Medicated Skincare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.28 Billion |

| Market Size (2031) | USD 41.41 Billion |

| Growth Rate (2026 - 2031) | 10.35% CAGR |

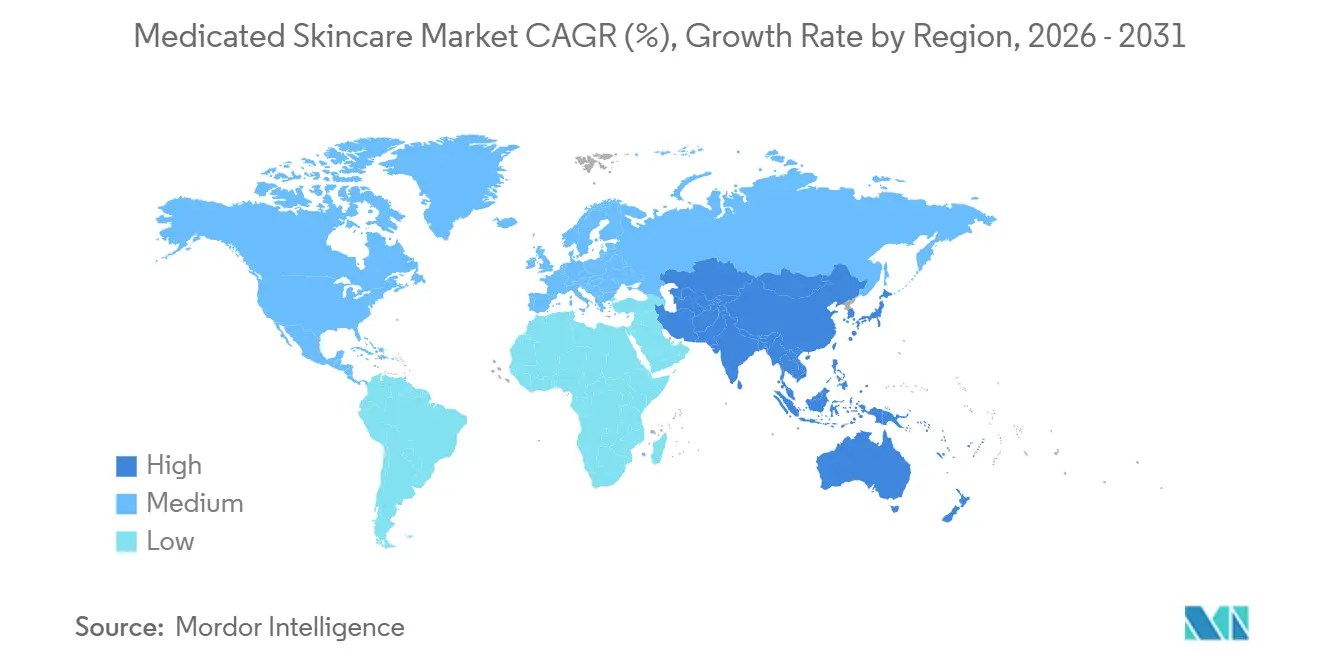

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

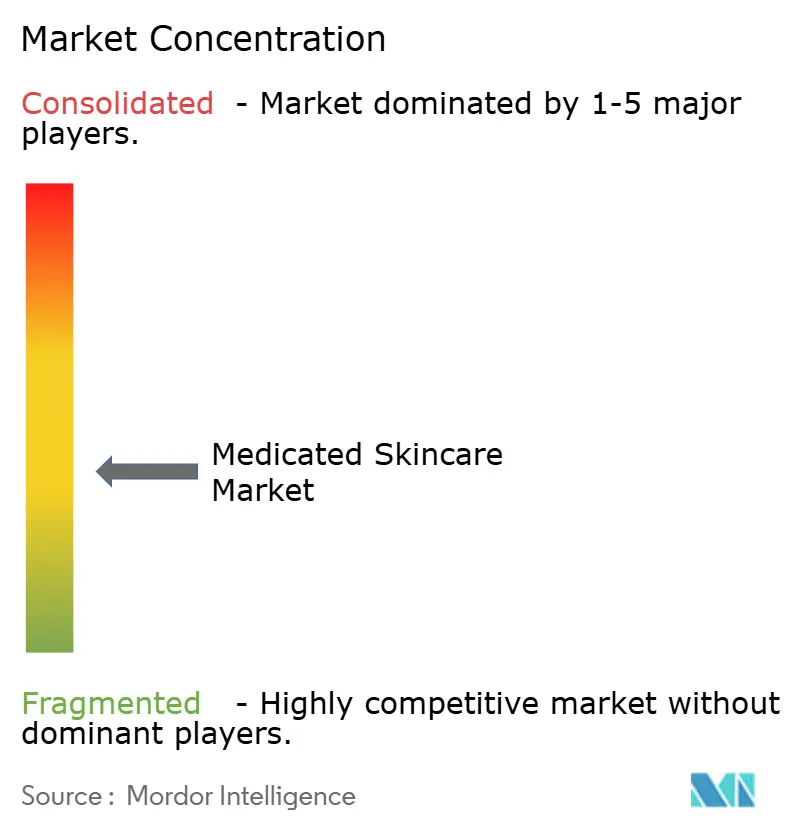

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medicated Skincare Market Analysis by Mordor Intelligence

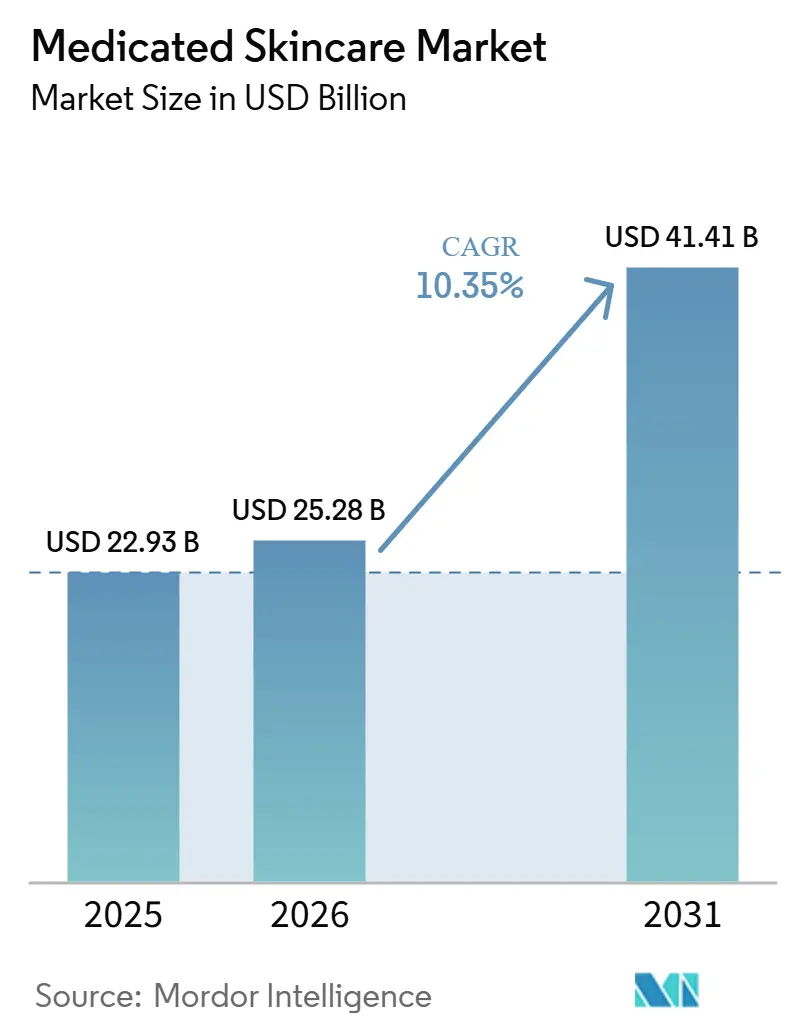

The Medicated Skincare Market size is projected to be USD 22.93 billion in 2025, USD 25.28 billion in 2026, and reach USD 41.41 billion by 2031, growing at a CAGR of 10.35% from 2026 to 2031.

The medicated skincare market is supported by a large treatment base because 84.5 million people in the United States live with a skin condition, which keeps demand tied to ongoing care rather than short seasonal buying cycles. The category is moving further toward therapeutic and evidence-led routines, and that shift gives more weight to medical credibility, ingredient tolerance, and repeat-use performance than to broad cosmetic branding alone. The medicated skincare market is also benefiting from stronger consumer acceptance of dermatologist-backed products, especially in sensitive-skin care where trust influences both trial and long-term retention. Digital retail and teledermatology are making discovery easier, but they are also exposing weak claims faster and raising the commercial cost of standing out with real clinical support. In this setting, brands that build physician relationships, validate formulations, and protect differentiated active platforms are likely to widen their advantage in the medicated skincare market.

Key Report Takeaways

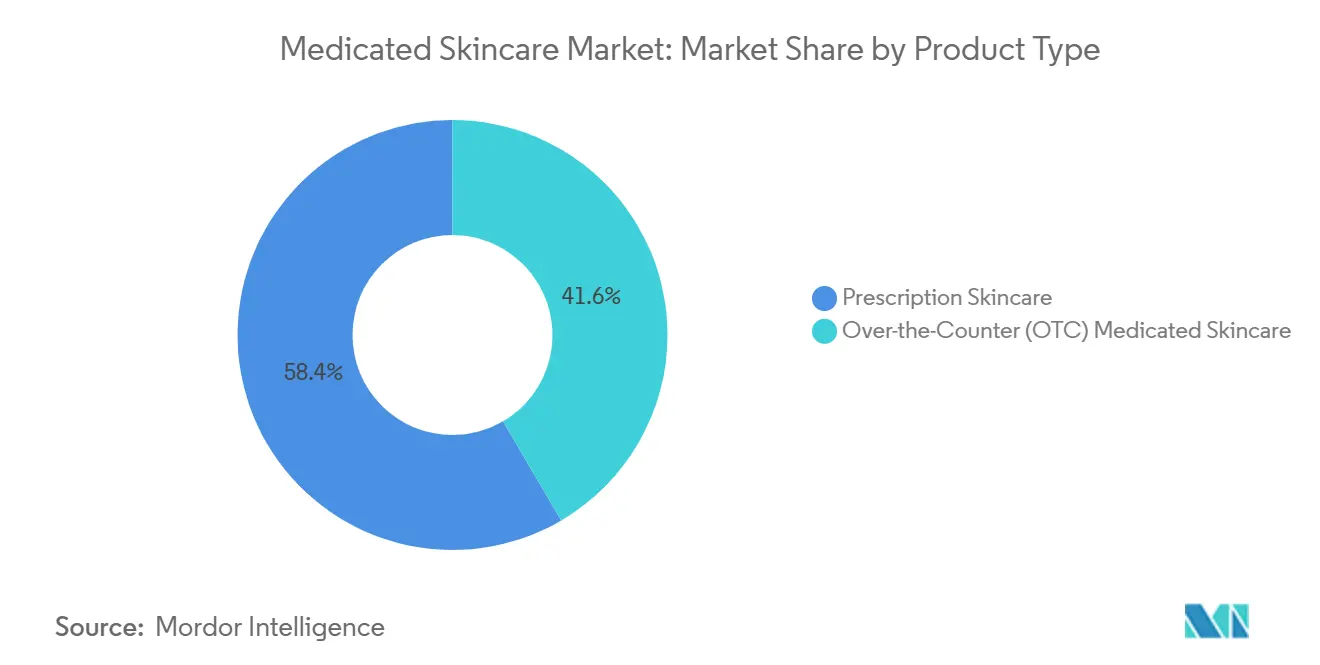

- By product type, prescription skincare held 58.4% of the medicated skincare market share in 2025, while OTC medicated skincare is projected to grow at 12.3% CAGR through 2031.

- By skin condition, acne accounted for 36.2% share of the medicated skincare market size in 2025, while rosacea is forecast to expand at 11.9% CAGR through 2031.

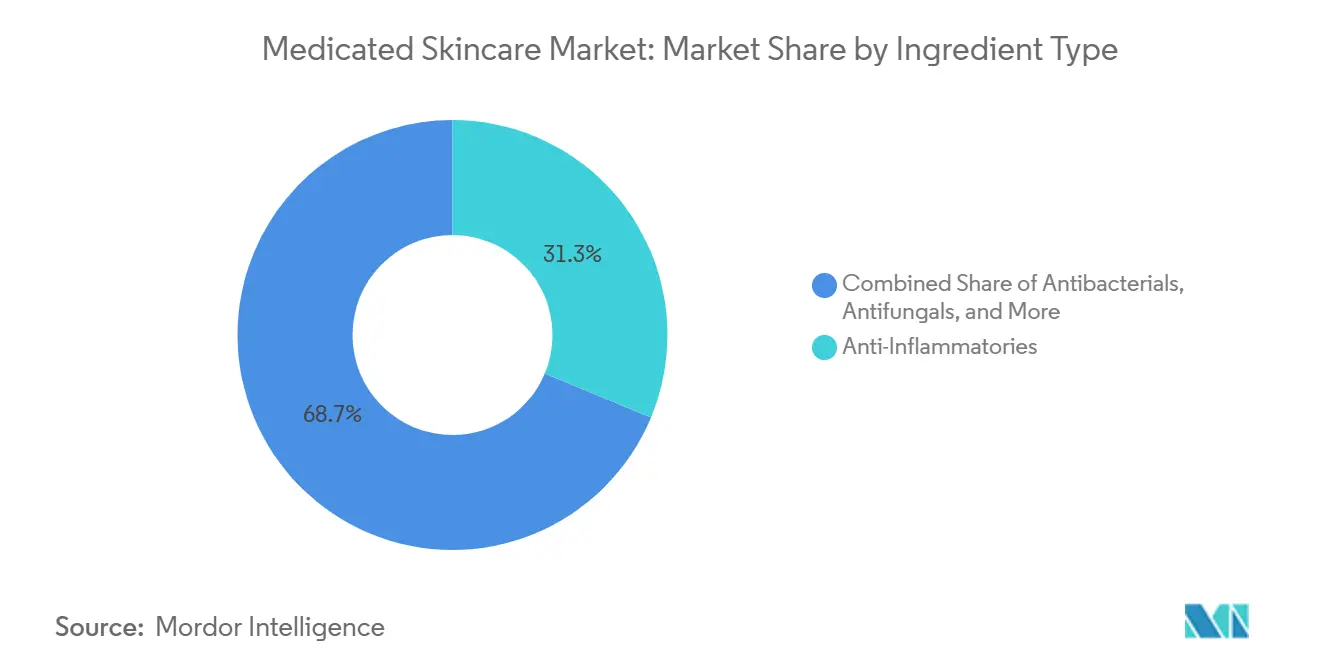

- By ingredient type, anti-inflammatories led with 31.3% revenue share in 2025, while antibacterials are projected to advance at 11.6% CAGR through 2031.

- By application, creams captured 38.4% revenue share in 2025, while gels are expected to grow at 12.2% CAGR through 2031.

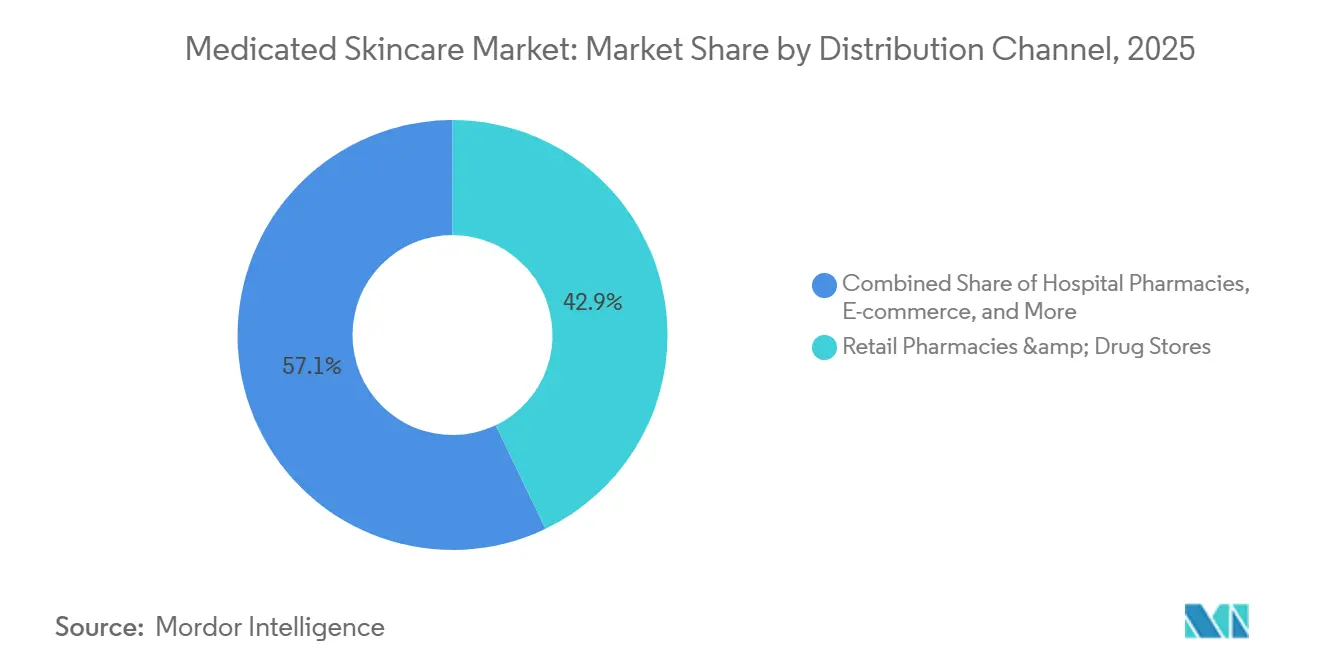

- By distribution channel, retail pharmacies and drug stores held 42.9% revenue share in 2025, while e-commerce is forecast to expand at 12.4% CAGR through 2031.

- By geography, North America held 39.8% of the medicated skincare market share in 2025, while Asia-Pacific is projected to record the highest CAGR at 12.0% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medicated Skincare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preference for Dermatologist-Backed Skincare Routines | +1.2% | Global, with strongest pull in North America and Europe | Medium term (2-4 years) |

| Higher Diagnosis and Self-Identification of Acne, Eczema, and Rosacea | +1.0% | Global, particularly acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Premiumization of Science-Led Dermocosmetics in Mass and Prestige Channels | +1.1% | North America, Europe, and South Korea | Medium term (2-4 years) |

| Faster E-Commerce Conversion for Problem-Solution Skincare | +0.9% | Asia-Pacific core, with spillover to North America and Europe | Short term (≤ 2 years) |

| Expansion of Fragrance-Free, Sensitive-Skin Formulations in Daily Care | +0.8% | Global, with early concentration in Europe and Asia-Pacific | Medium term (2-4 years) |

| Increasing Integration of Teledermatology with Prescription Skincare | +0.7% | North America, Germany, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Preference for Dermatologist-Backed Skincare Routines

Consumer trust in the medicated skincare market now leans more heavily on physician validation than on broad beauty branding. That shift is reinforced by the scale of acne treatment need, because acne affects up to 50 million Americans each year, and adult female acne remains a persistent issue.[1]American Academy of Dermatology, “Skin Conditions by the Numbers,” American Academy of Dermatology, aad.org When product choice is shaped inside clinics and pharmacist conversations, consumers usually become less price sensitive and more loyal to known therapeutic brands. Galderma strengthens this pattern in 2026 with Cetaphil AM/PM Antioxidant Serums, which the company says deliver 2x greater antioxidant efficacy than Vitamin C in laboratory testing and 2x faster overnight skin barrier repair. The medicated skincare market therefore, rewards brands that can turn clinical acceptance into broad retail confidence without weakening the medical basis of their claims.

Higher Diagnosis and Self-Identification of Acne, Eczema, and Rosacea

The medicated skincare market is gaining from a wider pool of consumers who recognize symptoms earlier and start treatment sooner. Eczema affects nearly 1 in 10 Americans across age groups and up to 1 in 5 children under 18, which keeps self-directed search activity high between formal visits. Consumer education around acne, eczema, and rosacea is no longer limited to physician offices because people often reach digital content before they reach a clinic. That shift matters because the first trial now often begins with an accessible product rather than a prescription, especially in mild or newly recognized cases. Brands that explain symptoms clearly and then validate outcomes through medical framing are in a stronger position to capture early loyalty in the medicated skincare market.

Premiumization of Science-Led Dermocosmetics in Mass and Prestige Channels

Premium demand in the medicated skincare market is being shaped less by brand heritage and more by proof around actives, delivery systems, and sensitivity claims. Beiersdorf used this playbook by first introducing EPICELLINE under Eucerin and then extending the same technology into the NIVEA Cellular Epigenetics Rejuvenating Serum across 30 countries in 2025.[2]Beiersdorf AG, “Beiersdorf Brings Epigenetic Innovation to the Mass Market: NIVEA Serum Featuring EPICELLINE®,” Beiersdorf, beiersdorf.com That approach lets a company defend premium authority while also widening access through a larger consumer base. It also raises expectations for competitors because shoppers increasingly read claims around repair, soothing, and sensitivity as technical statements rather than simple marketing language. As a result, the medicated skincare market is giving more value to brands that can move one validated active across price tiers without diluting credibility.

Faster E-Commerce Conversion for Problem-Solution Skincare

Online conversion is becoming more efficient in the medicated skincare market because consumers often search by condition, ingredient, or symptom rather than by brand alone. That search behavior favors products with clear problem-solution positioning and ingredients that are easy to understand at first glance. Digital channels also compress the time between education and purchase, which is especially important for acne, redness, and barrier-repair needs that consumers want to address quickly. The same shift increases competition because private label and lower-priced lookalikes appear beside branded products in the same search journey. Brands that pair transparent claims with recognizable clinical support are more likely to defend pricing as the medicated skincare market moves further online.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Product Credibility Pressure from Weak Clinical Differentiation | -0.8% | Global, with highest intensity in North America and Europe | Medium term (2-4 years) |

| Ingredient Sensitization and Tolerance Risk Across Chronic Use Segments | -0.6% | Global, concentrated in eczema and psoriasis chronic-use cohorts | Long term (≥ 4 years) |

| Regulatory Complexity Around Therapeutic Claims and OTC Positioning | -0.7% | North America and Europe, with secondary exposure in Asia-Pacific | Medium term (2-4 years) |

| Channel Margin Compression from Private Label and Marketplace Price Transparency | -0.5% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Product Credibility Pressure from Weak Clinical Differentiation

The medicated skincare market is under more pressure to prove real differentiation because clinical language is now used across both premium and mass brands. Terms such as dermatologist-tested or clinically proven no longer create enough separation on their own when shoppers can compare many similar claims in minutes. Large players with publication programs, patent-backed actives, and deeper testing budgets can widen this credibility gap faster than smaller rivals. That leaves mid-tier brands in a difficult position because they face price competition below and evidence competition above. In the medicated skincare market, weak proof can now limit conversion just as directly as weak distribution.

Ingredient Sensitization and Tolerance Risk Across Chronic Use Segments

Long-term tolerance remains a practical limit in the medicated skincare market because some consumers cannot stay on the same active regimen indefinitely. This issue is most visible in eczema and psoriasis care, where extended topical use can create irritation, sensitization, or routine fatigue. Once a consumer loses comfort with a product, the cost is not limited to one purchase because the brand can also lose trust across a longer treatment relationship. That makes formulation gentleness, staged use guidance, and patient education central to retention in chronic-use categories. Brands that do not manage tolerance risk carefully may see lower repeat buying than their chronic-care positioning suggests in the medicated skincare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Prescription Channels Underpin Scale as OTC Accelerates

Prescription skincare held 58.4% of the medicated skincare market share in 2025, which shows how much volume still depends on clinician-directed care for moderate and severe conditions. Its scale is supported by referral networks, reimbursement systems, and prescriber habits that keep patients inside more formal treatment pathways for longer periods. That structure gives the segment a durable base, especially in acne, psoriasis, and rosacea, where physician oversight remains important for therapy choice and product rotation. At the same time, the need for a clinical visit slows new-user conversion and makes provider capacity a real growth limit in several countries.

OTC medicated skincare is projected to grow at 12.3% CAGR through 2031, making it the fastest-moving side of this product split. Easier self-selection, better ingredient literacy, and growing comfort with therapeutic daily-care routines are drawing more consumers toward accessible formats that can fit between or outside clinic visits. The strategic balance now favors companies that can operate on both sides, because prescription credibility can strengthen OTC trust. At the same time, the OTC scale can broaden reach and awareness across younger user groups. For single-channel brands, the harder task is to build authority without the physician halo that prescription-originated portfolios bring into the medicated skincare market.

By Skin Condition: Acne Anchors Volume While Rosacea Draws Faster Expansion

Acne accounted for 36.2% share of the medicated skincare market size in 2025, which reflects its unmatched breadth across adolescent and adult users. The condition remains commercially central because at least minor acne affects around 85% of people aged 12 to 24, which keeps product relevance broad even before more severe cases are considered. A 2025 study in Archives of Dermatological Research found acne prescribing moving away from oral antibiotics and more toward antiandrogenic agents and topical combination therapy, which supports further innovation around topical regimens.[3]“Prescribing Patterns for Treatment of Acne Vulgaris: A Retrospective Chart Review at an Urban Public and Private Hospital,” Archives of Dermatological Research, Springer Nature, link.springer.com Eczema and psoriasis add a different kind of value because they depend more on ongoing management and repeat product use than on short treatment bursts.

Rosacea is set to grow at 11.9% CAGR through 2031, the strongest pace among condition groups in the medicated skincare market. A wider diagnosed pool, expanding non-antibiotic treatment pipelines, and more teledermatology access are making the category more visible and more investable for branded players. Hyperpigmentation and other dyspigmentation conditions are also drawing greater attention, especially where consumers want medicated formats that still feel cosmetically refined and easy to layer into daily routines. That widening clinical-to-cosmetic overlap creates opportunity, but it also raises the standard for careful claim language when brands move close to therapeutic positioning.

By Ingredient Type: Anti-Inflammatory Platforms Lead While Antibacterials Gain Pace

Anti-inflammatories held 31.3% of the medicated skincare market in 2025 because they fit across acne, eczema, psoriasis, and rosacea with one broad therapeutic role. Their lead also comes from platform flexibility, since the same inflammation-control logic can support multiple condition stories inside one development base and across several price tiers. Upstream innovation is expanding beyond classic categories, with BASF introducing Ameriflor™ Calm in 2025 as a clinically supported botanical active for redness and transepidermal water loss in sensitive skin. Beiersdorf also showed how novel actives can scale across price tiers when it rolled EPICELLINE® from Eucerin into NIVEA in 2025.

Antibacterials are forecast to expand at 11.6% CAGR through 2031, giving them the fastest outlook within ingredient types. Part of that growth comes from the shift in acne care toward topical combinations and away from heavier reliance on oral antibiotics, which increases room for localized regimens that align with stewardship concerns. As topical delivery improves, these products can address efficacy needs while staying closer to consumer preference for targeted treatment with less systemic burden. Antifungals and other specialist ingredient groups remain smaller, but they keep a steady role in recurrent conditions where targeted treatment matters more than broad appeal.

By Formulation: Creams Hold the Base While Gels Gain Consumer Preference

Creams represented 38.4% of the medicated skincare market in 2025, keeping the leading position across delivery formats. They remain the default choice in many physician-led routines because they support barrier repair, emollient delivery, and patient comfort in dry or inflamed conditions that need regular use. Their position is reinforced by formularies, hospital protocols, and sampling practices that have long favored cream-based treatment, especially in prescription settings. Ointments and lotions continue to serve more specific needs, including heavy occlusion for severe dryness and easier spread over larger body areas.

Gels are expected to grow at 12.2% CAGR through 2031, which makes them the fastest-rising application format in the medicated skincare market. Their appeal is strongest in acne and rosacea, where lighter feel, faster absorption, and minimal residue fit daily routines better and reduce reluctance around frequent use. Galderma's 2026 Cetaphil antioxidant serum system reflects this direction because it combines sensitive-skin positioning with a lighter delivery experience and strong barrier-repair claims. As more actives become stable in lighter systems, gels and serum-like textures are likely to take share from heavier formats over the forecast period.

By Distribution Channel: Pharmacy Strength Persists as Digital Gains Speed

Retail pharmacies and drug stores held 42.9% of the medicated skincare market in 2025, showing that clinical adjacency still matters at the point of purchase. The channel benefits from pharmacist input, trusted store environments, and easy comparison with nearby therapeutic categories that make skin treatment decisions feel more credible. It is especially important for consumers who want reassurance before choosing a product for acne, eczema, redness, or sensitivity, even when the product itself does not require a prescription. Hospital and specialty pharmacy settings remain important for more acute prescription needs, while broader retail formats help lower-acuity OTC products reach scale.

E-commerce is forecast to grow at 12.4% CAGR through 2031, making it the fastest-moving channel in the medicated skincare market. Online shopping changes the journey because content, reviews, and symptom-led search can replace much of the discovery role once held by physical shelves and in-store recommendations. That expands brand reach, especially among younger users, but it also removes some of the advisory support that has helped sustain premium pricing in pharmacy settings. The channel advantage will stay with brands that can make therapeutic claims easy to understand without losing the credibility that the medicated skincare market still expects from evidence-led care.

Geography Analysis

North America held 39.8% of the medicated skincare market share in 2025, making it the largest regional contributor. The region benefits from dense pharmacy access, high dermatologist visit rates, and a consumer base that is already comfortable with therapeutic skincare language and clinically framed product selection. Demand is also supported by the prevalence of common conditions, with acne affecting up to 50 million Americans each year and eczema affecting nearly 1 in 10 people across age groups. The region is therefore well-suited to both prescription-led care and advanced OTC formats that depend on consumer trust rather than impulse buying. In the medicated skincare market, North America continues to set the tone for evidence-backed positioning and sensitive-skin product standards.

Europe remained a major part of the medicated skincare market in 2025, with France and Germany anchoring regional demand. Germany was valued at USD 2.9 billion in 2025, while France continues to benefit from a pharmacy-led dermocosmetics model that gives pharmacist advice a strong role in mild and moderate skin concerns. Across the region, brands with fragrance-minimized and sensitive-skin positioning fit well with stricter product expectations and mature consumer awareness. Perrigo's sale of ACO, Biodermal, Emolium, and Iwostin to Karo Healthcare in 2026 also points to continued portfolio reshaping in European dermocosmetics.[4]Perrigo Company plc, “Perrigo Completes Divestiture of Dermacosmetics Business,” Perrigo Investor Relations, perrigo.com

Asia-Pacific is projected to grow at 12.0% CAGR through 2031, the fastest pace of any regional segment in the medicated skincare market. The region is being lifted by urban skin-stress concerns, stronger digital health infrastructure, and consumer willingness to buy condition-led products online with less dependence on legacy retail discovery. Japan adds regulatory credibility through its quasi-drug structure, and Beiersdorf entered that market with Eucerin in late 2025 using locally tuned product design and ingredient positioning.

Competitive Landscape

The medicated skincare market is moderately concentrated, led by integrated players such as Galderma, L'Oréal, Beiersdorf, AbbVie, and Pierre Fabre. These companies compete across prescription, OTC, pharmacy, and professional channels, which gives them more ways to convert trust into repeat purchasing and more flexibility when one route softens. Their main advantage is not only scale but the ability to connect research, physician education, retailer relationships, and consumer branding in one system. That makes it harder for smaller entrants to defend premium pricing unless they bring a clearly differentiated active, a narrow specialty focus, or unusually strong practitioner support. In the medicated skincare market, clinical credibility now works as the main entry barrier rather than simple shelf presence.

Galderma is strengthening its position in 2026 through the Cetaphil AM/PM Antioxidant Serum launch, using laboratory-backed performance and sensitive-skin messaging to support wider recommendation. L'Oréal is also expanding its reach with a planned majority stake in Innovist in India, which deepens its exposure to fast-growing clinical and functional skincare demand. Perrigo's 2026 dermocosmetics divestiture shows that companies are still pruning portfolios and reallocating capital toward categories where they see stronger strategic fit. Together, these moves show that brand groups are pursuing growth through both innovation platforms and selective portfolio redesign in the medicated skincare market.

The clearest openings remain in rosacea, hyperpigmentation, and digitally enabled treatment ecosystems, where differentiation is less locked than in mature acne segments and where diagnosis-to-purchase pathways are still evolving. Asia-Pacific and Latin America also offer room for challenger brands that can adapt texture, pricing, and communication to local preferences faster than global incumbents with broader portfolio complexity. Teledermatology-linked models could become especially disruptive because they connect diagnosis, product choice, and refill behavior in one flow instead of several separate steps. At the same time, mid-market brands face the greatest pressure because they sit between premium clinical authority and low-price alternatives, a gap that can be difficult to defend over time.

Medicated Skincare Industry Leaders

AbbVie Inc.

Beiersdorf AG

Galderma SA

Johnson and Johnson

L'Oréal S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: FDA Approved AbbVie's SKINVIVE for Neck Line Reduction. Allergan Aesthetics, part of AbbVie, received U.S. FDA approval for SKINVIVE by JUVÉDERM as the first hyaluronic acid injectable approved to reduce neck wrinkles and improve neck skin hydration, extending approved use beyond cheek smoothness and broadening AbbVie's clinical skincare positioning in the medical aesthetics adjacency.

- June 2026: L'Oréal signed an agreement to acquire a majority stake in Innovist, India. L'Oréal signed an agreement to acquire a majority stake in Innovist, a leading Indian personal care house of brands including Bare Anatomy, which marks a strategic expansion into India's fast-growing clinical and functional skincare segment, with the founding team remaining as minority shareholders.

- June 2026: Eucerin launched the Radiant Tone Body Collection in June 2026, extending its clinically proven dark spot and radiance technology, introduced in its facial range in 2025, into body care for the first time and widening its addressable base within hyperpigmentation-focused medicated skincare.

- April 2026: LEO Pharma acquired the Replay Gene Therapy Platform for USD 50 Million. LEO Pharma acquired Replay, a gene therapy company targeting rare genetic skin conditions, including dystrophic epidermolysis bullosa, for USD 50 million upfront plus milestone payments and tiered royalties, adding a high-payload HSV gene delivery vector to its dermatology pipeline.

- April 2026: Perrigo Completed Divestiture of Dermacosmetics Business to Karo Healthcare. Perrigo divested brands including ACO, Biodermal, Emolium, and Iwostin, which generated around EUR 120 million in 2025 net sales, to Karo Healthcare for up to EUR 332.6 million, including EUR 305.6 million upfront, as part of its Three-S Plan to sharpen focus on core consumer health categories.

Global Medicated Skincare Market Report Scope

The Medicated Cosmetics Market comprises cosmetic products formulated with clinically proven active ingredients that provide therapeutic benefits while enhancing skin, hair, or oral health and appearance. These products are designed to help manage mild to moderate conditions such as acne, hyperpigmentation, dandruff, sensitive skin, and dry skin, while complying with cosmetic regulations in their respective markets. The market is driven by increasing consumer preference for science-backed personal care products, growing awareness of preventive skincare, and rising demand for dermatologist-recommended formulations that bridge the gap between conventional cosmetics and pharmaceutical treatments.

The medicated skincare market is segmented by product type, skin condition, ingredient type, formulation, distribution channel, and geography. By product type, it is further divided into prescription skincare and over-the-counter (OTC) medicated skincare. By skin condition, it is segmented into acne, eczema, psoriasis, rosacea, hyperpigmentation, and others. By ingredient type, the market is segmented into anti-inflammatories, antibacterials, antifungals, antioxidants, and others. By formulation, the market is segmented into creams, lotions, ointments, gels, and others. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, E-commerce, and others. The geography segment is further divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecasts in value (USD) for the above segments.

| Prescription Skincare |

| Over-the-Counter (OTC) Medicated Skincare |

| Acne |

| Eczema |

| Psoriasis |

| Rosacea |

| Hyperpigmentation |

| Others (Vitiligo, Melasma, etc.) |

| Anti-Inflammatories |

| Antibacterials |

| Antifungals |

| Antioxidants |

| Others (Retinoids, Corticosteroids, etc.) |

| Creams |

| Lotions |

| Ointments |

| Gels |

| Others (Serums, Foams, etc.) |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| E-commerce |

| Others (Specialty Pharmacies, Supermarkets & Hypermarkets, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Prescription Skincare | |

| Over-the-Counter (OTC) Medicated Skincare | ||

| By Skin Condition | Acne | |

| Eczema | ||

| Psoriasis | ||

| Rosacea | ||

| Hyperpigmentation | ||

| Others (Vitiligo, Melasma, etc.) | ||

| By Ingredient Type | Anti-Inflammatories | |

| Antibacterials | ||

| Antifungals | ||

| Antioxidants | ||

| Others (Retinoids, Corticosteroids, etc.) | ||

| By Formulation | Creams | |

| Lotions | ||

| Ointments | ||

| Gels | ||

| Others (Serums, Foams, etc.) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| E-commerce | ||

| Others (Specialty Pharmacies, Supermarkets & Hypermarkets, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of medicated skincare by 2031?

The medicated skincare market is forecast to reach USD 41.4 billion by 2031, rising from USD 25.3 billion in 2026 at a 7.4% CAGR over 2026 to 2031.

Which product category leads revenue today

Prescription skincare led in 2025 with 58.4% share, supported by clinician-led care, reimbursement structures, and strong retention in moderate and severe conditions.

Which product category is growing the fastest through 2031?

OTC medicated skincare is projected to grow the fastest at 12.3% CAGR, helped by easier self-selection and stronger consumer comfort with therapeutic daily-care routines.

Which skin concern creates the largest revenue base?

Acne remained the largest condition segment in 2025 with 36.2% share, supported by broad prevalence and continued movement toward topical combination therapy.

Which region offers the strongest growth outlook?

Asia-Pacific is expected to post the fastest regional expansion at 12.0% CAGR through 2031, supported by digital health growth, online conversion, and rising condition-led demand.

Why do retail pharmacies still matter if e-commerce is expanding quickly?

Retail pharmacies and drug stores still held 42.9% share in 2025 because pharmacist guidance and a clinically trusted retail setting remain important for therapeutic skincare decisions.

Page last updated on: