Anti Acne Cosmetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.52 Billion |

| Market Size (2031) | USD 8.28 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

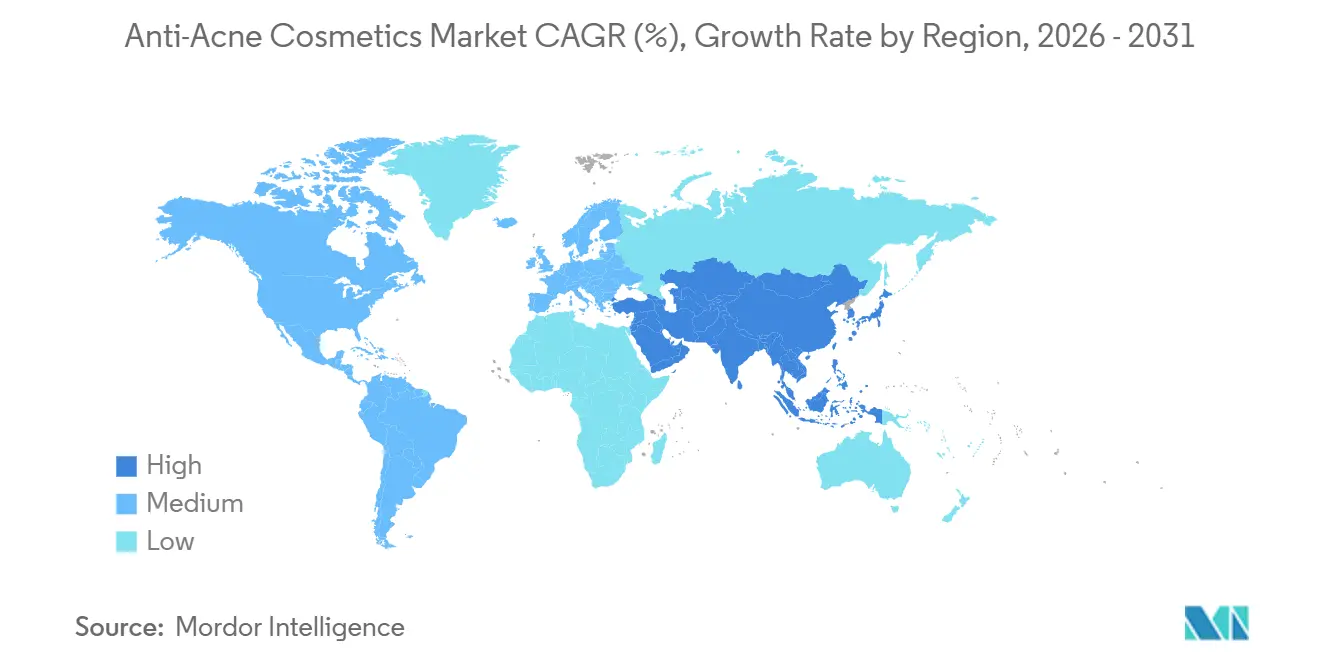

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

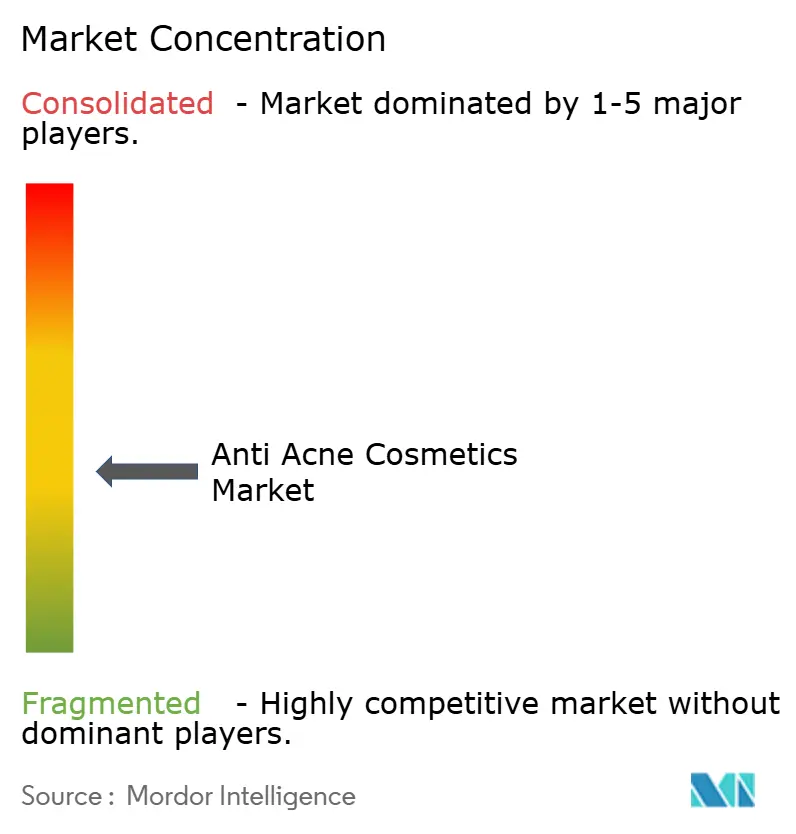

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti Acne Cosmetics Market Analysis by Mordor Intelligence

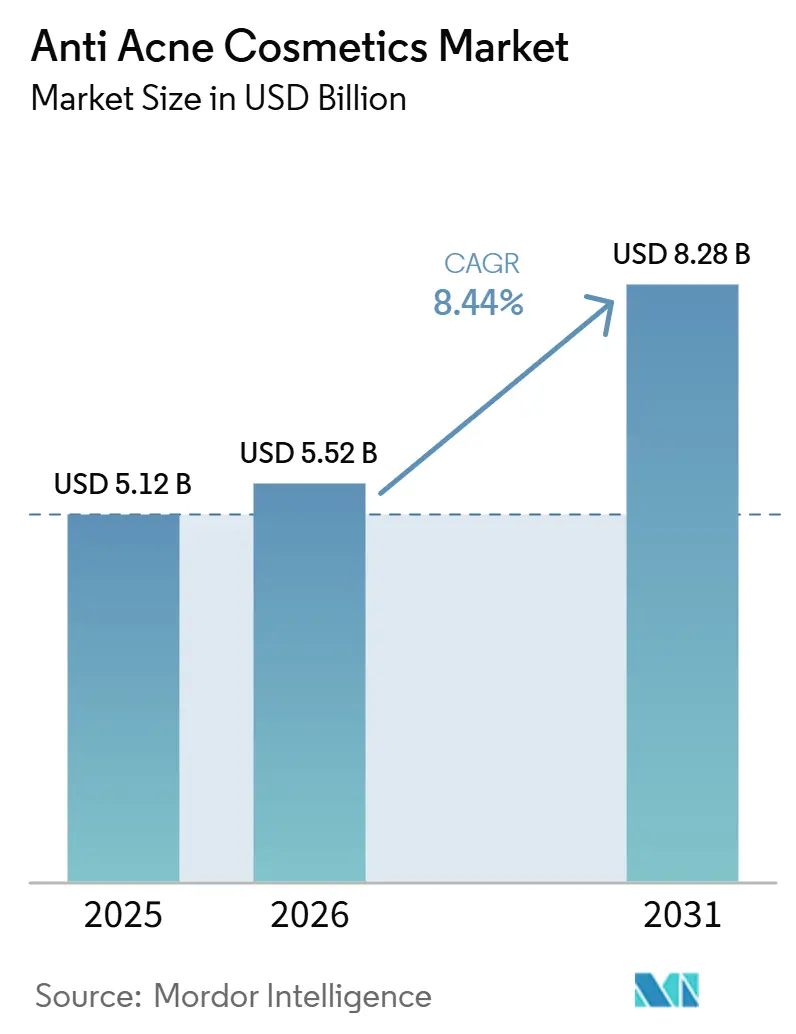

The Anti Acne Cosmetics Market size was valued at USD 5.12 billion in 2025 and is estimated to grow from USD 5.52 billion in 2026 to reach USD 8.28 billion by 2031, at a CAGR of 8.44% during the forecast period (2026-2031).

The anti-acne cosmetics market is benefiting from a broader acne care population, as the Global Burden of Disease study reported 184.3 million prevalent acne cases among people aged 10-24 in 2021, while post-adolescent acne in adults aged 25-49 is also rising and is projected to continue increasing through 2050. This change extends the anti-acne cosmetics market well beyond teenage use and supports steady demand for daily maintenance formats, gentle formulations, and premium treatment routines. Competitive activity in the anti-acne cosmetics market is also moving closer to clinical dermatology, with L'Oréal deepening its Galderma stake and expanding through Dr.G and Medik8 acquisitions, while Galderma is widening over-the-counter access with its 2026 Differin Epiduo approval. At the same time, ingredient safety scrutiny has become more visible after the FDA found elevated benzene levels in 6 benzoyl peroxide products in March 2025, which is pushing the anti-acne cosmetics market toward more stable alternatives and more careful formulation choices. The anti-acne cosmetics market is also being supported by stronger demand for multi-function, skin-barrier friendly products that combine acne control with lower irritation and better routine compatibility.

Key Report Takeaways

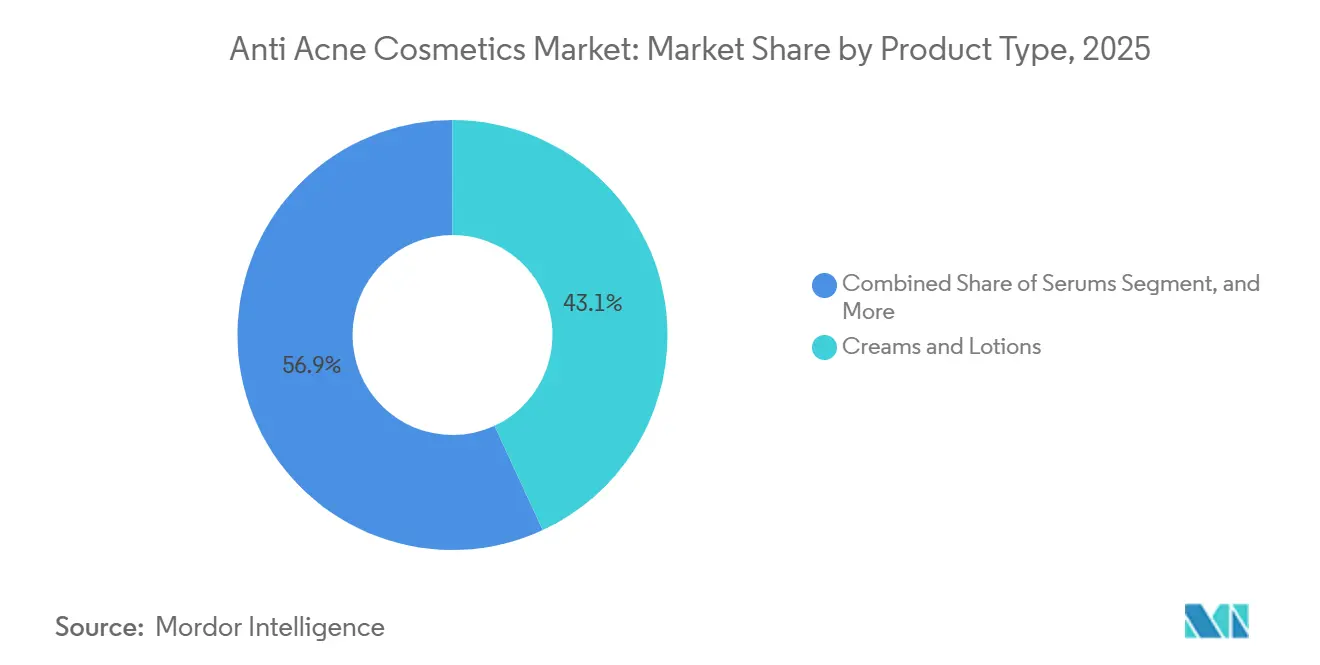

- By product type, creams and lotions led with 43.13% revenue share in 2025, while serums are projected to grow at 8.78% CAGR through 2031.

- By active ingredient, salicylic acid held 37.38% share in 2025, while tea tree oil is forecast to expand at 10.42% CAGR through 2031.

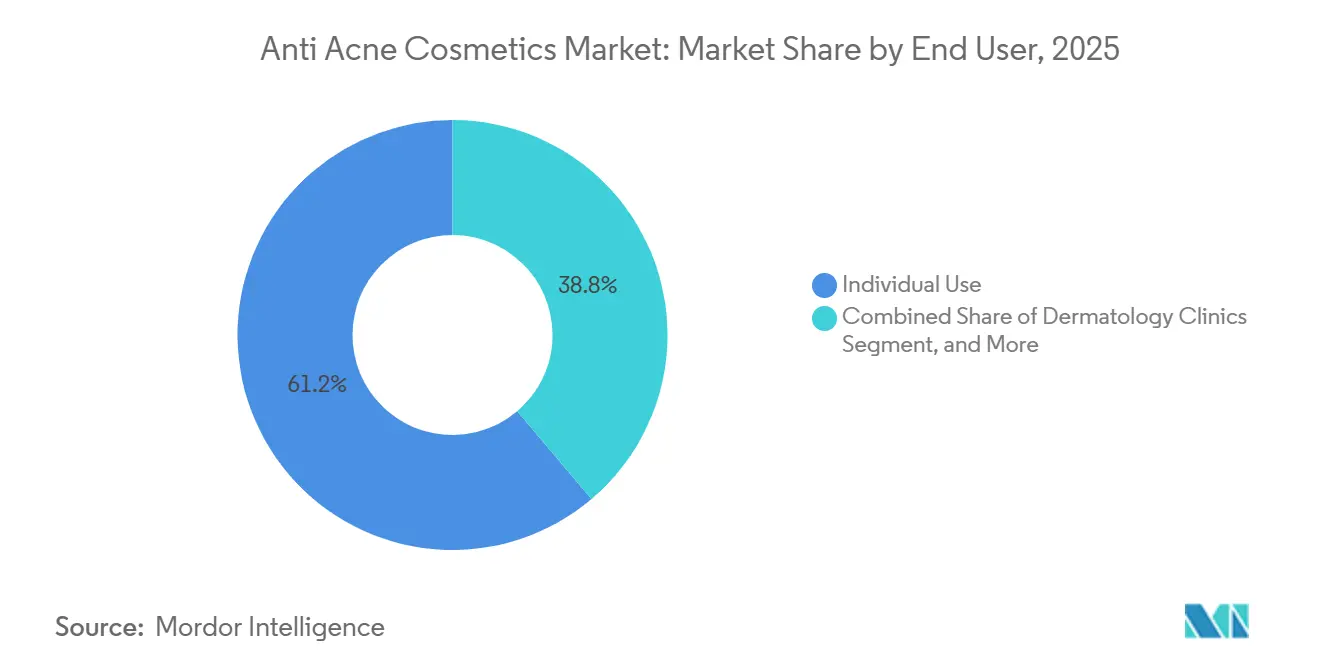

- By end user, individual use accounted for 61.16% share in 2025, while medspas and aesthetic clinics are projected to grow at 9.83% CAGR through 2031.

- By gender, women held 53.26% share in 2025, while men are forecast to grow at 9.02% CAGR through 2031.

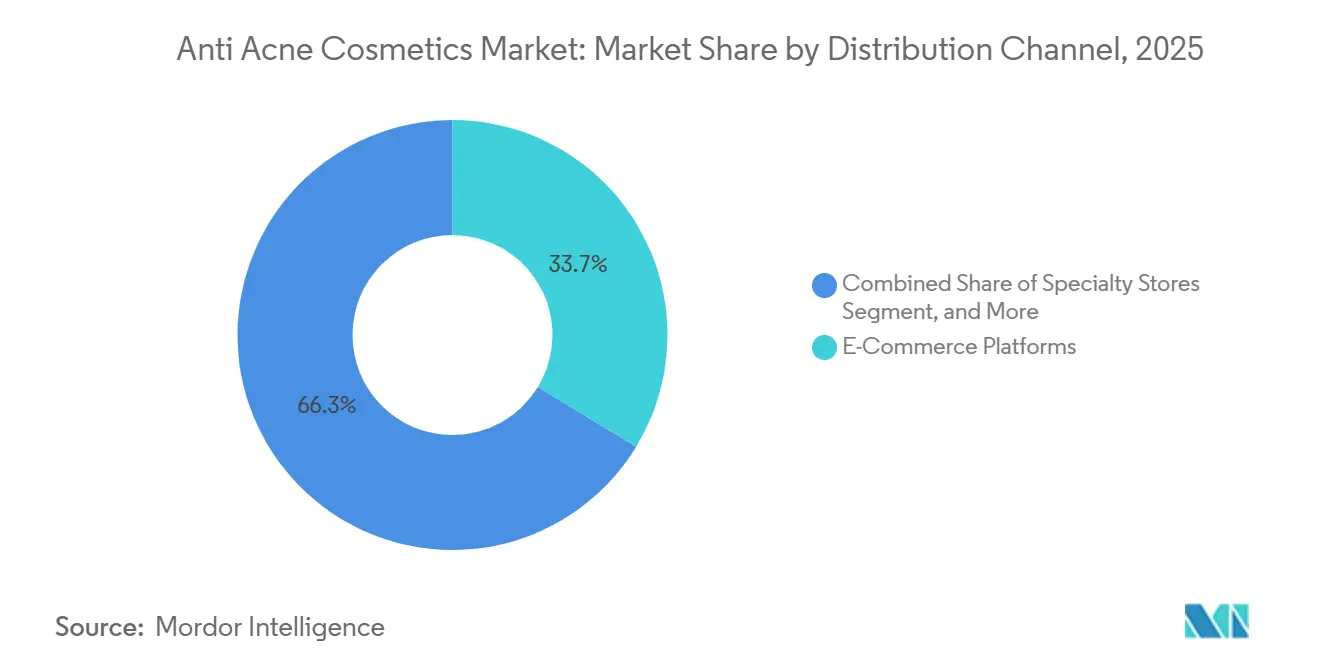

- By distribution channel, e-commerce platforms captured 33.72% share in 2025, while dermatology clinics are expected to expand at 10.11% CAGR through 2031.

- By geography, North America held 45.63% share in 2025, while Asia-Pacific is projected to grow at 9.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Anti Acne Cosmetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Acne Incidence Across Teen and Adult Populations | +1.8% | Global, with the highest burden in Western Europe and North America and faster increases in lower-middle SDI regions | Long term (≥ 4 years) |

| Premiumization of Clinically Validated Dermocosmetic Formulas | +1.5% | North America and Europe, with uptake accelerating in Asia-Pacific | Medium term (2-4 years) |

| E-Commerce Discovery and Social Commerce Conversion | +1.2% | Global, with strong relevance in North America and Asia-Pacific | Short term (≤ 2 years) |

| Demand for Multi-Functional, Skin-Barrier Friendly Products | +1.0% | Global, with stronger relevance in North America, Europe, and South Korea | Medium term (2-4 years) |

| Rising Male Grooming and Adult Acne Care Adoption | +0.8% | North America, Europe, South Korea, and India | Medium term (2-4 years) |

| Urban Pollution, Mask Use, and Stress-Linked Breakouts | +0.6% | Asia-Pacific, with spillover into the Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Acne Incidence Across Teen and Adult Populations

The anti-acne cosmetics market is expanding because the acne care population is changing in both size and age profile. The Global Burden of Disease study reported an age-standardized acne prevalence rate of 9,790.5 per 100,000 among people aged 10-24 in 2021, up from 8,563.4 in 1990, with 184.3 million prevalent cases in that younger cohort. Separate research on adults aged 25-49 showed that post-adolescent acne is rising and is projected to continue increasing through 2050, with women carrying a higher burden across ages. In the United Kingdom, the British Association of Dermatologists reported that 14.6% of adolescents and young people had been diagnosed with acne by 2021, which was 7.4% higher than in 1990.[1]British Association of Dermatologists, “Diagnosis of Acne on the Rise in the UK and Globally Since 1990,” British Association of Dermatologists, bad.org.uk This pattern matters because adult consumers usually look for clinically supported and lower-irritation routines rather than basic teenage spot care. It also gives the anti-acne cosmetics market a broader premium customer base in countries where persistent adult acne is already pronounced, including Germany, which the adult acne study identified as having the highest age-standardized prevalence rate globally.

Premiumization of Clinically Validated Dermocosmetic Formulas

The anti-acne cosmetics market is also moving toward products that promise prescription-like credibility in consumer-friendly formats. Galderma received FDA approval in May 2026 for Differin Epiduo Acne Gel for over-the-counter use in patients aged 12 and older, making it the first prescription-to-OTC switch for this adapalene and benzoyl peroxide combination in the United States.[2]Galderma, “Galderma Receives U.S. FDA Approval for Differin Epiduo Acne Gel Prescription-to-OTC Switch,” BioSpace, biospace.com The company stated that the product is supported by more than 10 clinical studies and more than 3,200 patient data points, which raises the efficacy bar for the wider OTC aisle once the product reaches Walmart, Ulta, Target, and Amazon. This shift favors brands that can fund trials, secure dermatologist endorsement, and explain active systems in a clear way across both physical and digital shelves. It also supports higher value growth in the anti-acne cosmetics market because consumers are showing willingness to pay for products that feel closer to dermatology than to mass beauty.

E-Commerce Discovery and Social Commerce Conversion

The anti-acne cosmetics market has become more responsive to online discovery because acne care products lend themselves well to routine-based education and visible use cases. E-commerce also led the distribution mix in 2025 with 33.7% share, which shows that online channels are already central to the anti-acne cosmetics market. Acne patches, cleansers, and serums are especially well-suited to short-format demonstrations because the value proposition is easy to explain through steps, textures, and repeated use. That environment helps agile brands move faster than traditional mass brands when they need to adapt packaging, messaging, or product format to what performs well online. It also shortens the path from awareness to first purchase because product education, reviews, and checkout now sit in the same consumer flow. Over time, that gives the anti-acne cosmetics market a stronger repeat-purchase loop, since users often return to the same product once they find a routine that balances visible results with tolerability.

Demand for Multi-Functional, Skin-Barrier Friendly Products

The anti-acne cosmetics market is being reshaped by products that treat breakouts while protecting the skin barrier. Kiehl's launched its Gently Effective Acne-Treating Cleansing Paste in June 2025 as a triple-use product that works as a cleanser, overnight spot treatment, and face mask. Revance expanded PanOxyl in August 2025 with a salicylic acid Acne Gel Wash and Daytime Invisible Patches that include Centella Asiatica and green tea extract, which points to a stronger focus on soothing support alongside active treatment. Unilever also published skin microbiome research in 2025 across Dove, Pond's, Vaseline, and Dermalogica, which shows that large consumer groups now see barrier health and microbiome balance as part of mainstream product development rather than niche add-ons.[3]Unilever, “How Unilever's Pioneering Skin Microbiome Research Is Shaping Product Innovation,” Unilever, unilever.com A 2024 clinical study in the Journal of Clinical and Aesthetic Dermatology found that a dermocosmetic serum with a multi-acid complex and niacinamide was effective and well tolerated in Japanese women with mild acne. As a result, the anti-acne cosmetics market is rewarding brands that can combine visible acne control with daily comfort, lower irritation, and simpler routines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skin Irritation and Sensitization Risks from Active Ingredients | -0.8% | Global; higher sensitivity in East & Southeast Asia | Short to medium term (≤ 3 years) |

| Regulatory Scrutiny on Acne Claims and Ingredient Safety | -0.5% | North America, EU, Global OTC jurisdictions | Medium to long term (2–5 years) |

| Price Sensitivity in Premium Dermocosmetic Tiers | -0.4% | South America, MEA, Southeast Asia; secondary pressure in NA & Europe | Medium term (2–4 years) |

| Slow-Perceived Efficacy Versus Instant-Claim Alternatives | -0.3% | Global; acute in APAC and North American Gen Z/Millennial segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skin Irritation and Sensitization Risks from Active Ingredients

The anti-acne cosmetics market still faces a clear tolerability challenge because stronger efficacy is often associated with dryness, irritation, or user drop-off. This issue became more visible in March 2025 when the FDA tested 95 benzoyl peroxide products and found elevated benzene levels in 6 products, which led to voluntary retail-level recalls. The event widened consumer concern beyond the recalled lots and brought more attention to ingredient stability, storage, and degradation risk across the anti-acne cosmetics market. Research published in Frontiers in Pediatrics in 2025 also described the thermal instability of benzoyl peroxide as a structural formulation issue rather than a one-time manufacturing problem. This makes formulation expertise more important, and it favors brands that can stabilize actives or shift consumers toward effective options with lower perceived irritation and lower degradation risk.

Regulatory Scrutiny on Acne Claims and Ingredient Safety

The anti-acne cosmetics market is also constrained by tighter rules around nonprescription use, ingredient claims, and supporting documentation. In the United States, OTC acne treatment sits inside a defined regulatory framework, and any active or pathway outside those boundaries can require a much longer development route. The FDA's December 2024 final rule on additional conditions for nonprescription use created a new regulatory category that may affect future prescription-to-OTC switches beyond adapalene and benzoyl peroxide combinations. In Europe, separate cosmetics compliance expectations still add labeling and safety work for brands that want to keep one anti-acne portfolio active across regions. The result is that launch timelines can stretch, clinical positioning becomes more expensive, and the anti-acne cosmetics market keeps a structural advantage for companies with experienced regulatory teams and broader scientific infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Creams and Lotions Lead While Serums Extend Premium Growth

Creams and lotions accounted for 43.13% share of the anti-acne cosmetics market size in 2025, making them the leading product type by revenue. The anti-acne cosmetics market favors these leave-on formats because they keep active ingredients in contact with the skin for longer periods and fit daily routines more easily than occasional treatments. Cleansers and face wash still generate high purchase frequency because they are used every day and are widely available across pharmacies, mass retail, and online channels. Spot treatments remain important for targeted use, while masks and toners continue to serve as add-on products for consumers who want periodic intensification within a larger acne routine.

Serums are projected to grow at 8.78% CAGR through 2031, making them the fastest-expanding product format in the anti-acne cosmetics market. A 2024 clinical study in the Journal of Clinical and Aesthetic Dermatology showed that a dermocosmetic serum with a multi-acid complex and niacinamide was effective and well-tolerated in Japanese women with mild acne. That supports the shift toward lightweight, layerable, and clinically positioned products that fit both adult acne management and sensitive-skin routines. The serum format also gives brands room to combine acne-focused actives with calming and barrier-support ingredients, which strengthens premium positioning without forcing every product into a classic drug-style presentation.

By Active Ingredient: Salicylic Acid Holds the Base While Tea Tree Oil Leads Expansion

Salicylic acid held 37.38% share in 2025, which kept it at the center of the anti-acne cosmetics market by active ingredient. Its position reflects a long commercial history and a good fit with oily and comedonal acne, where follicular penetration and routine-friendly use matter. A 2025 paper in Biosciences Biotechnology Research Asia also highlighted salicylic acid's role in post-acne hyperpigmentation management, which expands its value beyond lesion control for consumers who are also concerned about residual marks. Benzoyl peroxide remains important, but the FDA's 2025 benzene findings put short-term pressure on trust and may redirect some demand toward salicylic acid, retinoid, and other alternatives.

Tea tree oil is projected to grow at 10.42% CAGR through 2031, making it the fastest-growing active in the anti-acne cosmetics market. A 2025 review in Future Journal of Pharmaceutical Sciences described plant-derived antimicrobials such as tea tree oil, propolis, and willow bark as scientifically supported candidates for anti-acne cosmeceutical formulation. That matters because more consumers are looking for lower-irritation and more natural-feeling acne solutions, especially after heightened scrutiny around harsh synthetic actives. The shift does not remove the role of traditional actives, but it does widen the room in the anti-acne cosmetics market for brands that can translate plant-based efficacy into credible daily-use products.

By End User: Individual Use Dominates While Medspas Build a Stronger Professional Role

Individual use accounted for 61.16% of the 2025 anti-acne cosmetics market, which confirms that at-home regimens remain the core end-user base. This dominance reflects broad OTC availability, repeat replenishment across cleansers and leave-on products, and a consumer habit of managing acne through ongoing routines rather than one-time interventions. The anti-acne cosmetics industry also benefits when users can build routines step by step, since each added product can increase annual spending without requiring a clinic visit. Clinics and specialty beauty settings still influence demand, especially when consumers want stronger guidance, more confidence in product choice, or a bridge between consumer skincare and professional treatment.

Medspas and aesthetic clinics are projected to grow at 9.83% CAGR through 2031, which makes them the fastest-growing end-user group in the anti-acne cosmetics market. Their appeal comes from bundled services such as peels, microneedling, and light-based care, which create a natural setting for attached retail sales and maintenance products. This channel sits between medical authority and service convenience, so it appeals to consumers who want visible intervention but still expect routine-based home care. Galderma's 2026 OTC switch for Differin Epiduo may move some mild and moderate users toward self-management, which can push professional settings to focus more heavily on complex cases and combination protocols.

By Gender: Women Lead Current Demand While Men Offer Faster Growth

Women held 53.26% of the 2025 anti-acne cosmetics market, which reflects both a higher diagnosed burden and stronger routine participation. The Global Burden of Disease study reported that age-standardized acne prevalence among women aged 10-24 was higher than among age-matched males in 2021, at 10,911.8 per 100,000 versus 8,727.8 per 100,000. Adult female acne often requires products that can be used for longer periods without weakening the skin barrier, which supports premium dermocosmetic formats and gentle leave-on regimens. That is one reason clinically endorsed brands have done well in the anti-acne cosmetics market, especially when they can combine tolerability with visible efficacy.

Men are projected to grow at 9.83% CAGR through 2031, which makes them the fastest-growing gender cohort in the anti-acne cosmetics market. This segment still has room to move from sensory-led positioning toward more clinical and performance-led treatment claims. Products built around oil control, salicylic acid support, and short routine steps are especially relevant because they fit common male use habits without adding too much regimen complexity. As male skincare becomes more normalized, the anti-acne cosmetics market has more room for targeted communication, clearer active systems, and a stronger product mix built specifically for this user group.

By Distribution Channel: E-Commerce Leads the Current Mix While Clinics Grow the Fastest

E-commerce platforms held 33.72% of the anti-acne cosmetics market share in 2025, which made online retail the largest channel by value. That lead reflects the privacy of online shopping, easier product comparison, broad review access, and the ability to discover a full acne routine in one session. The anti-acne cosmetics market also fits online behavior because consumers often research ingredients, compare before-and-after narratives, and repurchase on a predictable cycle once a routine works. Pharmacies and drugstores remain important because they carry clinical cues, trusted shelf environments, and a stronger role for pharmacist guidance in first-line acne care.

The anti-acne cosmetics market size for dermatology clinics is projected to expand at 10.11% CAGR through 2031, making clinics the fastest-growing channel. Direct dispensing at the consultation point allows more personalized protocols and gives dermatologists a stronger role in product selection and routine compliance. Specialty stores continue to bridge the gap between mass beauty and professional skincare by offering stronger education and better merchandising for ingredient-led brands. Supermarkets and hypermarkets still matter for basic accessibility, but the anti-acne cosmetics market is gradually shifting toward channels that convey more clinical credibility and more informed product choice.

Geography Analysis

North America held 45.63% of the anti-acne cosmetics market share in 2025, which kept it as the largest regional contributor. The region benefits from a deep OTC structure, strong dermatologist engagement, and a retail landscape that rewards brands with clinical stories and wide availability. Galderma's May 2026 approval for Differin Epiduo OTC use is especially important for the anti-acne cosmetics market in North America because it extends a prescription-heritage product into major retail chains and online channels. Canada supports regional stability, while Mexico adds a faster-growth angle as skincare spending and online access continue to improve.

Europe remained the second-largest region in the anti-acne cosmetics market, supported by a high disease burden and strong demand for pharmacy-led skincare. The adult acne burden is especially relevant in Germany, which the post-adolescent acne study identified as having the highest age-standardized prevalence rate globally. That demand profile supports clinically positioned products and helps explain the durable role of professional and pharmacist recommendations in the regional mix. Europe also favors larger players because regulatory expectations around claims, safety files, and classification reward companies with stronger compliance resources. Beiersdorf's 2025 Eucerin launch in Japan shows how European dermocosmetic brands are also using their formulation credibility to grow well beyond home markets.

Asia-Pacific is projected to grow at 9.46% CAGR through 2031, making it the fastest-growing region in the anti-acne cosmetics market. The region benefits from large consumer pools, rising urban stressors, and a high level of skincare engagement that supports repeat use. South Korea remains important because clinically styled skincare routines and dermocosmetic aesthetics from that market continue to influence product expectations across the region. L'Oréal's 2024 acquisition of Dr.G and its 2025 acquisition of Medik8 also show that major groups view clinical skincare capability and Asia-linked growth as closely connected priorities. India strengthens the regional outlook because dermatologist-approved products are reaching more consumers through expanding digital retail access and broader awareness of active-based acne care.

Competitive Landscape

The anti-acne cosmetics market is moderately concentrated at the upper tier, with large dermatology and beauty groups setting the tone on clinical credibility, scale, and channel access. L'Oréal, Beiersdorf, Unilever, Galderma, Johnson & Johnson, and Shiseido hold strong positions because they combine recognized brands with broader scientific resources and international distribution. L'Oréal's move to increase its Galderma stake to 20% by December 2025 deepened a structure that links beauty scale with dermatology science in a way few rivals can match. Galderma's May 2026 OTC approval for Differin Epiduo further widened that clinical edge by moving a prescription-heritage treatment into mass retail and e-commerce. In practical terms, the anti-acne cosmetics market now rewards players that can translate medical-style efficacy into formats that still feel easy to buy and use every day.

Competitive differentiation in the anti-acne cosmetics market is moving toward better delivery systems, gentler routines, and data-backed formulation design. L'Oréal's April 2026 partnership with the Institut Pasteur is a long-term move to discover next-generation skin health actives, including work relevant to acne-related conditions. Unilever's 2025 skin microbiome research shows how large consumer groups are using proprietary skin data to shape new acne care concepts across multiple brands. Kiehl's and PanOxyl both launched acne products in 2025 that combine active treatment with multi-function use or barrier-soothing support, which reflects a wider shift toward easier and gentler routines. These moves show that the anti-acne cosmetics market is not only about stronger actives, but also about making those actives more compatible with daily consumer habits.

The clearest white space in the anti-acne cosmetics market remains male-focused clinical care, sensitive-skin serums, and professionally endorsed retail lines for medspas and clinics. Compliance demands in the United States and Europe also continue to favor companies that can manage testing, labeling, and claim discipline across markets. That still leaves room for focused specialists, but it preserves a durable advantage for companies that can fund trials, acquisitions, and multi-channel rollouts at the same time. Overall, the anti-acne cosmetics market is becoming harder to win through branding alone, because durable growth increasingly depends on science, tolerability, and disciplined execution across channels.

Anti Acne Cosmetics Industry Leaders

AbbVie Inc.

Galderma Laboratories, L.P.

L’Oréal S.A.

Johnson and Johnson Inc.

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Galderma received US FDA approval for Differin® Epiduo® Acne Gel (adapalene 0.1% + benzoyl peroxide 2.5%) for OTC use in patients aged 12 and older, marking the first Rx-to-OTC transition for this dual-active combination in the United States; retail availability at Walmart, Ulta, Target, and Amazon is set for summer 2026, extending prescription-heritage acne treatment into mainstream consumer channels.

- April 2026: L'Oréal and the Institut Pasteur formalized a landmark scientific research partnership, the first agreement between both institutions, targeting discovery of next-generation active ingredients for advanced skin health, including acne-related conditions, in a collaboration announced during a December 2025 scientific symposium and formalized in April 2026.

- December 2025: L'Oréal Groupe increased its equity stake in Galderma Group AG from 10% to 20%, deepening a strategic scientific alliance that combines L'Oréal's skin biology and diagnostic expertise with Galderma's dermatology portfolio; the transaction closed by Q1 2026 following regulatory approvals.

- August 2025: Revance launched a salicylic acid-based Acne Gel Wash and Daytime Invisible Patches featuring Centella Asiatica and green tea extract for concurrent barrier soothing, expanding PanOxyl's anti-acne portfolio with multi-functional, irritation-minimizing formats.

Global Anti Acne Cosmetics Market Report Scope

The Anti-Acne Cosmetics Market comprises cosmetic and personal care products formulated to help prevent, reduce, or manage acne and acne-prone skin while improving overall skin appearance. These products are intended for daily skincare and cosmetic use and typically contain ingredients that help control excess sebum, unclog pores, exfoliate dead skin cells, soothe inflammation, and minimize the appearance of blemishes and post-acne marks.

The Anti-Acne Cosmetics Market is segmented by product type, active ingredient, end user, gender, and distribution channel. By product type, the market includes cleansers and face washes, creams and lotions, masks, spot treatments, serums, toners, and other product types. Based on active ingredient, the market comprises products formulated with salicylic acid, benzoyl peroxide, retinoids, niacinamide, alpha hydroxy acids (AHAs), tea tree oil, and other active ingredients. By end user, the market is categorized into individual use, dermatology clinics, medspas and aesthetic clinics, and specialty beauty salons. By gender, the market is divided into women, men, and unisex segments. Based on distribution channel, the market includes e-commerce platforms, pharmacies and drugstores, specialty stores, supermarkets and hypermarkets, and dermatology clinics. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

| Cleansers and Face Wash |

| Creams and Lotions |

| Masks |

| Spot Treatments |

| Serums |

| Toners |

| Other Product Types |

| Salicylic Acid |

| Benzoyl Peroxide |

| Retinoids |

| Niacinamide |

| Alpha Hydroxy Acids |

| Tea Tree Oil |

| Other Active Ingredients |

| Individual Use |

| Dermatology Clinics |

| Medspas and Aesthetic Clinics |

| Specialty Beauty Salons |

| Women |

| Men |

| Unisex |

| E-Commerce Platforms |

| Pharmacies and Drugstores |

| Specialty Stores |

| Supermarkets and Hypermarkets |

| Dermatology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Cleansers and Face Wash | |

| Creams and Lotions | ||

| Masks | ||

| Spot Treatments | ||

| Serums | ||

| Toners | ||

| Other Product Types | ||

| By Active Ingredient | Salicylic Acid | |

| Benzoyl Peroxide | ||

| Retinoids | ||

| Niacinamide | ||

| Alpha Hydroxy Acids | ||

| Tea Tree Oil | ||

| Other Active Ingredients | ||

| By End User | Individual Use | |

| Dermatology Clinics | ||

| Medspas and Aesthetic Clinics | ||

| Specialty Beauty Salons | ||

| By Gender | Women | |

| Men | ||

| Unisex | ||

| By Distribution Channel | E-Commerce Platforms | |

| Pharmacies and Drugstores | ||

| Specialty Stores | ||

| Supermarkets and Hypermarkets | ||

| Dermatology Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving anti-acne cosmetics demand through 2031?

Growth is being supported by rising acne burden across both teenagers and adults, stronger demand for clinically validated OTC solutions, and a shift toward gentler multi-function routines. The category is projected to grow from USD 5.52 billion in 2026 to USD 8.28 billion by 2031 at 8.4% CAGR.

Which product type currently leads anti-acne cosmetics sales?

Creams and lotions lead by revenue with 43.13% share in 2025 because leave-on treatment formats fit daily acne care and extend active contact time.

Which ingredient is growing the fastest in anti-acne cosmetics?

Tea tree oil is the fastest-growing active at 10.42% CAGR through 2031, helped by demand for lower-irritation and more natural-feeling treatment options.

Which channel matters most for anti-acne cosmetics brands today?

E-commerce is the largest channel with 33.72% share in 2025 because it offers privacy, comparison, and easy replenishment. Dermatology clinics are growing the fastest at 10.11% CAGR.

Which regions lead and grow fastest in anti-acne cosmetics?

North America leads with 45.63% share in 2025, while Asia-Pacific is the fastest-growing region at 9.46% CAGR through 2031.

How are major companies competing in anti-acne cosmetics?

Leading players are using acquisitions, scientific partnerships, and clinically backed launches. Recent examples include L'Oréal's deeper Galderma relationship, its Institut Pasteur partnership, and Galderma's 2026 OTC approval for Differin Epiduo.

Page last updated on: