tied to automation and AI.

Geography Analysis

The United States practice management system market is a single-country market, but demand patterns differ materially by region. The Northeast remains one of the most commercially important areas because it has a dense concentration of academic medical centers, large multispecialty groups, and sophisticated payer relationships that reward earlier adoption of integrated administrative systems. This region is also well aligned with interoperability investment because TEFCA participation has continued to broaden, with designated QHINs now linking more than 9,200 organizations and 41,000 unique endpoints. That matters for large provider organizations in referral-heavy networks because seamless exchange increasingly influences procurement decisions for administrative and revenue cycle platforms. The Northeast therefore remains a leading market for integrated systems, enterprise deployments, and early adoption of AI-linked workflow tools inside the United States practice management system market.

The South and Southeast represent the fastest organic expansion zone because population growth, ambulatory build-out, and physician group formation continue to widen the customer base. This geography is also exposed to heavier prior authorization complexity in many payer environments, which raises the value of workflow automation and FHIR-ready administrative tools under the CMS compliance calendar. The region is therefore favorable for cloud deployment, multi-site group administration, and vendors that can combine eligibility, scheduling, and claims workflows in one platform. In practical terms, that keeps the United States practice management system market strongest, where provider networks are expanding and where administrative friction quickly scales across many sites.

The Midwest and many rural corridors present a slower but still meaningful replacement opportunity. Budget pressure and limited internal IT capacity continue to delay some system changes, yet rural operators still need resilient cloud access, simpler maintenance, and stronger interoperability as they protect independence and extend service reach. MEDITECH reported in February 2026 that 15 rural hospitals selected MEDITECH Expanse in 2025 and that more than 250 rural sites are already on the platform, which shows that rural modernization is active even if it is uneven. Western and Pacific markets remain favorable for SaaS-first architecture and AI-linked product rollout because technology acceptance is stronger and buyers are more open to cloud-native operating models. athenahealth’s 2026 Physician Sentiment Survey found that 65% of Millennial physicians are comfortable with AI, versus 49% of Gen X and Boomer physicians, which helps explain why regions with younger physician mixes can adopt newer administrative workflows more quickly. Across all regions, the United States practice management system market is being shaped by the same core issues, but the pace of adoption still depends on provider scale, payer complexity, workforce readiness, and capital capacity.

Competitive Landscape

The United States practice management system market is moderately concentrated at the enterprise level and fragmented across smaller and specialty accounts. Epic, Oracle Health, athenahealth, and eClinicalWorks remain the most influential vendors in large-group and health-system buying cycles because they can offer broad workflow coverage, deeper integration, and stronger compliance credibility. At the same time, the market stays crowded below that tier, where specialty depth, lower switching friction, and price sensitivity allow a wider vendor set to remain relevant. This split structure means that concentration is visible in large accounts, while competitive variety remains high in independent physician offices, outpatient specialties, and narrower administrative use cases. The result is a market where leadership is clear in some customer groups, but no single vendor controls the full national field.

Strategy in 2025 and 2026 has centered on AI embedding, operational automation, and interoperability-led account expansion. Epic advanced that position with Penny for billing and denial avoidance and with broader agent-based workflow development inside its platform, reinforcing its push toward measurable administrative outcomes. athenahealth’s Spring 2026 athenaOne update added embedded revenue cycle and workflow improvements, which support its position in ambulatory and community-based provider environments. eClinicalWorks also launched new care management and healowIQ capabilities in 2026, showing that competitive differentiation is extending into point-of-care intelligence, chronic care coordination, and staff burden reduction. These moves show that vendors are competing less on the number of modules alone and more on whether the platform improves claims quality, staff output, and connected care execution.

Several targeted strategic moves also stand out in the United States practice management system market. Veradigm launched its Health Network Architecture in May 2026 to create a unified interoperability and AI layer across EHR, practice management, payer, and patient-facing assets, which strengthens its independent practice proposition. ModMed acquired Bonsai Health in April 2026 to expand automated patient engagement and self-scheduling across its specialty provider network, which sharpened its specialty-focused growth path. Waystar and Google Cloud reported in March 2026 that AltitudeAI had prevented over USD 15 billion in denied claims in less than a year and reduced denial appeal workflow time by 90%, which underlines how revenue cycle AI is becoming a stand-alone competitive lever and not just a supporting feature. Even with these advances, the broader United States practice management system market remains open enough that niche vendors can still grow when they serve specialty workflows, rural operating needs, or pharmacy-linked care models better than enterprise platforms do.

United States Practice Management System Industry Leaders

athenahealth

eClinicalWorks

Epic Systems Corporation

Oracle Health

Veradigm

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Veradigm launches Health Network Architecture, a unified interoperability and AI layer available across Veradigm EHR, Practice Management, Payerpath, and FollowMyHealth, with intelligent claim scrubbing and AI-assisted prior authorization planned for rollout throughout 2026.

- April 2026: ModMed acquires Bonsai Health, an agentic AI patient engagement platform, to accelerate automated patient reactivation and AI-driven self-scheduling across its network of nearly 50,000 specialty providers.

- April 2026: AdvancedMD launches eMAR solution integrated directly within its EHR platform for behavioral health, substance use disorder, and specialty clinical environments, extending its unified practice management suite.

- March 2026: Waystar and Google Cloud expand collaboration on agentic AI, with Waystar's AltitudeAI platform having prevented over USD 15 billion in denied claims in less than a year and reduced denial appeal time by 90%.

- March 2026: Oasis Health Partners acquires Premier Health, a revenue cycle management and practice operations services organization, to build a full-service platform for independent primary care with value-based care contracting and EMR modernization services.

United States Practice Management System Market Report Scope

The United States Practice Management System (PMS) market encompasses the ecosystem of software, hardware, and IT services utilized by healthcare providers to automate and streamline the administrative, financial, and operational workflows of medical practices.

The United States Practice Management System Market is segmented across multiple dimensions to reflect the diverse solutions available for healthcare providers. By product type, the market is divided into integrated practice management systems, which include EHR/EMR‑integrated systems, billing and revenue‑cycle‑integrated systems, patient engagement‑integrated systems, and e‑prescribing‑integrated systems, as well as standalone practice management systems. By component, the market includes software and services, with services further segmented into implementation and configuration, training and support, and managed revenue cycle services. In terms of delivery mode, solutions are offered as web‑based, cloud‑based/SaaS, or on‑premise platforms.

By functionality, systems cover appointment scheduling and registration, billing, coding and claims management, insurance eligibility and prior authorization workflows, patient record tracking and document management, reporting, analytics and dashboarding, patient engagement and communication, telehealth coordination, and e‑prescribing and referral management. Finally, by end user, adoption spans physician back offices/physician offices, hospitals and health systems, diagnostic laboratories, pharmacies, and ambulatory and other outpatient settings.

| Integrated Practice Management Systems | EHR / EMR-Integrated Systems |

| Billing and Revenue-Cycle-Integrated Systems | |

| Patient Engagement-Integrated Systems | |

| E-Prescribing-Integrated Systems | |

| Standalone Practice Management Systems |

| Software | |

| Services | Implementation and Configuration Services |

| Training and Support Services | |

| Managed Revenue Cycle Services |

| Web-Based |

| Cloud-Based / SaaS |

| On-Premise |

| Appointment Scheduling and Registration |

| Billing, Coding and Claims Management |

| Insurance Eligibility and Prior Authorization Workflow |

| Patient Record Tracking and Document Management |

| Reporting, Analytics and Dashboarding |

| Patient Engagement and Communication |

| Telehealth Coordination |

| E-Prescribing and Referral Management |

| Physician Back Offices / Physician Offices |

| Hospitals and Health Systems |

| Diagnostic Laboratories |

| Pharmacies |

| Ambulatory and Other Outpatient Settings |

| By Product | Integrated Practice Management Systems | EHR / EMR-Integrated Systems |

| Billing and Revenue-Cycle-Integrated Systems | ||

| Patient Engagement-Integrated Systems | ||

| E-Prescribing-Integrated Systems | ||

| Standalone Practice Management Systems | ||

| By Component | Software | |

| Services | Implementation and Configuration Services | |

| Training and Support Services | ||

| Managed Revenue Cycle Services | ||

| By Delivery Mode | Web-Based | |

| Cloud-Based / SaaS | ||

| On-Premise | ||

| By Functionality | Appointment Scheduling and Registration | |

| Billing, Coding and Claims Management | ||

| Insurance Eligibility and Prior Authorization Workflow | ||

| Patient Record Tracking and Document Management | ||

| Reporting, Analytics and Dashboarding | ||

| Patient Engagement and Communication | ||

| Telehealth Coordination | ||

| E-Prescribing and Referral Management | ||

| By End User | Physician Back Offices / Physician Offices | |

| Hospitals and Health Systems | ||

| Diagnostic Laboratories | ||

| Pharmacies | ||

| Ambulatory and Other Outpatient Settings | ||

Key Questions Answered in the Report

What is the projected value of the United States practice management system space by 2031?

It is forecast to reach USD 7.37 billion by 2031, rising from USD 5.08 billion in 2026 at a 7.73% CAGR over 2026-2031.

Which product type leads revenue in the United States practice management system market?

Integrated practice management systems lead with 61.87% of revenue in 2025 and are also the fastest-growing product type at 8.25% CAGR through 2031.

Why are providers replacing older administrative platforms now?

The strongest reasons are denial reduction, administrative cost control, interoperability compliance, and the need for connected billing and scheduling workflows. Hospitals lost USD 48.4 billion in 2025 from final denials and uncollected balances.

Which deployment model is gaining the most traction among providers?

Cloud-based/SaaS is the leading and fastest-growing delivery mode, with 57.12% share in 2025 and 8.69% CAGR through 2031, because it supports multi-site workflows, frequent updates, and better resilience planning.

Which functional area has the largest revenue base?

Billing, coding and claims management leads with 33.28% of 2025 revenue because it connects directly to cash flow, denial avoidance, and revenue recovery.

Page last updated on: