U.S. Acne Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 3.62 Billion |

| Market Size (2026) | USD 3.79 Billion |

| Market Size (2031) | USD 4.78 Billion |

| Growth Rate (2026 - 2031) | 4.75% CAGR |

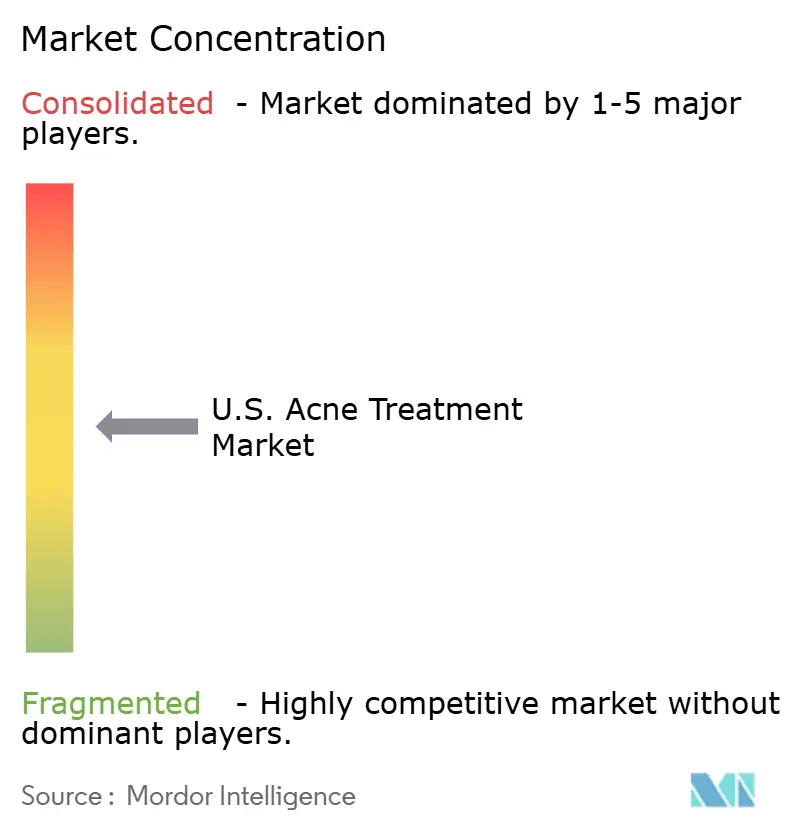

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Acne Treatment Market Analysis by Mordor Intelligence

The U.S. Acne Treatment Market size is expected to grow from USD 3.62 billion in 2025 to USD 3.79 billion in 2026 and is forecast to reach USD 4.78 billion by 2031 at 4.75% CAGR over 2026-2031.

Acne affects nearly 50 million individuals annually in the United States, providing a stable and diverse patient base across age groups for the acne treatment market.[1]American Academy of Dermatology, “Skin Conditions by the Numbers,” American Academy of Dermatology, aad.org By 2026, new product approvals, expanded use of combination regimens, and the shift of clinically validated retinoid combinations from prescription to OTC are transforming treatment approaches and intensifying competition in prescription and retail channels. The 2024 American Academy of Dermatology (AAD) guidelines are driving the market toward shorter antibiotic use, combination-based topical therapies, and increased reliance on non-antibiotic solutions.[2]R.V. Reynolds, “Guidelines of Care for the Management of Acne Vulgaris,” Journal of the American Academy of Dermatology, jaad.org This shift benefits fixed-dose brands and innovative topical platforms while addressing evolving patient needs. However, the market faces challenges from generic competition in mature categories and the growing influence of telehealth platforms on prescribing and fulfillment practices. The February 2026 update to the iPLEDGE Risk Evaluation and Mitigation Strategy (REMS) is expected to reduce access barriers for isotretinoin. This change is anticipated to support a gradual recovery in the tightly regulated segment of the United States acne treatment market during the later forecast years.[3]U.S. Food and Drug Administration, “iPLEDGE Risk Evaluation and Mitigation Strategy,” U.S. Food and Drug Administration, fda.gov

Key Report Takeaways

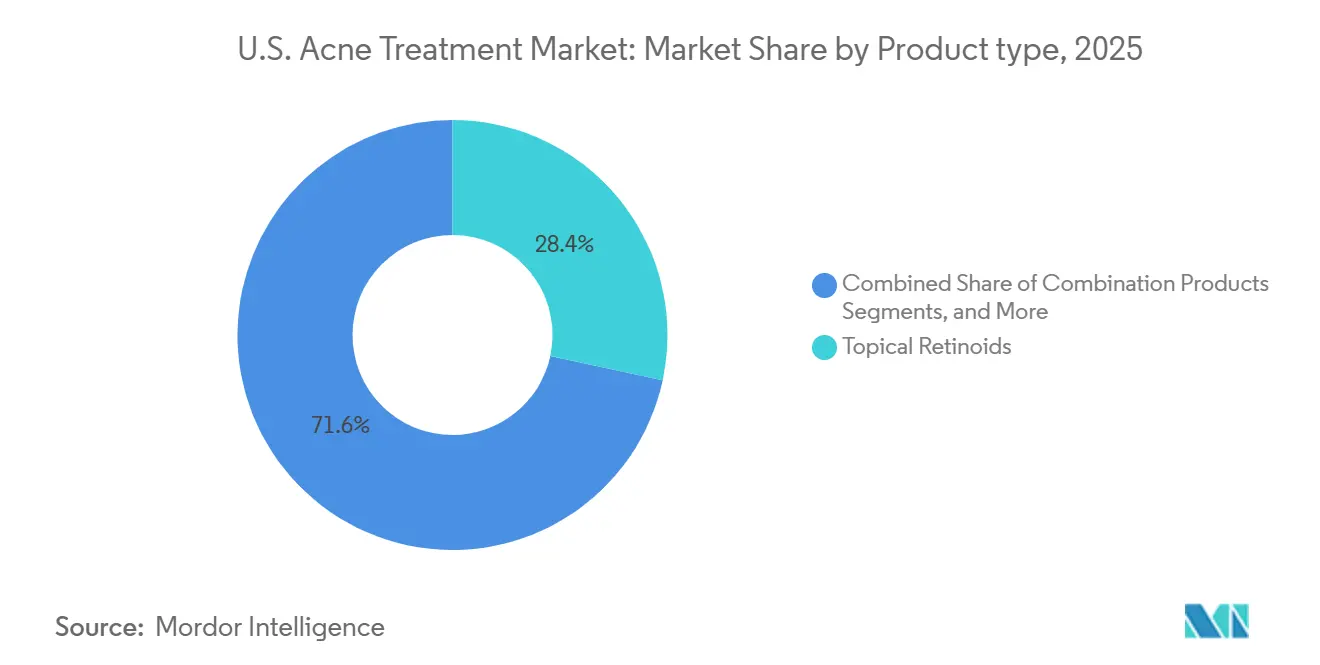

- By product type, topical retinoids held 28.35% share in 2025, while combination products are forecasted to expand at a 5.67% CAGR through 2031.

- By route of administration, topical formulations accounted for 63.76% share in 2025, while oral therapies are projected to grow at a 5.55% CAGR through 2031.

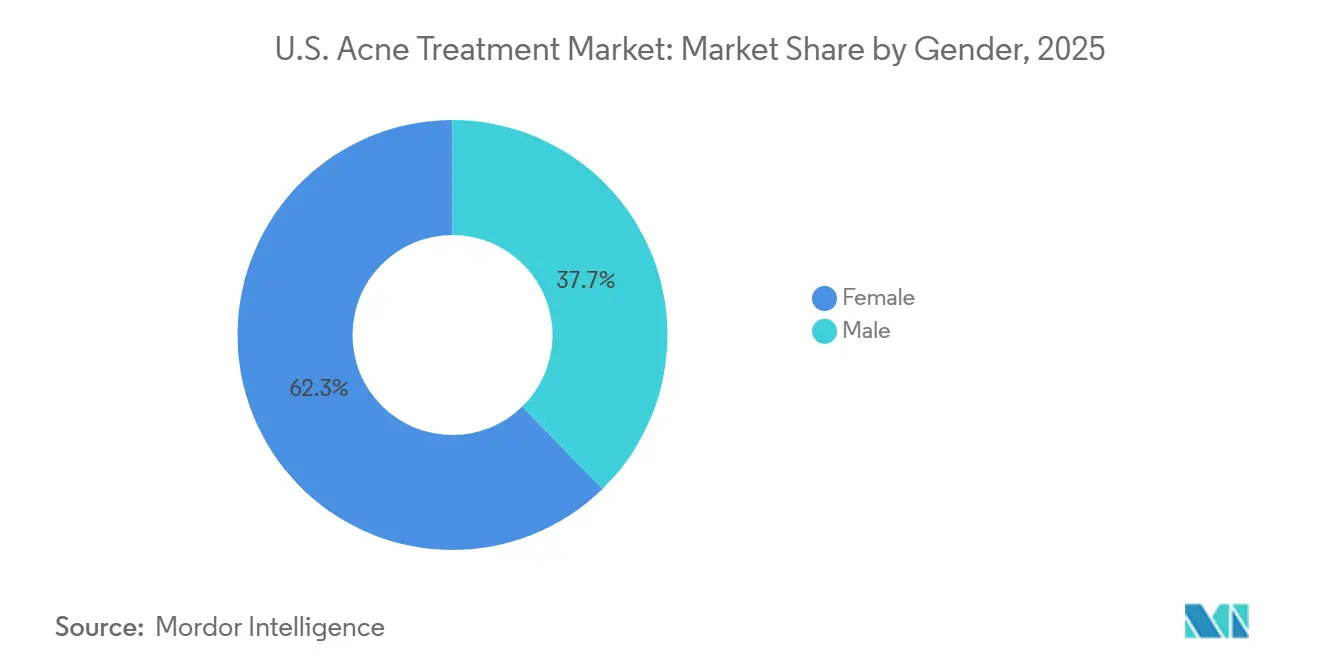

- By gender, female patients held 62.34% of the U.S. acne treatment market share in 2025, while the same segment is projected to record the fastest CAGR at 6.72% through 2031.

- By distribution channel, retail pharmacies accounted for 51.34% share in 2025, while online pharmacies are projected to expand at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Acne Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High prevalence across adolescents and adults | +1.3% | National | Short term (≤ 2 years) |

| Rising demand for combination therapy regimens | +0.9% | National, with stronger concentration in urban dermatology markets | Medium term (2-4 years) |

| Growth in female hormonal acne diagnosis | +0.7% | National, with higher prevalence in Northeast and Pacific coast metro areas | Medium term (2-4 years) |

| Expanding OTC access to acne therapies | +0.6% | National, with early gains in suburban and rural markets historically underserved by dermatologists | Short term (≤ 2 years) |

| Digital dermatology and tele-dermatology platforms | +0.5% | National, with concentration in telehealth-permissive states and areas with low dermatologist density | Short term (≤ 2 years) to Medium term (2-4 years) |

| Strong clinical preference for long-term management | +0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Prevalence Across Adolescents and Adults

Acne, the most common skin condition in the United States, affects approximately 50 million Americans annually, anchoring the acne treatment market to a broad recurring treatment base. While acne typically begins in adolescence, treatment demand now extends into adulthood, driven by repeat physician visits and long-term maintenance routines. This diverse patient base sustains demand for OTC products, prescription topicals, oral therapies, and maintenance regimens. The focus on quality-of-life improvements and newer formulations further strengthens market resilience, even amid generic competition.

Rising Demand for Combination Therapy Regimens

The United States acne treatment market is shifting toward combination therapies as clinicians seek regimens addressing multiple disease pathways in a single prescription. CABTREO's FDA approval and launch validated this trend, setting a benchmark for innovation. The 2024 AAD guidelines favor complementary mechanisms over antibiotic monotherapy, enhancing the appeal of fixed-dose combinations. The FDA's OTC approval for adapalene and benzoyl peroxide further expands access to dual-mechanism care, intensifying competition with single-agent products.

Growth in Female Hormonal Acne Diagnosis

Female demand is a key growth driver in the United States acne treatment market, with increasing attention on adult-onset and persistent acne in women. The 2024 AAD guidelines support hormone-linked treatments like spironolactone and clascoterone, encouraging broader use. Sun Pharma highlighted clascoterone's benefits, including sebum reduction and tolerability for diverse skin types. Female patients often require long-term management strategies, expanding the prescribing base to include gynecology, primary care, and telehealth alongside dermatology.

Expanding OTC Access to Acne Therapies

The FDA's approval for Differin Epiduo Acne Gel's OTC switch in May 2026 will significantly enhance treatment accessibility. Galderma plans to distribute the product through major retailers like Walmart, Ulta, Target, and Amazon by summer 2026. This transition positions a guideline-endorsed dual-mechanism product to compete directly with cosmetic acne solutions, encouraging treatment starts without dermatologist visits. The market is evolving, with OTC solutions gaining prominence for mild-to-moderate cases and specialists focusing on more severe conditions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Antibiotic stewardship pressure on oral and topical antibiotics | -1.2% | National | Medium term (2-4 years) |

| Irritation, dryness, and photosensitivity limitations | -0.9% | National, pronounced in Southern and Sun Belt states | Short term (≤ 2 years) to Medium term (2-4 years) |

| iPLEDGE and pregnancy-prevention compliance burden | -0.7% | National | Short term (≤ 2 years) |

| High out-of-pocket sensitivity for brand-name products | -0.6% | National, more acute in non-commercially insured populations | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Antibiotic Stewardship Pressure on Oral and Topical Antibiotics

The American Academy of Dermatology (AAD) in 2024 introduced stricter guidelines for acne treatment, capping systemic antibiotic use at 3 to 4 months and eliminating antibiotic monotherapy. These measures limit the growth of older oral and topical antibiotics in the United States acne treatment market. While doxycycline, minocycline, and clindamycin remain part of care pathways, their restricted use reduces repeat prescriptions and long-term revenue. The market is shifting toward combination therapies and non-antibiotic alternatives, driving value growth but constraining unit expansion in the antibiotic segment.

Irritation, Dryness, and Photosensitivity Limitations

Patient tolerability remains a challenge in the United States acne treatment market, as retinoids and benzoyl peroxide often cause irritation, dryness, and photosensitivity. These side effects, particularly during early treatment, can lead to poor adherence. The issue is more pronounced in high-UV regions, where maintaining sunscreen use is difficult, and sun exposure worsens discomfort. Patients with sensitive skin or a risk of post-inflammatory hyperpigmentation face additional challenges. While newer formulations improve tolerability, their higher costs impact both adherence and accessibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combination Products Disrupt a Retinoid-Led Market

Combination products are expected to grow at a 5.67% CAGR in the United States acne treatment market from 2026 to 2031, while topical retinoids held a 28.35% market share in 2025. This indicates a shift in the product mix, though retinoids remain central as first-line acne care and key ingredients in combination formulations. Topical retinoids maintain a strong position compared to older single-agent categories facing commoditization due to generics and OTC competition.

The shift toward combination products has been driven by CABTREO's prescription adoption and the Differin Epiduo OTC switch, increasing visibility of multi-ingredient care. Benzoyl peroxide retains volume presence but is now more valuable in premium combination products. Antibiotics remain relevant but face limited long-term roles as guidelines favor pairing and shorter usage. Innovation continues with Galderma's trifarotene expansion and Pfizer's Phase 1 acne study in 2025, targeting higher-value niches beyond mature topical categories.

By Route of Administration: Oral Uptake Accelerates Against a Large Topical Base

Topical formulations accounted for 63.76% of the United States acne treatment market in 2025, while oral therapies are projected to grow at a 5.55% CAGR through 2031. Topicals dominate due to their role in first-line care for mild-to-moderate cases, ensuring a durable volume base. However, growth is slowing as complex cases and adult patients shift to longer-duration oral management.

Oral therapies are gaining traction with high-value treatments requiring extended courses or greater clinical intensity, especially for patients unresponsive to topicals. The 2026 REMS update is expected to ease isotretinoin access by reducing testing barriers, benefiting patients reliant on systemic treatments and telehealth pathways. Oral growth is driven by patient value and continuity of use rather than broad volume expansion in older antibiotic categories.

By Gender: Female Segment Leads While Male Treatment Gap Presents Latent Opportunity

Female patients held 62.34% of the United States acne treatment market in 2025, with a projected 6.72% CAGR growth through 2031. This reflects the influence of adult female care, hormonal acne management, and extended treatment journeys. The 2024 AAD guidelines support this trend with recommendations for spironolactone, clascoterone, and combined oral contraceptives. Telehealth access and recognition of hormonal triggers further drive growth.

The male segment remains under-addressed, presenting opportunities for targeted growth later in the forecast period. Clascoterone, the only FDA-approved androgen receptor inhibitor for acne, offers a differentiated option for both genders. Strategic partnerships, such as those between Galderma and L'Oréal, could enhance male-focused product development. Female care remains the primary value driver, while male engagement offers untapped potential.

By Distribution Channel: Online Pharmacies Outgrow Retail While Clinical Channels Deepen

Retail pharmacies held a 51.34% share of the United States acne treatment market in 2025, while online pharmacies are projected to grow at a 7.12% CAGR through 2031. Retail remains dominant due to its combination of OTC products, generic prescriptions, and broad access. The 2026 OTC launch of Differin Epiduo at major retailers will further strengthen retail's position.

Online pharmacies are growing rapidly as telehealth platforms streamline consultation, prescription renewal, and fulfillment, creating recurring demand. Hims & Hers reported USD 2.35 billion in 2025 revenue, highlighting the expansion of digital care platforms. Hospital pharmacies and specialist clinics remain critical for severe acne and isotretinoin monitoring, but digital channels are reshaping patient loyalty and market dynamics.

Geography Analysis

In 2026, the United States acne treatment market, valued at USD 3.79 billion, remains a key player globally. This is driven by advanced dermatology infrastructure and diverse commercial opportunities across prescription, OTC, and telehealth channels. Urban hubs like the Northeast and Pacific coast dominate due to high dermatologist density, academic centers, and faster adoption of branded therapies. These regions also influence payer decisions and prescribing norms, making them critical for launching premium products, innovative topicals, and advanced retinoid strategies.

In rural states and parts of the South, limited dermatologist access shifts acne care reliance to primary care and retail pharmacies. This increases exposure to generics, OTC substitutes, and delays in specialist treatments. High UV exposure in Sun Belt states complicates adherence to retinoids and benzoyl peroxide due to irritation and photosensitivity. The 2026 OTC switch for adapalene and benzoyl peroxide, along with telehealth expansion, is expected to narrow this access gap.

State-level payer variations add complexity to the United States acne treatment market, as insurance mix impacts access to branded products and specialist visits. Commercially insured populations adopt newer branded therapies more readily, while Medicaid-reliant and uninsured patients often turn to generics and OTC options. The Midwest remains a stable volume base, supported by employer-sponsored insurance and balanced urban and rural demand, though it is slower to adopt premium innovations.

Competitive Landscape

The United States acne treatment market is moderately concentrated at the branded prescription level. Galderma, Bausch Health, and Sun Pharmaceutical lead the branded segment, while numerous generic suppliers maintain pricing pressure in established categories. Galderma reported global net sales of USD 5.21 billion for 2025, driven by its focus on prescription dermatology, consumer dermatology, and the planned OTC switch for Differin Epiduo in May 2026. Bausch Health strengthened its position with CABTREO, a triple-combination product aligning with the shift toward multi-mechanism therapy. Sun Pharma remains competitive with WINLEVI and an enhanced generics portfolio following the Taro merger. These companies compete by emphasizing mechanism differentiation, tolerability, access, and channel control.

Galderma made two key strategic moves. It transitioned Differin Epiduo to OTC status in May 2026, expanding consumer access and reshaping competition in retail and e-commerce. Additionally, its 2024 stake acquisition in L'Oréal, with a planned increase announced in December 2025, links professional dermatology expertise with large-scale consumer skin science capabilities. Sun Pharma enhanced its market position by completing the Taro merger in June 2024, strengthening its ability to compete in both branded and generic acne care.

Telehealth platforms are reshaping competition by influencing consultations, refill behaviors, and product fulfillment. Hims & Hers exemplifies this trend, with its 2025 revenue highlighting the growing relevance of these platforms in recurring dermatology demand. Companies now compete on product efficacy and the ease of initiating, refilling, and maintaining therapy. Opportunities remain in products designed for skin-of-color tolerability, male-specific acne needs, and digital adherence tools that improve outcomes and support payer discussions.

U.S. Acne Treatment Industry Leaders

Galderma Group AG

AbbVie Inc.

Bausch Health Companies Inc.

Bausch + Lomb Corporation

Hims & Hers Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Galderma received U.S. FDA approval to switch Differin Epiduo Acne Gel from prescription-only to OTC, targeting patients aged 12 and older, with retail availability starting summer 2026.

- February 2026: The FDA approved updates to the iPLEDGE program for isotretinoin, allowing home pregnancy testing and removing the need for CLIA-certified lab tests, effective within 180 days.

- December 2025: L'Oréal Groupe announced plans to increase its stake in Galderma by 10%, raising its total ownership to 20%.

- June 2025: Sun Pharma completed its merger with Taro, strengthening its position in dermatology generics and acne treatments.

U.S. Acne Treatment Market Report Scope

As per the scope of the report, acne treatments are medications and skincare therapies designed to clear existing blemishes, stop new pimples from forming, and prevent scarring. They work by targeting the four main causes of acne: excess oil (sebum), clogged pores (hyperkeratinization), bacteria, and inflammation.

The U.S. acne treatment market is segmented by product type, route of administration, gender, and distribution channel. By product type, the market includes topical retinoids, benzoyl peroxide, topical antibiotics, oral antibiotics, isotretinoin, hormonal therapies, combination products, and other acne therapies. By route of administration, the market is segmented into topical and oral. By gender, the market is categorized into female and male. By distribution channel, the market is segmented into retail pharmacies, hospital pharmacies, online pharmacies, and dermatology clinics and med spas. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Topical Retinoids |

| Benzoyl Peroxide |

| Topical Antibiotics |

| Oral Antibiotics |

| Isotretinoin |

| Hormonal Therapies |

| Combination Products |

| Other Acne Therapies |

| Topical |

| Oral |

| Female |

| Male |

| Retail Pharmacies |

| Hospital Pharmacies |

| Online Pharmacies |

| Dermatology Clinics and Med Spas |

| By Product Type | Topical Retinoids |

| Benzoyl Peroxide | |

| Topical Antibiotics | |

| Oral Antibiotics | |

| Isotretinoin | |

| Hormonal Therapies | |

| Combination Products | |

| Other Acne Therapies | |

| By Route of Administration | Topical |

| Oral | |

| By Gender | Female |

| Male | |

| By Distribution Channel | Retail Pharmacies |

| Hospital Pharmacies | |

| Online Pharmacies | |

| Dermatology Clinics and Med Spas |

Key Questions Answered in the Report

What is the current size of the U.S. acne treatment market?

The U.S. acne treatment market stands at USD 3.79 billion in 2026 and is projected to reach USD 4.78 billion by 2031 at a 4.75% CAGR.

Which product category leads acne treatment sales in the United States?

Topical retinoids led product demand with a 28.35% share in 2025, supported by their first-line role in treatment and their use inside combination products.

Which segment is growing fastest in U.S. acne treatment?

Combination products are the fastest-growing product type at a 5.67% CAGR, and online pharmacies are the fastest-growing distribution channel at a 7.12% CAGR through 2031.

Why are female patients driving more growth in acne care?

Female patients held 62.34% of market value in 2025 and are projected to grow at a 6.72% CAGR, supported by stronger focus on hormonal acne and broader access to ongoing treatment.

How is telehealth changing acne treatment in the United States?

Telehealth is shifting demand toward online pharmacies and subscription refill models, which makes treatment access easier and supports recurring prescription fulfillment.

What recent regulatory change could improve isotretinoin access?

The February 2026 iPLEDGE update allows home pregnancy testing and removes mandatory CLIA-certified lab testing, which should reduce treatment friction over time.

Page last updated on: